personal income tax (2012) the purpose of income tax is to provide financing for government...

TRANSCRIPT

PERSONAL INCOME TAX (2012)The purpose of INCOME TAX is to provide financing for government expenditure.

The taxable incomes are from the employment such as salary.

An individual can claim the deductions for cash donation to Government, State Government or an approved charitable institution or organization and the claim must be substantiated with original receipts. There is no maximum limit for the donation.

Taxable Income

Deduction on Donation

RELIEF

TYPES OF RELIEF LIMIT EXPLANATION

Self RM9,000 Granted automatically and for disable taxpayer another RM6000 is allowed.

Wife/husband(Joint assessment only)

RM3,000 Granted automatically if wife/husband has no income and for disable wife/husband another RM500 is allowed

Child Relief:Below 18 years

18 years andstudying in aninstitution of higherEducation

Disable child

RM1000

RM4,000

RM5,000

•Unmarried child

• No restriction on the number of children.

• The wife is eligible to claim child relief if she is assessed separately

Contribution to EPF and Life Insurance Premiums (LIP)

RM6,000 maximum

Insurance policy secured on the life of the individual or spouse

Medical Expenses for Parents

RM5,000 maximum

Receipt has to be certified by medical practitioner and the expenses can be claimed by more than one individual

Purchase of supporting equipment for disabled self, spouse, child or parent.

RM5,000 maximum

Claim must be supported by receipt

Full personal medical checkup

RM500 maximum

SSPN RM6,000 maximum

Nett saving

Personal computer

RM3,000 maximum

Every 3 years only

Books and megazines

RM1,000 maximum

Annual Internet Fee

RM500 maximum

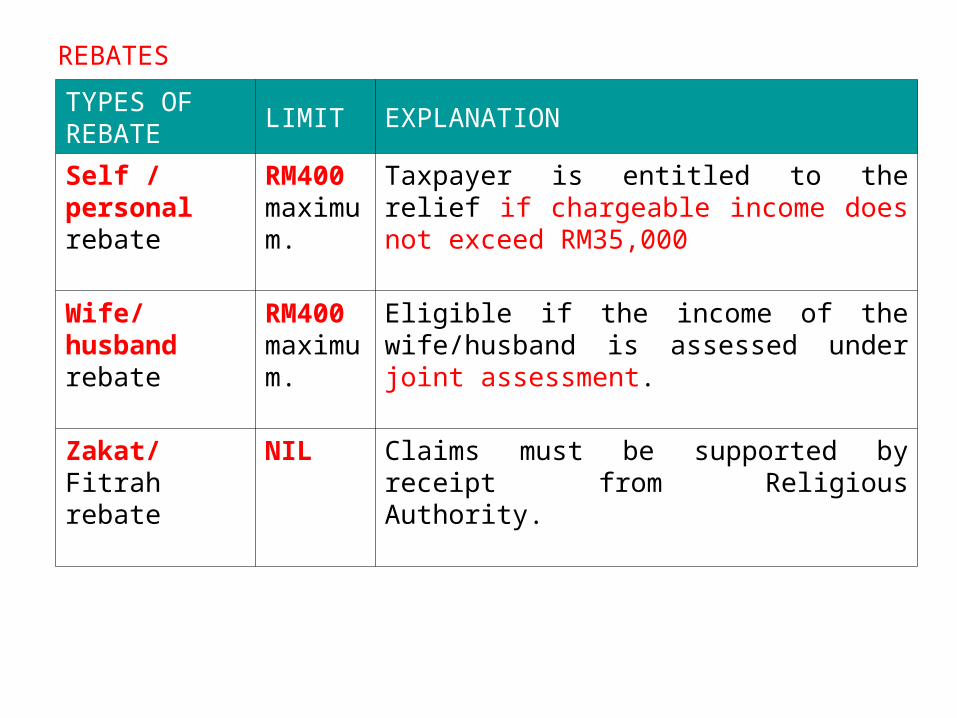

REBATES

TYPES OF REBATE

LIMIT EXPLANATION

Self / personal rebate

RM400 maximum.

