paying for college for higher income families easfaa may 21, 2002

TRANSCRIPT

Paying for College for Higher Income Families

EASFAAMay 21, 2002

2

Agenda

Why do we need a presentation specifically for families with higher income?

Review “Paying for College for Higher Income Families”

– Financial planning recommendations

– Understanding cost and EFC using case studies

– Understanding awards using case studies

– Scholarships

– Other financing options

– Tax Benefits

Why Do We Need This?

4

Why do we need this?

9 of the 14 EASFAA states rank in the top 20 states for highest income per capita

Economic downturn causing major impact on education investment plans

FA presentations focus on lower-to- middle income families

Higher income families have unique questions and issues

5

Dependent Undergrads By Family Income, 1995-96

Source: US Dept. Of Ed, NSES, 1995-96 National Postsecondary Student Aid

35%

37%

28%

Low IncomeBelow $35,000

Middle Income$35,000-$69,999

Higher IncomeOver $70,000

6

States with Highest Income Per Capita

Top 6 in Northeast

- - Top 6 states in

2001

7

Cost of College, Less Aid, Increases with Income

SOURCE: College is Possible, 1995-1996 data

$947

$4,004

$10,428

$4,017

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

Public Private

Tuit

ion, Le

ss G

rants

Family income$15,000 & less

Family income$70,000 & above

8

How You Market This Presentation

Affluent high schools, no special marketing

High schools with mixed income levels, targeted marketing to high income families

9

Paying For Collegefor Higher Income Families

10

Estimate total costs for all 4 years of college

Parents and Student together should develop a plan to fund and finance– know what you’re signing up for– know how you will pay for it

If you need to borrow– understand options: educational loans,

personal loans, home equity loan – know the terms

Apply to at least one financially ‘safe’ school

Financial Planning Recommendations

11

$44BLoans

$30BPay-as-you-go

$30BFrom Savings

$22BOther FinancialAid/Scholarships

$126 billion were spent by 14 million students in the 1997 - 1998 school year

Sources: Estimates based on College Board, College Savings Plan Network, research conducted by Richard Day Research, Inc. for Fidelity Investments

Families Use Several Sources to Finance College Costs

12

Financial Planning for Higher Education

13

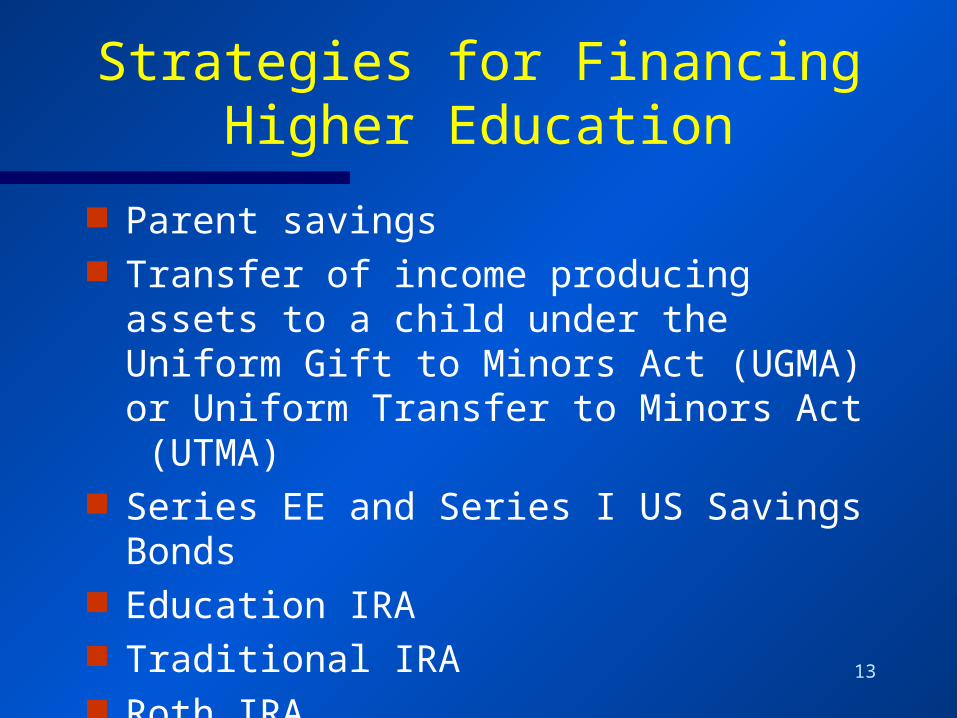

Parent savings Transfer of income producing assets to

a child under the Uniform Gift to Minors Act (UGMA) or Uniform Transfer to Minors Act (UTMA)

Series EE and Series I US Savings Bonds Education IRA Traditional IRA Roth IRA Qualified Tuition Savings Plans

