pakistan trade and transport facilitation project … project report.pdf · pakistan trade and...

TRANSCRIPT

PAKISTAN TRADE AND TRANSPORT FACILITATION PROJECT

(Trade Transactions Analysis)

PROJECT REPORT DECEMBER 06, 2004

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

2

TABLE OF CONTENTS

ABBREVIATIONS _____________________________________________________04

TASK DESCRIPTION__________________________________________________05

INTRODUCTION _____________________________________________________06

METHODOLGY ______________________________________________________08

EXECUTIVE SUMMARY _______________________________________________09

OVERVIEW OF EXTERNAL TRADE PROCESSES ________________________12

KEY TO READING THE PROCESS CHARTS_____________________________15

INTEGRATED FLOW CHART FOR TEXTILE EXPORTS__________________17

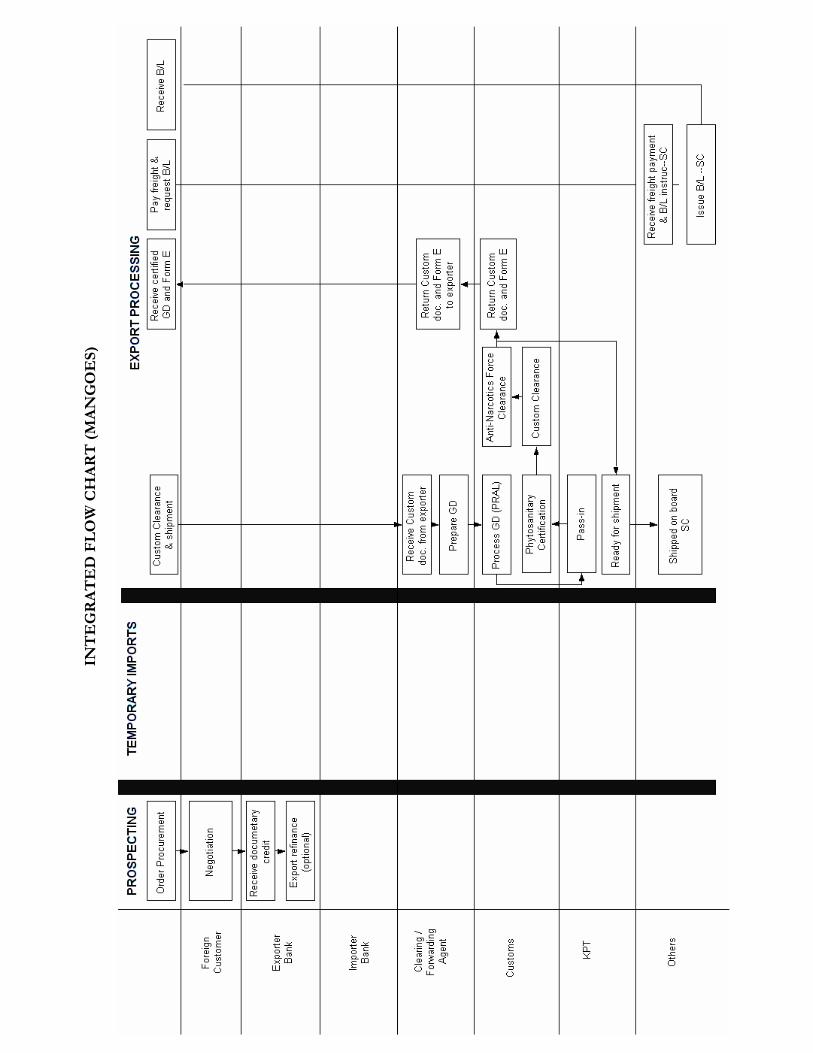

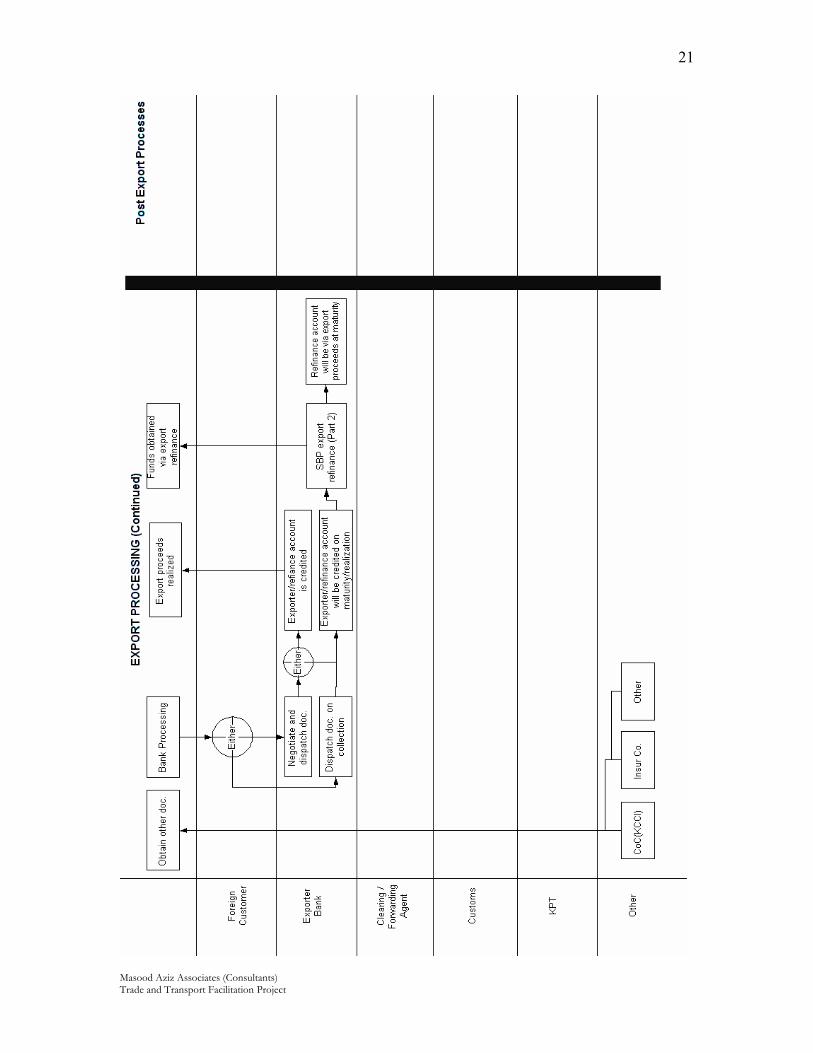

INTEGRATED FLOW CHART FOR MANGO EXPORTS___________________20

COMPARATIVE TRADE TRANSACTION ANALYSIS GRID________________22

AVERAGE TIME RANGES FOR SUB-PROCESSES ________________________23

INTRODUCTION TO BUSINESS PROCESSES ___________________________25

Exporters Bank 25 Clearing Agent 31 Export Facilitation Center 34 Karachi Port Trust 37 Pakistan Customs 39 Shipping Company 46 Export Promotion Bureau 49 Karachi Chamber of Commerce & Industry 51

BUSINESS PROCESSES DESCRIPTIONS AND FLOW CHARTS ____________52

Customer Interface 53 Importers' Bank 56 Exporters' Bank 62 All Pakistan Textile Manufacturers Association 65 Export Promotion Bureau 67 Clearing Agent (Temporary Imports) 71 Clearing Agent (Exports) 73 Insurance Company 77 Karachi Chamber of Commerce & Industry 80 Karachi Port Trust - Delivery 83 Karachi Port Trust - Pass-in 86 Shipping Company 88

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

3

Pakistan Customs - Customer Service Center 91 Pakistan Customs - Temporary Imports 96 Pakistan Customs - Manufacturing Bond (Bonded Warehouse) 100 Pakistan Customs - Manufacturing Bond (Custom House) 104 Pakistan Customs - Bank Guarantee (Deposit) 108 Export Facilitation Center - M. I. Yard 111 Export Facilitation Center - Air Freight Unit 115 Pakistan Customs - Goods Pass-in 117 Pakistan Customs - Examination 120 Pakistan Customs - Bank Guarantee Release 124 Pakistan Customs - Duty Drawback 128

ILLUSTRATED ANALYSIS - TOOLKIT _________________________________132

Process Re-engineering Framework 132 Problem Diagnosis (with reference to export of mangoes) 134 Proposed Trade Portal for exchange of e-documents and information 140

