peoplesoft/oracle merger analysis product review … merger analysis product review and strategic...

TRANSCRIPT

PeopleSoft/Oracle Merger Analysis Product Review and Strategic Direction

Executive Overview

April 14, 2006

2© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory

4. Oracle’s Migration Strategy for PeopleSoft Customers

5. SAP’s Migration Strategy for PeopleSoft Customers

6. Analysis of Financial / Business Impact to Client

7. Recommendation and Migration Strategy

8. Appendix

3© 2006 SpearMC Management Consulting, Inc.

PeopleSoft / Oracle Merger Background• June 2003 – Oracle falls to #3 slot in ERP marketplace after PeopleSoft pulls off successful bid for JDE;

• Late 2003 – PeopleSoft Acquisition Rationale is presented to Oracle Board of Directors that covers upsides and drawbacks in regards to a potential merger with PeopleSoft, which now includes JD Edwards;

Combination creates stronger ability to successfully

compete with SAP and Siebel;

Complementary expertise – Oracle in SCM, FIN and

MFG. PSFT in HRMS, CRM, Higher Ed and Services;

Addition of 4,900 PeopleSoft customers (mostly large-

scale) and 6,650 JDE customers (mostly mid-market);

Creates a stronger mid-market presence;

Encourage more PeopleSoft and JDE users to switch

from IBM and Microsoft databases to Oracle.

Upside

Forces the combined entity to support four or more

unique application suites/platforms in current release:

PeopleSoft Enterprise (web-based)

Oracle E-Business (java / web-based)

JDE World (AS/400) & OneWorld (client/server)

Merges three competing sales operations – possibly

causing significant sales disruptions;

PeopleSoft still has a significant number (~35%) of

customers running on Version 8.0 and 7.x;

Significant personnel changes and restructuring

Drawbacks

• December 2004 – PeopleSoft merges with Oracle: Oracle completes acquisition of PeopleSoft for $10.3 billion USD.

4© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory

4. Oracle’s Migration Strategy for PeopleSoft Customers

5. SAP’s Migration Strategy for PeopleSoft Customers

6. Analysis of Financial / Business Impact to Client

7. Recommendation and Migration Strategy

8. Appendix

5© 2006 SpearMC Management Consulting, Inc.

Big-3 Application Vendor Landscape

Enterprise Applications >>

Small and Mid-Market

(<$500M) Applications >>

Desktop Platform >>

Middleware >>

Databases >>

Operating System(s) >>

Application Vendor >>

Oracle continues to focus on Linux, Unix and J2EE – and away from Microsoft;

PeopleSoft will continue to be marketed on a limited basis until Oracle Fusion is ready for primetime distribution release (2008), however functionality and support will grow to favor running on an Oracle 9i or 10g database;

SAP may be in a position to capture disenfranchised PeopleSoft MS-SQL and IBM DB2 customers;

Oracle/SAP duopoly may force Microsoft (MS-Dynamics) into Enterprise Application market by 2008 or 2009.

Impact of PS/Oracle

Merger

Oracle11i, JDE, PeopleSoft

Oracle Small Business

Suite (<$100M)

Interoperable: Partner with

StarOffice from Sun

AppServer 9iAS, J2EE,

9iJDeveloper, Fusion

Oracle, MS-SQL, IBM, etc.

Interoperable: Linux focus

Oracle / PeopleSoft SAP Microsoft

Enterprise R/3 & mySAP

BusinessOne (<$250M) &

All-In-One (<$500M)

Interoperable

Net Weaver

Oracle, MS-SQL, IBM

Interoperable

Not Currently Available

Axapta, Great Plains,

Navision, Solomon

MS-Office

.NET

MS-SQL

MS-Windows

6© 2006 SpearMC Management Consulting, Inc.

• Overall Industry R&D and Marketing spending are not justified at current levels of license revenue:

• Maintenance revenue, not new license fees, currently drive profitability of most application vendors;

• Development and sales of a new release has a negative ROI for many application vendors.

• Acquisition of companies with customers on older or obsolete platforms is the current trend:

• This approach is often more economical than competing for those same customers;

• Ultimately leads to an improved chance to migrate customers to a common platform and release.

• Better integrated products are better for customers, while capturing more revenue for vendors:

• For example – Oracle’s future ERP releases may require customers to run on Oracle databases;

• SAP and Microsoft are also moving in this direction.

