management & cost accounting - se 4.pdf · profit calculation : marginal costing marginal...

TRANSCRIPT

MANAGEMENT & COST ACCOUNTINGLO 2: LESSON 4 : MARGINAL VS. ABSORPTION COSTING PROFIT CALCULATIONS

INTRODUCTION TO AN INCOME STATEMENT

Income statement is prepared to assess the profit or loss derived by an organisation.

It includes three main elements;

Revenues/ Turnover : refers to a company’s actual or promised cash inflows resulting from

completed sale of the company’s products or the satisfactory delivery of its services.

Expenses : refers to the benefits consumed or used up in the process of earning revenues.

When preparing income statement, all the expenses are required to be deducted from

revenues to determine profit or loss of the accounting period.

Gains and losses : A gain is the net revenue of a company earned as a result of a business

transaction and vice versa.

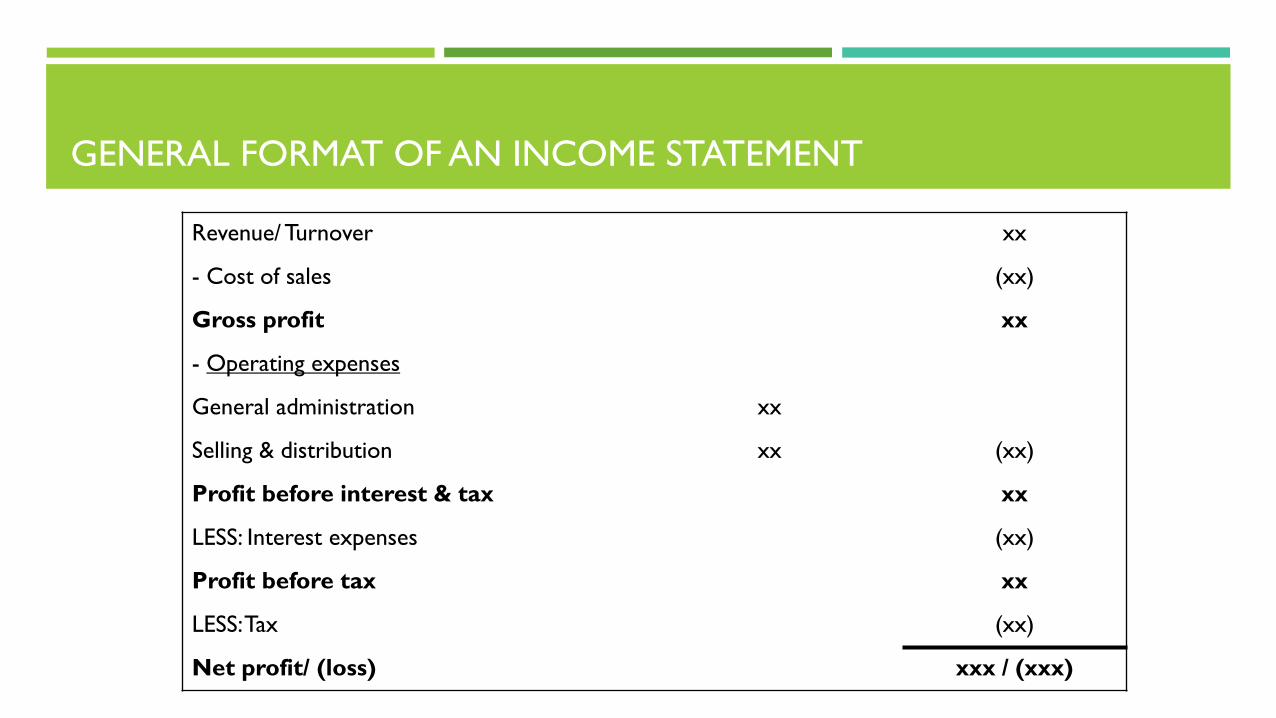

GENERAL FORMAT OF AN INCOME STATEMENT

Revenue/ Turnover xx

- Cost of sales (xx)

Gross profit xx

- Operating expenses

General administration xx

Selling & distribution xx (xx)

Profit before interest & tax xx

LESS: Interest expenses (xx)

Profit before tax xx

LESS:Tax (xx)

Net profit/ (loss) xxx / (xxx)

PROFIT CALCULATION : MARGINAL COSTING

Marginal costing is an alternative method of costing to

absorption costing.

In marginal costing ONLY variable costs are charged as cost of

sale and contribution is calculated i.e. Sales revenue –Variable

cost of sales.

