philip morris - marlboro friday (a)

DESCRIPTION

Case of Malboro FridayTRANSCRIPT

x Harvard Business School

Philip Morris : Marlboro Friday (A)

9-596-001Rev. May 21, 1996

We think the pain was worth the effort. We are not in this for the short term. We arein this for the long term . Great brands are'still great brands, but you have to keep the pricevalue in line with today's discerning consumers .1

-William CampbellPresident and CEO, Philip Morris USA

Why are they doing this? I still don't understand it, to this day .

-Karl Von der HeydenCFO RJR Nabisco, 1989-19932

In' the annals of business history, Philip Morris,' action is bigger than New Coke .MBAs will study this decision for the next century .3

-Roger EnricoVice Chairman, PepsiCo

On Apr•i12, 1993, Philip Morris USA announced plans for an elaborate program of consumerand retail promotions of unspecified duration which effectively slashed the retail price of itspremium-priced Marlboro brand of cigarettes by 20"/o in the U.S. market. Philip Morris described theactions as a "major shift in business strategy designed to increase market share and grow long-termpcofitability in a highly price sensitive market environment."4 In addition to launching major newprice promotions for Marlboro, the company also announced plans to freeze the list prices of all itspremium brlfnds and to compete more aggressively in the discount brand segment .

Marlboro was the flagship brand at Philip Morris, a company that claimed to maintain the"best brands in the world." The day these actions were announced was immediately labeled

i .

1Quoted in: IraTeinowitz, "Marlboro Friday; Still Smoking," Advertising Age,March 28, 1994, p . 25. ZQuotedin: Elizabeth Lesly, "Tobacco Companies have Created their Own Monster ;" Business Week, August 30,

1993, p. 59.3Quoted in: PatrioaSellen,'Pall for Philip Morris," Fortune, May 3,1993, p . 68

. - 4Cited in Teinowitz, op. cit., p . 24. . -, -

Doctoral Candidate Bruce Isaacson and P .ofessor Alvin Silk prepared this case as the basisjo r class discussion rather than ~ ~ ito illustrate either effective or ineffective handling of an administrative situation . The authors are indebted to Bob Dolan, oJohn Quelch, and Ben Shapiro far helpful comments and suggestions and to Rick Pollay and Mike Siegel for assistance with ~data sources. - - . . . 0 .

Copyright ©~1995 by the President and Fellows of Harvard College.- To order copres or request permission to ' ~reproduce materials, call 1-800-545-7685 or write Harvard Business School Publishing, Boston, MA 02163 . No~p

part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in Coany form or by any means-electronic, mechanical, photocopying, recording, or otherwise-without the -~permission of Harvard Business School. -L..

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-007 - . Philip Morris: Marlboro Friday (A) -

"Marlboro Friday" and heralded as a milestone in marketing history . On that day, the price of PhilipMorris stock dropped 23%, consuming $13.4 billion in shareholder equity. . The stocks of manyconsumer products companies also experienced double-digit declines on "Marlboro Friday,"accounting for a 69-point drop in the Dow Jones Industrial Average . These events touched off anextended debate concerning the wisdom and long-term implications of Philip Morris' drastic actions .

The Cigarette Industry

In 1993, the U.S. cigarette market was served by six major domestic suppliers : Philip Morris, 'RJ Reynolds (RJR), Brown & Williamson, Lori)lard, American Tobacco, and Liggett & Myers . Overtime, these six companies had built extensive distribution organizations, made large investments inautomated production equipment, spent heavily on advertising and promotion, and developedwidespread recognition for their brands . Consequently, there were no other sizeable domesticcigarette manufactures in the U.S. market.

As shown in Exhibit 1, Philip Morris and RJ Reynolds dominated the market, with almost73% of the unit volume produced in the U .S. cigarette market in 1993. Exhibit 2 presents the netrevenues and operating contributions generated by these companies in 1992 . As indicated there, thecigarette business was highly profitable for all the major domestic suppliers listed, except Liggett &Myers. In 1992, for the industry as a whole, manufacturers' gross profit margin (average across alltypes of cigarettes) were estimated to be 76% of operating revenues where gross margins werecalculated as operating revenues minus variable costs minus factory overhead . Variable costs ,included tobacco leaf costs, which averaged 18% of operating .revenues while factory overheadaccounted for an additional 6°/a 5

Cigarettes prices experienced double-digit annual increases during the 1980s (see Exhibit 3and 4), consistently rising faster than the consumer price index . Over the decade 1983-1992, theaverage retail price of a pack of 20 cigarettes rose from $0 .87 to $1 :61 .

