pcg company presentation - july 2011

TRANSCRIPT

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 1/30

0

Company Presentation

July 2011

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 2/30

1

Warranties and Exclusion of Liability

While care has been taken in ensuring the correctness of information, statements, text, articles, data, images and other materials contained andappearing in this presentation and the associated slides (hereinafter referred to as "the MATERIALS"), PETRONAS Chemicals Group Berhad(“PCG”), its subsidiaries and related corporations and its or their directors, officers, employees, agents and advisers (hereinafter referred to as "We")make no representations, guarantees or warranties as to the accuracy, reliability, quality, truth, suitability and completeness of the said MATERIALS.We reserve the right to add, delete or make any changes to the MATERIALS without prior notice.

We do not accept any liability for inaccuracies or omissions in the MATERIALS. We further disclaim all liabilities whatsoever for any direct, indirect,

special or consequential loss or damages howsoever resulting directly or indirectly from the access to or the use of this MATERIALS and the relianceon the MATERIALS contained herein. Any decisions made by you based on the MATERIALS are your sole responsibility.

The MATERIALS may also contain information provided by third parties and we make no representation or warranty regarding the said third parties'information.In no event would the MATERIALS constitute or be deemed to constitute an invitation to invest in PCG, its subsidiaries and related corporations or aninvitation by PCG, its subsidiaries and related corporations to enter into a contract with you.

Forward Looking Statements and Associated Risks

The MATERIALS and related discussions, including but not limited to those regarding the petrochemicals environment, anticipated demand forpetrochemicals, plant turnaround activity and costs, investments in safety and operational risk, increase in turnaround activity and impact onproduction, future capital expenditures in general, generation of future receivables, sales to customers, cash flows, costs, cost savings, debt, demand,disposals, dividends, earnings, efficiency, gearing, growth, strategy, trends, reserves and productivity together with statements that contain wordssuch as "believe", "plan", "expect" and "anticipate" and similar expressions thereof may constitute forward looking statements.

Such forward-looking statements are subject to certain risks and uncertainties, including but not limited to, the economic situation in Malaysia andcountries in which we transact business internationally, increases in regulatory burdens in Malaysia and such countries, changes in import control orimport duties, levies or taxes in international markets or in Malaysia, and changes in prices or demand for products produced by us, both in Malaysiaand in international markets, as a result of competitive actions or economic factors. Such forward looking statements are also subject to the risks ofincreased costs in related technologies and such technologies producing expected results, and performance by third parties in accordance with

contractual terms and specifications.

Should one or more of these uncertainties or risks, among others, materialize, actual results may vary materially from those estimated, anticipated orprojected. Specifically, but without limitation, capital costs could increase, projects could be delayed, and anticipated improvements in capacity orperformance may not be fully realised. Although We believe that the expectations of management as reflected by such forward looking statements arereasonable based on information currently available, no assurances can be given that such expectations will prove to have been correct. Accordingly,you are cautioned not to place undue reliance on the forward looking statements. We undertake no obligation to update or revise any of them, whetheras a result of new information, future events or otherwise.

This presentation and its contents are strictly confidential and must not be copied, reproduced, distributed, summarised, disclosed, referred or passedto others at any time without the prior written consent of PCG.

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 3/30

2

Table of Contents

Company Overview

1

Company Highlights

2

Financials

4

Key Strategies & Future Developments

3

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 4/30

3

Company Overview

Section 1

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 5/30

4

PCG at a glance – Leader in South East Asia

Key facts

One of the largest integrated petrochemicals producers in South East Asia

Production capacity of over 11m mtpa(1) across a wide range of petrochemicals

Established as part of the PETRONAS Group in 1985 to monetise Malaysia‟s natural gas

resources – over 4,000 employees

Highly integrated facilities, attractive feedstock supply and close to key markets of our Asiancustomer base

Productionfacilities

2 integrated petrochemical complexes (“IPCs”) focused on ethane and propane derived

products

3 additional manufacturing complexes focused on fertiliser and methanol production

Marine port facilities and access to Kuantan, Bintulu and Butterworth Ports

Joint ventures with leading industry players including BASF, BP and Sasol

Financialsummary

FY Mar 10 FY Mar 11

Revenue RM12.2bn (US$4.1bn) RM14.6bn (US$4.9bn)

EBITDA(2) RM3.8bn (US$1.3bn) RM4.7bn (US$1.6bn)

EBITDA margin 31.2% 32.1%

ROA(3) 19.3% 23.6%

ROE(4) 12.9% 15.2%

(1) Includes share of production capacities of associates and jointly controlled entities(2) Excludes interest income, share of associates and other exceptional items(3) ROA = NOPAT / fixed assets

© 2011 PETRONAS Chemicals Group Berhad

(4) ROE = net profit attributable to shareholders / shareholders‟ equity

Note: Exchange rate of US$1 = RM3.00 used throughout this presentation unless otherwise stated