• Customers should ultimately benefit from more-integrated, easy-to-deploy products…but with many suffering near-term disruptions;

• Current JD Edwards and PeopleSoft customers should plan as if a migration to Oracle Fusion will be a major upgrade to new applications, middleware and database platforms;

• Investments in the adaptation of new business processes may be substantial;

• IT resources may require updates to their technical skills if they have not already deployed the Oracle technology stack;

• Gap analysis for new capabilities will be required to determine if current customizations are still needed, the effort to migrate existing customizations, and if new customizations will be required.

Big-3 Vendor Landscape – Market Dynamics

7© 2006 SpearMC Management Consulting, Inc.

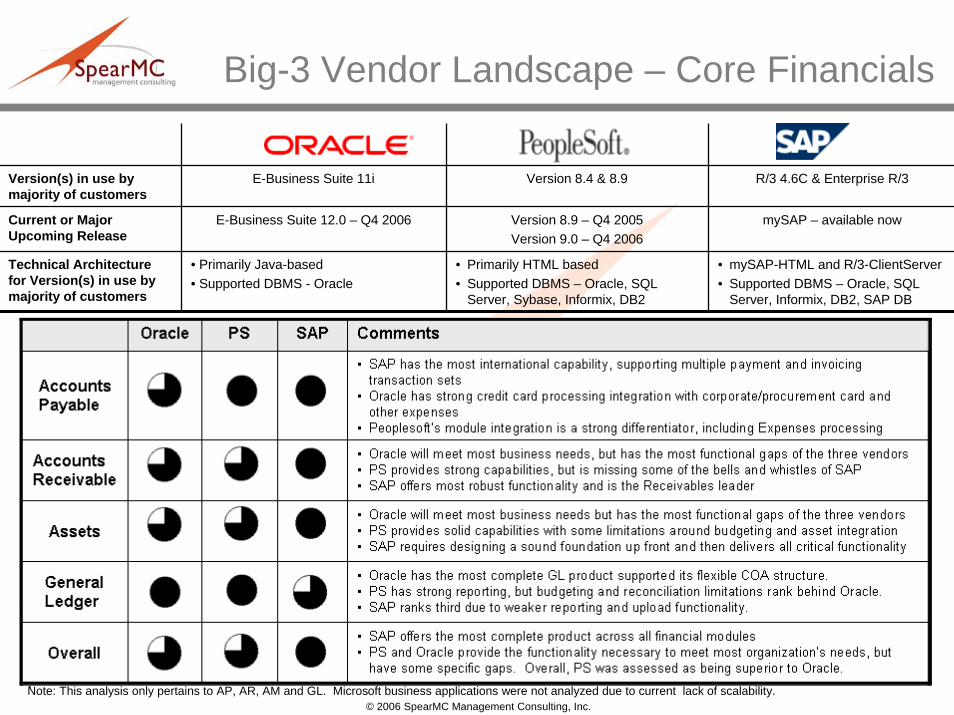

• mySAP-HTML and R/3-ClientServer• Supported DBMS – Oracle, SQL

Server, Informix, DB2, SAP DB

• Primarily HTML based• Supported DBMS – Oracle, SQL

Server, Sybase, Informix, DB2

• Primarily Java-based• Supported DBMS - Oracle

Technical Architecture for Version(s) in use by majority of customers

mySAP – available nowVersion 8.9 – Q4 2005Version 9.0 – Q4 2006

E-Business Suite 12.0 – Q4 2006Current or Major Upcoming Release

R/3 4.6C & Enterprise R/3Version 8.4 & 8.9E-Business Suite 11iVersion(s) in use by majority of customers

Big-3 Vendor Landscape – Core Financials

Note: This analysis only pertains to AP, AR, AM and GL. Microsoft business applications were not analyzed due to current lack of scalability.

8© 2006 SpearMC Management Consulting, Inc.

• Oracle – Customer success hinges on ability to support and migrate applications:

• Over 23,000 ERP customers running different versions of Oracle, PeopleSoft, JD Edwards and Retek. The current application suites will need to be supported and eventually migrated;

• Looking to aggressively close the gap between Oracle and SAP in the ERP marketplace;

• Customers that adopt or use Oracle middleware and databases to support Oracle applications will have a lower Total Cost of Ownership vs. customers staying with MS-SQL, IBM or other databases;

• Oracle will continue to grow their own internal consulting force to meet integration demand.