Strategies for Financing Higher Education

14

Comparing and Contrasting Financing

Strategies

+ -

15

Parent Invests Money in His or Her Name

Advantages: Maintains parental control over savings Can ease tax bite by using tax efficient

investments and take advantage of favorable long-term capital gains tax rates

Minimizes impact on financial aid eligibility Can gift funds to the child as college gets closer Withdrawals can be made for any need of the

child—not just college

16

Parent Invests Money in His or Her Name

Disadvantages: Earnings and capital gains taxed at

parent’s rate during accumulation and distribution

17

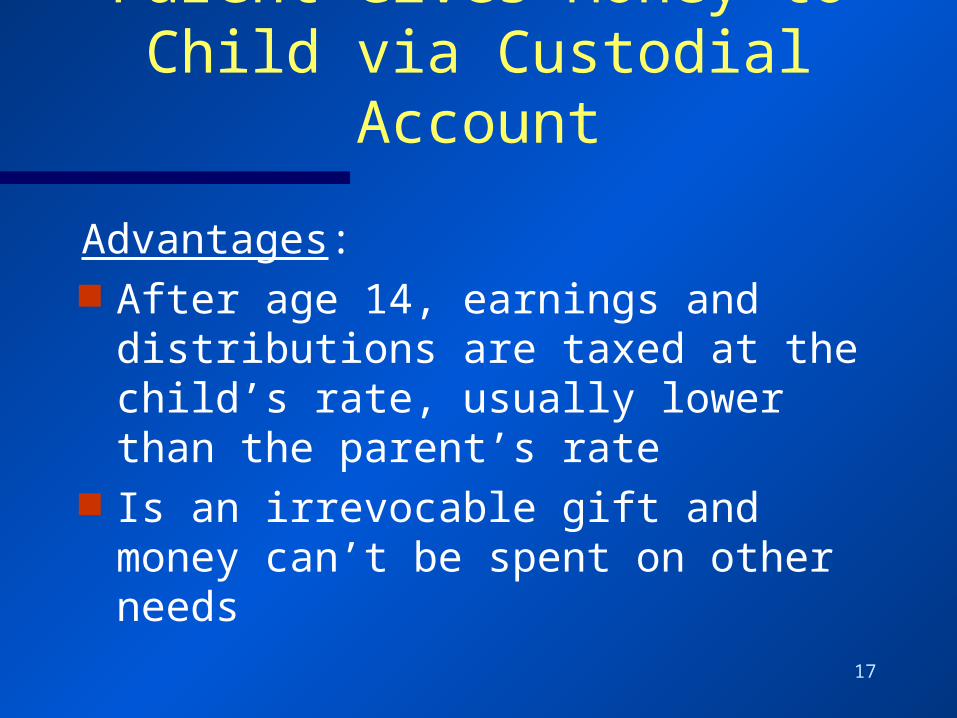

Parent Gives Money to Child via Custodial

Account

Advantages: After age 14, earnings and

distributions are taxed at the child’s rate, usually lower than the parent’s rate

