payment trends in the european retail sector - aci...

TRANSCRIPT

SPONSORED BY

Payment trends in the European retail sector

Edgar, Dunn & Company Fifth Annual Retailer Survey

February 2017

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page i

Contents

1 Foreword – ACI Worldwide ............................................................................................. 1

2 Executive summary ......................................................................................................... 2 2.1 Introduction ........................................................................................................ 2 2.2 Methodology ...................................................................................................... 2 2.3 Key findings ......................................................................................................... 3

3 Omnichannel is here to stay ........................................................................................... 4 3.1 Defining Omnichannel ........................................................................................ 5 3.2 Benefits of an Omnichannel strategy ............................................................... 6 3.3 Facing the Omnichannel Challenge ................................................................... 7

4 Payment mix is at the heart of an Omnichannel strategy ............................................ 9 4.1 Payments are key to linking different sales channels ..................................... 10 4.2 Counting the costs of an Omnichannel payment strategy .............................. 11 4.3 Issuing new payments products ...................................................................... 12 4.4 Technology is changing retail ........................................................................... 13

5 The evolving customer experience ............................................................................... 15 5.1 Seamless cross-‐channel interaction ................................................................. 15 5.2 Immediate Payments ........................................................................................ 16 5.3 In-‐app payments, in-‐store ................................................................................ 16 5.4 Shaping the future of retail .............................................................................. 17

6 Where should retailers start? ........................................................................................ 18

Figures

FIGURE 1: CHANNELS USED BY RESPONDENTS ............................................................................................... 4 FIGURE 2: RETAILERS WHO HAVE STARTED TO DEVELOP THEIR OMNICHANNEL STRATEGIES ................................. 5 FIGURE 3: WHICH BUSINESS DRIVERS WOULD INFLUENCE YOUR CHOICE OF ACCEPTING NEW PAYMENT METHODS? . 9 FIGURE 4: KEY CHALLENGES IN ACCEPTING PAYMENTS ................................................................................... 11 FIGURE 5: WOULD YOU CONSIDER USING THIRD-‐PARTY PROVIDERS? ............................................................... 13 FIGURE 6: WHICH RETAIL TECHNOLOGIES ARE RETAILERS ALREADY TAKING ADVANTAGE OF? .............................. 14 FIGURE 7: WHICH OF THE FOLLOWING WILL HAVE THE GREATEST IMPACT ON THE RETAIL INDUSTRY OVER THE NEXT 2

– 3 YEARS? ...................................................................................................................................... 15

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 1

1 Foreword – ACI Worldwide

We are pleased to be sponsors of this survey addressing, as it does, some of the key payments-‐related issues facing retailers today. The findings clearly indicate the challenges faced by those seeking to develop a long-‐term retail strategy in a fast-‐changing, highly competitive environment – but they also reveal widespread agreement on the importance of payments as part of that strategy. The payments strategy is crucial, and a payments process that links channels across all payment methods is fundamental to the delivery of the seamless customer experience to which today’s retailers aspire.

It is clear that respondents to this survey have an appetite for new technologies that will help them to deliver a high quality, differentiated service to their customers. At the same time, they are very mindful of the continuing need to improve productivity and hold down costs. Given the pace of change -‐ and the wealth of new technologies, apps and payment methods available or on the horizon -‐ perhaps the overriding requirement is for retailers to secure payments capabilities that keep their options open. Flexibility, control, scalability and vendor independence should be key features of the payments infrastructure, positioning retailers to manage costs now and into the future as they take advantage of new opportunities to engage with and delight their customers.

Andrew Quartermaine, VP SaaS Solutions, ACI Worldwide – www.aciworldwide.com

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 2

2 Executive summary

2.1 Introduction This is the fifth annual EDC retailer survey and payments continue to be a hot topic for retailers, both online and offline at the point of sale.

One of the oldest mottos in retail is that the customer comes first. This isn’t in any way a new concept and yet one of the biggest challenges in today’s retail environment is meeting the increasingly sophisticated demands of customers. Retailers know all too well that consumers today have greater expectations than ever before and it is simply no longer enough to provide good customer service, it needs to stand out.

Today’s customer is well informed, technologically adept and wants to shop on their own terms. These connected consumers are assimilating multiple sources for product information, from in-‐store displays to social media, engaging across channels to shop at their own convenience. Retailers are adapting to meet these evolving consumer preferences and to deliver seamless customer experiences.

Technology will be at the heart of the retail strategy – facilitating enhanced customer support, visibility of inventory and delivering on the complex cross-‐channel fulfilment situations that are arising. Alongside this, developments in customer experience will drive innovation in the industry with seamless customer journeys, immediate payments and in-‐app purchases and connected commerce regardless of the sales channel.