• SAP – #1 ERP vendor with 65% of Fortune 500 and majority of Global 2000 companies:

• Mid-market organizations of growing importance, with 30% of sales coming from companies with less than $1 billion in revenues. 66% of SAP’s 20,000 ERP customers have <$500 million in sales;

• Current upgrade cycle to mySAP from R/3 versions is in full-swing – expected completion in 2008;

• Strong track record of customer retention (R/2 to R/3 upgrade cycle kept 97% of customers);

• SAP remains product-focused and relies mainly on systems integrators for direct customer contact.

• Microsoft – Small & Mid-sized Business market leader capitalizing on recent acquisitions:

• Microsoft Business Solutions (MBS) targets small (<$100M) and mid-sized businesses (<$500M);

• MBS customers are spread across four entirely different business applications – making a seamless upgrade path to an eventual ERP product (Project Green) unlikely;

• Customers enjoy full integration with MS-Office, Windows, MS-SQL and .NET platform.

Big-3 Vendor Landscape

9© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory (not included)

4. Oracle’s Migration Strategy for PeopleSoft Customers

PeopleSoft Retirement and Release Schedule

Oracle Applications / Fusion

5. SAP’s Migration Strategy for PeopleSoft Customers

6. Analysis of Financial / Business Impact to Client

7. Recommendation and Migration Strategy

10© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory

4. Oracle’s Migration Strategy for PeopleSoft Customers

PeopleSoft Retirement and Release Schedule

Oracle Applications / Fusion

5. SAP’s Migration Strategy for PeopleSoft Customers

6. Analysis of Financial / Business Impact to Client

7. Recommendation and Migration Strategy

11© 2006 SpearMC Management Consulting, Inc.

