pearson lcci level 3 management accounting · 3.1 absorption and marginal costing – terms 3.2...

TRANSCRIPT

Pearson LCCI

Level 3 Management

Accounting (ASE3024)

Annual Qualification

Review 2014/2015

2012-2013

2 Annual Qualification Review qualifications.pearson.com/lcci

CONTENTS

Introduction 2 Pass Rate Statistics 2

General Strengths and Weaknesses 3 Teaching Points by Syllabus Topic 4

Examples of Candidate Responses 5

3 Annual Qualification Review qualifications.pearson.com/lcci

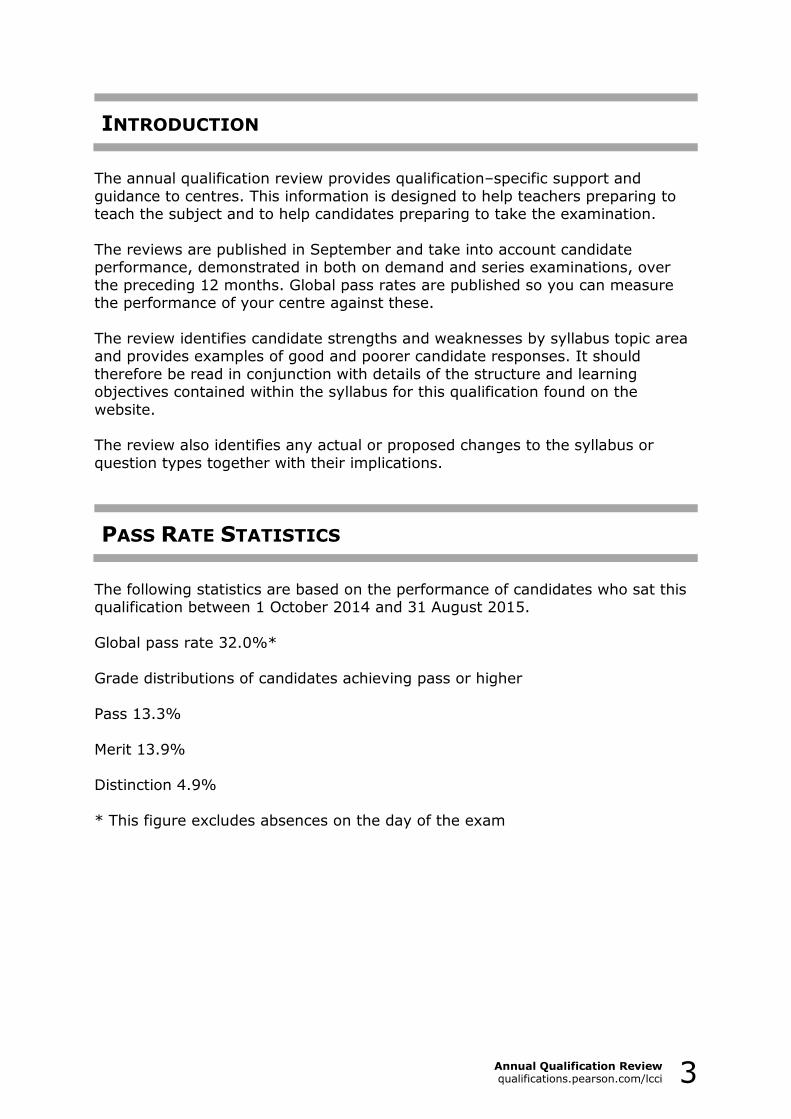

INTRODUCTION

The annual qualification review provides qualification–specific support and

guidance to centres. This information is designed to help teachers preparing to teach the subject and to help candidates preparing to take the examination.

The reviews are published in September and take into account candidate performance, demonstrated in both on demand and series examinations, over

the preceding 12 months. Global pass rates are published so you can measure the performance of your centre against these.

The review identifies candidate strengths and weaknesses by syllabus topic area and provides examples of good and poorer candidate responses. It should

therefore be read in conjunction with details of the structure and learning objectives contained within the syllabus for this qualification found on the

website. The review also identifies any actual or proposed changes to the syllabus or

question types together with their implications.

PASS RATE STATISTICS

The following statistics are based on the performance of candidates who sat this qualification between 1 October 2014 and 31 August 2015.