Is an irrevocable gift and money can’t be spent on other needs

18

Parent Gives Money to Child via Custodial Account

Disadvantages: Money belongs to the child when

he or she reaches the age of majority

May have negative impact on financial aid eligibility

19

Series EE and Series I Savings Bonds

Advantages: Interest excludable from income

when used for qualified educational expenses

Bonds belong to parents

20

Series EE and Series I Savings Bonds

Disadvantages: Benefits phase out at certain income

ranges Bonds pay lower interest rates than other

fixed income investments Exclusion does not apply to room and

board expense, only tuition and fees

21

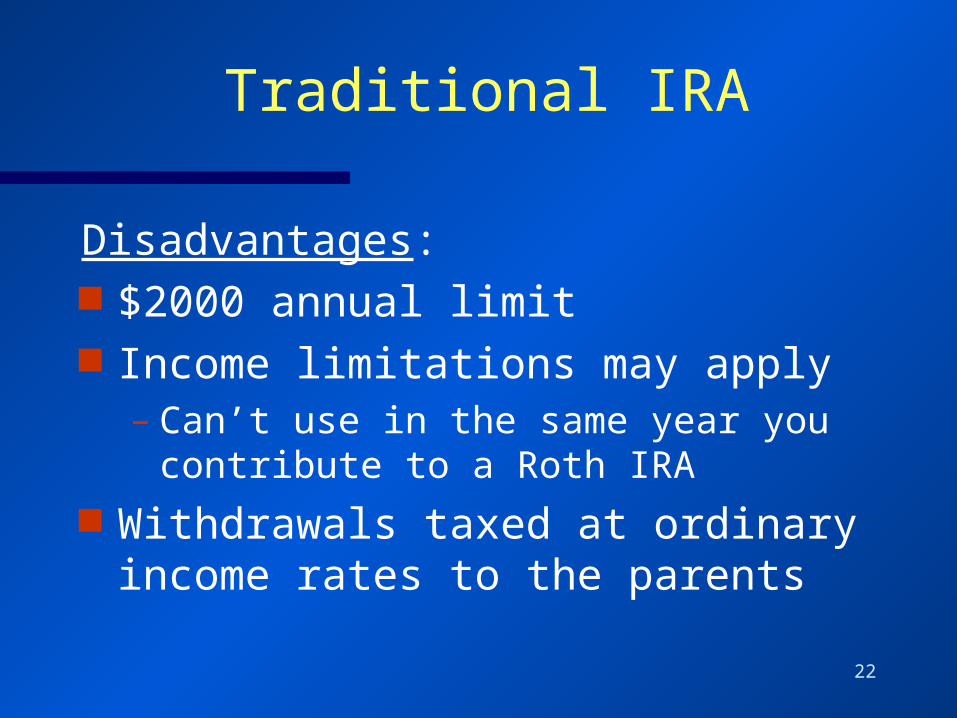

Traditional IRA

Advantages: Both deductible and non-deductible

IRA’s allow money to grow tax deferred IRA withdrawals prior to age 59½ are

penalty-free if used for qualified educational expenses

Funds remain in parental control IRA savings are typically exempt when

determining eligibility for financial aid

22

Traditional IRA

Disadvantages: $2000 annual limit Income limitations may apply

– Can’t use in the same year you contribute to a Roth IRA

Withdrawals taxed at ordinary income rates to the parents

23

Roth IRA

Advantages: Money grows tax free Withdrawals prior to age 59½ are

penalty-free if used for qualified educational expenses– Account established for 5 years

Funds remain in parental control Roth IRA savings are exempt when

determining eligibility for financial aid

24

Roth IRA

Disadvantages: $2000 annual limit Income limitations apply for

making contributions– Can’t use in the same year you

contribute to a traditional IRA

25

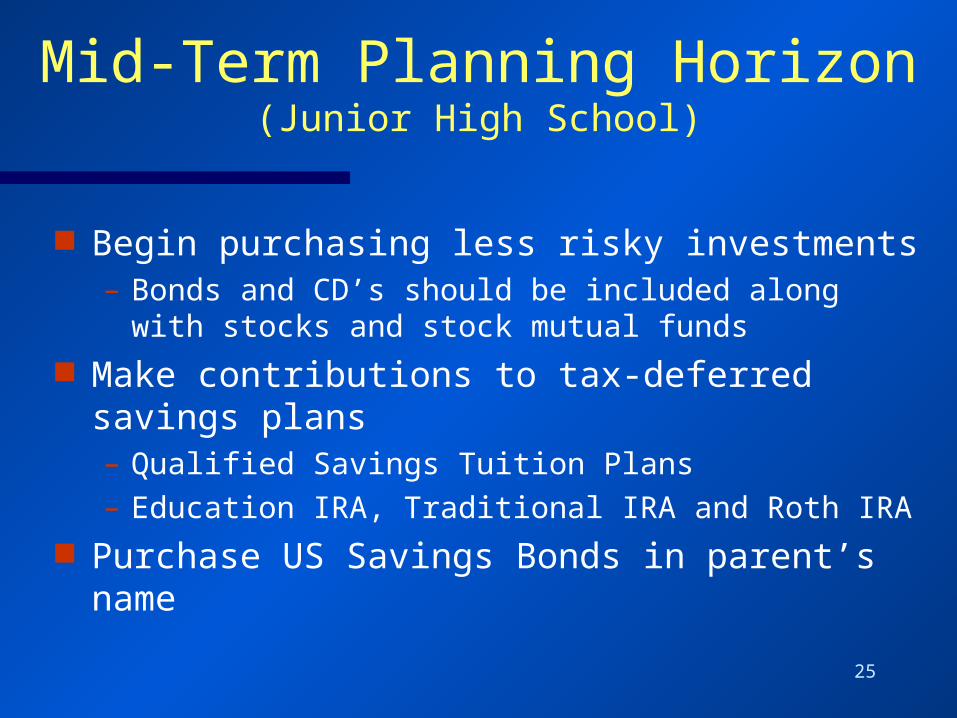

Mid-Term Planning Horizon(Junior High School)

Begin purchasing less risky investments– Bonds and CD’s should be included along with

stocks and stock mutual funds Make contributions to tax-deferred savings

plans– Qualified Savings Tuition Plans– Education IRA, Traditional IRA and Roth IRA

Purchase US Savings Bonds in parent’s name

26

Short-Term Planning Horizon(High School)