PROPOSALS / RECOMMENDATIONS _________________________________145

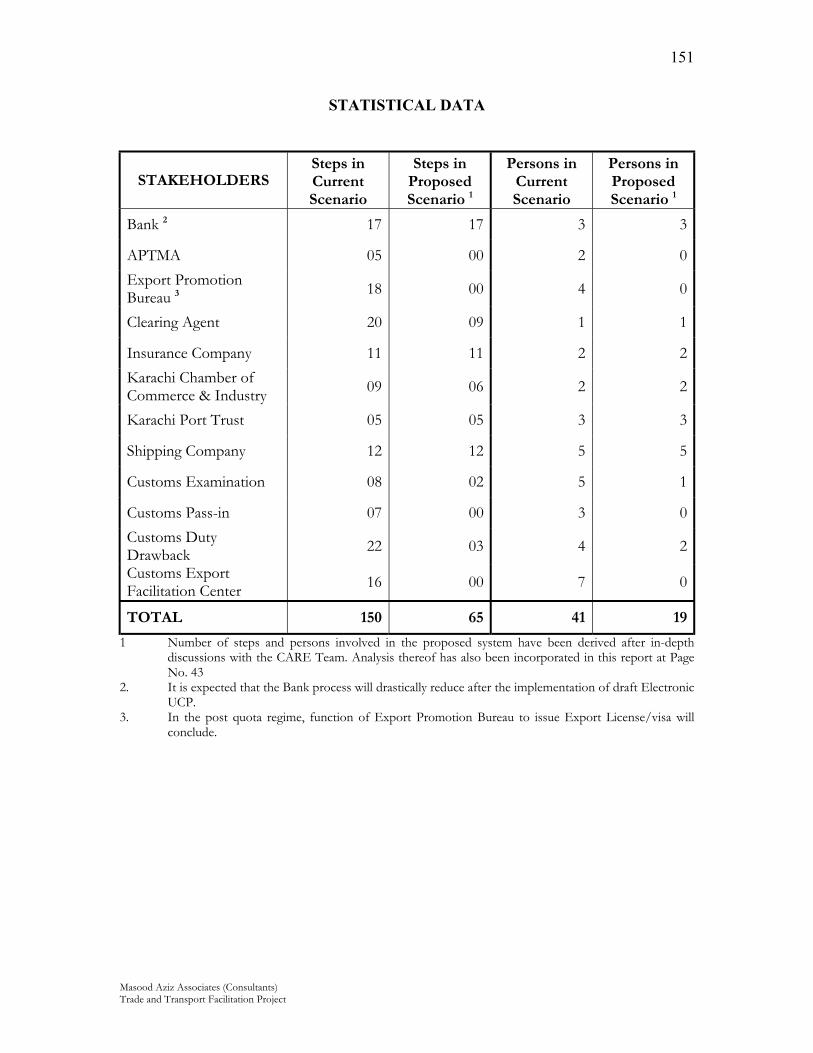

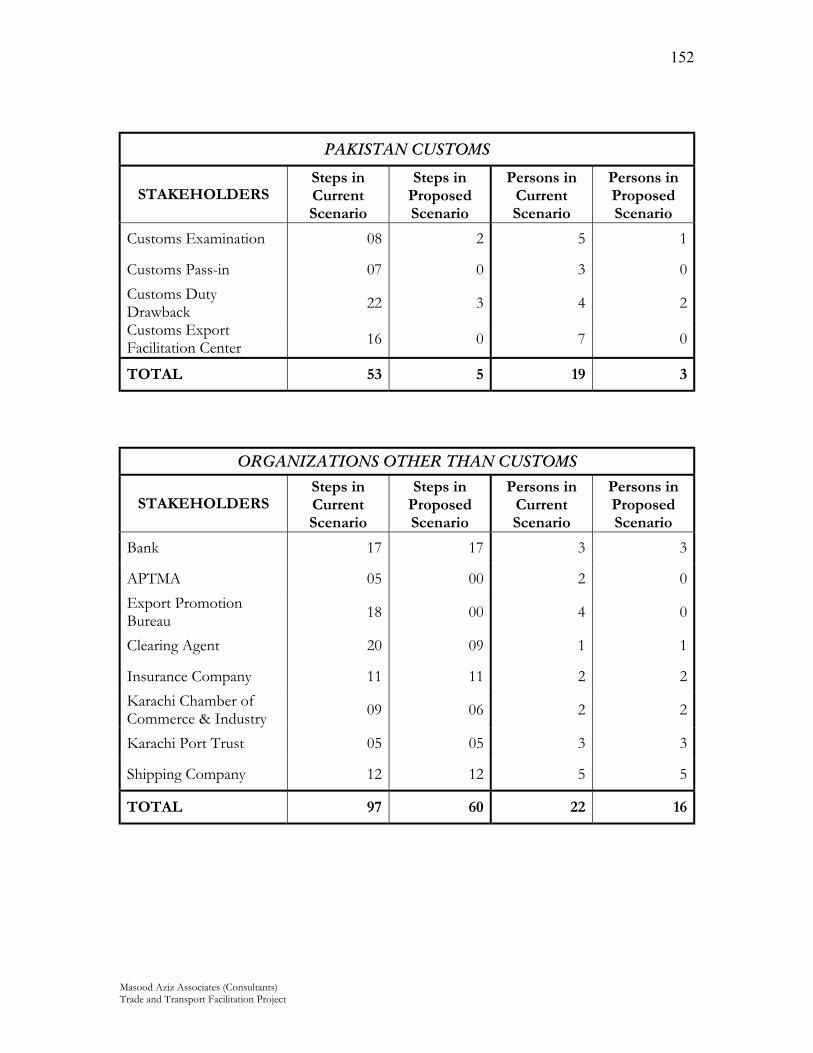

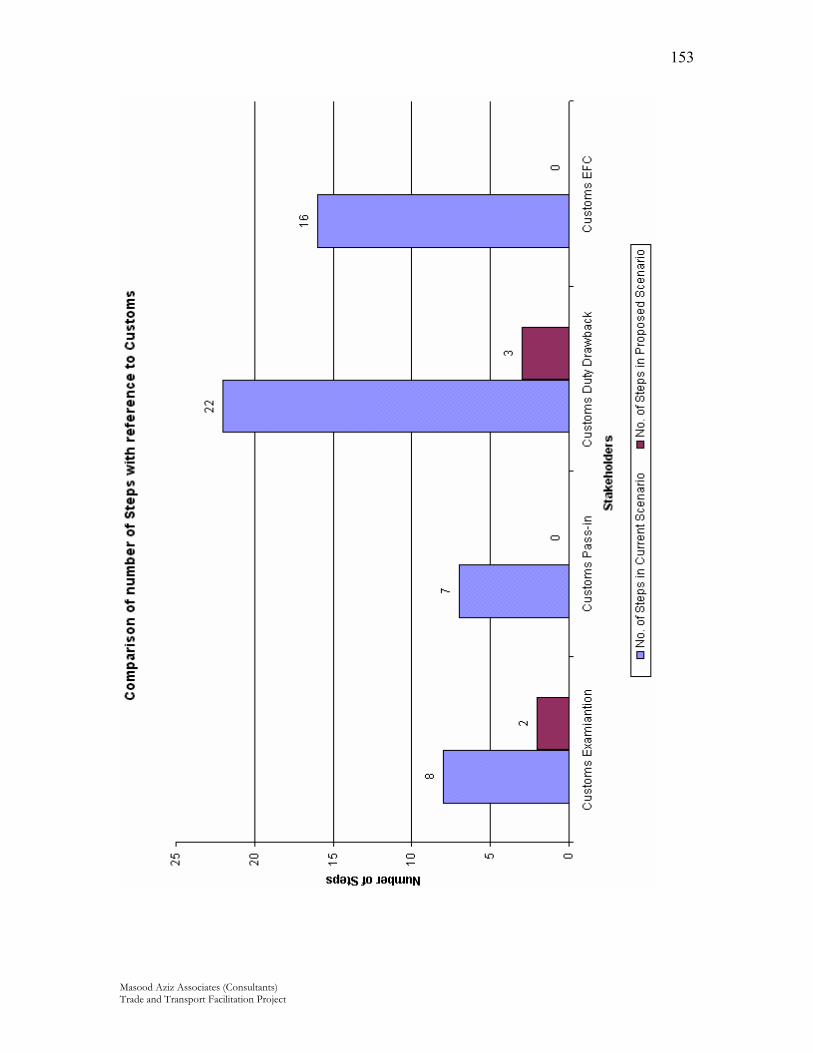

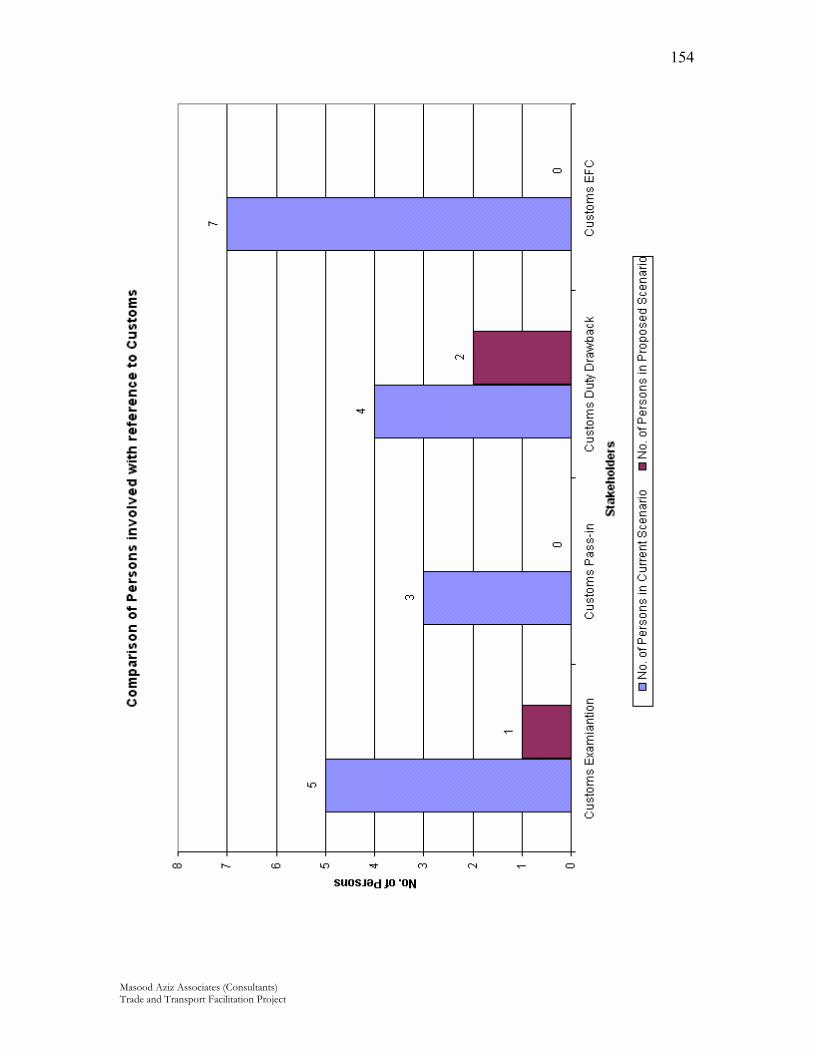

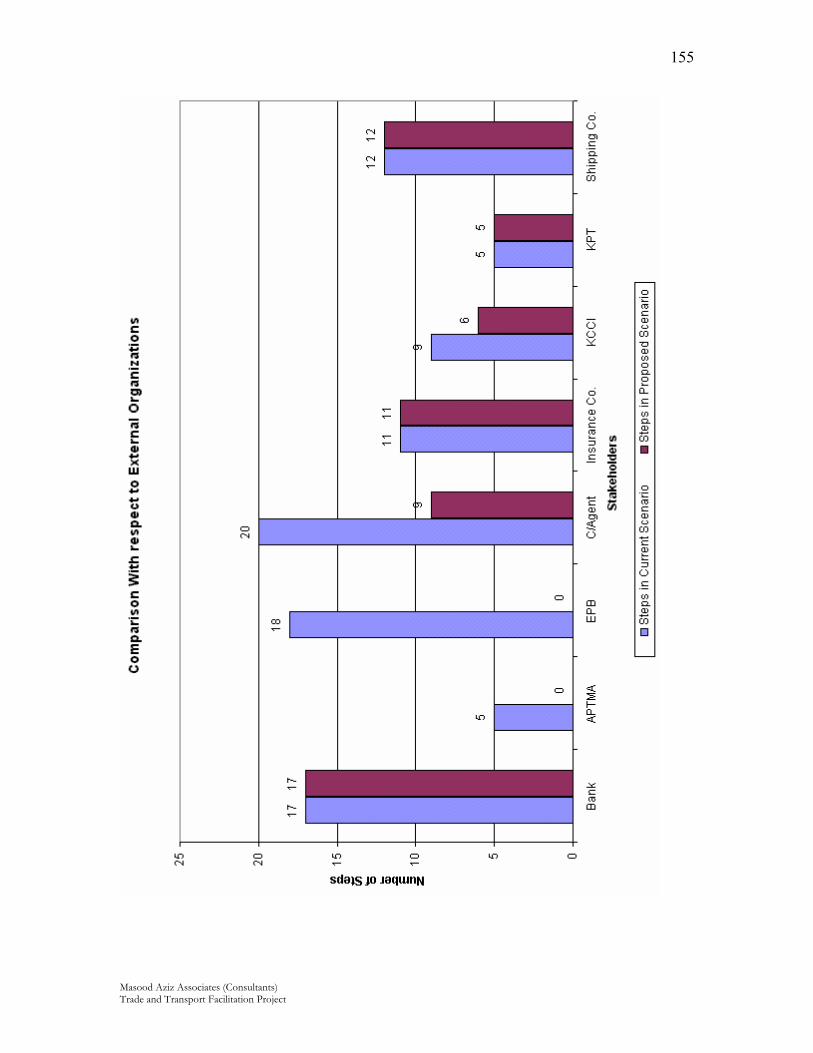

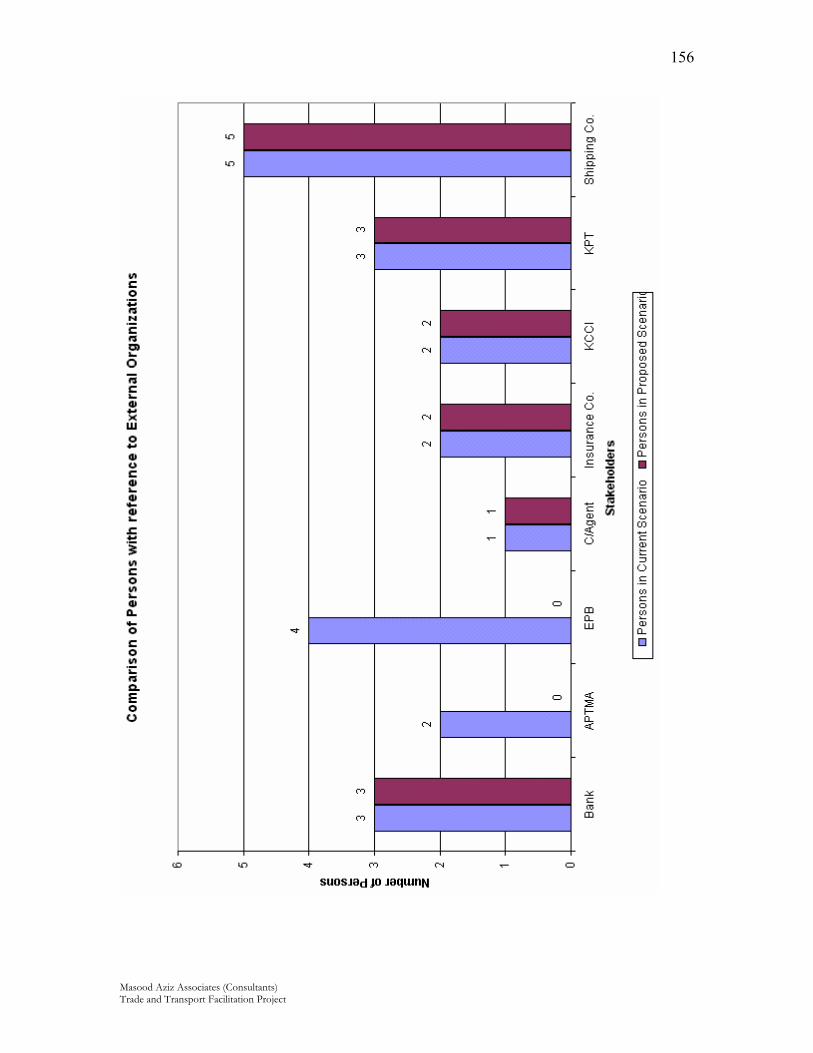

STATISTICS _________________________________________________________ 151

Statistical Data of overall Export Supply Chain 151 Statistical Data - Customs segregated from external organizations 152 Graphical Representations 153

ANNEXURE_________________________________________________________158 Electronic UCP 158 Good practice in trade facilitation: Lessons from Tunisia 163

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

4

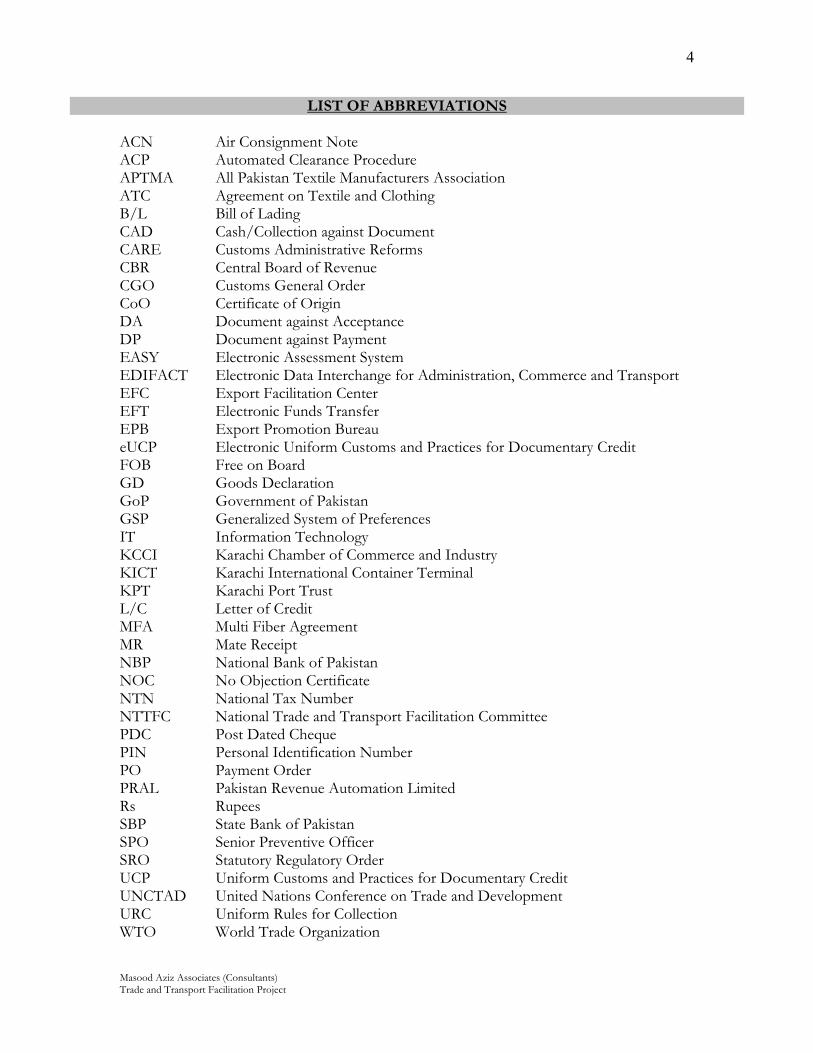

LIST OF ABBREVIATIONS ACN Air Consignment Note ACP Automated Clearance Procedure APTMA All Pakistan Textile Manufacturers Association ATC Agreement on Textile and Clothing B/L Bill of Lading CAD Cash/Collection against Document CARE Customs Administrative Reforms CBR Central Board of Revenue CGO Customs General Order CoO Certificate of Origin DA Document against Acceptance DP Document against Payment EASY Electronic Assessment System EDIFACT Electronic Data Interchange for Administration, Commerce and Transport EFC Export Facilitation Center EFT Electronic Funds Transfer EPB Export Promotion Bureau eUCP Electronic Uniform Customs and Practices for Documentary Credit FOB Free on Board GD Goods Declaration GoP Government of Pakistan GSP Generalized System of Preferences IT Information Technology KCCI Karachi Chamber of Commerce and Industry KICT Karachi International Container Terminal KPT Karachi Port Trust L/C Letter of Credit MFA Multi Fiber Agreement MR Mate Receipt NBP National Bank of Pakistan NOC No Objection Certificate NTN National Tax Number NTTFC National Trade and Transport Facilitation Committee PDC Post Dated Cheque PIN Personal Identification Number PO Payment Order PRAL Pakistan Revenue Automation Limited Rs Rupees SBP State Bank of Pakistan SPO Senior Preventive Officer SRO Statutory Regulatory Order UCP Uniform Customs and Practices for Documentary Credit UNCTAD United Nations Conference on Trade and Development URC Uniform Rules for Collection WTO World Trade Organization

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

5

TASK DESCRIPTION (TERMS OF REFERENCE) Masood Aziz Associates were assigned the task of mapping external business processes

relating to export transactions by UNCTAD. The project was to be undertaken in liaison

with NTTFC. For this purpose textile sector was selected for carrying out detailed analysis.

The scope of the project was defined as follows:

• To map the processes on ‘as is’ basis

• Analyze and breakdown the processes into singular activities and tasks;

• Plot each activity (sub-process) in the form of a process (flow) chart;

• Prepare an integrated flow chart providing linkages and interdependencies of each sub process;

• Conduct an analysis of the processes and make indicative recommendations for simplification and standardization;

• Prepare indicative criteria for articulating modifications in the ‘as is’ scenario involving IT/E-commerce intervention

• To translate the outcome of the assignment into generic approach.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

6

INTRODUCTION Trade facilitation in the context of international trade refers to all components of trade

transactions namely physical, procedural and administrative. Singapore Declaration and

Doha Development Round of WTO Ministerial conferences have identified trade facilitation

as an essential component for the economic growth of member countries. Effective trade

facilitation should lead to an increase in competitiveness and in turn raise the quantum of

business activity. Any effort to address constraining factors in the context of trade

facilitation would require revisiting the entire spectrum of trade environment of a country

with a view to making its trade industry competitive in the global market. Important aspects

of international trade environment include: trade policy, trade logistics, documents and

business processes. The Government of Pakistan recognized the importance of this issue

and took a major initiative by setting up a Task Force in the year 2000 to analyze the entire

gamut of Customs business processes. Based on the recommendations of the Task Force a

comprehensive strategy was developed for initiating Customs reforms programme to

facilitate international trade. The Central Board Revenue set up an organization namely, the

Customs Administrative Reforms Cell (CARE) for implementing the reforms programme

approved by the Government.

Simultaneously, the National Trade and Transport Facilitation Committee (NTFFC), which

operates under the aegis of the Ministry of Commerce, has been engaged in analyzing trade

documents, processes, laws and institutional setup to address the various constraints that

affect Pakistan’s international trade.

This project is an extension of the initiative of the NTFFC with reference to simplification

of documents and procedures related to international trade transactions. NTFFC has already

successfully implemented the Goods Declaration and Ship Clearance forms besides

developing an inventory of trade documents. This project essentially focuses on analyzing

the series of steps involved in the external trade transactions, with a special focus on export

trade. For this purpose, the textile sector was identified as a prototype for analyzing

international trade transactions in a manner that could be adopted for different

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

7

industries/sectors. The analysis encompasses all steps involved from the point of production

of goods until the receipt of payment (export proceeds). This study identifies agents, number

of steps and average time consumed in the completion of various processes pertaining to the

export trade transactions. This will provide the various stakeholders with an opportunity to

rationalize the processes to enhance the competitiveness of Pakistan’s exports. Besides,

export trade transaction in respect of mangoes was also studied to draw comparison between

the two. This report includes a brief analysis to highlight the points of convergence and

variation with reference to processes impacting export of the two export products.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

8

METHODOLOGY

The project followed a preconceived path. We began with developing a conceptual model on

trade facilitation from the perspective of external trade processes. This was followed by

physical observation of the processes in action. Simultaneously, the various functionaries in

each process were identified and interviewed for clarity and conceptual understanding of

various activities in a particular process. On the basis of our physical observations and

discussions, process description and charts were developed. Subsequently, the process

descriptions and flow charts were taken to a senior person in each department (process) for

his review and validation. The processes are analyzed from various dimensions, such as

number of steps involved, number of persons involved, type and nature of tasks / activities

involved, and average time taken to complete each process. The processes were further

analyzed to understand the value-significance of each process on the export supply chain

with a view to identifying factors, which tend to slow down the processes.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

9

EXECUTIVE SUMMARY For carrying out this study, the following processes were identified for mapping the steps

involved in the export supply chain of textile goods:

• Opening of L/c

• Processing of Goods Declaration

• Pass-in of Export Consignments

• Examination of Goods

• Issuance of Export Visa by EPB for quota items

• Insurance of Goods

• Issuance of Certificate of Origin

• Issuance of Bill of Lading

• Sanctioning of Duty Drawback

• Temporary Importation

• Manufacturing Bond

Result of the study depicted in the flow charts revealed that the processes are predominantly

manual, involve excessive/frequent interface of functionaries and clients and that there is a

lack of facilitative/enabling environment for efficient performance of individual tasks. For

instance, the process of temporary imports is completed in eighteen steps under ideal

conditions. The documents move back and forth fifteen times and require signatures of

concerned authorities at seven different occasions.

Of all the business reports mapped, Customs clearance of goods is perhaps the most critical

/ important in the export supply chain considering the regulations/procedures that need to

be followed to dispatch the export consignment to the buyers abroad.

Fortunately, considerable effort has already gone into revamping the Customs Business

Processes. Customs Administrative Reforms (CARE) organization is in an advanced stage of

implementation of automated solutions to the existing manual-cum-computerized system at

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

10

Customs, which involves a fairly large number of steps. For example the GD at Export

Facilitation Center is processed in sixteen steps and include intervention of seven persons.

A pilot project covering all imports and exports through KICT is likely to be operative by

March 2005. The hallmark of the proposed prototype project would be:

• Customs would function in a paperless environment;

• Goods Declaration would be lodged and processed electronically;

• System would work based on a comprehensive Risk Management criteria;

• There will be virtually no physical interfacing with the Customs clients; and

• Data would be interchanged with the major stakeholders through (EDIFACT)

Subsequent to shipment of goods comes the point of negotiating documents with the bank.

This process is equally critical, for a successful and timely negotiation would enable the

exporter to realize his proceeds at an appropriate point in time. The usual reason for delay is

incomplete and/or incorrect document submission by the exporter. It is imperative to

mention that quite a few documents need to be issued by an external organization, such

Certificate of Origin, Visa, GSP etc. It is ironical to point out that in theory little time is

required for the issuance of these documents. However, in practice it is observed that the

delay in issuance of these documents sometimes exceeds a week.

Upon successful shipment of goods and negotiation of documents at the bank counter, the

exporter initiates his claim for the payment of duty draw back and sales tax return on the

exported goods. The claims are critical for the exporter in the context of maintaining

competitiveness and capping his cost of funds. Duty draw back and sales tax return are also

usually taken away from the export prices to make the products even more competitive.

However, if these claims are not settled in timely manner it results in loss to the exporter.

For instance, the standard settlement time for duty draw back is from 24 hours to one

month for Gold, Silver and Others categories, respectively. Stakeholders, however, inform

that sometimes it takes much longer.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

11

An analysis of other processes viz. opening of L/c, issuance of Bill of Lading, Form E, and

Certificate of Origin, etc. indicates that IT based solutions could be dovetailed with the

CARE project both as a short and medium term solutions. Simultaneously, stakeholders may

work out simplified/reengineered processes by deleting unnecessary steps and rationalizing

the existing procedures.

The recommendations incorporated in the report essentially aim at finding IT based

solutions viz. electronic customs declaration/ processing as envisaged in CARE project,

development of a portal system for data interchange between various stakeholders and

modernization of relevant banking procedures in terms of ICC’s proposed electronic

document submission.