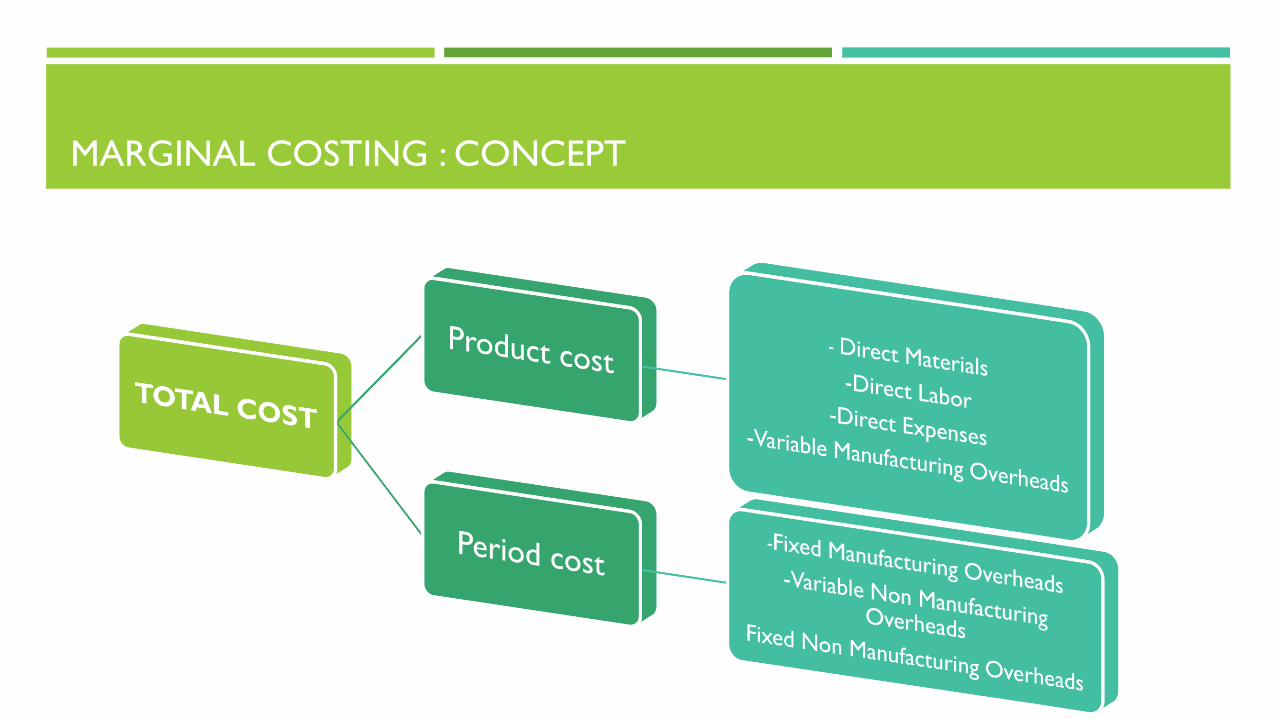

MARGINAL COSTING : CONCEPT

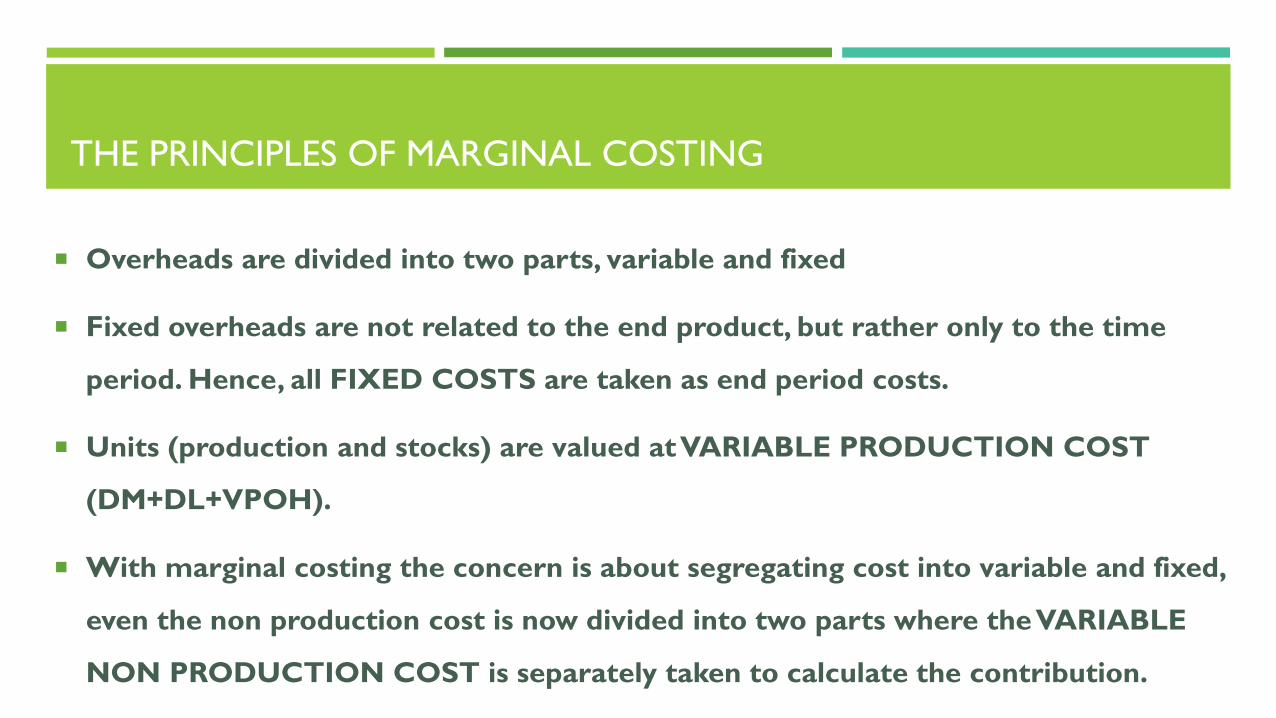

THE PRINCIPLES OF MARGINAL COSTING

Overheads are divided into two parts, variable and fixed

Fixed overheads are not related to the end product, but rather only to the time

period. Hence, all FIXED COSTS are taken as end period costs.