Evaluate likelihood of receiving financial aid

If financial aid is unlikely, begin to transfer assets from parent’s name into child’s name using a custodial account (UTMA/UGMA account)

27

Short-Term Planning Horizon(High School)

Calculate the cost of college and incidental expenses

Planning horizon less than five years Invest in low risk fixed income

investments such as CD’s, zero coupon bonds with maturities set for a specific college year, and money market funds

28

Short-Term Planning Horizon(High School)

Shift higher risk investments into lower risk investments

Continue contributions to tax-deferred savings plans– Qualified Savings Tuition Plans– Education IRA, Traditional IRA and

Roth IRA

29

Short-Term Planning Horizon(College)

Evaluate different loan options Use Hope Credit and Lifetime

Learning Credit

30

“Financially Manageable”During And AFTER

The College Years

PARENTPARENT STUDENTSTUDENT

Will not jeopardize Financial Security Comfortable

Retirement Educating other

children Other financial goals

Will not leave excessive debt

Will not jeopardize financial independence after graduation

Estimate the ‘Total’

Cost of Education4+ years of expenses

Estimate the ‘Total’

Cost of Education4+ years of expenses

Look at your entireFinancial Situation

Look at your entireFinancial Situation

Make financial decisions that :

31

Understanding Cost and

Expected Family Contribution (EFC)

32

Tuition

Fees

Room and Board

Books and Supplies

Transportation

Other Costs

How Much Will College REALLY Cost?

33

Cost Case Study

Meet Maria Martinez– good student, highly ranked tennis player– plans to major in biology and pursue pre-med– lives with parents– mother is dentist, father real estate broker– two children, including Maria and a brother in

junior college– parents are homeowners

34

Maria Martinez’s Cost

Public Univ (2 yr commuter)

Private Univ Public Univ (4 yr resident)

Tuition/Fees $1,425 $17,000 $12,725

Room/Board $2,350 $6,475 $5,575

Books/Supplies $1,000 $1,100 $1,000

Personal Exp. $1,350 $1,150 $1,075

Transportation $1,075 $625 $750

Total Cost $7,200 $26,350 $21,125

35

How Much Will We Be Expected To Pay?

Expected Family Contribution

Federal Methodology

Institutional Methodology

36

Need Analysis

A process of determining a student’s financial need by analyzing information provided by the student and the parent on a financial aid form.

Need analysis forms include the FAFSA and the CSS/Financial Aid PROFILE.

Cost of Attendance (COA) - Expected Family Contribution (EFC)

= Student’s Financial Need (eligibility for aid)

37

Financial Aid Application Process (All Schools)

Free Application for Federal Student Aid Required for federal and state aid Deadlines vary from school to school,

earliest date is January 1st Several filing methods

– Paper (guidance and financial aid office)– FAFSA on the Web (www.fafsa.ed.gov)

38

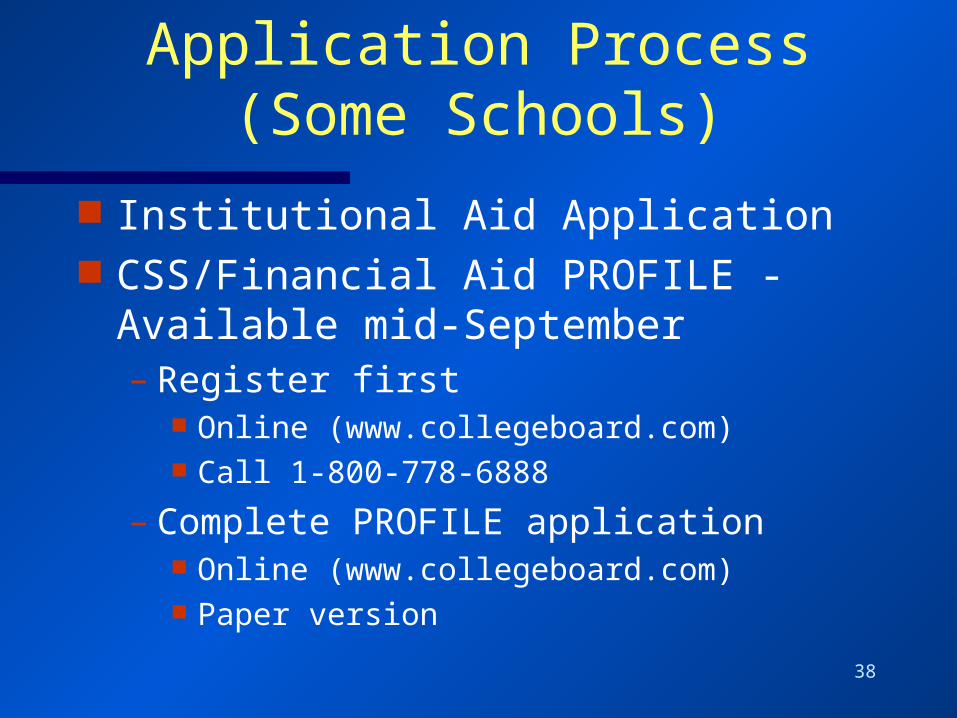

Financial Aid Application Process (Some Schools)