Change in the way consumers pay for goods and services will be fast. Consumers are responding positively to technological innovation and many retailers are finding it challenging to respond to this changing behaviour. It has become meaningless to talk about online and offline as two separate channels. This will have a profound impact on consumers’ lives and habits, with massive implications on our shopping behaviour, which increasingly depends on having access to new technologies.

2.2 Methodology We approached more than 400 contacts across Europe and with a focus on the three largest retailing markets (UK, France, and Germany) to complete an online survey between November 2016 and early January 2017. The findings described in this paper provide a representative sample of multichannel1 retailers and the opinions of experts within the industry whose jobs depend on the efficient processing of consumer payments in the retail sector.

The objective of this paper is to gain a better understanding of merchant needs and how payment-‐related changes could affect the way multichannel retailers are doing business. It looks at how retailers are creating opportunities to increase sales, enhance

1 Multichannel refers to merchants selling their goods and service across more than one sale channel. Omnichannel is described later

Today consumers expect and demand seamless customer experiences across all channels

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 3

the customer experience and optimise payments. Several additional qualitative interviews were conducted with leading retailers and this report offers additional in-‐depth analysis and insight.

2.3 Key findings In our fifth annual survey, EDC has found some interesting differences of opinions and a shift in the survey results that are indicative of the direction that retailers are moving and focusing their attention in the next few years. The findings suggest that many multichannel retailers are continuing to focus on payments to reduce costs, improve customer service and differentiate their service in a highly competitive market. The key findings of this survey can be grouped under the following captions:

¡ Omnichannel is here to stay

¡ The payment mix is at the heart of an integrated Omnichannel strategy

¡ Customer experiences and journeys continue to evolve

This year the survey has shown that retailers are busy integrating new technologies into their front-‐office (i.e. shop floor) and their back-‐office retail strategy and are anticipating new trends impacting the evolving retail customer experience.

The payments piece for any retailer must be strategic, supported at board level, cover the issuing of payment methods, payment acceptance and payment processing, and be incorporated into an Omnichannel strategy.

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 4

3 Omnichannel is here to stay

Omnichannel shoppers are here. Today, consumers have access to a vast array of options when it comes to researching and purchasing a product. Consumers can and will use all types of device to complete orders anytime, anywhere. Retail success hinges upon connecting to these customers, which means reaching consumers wherever they are, on whatever device or point of interaction they choose to use.

Our respondents are recognising this need to operate and connect multiple channels. There is an increasing trend towards digital channels, with the proportion of respondents with internet (87%), mobile app (39%) and mobile website (59%) channels all increasing. This year, we did notice a reduction in respondents offering a physical brick and mortar channel, however, this was driven primarily from an increase in digital only participants.

Figure 1: Channels used by respondents

As Omnichannel shopping behaviour continues to impact the customer journey, retailers who operate multiple channels are having to respond. Adapting to the expectations of their Omnichannel consumers and what their behaviour means for the retail business has become vital. A growing proportion of shoppers happily jump between online, mobile and physical touchpoints, in journeys that could see them finding a product on social media, researching online reviews and reserving a product for in-‐store collection. In this evolving retail reality, there is a need to re-‐engineer retail strategies to offer a seamless customer experience to shoppers, regardless of their journey.

Alongside this, there is a growing recognition that shoppers buying across multiple channels have become the most valuable type of customer. In the UK, John Lewis has found that Omnichannel shoppers spend, on average, three times more than single channel shoppers.

77% 80%

37%31%

14%

43%

26%

3%

56%

87%

39%

59%

13%

44%

26%

15%

Brick and mortar shops

Internet Mobile app Mobile website

Kiosk Phone order Mail order Other

2013

2016

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 5

3.1 Defining Omnichannel Omnichannel has become synonymous with both the evolution of the retail experience and changing consumer behaviour. It’s hard to read an article or attend a conference on retail without seeing it but at the same time is has no single agreed definition.

What is Omnichannel?

Google defines it as: “ensuring marketing strategies are geared toward enabling customers to convert on any channel”

HubSpot defines it as: “a multichannel sales approach that provides the customer with an integrated shopping experience”

We asked our retailers how they would best describe their view of Omnichannel retail strategy. The following statements were presented to respondents:

¡ An integrated marketing strategy

¡ Bringing together both business processes and technology systems

¡ Maximise revenue

¡ Consolidate purchasing data to form a single customer database

¡ Increase efficiency and reduce costs across channels

Unsurprisingly, opinion varied widely. However, in contrast to last year’s results, the most commonly picked definition was “bringing together both business processes and technology systems” at 33% up from 12% in 2015. Last year’s respondents favoured maximising revenue (at 51%), which fell to 18% in 2016. This perhaps reflects a wider recognition of the technical and business challenges of successfully implementing an Omnichannel retailing strategy.

EDC also asked retailers to indicate the status of their Omnichannel strategy. 31% of respondents indicated that they had already put their strategy live and a further 46% have their strategy in development.