Table A shows the structure of trade prices and costs for a pack of 20 cigarettes in 1991 and1992. Cigarettes were typically sold at a retail price more than double the manufacturer's sellingprice. By law, retail prices were set by retailers, and a significant portion of retail cigarette priceswent to federal, state, and local taxes. These taxes amounted to an average of 51 cents per pack in1993, iip from 47 cents in 1992, and 22 cents in 1983 .

SMarc I. Cohen and Gavin Launder, The Tobacco Handbook, New York : Goldman Sachs, April 8, 1994, p . 30.

2 .

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

0

Philip Morris: Marlboro Friday (A)

Table A Industry Price and Cost Structure, 1991-1992a

1991 . 1992 . .$lPackage % - $/Packaqe %

Retail Price1 .61 100.00 1.72- 100.00

0 -Trade Mark-Up Manufacturer's List Price

.361 .25

22.277.8

0.371.35 .

21 .678.4

Taxes(Federal, State and Local) 0.44 27.2 _ . 0.47 27.4Variable Production Cost 0.15 9.6 - 0.16 - 9.1Contribution 0.66 ' 41 .0 0.72 41 .9Factory Overhead, Marketing,General and Administrative CostsOperating Profit

0.310.35

19 .121 .9

0.35 ,0.37

20.3 -21 .6 -

596-001

Source: Calculated from data presented in Marc I . Cohen and Gavin Launder, The Tobacco Handbook, Goldman, Sachs and Co., April 8, 1994, pp .,29-30

. °Cigarette taxes were set as a $ amount per package, rather than as a percentage of a selling price . .Table A treats all taxes as being included in the manufacturer's selling price . This is anoversimplification inasmuch as certainYaxes may be incorporated in wholesale and/or retail prices ratherthan entirely in manufacturers prices

. - , Cigarettes were available in a wide variety of retail outlets . In 1993, it was estimated that39% of all cigarettes were sold in supermarkets, 17% in convenience stores, 13% in gas and servicestations, 2%o in warehouse club stores, 8% in drug stores, 7% in mass merchandisers, and 14% in otheroutlets, such as eating and drinking establishments, vending machines, and other types of retailestablishments . About 20% of all cigarettes were sold on promotion . Package sizes and purchasequantities varied by type of outlet-in supermarkets, two-thirds of the unit volume sold was incartons, while the vast majority of the cigarettes sold in convenience stores and gas stations was soldby the pack. (A packcontained 20 cigarettes, while a Carton contained 10 packs .)

Although increases in manufacturer prices during the 1980s were generally greater thanincreases in retail prices, cigarettes remained highly profitable for retailers . A sales analysisconducted at Marsh Supermarkets, a representative supermarket chain, showed that the cigarette/tobacco category generated sales of $70 .39 per foot of shelf space, the highest of all categoriesanalyzed. Cigarettes/tobaceo was ranked fourth among all categories in total weekly sales,accounting for 2.0% of the store's weekly grpss profit, and had the fifth highest percentagecontribution of all grocery products analyzed .6

Brand extensions were common in the cigarette industry . . For example, in 1993, Marlborocigarettes were available in 17 varieties, including regular Marlboro's; Marlboro Lights (a low tarcigarette); Marlboro Mediums (higher tar and stronger flavor than Marlboro Lights) ; Marlboro 100's(a longer cigarette) ; and Marlboro Menthols. As shown in Exhibit 5, the number of branlintroductions in the industry variedd by company,but had increased considerably during the 1980 :The six cigarette companies produced over 500 different brands and product/package varieties ccigarettes in 1992, up from about 165 in 1980 .

Despite the proliferation of brands, a few major brands dominated the market . The 11 brandlisted in Exhibit 6 accounted for 64 .4% of the U.S. market's unit volume in 1992. To support this salevolume, cigarette makers spent over $370 million on advertising in measured media in 199 :primarily for premium brands . Media advertising was generally very limited or entirely absent fcdiscount brands. Over time, expenditures for media advertising as a percentage of total outlays fC,

6Michael Garry, "Taking on the Generics;" Progressive Grocer, August 1993; p . 129.

aW

.

3

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001 Philip Morris: Marlboro Friday (A)

advertising and promotion had declined . Exhibit 7 shows total advertising and promotionexpenditures in the U.S. cigarette industry for 1986-1990 .