Units (production and stocks) are valued at VARIABLE PRODUCTION COST

(DM+DL+VPOH).

With marginal costing the concern is about segregating cost into variable and fixed,

even the non production cost is now divided into two parts where the VARIABLE

NON PRODUCTION COST is separately taken to calculate the contribution.

MARGINAL COSTING : CONCEPT

The MARGINAL PRODUCTION COST per unit of an item usually consists the

following.

Direct materials

Direct labour

Variable PRODUCTION overheads

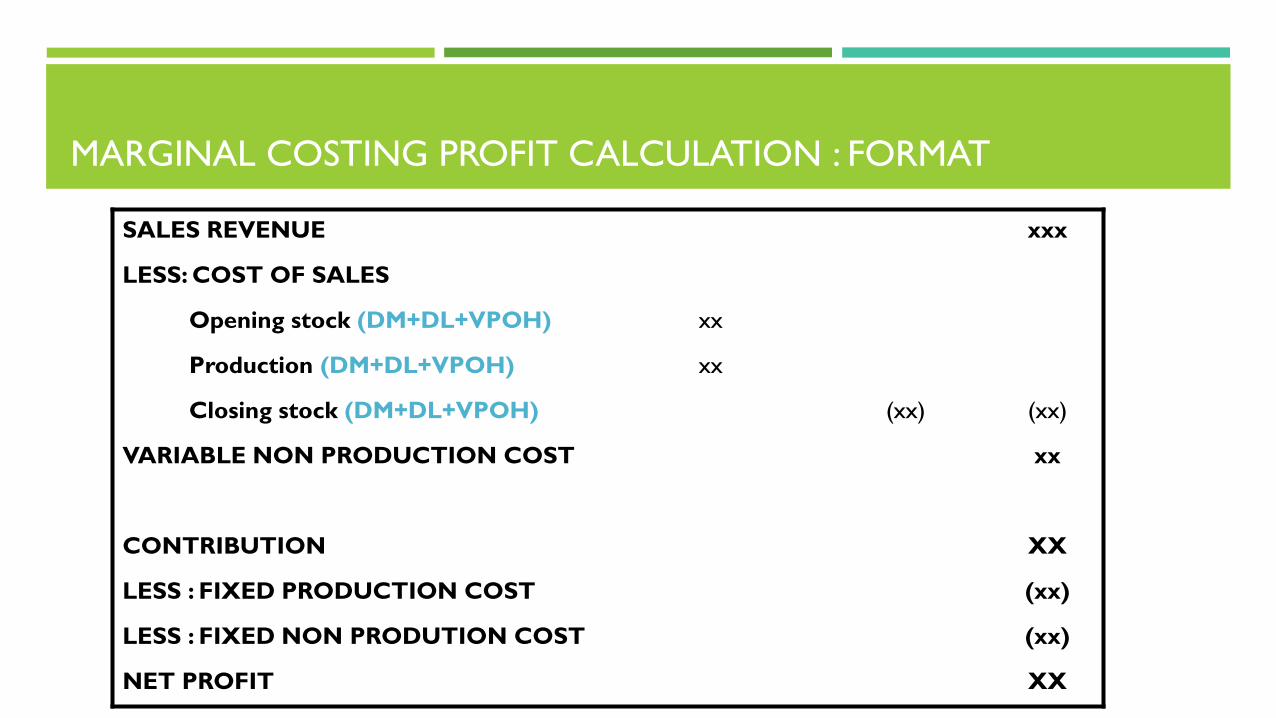

MARGINAL COSTING PROFIT CALCULATION : FORMAT

SALES REVENUE xxx

LESS: COST OF SALES

Opening stock (DM+DL+VPOH) xx

Production (DM+DL+VPOH) xx

Closing stock (DM+DL+VPOH) (xx) (xx)

VARIABLE NON PRODUCTION COST xx

CONTRIBUTION XX

LESS : FIXED PRODUCTION COST (xx)

LESS : FIXED NON PRODUTION COST (xx)

