personal financial statements and accounting for governments and not-for-profit organizations...

TRANSCRIPT

Personal Financial Statements and

Accounting for Governments and Not-For-Profit

Organizations

Chapter 13

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #2

• Prepared for– Individuals– Husband and wife– Larger family groups

• For the purpose of– Obtaining credit– Tax planning– Retirement planning– Estate planning

Personal Financial Statements

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #3

Personal Financial Statements (cont’d)

• Statement of financial condition– Similar to the business entity balance sheet– Prepared on the accrual basis– Assets reported at their estimated current values

• Presented in order of liquidity

– Liabilities reported at their estimated current amounts

• Presented in order of maturity

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #4

Personal Financial Statements (cont’d)

• Statement of financial condition– Tax liability for the difference between the stated

amounts and tax basis amounts of the reported assets and liabilities

– Excess of assets over liabilities is described as net worth which is equivalent to equity section in a commercial balance sheet.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #5

Personal Financial Statements (cont’d)

• Statement of changes in net worth– Realized increases (decreases) in net worth

• Salaries• Dividends• Income taxes• Personal expenditures

– Unrealized increases (decreases) in net worth• Change in current value of securities• Change in current value of personal residence and other real estate• Change in estimated tax liability for the difference between the

stated amounts and tax basis amounts of the reported assets and liabilities

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #6

Personal Financial Statements (cont’d)

• Reviewing the Statement of Financial Condition– Net worth indicates the level of wealth– Identify very liquid (readily available) assets like

cash, savings, marketable securities, an so on.– Note the due dates of liabilities– Compare specific assets with related liabilities.

This will indicate the net investment in the asset.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #7

Personal Financial Statements (cont’d)

• Reviewing the Statement of Changes in Net Worth– Review realized and unrealized changes in net

worth– Observe whether the net realized and unrealized

amount increased or decreased– Observe whether the net change increased or

decreased– Observe the net worth at the end of the year. This

indicates the level of wealth.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. .

Chapter 13, Slide #8

• Terminology– Appropriations= Provision for necessary resources.– Debt service= Receipts and disbursement relating to interest

and principal on long-term debt.– Capital projects= Relating to acquisition of long-lived assets.– Special assessments= Improvement or services for which a

special property assessment has been levied.– Enterprises= Similar to a business where users are charged

user fees.

Governments

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #9

Governments (cont’d)

• Terminology– Internal service= Supply good or service on to

government.– General fund= All activity not account in another

fund.– Proprietary funds= Maintain assets through cost

reimbursement by users.– Fiduciary funds= Principal must remain intact.– Encumbrances= Future commitments for

expenditures.

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #10

Governments (cont’d)

• Accounting authority– 1980: Governmental Accounting Standards Board

Organizing Committee– 1984: Governmental Accounting Standards Board

• Auspices of the Financial Accounting Foundation• 7-member board• Pronouncements: Governmental Accounting Standards

Board Statements

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #11

Governments (cont’d)

• Fund accounting– Funds: Independent fiscal and accounting entity

with a self-balancing set of accounts– Basis used: cash, modified accrual, or accrual

• Trend is towards modified accrual• Some states require modified accrual basis

– Categories of funds• Governmental• Proprietary• Fiduciary

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #12

Governments (cont’d)

• Governmental funds– Account for the general operations of government

• Proprietary funds– Account for maintaining capital or producing income

• Fiduciary funds– Account for assets held in a trustee or agency

capacity

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #13

Governments (cont’d)

• Financial statements (GASB 34)– Management discussion and analysis (MD&A)– Government-wide and fund financial statements

(neither one is considered superior to the other)– Notes to the financial statements– Required supplementary information