Global pass rate 32.0%*

Grade distributions of candidates achieving pass or higher

Pass 13.3%

Merit 13.9% Distinction 4.9%

* This figure excludes absences on the day of the exam

4 Annual Qualification Review qualifications.pearson.com/lcci

GENERAL STRENGTHS AND WEAKNESSES

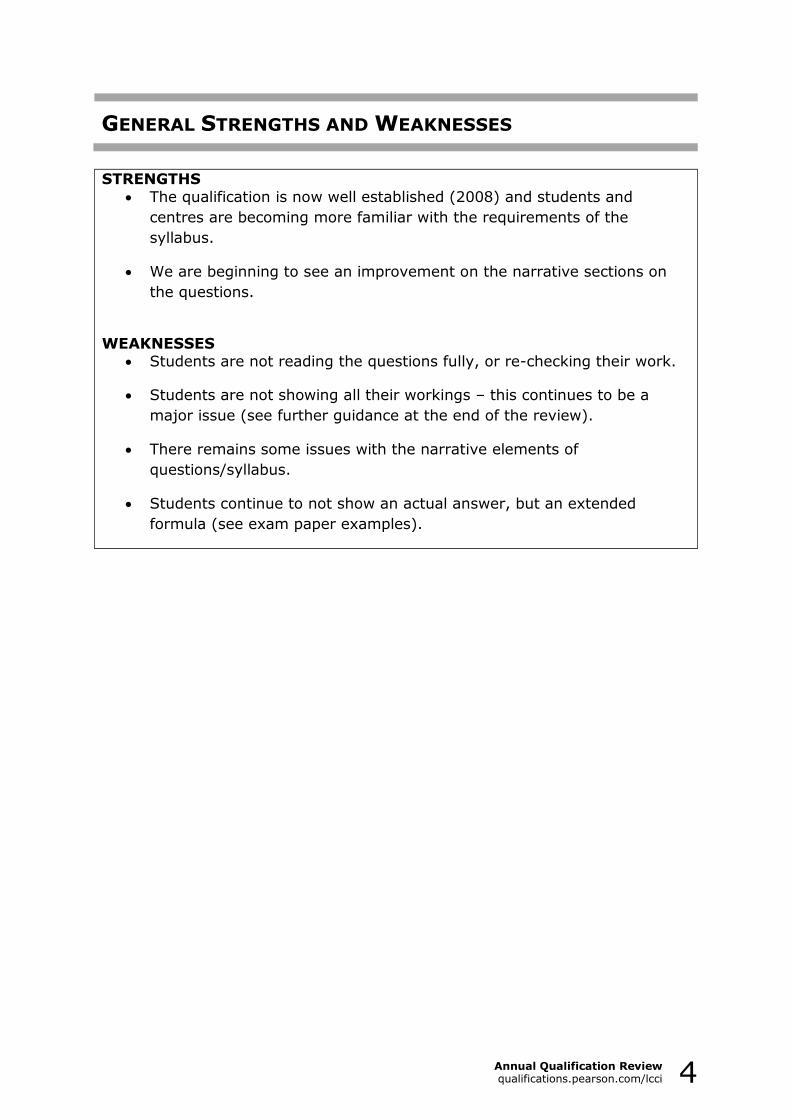

STRENGTHS

The qualification is now well established (2008) and students and

centres are becoming more familiar with the requirements of the

syllabus.

We are beginning to see an improvement on the narrative sections on

the questions.

WEAKNESSES Students are not reading the questions fully, or re-checking their work.

Students are not showing all their workings – this continues to be a

major issue (see further guidance at the end of the review).

There remains some issues with the narrative elements of

questions/syllabus.

Students continue to not show an actual answer, but an extended

formula (see exam paper examples).

5 Annual Qualification Review qualifications.pearson.com/lcci

TEACHING POINTS BY SYLLABUS TOPIC

1 Short-term cost behaviour

1.1 Define costs as variable, semi-variable, stepped or fixed (Series 2)

1.2 Separate costs into fixed and variable (Series 2)

1.3 Use the high low method (Series 2)

1.4 Calculate costs per period (Series 2)

1.5 Forecast costs using the high/low method (Series 2)

1.6 Explain the effect of time on cost behaviour

Question 1 a, b & c (Series 2) was reasonably well answered by the majority of

candidates.

2 Cost/volume/profit analysis

2.1 Calculate the contribution/sales ratio

2.2 Explain and calculate the break-even point

2.3 Explain and calculate the margin of safety

2.4 Apply CVP analysis (Series 2) (Series 3)

2.5 Construct charts

2.6 Read the B.E and MOS from a chart

2.7 Discuss the assumptions and limitations of CVP analysis

Question 1d (Series 2) caused problems for many candidates. This is an area of the syllabus (applying CVP analysis) that candidates need to fully

understand, if they are to be able to provide a reasonable answer. There is no set formula or procedure; it requires an understanding of CVP analysis. The basic premise is that fixed costs (tend to) remain unaltered and it is only the

variable costs (and sales units/price) that are relevant.

Question 1a (Series 3) was an expanded form of question that appeared in

series 2. It was not well answered by the majority of candidates. A good technique would be to try and 'un-pick' the model answer to Q1a series 3 2015, to identify the key techniques and principles and then go on to practice

these techniques.

Question 1c (Series 3) was only answered well by merit/distinction level

candidates. Although only a small question, it has featured on a number of occasions. Candidates need to read and understand what the question requires. The scenario states that the company plans to make and sell TWO

types of product. Selling two units of X (2/3) and one unit of Y (1/3). The question asks "Calculate the number of units (MIX) of Product X AND Product Y

the company needs to sell." Many students provided an answer of total units, without specifying X or Y; or stated a total number of X or Y that the company could sell.

6 Annual Qualification Review qualifications.pearson.com/lcci

3 Short-term decision-making - This syllabus topic area is a compulsory topic area

3.1 Absorption and marginal costing – terms

3.2 Absorption and marginal costing – profit statements

3.3 Usefulness of absorption and marginal costing

3.4 Relevant costs and limitations (3.10)

3.5 Limiting factor analysis (3.6, 3.7 and 3.9) (Series 2)

3.8 Linear programming

3.11 Identify products or departments for closure

3.12 The limitations of short term decision making

3.13 Calculate a selling price for a product

Question 2a (Series 2) was a limiting factor question, which was quite well

answered by many candidates. However, what cost many candidates marks was in calculating the contribution per labour. The contribution per unit for

product X was £4.50 per unit. The question advices the candidate that the output per direct labour hour was 10 units, so the contribution per direct labour hour was £45 (£4.50 x 10 units) Many candidates made this figure 45p

(dividing £4.50 by 10 units). This mistake was repeated on products Y and Z.