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 6/30

5

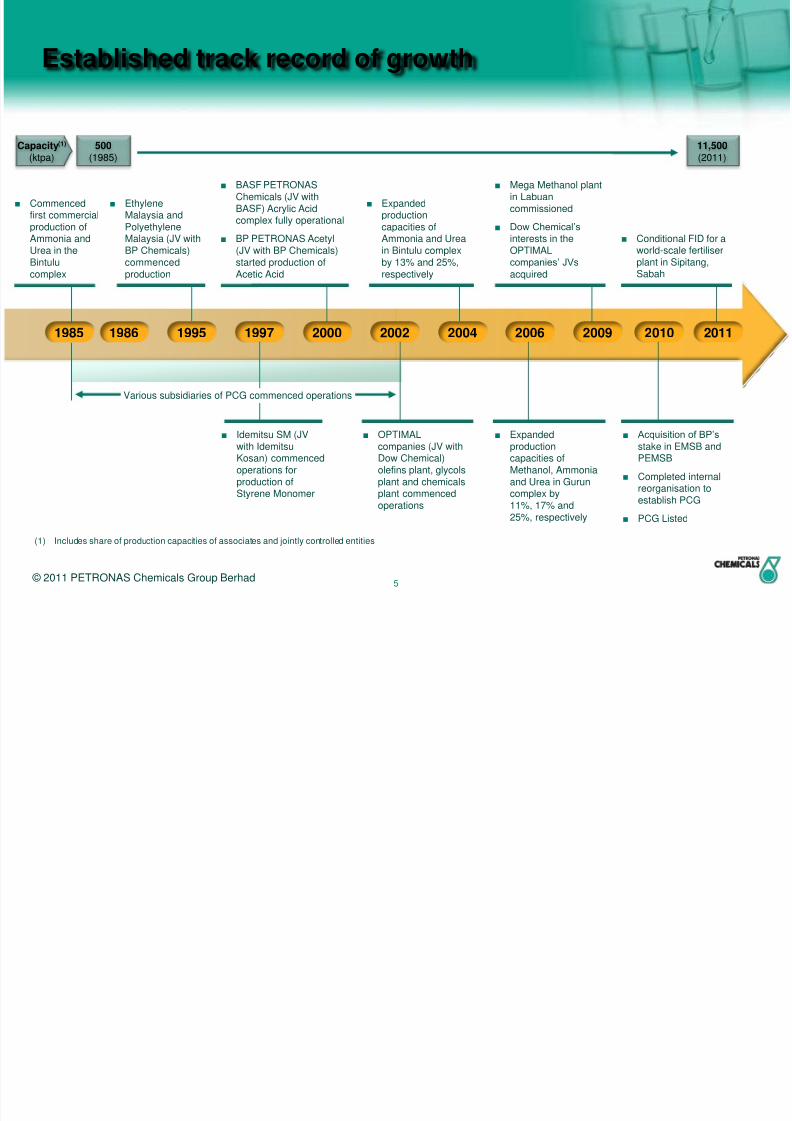

Established track record of growth

1985 1986 1995 1997 2000 2002 2004 2010

■ Commencedfirst commercialproduction ofAmmonia andUrea in theBintulu

complex

■ EthyleneMalaysia andPolyethyleneMalaysia (JV withBP Chemicals)commenced

production

■ BASF PETRONASChemicals (JV withBASF) Acrylic Acidcomplex fully operational

■ BP PETRONAS Acetyl(JV with BP Chemicals)started production of

Acetic Acid

■ Idemitsu SM (JVwith IdemitsuKosan) commencedoperations forproduction ofStyrene Monomer

■ Expandedproductioncapacities ofAmmonia and Ureain Bintulu complexby 13% and 25%,

respectively

■ OPTIMALcompanies (JV withDow Chemical)olefins plant, glycolsplant and chemicalsplant commencedoperations

■ Acquisition of BP‟s

stake in EMSB andPEMSB

■ Completed internalreorganisation toestablish PCG

■ PCG Listed

2006 2009

■ Expandedproductioncapacities ofMethanol, Ammoniaand Urea in Guruncomplex by11%, 17% and25%, respectively

■ Mega Methanol plantin Labuancommissioned

■ Dow Chemical‟s

interests in theOPTIMALcompanies‟ JVs

acquired

Various subsidiaries of PCG commenced operations

500

(1985)Capacity(1)

(ktpa)11,500

(2011)

(1) Includes share of production capacities of associates and jointly controlled entities

■ Conditional FID for aworld-scale fertiliserplant in Sipitang,

Sabah

2011

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 7/30

6

PCG’s unified corporate structure

OPTIMALOlefins

685 ktpa(2)

EthyleneMalaysia

400 ktpa(2)

Phu My100 ktpa(2)

AromaticsMalaysia

688 ktpa(2)

MalaysianNPK

Fertilizer310 ktpa(2)

PETRONASFertilizer

1,150 ktpa(2)

PETRONASMethanol

2,331 ktpa(2)

PETRONASAmmonia

1,132 ktpa(2)

MTBEMalaysia SB815 ktpa(2)

PolyethyleneMalaysia

300 ktpa(2)

KertihPort

PETRONASChemicalsMarketing

BASFPETRONASChemicals905 ktpa(2)

Idemitsu SM240 ktpa(2)

ASEANBintulu

Fertilizer1,200 ktpa(2)

KertihTerminals

BPPETRONAS

Acetyls500 ktpa(2)

PETLIN255 ktpa(2)

Vinyl ChlorideMalaysia

580 ktpa(2)

OPTIMALGlycols

765 ktpa(2)

OPTIMALChemicals410 ktpa(2)

PolypropyleneMalaysia80 ktpa(2)

Olefins and Derivatives Business Segment Fertilisers and Methanol Business Segment

100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

60% 87.5% 93.11%70% 88%

40% 30%

63.47%

30% 20% 40%

Partly-owned Subsidiaries Associates(1) Jointly Controlled EntityWholly-owned Subsidiaries

35.6%

(1) Associates in which PCG has a significant operational role (2) Production capacity

64.4%

Other Investors

© 2011 PETRONAS Chemicals Group Berhad

PETRONASChemicalsTrading Ltd

PETRONASChemicalsFertiliserSabah

100%

100%

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 8/30

7

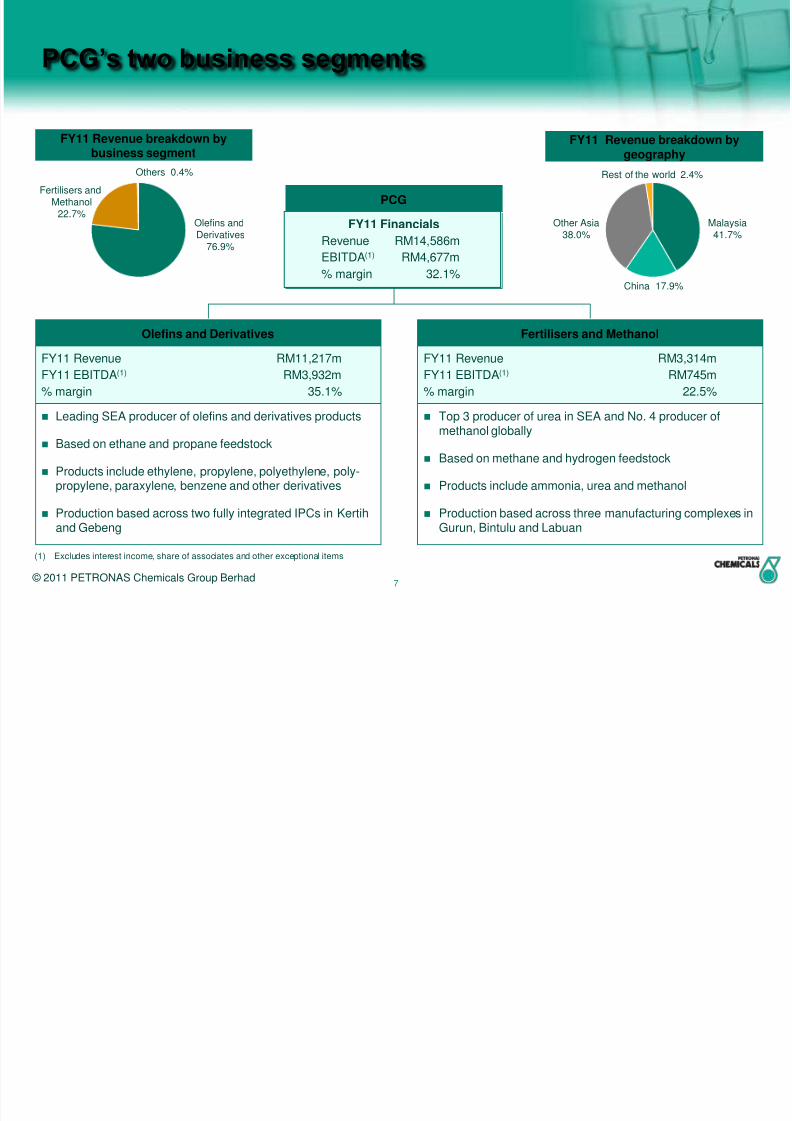

PCG’s two business segments

FY11 Revenue breakdown bybusiness segment

FY11 Revenue breakdown bygeography

FY 2010 financials

Revenue RM12,203m

EBITDA(1) RM3,802m

% margin 31%

Olefins and Derivatives

FY11 Revenue RM11,217m

FY11 EBITDA(1) RM3,932m

% margin 35.1%

Leading SEA producer of olefins and derivatives products

Based on ethane and propane feedstock

Products include ethylene, propylene, polyethylene, poly-propylene, paraxylene, benzene and other derivatives