Figure 2: Retailers who have started to develop their Omnichannel strategies

31%

46%

18%

5%

Operational

In Development

Planned (Within 2 Years)

N/A

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 6

Omnichannel puts the consumer at the core of the retail strategy. The goal of an Omnichannel strategy is delivery of seamless and consistent retail experiences to the customer to better engage and convert them. Achieving this comes with both significant benefits and challenges.

EDC Perspective: Retailers are coming to grips with the reality that Omnichannel is a necessary part of their strategy and are recognising the challenges

3.2 Benefits of an Omnichannel strategy While retailers are having to adjust to the evolving consumer, success in delivering a seamless retail experience will undoubtedly deliver benefits, including:

¡ Increase sales

¡ Provide competitive advantage

¡ Access new customer segments

¡ Improve operational efficiency

¡ Improve loyalty

¡ Improve shopping experience

¡ Improve customer satisfaction

¡ Create a single brand identity

¡ Optimise payments acceptance

We asked our respondents which benefits they considered the most valuable. Respondents indicated that improving the customer shopping experience (83% important/very important) and improving customer satisfaction (81% important/very important) were the two greatest factors. Following this, creating a single brand identity (78%) and increasing sales (77%) also emerged very strongly.

Case Study: Argos has become a best practice example for Click&Collect, offering immediate availability of online and in-‐app orders for collection. Alongside this, since acquiring Home Retail Group in 2016, Sainsbury’s is rolling out Argos Click&Collect service points within their grocery stores

Improved customer experiences and satisfaction

The retail industry is experiencing a huge shift in consumer awareness – the new breed of shoppers that are always connected, informed and therefore empowered. They expect instant, relevant and up-‐to-‐date information. The traditional multiple channel approach to serving the customer falls apart in the face of these demands. Omnichannel strategies give retailers the opportunity to interact with their customers in new and innovative ways and thus address increasingly high consumer expectations.

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 7

Increasing sales

Retailers who have better visibility of their customer and who provide the experiences shoppers now look for will have a better opportunity to complete a sale. Omnichannel shoppers make purchases wherever and whenever they please, providing this convenience to customers substantially increases the buying opportunities they have.

Brand Identity

An Omnichannel strategy allows for seamless and consistent brand communication. When a brand is present across all channels, online and offline, shoppers will experience a brand, not a sale channel. Customers who engage with a brand in multiple areas have more opportunity to purchase.

EDC perspective: Using various devices and readily accessing a wealth of information, today’s consumer is becoming more complex to understand. Retailers should turn this into an advantage through a tailored retail strategy that delivers the personal retail experience that customers now seek.

3.3 Facing the Omnichannel Challenge Developing a long-‐term retail strategy is often viewed as a challenge by many retailers, especially considering the rapid pace of change experienced in the industry. Customer buying preferences and behaviour are evolving on a constant basis, while the sheer scale of integrating multiple channels, often across different countries and brands becomes very difficult to manage.

In this year’s survey, we asked our retailers to identify some of the key challenges they face while pursuing truly integrated retail strategies. Data integration emerged as the greatest challenge our respondents face when implementing an Omnichannel strategy, with 69% of respondents rating this high / very high. Understanding Omnichannel shoppers starts with data, enabling retailers to uniquely identify customers across channels, understanding their behaviour and preferences. The costs of implementing an Omnichannel strategy is also cited as a significant challenge for retailers.

Data integration

Customer transactions (both online and offline), conversations and intentions can all be brought together by retailers and used to both improve the retail shopping experience and maximise revenues. Collectively, this information is commonly referred to as 'Big Data'.

The issue lies in that Big Data refers to both structured and unstructured data:

Structured data -‐ refers to data easily captured in existing databases and may include transaction and conversion rates, amongst other statistical indicators

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 8

Unstructured data -‐ this is more fluid, being comprised primarily of social media interactions.

EDC customer experience indicates that unstructured data is currently less of a priority for retailers, who already face a significant challenge in making productive use of the sheer amount of structured data they collect. Going forward, integrating structured and unstructured data into a single database will be a key challenge, but will provide retailers with a wealth of actionable customer information.

Costs of Omnichannel Offering

With many retailers shifting their strategies to delivering a premium Omnichannel experience for their customers, the costs are beginning to show. As integration of channels continues to deliver consistent customer experiences, the cost of fulfilling these Omnichannel orders is rising. A recent survey by JDA showed two-‐thirds of retailers reported fulfilment costs growing as they focus on selling across channels. As attention focuses on same-‐day, next day delivery and click&collect, the costs associated are increasing:

¡ Handling returns from both online and in-‐store

¡ Shipping to stores for click&collect

¡ Purchases made online but returned in-‐store

¡ Shipping costs directly to customers

With costs rising, meeting the demand of Omnichannel consumers must be balanced with profitability. Alongside this, retailers need to deliver on multiple channels without compromising on brand promises and identity.