Institutional Aid Application CSS/Financial Aid PROFILE -

Available mid-September– Register first

Online (www.collegeboard.com) Call 1-800-778-6888

– Complete PROFILE application Online (www.collegeboard.com) Paper version

39

Determining EFC

Parents’ Contribution– Income and Assets– More than one child in college– Divorced parents (IM)– Private elementary or secondary schools (IM)– Unusually high medical expenses(IM)

Student’s Contribution– Income and Assets– Independent or Dependent

40

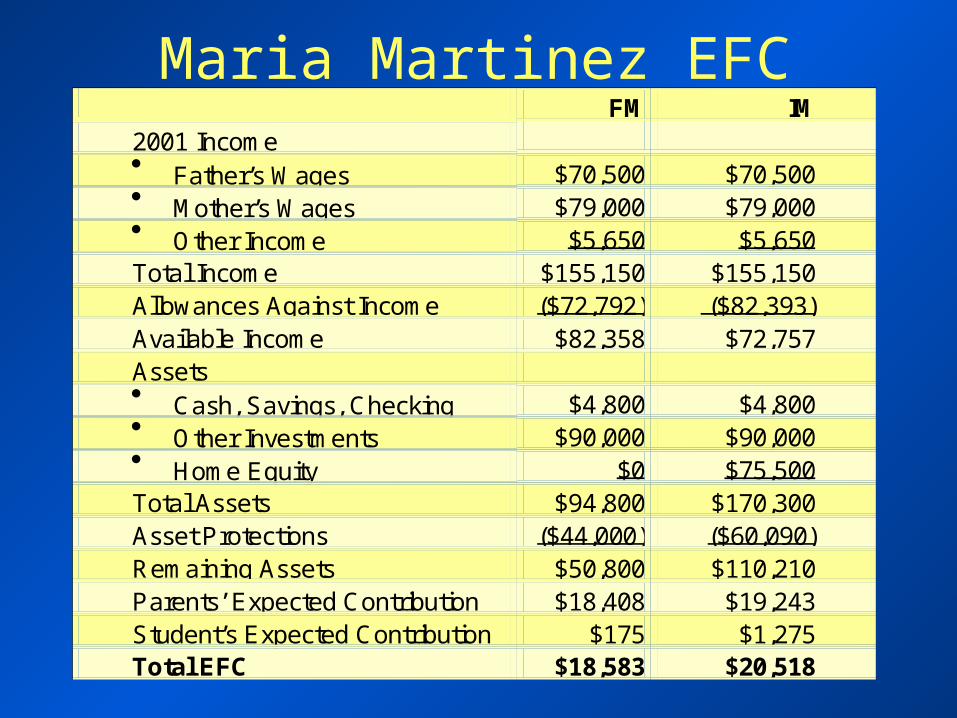

Maria Martinez EFC Case Study

Applying to both an IM and FM school Father earned $70,500 Mother earned $79,000 Both parents, 50 years old Parents earned $5,650 in interest on

investments Total family income $155,150 Maria earned $600 in wages and $30 in

investments; has $500 in savings FM SC is $175 IM SC is $1,275

41

EFC Case Study

Maria Martinez– IM provides allowance for medical expenses– IM protects a portion of assets for other

children’s college expenses– FM protects a portion of assets for

retirement– IM considers home equity of $75,500 (not

FM)– Sibling attending college taken into account

Maria Martinez EFC FM IM 2001 Income Father’s Wages $70,500 $70,500 Mother’s Wages $79,000 $79,000 Other Income $5,650 $5,650 Total Income $155,150 $155,150 Allowances Against Income ($72,792) ($82,393) Available Income $82,358 $72,757 Assets Cash, Savings, Checking $4,800 $4,800 Other Investments $90,000 $90,000 Home Equity $0 $75,500 Total Assets $94,800 $170,300 Asset Protections ($44,000) ($60,090) Remaining Assets $50,800 $110,210 Parents’ Expected Contribution $18,408 $19,243 Student’s Expected Contribution $175 $1,275 Total EFC $18,583 $20,518

43

Understanding Your Award

44

Award Package

Total amount of financial aid that the school is offering.

Scholarships - does not have to be repaid

Gift Aid - does not have to be repaid Work-Study - school affiliated

employment Loans - must be repaid

45

What Does the Award Package Really Mean?