4 Budgetary planning and control

4.1 Benefits, limitations and process

4.2 Budget planning and control

4.3 Principle budget factor (4.4)

4.4 Prepare a variety of budgets (4.5) (Series 2)

4.6 Flexible budgets (4.7 and 4.8) (Series 3)

4.9 Other approaches and behaviour

4.10 Behavioural aspects

Question 2b (Series 2) required candidates to prepare production budgets. This was generally answered very well. It is clear that candidates are well prepared

for this topic area.

Question 5c (Series 3) was a question of flexible budgets, which was well

answered by the majority of candidates.

5 Cash & working capital management

5.1 Explain liquidity and cash flow

5.2 Cash budgets (5.3) (Series 3)

5.4 Working capital requirements (5.6) (Series 2)

5.5 Working capital budgets (Series 2)

5.7 Reconcile profit and cash (budgets)

7 Annual Qualification Review qualifications.pearson.com/lcci

5.8 Interpret w/c ratios (5.9) (Series 3)

5.10 Calculate the w/c cycle

Q3a (Series 2) involved the calculation of working capital management. A lot of candidates found this to be problematic.

Only the merit/distinction level candidates scored high marks. One possible concern was with the calculation of the work-in-progress (part 4 on the question) which involved materials, labour and production overheads. Many

candidates showed a correct (total) answer of £42,135 with NO workings. This is acceptable if the answer is correct and will gain the maximum (4) marks

available.

However, a significant number of candidates showed an incorrect answer with no breakdown of the three elements and no workings and were unable to gain

any of the part marks that were available.

Question 2a (Series 3) had a cash budget, which was relatively well answered

by many candidates. Three problems were generally associated with this question:

1. Candidates calculated the sales receipts by 60% of one month, 35% of

another month, and then deducted a further 5% for bad debts, which

had already been accounted for in the question

2. Candidates had issues with the timing(s) associated with receipts and

payments. The candidate was able to calculate the correct amount(s)

but placed these figure in the wrong months

3. The calculation of the purchase figure proved the major difficulty,

combined with getting the correct figure in the correct months

Q3 (Series 3) asked for ratios to be calculated (12 marks), together with an

analysis of the ratios (using the company's financial accounts provided) (8 marks). Most candidates could calculate the ratios reasonably well but the

majority of students failed to give a reasonable analysis (8 marks) of what the ratios actually meant. Far too often candidates said that year 1 was better/higher/lower/worse than year 2. Candidates also used a 'text book'

analysis saying that the liquidity ratios were around the expected benchmark and showed that the company's liquidity was 'healthy'. If the student had

referred to the accounts provided in the question they would have seen that the company had a massive bank overdraft in year 2; therefore had no money to pay its Creditors, indicating a serious liquidity problem. The stock level had

increased by 50% (Why?), resulting in Creditors increasing. Too many of the increased Sales were on credit, resulting in the company having to take out an

overdraft to continue operating. This question provided a classic working capital (mis)management scenario.

Candidates needed to look at the accounts as well as the ratios, before making a judgement/comment, and are expected to be able to make a reasonable analysis based on their ratios and the financial information provided.

Similar questions appeared in Series 2 2013 and Series 3 2014, with similar comments appearing in the annual reports. This is an area that centres need to

focus on to develop the student's ability.

8 Annual Qualification Review qualifications.pearson.com/lcci

6 Standard costing and variances

6.1 Explain the meaning of a standard cost

6.2 Calculate total sales, selling price and sales volume

6.3 Direct material variances

6.4 Define the standard hour

6.5 Direct labour variances

6.6 Fixed production overhead variances

6.8 Reconcile budgeted and actual profits

6.9 Calculate standard or actual costs

6.10 Cost control

6.11 Interpret variances

6.12 Calculate production ratios

6.13 Explain the use of ex-ante and ex-post standards

6.14 Calculate and interpret planning/operational variances (Series 2)

(Series 3)

Q3b (Series 2) featured the calculation of planning and operational variances. This was generally well answered, with many candidates gaining partial or full

marks. Q5b (Series 3) once again featured the calculation of planning and operational variances. This was generally well answered, with many candidates

gaining partial or full marks. This was welcoming to see, as this is arguably the hardest situation regarding variances. There was evidence that a lot of

candidates had studied the question and prepared an analytical answer.