Production based across two fully integrated IPCs in Kertihand Gebeng

Fertilisers and Methanol

FY11 Revenue RM3,314m

FY11 EBITDA(1) RM745m

% margin 22.5%

Top 3 producer of urea in SEA and No. 4 producer ofmethanol globally

Based on methane and hydrogen feedstock

Products include ammonia, urea and methanol

Production based across three manufacturing complexes inGurun, Bintulu and Labuan

(1) Excludes interest income, share of associates and other exceptional items

PCG

FY11 Financials

Revenue RM14,586m

EBITDA(1) RM4,677m

% margin 32.1%

© 2011 PETRONAS Chemicals Group Berhad

Malaysia41.7%

Other Asia38.0%

China 17.9%

Rest of the world 2.4%

Olefins andDerivatives

76.9%

Fertilisers andMethanol

22.7%

Others 0.4%

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 9/308

Company Highlights

Section 2

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 10/309

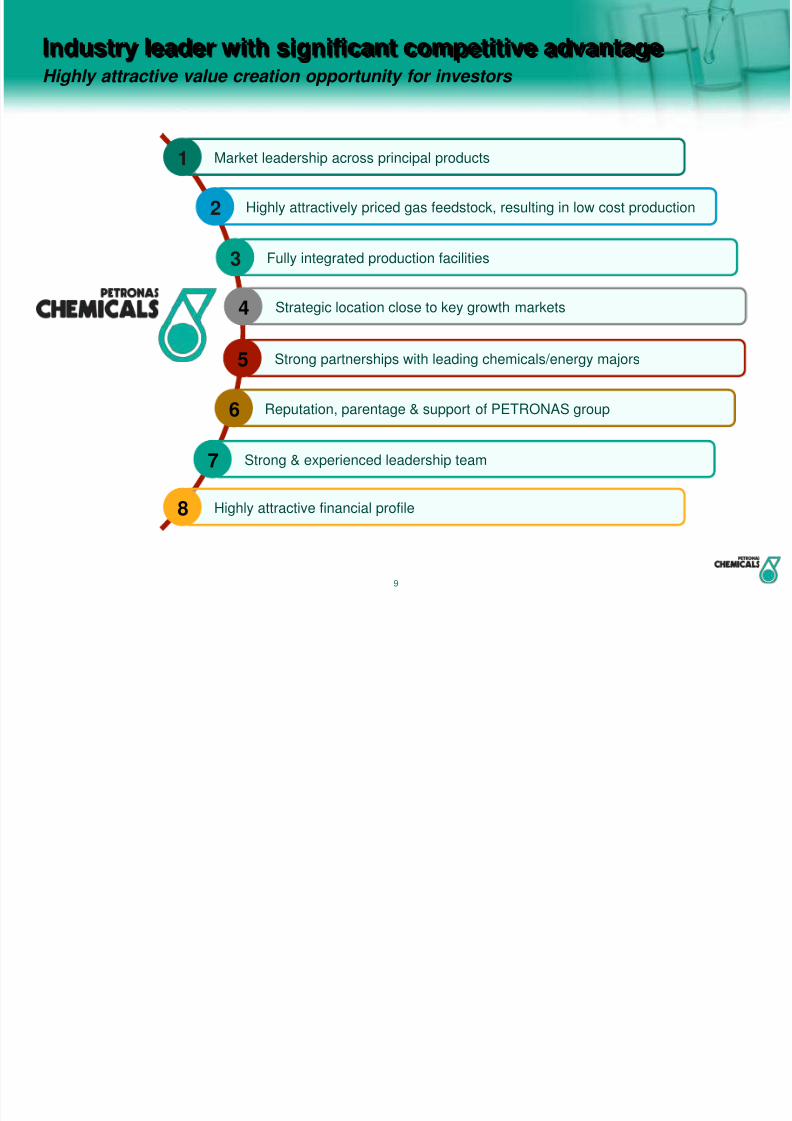

Highly attractive value creation opportunity for investors

Industry leader with significant competitive advantage

Market leadership across principal products1

Highly attractively priced gas feedstock, resulting in low cost production2

Reputation, parentage & support of PETRONAS group6

Strong & experienced leadership team7

Strategic location close to key growth markets4

Strong partnerships with leading chemicals/energy majors5

Highly attractive financial profile8

Fully integrated production facilities3

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 11/30

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 12/3011

Fully integrated production facilitiesResulting in significant production chain efficiencies…

FeedstockUpstreamproducts

Downstream products

K e r t i h I P C

Ethane

Paraxylene Benzene

Ethylene

Styrene Monomer LLDPE/HDPE VCM

LDPE

Ethylene Oxide

Butanol Chemicals

EthylenePropylene

NaturalGas

CrudeOil

MethaneAmmoniaOxogas

Propane

Ethylene Glycols

PVC

HeavyNaphtha

N-Butane

Propane

Butane

G e b e n g I P C

NaturalGas

Propylene

MTBE

PP

AcrylicsOxo Alcohols

Butanediol

Increased margin capture

Methane

L a b u a n

NaturalGas

Methanol

Methane

B i n t u l u /

G u r u n

NaturalGas

UreaAmmonia

= Ethane Chain= Basic feedstock = Propane Chain = Butane Chain = Naphtha Chain= Methane Chain

Integration from feedstock to downstream products minimises molecule loss, maximising production efficiency, as well asmargins, across the entire value chain