Taxpayer is entitled to the relief if chargeable income does not exceed RM35,000

Wife/husband rebate

RM400 maximum.

Eligible if the income of the wife/husband is assessed under joint assessment.

Zakat/Fitrah rebate

NIL Claims must be supported by receipt from Religious Authority.

TAX RATE SCHEDULE FOR PERSONAL INCOME

Taxable Income (RM) Rate Tax (RM)

On the firstOn the next

2,5002,500

0%1%

025

On the firstOn the next

5,0005,000 3%

25150

On the firstOn the next

10,00010,000 3%

175300

On the firstOn the next

20,00015,000 7%

4751,050

On the firstOn the next

35,00015,000 13%

1,5251,950

On the firstOn the next

50,00020,000 19%

3,4753,800

On the firstOn the next

70,00030,000 24%

7,2757,200

On the firstOn the next

100,000150,000 27%

14,47540,500

On the firstExcess over

250,000250,000 28%

54,975

COMPUTATIONAL OF INCOME TAX

Formula

Total Income = Aggregate Income – Donation

Total Relief = Self + spouse + Children + EPF + LIP + Parent Medical

Chargeable Income = Total Income – Total Relief

Amount of Tax = use Tax Rate Schedule to compute.

Tax payable = Amount of Tax – Total Rebates

Total Rebate = self + spouse + zakat + computer rebates

TWO TYPES OF ASSESSMENTS

A) JOINT ASSESSMENT

Only one assessment for both of them and their incomes must be combined. Whatever deduction claimed will be limited to the amount stated except for EPF + LIP (husband + wife) are limited to RM6,000 only.

B) SEPARATE ASSESSMENT ( individual assessment )

Both husband and wife make their own assessment as a single person. In the case of children when wife is assessed separately, she may elect the appropriate deduction be allowed to her. If she so elects, relief in respect of the relevant child will be given fully to her. EPF + LIP are limited to RM6,000 to the husband and RM6,000 to the wife.

Example ( AL/OCT 2003/MAT112 – modified )

Zamri and his wife have 3 children below 18 years old. Their income for the year 2004 are as follows:

Zamri Wife

Monthly salary RM10,000 per month RM3,000 per month

EPF monthly RM1,000 per month RM300 per month

LIP monthly RM 20 -

Approved donation RM5,000 -

Zakat RM2,000 RM50

Calculate their tax payable for the assessment year 2005 if they elect separate assessment.