7 Long-term decision-making - Once again a compulsory topic area

7.1 Difference between long term and short term decision making

7.2 Relevant and irrelevant costs (Series 3)

7.3 Capital appraisal techniques – payback and ARR (Series 2)

7.4 DCF appraisal techniques (7.5 and 7.7)

7.6 NPV and IRR discounting methods (7.8 and 7.9)

7.10 Calculate discounted payback

7.11 Calculate a profitability index

7.12 Calculate a weighted average cost of capital

7.13 Apply risk analysis

7.14 Incorporate inflation in appraisal techniques

7.15 Interpret analysis

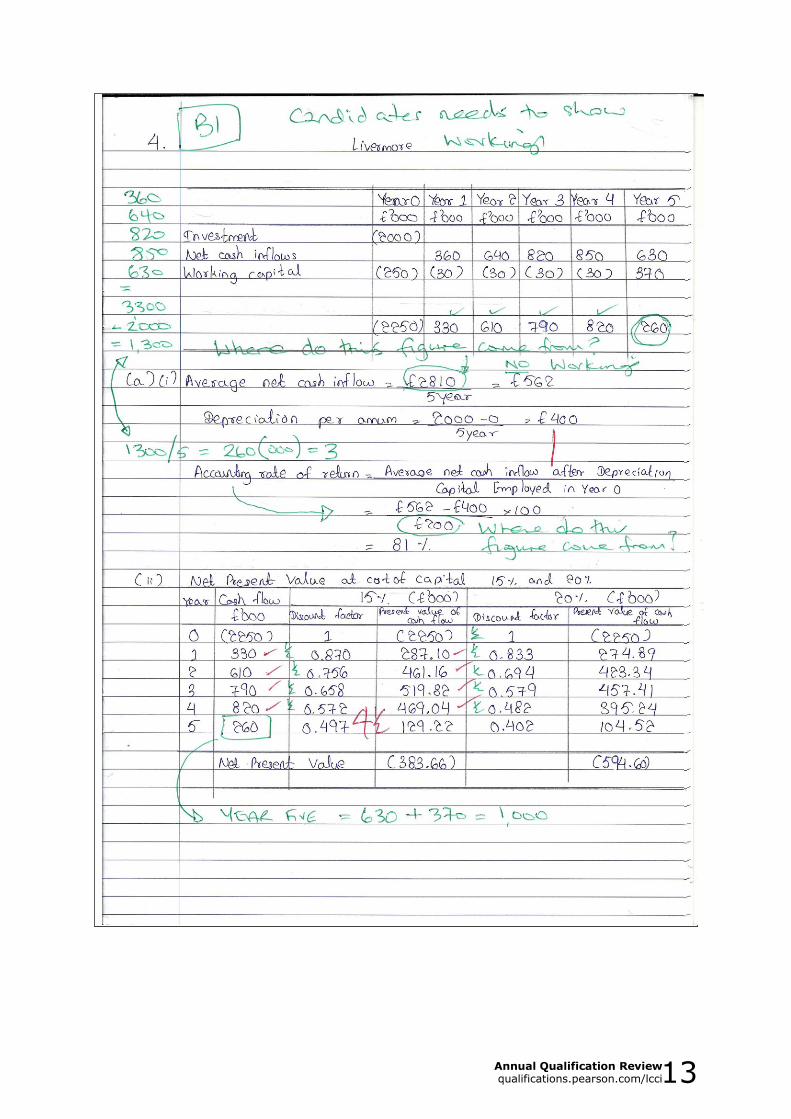

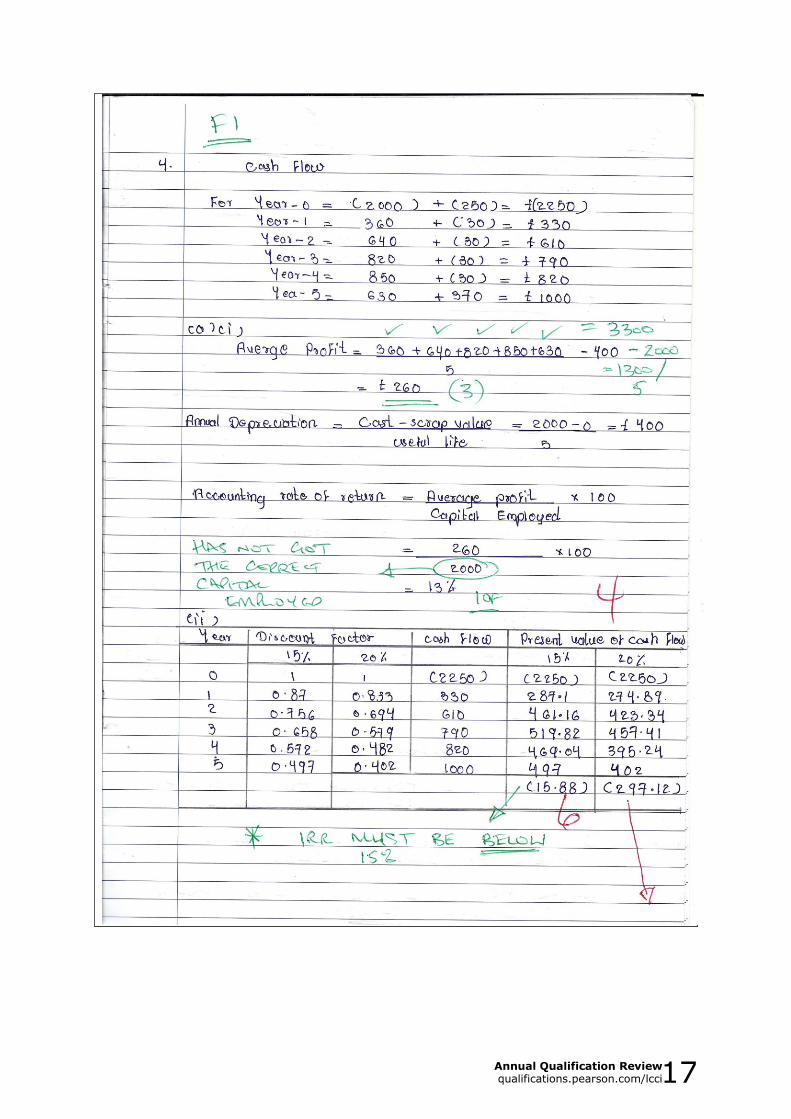

Q4 (Series 2) was not as complex as many DCF/NPV questions that have

appeared on the exam paper.

Despite it being a compulsory topic in the exam it still continues to cause problems for candidates. Part (a)(i) was reasonably well answered, with a lot

9 Annual Qualification Review qualifications.pearson.com/lcci

of candidates scoring 3/6 marks. The majority of candidates were able to make a good attempt at calculating the required profit, despite it being a fairly

complicated calculation. The ARR required the average investment, which many candidates made a reasonable attempt at calculating. Candidates should

take care about which method of calculation is required for the investment value.