Simplified Production Value Chain

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 13/3012

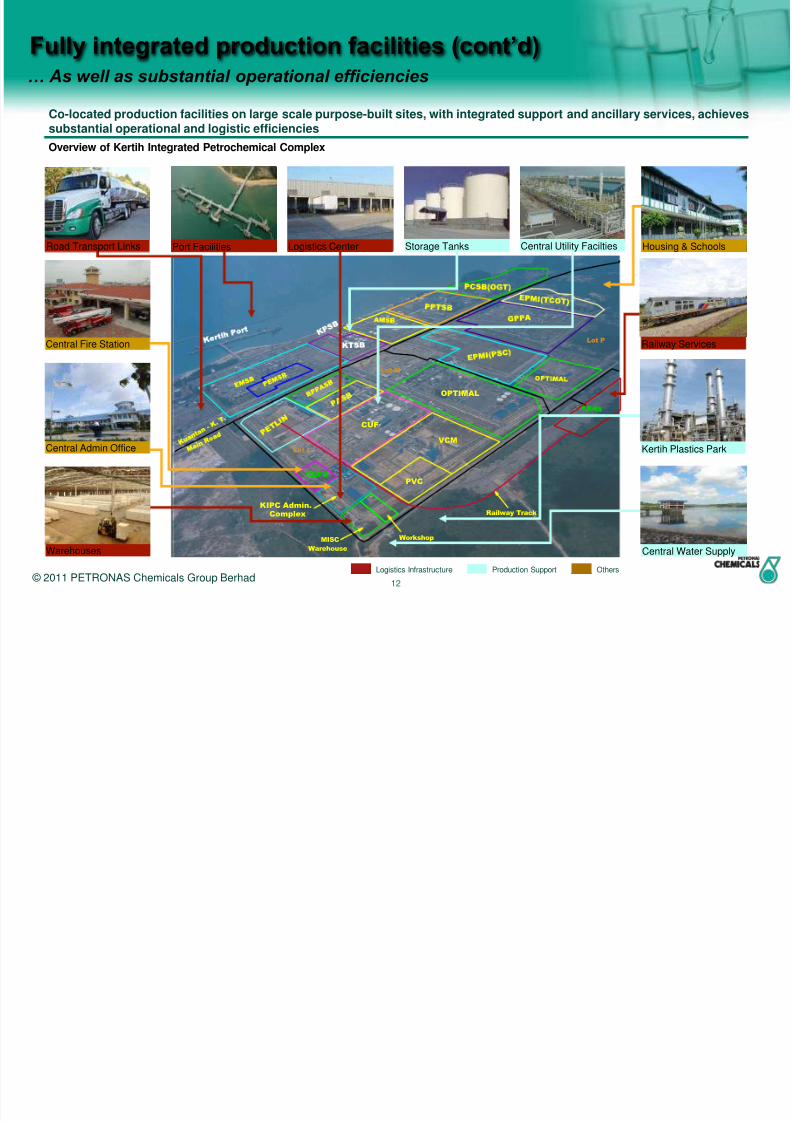

… As well as substantial operational efficiencies

Fully integrated production facilities (cont’d)

Co-located production facilities on large scale purpose-built sites, with integrated support and ancillary services, achievessubstantial operational and logistic efficiencies

Overview of Kertih Integrated Petrochemical Complex

OPTIMAL

VCM

PVC

CUF

CEFS

Lot L

KIPC Admin.Complex

MISC

Warehouse

Lot P

Lot M

Number ofcustomerproductionfacilities(1)

Logistics Infrastructure Production Support Others

Logistics Center Housing & SchoolsStorage Tanks

Warehouses

Central Utility Facilties

Central Admin Office

Central Fire Station Railway Services

Central Water Supply

Kertih Plastics Park

Road Transport Links Port Facilities

Workshop

Railway Track

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 14/3013

Strategic location close to key growth marketsMalaysia is an ideal production base to export to the high growth Asia Pacific markets

2.2%

3.5%

2.0%2.8%

2.2%

5.6%5.0%

5.4%5.8%

12.1%

2.7%3.4%

0%

3%

6%

9%

12%

15%

Po lyet hylene Et hylene

Glycol

P olypropylene Acrylic A cid M ethanol Urea

Asia Pacific economies have substantially higherpetrochemical demand outlook than developed economies

And Malaysia’s strategic location allows for much

shorter shipping times to those key markets

Petrochemical Demand by Key Markets

CAGR 2010-2017E

Shipping Distances from Malaysia vs. Middle East

(2) Assuming 12 knots/hr average cruising speed(1) North America + Europe

Key driversfor growth inAsia Pacific

Expansion ofmanufacturing

Rising wealth

Increasing substitution

New applications

Population and wealthgrowth

Ethylene & Propylene Methanol & Urea

Shipping

Days (2)

Malaysia

(Kertih)

Middle East

(Jubail, Saudi Arabia)

China (Xiamen) 4 days 19 days

Japan

(avg. Shimizu, Sakai,Kobe, Mizushima)

7 days 22 days

Taiwan (Kaohsiung) 4 days 18 days

Indonesia (avg.Surabaya, Semarang)

4 days 15 days

Thailand (Bangkok) 4 days 16 days

ShippingConsiderations

Smaller ships and smallerloads economically viable

Less crowded routes

More frequent vessels

Only large ships to maintaineconomies of scale

Potential delay throughcrowded Straits of Malacca

Source Nexant as at October 2010

Developed Countries (1) Asia Pacific

© 2011 PETRONAS Chemicals Group Berhad

Source World Ports Distances (www.distances.com)

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 15/3014

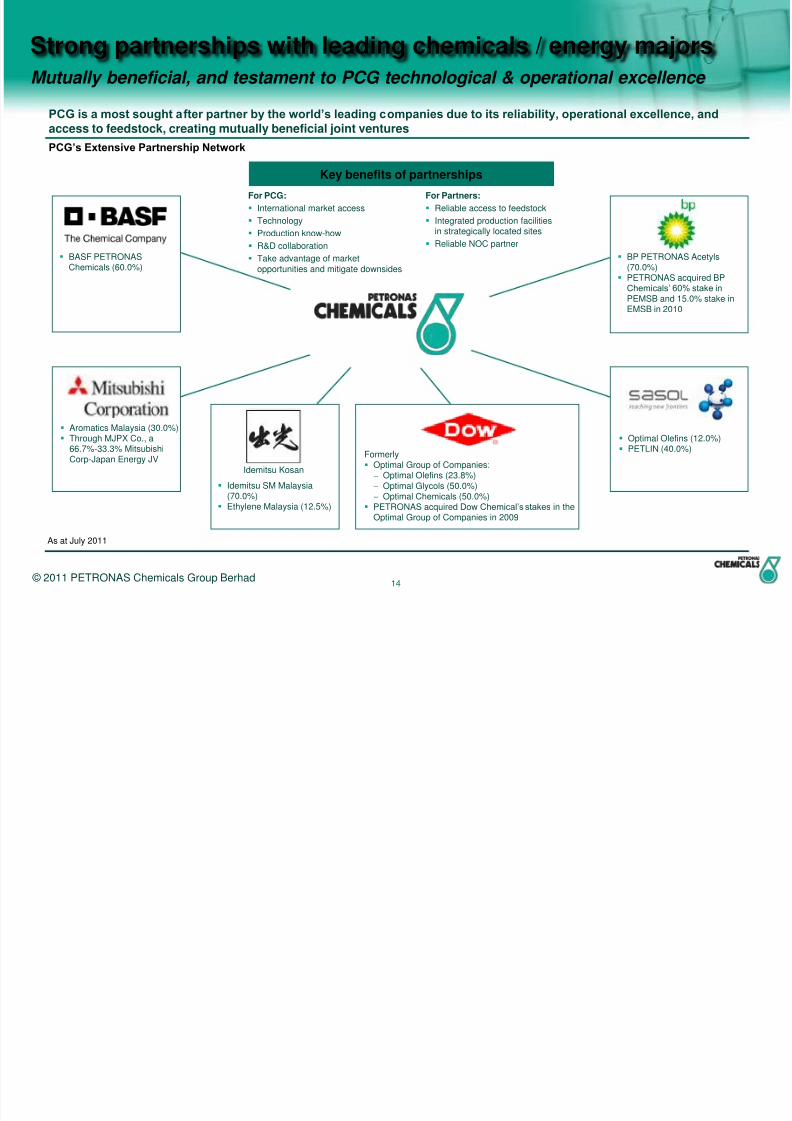

Strong partnerships with leading chemicals / energy majors

Mutually beneficial, and testament to PCG technological & operational excellence

Formerly Optimal Group of Companies: Optimal Olefins (23.8%) Optimal Glycols (50.0%) Optimal Chemicals (50.0%)