This will, however, require a holistic and coordinated effort in consultation with all the

stakeholders

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

12

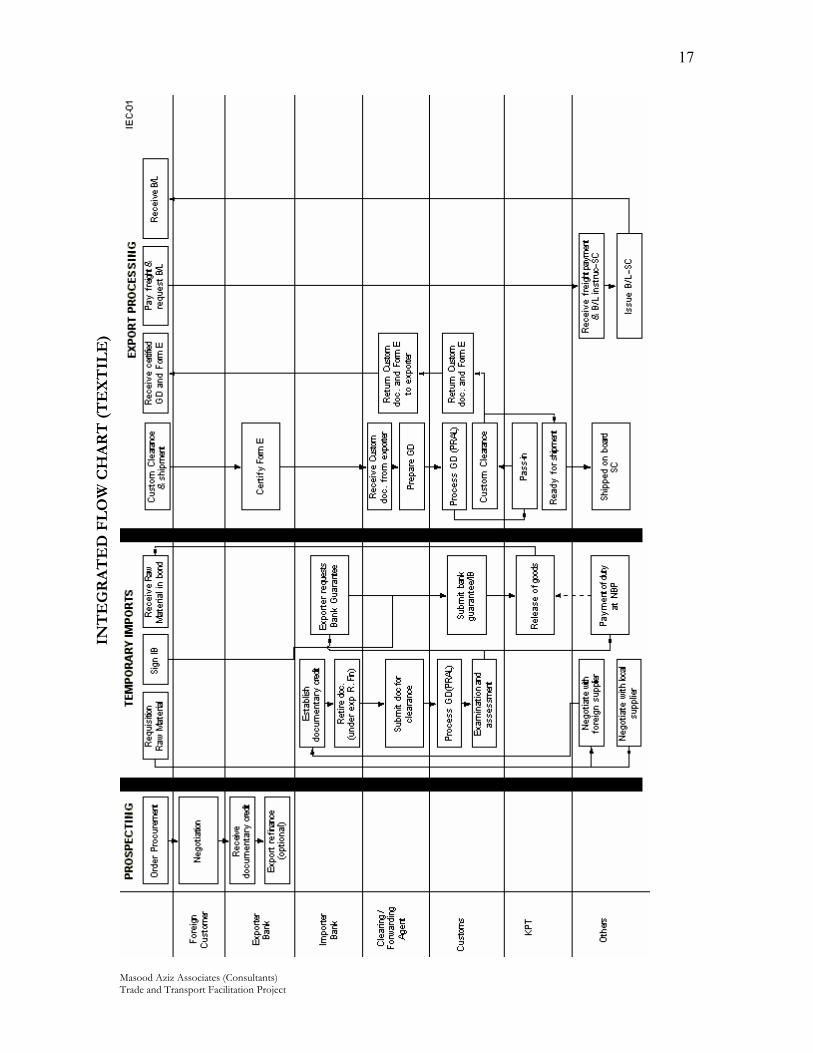

OVERVIEW OF EXTERNAL EXPORT PROCESSES (AS IS BASIS)

Export supply chain of a typical textile fabric export is analyzed with a view to presenting a

comprehensive perspective on various intervening processes involved. A dual level analysis

has been done in this regard. The primary level analysis focused on capturing the tasks and

activities that make up each process on ‘as-is basis’. Secondary level analysis is done from the

holistic orientation, wherein each primary level process is integrated with the other to

highlight the inter-dependencies of primary level processes and to portray the resulting

complexity of the export supply chain. A diagrammatic illustration of the above is portrayed

in the following Integrated Process Chart.

The primary level processes are split into four clusters, namely;

• Order prospecting,

• Temporary Imports,

• Documentation and goods dispatch, and

• Post dispatch processes.

1. Order prospecting process captures tasks involved in selling to a foreign buyer. This

includes sampling, negotiation, and contracting. This process is relatively simple and

flexible, for the seller and buyer mostly control the activities according to their

convenience.

2. Temporary Imports refer to acquisition (import) of requisite raw materials, including tags

and labels from the buyers. This process is rather cumbersome, for most of the tasks in

this process are controlled by a third party other than buyer or seller. For instance, bank

procedures are controlled by the exchange control regulations in force, custom processes

are regulated by the Trade Policy, Customs Act and other regulatory procedures notified

by the CBR. These activities are complex and cut across multiple external organizations.

Moreover, the tasks here are also linked with the processes at post-exportation stage,

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

13

such as claiming of duty draw back etc. Due to the inherent complexity and external

interdependencies the processes here are prone to dysfunctional influences leading to

unwarranted delays.

3. Documentation and dispatch of goods represents the third cluster of activities, which

begin with dispatch of goods from factory for shipment. The goods go through a host of

intermediaries before these are shipped on board, such as Forwarding Agents, Customs,

Terminal Operators, Port Authorities, etc. The most critical interaction occurs with

Customs authorities, who by virtue of their statutory role and responsibility are supposed

to clear the goods for shipment. The underlying rationales of Customs control are: to

ensure if the physical goods conform to the declared description, especially on Customs

documents. Secondly, the customs also ensures if no contra band as per trade policy and

other regulations or hazardous or destructive goods are exported from the country.

The procedures in vogues at Customs were put in place many years ago when neither the

trade traffic was so voluminous nor time efficiency standards were so high. However, as

of today the scenario has changed paradigmatically. International trade has increased

manifolds both in terms of volume and value. Similarly, time has become extremely

critical in view of competition in the international markets. The procedures in vogue

become a bottle-neck in the supply chain unless extensive use of Information

Technology (IT) is done at all levels by all stakeholders tinkering with the manual

procedures would at best result only in marginal improvement. Further, there is a need

for a shift from the strictly “Control Orientation” to “Facilitative Orientation” whereby

legitimate traders are given due recognition and their goods are cleared through simpler

processes in lesser time.

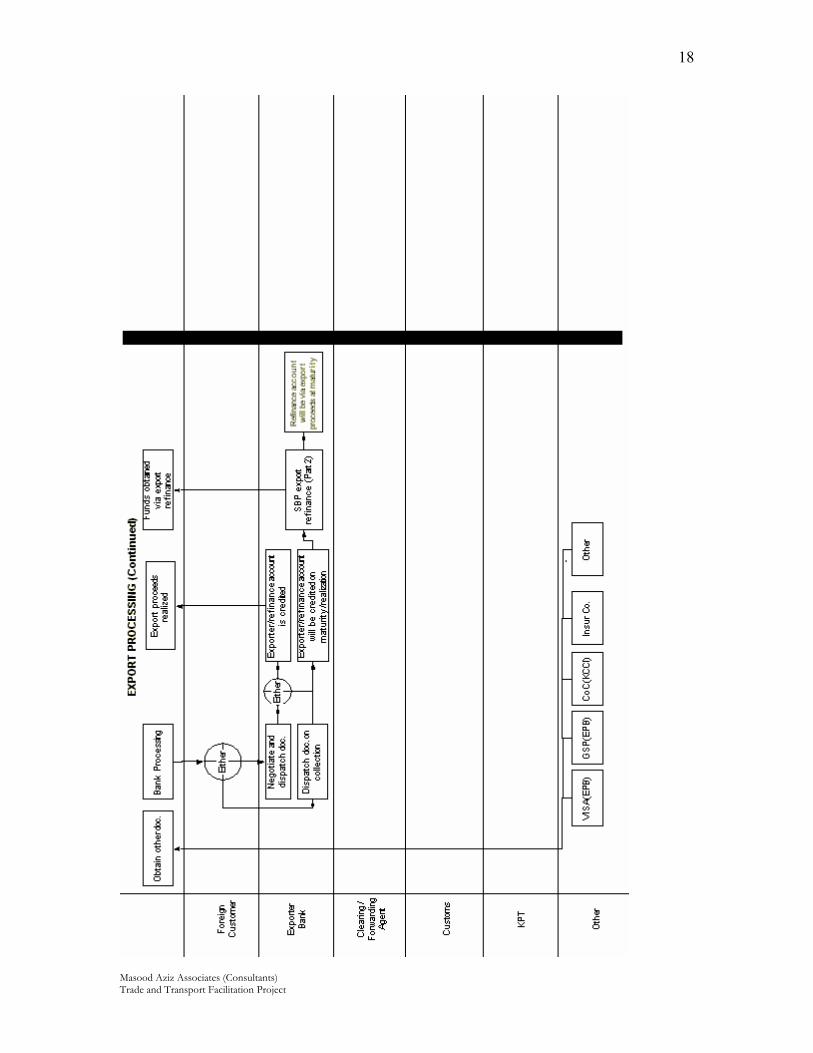

Subsequent to the shipment of goods comes the point of negotiating documents with

the bank. This process is equally critical, for a successful and timely negotiation would

enable the exporter to realize his proceeds at an appropriate point in time. Conversely,

any delay here could stretch the time horizon for realizing the proceeds and hence export

asset conversion cycle. As cited in the following report, the usual reason for delay is

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

14

incomplete and/or incorrect document submission by the exporter. It is imperative to

mention that quite a few documents need to be issued by an external organization, such

as Certificate of Origin, Visa, GSP etc. It is ironical to point out that in theory little time

is required for the issuance of these documents. However, in practice it is observed that

the delay in issuance of these documents sometimes exceeds a week.

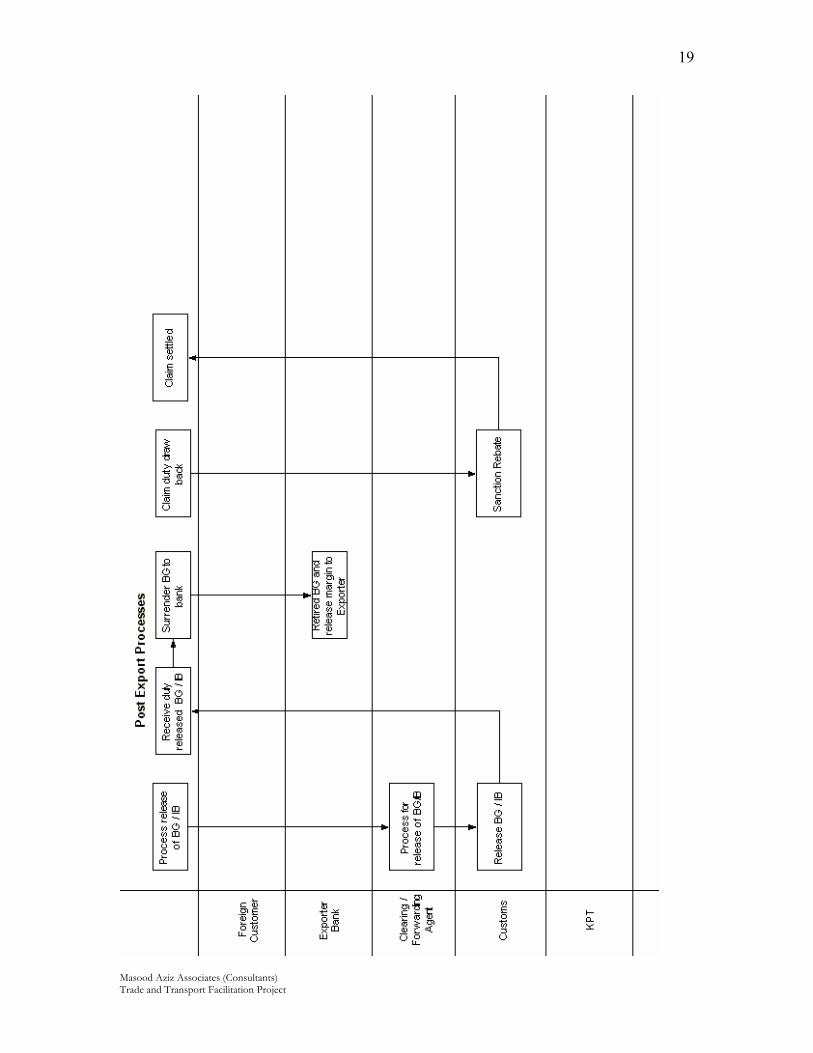

4. Upon successful shipment of goods and negotiation of documents at the bank counter,

the exporter initiates his claim for the payment of duty draw back and sales tax return on

the exported goods. The claims are critical for the exporter in the context of maintaining

competitiveness and capping his cost of funds. The exporter competes in the

international markets by quoting as low price as he could manage. Duty draw back and

sales tax return are also usually taken away from the export prices to make the products

even more competitive. However, if these claims are not settled in timely manner, it

results in loss to the exporter. For instance, the standard settlement time for duty draw

back varies from 24 hours to one month for Gold, Silver and Others categories,

respectively. However, the payments sometimes are not released for much longer period

of time.

In nutshell the external processes along the export supply chain need immediate

rationalization to redress the issues of process inefficiencies, redundancies, susceptibility to

corruption, and high cost of execution. To achieve this, it is imperative that a cooperative

partnership of Government and Industry is forged based on mutual trust and to create an

enabling environment characterized by transparency, information sharing and speed.

The respective processes appear in the following pages, for a detailed review in the format of