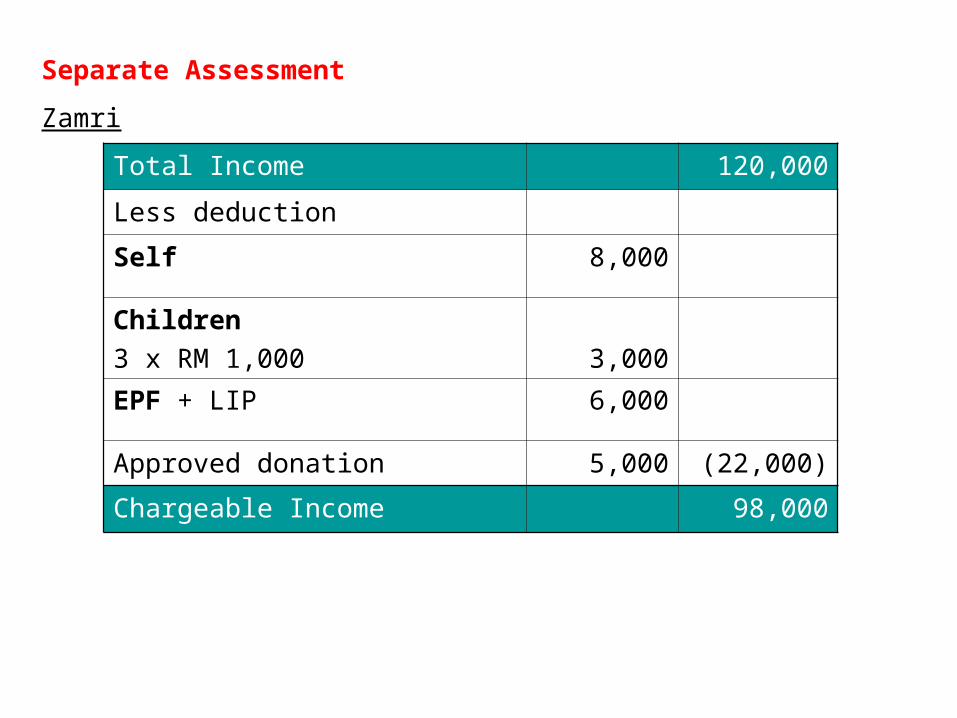

Separate Assessment

Zamri

Total Income 120,000

Less deduction

Self 8,000

Children

3 x RM 1,000 3,000

EPF + LIP 6,000

Approved donation 5,000 (22,000)

Chargeable Income 98,000

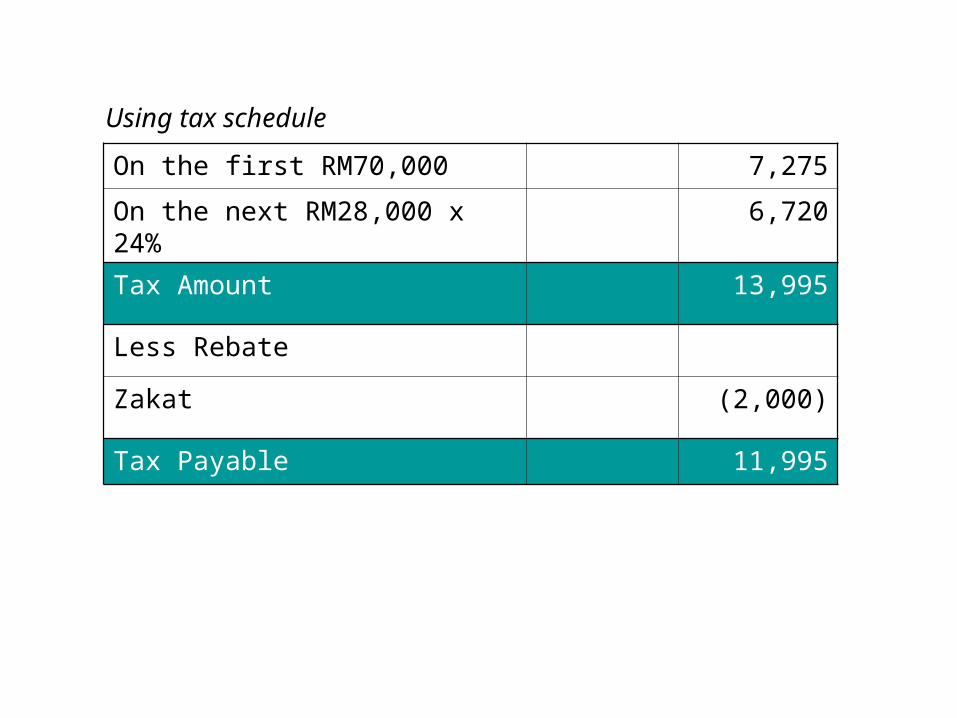

Using tax schedule

On the first RM70,000 7,275

On the next RM28,000 x 24% 6,720

Tax Amount 13,995

Less Rebate

Zakat (2,000)

Tax Payable 11,995

Wife

Total Income 36,000

Less deduction

Self 8,000

EPF + LIP 3,600 (11,600)

Chargeable Income 24,400

On the first RM20,000 475

On the next RM4,400 x 7% 308

Tax Amount 783

Less Rebate

Personal rebate 350

Zakat 50 (400)

Tax Payable 383

Example ( CS/MAR 2005/MAT112 – modified )

En Harris has 5 children and his wife is a housewife. His eldest child is studying in UiTM while the rest are still schooling. His income and expenses for the year 2004 were as follows:

RM

Salary 48,000

EPF 5,280

LIP 1,000

Parent medical fees 2,000

Donations 500

Zakat 200

Calculate the tax payable for the assessment year 2005.