However, the majority of candidates were unable to calculate the net cash flow

for part (a)(ii), despite it being displayed quite clearly on the question, and it being a simple calculation (which probably was undertaken in part (a)(i)).

Thus, many candidates lost out on 5/6 marks for this part (a)(ii) and then relied on own figure marks for part (a)(iii).

Centres must ensure that candidates appreciate the difference between profit

and cash flow. How these two items are calculated and when they are required in the question.

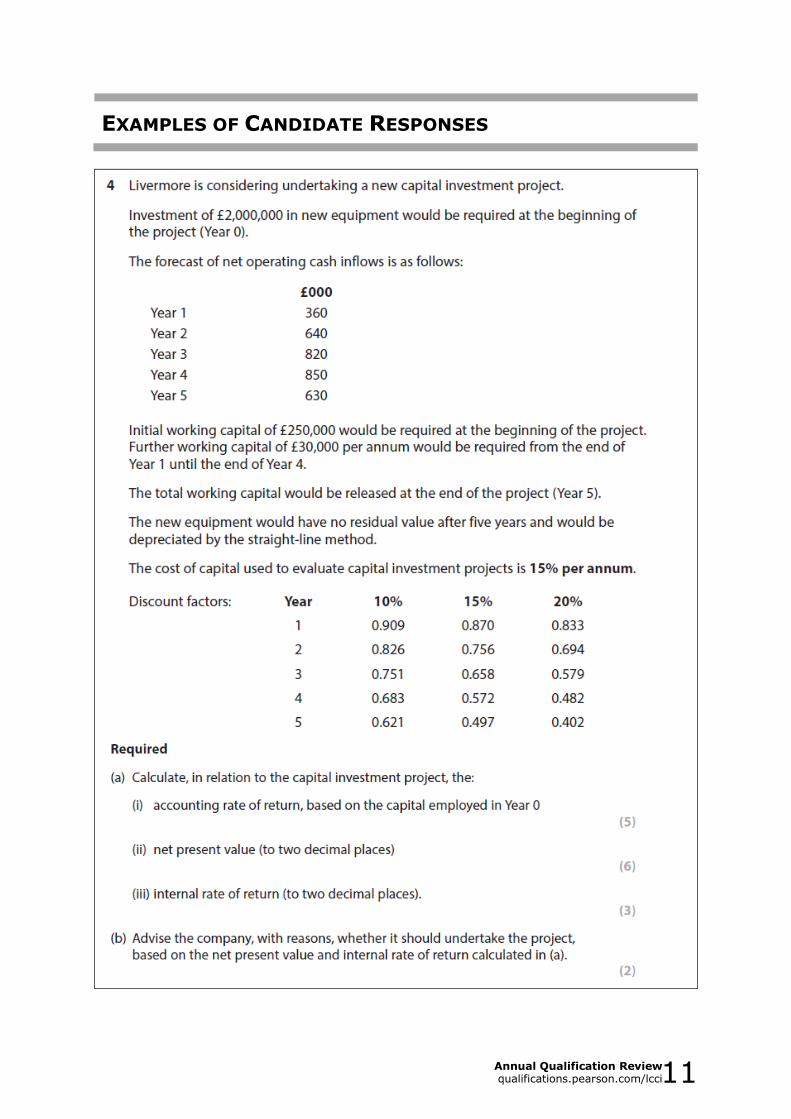

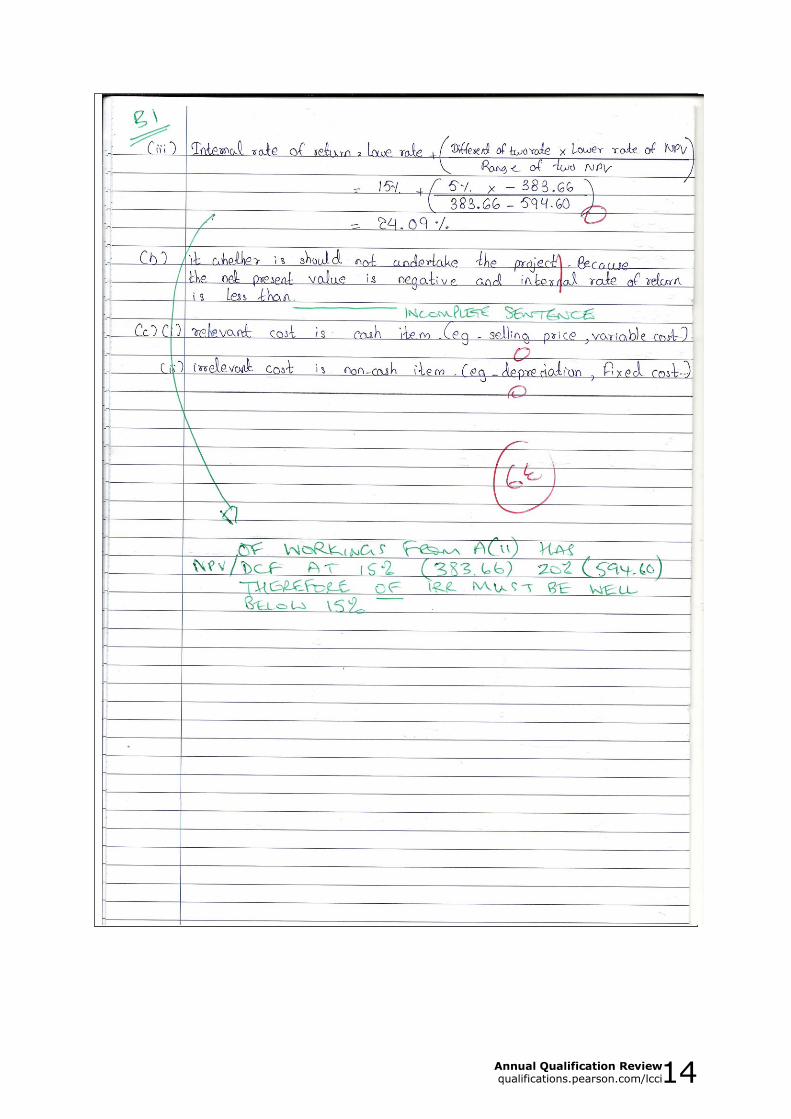

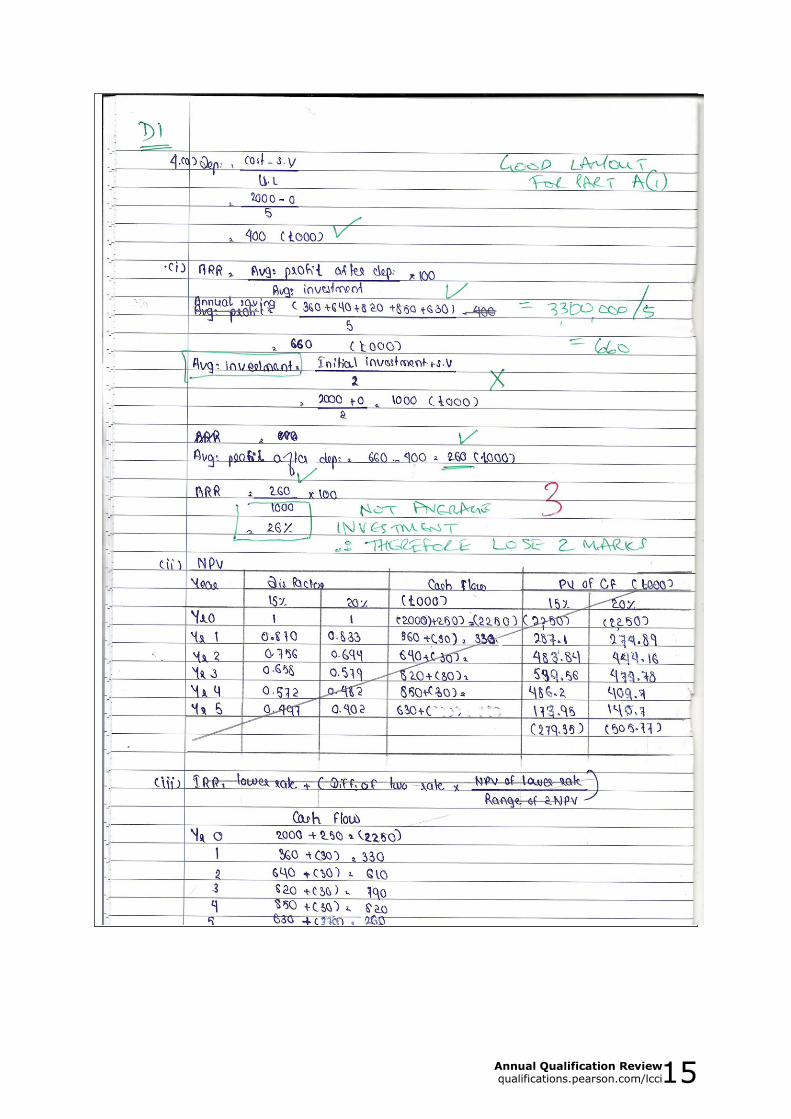

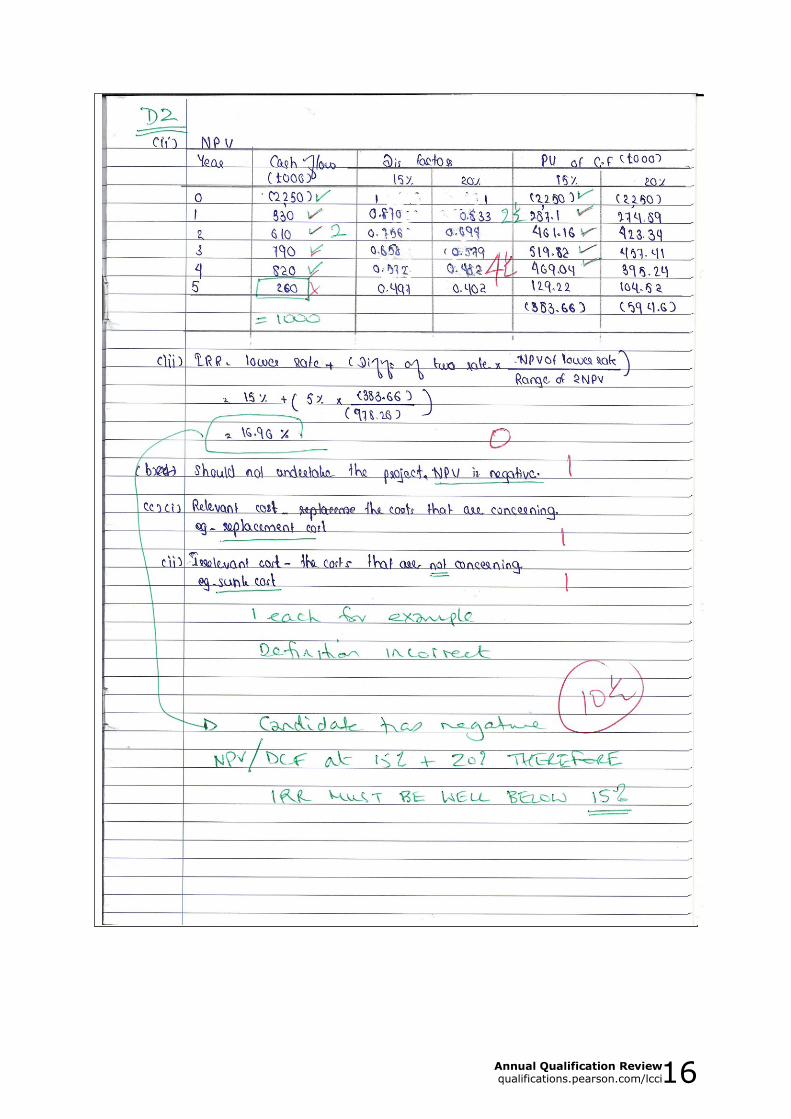

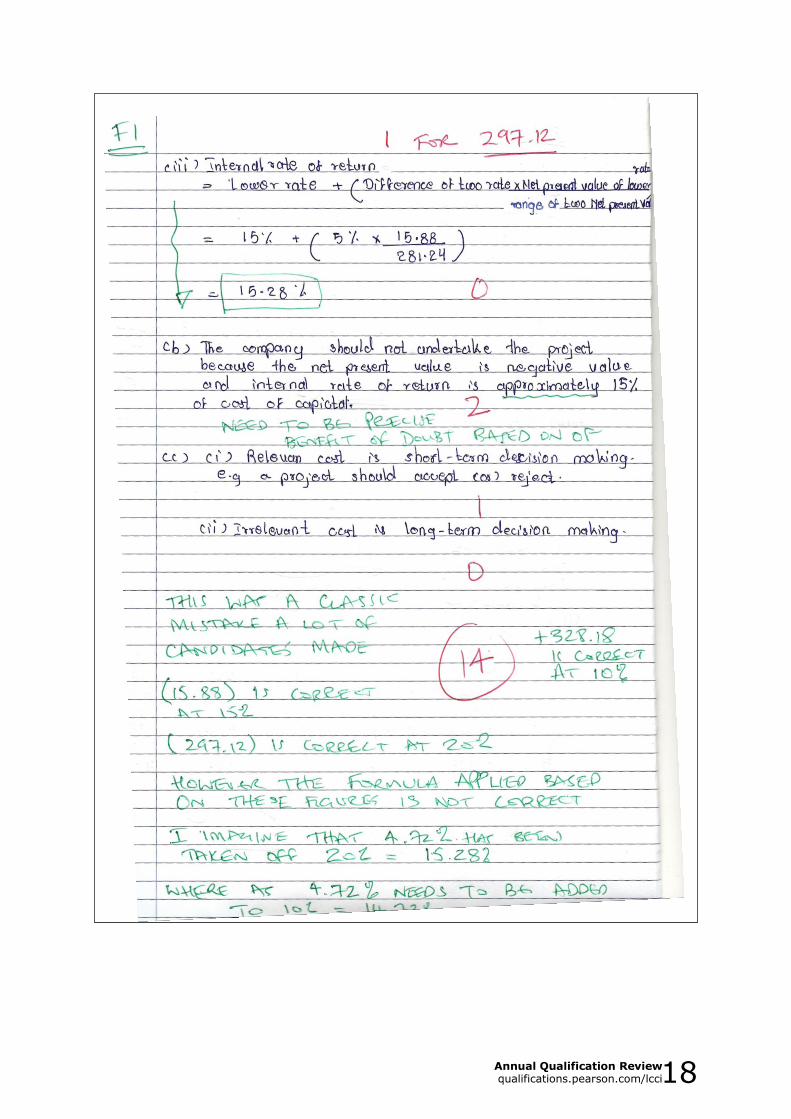

Q4 (Series 3) was very similar to the Series 2 question and presented exactly the same challenges.

Part (a)(i) asked for the ARR to be based on capital employed, and the

majority of candidates used the average investment, losing 2 marks.

On part (a)(ii) the majority of students couldn't calculate the net cash flow and

lost out on at least 4/6 marks

Once again, they were having to rely on the own figure rule for the three

marks on part (a)(iii). This was one question were quite a number of the calculations submitted by candidates showed they had no concept about the syllabus topic. Despite the question stating the asset cost £2.25m (£2m cost

and a further injection of £250k at the start of the project - which many students ignored) and 'forecast' cash flows totalling £3.55m at the start of the

project (year 0), students had discounted cash flows in the £millions.