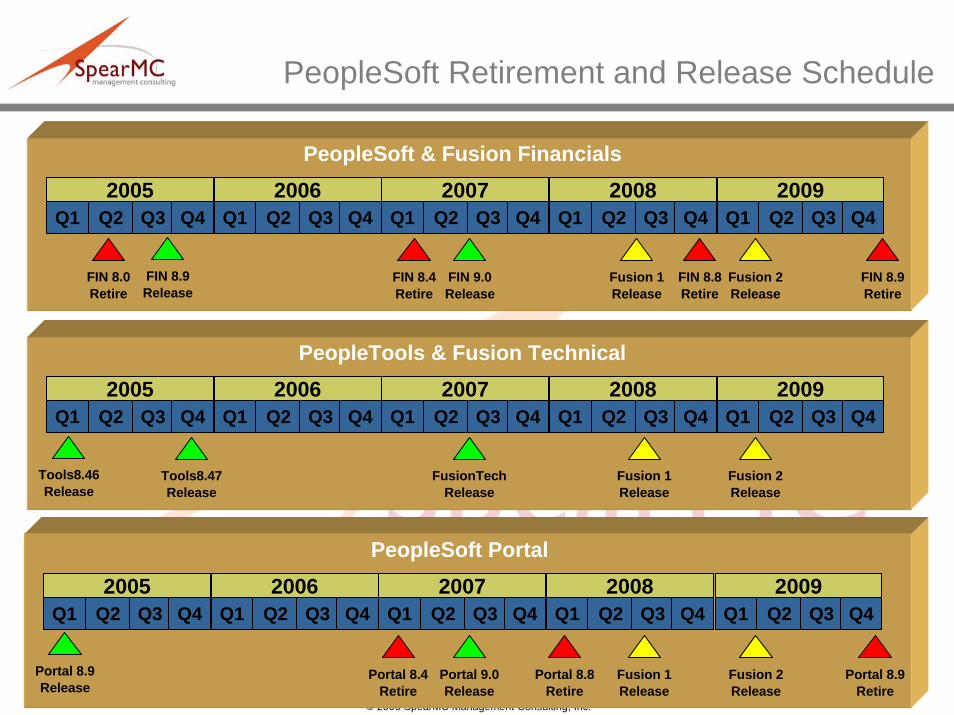

PeopleSoft Retirement and Release Schedule

2005Q1

FIN 8.9Release

PeopleSoft & Fusion Financials

Q2 Q3 Q42006

Q1 Q2 Q3 Q42007

Q1 Q2 Q3 Q42008

Q1 Q2 Q3 Q42009

Q1 Q2 Q3 Q4

FIN 8.4Retire

FIN 8.9Retire

FIN 9.0Release

2005Q1

Portal 8.9Release

PeopleSoft Portal

Q2 Q3 Q42006

Q1 Q2 Q3 Q42007

Q1 Q2 Q3 Q42008

Q1 Q2 Q3 Q42009

Q1 Q2 Q3 Q4

Portal 8.9Retire

Portal 9.0Release

Fusion 1Release

Fusion 2Release

Fusion 2Release

FIN 8.0Retire

Fusion 1Release

2005Q1

PeopleTools & Fusion Technical

Q2 Q3 Q42006

Q1 Q2 Q3 Q42007

Q1 Q2 Q3 Q42008

Q1 Q2 Q3 Q42009

Q1 Q2 Q3 Q4

Fusion 1Release

Fusion 2Release

Tools8.46Release

FusionTechRelease

Portal 8.4Retire

Tools8.47Release

Portal 8.8Retire

FIN 8.8Retire

12© 2006 SpearMC Management Consulting, Inc.

PeopleSoft Retirement and Release Schedule

2005Q1

HR 8.9(Q4/04)

PeopleSoft HRMS

Q2 Q3 Q42006

Q1 Q2 Q3 Q42007

Q1 Q2 Q3 Q42008

Q1 Q2 Q3 Q42009

Q1 Q2 Q3 Q4

HR 8.9Retire

HR 9.0Release

2005Q1

CRM 8.9(Q2/04)

PeopleSoft CRM

Q2 Q3 Q42006

Q1 Q2 Q3 Q42007

Q1 Q2 Q3 Q42008

Q1 Q2 Q3 Q42009

Q1 Q2 Q3 Q4

CRM 8.9Retire

CRM 9.0Release

2005Q1

EPM 8.9Release

PeopleSoft EPM

Q2 Q3 Q42006

Q1 Q2 Q3 Q42007

Q1 Q2 Q3 Q42008

Q1 Q2 Q3 Q42009

Q1 Q2 Q3 Q4

EPM 8.9Retire

EPM 9.0Release

HR 8.3Retire

CRM8.1Retire

EPM8.3Retire

CRM8.4Retire

CRM 8.8Retire

EPM8.8Retire

HR 8.8Retire

Fusion 1Release

Fusion 2Release

Fusion 1Release

Fusion 2Release

Fusion 1Release

Fusion 2Release

13© 2006 SpearMC Management Consulting, Inc.

• Oracle will follow PeopleSoft’s Product Roadmap and Retirement Schedule: Following PeopleSoft’s current support policy and roadmaps, Oracle has pledged to maintain the following support terms:

• Four years of support from the general availability date for new patches and fixes, five years of support for new upgrade scripts (e.g. FIN 8.4/8.8 to FIN 9.0), and six years of support for new tax and regulatory changes.

• PeopleSoft customers can and will run on retired products: While support for new patches and fixes ends after four years from the general availability date – this does not necessarily force a customer into upgrading to a supported release.

• For example: Company is on a supported release of PeopleSoft Financials Version 8.4, slated to be retired in March 2007. While Financials Version 8.9 will be released in August 2005, it may make more sense for Client to hold-off on upgrading until Financials Version 9.0 is released in the late-2006/early-2007 timeframe. Following the current support schedule, scripts to upgrade from 8.4 to 9.0 (or the most current release at the time) will be made available until March 2007.

• Current version of PeopleTools 8.x will not be upgraded: In line with Oracle’s push to develop Fusion architecture, the current release of PeopleTools 8.x will be last version of Tools to be released.

• Customer demand may necessitate a supported Version 8.4 to Fusion upgrade path: While Oracle states that Version 8.9 will be the first release upgradeable to Fusion (Oracle’s eventual replacement for the PeopleSoft product line) – roughly 85% of all PeopleSoft Financial customers are still on Version 8.4 or a prior release (e.g. 8.0 or 7.x).

PeopleSoft Retirement and Release Schedule

14© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory

4. Oracle’s Migration Strategy for PeopleSoft Customers

PeopleSoft Retirement and Release Schedule

Oracle Applications / Fusion

5. SAP’s Migration Strategy for PeopleSoft Customers

6. Analysis of Financial / Business Impact to Client

7. Recommendation and Migration Strategy

15© 2006 SpearMC Management Consulting, Inc.