Working with a third-‐party fulfilment company may provide a logistics solution for the retailer, but it can be at a high cost to the customer experience. The retailer’s brand promise and identity may be diluted because customers become alienated or dissatisfied where they must deal with a third-‐party to resolve shipping exceptions, such as tracking a delivery, lost packages or returns.

EDC Perspective: Whilst there are no ‘one size fits all’ solutions to Omnichannel retailing, EDC believes that a more centralised, integrated organisational structure offers a more efficient approach when operating in multiple channels. If a retailer sells through multiple channels, but manages each one as a separate entity, it is likely to pose difficulties in creating a single brand identity, which is vital to securing customer loyalty. Nor will it facilitate the sharing of customer behaviour and preferences across channels, which is an integral part of delivering a compelling retail experience.

By 2018 ‘Click & Collect’ is expected to reach €20-‐25 billion in Europe

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 9

4 Payment mix is at the heart of an Omnichannel strategy

Retailers need to differentiate themselves in a highly competitive environment and the payment mix can become a significant differentiating factor as part of an Omnichannel strategy.

According to the survey, retailers acknowledge the significance of different forms of payment. When asked which business drivers influence their choice of new payment methods, respondents indicated a wide range of factors. Improving the consumers’ experience emerged overwhelmingly as the most imperative business driver with 78% of respondents citing this. Beyond this, improving operational efficiency (38%) and increasing sales in-‐store (38%) came through as important drivers.

Figure 3: Which business drivers would influence your choice of accepting new payment

methods?

New payment methods can unlock specific customer segments and generate additional sales. For instance, American Express, with its feature-‐rich programmes, tends to generate higher transaction value and PayPal provides access to a global customer base of more than 120 million PayPal accountholders. Appropriate payment methods need to be offered taking into consideration opportunities and restrictions relevant to each channel.

The ‘1-‐click ordering’ feature developed by Amazon is characteristic of a simple customer experience designed to encourage repeat sales and is positioned at the core of Amazon's payment checkout strategy. Retailers need to decide which payment methods to accept and which payment methods to issue.

EDC Perspective: This year EDC has found that retailers view the customer experience as critical to their payments strategy. This forms the primary driver influencing additional payment methods and alongside customer satisfaction is core to the Omnichannel experience

38%44%

78%

34% 34% 31%38%

Increase sales in-‐store

Target new customer

segments and geographies

Improve consumer experience

Improve loyalty

Decrease payment

acceptance costs

Decrease fraud

Add operational benefits

New payment methods can unlock specific customer segments and generate additional sales

Appropriate payment methods increase sales and improve customer experience

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 10

4.1 Payments are key to linking different sales channels Besides increasing sales and unlocking customer segments, payments can also play an even greater role and link different channels. The payment process needs to be consistent and support brand identity across all channels. Customers increasingly use a combination of channels (in-‐store, social media, computer, tablet, smartphone) to support their purchase decisions. According to one survey, 70% shopped virtually before buying in store while 68% browsed items in store before buying online.2

Case Study: In 2016 ASOS reported a 26% rise in retail sales, citing mobile as critical to this success. 66% of traffic was driven by mobile devices resulting in 51% of all orders being placed from mobile platforms. Alongside this mobile has been identified as driving increased customer engagement, from visits to basket size and order frequency

'Showrooming' is the practice of visiting a shop or shops to examine a product before buying it online at a lower price. Often feared by many retailers, in contrast, John Lewis (along with many others) has embraced showrooming and found that more than 60% of their customers researched products online before visiting a shop to make a purchase. In-‐store WiFi access at John Lewis allows them to continue and complete that journey, accessing product information and viewing ratings and reviews to influence their purchase. Similar research in other markets has indicated that customers are becoming channel agnostic, there is a constant blurring of the lines of distinction between in-‐store and online browsing, price comparing, reviewing, researching and buying.

A retailer's website has evolved beyond a 'simple' e-‐commerce channel for online sales to become a multichannel source of information. A retailer's website becomes a significant sales driver for in-‐store, online and mobile interactions and needs to assist customers at the three major points-‐of-‐interaction: in-‐store, on the go or at home. Similarly, mobile advertising appears to be growing at a phenomenal rate. If forecasts for 2016 are fulfilled, the $101.37 billion to be spent on ads served to mobile phones and tablets worldwide represent a nearly 430% increase from 2013.3 The UK, Germany, France and the Netherlands are all in the global top 10 for mobile internet ad spending between 2013-‐2018.

Retailers need to consider the whole payment process to generate synergies across channels. Design of the payment process should not only consider the last step in concluding the purchase transaction, but it should be viewed as playing a core role in a Omnichannel strategy, linking different channels across all payment methods and non-‐payment types of interaction between the customer and retailer.