. In 1993, the cigarette industry faced a number of significant threats . Foremost among thesewere proposals to increase taxes. Taxes were assessed on cigarettes by both federal and stategovernments, as well as some cities and counties . These levies varied widely from location tolocation; for example, state tax rates ranged from two to three cents per pack in Virginia andKentucky to 75 cents in Michigan .

In 1993, proposals for additional taxes ranging from $0 .25 to $1 .50 per pack were underdiscussion, possibly as part of a comprehensive program to reform the Adterican health care system .Although the amount of the increase was uncertairi, most analysts felt some increases in federal taxeswould be implemented. However, consumer demand for cigarettes did not change greatly withmoderate changes in retail prices . To illustrate, studies by the American Lung Association hadestimated that every 10% increase in cigarette prices reduced demand by 4% .

A second threat was the increasing number of restrictions on smoking . By .1993, a third ofAmerican companies had instituted smoke-free workplaces and the Occupational Health and SafetyAdministration was considering regulations to ban smoking in all U .S. indoor workplaces . The U.S .Environmental Protection~ Agency (EPA) had classified second-hand smoke as a carcinogen, andmany cities or states forbid smoking in public places .

A third threat facing the cigarette industry was the increasing array of restrictions onmarketing activities . On January 2, 1971, cigarette'advertising had been banned on television andradio in the United States. However, cigarette companies spent large sums on other media such asprint and outdoor advertising, database marketing, and promotions at events such as music concertsand sports-car races . Some critics argued that this advertising should .be further restricted or bannedaltogether . For example, one study claimed that an ad campaign for RJR's Camel cigarettes, whichfeatured a cartoon character, "Old Joe Camel," was aimed at children rather than adults and enticedchildren to smoke.7 Public agencies, such as the Massachusetts Department of Public Health, ranantismoking ads in a variety of media .

A fourth threat confronting the industry was product liability lawsuits . Tn 1993, 47 liabilitycases were pending against the industry, including 22 that named Philip Morris as a defendant .Philip Morris vigorously defended itself against such cases, stating in its 1991 Annual Report that,"We regard smoking as a voluntary lifestyle decision that need not be subjected to new marketing oruse restrictions ." The company had never lost or paid to settle a tobacco product liability case .

Despite being second only to Philip Morris in domestic market share, RJR was in a somewhatweakened position. The company was heavily in debt from a $25 billion leveraged buyout (LBO) inNovember 1988 . In 1993, its debt level was $12.5 billion, down from $29.1 billion at the time of theLBO. Nonetheless, its debt-to-equity ratio was still 1 .4 to 1. Also, RJR's chairman, Louis Gerstnerabruptly resigned on March 26, 1993 to head IBM. In April 1993, RJR was planning to create aseparate class of stock for its food division, seeking to reduce debt by selling 25% of the company tothe public.

Consumer Behavior and Smoking

Once a person started smoking, it was very difficult to stop. Cigarettes contained nicotine, aasubstance widely considered to be addictive . Withdrawal from nicotine caused both physical and

7Journal of the American Medical Association, December 11, 1991, cited in Walecia Konrad, "I'd Toddle a Mile for aCamel;" Business Week, December 23, 1991, p 34. ' . . -

,

4

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

. Philip Morfis : Marlboro Friday (A) . . . sss-oo1

psychological distress. Although 80% of all smokers said they wanted. to quit, only 69% believed theywould succeed if they decided to try, and a mere 2 .5% of smokers permanently quit smoking eachyear .8

Consumers were exposed to a continuing stream of scientific evidence published by the U .S.Surgeon General, the British Royal College of Physicians of London, and other agencies which linkedsmoking to a variety of illnesses, including coronary heart disease, lung cancer, chronic bronchitis,emphysema, chronic sinusitis, peptic ulcer disease, cancer of the larynx, oral cancer, and cancer of theesophagus. Maternal smoking during pregnancy was associated with higher rates of fetal death,spontaneous abortion, and Sudden Infant Death Syndrome (SIDS) .

Partly in response to' growing concern over smoking's health risks, per'capita consumption ofcigarettes had declined steadily in the United States, falling to 2,640 cigarettes per adult (18 years ofage and older) in 1992 from 3,746 in 1983 . The volume of cigarettes consumed' in the United Statesfell by 21% from 1982 to 1992 (see Exhibit 3), while dollar expenditures on cigarettes increased by95% during the same period.