NET PROFIT XX

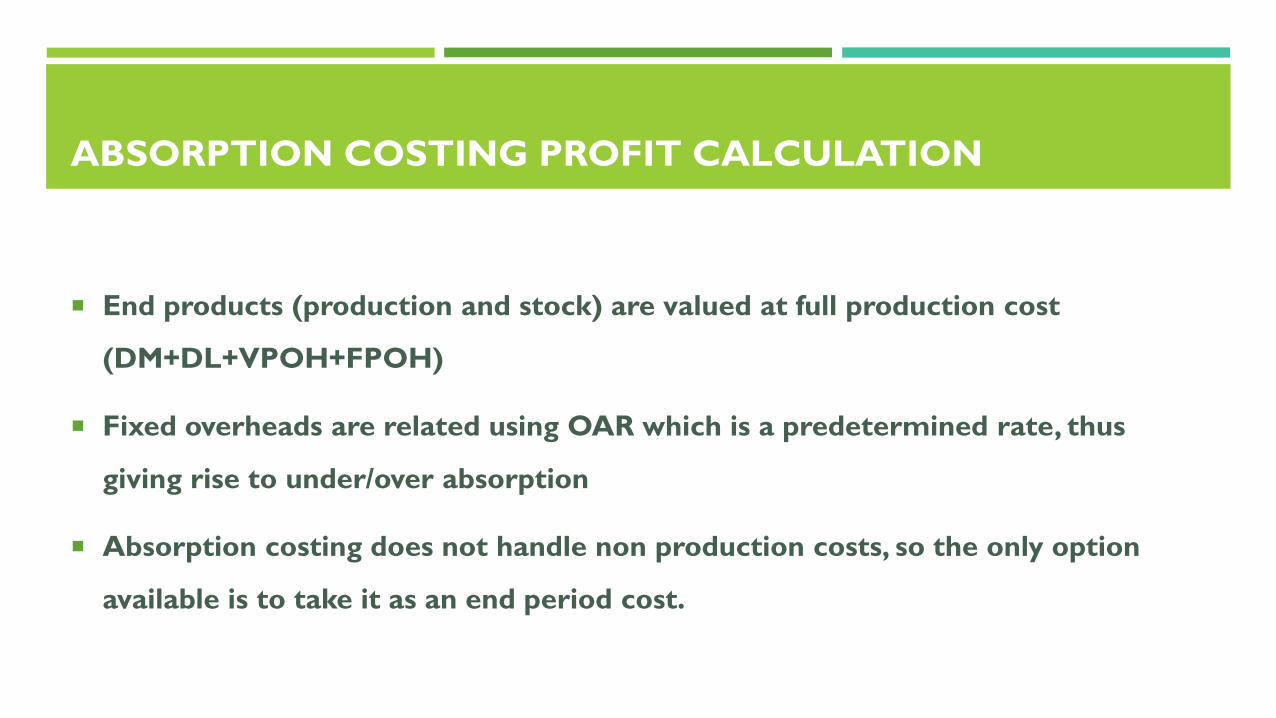

ABSORPTION COSTING PROFIT CALCULATION

End products (production and stock) are valued at full production cost

(DM+DL+VPOH+FPOH)

Fixed overheads are related using OAR which is a predetermined rate, thus

giving rise to under/over absorption

Absorption costing does not handle non production costs, so the only option

available is to take it as an end period cost.

ABSORPTION COSTING: CONCEPT

ABSORPTION COSTING PROFIT CALCULATION : FORMAT

SALES REVENUE xxx

LESS: COST OF SALES

Opening stock (DM+DL+VPOH+FPOH) xx

Production (DM+DL+VPOH+FPOH) xx

Closing stock (DM+DL+VPOH+FPOH) (xx) (xx)

GROSS PROFIT xx

ADJUSTMENT (UNDER)/ OVER ABSORPTION (xx)/xx

LESS : NON PRODUCTION

-VARIABLE COST (xx)

- FIXED COST (xx)