Retailers using an Omnichannel strategy could identify customers based on the usage of payment methods and provide loyalty or marketing offers at the time of purchase. Retailers can also use electronic wallets to store customers' personal and payments information. Electronic wallets link online and mobile channels to provide a consistent customer experience, simplify payments and encourage repeat sales.

2 Global PwC 2015 Total Retail Survey 3 eMarketer, 2015

Retailers need to consider the whole shopping experience to generate synergies across channels

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 11

EDC Perspective: By considering the whole payment process and all the points-‐of-‐interaction, retailers can optimise both front and back-‐end payment processes. For instance, returns or refunds ought to be part of a holistic approach. Retailers would need to brush aside inconsistencies and focus on implementing consistent return and refund policies regardless of the channels used. This will contribute to providing a consistent customer experience and will strengthen customer loyalty.

4.2 Counting the costs of an Omnichannel payment strategy Respondents in this year's survey identified three standout challenges to accepting payments: managing fraud without impacting customers (59%), simplicity for consumers (56%) and the impact of payment fees (53%).

Figure 4: Key challenges in accepting payments

Omnichannel Fraud Management

With consumers engaging across multiple channels with an increasingly complex range of payment methods and devices, retailers are faced with added challenges, including a potentially heightened complexity of fraud management. The increased quantity of personal information shared with different entities across different channels makes customers apprehensive of potential data issues. Security breaches as evidenced in different cases in the US and Europe have become a significant issue and source of genuine concerns for retailers and customers.

Acceptance of mobile and other new forms of payments is expected to double in the next two years according to a recent global survey among IT security practitioners4, which means that retailers need to have mastered online security in existing payment methods. The results of the study show that security in online payments is a top concern but surprisingly most respondents felt that this has not been addressed as well as it should have been by their companies, which has resulted in data breaches in some cases.

We have found that with retailers aiming to ensure a seamless customer experience across channels, they should equally tackle fraud across all channels. They need a cross-‐

4 Ponemon Institute report on behalf of Gemalto, 2016

45%55%

42%

55%

18%

33%

12%

53%

41%

59% 56%

31%22%

28%

Payment fees Security & Compliance Managing fraud without impacting genuine customers

Delivering simplicity and speed for consumers

Financial data reconciliation

with bank’s clearing & settlement

Acceptance of alternative payments

at POS

Acceptance of alternative payments, online and via mobile

devices

2013

2016

The customer experience should be at the heart of the value proposition whilst ensuring a high level of security

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 12

channel view of their customer’s purchasing history, browsing history and preferred channel history -‐ in-‐store, on a smartphone, on a tablet, on a laptop, on a desktop, via an in-‐store kiosk -‐ to ensure that a customer is a good customer and not deviating from their normal channel behaviour.

Meeting this challenge and maintaining the level of experience that consumers have become accustomed to is proving difficult in the quickly changing environment of Omnichannel fraud.

Simplicity

On one hand, today’s consumer makes the most sophisticated demands ever faced by the industry -‐ on the other, there is an overwhelming desire for simplicity. With so many ways to interact consumers are faced with an overabundance of clutter. A move towards more personalised shopping experiences, with a focus on the information relevant to each consumer, will help relieve some of this pressure.

The reality is that retailers are having to implement new technologies, payment methods and strategies to delivery these increasing personal experiences while hiding the complexity of this from the consumer – a challenge to say the least. By reviewing processes, prioritising payment method offering and consolidating data, retailers can manage this complexity, both for the consumer and themselves.

4.3 Issuing new payments products Retailer payments have been relatively constant with cards, cash and cheques being dominant until the early 2000s. However, since then there has been a proliferation of new payment methods and the advent of online and mobile commerce has contributed to increased complexity in accepting payments.

The change in the payment landscape provides an opportunity for retailers to issue new payment instruments. Beyond loyalty cards, some retailers have issued store cards, co-‐branded cards or prepaid gift cards to issue their own payment instruments and strengthen the customer relationship.

Payments play a central role in the strategy of retailers to offer new points-‐of-‐interaction and strengthen customer loyalty. It is expected that new payments using recent technological developments (e.g. contactless for card payments, online or mobile channels for wallets) will become increasingly valuable for interacting directly with customers. The different functionalities of smartphones (e.g. internet, camera, in-‐app features) or the use of social media are very likely to create new use-‐cases and generate additional sales. For instance, push messages or location-‐based offers will create targeted incentives for customers and are likely to increase in-‐store or online conversion rates.