PETRONAS acquired Dow Chemical‟s stakes in theOptimal Group of Companies in 2009

Optimal Olefins (12.0%) PETLIN (40.0%)

Aromatics Malaysia (30.0%) Through MJPX Co., a

66.7%-33.3% MitsubishiCorp-Japan Energy JV

BASF PETRONASChemicals (60.0%)

BP PETRONAS Acetyls(70.0%)

PETRONAS acquired BPChemicals‟ 60% stake in

PEMSB and 15.0% stake inEMSB in 2010

Idemitsu SM Malaysia(70.0%)

Ethylene Malaysia (12.5%)

PCG is a most sought after partner by the world’s leading companies due to its reliability, operational excellence, and

access to feedstock, creating mutually beneficial joint ventures

PCG’s Extensive Partnership Network

Idemitsu Kosan

Key benefits of partnerships

For Partners:

Reliable access to feedstock

Integrated production facilitiesin strategically located sites

Reliable NOC partner

For PCG:

International market access

Technology

Production know-how

R&D collaboration

Take advantage of marketopportunities and mitigate downsides

© 2011 PETRONAS Chemicals Group Berhad

As at July 2011

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 16/3015

17.9% 23.6%

47.2%

5.2%

6.1%PCG(1)

Reputation, parentage & support of PETRONAS GroupMaintains PCG’s competitiveness and provides synergies for future growth

PCG is Malaysia’s chemical industry champion, and with the on-going support of PETRONAS Group, will be a strongplatform for future growth

PETRONAS Group Overview

Source PETRONAS company reports as at 31 March 2011

National oil company wholly-owned by the Government ofMalaysia

Entrusted with the management of all the oil and gasreserves in Malaysia

Manages the issuances of all PSCs issued in Malaysia

Revenues = US$77 bn EBITDA= US$34 bn Total Assets= US$145 bn

Integrated Oil & Gas producer with E&P, R&M, chemicalsand shipping businesses

Operations in over 30 countries globally Retains majority stakes in listed companies such as

PETRONAS Gas, PETRONAS Dagangan and MISC

Financials FY11A

Cash & Investments = US$35 bn Credit rating of A1/A-/A (Moody‟s/S&P/Fitch)

Ranked 86 among Fortune 500 companies

E&P Business- Crude oil- Natural gas

Gas & Power Business- LNG- Processed gas

Other Businesses

- Logistics & maritimebusiness

- Others

Downstream Business

- Refined petroleumproducts- Crude oil trading

(1) Converted to US$ from MYR at the daily average exchange rate for FY11A, US$1 = MYR3.14

© 2011 PETRONAS Chemicals Group Berhad

Revenue FY11A

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 17/3016

Strong and experienced leadership teamWith significant experience across the entire petrochemicals value chain

Seasoned management team, with in-depth knowledge of the petrochemicals industry, and with ambitious plans forPCG…

PCG Senior Management

…building upon a strong track record of successful growth, and poised for future developments

(1) “Industry” = Petrochemicals Value Chain, including Chemicals and oil & gas (2) “Industry” = Petrochemicals Value Chain, including Chemicals and oil & gas, and financial functions

CFO

17 years in industry(2)

14 years at PETRONAS

WanShamilah

Saidi

Chairman

29 years in industry(1)

29 years at PETRONAS

WanZulkiflee

Head, Olefins &

Derivatives Division 28 years in industry(1)

28 years at PETRONAS

YusaHassan

Head, Fertiliser &

Methanol Division 18 years at PETRONAS

MahmadZahri

Mahzan

President/CEO

25 years in industry(1)

Joined May 1st 2011

Dr. A. HapizAbdullah

PCG’s Total Petrochemical Production Capacity

„000s mtpa

0

3,000

6,000

9,000

12,000

1985 1992 1994 1995 1997 1999 2000 2002 2004 2006 2009 2010

ASEAN BintuluFertilizer startedoperations

MTBE & PMSB startedoperations; LabuanMethanol plant acquired

PEMSB & EMSBstarted operations

CUF in Kertih andGebeng in operation;PETRONAS Fertilizerstarted operations

BASF PETRONAS, Aromatics Malaysia,PETRONAS Ammonia, Vinyl ChlorideMalaysia, BP PETRONAS Acetylsstarted operations

OPTIMAL Companies,PETLIN, Phu My startedoperations

Mega Methanol plant in Labuancommissioned; acquired DowChemical‟s stake in OPTIMAL

Companies

Acquired BPChemicals‟ stake in

PEMSB and EMSB

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 18/3017

Key Strategies & Future Developments

Section 3

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 19/3018

Time

Long TermShort Term

Consolidation of ourpetrochemicals activities1

■ Centralise management

■ Optimisation of hydrocarbon

chain■ Economies of scale

■ Higher overall utilisation

Expand our productportfolio2

■ Premium pricing

■ Wider customer base

■ Resilience to economic cycles

■ Enhanced profitability

Increase our productioncapacity3

■ Greenfield integrated refineryand petrochemical complex

■ World-scale, greenfieldammonia and urea productionfacility

Selective synergistic growth acquisitions4

■ Asia Pacific market

■ Existing or complementary products

■ Enhance strategic competitiveness

■ Disciplined financial evaluation

Key strategies & future developmentsMaximise shareholder value through achievable short, medium and long term plans