Joint Assessment

En Harris and his wife

Total Income (Husband + Wife) 48,000

Less deduction

Self 8,000

Wife 3,000

Children

1x4,000 – University

4x1,000 – below 18 years old

4,000

4,000

EPF + LIP 6,000

Parent Medical Fees 2,000

Approved donation 500 (27,500)

Chargeable Income 20,500

Using tax schedule

On the first RM20,000 475

On the next RM500 x 7% 35

Tax Amount 510

Less Rebate

Personal Rebate

Wife Rebate

350

350

Zakat 200 (900)

Tax Payable 0

No tax payable for the assessment year 2005

Example

A couple with 3 children aged below 18 years old had an annual income as follows

Husband Wife

Annual Salary 50,000 40,000

EPF (Employee Provident Fund) 5,000 4,000

LIP (Life Insurance Premium)) 1,500 1,200

Parent Medical Bill 300 6,000

Zakat 60 50

Computer - 3,500

Donation - 100

Compute their tax liability if they choose

a) Joint Assessment

b) Separate Assessment

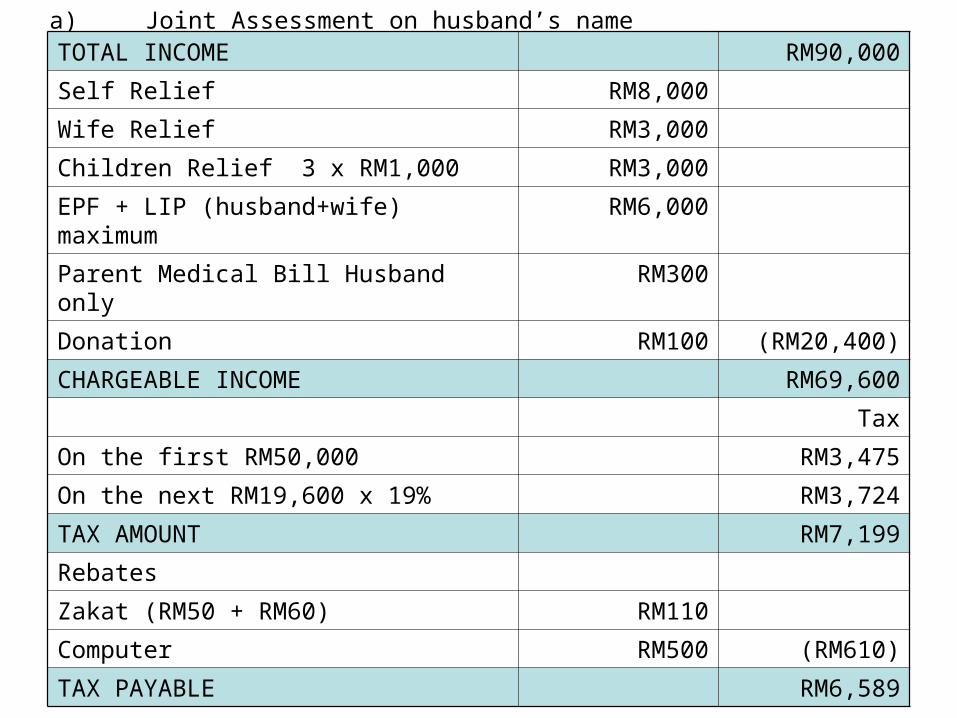

a) Joint Assessment on husband’s nameTOTAL INCOME RM90,000

Self Relief RM8,000

Wife Relief RM3,000

Children Relief 3 x RM1,000 RM3,000

EPF + LIP (husband+wife) maximum RM6,000

Parent Medical Bill Husband only RM300

Donation RM100 (RM20,400)