Non-‐payments activities will play a key role at the various points-‐of-‐interaction and will strengthen the customer loyalty via the smartphone

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 13

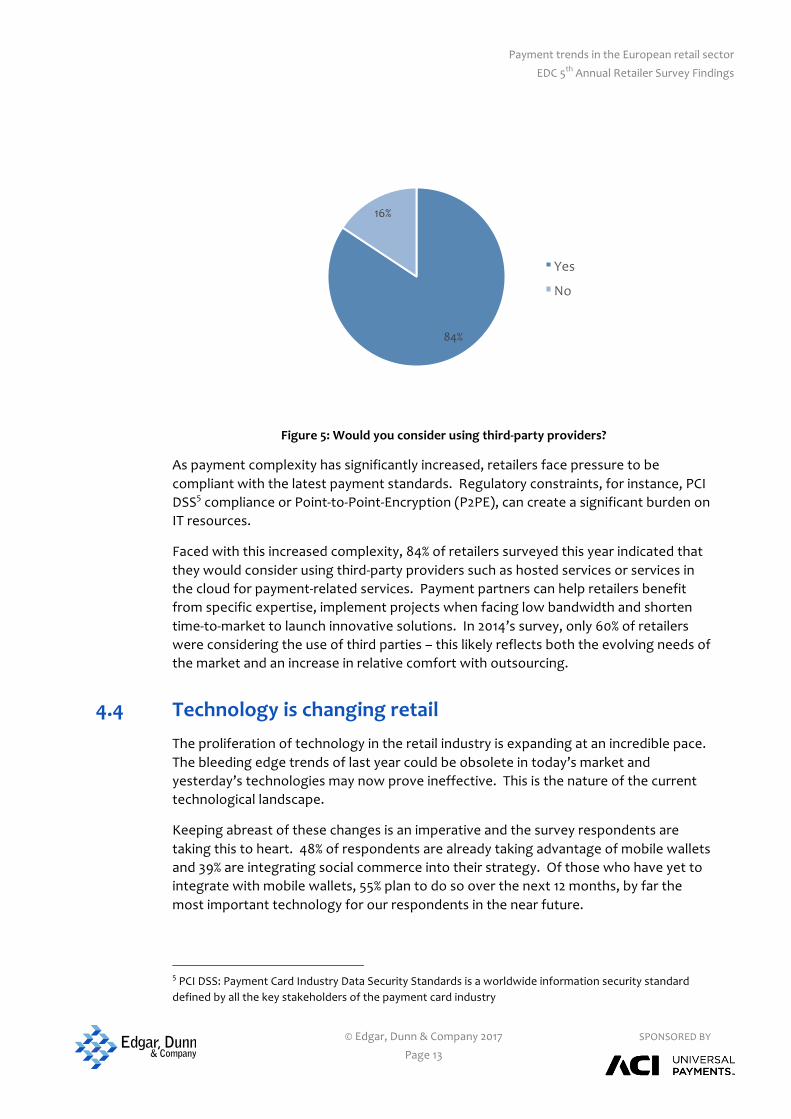

Figure 5: Would you consider using third-‐party providers?

As payment complexity has significantly increased, retailers face pressure to be compliant with the latest payment standards. Regulatory constraints, for instance, PCI DSS5 compliance or Point-‐to-‐Point-‐Encryption (P2PE), can create a significant burden on IT resources.

Faced with this increased complexity, 84% of retailers surveyed this year indicated that they would consider using third-‐party providers such as hosted services or services in the cloud for payment-‐related services. Payment partners can help retailers benefit from specific expertise, implement projects when facing low bandwidth and shorten time-‐to-‐market to launch innovative solutions. In 2014’s survey, only 60% of retailers were considering the use of third parties – this likely reflects both the evolving needs of the market and an increase in relative comfort with outsourcing.

4.4 Technology is changing retail The proliferation of technology in the retail industry is expanding at an incredible pace. The bleeding edge trends of last year could be obsolete in today’s market and yesterday’s technologies may now prove ineffective. This is the nature of the current technological landscape.

Keeping abreast of these changes is an imperative and the survey respondents are taking this to heart. 48% of respondents are already taking advantage of mobile wallets and 39% are integrating social commerce into their strategy. Of those who have yet to integrate with mobile wallets, 55% plan to do so over the next 12 months, by far the most important technology for our respondents in the near future.

5 PCI DSS: Payment Card Industry Data Security Standards is a worldwide information security standard defined by all the key stakeholders of the payment card industry

84%

16%

Yes

No

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 14

Figure 6: Which retail technologies are retailers already taking advantage of?

The shopping experience has undergone massive changes over the past two decades. e-‐Commerce has won over consumers and smartphones have become a must-‐have piece of technology. Retailers have undertaken a shift from paper to digital technologies while tech-‐savvy consumers demand more personalised and seamless shopping experiences, wherever and however they choose to shop.

e-‐Commerce has long been the focus of retail innovation, however, no matter how easy it has become to shop online, sometimes you want to visit an actual store. In-‐store experience matters and technology is providing new ways to improve it all the time.