flow charts.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

15

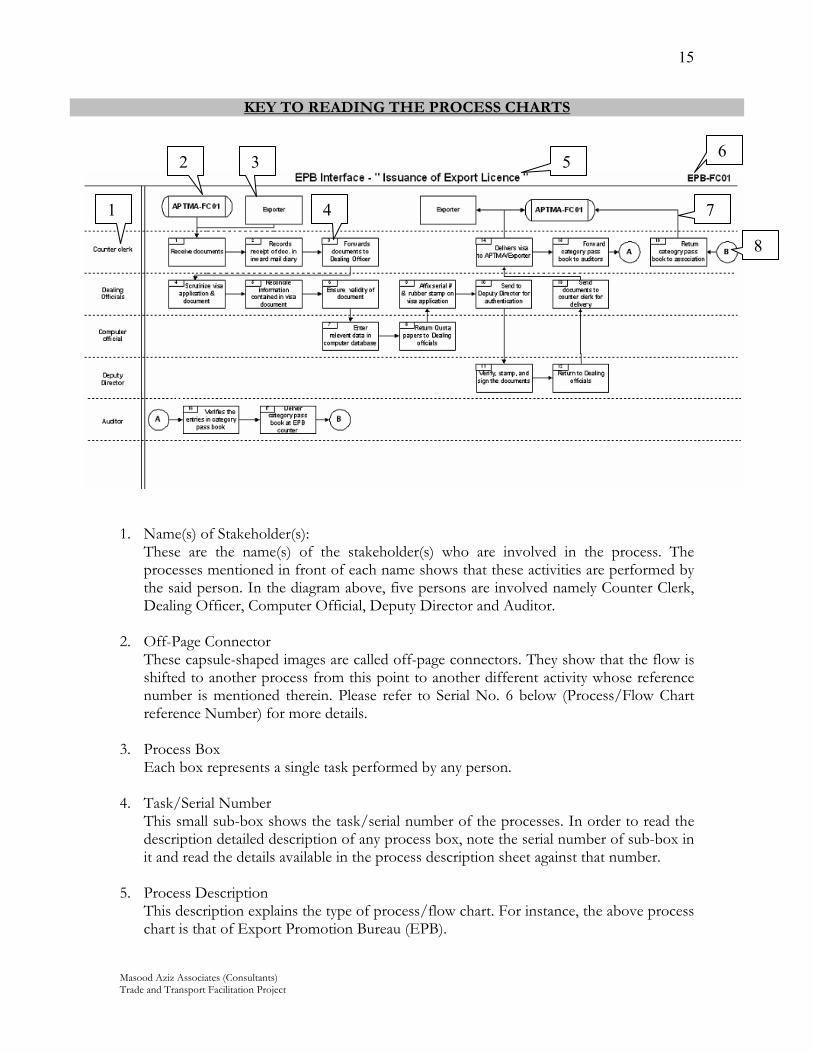

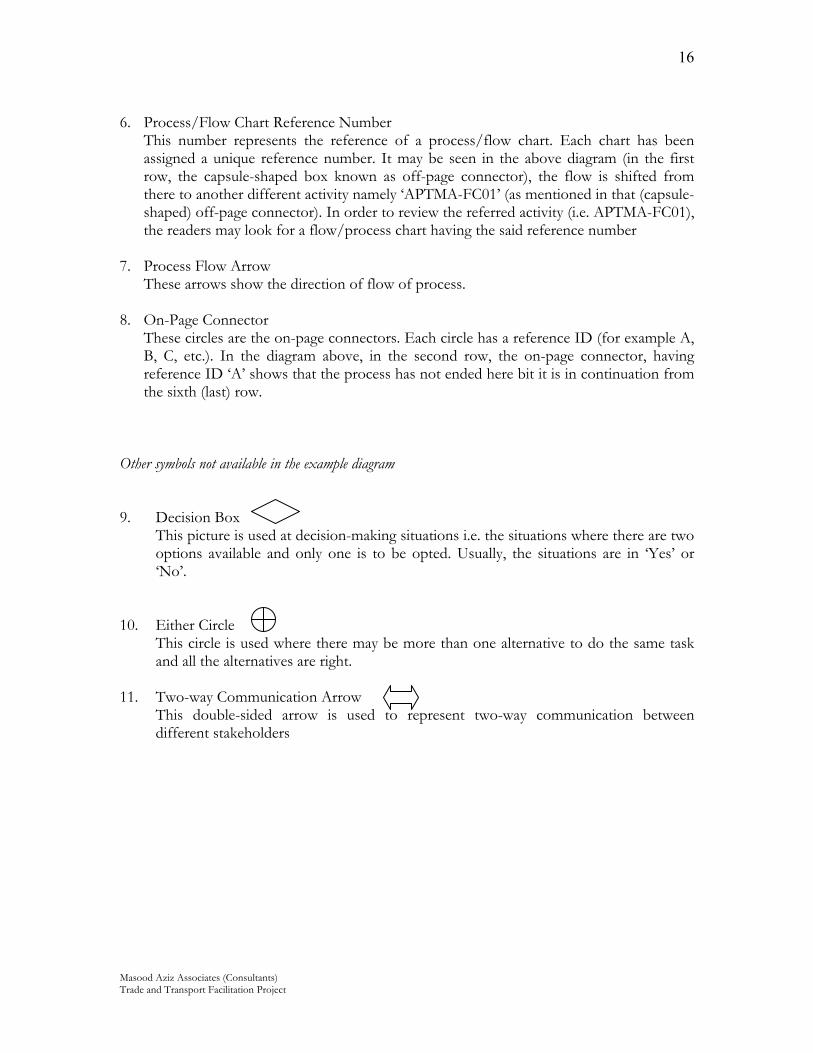

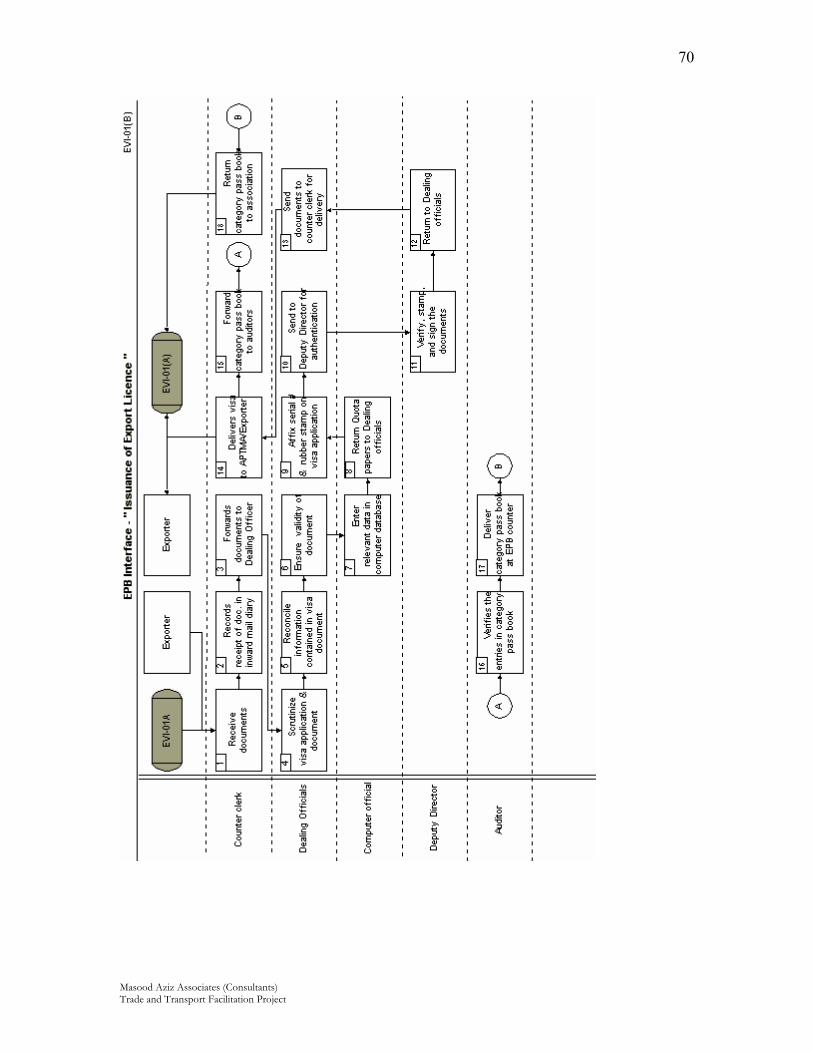

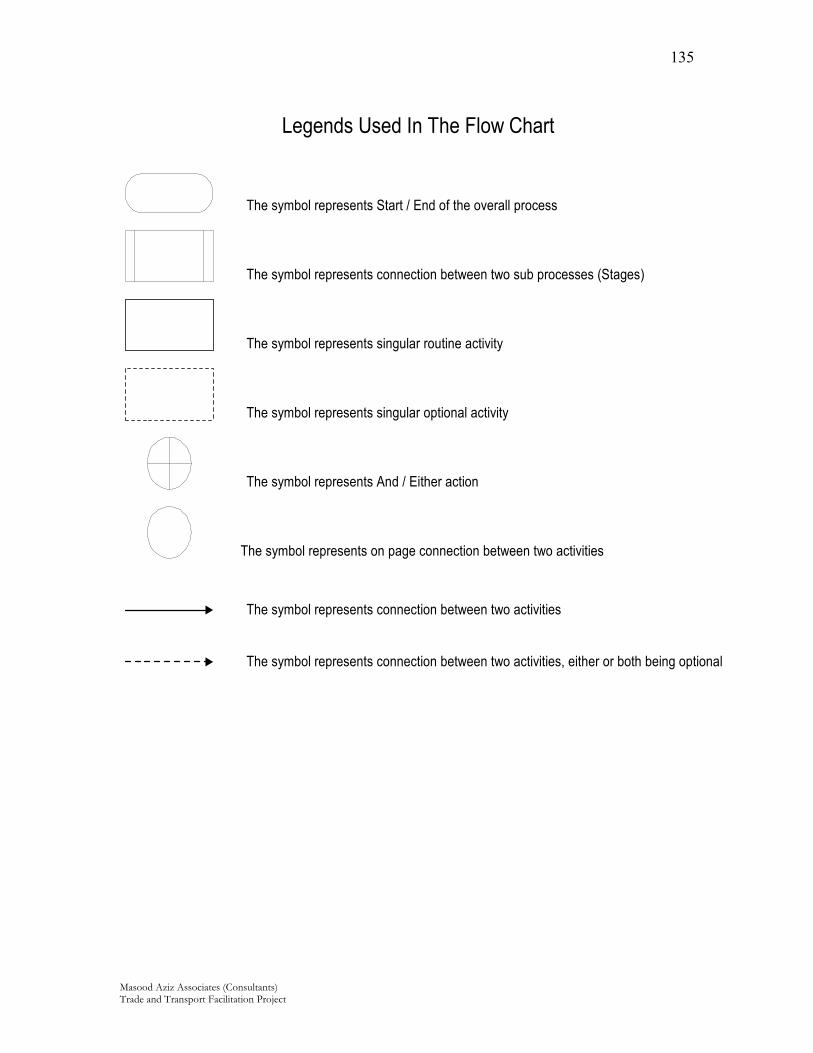

KEY TO READING THE PROCESS CHARTS

1. Name(s) of Stakeholder(s):

These are the name(s) of the stakeholder(s) who are involved in the process. The processes mentioned in front of each name shows that these activities are performed by the said person. In the diagram above, five persons are involved namely Counter Clerk, Dealing Officer, Computer Official, Deputy Director and Auditor.

2. Off-Page Connector These capsule-shaped images are called off-page connectors. They show that the flow is shifted to another process from this point to another different activity whose reference number is mentioned therein. Please refer to Serial No. 6 below (Process/Flow Chart reference Number) for more details.

3. Process Box Each box represents a single task performed by any person.

4. Task/Serial Number

This small sub-box shows the task/serial number of the processes. In order to read the description detailed description of any process box, note the serial number of sub-box in it and read the details available in the process description sheet against that number.

5. Process Description

This description explains the type of process/flow chart. For instance, the above process chart is that of Export Promotion Bureau (EPB).

2

1

3

4

6

8

5

7

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

16

6. Process/Flow Chart Reference Number

This number represents the reference of a process/flow chart. Each chart has been assigned a unique reference number. It may be seen in the above diagram (in the first row, the capsule-shaped box known as off-page connector), the flow is shifted from there to another different activity namely ‘APTMA-FC01’ (as mentioned in that (capsule-shaped) off-page connector). In order to review the referred activity (i.e. APTMA-FC01), the readers may look for a flow/process chart having the said reference number

7. Process Flow Arrow

These arrows show the direction of flow of process. 8. On-Page Connector

These circles are the on-page connectors. Each circle has a reference ID (for example A, B, C, etc.). In the diagram above, in the second row, the on-page connector, having reference ID ‘A’ shows that the process has not ended here bit it is in continuation from the sixth (last) row.

Other symbols not available in the example diagram 9. Decision Box

This picture is used at decision-making situations i.e. the situations where there are two options available and only one is to be opted. Usually, the situations are in ‘Yes’ or ‘No’.

10. Either Circle This circle is used where there may be more than one alternative to do the same task and all the alternatives are right.

11. Two-way Communication Arrow

This double-sided arrow is used to represent two-way communication between different stakeholders

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

17

INT

EG

RA

TE

D F

LO

W C

HA

RT

(T

EX

TIL

E)

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

18

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

19

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

20

IN

TE

GR

AT

ED

FL

OW

CH

AR

T (

MA

NG

OE

S)

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

21

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

22

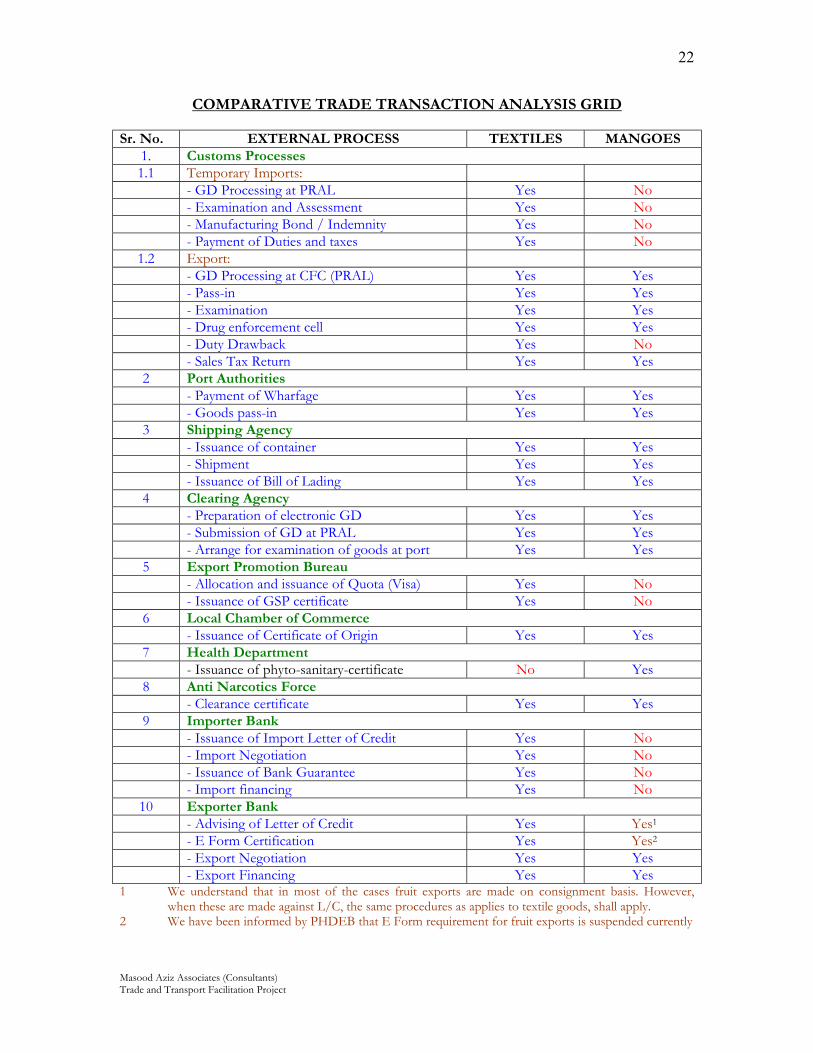

COMPARATIVE TRADE TRANSACTION ANALYSIS GRID

Sr. No. EXTERNAL PROCESS TEXTILES MANGOES 1. Customs Processes 1.1 Temporary Imports:

- GD Processing at PRAL Yes No - Examination and Assessment Yes No - Manufacturing Bond / Indemnity Yes No - Payment of Duties and taxes Yes No

1.2 Export: - GD Processing at CFC (PRAL) Yes Yes - Pass-in Yes Yes - Examination Yes Yes - Drug enforcement cell Yes Yes - Duty Drawback Yes No - Sales Tax Return Yes Yes 2 Port Authorities - Payment of Wharfage Yes Yes - Goods pass-in Yes Yes 3 Shipping Agency - Issuance of container Yes Yes - Shipment Yes Yes - Issuance of Bill of Lading Yes Yes 4 Clearing Agency - Preparation of electronic GD Yes Yes - Submission of GD at PRAL Yes Yes - Arrange for examination of goods at port Yes Yes 5 Export Promotion Bureau - Allocation and issuance of Quota (Visa) Yes No - Issuance of GSP certificate Yes No 6 Local Chamber of Commerce - Issuance of Certificate of Origin Yes Yes 7 Health Department - Issuance of phyto-sanitary-certificate No Yes 8 Anti Narcotics Force - Clearance certificate Yes Yes 9 Importer Bank - Issuance of Import Letter of Credit Yes No - Import Negotiation Yes No - Issuance of Bank Guarantee Yes No - Import financing Yes No

10 Exporter Bank - Advising of Letter of Credit Yes Yes1 - E Form Certification Yes Yes2 - Export Negotiation Yes Yes - Export Financing Yes Yes

1 We understand that in most of the cases fruit exports are made on consignment basis. However, when these are made against L/C, the same procedures as applies to textile goods, shall apply.

2 We have been informed by PHDEB that E Form requirement for fruit exports is suspended currently

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

23

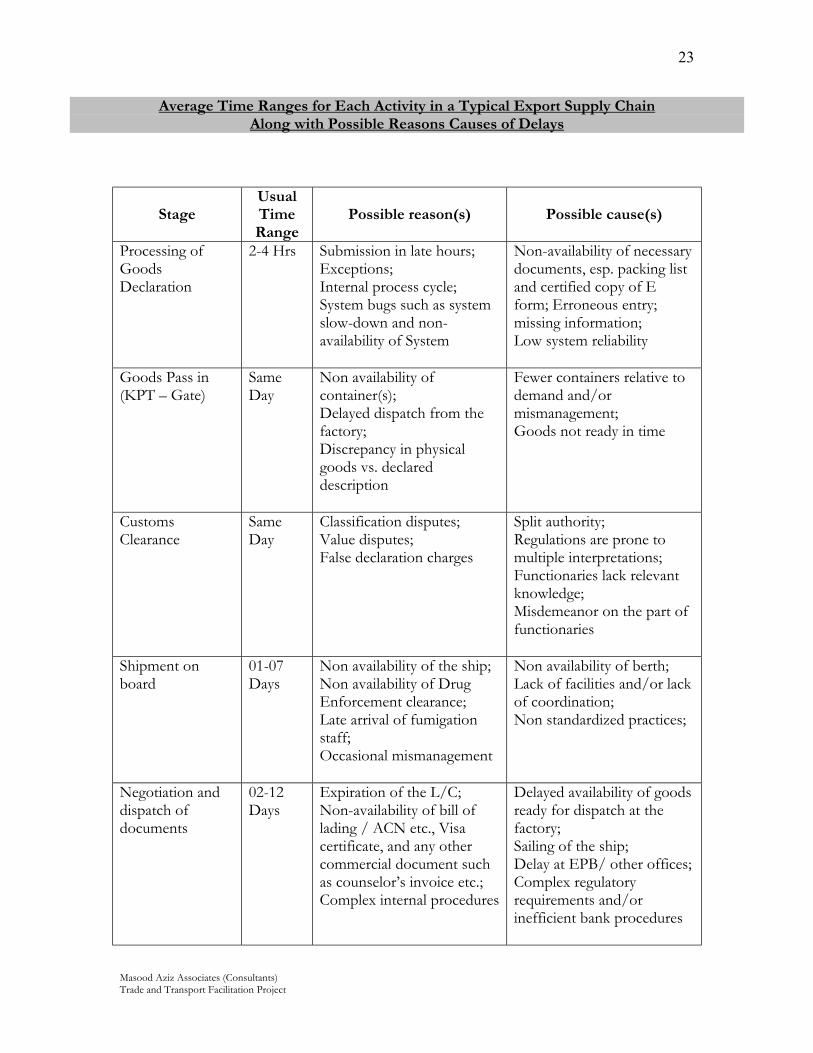

Average Time Ranges for Each Activity in a Typical Export Supply Chain Along with Possible Reasons Causes of Delays

Stage Usual Time Range

Possible reason(s) Possible cause(s)

Processing of Goods Declaration

2-4 Hrs Submission in late hours; Exceptions; Internal process cycle; System bugs such as system slow-down and non-availability of System

Non-availability of necessary documents, esp. packing list and certified copy of E form; Erroneous entry; missing information; Low system reliability

Goods Pass in (KPT – Gate)

Same Day

Non availability of container(s); Delayed dispatch from the factory; Discrepancy in physical goods vs. declared description

Fewer containers relative to demand and/or mismanagement; Goods not ready in time

Customs Clearance

Same Day

Classification disputes; Value disputes; False declaration charges

Split authority; Regulations are prone to multiple interpretations; Functionaries lack relevant knowledge; Misdemeanor on the part of functionaries

Shipment on board

01-07 Days

Non availability of the ship; Non availability of Drug Enforcement clearance; Late arrival of fumigation staff; Occasional mismanagement

Non availability of berth; Lack of facilities and/or lack of coordination; Non standardized practices;

Negotiation and dispatch of documents

02-12 Days

Expiration of the L/C; Non-availability of bill of lading / ACN etc., Visa certificate, and any other commercial document such as counselor’s invoice etc.; Complex internal procedures

Delayed availability of goods ready for dispatch at the factory; Sailing of the ship; Delay at EPB/ other offices; Complex regulatory requirements and/or inefficient bank procedures

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

24

Duty drawback1

- Gold Category - Silver Category - Others

72 Hrs 7 Days 1 Month

Delayed submission; Complex sanctioning procedure

Lack of procedural understanding by the constituent; Revenue biased system; Split authority

Reimbursement of Proceeds

180 days max. as per SBP

Dispatch of documents as cash against documents

Non-availability of L/c, or L/c expires before shipment; Discrepancy in documents

1. Time ranges mentioned for Duty Drawback indicates the minimum time range. In practice however, the sanctioning of Duty Drawback may take longer period of time particularly during May/June of every financial year when Duty Drawback payments are reportedly withheld to meet the annual net Customs revenue targets.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