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #14

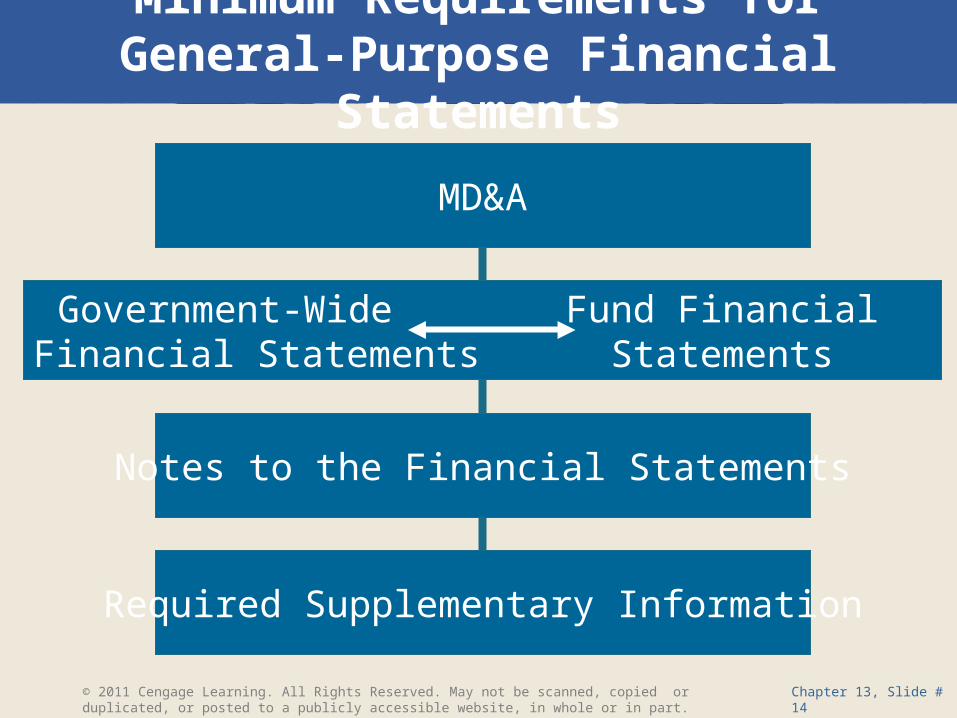

Minimum Requirements for General-Purpose Financial Statements

MD&A

Notes to the Financial Statements

Required Supplementary Information

Government-Wide Fund FinancialFinancial Statements Statements

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #15

Governmental General Purpose Financial Statements

• MD&A– Provides an objective analysis of the financial

activities of the government based on known acts, decisions, and conditions

– Provides financial managers with the opportunity to present both a short-term and a long-term analysis of the government’s activities

• Government-wide financial statements– Prepared on the accrual basis

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #16

Governmental General Purpose Financial Statements (cont’d)

• Fund financial statements– Governmental funds

• Modified accrual basis

– Proprietary funds• Accrual basis

– Fiduciary funds• Accrual basis

• Required reconciliation– Reconcile fund financial statements to the

government-wide financial statements

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #17

Governmental General Purpose Financial Statements (cont’d)

• Notes to the financial statements– Similar to corporate reporting– Must also present the original and revised budgets for

the reporting period

• Statistical section– Historical– Financial– Analytical– Economic– Demographic

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #18

Governmental General Purpose Financial Statements (cont’d)

• Independent auditor’s report– Contains information relating to both financial

information and the internal controls of the entity

• Component units– Legally separate organizations– Significant relationship to the governmental entity– Elected officials of the primary government are

financially accountable

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #19

Not-for-Profit Organizations

• Examples of not-for-profit organizations– Hospitals– Religious institutions– Professional organizations– Universities– Museums

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #20

Not-for-Profit Organizations (cont’d)

• Accounting authority– Generally Accepted Accounting Principles

• SFAS 93: Recognition of Depreciation by Not-for-Profit Organizations

• SFAS 116: Accounting for Contributions Received and Contributions Made

• SFAS 117: Financial Statements of Not-for-Profit Organizations

• SFAS 124: Accounting for Certain Investments Held by Not-for-Profit Organizations

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #21

Not-for-Profit Organizations (cont’d)

• SFAS 93: Recognition of Depreciation by Not-for-Profit Organizations– Requires depreciation of long-lived tangible assets– Exempts assets that meet two requirements

• Asset has value worth preserving in perpetuity• Organization has the ability to preserve the asset

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #22

Not-for-Profit Organizations (cont’d)

• SFAS 116: Accounting for Contributions Received and Contributions Made– Contributions Received

• Revenue in the period received• Measured at fair value• Reported as restricted or unrestricted

– Exemptions• Contributed items are held for public service• Contributed items are protected and preserved

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #23

Not-for-Profit Organizations (cont’d)

• SFAS 117: Financial Statements of Not-for-Profit Organizations– Statement of financial position

• Assets and liabilities are reported in homogeneous groups• Net assets are classified as permanently restricted, temporarily

restricted, or unrestricted

– Statement of activity• Revenues and expenses are separated into homogeneous

groups• Activities are classified as affecting permanently restricted,

temporarily restricted, and unrestricted assets• Discloses changes in the amounts of permanently restricted,

temporarily restricted, and unrestricted net assets

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #24

Not-for-Profit Organizations (cont’d)

• SFAS 117: Financial Statements of Not-for-Profit Organizations– Statement of cash flows

• Comply with SFAS 95• Financing activities include receipts restricted for

acquiring, constructing, or improving long-lived assets

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #25

Not-for-Profit Organizations (cont’d)

• SFAS 124: Accounting for Certain Investments Held by Not-for-Profit Organizations– Equity securities with readily determinable fair value

are reported at fair value• Does not apply to equity-method investments or

consolidated investments

– All investments in debt securities are shown at fair value

– Realized and unrealized gains and losses are shown on the statement of activities

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Chapter 13, Slide #26

Not-for-Profit Organizations (cont’d)

• Applicability of GAAP to not-for-profit organizations– AICPA’s SOP 94-2

• All GAAP applies to not-for-profit organizations unless– Specifically exempted– Subject matter precludes applicability

© 2011 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. .

Chapter 13, Slide #27

Not-for-Profit Organizations (cont’d)

• Budgeting– Difference from profit-oriented enterprises

• Accounting for not-for-profit organizations does not include the entity concept or efficiency

• Net income is not an available measure for not-for-profit organizations

– Objective-based budgeting• Identify objectives of the entity• Develop a budget that supports the objectives

– Measures of productivity as assessment• Productivity achieved that relate to objectives reflect the

success of the entity’s operations