© 2011 PETRONAS Chemicals Group Berhad

Medium Term

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 20/3019

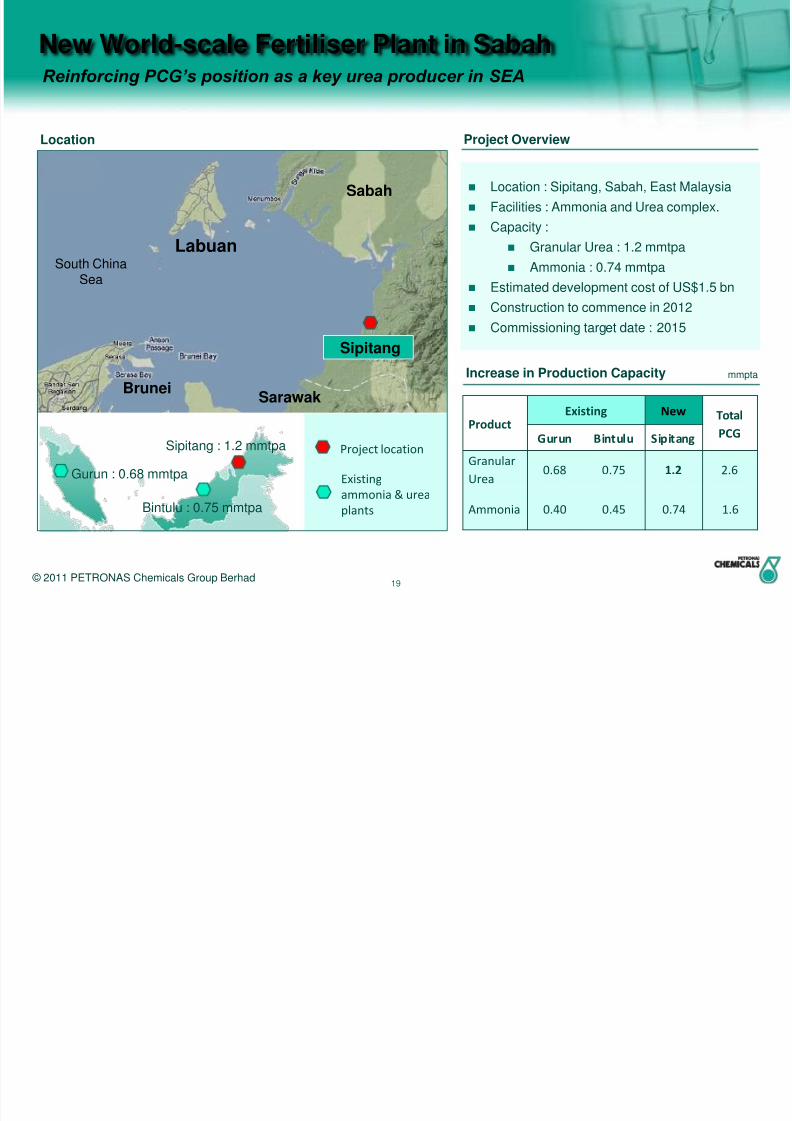

New World-scale Fertiliser Plant in Sabah

Location : Sipitang, Sabah, East Malaysia

Facilities : Ammonia and Urea complex.

Capacity :

Granular Urea : 1.2 mmtpa

Ammonia : 0.74 mmtpa

Estimated development cost of US$1.5 bn

Construction to commence in 2012

Commissioning target date : 2015

Project Overview

Gurun : 0.68 mmtpa

Bintulu : 0.75 mmtpa

Project location

Existing

ammonia & urea

plants

Reinforcing PCG’s position as a key urea producer in SEA

Product Existing New TotalPCGGurun Bintulu Sipitang

Granular

Urea0.68 0.75 1.2 2.6

Ammonia 0.40 0.45 0.74 1.6

Increase in Production Capacity mmpta

Sipitang : 1.2 mmtpa

© 2011 PETRONAS Chemicals Group Berhad

Sipitang

Labuan

Sarawak

Sabah

Brunei

South China

Sea

Location

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 21/3020

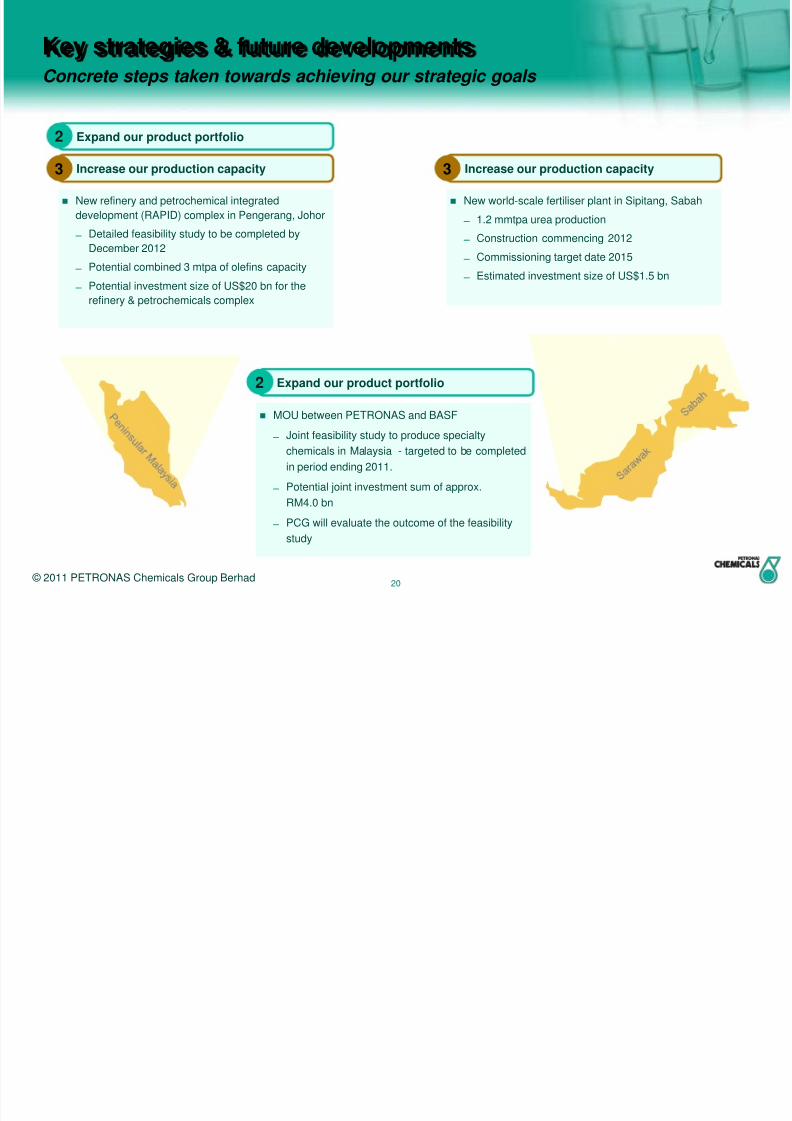

New world-scale fertiliser plant in Sipitang, Sabah

1.2 mmtpa urea production

Construction commencing 2012

Commissioning target date 2015

Estimated investment size of US$1.5 bn

Key strategies & future developmentsConcrete steps taken towards achieving our strategic goals

Expand our product portfolio2

Increase our production capacity3

New refinery and petrochemical integrated

development (RAPID) complex in Pengerang, Johor

Detailed feasibility study to be completed by

December 2012

Potential combined 3 mtpa of olefins capacity

Potential investment size of US$20 bn for the

refinery & petrochemicals complex

Increase our production capacity3

Expand our product portfolio2

MOU between PETRONAS and BASF Joint feasibility study to produce specialty

chemicals in Malaysia - targeted to be completed

in period ending 2011.

Potential joint investment sum of approx.