Factors to consider in comparing offers– Grant aid vs. loan aid– Terms of loans– Unmet need– Aid renewal

Comparing Financial Aid Packages– www.collegeboard.com

46

Scholarships

47

Where are the Scholarships?

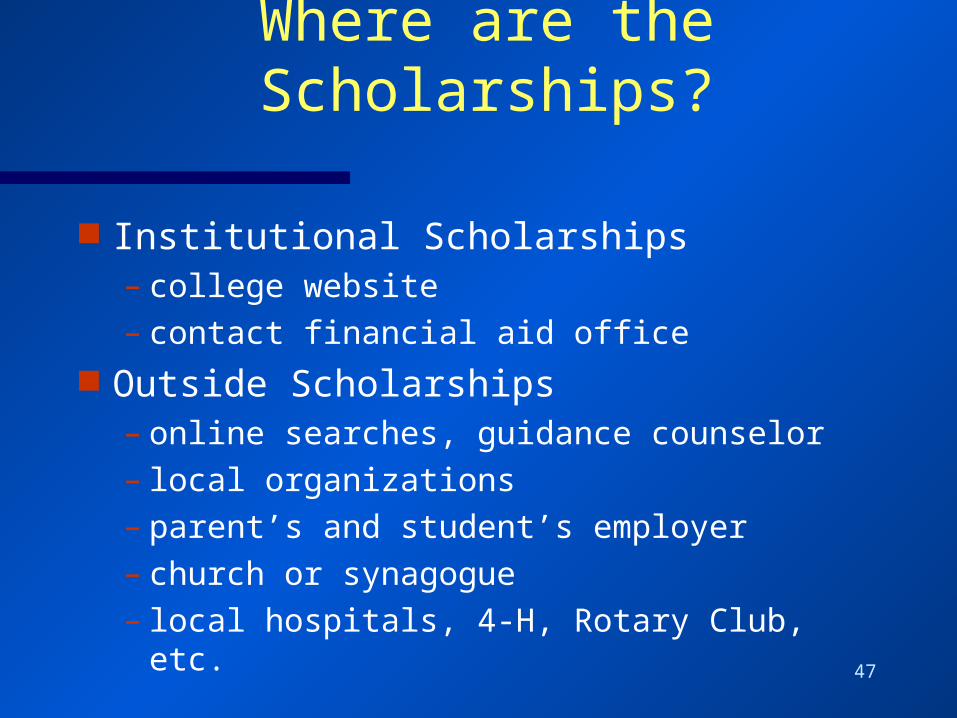

Institutional Scholarships– college website– contact financial aid office

Outside Scholarships– online searches, guidance counselor– local organizations– parent’s and student’s employer– church or synagogue– local hospitals, 4-H, Rotary Club, etc.

48

Scholarship Tips

Apply early Take your time on application and

essays, get a teacher or parent to critique

Find out college policy on handling outside scholarships

49

Scholarship Scams

Look out for the scams! Application fee Guaranteed winning Everyone is eligible We apply on your behalf Claim high success rate Request for credit card, bank account

50

Need-based Aid

Federal Pell Grant Federal Supplemental Educational

Opportunity Grant Federal Work-Study Federal Perkins Loan Subsidized Federal Stafford Loan

51

Financial Aid for No-Need Students

Unsubsidized Federal Stafford Loan Interest not subsidized by government Low interest rate, payments deferred in

school 3% origination fee, up to 1% insurance fee Annual loan limits

– $2,625 (1st year)– $3,500 (2nd year)– $5,500 (remaining undergraduate years)– $8,500 (each year in graduate study)