25

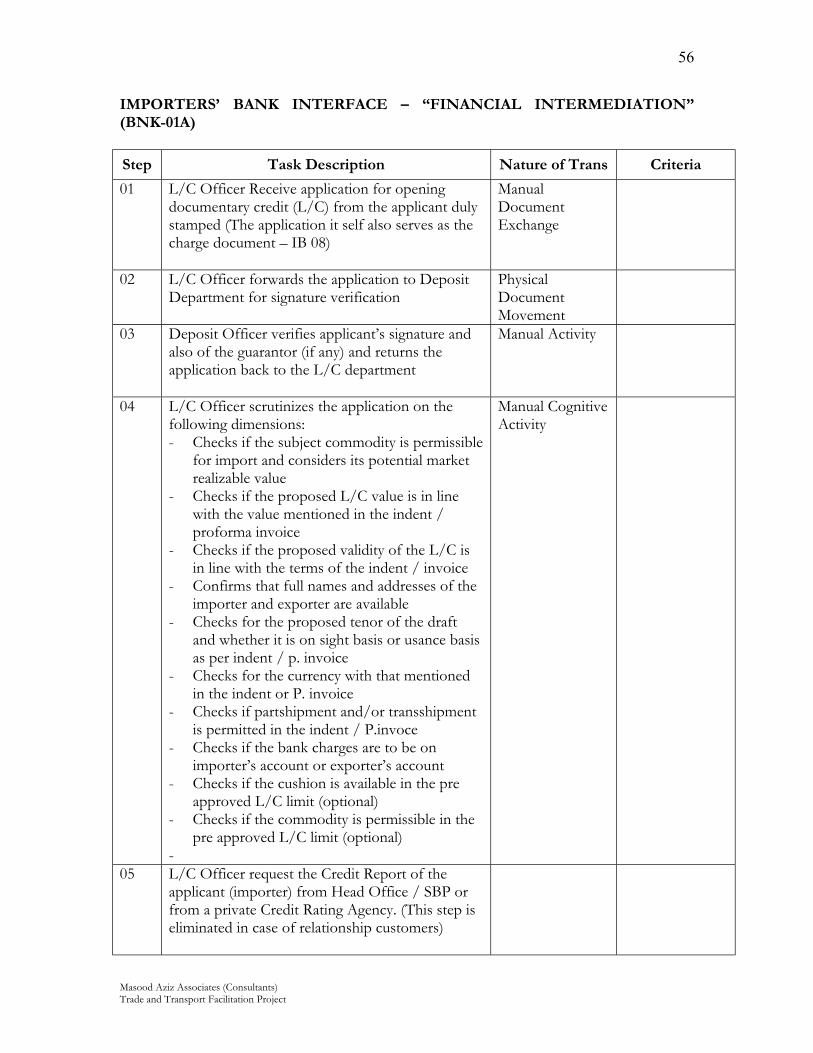

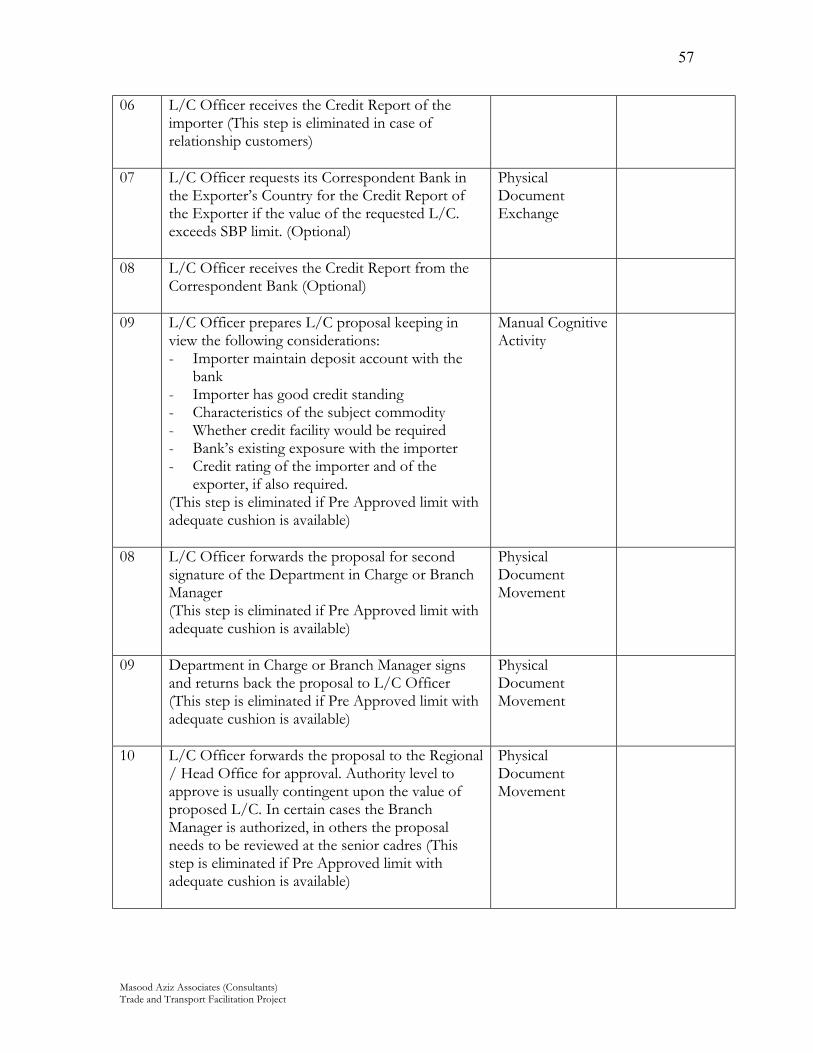

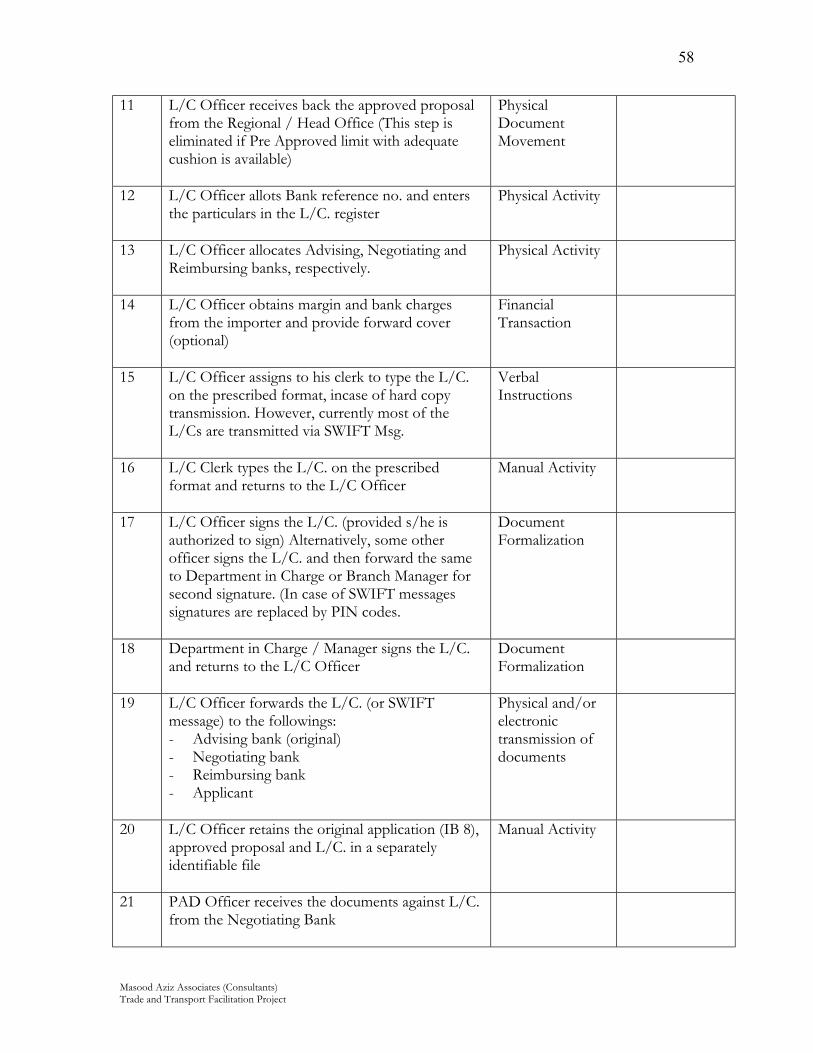

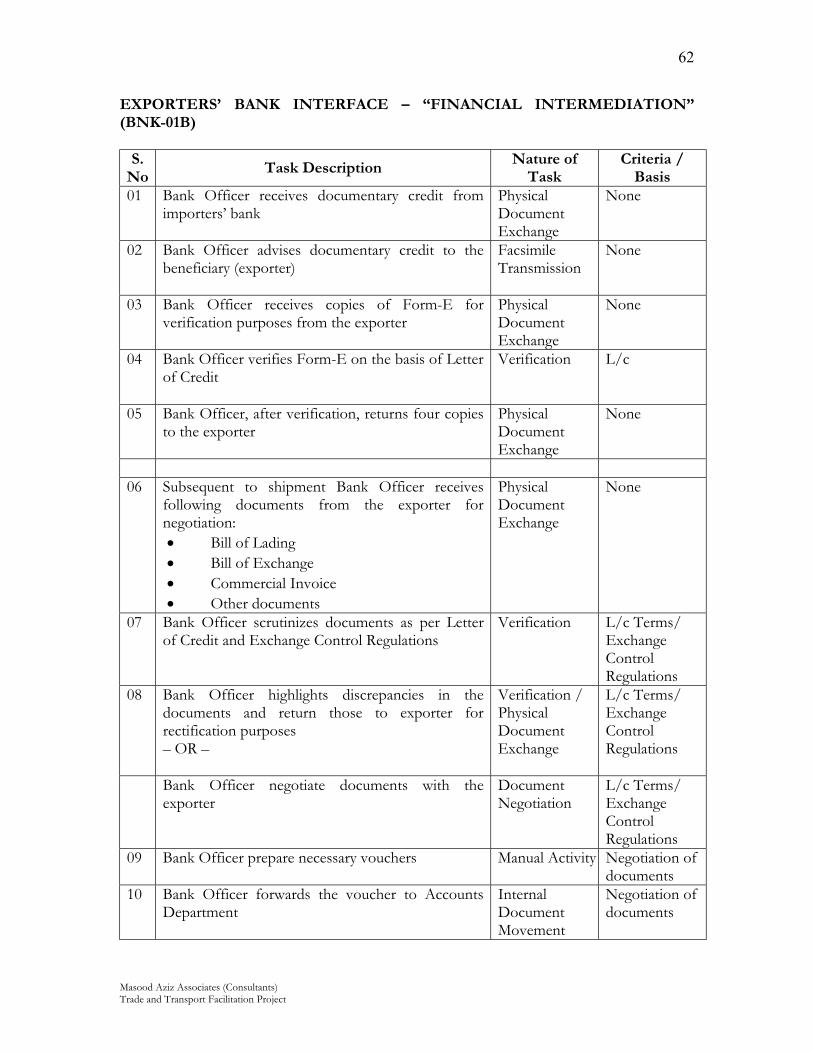

INTRODUCTION TO BUSINESS PROCESSES

1. Process: Exporter’s Bank 1.1 Key Performance

Areas: Commercial bank has many roles in the Export Value Chain. From the standpoint of this study, these are: 1.1.1 Financial inter-mediation between exporter(s) and the

importer(s) 1.1.2 Export Trade Financing

1.1.3 To ensure compliance of State Bank of Pakistan’s (SBP)

regulations which are aimed primarily at timely realization of foreign exchange proceeds.

1.1.1 Financial Intermediation: It has primarily two manifestations, namely, under Documentary

Credit and/or Collection. In the former, the bank acts as an agent to the importer and is liable by virtue of documentary credit to pay to the exporter on behalf of the importer sale proceeds subsequent to the submission of requisite documents at the bank counters on or before the stipulated date. In the latter, the bank acts as agent to exporter and collects the proceeds against documents from the Importer on behalf of the Exporter. Documentary credit can be made either on ‘Document against Payment’ (DP) basis or ‘Document against Acceptance’ (DA) basis. The term DP refers to the scenario where the importer or the bank, under the Documentary Credit, have agreed to pay as soon as the requisite documents are presented at the Negotiating Bank’s counter. The DA basis refers to the scenario whereby mutual consent of both the importer and exporter, the Documentary Credit permits release of documents on deferred payment basis. In this case, the importer or his bank accepts the annexed bill-of-exchange for payment at a future date, that could be a fixed future date or determinable future date. In either of these two situations, the issuing-bank of the documentary credit is equally liable to pay and/or accept the bill-of-exchange if otherwise in order. These transactions are governed under the Uniform Customs and Practices for Documentary Credits # 500, of International Chamber of Commerce and the local regulations.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

26

Similarly, the Exporter may approach its bank to arrange collection of the documents at the risk and responsibility of the exporter. Here the bank’s liability is restricted only to the extent of presenting the documents to the importer or his agent(s) in due course. In case the importer or his agent(s) refuses to pay or accept the annexed bill-of-exchange, the bank is not liable in any manner. However, the bank may offer to assist the exporter to find an alternate customer for the consignment, who is also willing to pay or accept the annexed bill-of-exchange. These transactions are governed under the Uniform Rules for Collection, of International Chamber of Commerce and local regulations.

Document(s) Documentary Credits (UCP) Collection (URC) Financial Documents - Bill of Exchange - Cheque, Draft - Trust receipt

Financial Documents - Bill of Exchange - Cheque, Draft - Trust receipt

Title Documents - Negotiable bill-of-lading

Title Documents - Negotiable bill-of-lading

Commercial Documents - Invoice - Certificate of origin - Packing list, etc. Transport Documents - Bill-of-lading (all inclusive) - Air consignment note - Truck receipt, etc.

Commercial Documents - Invoice - Certificate of origin - Packing list, - Bill-of-lading (all inclusive) - Air consignment note - Truck receipt, etc.

Stakeholders:

Documentary Credits (UCP) Collection (URC) Importer / Applicant Exporter / Beneficiary Importer’s / Issuing bank Advising bank Confirming bank (optional) Negotiating bank

Exporter / Drawer Importer / Drawee Exporter’s / collecting bank Presenting bank Remitting bank

Liabilities and Responsibilities:

Documentary Credits (UCP) Collection (URC) Importer / Applicant - To pay / accept bill of

exchange when presented, unless otherwise in order.

Exporter / Drawer - To make arrangement to

present the documents in due course of business

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

27

Exporter / Beneficiary - To make and present the

documents as per the terms and conditions of the documentary credit and unless otherwise in order.

Importer’s / Issuing bank - To reimburse payment to the

negotiating bank upon receipt of documents as per the terms and conditions of the documentary credit and unless otherwise in order.

Advising bank - To convey to the exporter or

his agent that the documentary credit has been established along with all the necessary details therein in due course of business and without loss of time.

Negotiating bank - To accept and/or pay the

annexed bill-of-exchange on behalf of the issuing bank (importer) when the exporter presents stipulated documents as per terms and conditions of the documentary credit and unless otherwise in order.

Confirming bank (optional) - A third bank may at the

request of importer confirms the documentary credit and whereby undertakes to reimburse to the negotiating bank. The liability is contingent upon the issuing bank’s non-performance.

Importer / Drawee - To pay and/or accept the

bill-of-exchange, as the case may be, upon acceptance of the document(s).

Exporter’s / collecting bank - To make arrangement to

present the documents for payment and/or acceptance, as the case may be, on behalf of the exporter and in due course of business.

Presenting bank - To make arrangement to

present the documents for payment and/or acceptance, as the case may be, on behalf of the collecting bank and in due course of business.

Remitting bank - To make arrangement to

remit the funds so collected to the collecting bank in due course of business, after deducting its usual charges or as mutually agreed upon.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

28

1.1.2 Export Trade Financing:

Another important service that export bank provides is Export Trade Financing. The financing has two manifestations, namely; financing for acquisition of raw materials and/or production, and typically up-front discounting of export documents. The former is known as pre-shipment financing and the latter is known as post shipment financing. SBP provides a refinance to the exporter bank thus affecting the rate of interest to decrease to 2.5% from 11% and so. This provides added advantage to the exporter. However, the finance on subsidized rates is made available to the exporter on the condition that either the export is effected within 180 days from the date of borrowing or export proceeds are received within 180 days of shipment, respectively. In the event of delay in either, the bank reverts back to normal rate of interest for the entire period.

Three variants of export financing are available on

a) Pre-shipment (Part 1) for raw material and production b) Pre-shipment (Part 2) for discounting of export documents c) Post-shipment based on last year’s performance and on the

condition that current year’s performance shall be doubled. It is available in the form of line of credit.

Stakeholders:

a) Exporter b) Authorized Dealer c) State Bank Pakistan

Liabilities and Responsibilities:

Exporter is liable to utilize the funds towards the purchase of raw materials and production of goods for export purpose only. Moreover, the exporter is obligated to effect shipment or realize proceeds from abroad within 180 days from the date of borrowing or shipment respectively, to avail financing at subsidized rates. Furthermore, in case of post shipment facility, the exporter is required to achieve 100% increase in export earnings over the last year.

The Bank is responsible for arranging subsidized financing through

SBP and for ensuring that the exporter fulfills his/her obligations as envisaged in the scheme.

State Bank of Pakistan is responsible for framing laws to regulate the

export trade financing and for making funds available at subsidized rates to the respective banks. .

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

29

1.1.3 SBP Representative:

In Pakistan the SBP is the legitimate custodian of foreign exchange and regulates its inflow and outflow. Commercial banks, as Authorized Dealers of SBP, are required to exercise vigilance on international trade transactions (on documentary basis alone) to ensure compliance with SBP regulations. Moreover, the banks are also required to monitor realization of export proceeds into Pakistan within the stipulated time period and provide timely information to SBP in either case.

To monitor the inflow of export proceeds into Pakistan, SBP uses Form E as an instrument to account for and monitor the realization of export proceeds into Pakistan. Authorized dealers are required to issue such forms to the Exporter either against confirmed documentary credit or a firm contract in case of Cash/Collection against Documents (CAD), whereby the exporter undertakes to effect remittance into Pakistan within a stipulated time i.e. 180 days. In case of failure on the part of the exporter, the authorized dealer is under obligation to pursue and compel the exporter for the remittance. The remittance into Pakistan under a confirmed documentary credit stands a fairly good chance to be effected in time, because the issuing bank is directly liable to reimburse to the negotiating bank under the documentary credit. However, under CAD transactions this advantage is automatically forfeited, as no bank is otherwise liable for the remittance of proceeds. This poses serious problems for the authorized dealers in tracking the remittance. An effective mechanism is not in place to monitor and ensure timely receipt of export proceeds. Mere undertaking of the exporter on the face of Form E does not provide effective control to the authorized dealer over the envisaged remittance. It does, however, serve as a basis to pursue the exporter to ensure timely inward remittance of foreign exchange proceeds.

Stakeholders:

a) Exporter b) Authorized Dealer c) State Bank Pakistan d) Customs

Liabilities and Responsibilities:

The Exporter by virtue of the undertaking on Form E is liable to arrange inward remittance of the export proceeds within 180 days from the date of shipment.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

30

Authorized Dealer by virtue of its obligation arising out of certifying Form E stands at par with the exporter for inward remittance of export proceeds within 180 days from the date of shipment. However, the authorized dealer does exercise direct control over the remittance under CAD transactions.

State Bank of Pakistan is responsible for framing laws to regulate the

legitimate inflow and outflow of country’s foreign exchange. In the event of failure on the part of exporter and/or his bank to bring in the export proceeds into Pakistan within the stipulated time frame, the SBP has to take appropriate action against the failing party and ensure that the remittance is effected on time.

Customs has to certify on Form-E that the goods have been exported

out of Pakistan against the documentary credit and/or firm contract under CAD. A copy of certified Form-E goes to the SBP.

1.2 Analysis/Recommendations:

It is generally observed that some times unnecessary delay occurs in negotiating the documents due to a number of reasons, such as non-availability of complete set of requisite documents, discrepancies in the documents, and delayed dispatch. It is worth noting that the ICC has already presented a draft eUCP version that emphasizes introduction of electronic document submission under documentary credits. Once approved, this will hopefully redress the problem. A copy of draft eUCP is placed at Annex-A for reference.

It has also been observed during discussions with the stakeholders

that tracking of inward remittance into Pakistan under CAD transactions is very difficult. Some alternative procedures have to be developed to address this problem, such as Bank Guarantees to ensure that the exporter is obligated to bring in the export remittance on time for Form E has failed to accomplish the desired objective w.r.t CAD transactions. Moreover, one should also realize that the existence of hundi business is a serious threat to the above.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

31

2. Process: Clearing Agent 2.1 Key Performance

Areas: The Clearing Agent plays a vital role of linking the exporter with the stakeholders for clearance and shipment of the consignment. His function(s) are identified as follows: 2.1.1 Preparation of Goods Declaration (GD) and its processing at

the Export Facilitation Centres 2.1.2 Liaise with KPT and Customs for pass-in and clearance of

the consignment, respectively

2.1.3 Coordination with shipping companies for loading of the consignments

Stakeholders: a) Exporter b) Export Facilitation Centre c) Pakistan Customs d) Clearing Agent e) Karachi Port Trust f) Shipping Company

2.1.1 GD Preparation

and Processing: The clearing agent is provided with the necessary software to produce GD for the intended export consignments. On behalf of the exporter, the Clearing Agent prepares the GD on the basis of information/documents provided by the exporter and in accordance with the requirements of the regulatory regime in force. The Clearing Agent then submits the GD to the respective Export Facilitation Centre (EFC) for its processing.

Document(s)

Following documents are generated here: a) Goods declaration form (soft copy and hard copy) b) Form E, duly certified from the Authorized Dealer (4 copies) c) Invoice d) Packing list

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

32

Liabilities and Responsibilities:

The Clearing agent is liable to present Goods Declaration (electronic copy as well as hard copy) along with other necessary documents at the EFC counters during the usual working hours. It is imperative to note that the clearing agent is liable to make correct and complete declaration. The clearing agent is also liable to respond to the queries (exceptions), if any, arising in the course of processing the GD at EFC.