RM4.0 bn

PCG will evaluate the outcome of the feasibility

study

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 22/3021

Financials

Section 4

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 23/3022

PCG financial highlights

(1) Excludes interest income, share of associates and other exceptional items (2) ROA = NOPAT / fixed assets

Strong group revenue through the petrochemical cycle

– From FY2008 – FY2010, stable revenue of RM12.2bn to RM12.9bn (variance of 5%) through petrochemical

downturn

– In FY2011, revenue increased by 19.5% reflecting the upturn in petrochemical cycle

– Delivered through diversification across products, Optimal stake acquisition and capacity increases (mega

methanol plant start-up)

Superior EBITDA(1) margins

– FY2011 PCG EBITDA margin of 32.1%

– Advantaged feedstock and high degree of integration

Strong cashflow generation

– Cash conversion ratio of 86.7% in FY2011

– Driven by superior cost base and disciplined capital investment

Superior returns on assets

– Average ROA(2) of 24.7% over last 3 years

Prudent capital structure for future growth

– Net cash position of RM5.2bn

© 2011 PETRONAS Chemicals Group Berhad

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 24/3023

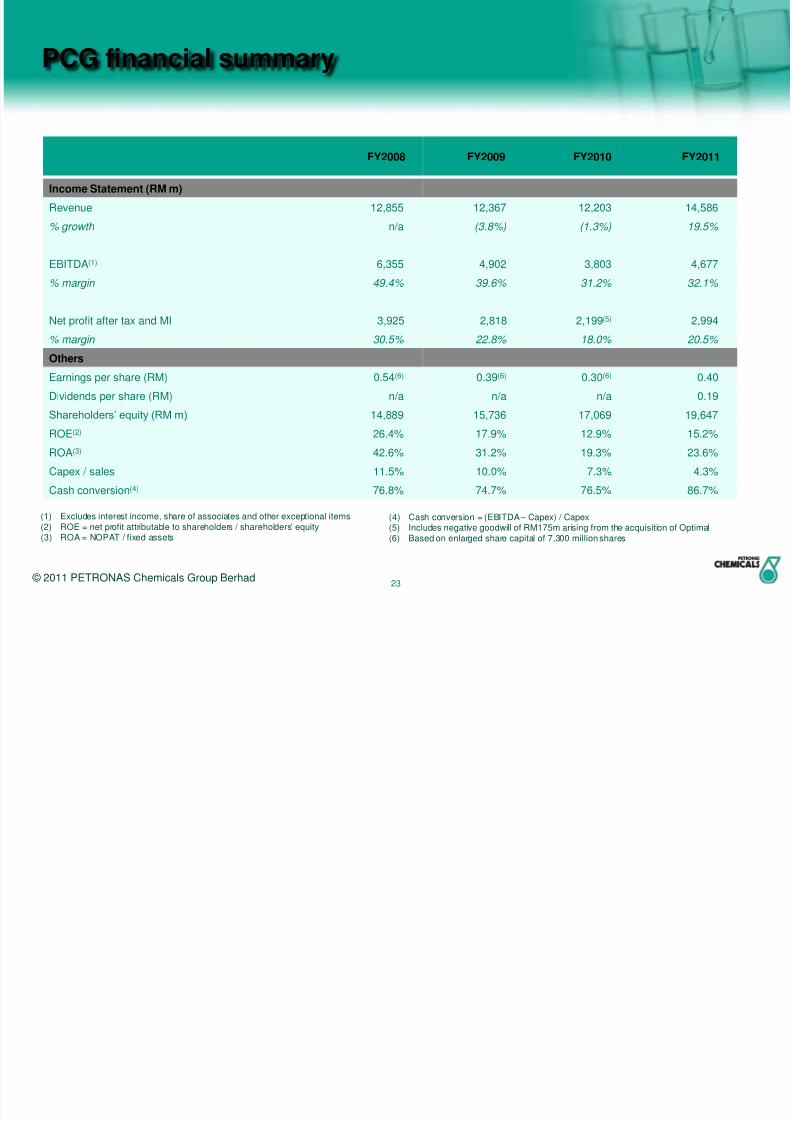

PCG financial summary

FY2008 FY2009 FY2010 FY2011

Income Statement (RM m)

Revenue 12,855 12,367 12,203 14,586

% growth n/a (3.8%) (1.3%) 19.5%

EBITDA(1) 6,355 4,902 3,803 4,677

% margin 49.4% 39.6% 31.2% 32.1%

Net profit after tax and MI 3,925 2,818 2,199(5) 2,994

% margin 30.5% 22.8% 18.0% 20.5%

Others

Earnings per share (RM) 0.54(6) 0.39(6) 0.30(6) 0.40

Dividends per share (RM) n/a n/a n/a 0.19

Shareholders‟ equity (RM m) 14,889 15,736 17,069 19,647ROE(2) 26.4% 17.9% 12.9% 15.2%

ROA(3) 42.6% 31.2% 19.3% 23.6%

Capex / sales 11.5% 10.0% 7.3% 4.3%

Cash conversion(4) 76.8% 74.7% 76.5% 86.7%

(1) Excludes interest income, share of associates and other exceptional items(2) ROE = net profit attributable to shareholders / shareholders‟ equity

(3) ROA = NOPAT / fixed assets

© 2011 PETRONAS Chemicals Group Berhad

(4) Cash conversion = (EBITDA – Capex) / Capex(5) Includes negative goodwill of RM175m arising from the acquisition of Optimal(6) Based on enlarged share capital of 7,300 million shares