52

Financial Aid for No-Need Students

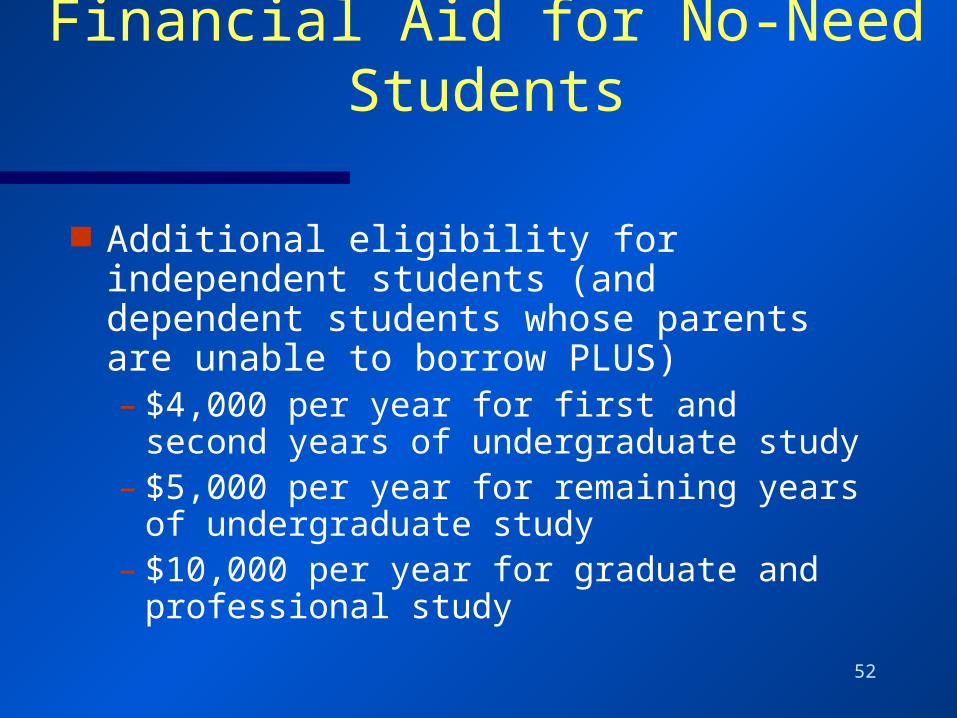

Additional eligibility for independent students (and dependent students whose parents are unable to borrow PLUS)– $4,000 per year for first and second

years of undergraduate study– $5,000 per year for remaining years

of undergraduate study– $10,000 per year for graduate and

professional study

53

Maria Martinez’s Awards

Public Univ (2 yr commuter)

Private Univ Public Univ (4 yr resident)

Cost of Attendance

$7,200 $26,350 $21,125

Less

EFC $18,583

(FM) $20,518

(IM) $18,583

(FM)

Equals

Eligibility (Financial Need)

$0 $5,832 $2,542

Maria Martinez’s Awards Public Univ

(2 yr commuter) Private Univ Public Univ

(4 yr resident) Eligibility (Financial Need)

0 $5,832 $2,542

Outside Scholarship

$1,000 $1,000 $1,000

Financial Aid Package

Pell Grant - - -

State Grant - - - Institutional Grant

- $1,000 -

Perkins Loan - - -

Sub Stafford - $2,625 $1,542

Unsub Stafford $2,625 - $1,083

Work Study - $1,200 - Total Assistance

$3,625 $5,825 $3,625

55

Financial Aid Award

Avoid comparing the aid award of your child

with what the student down the street received. Even though the parents are in the same income bracket, too many other factors may well have been involved.

TIP

56

Financial Aid Options: When the Award Package is Not

Enough

57

PLUS Loans

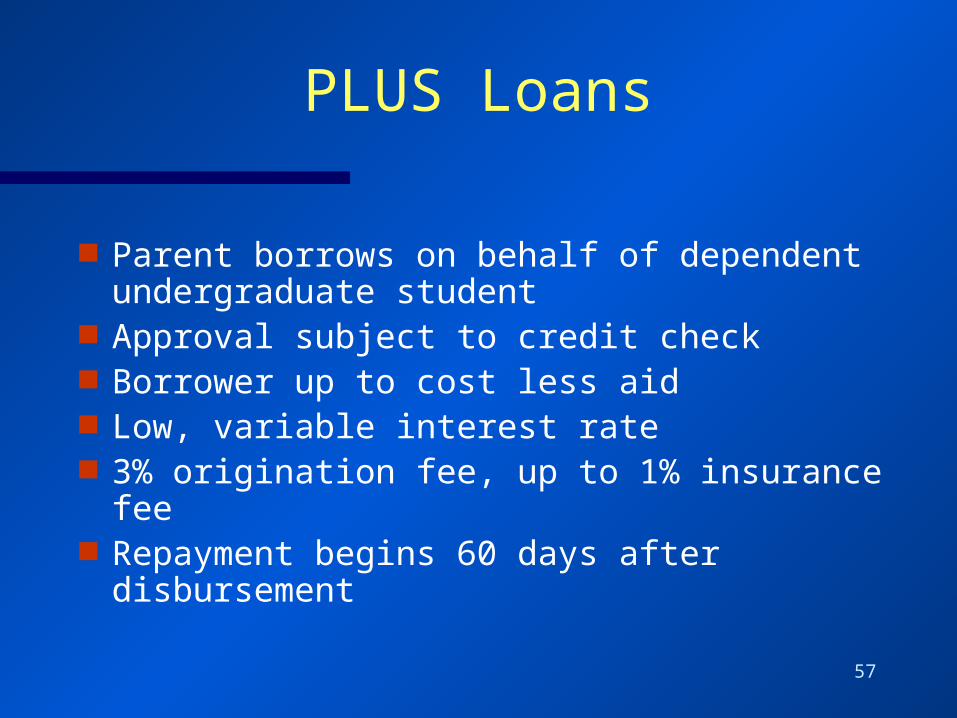

Parent borrows on behalf of dependent undergraduate student

Approval subject to credit check Borrower up to cost less aid Low, variable interest rate 3% origination fee, up to 1% insurance fee Repayment begins 60 days after