NET PROFIT XX

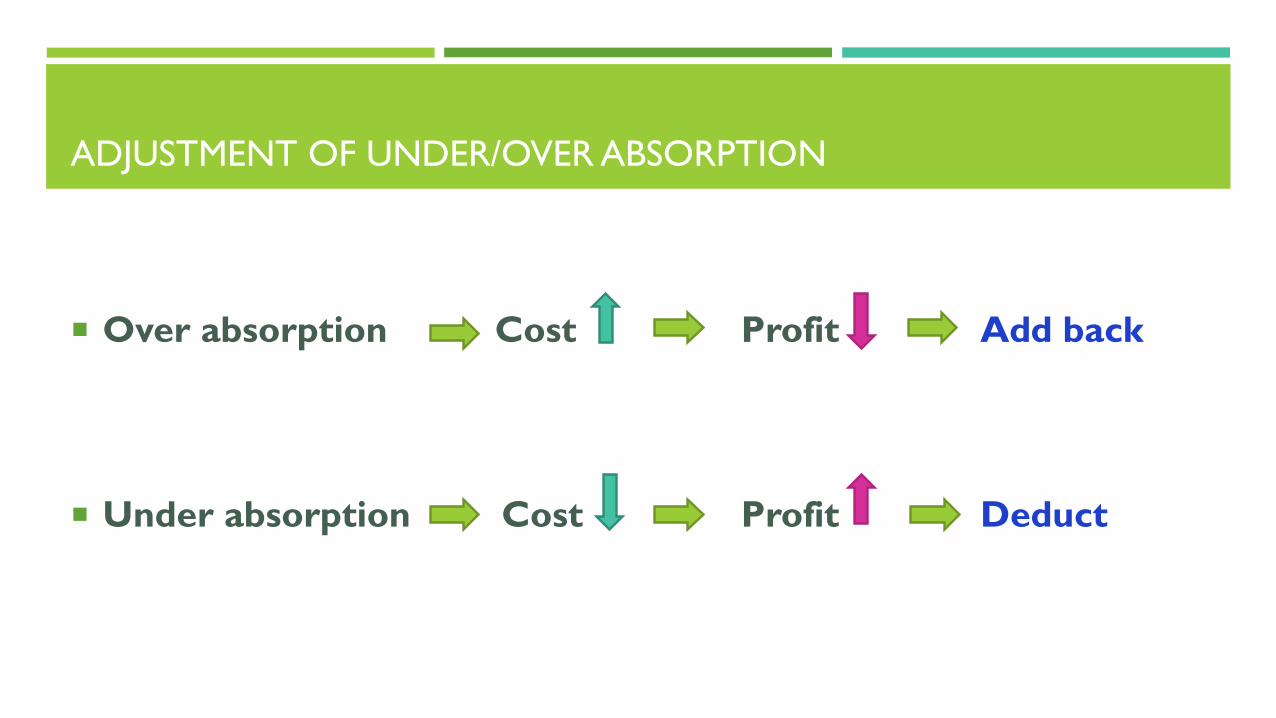

ADJUSTMENT OF UNDER/OVER ABSORPTION

Over absorption Cost Profit Add back

Under absorption Cost Profit Deduct

RECONCILIATION OF ABSORPTION AND MARGINAL COSTING

PROFITS

In spite of the fact the same information was used in arriving at the profit

figure, under MC and AC two different profit figures are achieved.

This is because of the two different techniques being applied

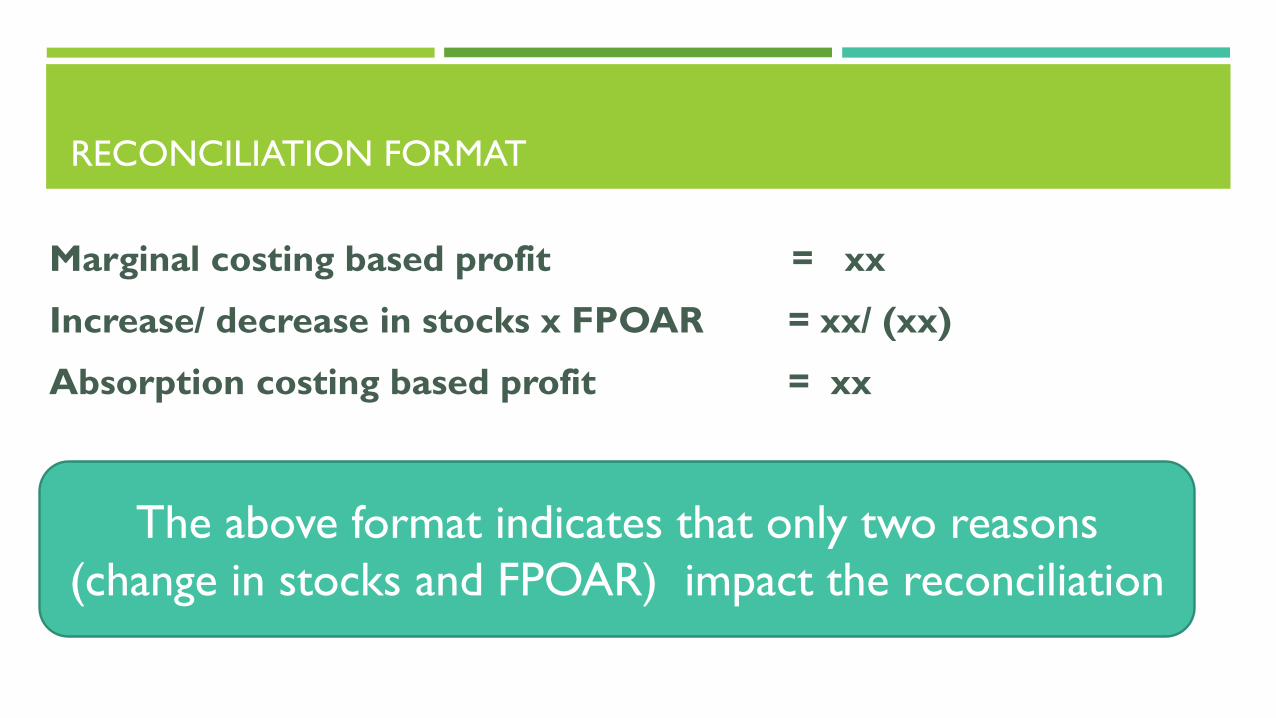

RECONCILIATION FORMAT

Marginal costing based profit = xx

Increase/ decrease in stocks x FPOAR = xx/ (xx)