The proportion of U .S. adults who smoked had also declined dramatically over the pastthree decades, falling from 42 .4% in 1965 to 37.4% in 1974 and 29 .9% in early 1993. A 1993 study byMediamark Research found that light users represented 10 .8% of the U.S. adult population andconsunied 10:3'/0 of all cigarettes smoked . By contrast, heavy smokers represented 9 .2% of the overallpopulation but consumed 61 .0% of the unit volume. (See Table B) .

Table B Cigarette Consumption, by User Group

Packs Smoked inLast Seven Days

Percent of U.S.Adult Population Share of Volume

Light smokers`

0•5 . 10.8% . --

10.3%b -Moderate smokersHeavysmokers

6-89ormore .

9.9 .. , 9.2

28.761.0' - .

Total 29.9% - 100.0%

Adapted from Mediamark Research Shopping & Tobacco Products Report, Spring 1993,.~. 142. . . . . . .

To be read, for example : "Of the overall population 10.8% are light smokers. These fighttsmokers consume 10.3% of the un8 volume consumed by all cigarette smokers .". .

The Mediamark study. also analyzed the social, demographic, and economic characteristics ofsmokers. As shown by Exhibit,8 ; compared to the general U .S. population, cigarette smokers weremore likely to be male and less likely to be college graduates . Also, smokers were younger, hadlower incomes,~and were less likely to read newspapers . . .

. Smokers tended- to be highly brand loyal. Estimates of cigarette brand switching wereobtained in . a nationwide survey conducted in 1986 for the U.S. Department of Health and HumanServices .9 Among 4,651 current smokers (aged 18 or older), 9 .2% reported having smoked a differentcigarette brand within the previous year from that which they smoked at the time of the survey .Brand switching was found to be higher among female smokers, among smokers with lowerhousehold incomes and among those who had recently attempted to give up smoking .

8Maggie Mahar,'Tobacco's Smoking Gun;' Barrons, May 16, 1994, p. 34 . .

. 9Michael Siegel, David E. Nelson, John P. Peddicord, Robert K. Merritt, Gary A,Giovino, and Michael P . Erikse"The Extent of Ci arette Brand and Company Switching: Results from the Adult Use of Tobacco Surve3American Journal of PreaeaBve Medicine, forthcoming, January-February, 1996. .

5 -

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-007 . . . Philip Morris : Marlboro Friday (A)

Discount Brands

Cigarette brands could be divided into two price tiers : (a) premium brands, which werehigher priced and sold primarily on attributes such as taste or image, and (b) discount brands, whichwere lower-priced.10 Discount cigarettes were much less profitable for manufacturers, who typicallymade profits of five cents per pack on discount brands, versus 55 cents on premium brarids?1 Thefirst discount cigarette was launched in 1980 by Liggett, the smallest U.S. cigarette manufacturer.Exhibit 9 shows the growth in discount brands' share from 1981-1992 . This growth was particularlymarked in early 1990's, a recessionary period in the U .S. economy. By early 1993, the market share ofdiscount brands had risen past 30% of all cigarette volume and was growing by almost one-half of ashare point per month.

Over time, the widening price differential between discount and premium brandS had fueledthe growth of discount brands. As shown by Table C, .in early 1993 this gap had reached almost$1.00 per pack. The average smoker bought 10 packs of cigarettes per-week . Thus in 1993, thisperson would spend $1133 if all purchases were premium brands and $630 if all purchases werediscount brands .

Table C Average Retail Prices per Pack, Premium and DiscountCigarettes

Date Premium Discount Differential

January 1992 $1.74 - $1 .25 $0.49 .January 1993 $2.18 $1 .21 $0.97

Source:Marc 1. Cohen and Gavin Launder, The Tobacco Handbook, - Now York: Goldman Sachs, April 8, 1994, p . 25 .

Table D shows the position of each of the major U .S. cigarette manufacturer in the premiumand discount segments. The table shows that Philip Morris had the highest share in the premiumsegment, while RJR had the highest share in the discount segment. Over .60% of all discountcigarettes were produced by either RJR or Philip Morris, although RJR was much more dependentupon discount volume.