Retailers can expect technology to shape the customer experience, in-‐store and online, for years to come and it should be considered an opportunity for incumbents and physical-‐only stores as much as purely tech-‐based retail companies. According to a recent survey conducted by Samsung among retailers, 94% of retailers believe the customer of the future will be driven by technology and 41% are already implementing it in their strategies to enhance the customer experience.6

Case Study: Following Amazon’s move into the world of physical bookstores in 2015, which has since expanded to 3 states (with plans for 4 more in 2017), Amazon is piloting AmazonGo a new bricks-‐and-‐mortar location designed to streamline the shopping experience with a controversial focus on using technology to remove human interaction

6 Samsung

48%

7%

39%

26%29%

Mobile wallets Beacons Social commerce Wearables Open APIs

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 15

5 The evolving customer experience

Change and transformation is no stranger to the retail industry. What began as a straight forward experience of visiting your local store has evolved into a myriad of vastly different experiences, including:

Shopping without ever leaving the house

Ordering online but collecting in-‐store

Shopping in-‐store without ever engaging with sales staff

These journeys are all unique and yet today’s customer expectations have come to include all these experiences. Technology has only encouraged this variety and retailers are having to adapt faster and more drastically than ever before.

Hovering over all of this is the pressure to integrate sales channels into a single, unified experience and it comes as no surprise that, of some of the trends impacting our respondents, ‘seamless cross-‐channel interaction’ was the most important factor with 79% of respondents indicating this would have great impact.

Figure 7: Which of the following will have the greatest impact on the retail industry over the

next 2 – 3 years?

Case Study: Last year, Visa Europe and Blippar demonstrated the world’s first augmented reality payment solution at the House of Holland’s London Fashion show. The consumer could use their smartphone to ‘view’ an item of clothing in the show and purchase on screen

5.1 Seamless cross-‐channel interaction Creating strategies to ensure a positive customer experience is not exactly a new idea. However, when you consider the multitude of shopping channels available and the evolving behaviour and preferences of today’s shoppers the goal shifts from merely

59%

79%

59%

28%

Immediate Payments Seamless Cross-‐Channel Interaction

In-‐App Payments, In-‐Store

Internet of Things & Connected Commerce

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 16

improving the customer experience to creating a single customer journey, regardless of sales channel. This has become vital to a successful retail strategy – a bad user experience in one channel may impact conversions in any other.

Our respondents cited “seamless cross-‐channel interaction” as most likely to have the greatest impact on the retail industry over the next 2 – 3 years (79%). While this recognises the importance of delivering these experiences it also suggests that retailers have yet to achieve this. A 2015 Economist Intelligence Unit study found that only 5% of executives surveyed could claim that they had deployed a seamless customer experience across channels.

Customer interaction and experience has become a key brand differentiator for all types of retailer and will form a crucial part of driving customer loyalty. Going forward, there cannot be a separate experience for different channels and delivering seamless, personalised and relevant experiences will be beneficial to both customers and retailers.

5.2 Immediate Payments Bank transfers are commonly accepted online, but in the physical store the retailer still does not have a proven solution.

A couple of years ago Euro Retail Payments Board (ERPB) invited the European Payments Council (EPC) to develop a pan-‐European instant payment scheme. The scheme will be based on the EPC’s current SEPA credit transfer (SCT) scheme and will be called ‘SCT Inst’, sometimes written as SCTinst. Don’t be fooled by the unimaginative name of the scheme, SCT Inst goes live 21st November 2017 for payment transactions in Euros.

Payment Service Providers are already preparing commercial solutions whereby merchants will be able to take advantage of the new SCT Inst payment scheme. By using immediate payments rather than traditional card payments, merchants will not only receive their funds faster, but the processing fees are expected to be less than a card payment. Both online retailers, as well as traditional bricks and mortar retailers, will benefit from these features.

Innovative payment solutions and potentially new overlay services are on the horizon because the underlying payment processing will be real-‐time. Call it instant or call it immediate, the genie is out of the bottle. Expectations are high and we have already started to see new overlay services, for example, Paym and Zapp in the UK, or Swish in Scandinavia. These new overlay services will build on the real-‐time payment infrastructures, as Zapp uses the UK’s Faster Payments Service.

5.3 In-‐app payments, in-‐store The concept of selecting the products you want in-‐store, paying and leaving without ever having to go to a checkout or POS system (as an extreme example) has become a

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 17

compelling idea for many consumers. The practicalities of this, from being able to identify what a customer has bought to the method of payment itself, have held this back from the mainstream, however, we are now seeing retailers taking on the challenge.

While not a direct comparison to a traditional retailer, Starbucks has been one of the few to successfully deliver this kind of experience. In 2015, Starbucks updated their app to allow customers to order and pay for items in advance, without waiting in line and paying at a POS.

Facilitating payment through an app under the retailer’s brand is a powerful tool and puts the retailer in competition with open-‐loop systems such as Apple Pay and Samsung. Walmart Pay, announced in December 2015, has now been rolled out in all 4,600 US stores and represents one of the first major retailers to offer a self-‐branded payment experience. For retailers without loyalty programmes these payment apps are a way to deepen information about shopper behaviour and facilitate improved shopping experiences.