Absorption costing based profit = xx

The above format indicates that only two reasons

(change in stocks and FPOAR) impact the reconciliation

RECONCILIATION OF ABSORPTION AND MARGINAL COSTING

PROFITS

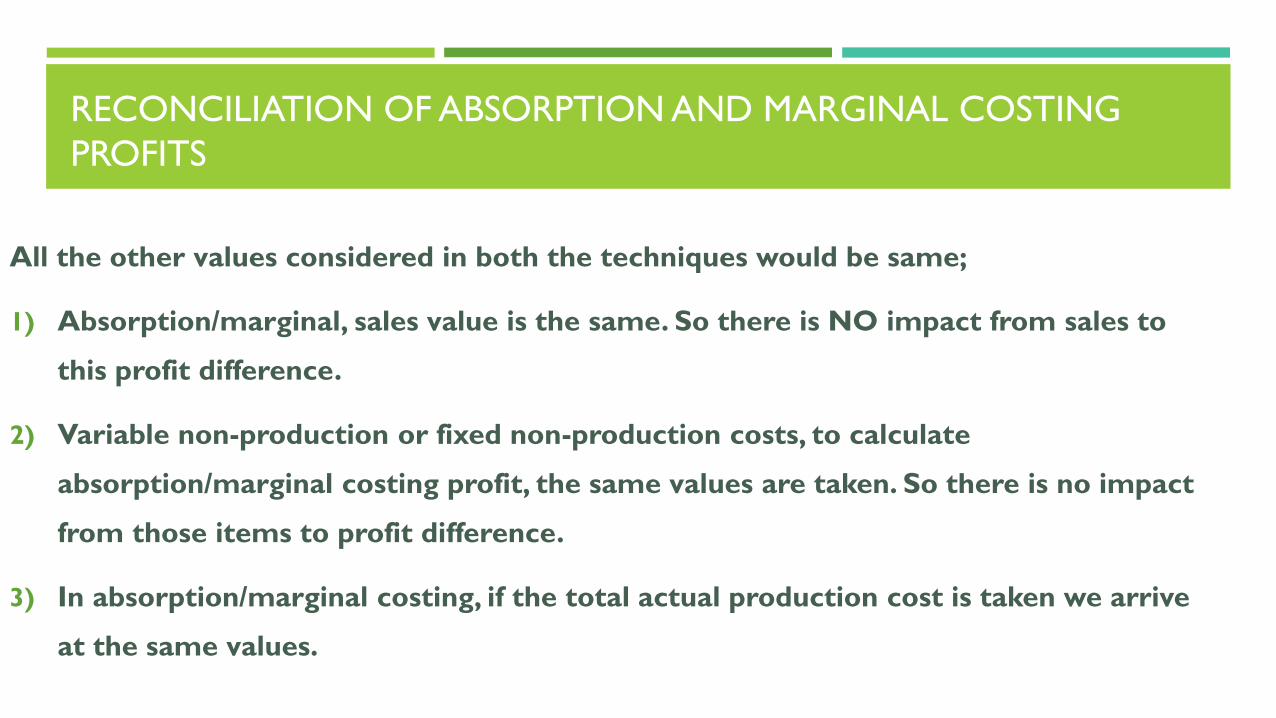

All the other values considered in both the techniques would be same;

1) Absorption/marginal, sales value is the same. So there is NO impact from sales to

this profit difference.

2) Variable non-production or fixed non-production costs, to calculate

absorption/marginal costing profit, the same values are taken. So there is no impact

from those items to profit difference.

3) In absorption/marginal costing, if the total actual production cost is taken we arrive

at the same values.

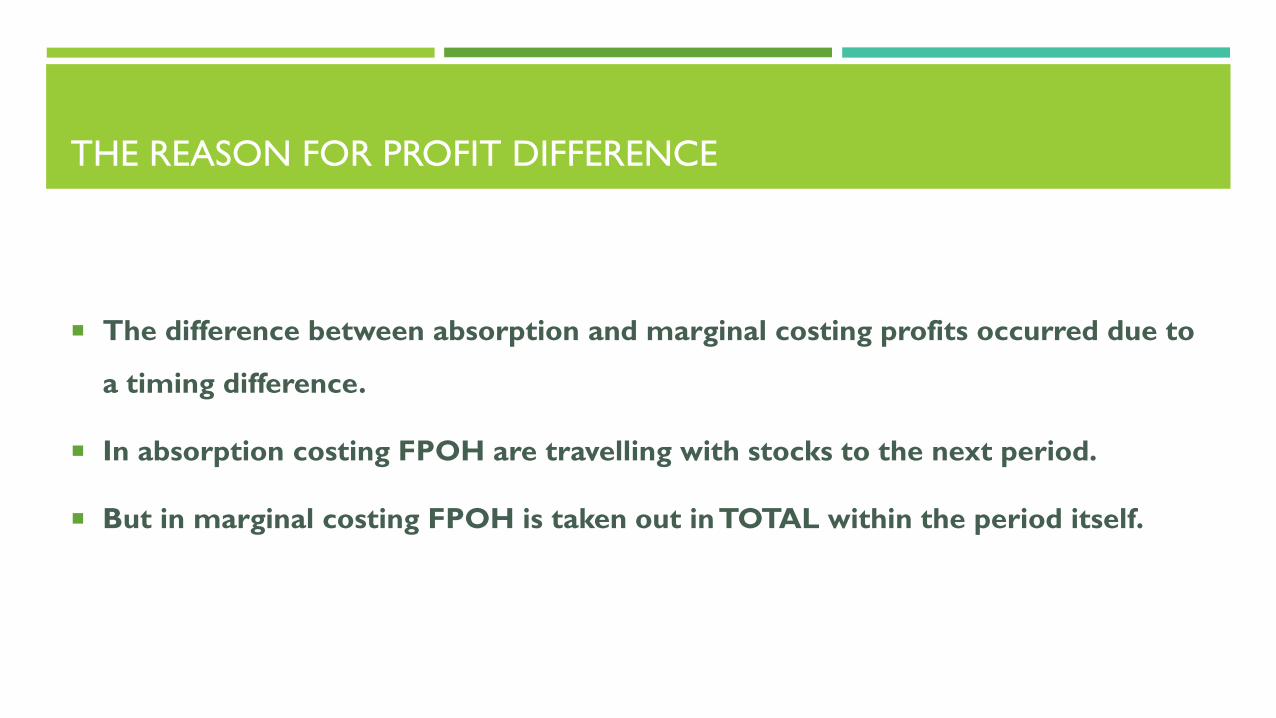

THE REASON FOR PROFIT DIFFERENCE

The difference between absorption and marginal costing profits occurred due to

a timing difference.