10The "discount" . tier could be further sub-divided into two finer segments : (a).-a mid-price tier ofmanufacturer discount brands which sold at retail prices ranginq from $1 .30 to $1.50 per pack in-early 1993 ; and(b) a deep discount tier of generic and retailer-controlled labels sold principally by mass merchandisers,convenience stores, and gas stahons for less than $1 per pack, sometimes for as little as $0 .69 . . -

11Eben Shapiro, "Price Cut on Marlboro Upsets Rosy Notions About Tobacco Profits," Wall Street Jottrnat, Apri15, 1993, pp. 1 and A10. Also see: Subrata N . Chakravarty and Amy Feldman, "Don t Underestimate

the Champ;" Forbes May 10, 1993, p . 109 . ' - -

6

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

I Philip Morris: Marlboro Friday (A) - - 596-001

Table D Position of Cigarette Manufacturers in Premium and Discount Segmentsa

. . .

Unit Volume Market Share, 1992

.

1992 Share of

Discount Sales as aPercentage ofManufacturer's

Total Unit VolumeManufacturer . Premium

SegmentDiscount Segment Total Market 1992 1991

Philip Morris 48.9% . 27.1% 42.3% 19.4% 17.0%RJ Reynolds .

. Brown & Williamson27.0. 7 .6 . - '-

33.221 .9

28.911.8

34.7255.6

5.547.4

Lorillard . 10 .0 ~ ~ 0.8 7.2 - 3.6 0.8American TobaccoLiggett & Myers - -

5.2 -- 1 .3 - -

-10 .07.0

6.83_0

44.9. 70.4

38.372.8

Total . 100.0% 100.0% 100.0 30.3 25.0

Source:Derived from data on factory shipments reported in: Marc I. Cohen and-Gavin .Launder, TheTobacco Handbook, New York . Goldman Sachs Co ., April 8, 1994, p . 24.

RJR had raised its share in the discount market over time, building a portfolio of over 200 "discount brands. These included national,brands as well as private-label brands producedexclusively for specific retailers, such as Austin brand for Circle K convenience stores, Jacks brand forSheetz convenience stores, or Highway brand for the 800 gas stations owned by British Petroleum OilCompany. RJR manufactured its discount cigarettes in the same factories as its premium brands, andused a powerful and efficient sales organization to generate distribution through retailers andwholesalers . RJR's operating margins from domestic tobacco, reflecting an increasing share ofdiscount brands, dropped to 27.6% in 1992 from 33.6% in 1990 .12 By contrast, Philip Morris' margins,driven by premium market share, grew to over 43% in 1992 from 40 .6% in 1990.13

The share of discount brands received a boost in the summer of 1992 when RJR ran a numberof temporary price promoHons on its discount cigarettes. Many retailers also cut margins, usingdiscount cigarettes to build store traffic. By 1993, some analysts felt the growth of discount brandswould slacken once they achieved broad distribution . Others argued that the discount brands wouldcontinue to grow and it would become increasingly difficult to woo smokers back to premiumbrands.

Philip Morris

Philip Morris was a $61 billion company with a proud legacy and a history of success .Between 1983 and 1993, the company realized a compound average annual growth rate of 16.5% inoperating revenues, 16.2% in net eamings,14.6% in net earnings per share, and 25.3% in total returnto stockholders. In 1993, Philip Morris directly employed 173,000 people . When taxes on corporateincome, cigarettes, employee wages, and other items were totalled, Philip Morris was the largesttaxpayer in the United States and the largest nongovemment tax collector in the United States .

In 1992, Philip Morris contributed more than $50 million to tax-exempt organizations . Thecompany had a long tradition of supporting a wide variety of artistic organizations, cultuial events,

`1zOperating margin is defined as operating contribution (per Exhibit 2) less additional operating company .ex enses

. 13Ehakravarty and Feldr3ian, op . cit .,p. 109 . . . ,

V i

7

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001 . . _ . , Philip Morris: Marlboro .Friday (A))

and charities . In the 1956s, 1960s, and 1970s, the company was known as a prominent and pioneeringemployer of minorities and women . .

. - The company achieved its financial success in part by building a portfolio of leading brands.As listed in Exhibit 10, other brand names owned by Philip Morris included Miller beer, Kraft cheese,and Post cereals . The 1993 Annual Report had "the world's best brands" as its central theme, stating :

Our unparalleled portfolio of the world best brands is the key to building- long-term value for our shareholders . . : . Heading the list

: Marlborocigarettes, the world's best-selling consumer packaged product and the ideal global brand,marketed with a consistent image and unmatched efficiency and profitability .

- Philip Morris relied heavily on advertising to support these brands . In 1992, and 1991,Advertising Age, in its annual survey of the 1001eading U .S: national advertisers, placed Philip Morris 'second in total spending . For 1992, expenditures totalled $2 .02 billion on media advertising, sales -promotion, and direct response .