The exporter is liable to provide all the relevant

information/document(s) to the Clearing agent for the purpose of producing and processing GD. The exporter is also liable to provide financial resources to the Clearing agent for the payment of necessary fee/levies.

Export Facilitation Centre is liable to accept the GDs for processing

from the Clearing agents upon payment of requisite fee and unless otherwise found in order.

2.1.2 Liaise with KPT

and Customs: After successful processing of the GD at EFC, the next steps are to bring the goods into port and get Customs clearance.

Liabilities and Responsibilities

The Clearing agent is responsible for paying wharfage and bringing the goods at the KPT gate in order to allow pass-in. Subsequent to the pass-in, the clearing agent is required to un-pack the goods for Customs examination. After the examination, the Clearing agent arranges for the re-packing of the goods for shipment. At present, all consignments are invariably opened for examination by the Customs.

KPT staff is liable to verify the physical contents of the consignment with declaration on GD and Gate pass, and make note in case of short shipment. Pakistan Customs conducts physical examination of the goods and makes a note on the GD, either confirming the contents or highlighting discrepancies, if any. Customs, after recording examination report, allows shipment. In case of any discrepancy, the same is noted usually after drawing samples and shipment is allowed. Occasionally, goods are detained pending a formal decision by senior Customs officials.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

33

2.1.3 Coordination with Shipping Company

Subsequent to the clearance of consignment from the Customs, the consignment is made available to the shipping company for loading on board.

Liabilities and Responsibilities

The Clearing agent is liable to make arrangements to deliver the consignment duly cleared for shipment and pay the usual freight and other charges. Moreover, the clearing agent is also responsible for providing to the shipping company, the specific format of the bill-of-lading on the basis of which the shipping company issues the bill-of-lading.

The Shipping Company is liable to ship the consignment on the vessel already intimated. However, in certain circumstances, mostly due to non-availability of space, the company may resort to shutting-out of the consignment. In this case the company has to convey this information to the Clearing agent / Exporter immediately and also notify what the alternate itinerary of the consignment would be.

2.2 Analysis/Recommendations: Clearing agents are licensed by the Customs and their licenses are renewed annually. There is a need to monitor and review the performance of Clearing Agents from the standpoint of their professional expertise, and compliance with Customs Law and procedure to ensure efficient processing of Customs formalities. An objective criterion to assess their performance needs to be developed and the renewal of their license may be linked thereto.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

34

3. Process: Export Facilitation Centres 3.1 Key Performance

Areas: The Export Facilitation Centres are responsible for electronic capturing, verifying and processing of customs data pertaining to exports. They have the following roles in the export value chain: 3.1.1 Electronic capturing, verifying and processing of Export

Goods Declarations, thus enhancing the completeness and integrity of the data contained in the GDs.

3.1.2 Generation of Management Information Reports / Statistics

primarily for the Central Board of Revenue, Customs and concerned ministries. It also provides relevant reports to the industry.

3.1.1 Electronic Data

Processing of GD: Goods Declarations initiated by the Exporters and/or their agents are submitted at Export Facilitation Counters prior to physical entry of the export consignment into port (Customs) area. The submission is done on a floppy disk as well as hardcopy. Here the data is processed through the available software for the following checks, namely, Pakistan Customs Tariff, Contra band items, Negative entry against the exporter(s), Negative entry against the clearing agent(s), etc. Subsequent to this, the system automatically determines the Govt. levies if any. Finally, the GD data is electronically submitted via intra-net to Customs, Bank, KPT etc. The hardcopies of processed GDs are stamped / machine numbered along with the certification, “Processed Electronically” and are handed back to the exporter(s) or their agents.

Document(s) Following documents are required/processed at EFC: a) Goods Declaration Form, 07 copies. b) Form E certified by the Authorized Dealer (Bank), 04 copies c) Customs invoice, one copy d) Packing list, one copy

Stakeholders: a) Exporter / Clearing Agent b) Pakistan Revenue Automation Ltd. c) Pakistan Customs d) Karachi Port Trust

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

35

Liabilities and Responsibilities:

Exporter / Clearing agent is liable to provide bona fide information regarding the goods being exported on the GD and its annexed documents. Moreover, the exporter / clearing agent is also liable to submit the GD prior to scheduled shipment and/or pass-in of the consignment at the EFC counters during the usual working hours and pay prescribed processing fee @ Rs.65/- for normal processing and a surcharge for late processing.

Pakistan Revenue Automation Ltd. (PRAL) is liable to make

necessary arrangement to process the GD submitted within a reasonable time on the same day. It is also required to identify any discrepancy to the exporter / clearing agent at the earliest for necessary rectification.

Pakistan Customs usually accepts the information contained on the

GD in general and conducts the usual scrutiny / physical examination of the consignment on the basis of it. Any discrepancy found shall be notified to the exporter / clearing agent and referred to the concerned senior officer for decision without delay. Shipment is allowed invariably if no major discrepancy is noticed on physical examination of goods.

Karachi Port Trust is liable to confirm the physical goods (number of

packages) against the goods description declared in the GD before allowing pass-in in the port area.

3.1.2 Management

Information Reports: EFC performs yet another important function of generating Management Information Reports for the Central Board of Revenue, Ministries of Commerce and others, Pakistan Customs and Exporters. In doing so, the EFC provides a rational basis for policy evaluation and decision making at various levels.

3.2 Analysis/Recommendations:

It is generally observed that at times unwarranted delays occur in processing the GDs. The reasons normally cited in this regard include submission of GD at late hours, input of incorrect/ incomplete data from the exporter / clearing agent end, existing IT system limitations. The problems are mentioned by the frequency of their occurrence.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

36

Submission of incorrect/ incomplete information by the exporter/clearing agent poses most of the problems. This problem is augmented due to lack of regulatory understanding of the staff of EFC. In view of the above, the following solutions are recommended:

The GD should be processed by Customs officials who are proficient in data entry / use of computer. This will eliminate dual interface by the Clearing Agent with Customs as well as EFC staff. In addition, it will be possible to detect any technical lapse in GD at a preliminary stage. Until the Custom Staff is trained to acquire these skills, there should be a concept of front end and back end work teams at EFC. Personnel in the front end should be Customs specialists while personnel at the back end should be IT specialists. Ideally, the in-charge of each EFC should be an experienced Assistant Collector.

Ultimately the entire declaration for exports should be automated in accordance with the CARE project vision. It is further suggested that export consignment of low risk exporters should be cleared for shipment directly upon processing of GD at EFC, and these consignments should not be subject to examination in general. However, randomly selected consignment may be examined physically to serve as a deterrence mechanism. Similar procedures have been in place for quite some time for imports, such as Electronic Assessment System (EASY), Automated Clearance Procedure (ACP) introduced by the Collectorate of Appraisement, Customs House, Karachi. The recommendation made above will reduce the time taken in the clearance of goods by Customs.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

37

4. Process: Karachi Port Trust 4.1 Key Performance

Areas: The Karachi Port Trust is a facilitating agency that provides infrastructure facilities for berthing vessels, and uploading or downloading of goods therein. In the context of exports from Pakistan, it primarily provides the following services 4.1.1 Physical verification of goods passing in for export by

respective exporters or their agents. Stakeholders:

a) Exporter/Clearing Agent b) Pakistan Customs c) Shipping Company d) Karachi Port Trust

4.1.1 Pass in of physical

goods into port area: Subsequent to successful processing of the GD at EFC, goods are passed-in into the port area for examination and shipment. At this point the KPT staff verifies the quantity and physical description of the goods with the details given on the GD, and confirms if the goods are passed-in in full or in part thereof.

Liabilities and Responsibilities

The Exporter/Clearing agent is liable to pay wharfage and bring the goods at the KPT gate for allowing pass-in. Subsequent to the pass-in the clearing agent is required to un-pack the goods for Customs examination. Subsequent to the examination, the Clearing agent arranges for the re-packing of the goods for shipment.

KPT staff is liable to verify the physical contents of the consignment with declaration on GD and Gate pass, and make note in case of short shipment and subsequently allow pass-in.

4.2 Analysis/Recommendations:

It is interesting to note that the goods are allowed pass-in 24 hours a day. However, Jaffar Bros. Staff at M.I. Yard, which has been assigned the task of collecting wharfage fee on behalf of KPT, works between 0900 hrs to 1700 hrs. This poses a problem for the goods coming during late hours, especially from outside Karachi, as the wharfage fee has to be paid before they can be passed-in. This results in unnecessary delay and constitutes risk of theft because the

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

38

containers remain in a public area till the fee is paid and pass-in is allowed.

It is recommended that: A one-window operation should be introduced at KPT: Arrangements should be made for the collection of wharfage fee at the KPT gate 24 hours. Alternatively, Prepaid Challans Electronic Fund Transfer (EFT) may be introduced. (N.B. It is interesting to note that while we were discussing the solutions with the stakeholders, KPT has launched pre-paid cards to redress the issue.)

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

39

5. Process: Pakistan Customs 5.1 Key Performance

Areas: Pakistan Customs operates under the Central Board of Revenue. There are four Collectorates of Customs in Karachi namely Appraisement, Preventive, Export and Port Qasim. The Collectorate of Customs (Export) is exclusively responsible for exports through Karachi port, Airport and Port Qasim. Business Processes of Customs (Exports) are essentially focused on regulating the movement of goofs across international borders. Its functions are identified as follows:

5.1.1 Pakistan Customs (Exports) is responsible for assessment of

exports consignments 5.1.2 Pakistan Customs (Exports) assists in pass-in of export

consignments

5.1.3 Examination of exported goods is carried out by the this organization

5.1.4 It is responsible for sanctioning of Duty Drawbacks

5.1.1 Assessment of

Goods: The leviable duties and taxes (if any) of Goods Declaration processed at Export Facilitation Center (EFC) are assessed by the Appraising Officer of Pakistan Customs, who is positioned in the EFC. The Appraising Officer, after thorough scrutiny of details of export consignment mentioned in a GD, corrects and/or verifies the declaration made therein by the Exporter/Clearing Agent.

Document(s)

Following documents are required at Pakistan Customs a) Goods Declaration Form b) Commercial Invoice c) Form-E

Stakeholders:

a) Exporter / Clearing Agent b) Export Facilitation Center operated by Pakistan Revenue

Automation Limited (PRAL) c) Pakistan Customs

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

40

Liabilities and Responsibilities

The Exporter/Clearing Agent has to provide bona fide information regarding the goods being exported declared on the GD and its annexed documents. Moreover, the Exporter/Clearing Agent is also liable to submit GD prior to scheduled shipment and after getting the same processed at EFC during the usual working hours. The Export Facilitation Center is responsible for accepting the GDs for processing from the Clearing Agent upon payment of requisite fee and unless otherwise in order. Appraising Officer, on behalf of Pakistan Customs, is liable to conduct the usual scrutiny of the same. Any discrepancy found shall be notified to the Exporter/Clearing Agent and the same will be rectified by the Appraising Officer.

5.1.2 Pass-in of Export

Consignments

Document(s) Following documents are required at Pakistan Customs a) Goods Declaration Form b) Commercial Invoice c) Packing List d) Form-E

Stakeholders:

a) Exporter / Clearing Agent b) Pakistan Customs

Liabilities and Responsibilities

The Exporter/Clearing Agent is liable to get the GD processed and assessed at EFC and thereafter to bring the goods as per the description mentioned in the GD along with requisite documents to the Customs staff positioned at Karachi Port Trust (KPT). The Clearing Agent/Exporter is also liable to respond to any queries that arise in due course of pass-in of export consignment. The concerned staff of Pakistan Customs has to verify the description and quantity of goods as per the declaration on the GD and thereafter facilitate/allow pass-in of goods meant for export.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

41

5.1.3 Examination of Goods

Document(s)

Following documents are required at Pakistan Customs a) Goods Declaration Form b) Commercial Invoice c) Packing List d) Form-E

Stakeholders:

a) Karachi Port Trust b) Exporter / Clearing Agent c) Pakistan Customs

Liabilities and Responsibilities

KPT authorities are responsible for allowing pass-in of goods by verifying the quantity and physical description of the goods with the details mentioned in the GD and on the Gate Pass submitted by the Clearing Agent so that the goods may be placed at the concerned yard for subsequent examination. The Exporter/Clearing Agent has to produce the relevant documents to the Examiner viz. processed GD, Invoice and Packing List. Exporter/Clearing Agent is also liable to respond to any queries which arise in due course of examination of export consignment. Pakistan Customs is liable to conduct physical examination of the goods and make a note on the GD, either confirming the contents or highlighting the discrepancies, if any. Subsequently, either allow shipment and opt to ratify the discrepancy later, or withhold the consignment for ratification of the discrepancy prior to shipment. In most cases, shipment is allowed on priority basis.

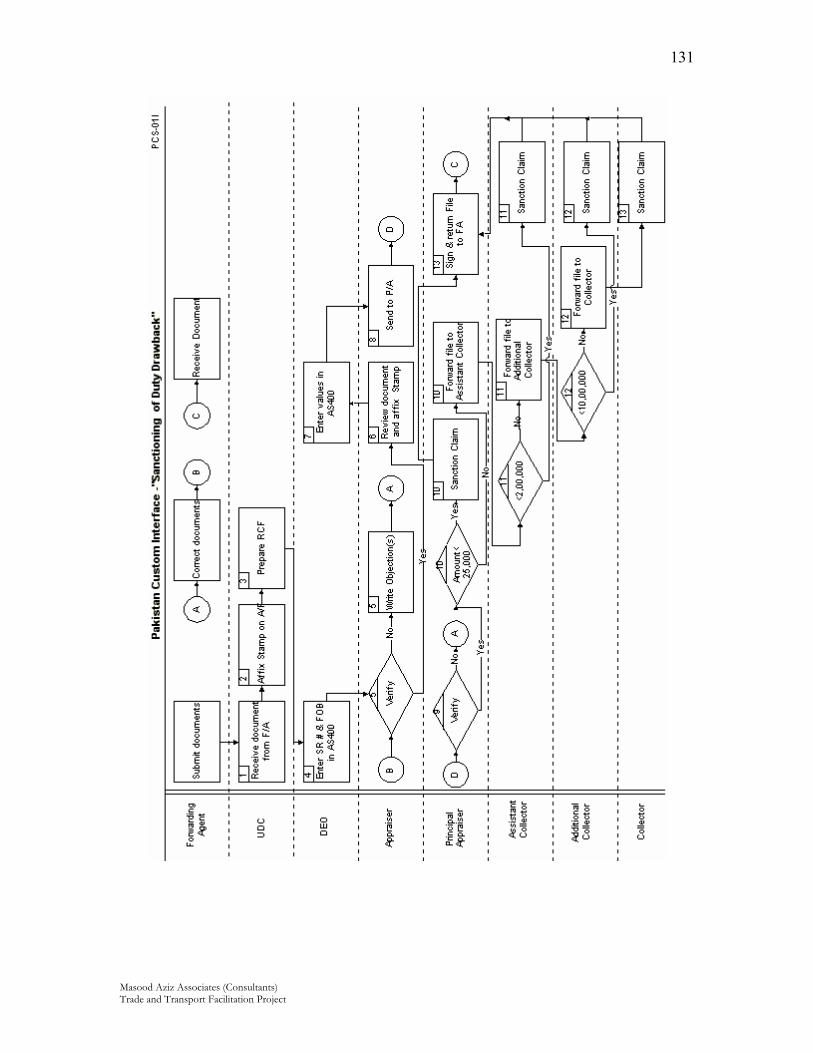

5.1.4 Sanctioning of

Duty Drawbacks

Document(s) Following document(s) are required at Pakistan Customs a) Goods Declaration Form

Stakeholders:

a) Karachi Port Trust b) Exporter / Clearing Agent c) Pakistan Customs

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

42

Liabilities and Responsibilities

Concerned authorities of Karachi Port Trust are liable to issue a Mate Receipt number on the GD confirming that the goods declared on the GD have been exported. Subsequently, Exporter/Clearing Agent applies for rebate to the Customs authorities.

The Exporter / Clearing Agent shall approach concerned KPT staff to obtain Mate Receipt number confirming that the goods have been exported. Subsequently Exporter / Clearing Agent approaches concerned staff of Pakistan Customs and claim Duty Drawback on the exported goods. Pakistan Customs is liable to facilitate Exporter / Clearing Agent applying for rebate in the process of sanctioning of the said claim.