Oracle Applications / Fusion

A Java-enabled Web browser (1) manages the download, start-up and execution of the Forms client on the desktop.

Another software component, the HTTP server (2), helps start a client session over the internal or external Web. The two exchange messages across a standard network connection, which may be either TCP/IP, or HTTP with or without SSL (Secure Sockets Layer).

The HTTP server in Release 11i is the Apache HTTP Server (3). In installations that have multiple Forms servers, only one of the Forms servers runs the HTTP server software.

The Forms server mediates between the Forms client, a Java applet running on the desktop, and the Oracle8i or newer database server on the back end (4&5).

The Forms server produces the effects a user sees on the desktop screen and causes changes to database records based on user actions (6). Both the Forms server and Forms client are components of Oracle Forms.

The Forms client (7) can display any Oracle Applications screen, and provides field-level validation, multiple coordinated windows, and data entry aids such as list of values.

• Oracle E-Business 11i currently uses a Forms-based architecture: Similar to PeopleSoft’s Internet Architecture (PIA), Oracle’s 11i framework runs on a three-tiered, distributed computing platform.

16© 2006 SpearMC Management Consulting, Inc.

Development of Fusion Technical

Framework

Development of Fusion Technical

Framework

Fusion 1.0 Development and

Release (Financials Only)

Fusion 1.0 Development and

Release (Financials Only)

Fusion 2.0 Development and

Release(Complete Suite)

Fusion 2.0 Development and

Release(Complete Suite)

Fusion 2.0 should encompass the best functionality from its predecessor applications on a stable architecture.Robust versions of HRMS, FIN, SCM, CRM, EPM, E&G, MFG, Portal, etc.

Fusion 2.0 should encompass the best functionality from its predecessor applications on a stable architecture.Robust versions of HRMS, FIN, SCM, CRM, EPM, E&G, MFG, Portal, etc.

Today 2008 2010 2012

• Project Fusion is more than a product: Fusion is Oracle’s vision, roadmap and architecture that will unite Oracle’s current E-Business Suite with products acquired from PeopleSoft, JD Edwards and Retek;

• Fusion’s Scope is growing: Since it was introduced in January 2005 as a blueprint for merging PeopleSoft and Oracle technologies, Fusion has grown to include middleware components designed to connect Oracle’s recently acquired applications to the company’s flagship database products.

First Fusion release will combine core functionality from latest releases of Oracle, PeopleSoft, JDE EnterpriseOne and Retek.Functionality present in first Fusion release may be less than current applications.

First Fusion release will combine core functionality from latest releases of Oracle, PeopleSoft, JDE EnterpriseOne and Retek.Functionality present in first Fusion release may be less than current applications.

New technical framework based on service-oriented (SOA), Java-based architecture.Embeds new technologies into Oracle 12i, PeopleSoft 9.0, JDE EnterpriseOne 8.12 and Retek.

New technical framework based on service-oriented (SOA), Java-based architecture.Embeds new technologies into Oracle 12i, PeopleSoft 9.0, JDE EnterpriseOne 8.12 and Retek.

Oracle Applications / Fusion (continued)

17© 2006 SpearMC Management Consulting, Inc.

• Oracle will abandon Forms in favor of a Java-based, service-oriented (SOA) architecture:

• Fusion will be a new product – developed on a new architecture;

• Fusion will likely run on an Oracle database and Oracle middleware, including the Oracle Application Server, Oracle Collaboration Suite and Oracle Data Hubs;

• Oracle has already started to certify Oracle middleware for PeopleSoft Enterprise to operate in place of BEA WebLogic or IBM WebSphere – this push to migrate customers from competing product lines to an Oracle-only solution will increase as Fusion Applications and Technology reach completion.

• Oracle will continue to support all current PeopleSoft infrastructure providers:

• Database support for Oracle, IBM DB2, Microsoft SQL, Informix and Sybase;

• Operating System support for AIX, HP-UX, Linux, Solaris, Windows Server 2003;

• Web Server support for BEA WebLogic and IBM WebSphere;

• Third-party tools such as Active Directory, COBOL, Crystal, CTI, Essbase, MS-Office and Tuxedo;

• Oracle has only committed to support the current infrastructure providers in pre-Fusion releases.

• Current PeopleSoft customers should be aware that a migration to Oracle Fusion may force the adoption of Oracle or Oracle-recommended databases and/or middleware.

• Oracle Sales will de-emphasize PeopleSoft or JDE products when marketing to new prospects.