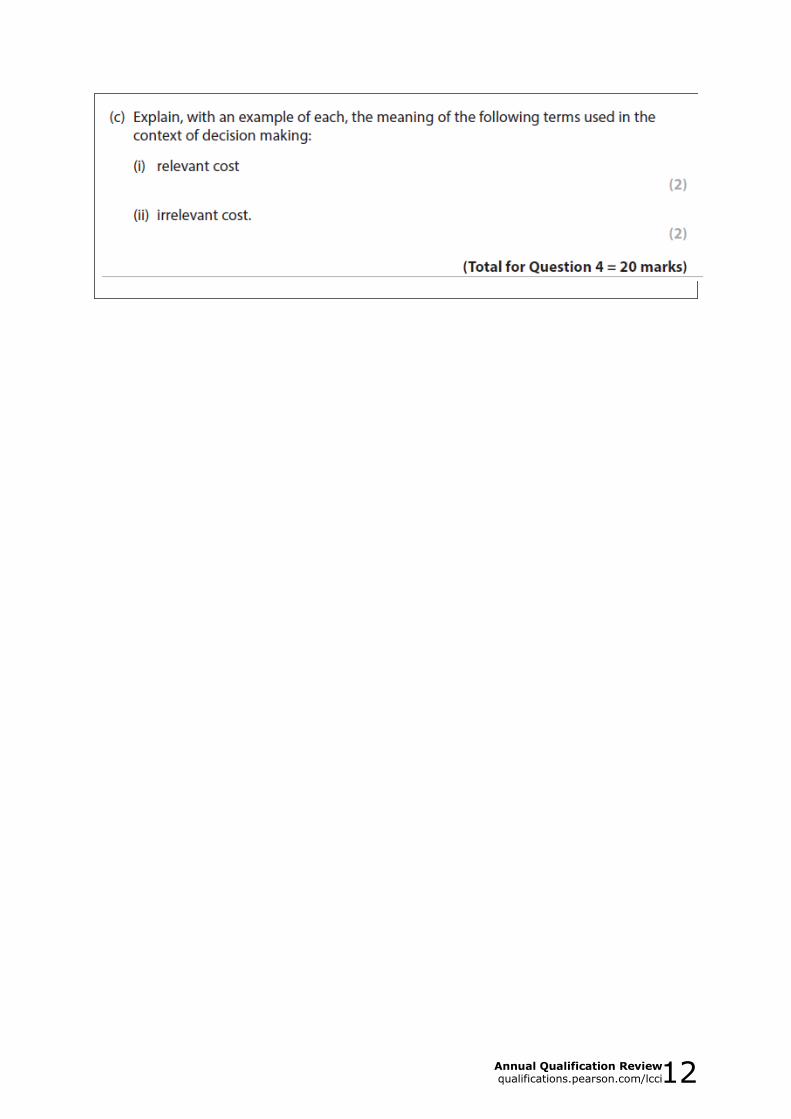

Q4 (Series 3) is featuring as the question with a variety of actual student responses, together with the Chief Examiner's comments on each answer

8 Performance evaluation

8.1 Explain why an enterprise may wish to decentralise

8.2 Define cost, profit and investment centres

8.3 Evaluate centres based on ROCE and RI (Series 2)

8.4 Contrast ROCE with RI (Series 2)

8.5 Calculate and interpret Profitability and use of Asset Ratios

8.6 The Balanced Scorecard (Series 2)

8.7 Financial and non-financial performance measures

8.6 Explain why transfer pricing is necessary

8.9 Calculate market and cost based transfer prices

Q5a (Series 2) asked students to calculate the ROCE and RI and was well

answered by the majority of candidates. Part (b) asked for the same calculations based on the division taking on an additional new investment.

10 Annual Qualification Review qualifications.pearson.com/lcci

Despite using the word 'additional' three times in the stem and once in the required section of the question, the majority of candidates calculated the

ROCE and RI for the new investment only.

Part (c) was relatively well answered, but very few candidates mentioned

anything significant for the four marks. The question asked for reasons why the Manager would be willing to undertake the new project, based on the calculations. This would suggest that they might not be willing to undertake

the project if it made a reduction in percentage terms on the ROCE. They might (conversely) be willing to undertake the project if it made some positive

residual income (in monetary terms). This particular question is testing the candidate's ability to understand the difference(s) between ROCE and Residual Income.

Part (c) was a narrative on the Balanced Scorecard. Very few candidates scored more than two marks. It could be that this is regarded as a 'wordy'

topic, which causes a problem for many candidates. Possibly, because this topic has appeared so infrequently, it might be being ignored by some candidates.

Further guidance

Centres should note that all the syllabus topics will be examined at some point.

In order to improve their performance and secure the minimum pass mark in

future examinations, candidates are advised to:

Have a clear understanding of the elements of the eight syllabus topics through formal instruction provided by reputable teaching institutions;

Learn the relevant managerial accounting concepts and terminologies in

order to adequately attempt the narrative parts of questions;

Practice past exam questions on a regular basis, under strict

examination condition;

Read the requirements of a question as these are designed to assist in

answering the question;

Plan the layout of an answer before beginning to carry out calculations;

Show clear workings in questions that require calculations.

A weakness for many candidates continues to be a lack of suitable workings. A further cause for concern seems to be that a lot of students (who are presumably good at Maths) are entering long calculations into their

mathematical calculators and then writing down the equation as the answer to the question. You will see examples of this in the section showing copies of

actual student responses.

Tutors should continue to make students aware that if an answer is correct

(without workings) the examiner will award the required marks. However, if the answer is incorrect, without 'adequate' workings, the examiner is not required to determine how the candidate arrived at that answer in an attempt

to award partial marks.

11 Annual Qualification Review qualifications.pearson.com/lcci

EXAMPLES OF CANDIDATE RESPONSES

12 Annual Qualification Review qualifications.pearson.com/lcci

13 Annual Qualification Review qualifications.pearson.com/lcci

14 Annual Qualification Review qualifications.pearson.com/lcci

15 Annual Qualification Review qualifications.pearson.com/lcci

16 Annual Qualification Review qualifications.pearson.com/lcci

17 Annual Qualification Review qualifications.pearson.com/lcci

18 Annual Qualification Review qualifications.pearson.com/lcci

Pearson Education Ltd

80 Strand London

WC2R 0RL

Tel. +44 (0) 247 651 8951 Fax. +44 (0) 247 651 6566

Email. [email protected] qualifications.pearson.com/lcci