5.2 Analysis/Recommendations

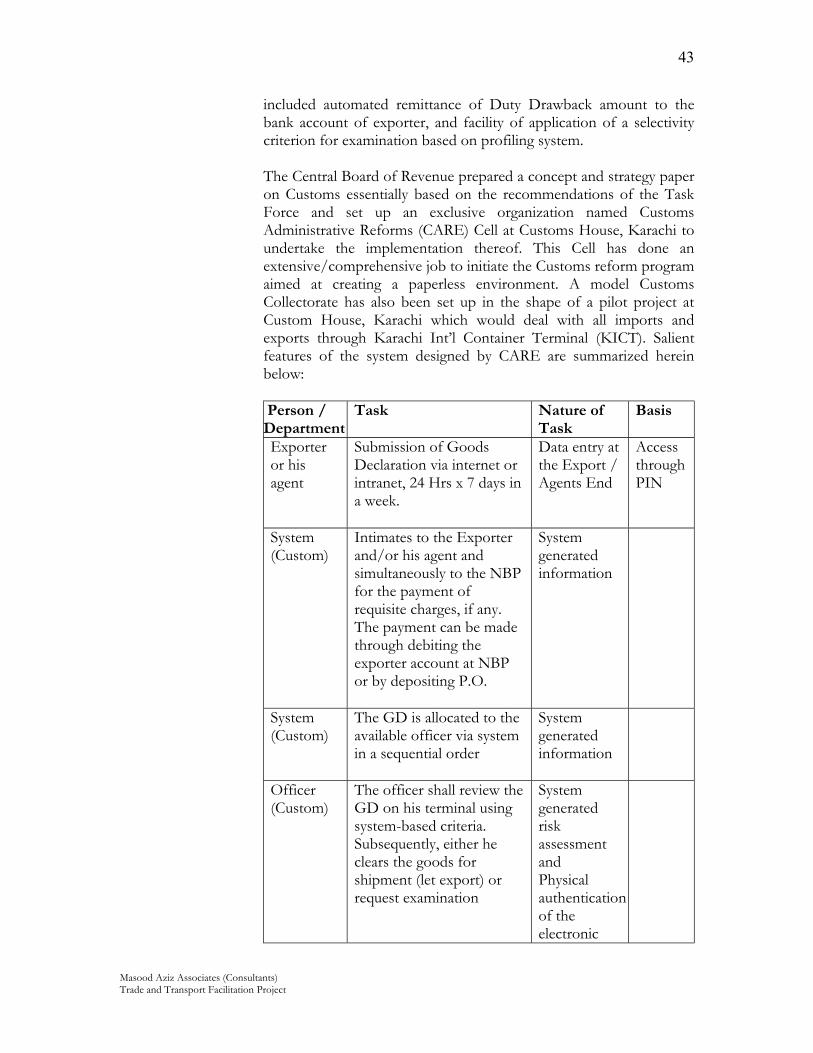

Customs plays a critical role in the movement of goods across the international borders. Besides collecting duty/taxes, it is responsible for enforcing a wide array of laws and regulations viz. checking movement of illicit goods, enforcement of intellectual property rights, classification and valuation of goods, sanctioning of duty drawbacks and performing security functions. They face the challenge of striking a balance between the imperatives of trade facilitation and effective enforcement of regulations. Fortunately, considerable work has already been accomplished to revamp the Customs regulatory system in Pakistan. Customs Business Processes were extensively reviewed by Task Force on Tax Administration set up by the Government in year 2000. Government had adopted the recommendations of the Task Force for simplifying and automating the business processes of Pakistan Customs. The recommendations included submission and validation of electronic declarations in the Customs Services Centre, automated allocation of GD to Appraising Officers at Processing Section, online linkage to Export Policy Order, Duty Drawback notifications and automated communication of examination instructions to the examining staff. It further included automated allocation of examination to Appraising Officers and automated random selection of package numbers to be examined and recording of examination report with a facility to view it on-screen by senior management. For the purposes of Duty Drawback, it was recommended that there should be no separate submission of duty drawback claims, automated calculation of Duty Drawback amount, Pre-audit of Duty Drawback claims simultaneously by the internal audit section. It also

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

43

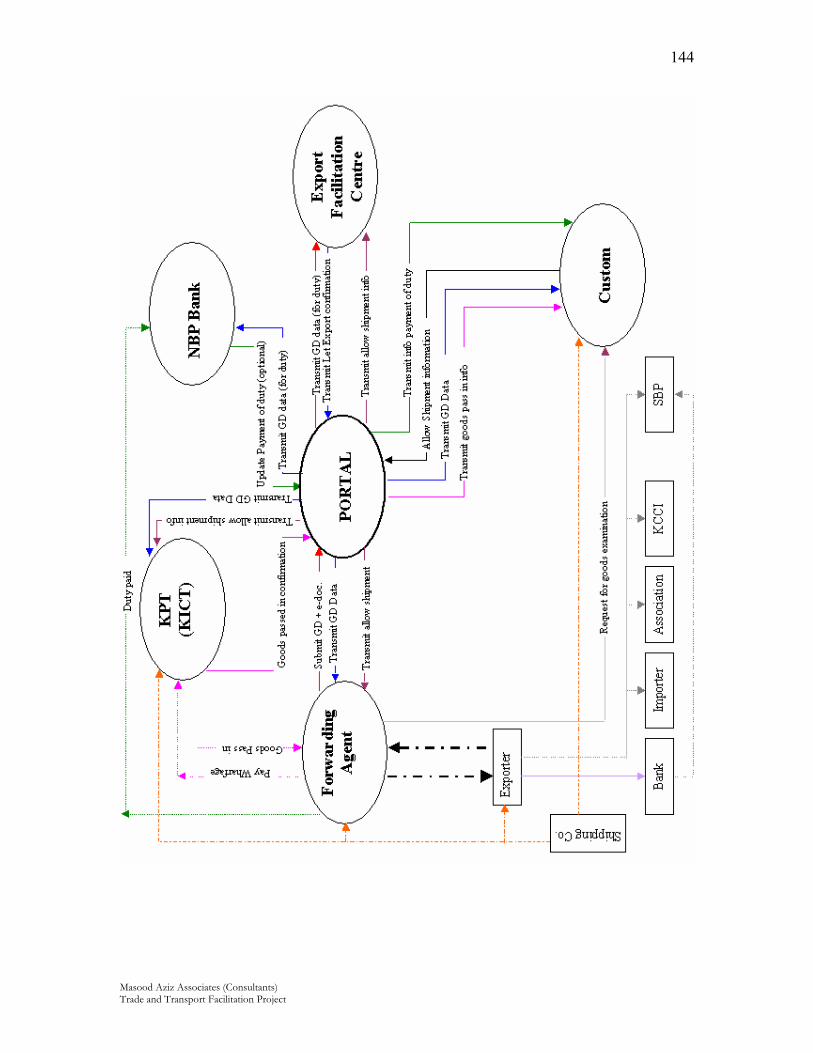

included automated remittance of Duty Drawback amount to the bank account of exporter, and facility of application of a selectivity criterion for examination based on profiling system. The Central Board of Revenue prepared a concept and strategy paper on Customs essentially based on the recommendations of the Task Force and set up an exclusive organization named Customs Administrative Reforms (CARE) Cell at Customs House, Karachi to undertake the implementation thereof. This Cell has done an extensive/comprehensive job to initiate the Customs reform program aimed at creating a paperless environment. A model Customs Collectorate has also been set up in the shape of a pilot project at Custom House, Karachi which would deal with all imports and exports through Karachi Int’l Container Terminal (KICT). Salient features of the system designed by CARE are summarized herein below: Person / Department

Task Nature of Task

Basis

Exporter or his agent

Submission of Goods Declaration via internet or intranet, 24 Hrs x 7 days in a week.

Data entry at the Export / Agents End

Access through PIN

System (Custom)

Intimates to the Exporter and/or his agent and simultaneously to the NBP for the payment of requisite charges, if any. The payment can be made through debiting the exporter account at NBP or by depositing P.O.

System generated information

System (Custom)

The GD is allocated to the available officer via system in a sequential order

System generated information

Officer (Custom)

The officer shall review the GD on his terminal using system-based criteria. Subsequently, either he clears the goods for shipment (let export) or request examination

System generated risk assessment and Physical authentication of the electronic

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

44

information contained in the GD

System The information is then communicated to the followings: - Exporter or his agent - Terminal Operators - Concerned Custom

officials

Auto generated process

Terminal Operators

Receive the container at gate, duly sealed by the exporter or his agent etc at least 12 hours prior to the scheduled time of vessel departure. Prior to pass in the container number and is fed into the system to determine the status of the goods.

Physical movement of goods

Terminal Operators

Either move the goods in the yard for shipment as per loading program, or transfer the container in the examination area as the case may be.

Physical movement of goods

Terminal Operators

Unload the goods in presence of custom officials for examination / withdrawal of samples

Physical movement of goods

Custom officials

Examine the goods or take samples to verify bonafideness of goods for export as per Pakistani laws and regulations. Upon satisfaction, authorizes “let export” via system

Physical examination

Terminal Operators

Reload the goods into the container

Physical movement of goods

Custom Officials

Puts Custom’s Seal confirming examination.

Physical action

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

45

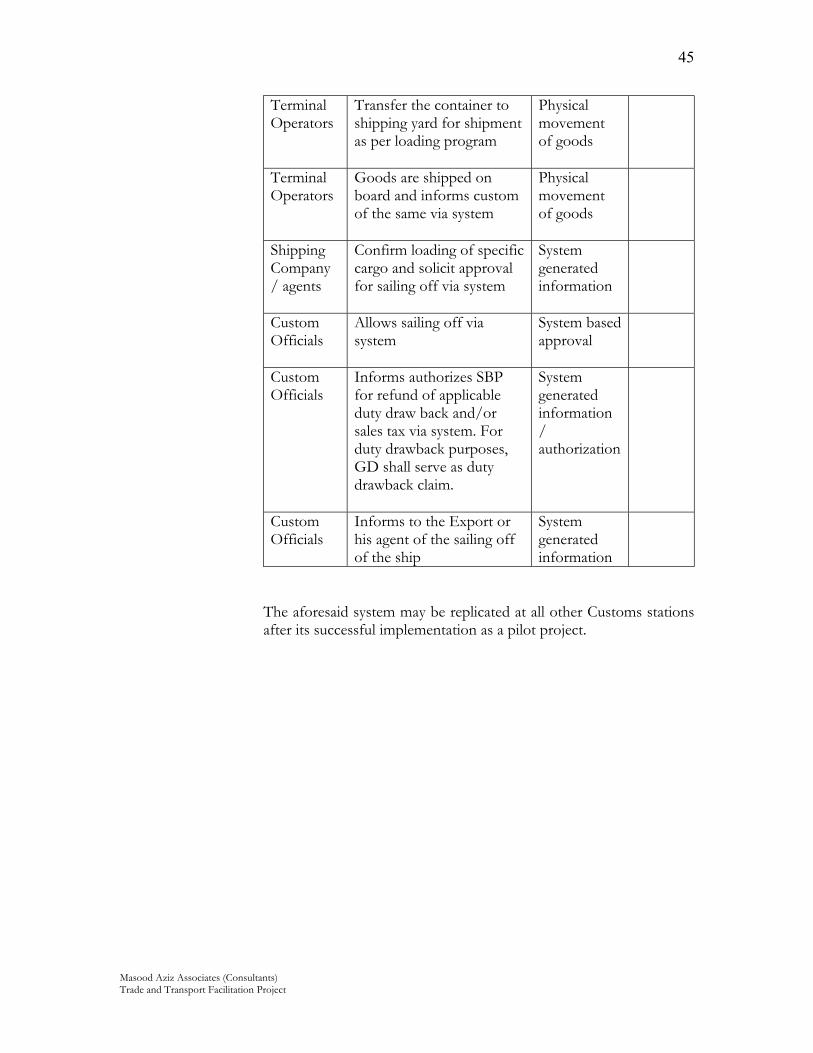

Terminal Operators

Transfer the container to shipping yard for shipment as per loading program

Physical movement of goods

Terminal Operators

Goods are shipped on board and informs custom of the same via system

Physical movement of goods

Shipping Company / agents

Confirm loading of specific cargo and solicit approval for sailing off via system

System generated information

Custom Officials

Allows sailing off via system

System based approval

Custom Officials

Informs authorizes SBP for refund of applicable duty draw back and/or sales tax via system. For duty drawback purposes, GD shall serve as duty drawback claim.

System generated information / authorization

Custom Officials

Informs to the Export or his agent of the sailing off of the ship

System generated information

The aforesaid system may be replicated at all other Customs stations after its successful implementation as a pilot project.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

46

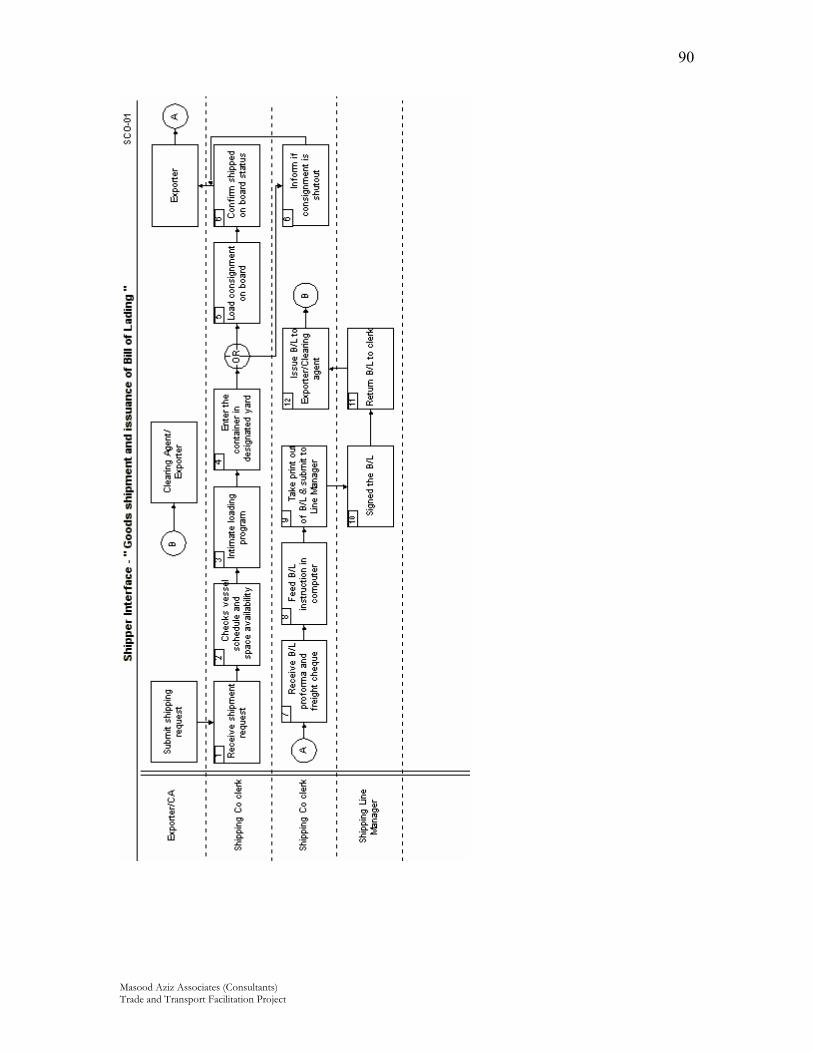

6. Process: Shipping Company 6.1 Key Performance

Areas: The Shipping Company has one of the most critical roles in the export supply chain. Its function(s) are identified as follows: 6.1.1 Physical transportation of the goods from port of origin to

the port of destination 6.1.2 Take possession of the consignment as bailee

6.1.1 Physical

Transportation: The shipping company provides one of the most valuable services in the Export Supply Chain, as they make possible safe, secured and timely delivery of the consignment(s) at port of destination.

Document(s) Following documents are generated here: a) Shipper Bill of Lading b) Shipper Export Manifest

Stakeholders: a) Exporter / Clearing Agent b) Importer / Clearing Agent c) Shipping Company d) Pakistan Customs e) Karachi Port Trust

Liabilities and Responsibilities:

The Exporter / Clearing agent has to make available the consignment (goods) at the port duly cleared for shipment on board, and pay usual freight and other charges.

Importer / Clearing agent at the port of destination is liable to make

arrangement to obtain the delivery of the consignment (goods) and pay usual levies as per local rules and regulations.

Pakistan Customs is the authority that allows shipment of the

consignment (goods) on board. Karachi Port Trust is responsible for making arrangements for

anchorage of the ship and loading of the consignment (goods) in the due course of business.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

47

6.1.2 Bailee: Shipping company receives the consignment (goods) in the capacity of a bailee, subsequently it undertakes the liabilities and responsibilities of a bailee of making arrangements for the safe keeping and transportation of the consignment (goods) on behalf of the bailor (consignor) in consideration of freight charges received.

Stakeholder(s)

a) Exporter / Consignor / Bailor b) Shipping Company / Bailee

Liabilities and Responsibilities:

The Exporter is liable for providing the goods (consignment) in an appropriately packed manner, and pays the usual freight charges to the shipping company.

The Shipping company as bailee is responsible for making

appropriate arrangements for the safe keeping and transportation of goods to the port of destination on behalf of the exporter (consignor) and deliver the consignment to or to the order of a third party, who happens to be the holder of the title document (Bill of Lading) in the due course.

6.2 Analysis/Recommendations:

It is the general practice that bill of lading is issued in 24 hours from the date of sailing of the ship. In practice, however, issuance of bill of lading some times takes even longer. Primarily two reasons are cited: firstly, the existence of multiple formats depending on importers’ requirement. Secondly, the manual exchange of documents also increases the time taken to issue Bill of Lading (B/L). Multiple formats requirement entails transmission of the specific format by the exporter to the shipping company on individual consignment basis.

It has been observed that shipping companies issue bills of lading in back date, which is usually prior to the date of sailing. This practice is improper and risky for the law does not permit issuance of the bill-of-lading prior to sailing of the ship. We understand that this practice exists in order to accommodate the exporters who fail to ship their consignments by the dead line prescribed in the documentary credits, therefore they obtain the bill of lading in back date to avoid the repercussions for non-compliance of the terms of documentary credit.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

48

It is recommended that: a. Initiatives should be taken to develop global template of bill-of –

lading. This would eliminate the unnecessary exchange of documents in addition to enabling automatic generation of bill-of-lading subsequent to sailing of the ship.

b. The shipping companies should switch onto electronic document

exchange and automate the issuance via an on line system. This will not only expedite the process but would also enable processing to continue 24 hours a day, seven days a week.

c. With regard to issuance of bill-of-lading from the back date,

shipping companies and their agents should be persuaded to stop this illegal practice forthwith.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