• PeopleSoft products will only be pitched in mid-market MFG, CRM, E&G or Healthcare deals.

Oracle Applications / Fusion (continued)

18© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory

4. Oracle’s Migration Strategy for PeopleSoft Customers

5. SAP’s Migration Strategy for PeopleSoft Customers

SAP Product Analysis

SAP Safe Passage

6. Analysis of Financial / Business Impact to Client

7. Recommendation and Migration Strategy

19© 2006 SpearMC Management Consulting, Inc.

• As it withdraws support for older products, SAP’s existing customers are upgrading to mySAP:

• Large percentage of SAP customers are still running Versions R/3 4.6 – a pure client-server application, or Enterprise R/3 – designed to be a stepping stone to an eventual upgrade to mySAP;

• Enterprise R/3 is a client-server product with the incorporation of SAP’s Web Application Server;

• Enterprise R/3 can be upgraded with components of mySAP Business Suite (e.g. CRM or SCM);

• Retirement dates for Versions R/3 4.6 and Enterprise R/3 are 2006 and 2008, respectively.

• mySAP Business Suite is SAP’s current flagship product of internet-based applications:

• Offers solutions across nearly all industries with product suites for ERP, CRM, SCM, MFG, HRMS;

• SAP NetWeaver is essentially a re-branding of what was previously known as mySAP Technology:

• Allows integration with non-SAP applications and fosters development of business processes;

• Incorporates a Master Data Management (MDM) component designed to allow customers with different applications and technologies to consolidate and centrally master data;

• Interoperable with IBM WebSphere and .NET;

• SAP xApps are collaborative applications which run on top of existing applications:

• Underlying technology comes from Exchange Infrastructure, which allows customers to structure business processes using various SAP and third-party applications – includes data warehouse capabilities, information management features and a portal;

• SAP has partnered with other systems integrators to develop xApps for a variety of industries.

SAP Product Analysis

20© 2006 SpearMC Management Consulting, Inc.

• mySAP All-In-One – Targeted at mid-market (<$500M) companies requiring some vertical functionality in addition to cost-effectiveness and ease of installation:

• Based on a pre-configured mySAP Business Suite for 200 specific industries;

• Competes with Lawson, PeopleSoft/JD Edwards (Oracle), and other ERP mid-market players;

• Targets companies with over 200 employees;

• Current customer base of approximately 4,500;

• Average Sales Price of $130K to $175K.

• Business One is a stand-alone solution for smaller business (<$250M) with anywhere from 10 to 250 employees:

• Based on TopManage platform acquired in 2002 – this is not a lighter version of mySAP All-In-One;

• Designed to meet common business needs in accounting, reporting, logistics, SFA;

• Separate code from other SAP products, but does have common interoperability with core products through open integration standards;

• Business One runs on a Microsoft platform (Windows OS and SQL server database);

• Roughly 1,500 customers stemming from a 2003 rollout in US, France and UK that followed a 2002 Germany debut;

• Average Sales Price of $4K per seat or $21K total average sale.

SAP Product Analysis (continued)

21© 2006 SpearMC Management Consulting, Inc.

• Strengths:

• Already the global leader in back office ERP systems, SAP will likely continue to grow its market share in some of the more specialized software functions. This will come at the expense of smaller, niche players and larger software makers alike. For example, analysts point to SAP’s recent displacement of Siebel Systems and Oracle at the top of the growing market for CRM software.

• SAP offers twenty-three industry solutions of its software and has recently shifted resources to focus on mid-sized business (<$500M) with its mySAP All-In-One product offering. All-In-One is a unique offering for the midmarket, because of its mySAP underpinnings coupled with industry-specific deployment templates and methodologies.

• Weaknesses:

• Requires specific SAP skills to setup, develop, enhance and manage. SAP’s proprietary programming language, ABAP, is considered more complicated as similar ERP programming languages such as Oracle Forms or PeopleSoft PeopleCode.

• Implementation lifecycles and upgrades typically take between nine and eighteen months, but some projects are scheduled over a number of years, as scope creep for SAP projects is not unheard of.

• The need to maintain expensive relationships with third-party integrators for development, support and maintenance is due to SAP being a predominantly product development-focused organization which relies heavily on systems integrators and consultancies for direct customer interaction.