In absorption costing FPOH are travelling with stocks to the next period.

But in marginal costing FPOH is taken out in TOTAL within the period itself.

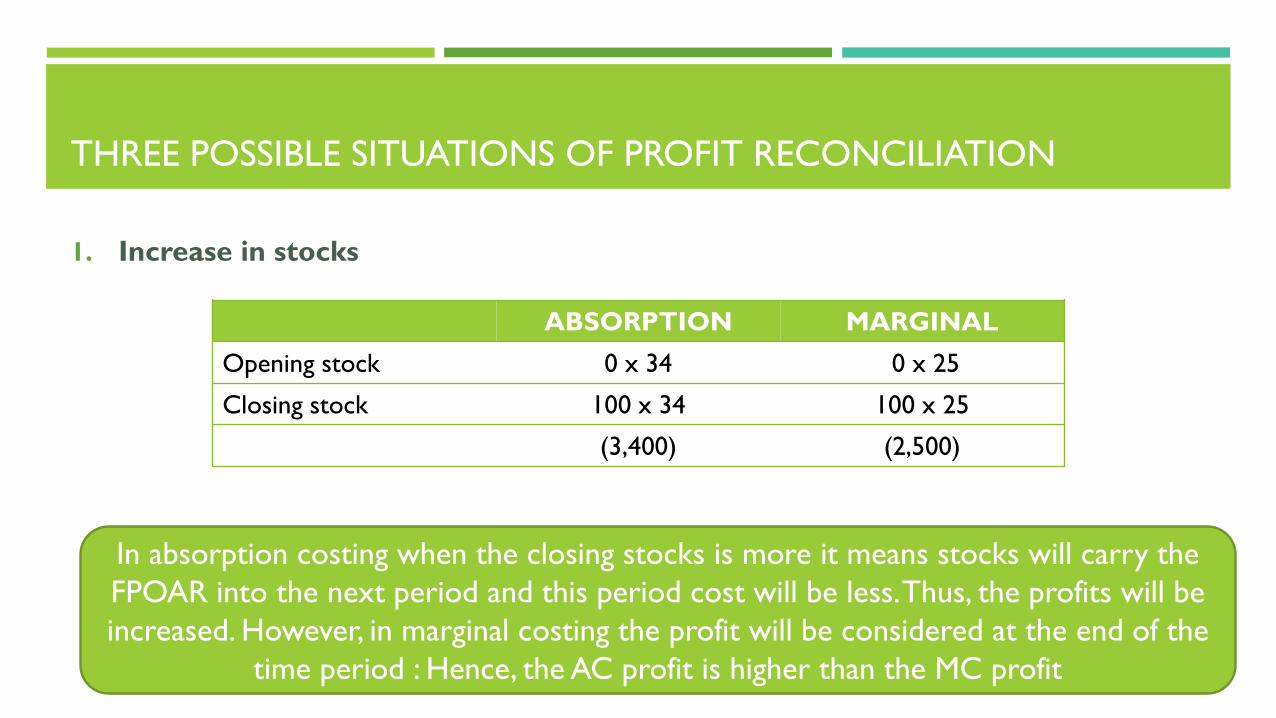

THREE POSSIBLE SITUATIONS OF PROFIT RECONCILIATION

1. Increase in stocks

ABSORPTION MARGINAL

Opening stock 0 x 34 0 x 25

Closing stock 100 x 34 100 x 25

(3,400) (2,500)

In absorption costing when the closing stocks is more it means stocks will carry the

FPOAR into the next period and this period cost will be less. Thus, the profits will be

increased. However, in marginal costing the profit will be considered at the end of the