CHARGEABLE INCOME RM69,600

Tax

On the first RM50,000 RM3,475

On the next RM19,600 x 19% RM3,724

TAX AMOUNT RM7,199

Rebates

Zakat (RM50 + RM60) RM110

Computer RM500 (RM610)

TAX PAYABLE RM6,589

b) Separate assessment - Husband

TOTAL INCOME RM50,000

Self Relief RM8,000

Children Relief 3 x RM1,000 RM3,000

EPF + LIP (husband) maximum RM6,000

Parent Medical Bill RM300 (RM17,300)

CHARGEABLE INCOME RM32,700

Tax

On the first RM20,000 RM475

On the next RM12,700 x 7% RM889

TAX AMOUNT RM1,364

Rebates

Self Rebates RM350

Zakat RM60 (RM410)

TAX PAYABLE RM954

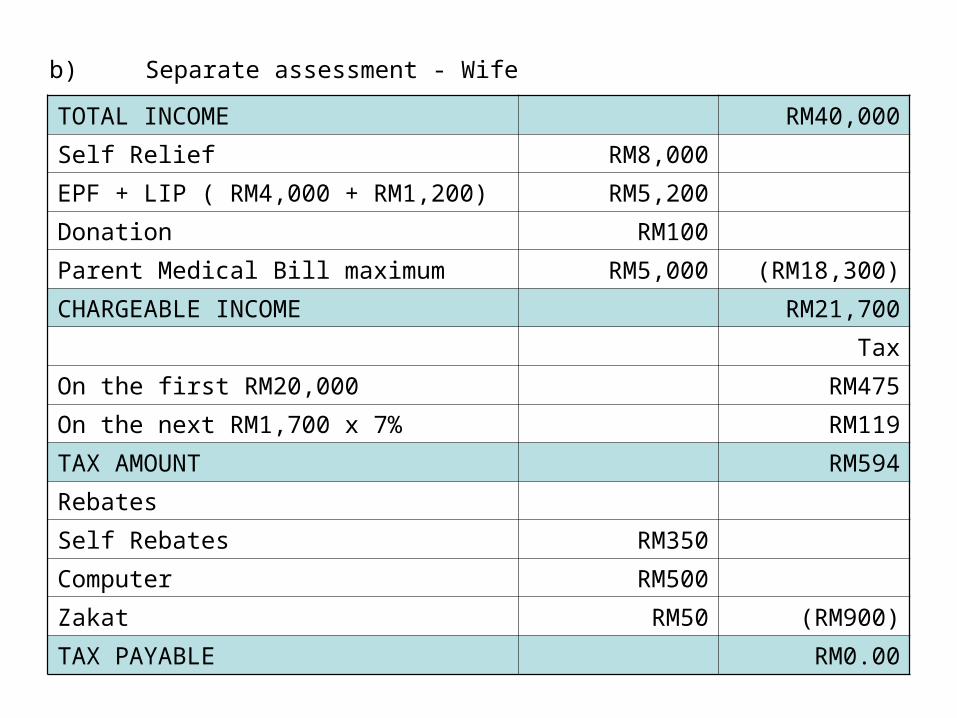

b) Separate assessment - Wife

TOTAL INCOME RM40,000

Self Relief RM8,000

EPF + LIP ( RM4,000 + RM1,200) RM5,200

Donation RM100

Parent Medical Bill maximum RM5,000 (RM18,300)

CHARGEABLE INCOME RM21,700

Tax

On the first RM20,000 RM475

On the next RM1,700 x 7% RM119

TAX AMOUNT RM594

Rebates

Self Rebates RM350

Computer RM500

Zakat RM50 (RM900)

TAX PAYABLE RM0.00