SAP Product Analysis (continued)

22© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory

4. Oracle’s Migration Strategy for PeopleSoft Customers

5. SAP’s Migration Strategy for PeopleSoft Customers

SAP Product Analysis

SAP Safe Passage

6. Analysis of Financial / Business Impact to Client

7. Recommendation and Migration Strategy

23© 2006 SpearMC Management Consulting, Inc.

• Safe Passage was announced soon after the PeopleSoft/Oracle merger: SAP’s roadmap and product offering to PeopleSoft and JD Edwards customer includes on-going maintenance and a roadmap for applications, technology and services to migrate from PeopleSoft/JDE to the latest version of mySAP.

• SAP also acquired TomorrowNow along with the release of Safe Passage: TomorrowNow, a third-party provider of maintenance and support for legacy versions of PeopleSoft and JDE, would handle on-going support for PeopleSoft/JDE customers on the Safe Passage program until live on mySAP.

• Safe Passage is directed at SAP customers running PeopleSoft or JDE: SAP indicates there are about 2,000 SAP customers that also run PeopleSoft and JDE. For these customers, the switch to SAP and related technologies would be less costly and resource-intensive than for non-SAP customers.

• Substantial Investments still need to be made: While SAP is offering a 70% discount on license fees for SAP products purchased through the Safe Passage program, substantial investments in application development, middleware, hardware and skilled SAP resources would still need to be made.

• For example: If a company paid $4 million in license fees to PeopleSoft, it would be able to apply a $2.8 million credit against any new SAP license fees that are acquired through the Safe Passage program. However, pricing for new SAP modules is not based on previous license fees and can be lower or higher than what was originally paid for modules with similar functionality.

• Technical challenges will exist for PeopleSoft customers with significant development: Migrating to SAP would involve multiple projects; namely converting databases, recoding or migrating business logic, reimplementing any client-side software and redeveloping custom applications and interfaces.

SAP Safe Passage

24© 2006 SpearMC Management Consulting, Inc.

Contents

1. PeopleSoft / Oracle Merger Background

2. Big-3 Business Application Vendor Landscape

3. Client Current PeopleSoft Inventory

4. Oracle’s Migration Strategy for PeopleSoft Customers

5. SAP’s Migration Strategy for PeopleSoft Customers

6. Analysis of Financial / Business Impact to Company (not included)

Client PeopleSoft Costs to Date (not included)

Business Impact and Industry Feedback (not included)

7. Industry Feedback

25© 2006 SpearMC Management Consulting, Inc.

• Oracle’s strategy to develop a new application suite and technical architecture is forcing PeopleSoft customers to take a longer planning view: Other organizations in similar situations are asking the most-common questions:

• How do we plan for Fusion, when will Fusion be available and will Oracle meet its delivery dates?

• Do we budget for a typical upgrade to Fusion or will it be a full-blown new implementation?

• Can we stay at current release levels or is a prerequisite upgrade required before migrating?

• Are migration programs from Oracle competitors feasible and worth exploring?

• While much speculation exists in the current marketplace, Oracle and its competitors both agree that PeopleSoft users with heavy modifications and development have a challenge in front of them:

• “How much customers have modified their core software can affect ease of migration. A customer with a financial package running relatively unaltered out of the box will face minimal aggravation. On the other hand, if the customer went wild with PeopleTools, it may take a while to recreate those customized modules” – Michael Grim, SAP VP for NetWeaver, March 2005

• “For at least the past five years, Oracle has strongly discouraged customization of its applications. Meanwhile, PeopleSoft made its advanced customization capabilities a competitive differentiator through its PeopleTools tool kit, leaving many PeopleSoft customers with heavily customized applications today. Those customers will have a more difficult time migrating and chances are they’ll have to do it again.” – John Wookey, Oracle Sr. VP of Applications, April 2005

Industry Feedback

26© 2006 SpearMC Management Consulting, Inc.

• Current market analysis from major consultancies and research firms points companies with a high investment in PeopleSoft Applications and Oracle Database to stay current with PeopleSoft:

• Stay on or upgrade to a supported release of business applications (e.g. PeopleSoft 8.9 or 9.0);

• Only deploy additional PeopleSoft applications and customizations based on short-term ROI;

• Evaluate and move to Fusion technical architecture starting in 2008-2009;

• Begin to evaluate Fusion applications and migration plan in 2009-2010;

• Budget for an application migration to Fusion that will protect only the initial license investment.

Industry Feedback