time period : Hence, the AC profit is higher than the MC profit

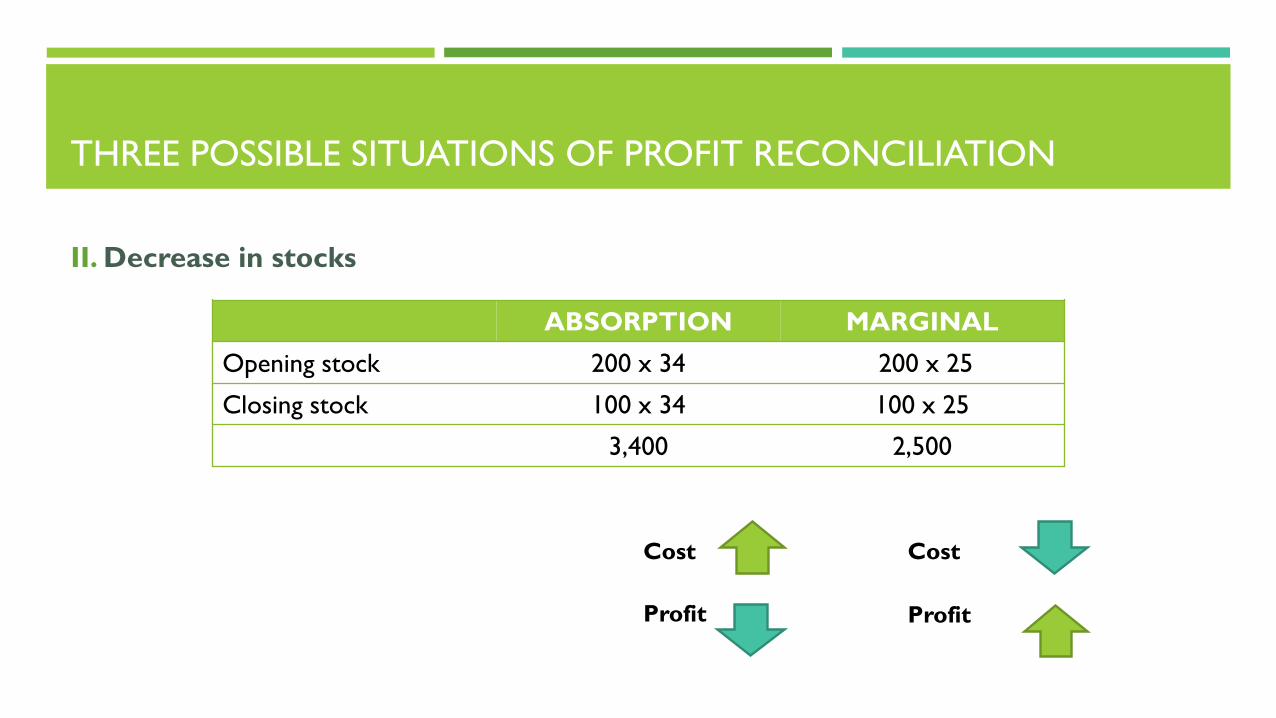

THREE POSSIBLE SITUATIONS OF PROFIT RECONCILIATION

II. Decrease in stocks

ABSORPTION MARGINAL

Opening stock 200 x 34 200 x 25

Closing stock 100 x 34 100 x 25

3,400 2,500

Cost

Profit

Cost

Profit

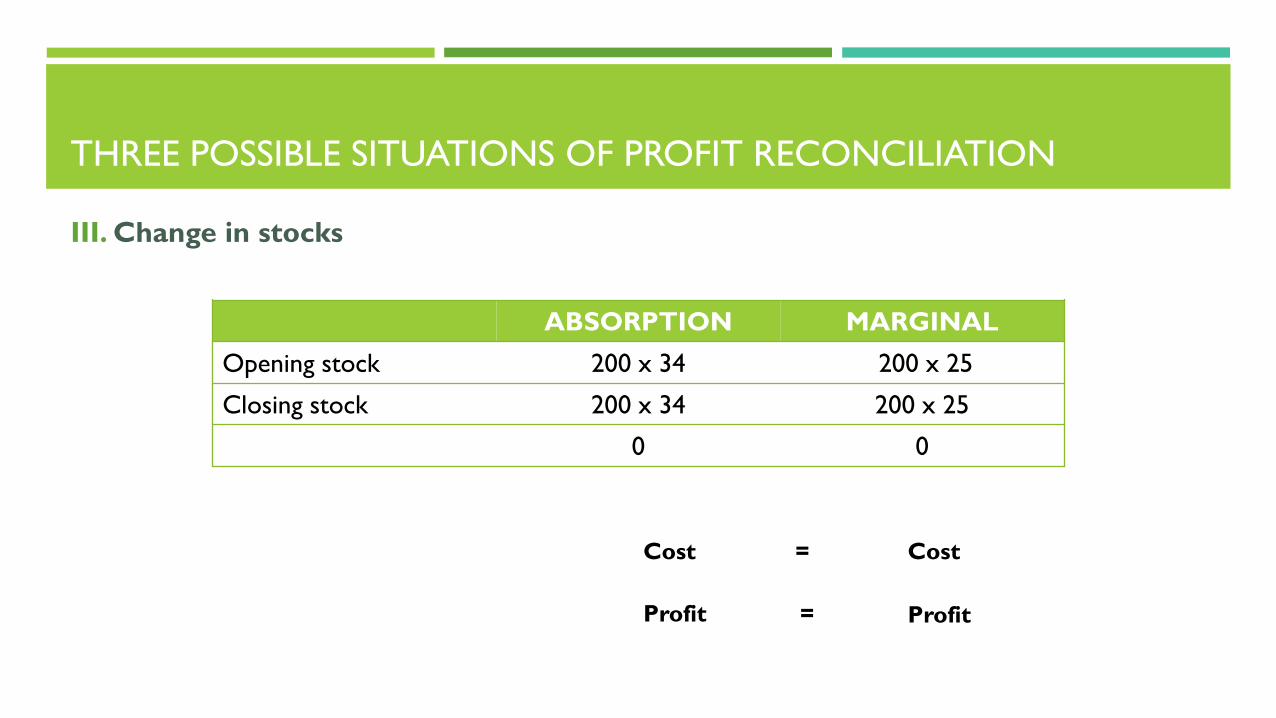

THREE POSSIBLE SITUATIONS OF PROFIT RECONCILIATION

III. Change in stocks

ABSORPTION MARGINAL

Opening stock 200 x 34 200 x 25

Closing stock 200 x 34 200 x 25

0 0

Cost = Cost

Profit = Profit

THANK YOU!