AmazonGo has perhaps gone the furthest in trying to implement this idea, where a customer enters the store by scanning an app generated barcode, selects their items and leave the store. The system detects when products are taken from or returned to the shelves and keeps track in a virtual cart. The customer is then automatically charged when the leave the store.

These ideas all take elements of bringing the application experience in-‐store, despite the differences in implementation. The goal in each case is around creating better customer experiences, however, it does suggest that there can be no one size fits all approach and what works in one segment could be disastrous in another.

5.4 Shaping the future of retail These trends and technologies can certainly be described as taking us closer to a frictionless or seamless customer experience, however, it is imperative to remember that they should be adopted in pursuit of positive customer experience. Customer experience design must be customer centric and hence it must be human centric, and removing this element completely is still a largely untested concept.

Retailers are now placing greater emphasis on the customer experience, ‘CX’, in both their product/service design and business model. Instead of making heavy investments in advertising or the sales strategy, customer experience design (CXD) is where retailers are starting to differentiate and create relevance in a crowded marketplace.

Customer experience design pioneers include Nordstrom, Apple, Nespresso, Tesla, Warby Parker, Casper, John Lewis Partnership and other retailers who understand that a good customer experience design is how to engage with customers in a more meaningful way.

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 18

EDC perspective: For the next few years EDC believes that customer experience design (CXD) will be a top priority for Omnichannel retailers. By using digital transformation technologies to enhance the customer experience, such as augmented and virtual reality technologies, retailers will be able to give customers immersive experiences on the shop floor

6 Where should retailers start?

Payments-‐related initiatives for retailers have never been as important as they are in today's Omnichannel environment where the customers’ expectations are so high. To make a purchase via one channel and return through another channel; a seamless customer experience that provides continuity for both the customer and the retailer’s back-‐office processes will be a differentiated proposition in a highly competitive retailing environment. Payments-‐related initiatives have already taken priority for many of the larger retailers and there are best practices where further opportunities can be identified to generate additional sales, reduce costs and fraud, enhance profitability and improve the customer experience.

EDC would suggest first starting with a 360° Payments Diagnostic™. This proven procedure can reveal many opportunities to place payments at the heart of the design of a PCI compliant Omnichannel customer experience.

The payments strategy for many retailers has failed to provide the basis for a successful business. Ironically, this is because payments have not commonly been fully understood or made it onto the agenda for many retailers. Payment has been an afterthought. EDC has found that this has significantly changed in the last few years.

The EDC 360° Payments Diagnostic can be the starting point for the retailer to develop a sound payment strategy which will be future proof in the rapidly evolving world of payments. EDC experts in payments can build a payments strategy in collaboration that supports the retailer’s corporate and business strategy. Our global payment specialists have worked with many of the leading global retailer brands in the US, UK and Europe across all areas of the business.

A foundation for a robust payments strategy for the retailer will be a basis for good customer experience design within the context of a Omnichannel retailing operation.

The 360° Payments Diagnostic sets the basis for identifying and prioritising improvement initiatives

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

© Edgar, Dunn & Company 2017 SPONSORED BY

Page 19

If you are interested in discussing any of these payments-‐related topics, EDC will be pleased to set up an initial conversation to discuss in further detail the learnings from

this study and how you can optimise your payments strategy.

Contact

Mark Beresford, Head of the Retailer Payments Practice

t: +44 (0)7283 1114

m: +44 (0)7825 027525

Max Shinerock, Retailer Payments Practice

EDC's contact in North America: Peter Ehmke

EDC's contact in Asia Pacific: Peter Sidenius

EDC would like to thank all the retailers for their contribution to this year’s retailer survey, and the many organisations and individuals that provided information and

perspectives that collectively form the foundation for this report. A special thanks to ACI Worldwide for the company’s continued support and participation in this year’s

survey.

The observations and conclusions in this document are entirely those of EDC and are not intended in any way or form to reflect the views or perspectives of any

individual or retailer.

Copyright © 2017 Edgar, Dunn & Company

All rights reserved. Reproduction by any method or un-‐authorised circulation is strictly prohibited, and is a violation of international copyright law.

Payment trends in the European retail sector

EDC 5th Annual Retailer Survey Findings

Edgar, Dunn & Company (EDC) is an independent global financial services and payments consultancy. Founded in 1978, the firm is widely regarded as a trusted advisor to its clients, providing a full range of strategy consulting services, expertise and market insight.

From offices in Frankfurt, London, Paris, San Francisco, and Singapore, EDC delivers actionable strategies, measurable results and a unique global perspective for clients in more than 45 countries on six continents.

For more information contact: Mark Beresford Tel: +44 (0) 7283 1114 Email: [email protected]

www.edgardunn.com

Strategy Consultants Specialised in Payments