disbursement

58

Private Loan Programs

Private Loan Programs Only recommended after federal

programs considered Cosigner may be required, credit

check required Compare fees, rates, and benefits Contact financial aid office for

recommendations

59

Financing Alternatives

Institutional Payment Plans Whole Life Insurance Policies Home Equity Loans Employer Benefits Retirement Plans Margin Loans against Investment

Portfolio

60

What to Consider in Comparing Options

Interest rate Evaluate true cost of loan including

loss of investment return Tax deductibility Repayment terms

61

Tax Benefits

62

Lifetime Learning Credit

Annual limit up to $1,000 per family (goes up to $2,000 in 2003)

Income phase out– $40,000 to $50,000 (Single)– $80,000 to $100,000 (Joint)

Qualifying expenses– Tuition and enrollment fees

What education qualifies– All undergraduate and graduate programs

Can be used for education to acquire and improve job skills

63

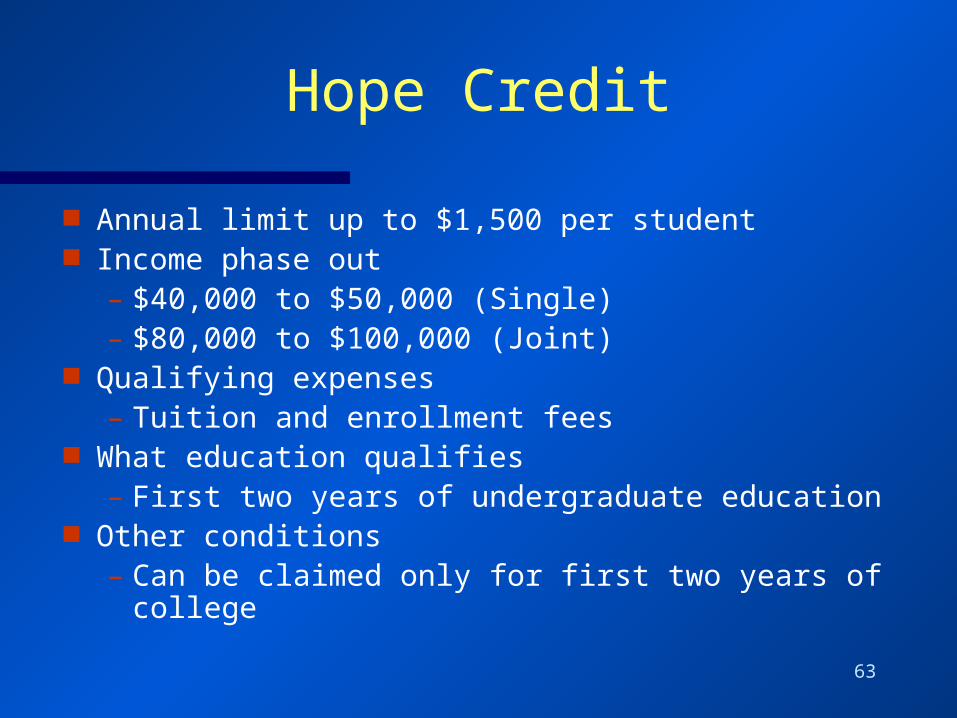

Hope Credit

Annual limit up to $1,500 per student Income phase out

– $40,000 to $50,000 (Single)– $80,000 to $100,000 (Joint)

Qualifying expenses– Tuition and enrollment fees

What education qualifies– First two years of undergraduate education

Other conditions– Can be claimed only for first two years of college

64

Deduction for Education

Tax deduction for qualified higher education expenses (same as HOPE definition)

Maximum deduction of $3,000 in 2002 Can’t be claimed in same year as HOPE

or Lifetime Learning for same student Income limits apply ($65,000/$130,000)

65

Additional Information

66

Website Resources

College Searchwww.collegeboard.comwww.wiredscholar.com

Scholarship Searchwww.collegeboard.com www.fastweb.comwww.usnews.com

Paying for College www.collegeispossible.org/paying/paying.htmwww.wiredscholar.com

67

Website Resources

Overview of Financial Aidwww.finaid.org

FAFSA on the Webwww.fafsa.ed.gov

Help in Completing the FAFSA www.ed.gov/prog_info/SFA/FAFSA

The Student Guidewww.ed.gov/prog_info/SFA/StudentGuide