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 25/3024

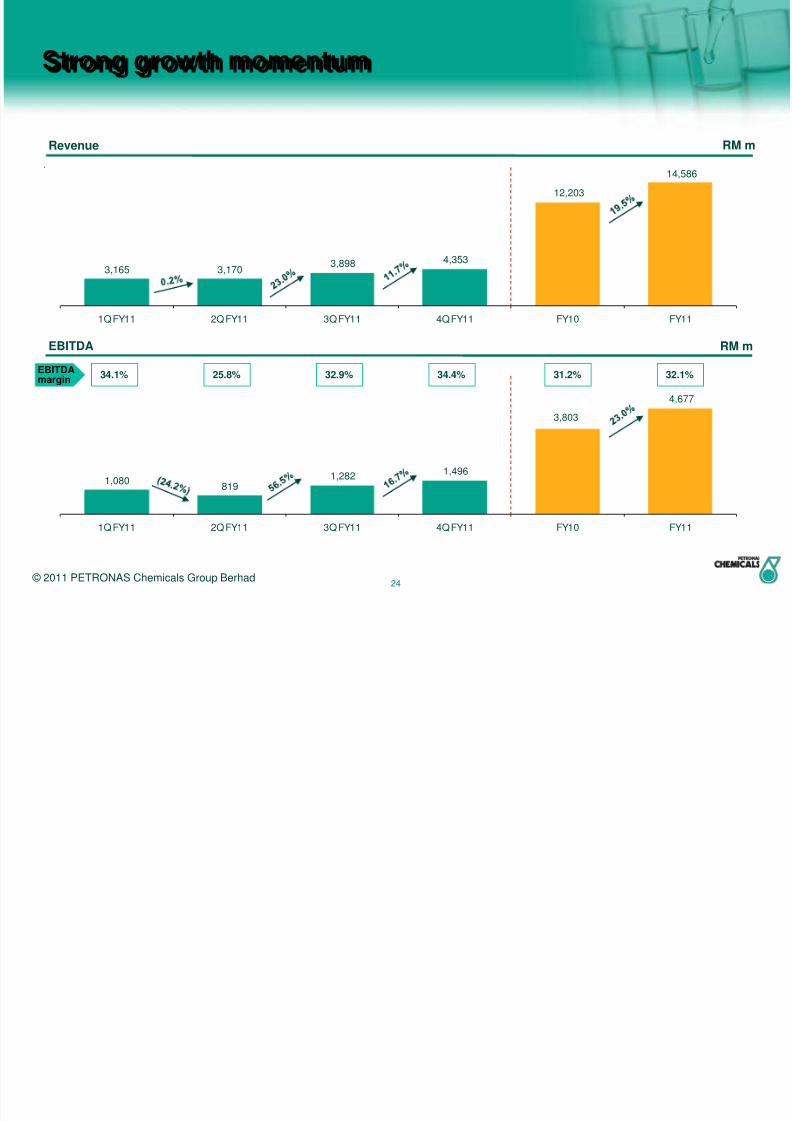

Strong growth momentum

3,165 3,1703,898 4,353

12,203

14,586

1Q FY11 2Q FY11 3Q FY11 4Q FY11 FY10 FY11

1,080819

1,2821,496

3,802

4,677

1Q FY11 2Q FY11 3Q FY11 4Q FY11 FY10 FY11

EBITDAmargin

34.1% 32.9% 34.4%25.8% 31.2% 32.1%

3,803

© 2011 PETRONAS Chemicals Group Berhad

Revenue

EBITDA RM m

RM m

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 26/3025

31.2%

19.3%

23.6%

FY09 FY10 FY11

Attractive through the cycle return on assets and equity

(1) ROA = NOPAT / fixed assets(2) ROE = net profit attributable to shareholders / shareholders‟ equity

Despite industry downturn from FY2008 to FY2010, ROA and ROE of PCG remained resilient

Higher YoY ROA and ROE

ROA(1) ROE(2)

© 2011 PETRONAS Chemicals Group Berhad

17.9%

12.9%

15.2%

FY09 FY10 FY11

AverageROA

24.7%AverageROE

15.3%

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 27/30

26

Group Utilisation

© 2011 PETRONAS Chemicals Group Berhad

86.6%

74.2%83.9% 82.5% 81.0%

4Q FY10 3Q FY11 4Q FY11 FY10 FY11

92.6%

98.6%

86.0%

90.2%88.3%

4Q FY10 3Q FY11 4Q FY11 FY10 FY11

81.1%

54.7%

82.0%

76.7% 74.6%

4Q FY10 3Q FY11 4Q FY11 FY10 FY11

Group Consolidated

Olefins and Derivatives Fertilisers and Methanol

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 28/30

27

3,114 3,274

9,255

11,217

3Q FY11 4Q FY11 FY10 FY11

9001,085

2,048

3,152

3Q FY11 4Q FY11 FY10 FY11

1,130 1,208

3,121

3,932

3Q FY11 4Q FY11 FY10 FY11

Olefins and Derivatives

EBITDAmargin

36% 34% 35%

98.6%

86.0%

90.2%88.3%

3Q FY11 4Q FY11 FY10 FY11

37%

Utilisation rate Revenue

EBITDA Profit for the period

© 2011 PETRONAS Chemicals Group Berhad

RM m RM m

RM m

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 29/30

28

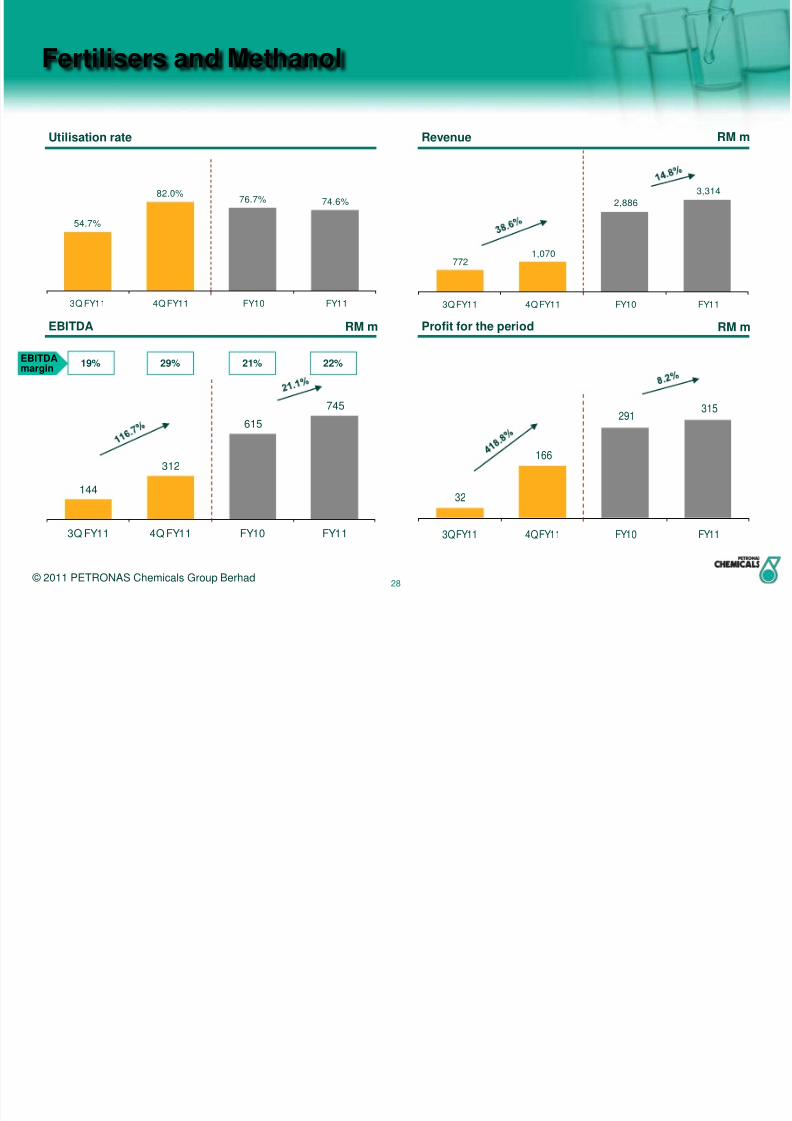

Fertilisers and Methanol

7721,070

2,886

3,314

3Q FY11 4Q FY11 FY10 FY11

54.7%

82.0%76.7% 74.6%

3Q FY11 4Q FY11 FY10 FY11

32

166

291

315

3Q FY11 4Q FY11 FY10 FY11

144

312

615

745

3Q FY11 4Q FY11 FY10 FY11

EBITDAmargin

19% 21% 22%29%

Utilisation rate Revenue

EBITDA Profit for the period

© 2011 PETRONAS Chemicals Group Berhad

RM m RM m

RM m

8/2/2019 PCG Company Presentation - July 2011

http://slidepdf.com/reader/full/pcg-company-presentation-july-2011 30/30

Thank Youwww.petronaschemicals.com