49

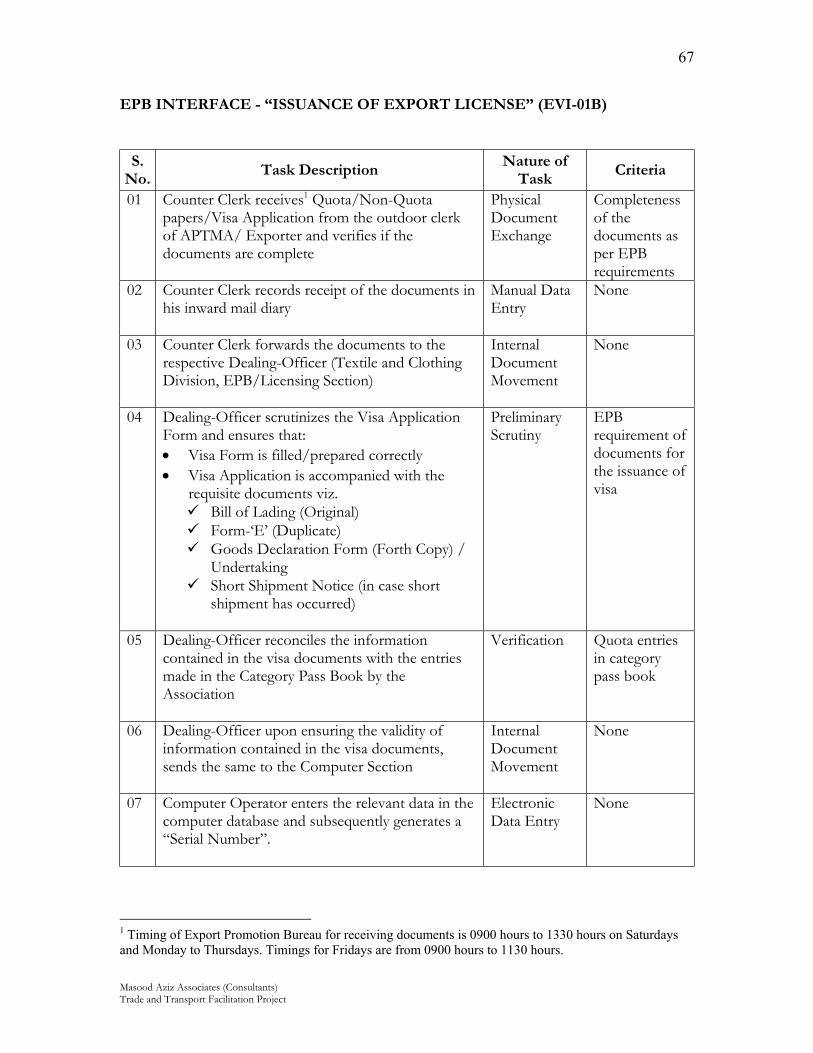

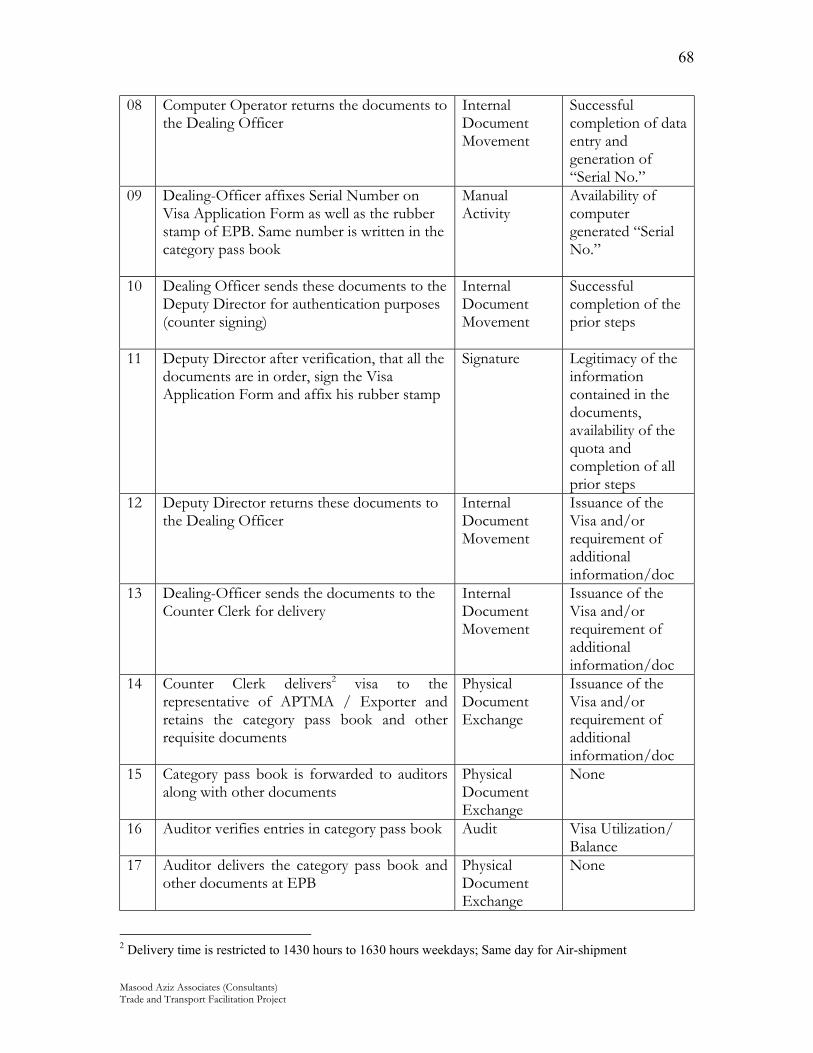

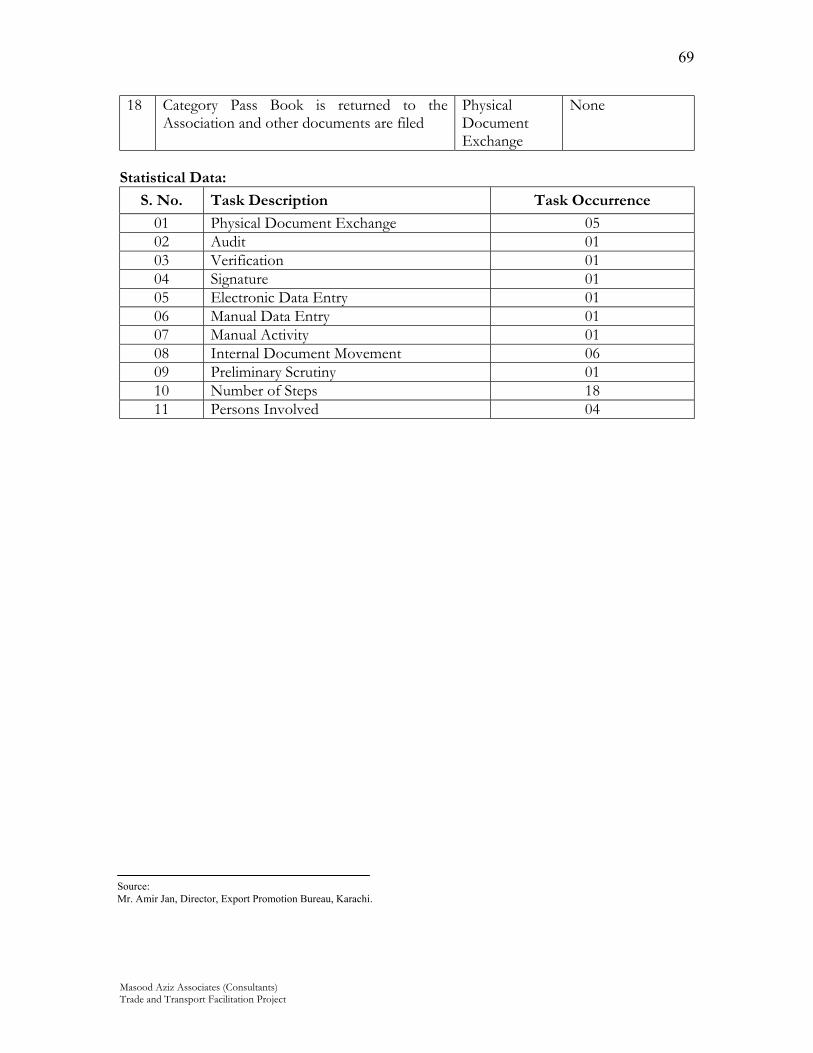

7. Process: Export Promotion Bureau (EPB) 7.1 Key Performance

Areas: The Export Promotion Bureau is the custodian of textile export quota. By virtue of its role under the quota regime, it is required to administer quotas i.e. allocate and/or sell quotas to the exporters, issue visas and maintain records. It is essential to note that the Export Promotion Bureau also issues certificates of origin in respect of textile exports under quota restrictions. Its function(s) are identified as follows: 7.1.1 Selling/Allocation of quota 7.1.2 Issuance of visa 7.1.3 Certification and issuance of Certificate-of-Origin for quota

items

Stakeholders: a) Exporter (Exporters’ Association), and b) Export Promotion Bureau

7.1.1 Allocation of Quota:

Textile export quota is allocated to different exporters on the basis of following criteria: a) Last year’s export performance (in respective category) b) Open auction. c) Residue allocation on first come first served basis.

7.1.2 Issuance of Visa:

Visa is a document issued by EPB authorizing export of textile products against allocated quota. Visa is issued against each export on the following criteria: - Availability of quota balance, as per entry in the category

passbook of the respective exporter. - Submission of visa application along with the following

document(s) a) Bill of lading (original) b) Form E (duplicate copy) c) Goods declaration (fourth copy) d) Short shipment notice, if applicable.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

50

7.1.3 Certificate of Origin: CoO (GSP certificate) in respect of quota items exported from Pakistan is issued on submission of the following documents: a) Application b) Bill of lading (copy) c) Commercial invoice d) Visa (copy)

Liabilities and Responsibilities:

The exporter (exporters’ association) has to apply to the EPB for the issuance of Export Visa and CoO, and provide bona fide details of and proof of the goods exported via bill of lading or other documents such as Airway bill, Truck receipt etc. confirming that the goods have been exported from Pakistan and pay fee @ Rs.250/- per request.

The EPB is liable to issue Export Visa and Certificate of Origin in

the due course, when demanded for and fee is paid by the exporter.

7.2 Analysis/Recommendations: Consequent to the WTO Agreement on Textile and Clothing (ATC) superceding the Multi-Fiber Agreement, the quota restrictions shall become void from Jan 2005. Hence, the requirement for Export visa shall not exist.

In view of the above, it is recommended that issuance of CoO may

be assigned at the Chamber of Commerce and Industry (KCCI) in respect of quota items, which was hitherto issued by the EPB as well. However, some alternative arrangement could be made to compile data in respect of export of textile products for informed decision making.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

51

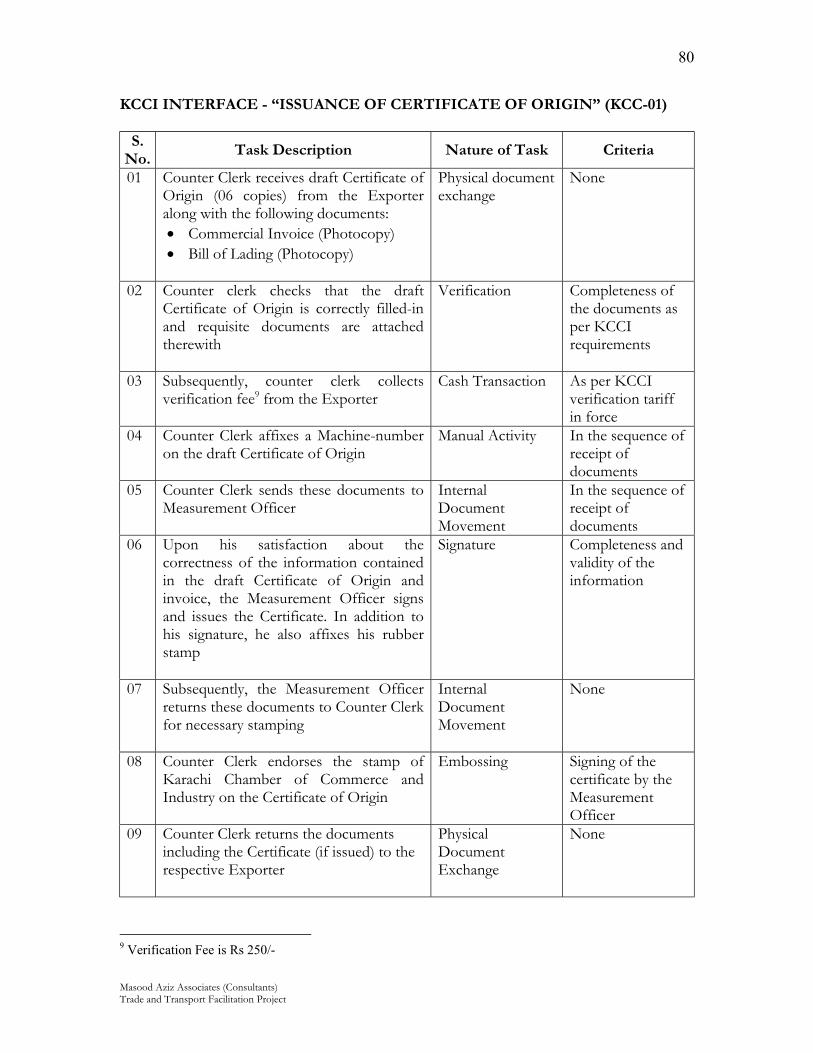

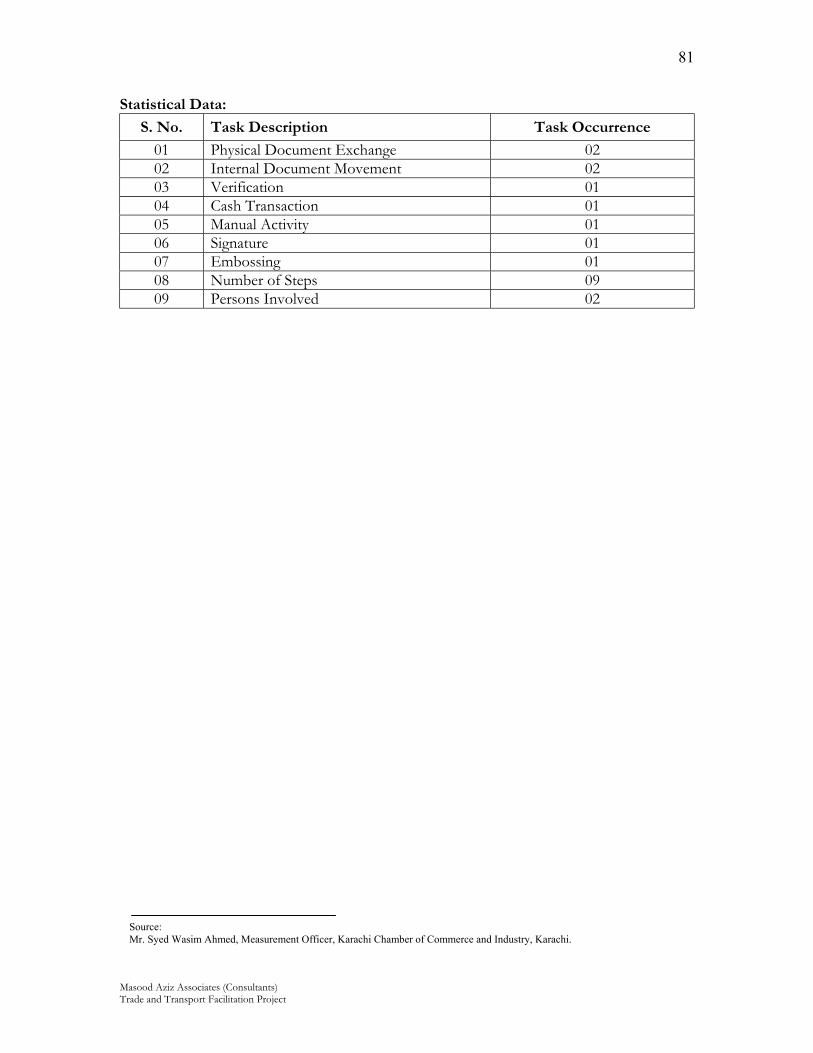

8. Process: Karachi Chamber of Commerce and Industry

8.1 Key Performance Areas:

The Karachi Chamber of Commerce and Industry is authorized by the Ministry of Commerce to award / issue certificate of origin in respect of exports from Pakistan This certificate is required by various importing countries. The Export Promotion Bureau issues certificates of origin in respect of textile exports under quota restrictions. Its function(s) are identified as follows: 8.1.1 Certification and issuance of Certificate-of-Origin

Stakeholders: a) Exporter, and b) Karachi Chamber of Commerce and Industry

8.1.1 Certificate of

Origin: Certificate of origin is a document issued by KCCI on behalf of Ministry of Commerce, Govt. of Pakistan. It certifies that the country of origin in respect of the export consignment(s) is Pakistan. It is a mandatory requirement for quite a few importing countries particularly those meant for GSP purposes.

Document(s)

a) Commercial Invoice issued by the Exporter (Xerox copy] b) Bill of lading (Xerox copy] c) Certificate of Origin

Liabilities and Responsibilities:

The exporter is liable to apply to the KCCI for the issuance of CoO and provide bona fide details of goods exported and proof of the goods exported via bill of lading or other documents confirming that the goods have been exported from Pakistan and pay a fee @ Rs.250/- per request.

The Karachi Chamber of Commerce is liable to issue Certificate of

Origin in the due course, when demanded for and the exporter pays the fee.

8.2 Analysis/Recommendations: The certificate is generally issued within one to two hours of submission of the requisite documents. Apparently, no problem exists in the process.

Masood Aziz Associates (Consultants) Trade and Transport Facilitation Project

52

BUSINESS PROCESSES DESCRIPTIONS AND FLOW CHARTS

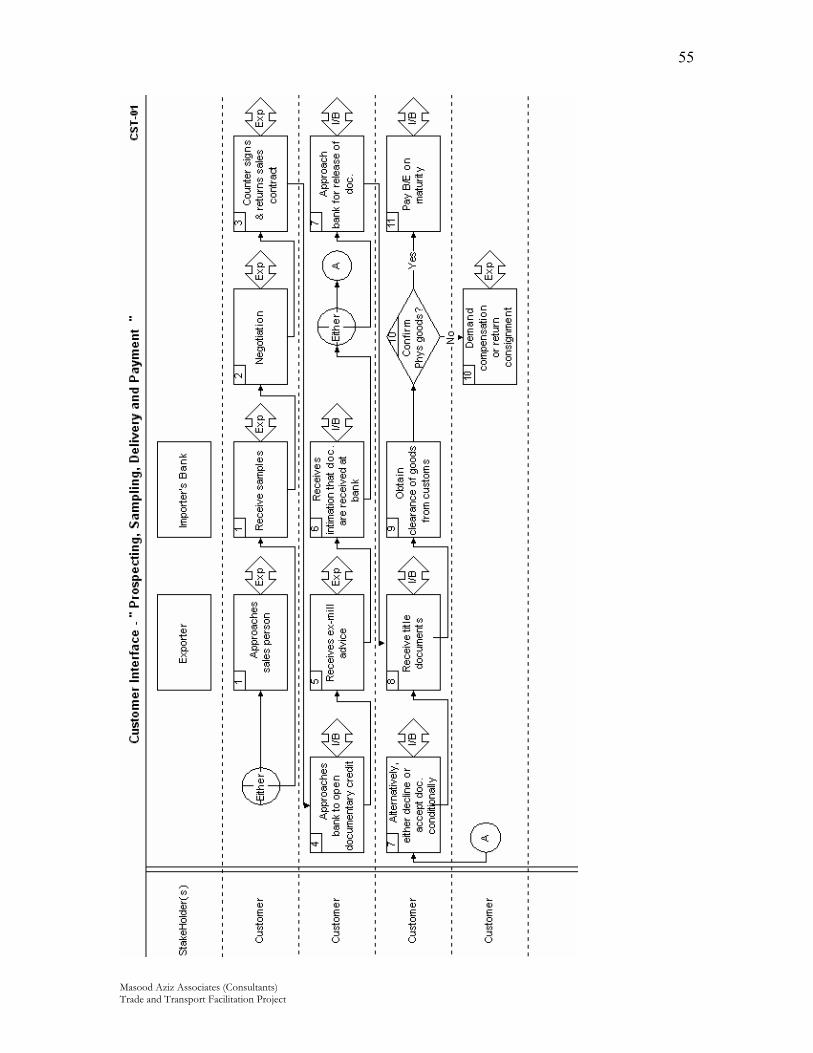

LIST OF PROCESSES Ref. No. Processes)

IEC 01 Integrated Process (External Export Supply Chain)

CST 01 Customer Interface

BNK 01 (a) Bank Interface (Opening of L/c and payment against import

documents)

BNK 01(b) Bank Interface (Advising of L/c and negotiation of export

documents)

CAG 01 (a) Clearing Agent (Assistance in clearance of imports)

CAG 01 (b) Clearing Agent (Assistance in clearance of exports)

PCS 01 (a) Pakistan Customs (CSC Import GD Processing)

PCS 01 (b) Pakistan Customs (Temporary Imports)

PCS 01 (c) Pakistan Customs (Import under Manufacturing Bond)

PCS 01 (d) Pakistan Customs (Bank Guarantee – deposit)

PCS 01 (e) Pakistan Customs (EFC Export GD Processing)

PCS 01 (f) Pakistan Customs (Pass in of Export Goods)

PCS 01 (g) Pakistan Customs (Export Examination)

PCS 01 (h) Pakistan Customs (Bank Guarantee – release)

PCS 01 (i) Pakistan Customs (Duty Drawback Sanctioning)

KPT 01 (a) Release of imported goods

KPT 01 (b) Pass in of Goods for Export

SCO 01 Shipment of goods and issuance of bill of lading

EVI 01 (a) APTMA (Assistance in Visa issuance)

EVI 01 (b) EPB (Issuance of Visa)