Despite the broad variety of product categories included in Philip Morris' brand portfolio,cigarettes remained a major source of profits and .income. As shown by Table E, domestic andinternational tobacco sales generated 43% of Philip Morris' revenues and 66% of profits. In 1992,Philip Morris sold approxiatately 100 billion more cigarettes than its closesbworldwide competitor ..As shown earlier by Exhibit 2, in 1990, 1991, and 1992, Philip Morris accounted for more than half ofthe domestic industry's profits . While international tobacco sales were increasingly important to thecompany, Marlboro accounted for 60% of Philip Morris USA's 1992 sales and 75% of its operatingincome. :

Table E Philip Morris Operating Revenues and Operating Income, 1991-1992

1991 1992

Operating Revenues. (in millions) :Domestic tobacco . $11,589 $12,010International tobacco . . 12,251 13,667Food, beer, financial services, real estate 32.618 33,454Total Operating Revenues . . $56,458 $59,131

Operating Income (in millions) : - . - ,Domestic tobacco . . $ 4,774 $ 5,185

. International tobacco 1,694 2,018Food, beer, financial services, real estate 3.442 3.757

Total Operating Revenues -- ,- $ 9,910 . $10,960

Source : .Annualreports .For several years, Philip Morris and other domestic cigarette manufacturers had been

criticized for their trade loading practices-encouraging wholesalers to "forward buy" extraquantities just prior to a price increase . While these practices had served to boost sales and earningsin the short-run, the risk was that once distributors no longer anticipated further price increases, theywould draw down the inventories they had built up and the manufacturers would take a big hit insales and earnings. In September, 1989, RJR announced that it was terminating trade loading in itsdomestic cigarette distribution operations. It was estimated that the firm forfeited $340 million inoperating profits by reducing production and allowing trade customers to sell down their excessinventories.14 ' - -

r4Carol J. Loomis, "The $600 Million Cigarette Scam," Fortune, December 4, 19$9, p .89 .

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

Philip Morris: Marlboro Friday (A) 596-001

Philip Morris allegedly continued to engage in trade loading.15 For example, in late 1992,Philip Morris suggested that distributors take on inventory before a price increase scheduled to occuron January 1, 1993. A larger wholesaler was quoted as saying, "I think Philip Morris is making aterrible mistake strategically . . . . If Philip Morris stopped loading tomorrow, it theoretically could,dose the plants for a month."16 In January, 1993, the company recommended that distributors stockup on new Marlboro packs containing coupons for a continuity promotional program . Again inMarch 1993, Philip Morris announced a small price increase for April, once more advocating thatdistributors stock up in advance of the price change . Some analysts endorsed this practice, arguingthat distributors who had higher warehouse inventories would encourage retailers to expand shelfspace for Philip Morris brands .

Marlboro

. Marlboro was first launched in the United States by Philip Morris in 1924 . Originallypositioned as a womeri s cigarette, Marlboro had a featured red filter tip and had been advertised asthe cigarette with "a cherry tip for your red lips." In the 1920s and 1930s, Marlboro had also beenpromoted as "mild as May ."

In 1954, three major changes were made to reposition Marlboro as a man's cigarette. First,Marlboro's mild blend of tobacco was changed to a stronger, more flavorful blend . Second, thepackaging was modified from a white package to a red-and-white chevron design . Third, the brancj'sadvertising strategy was- altered to focus upon males in tough, action-filled jobs . Initially, subjectsfeatured in these ads included pIlots and deep-sea fishermen, but a lean, weatherbeaten cowboy soonbecame the sole focus . This cowboy came to be known as the Marlboro Man . Beginning in 1964, hewas always photographed in the western United States, amid magnificent scenery which the adsidentified as "Mar1boro Country." One Iong-rtnuling slogan invited smokers to, "Come to MarlboroCountry . . . where the flavor is ." The Marlboro man, packaging, and advertising have since been .used in almost 150 countries.

These changes were intended to position Marlboro as a competitor to Camell cigarettes, .namely as a'brand for the strong, outdoor, independent man, the person .who thinks for himself,lives his own life, does his own thing ."?7 By 1975, Marlboro, supported by heavy spending onpromotion and advertising to communicate .a consistent message, had become the best-sellingcigarette in the United States . In 1992, Marlboro's market share was more than three times its closestcompetitor, its advertising expenditures far surpassed other brands, and one out of every fourcigarettes sold in the United States was a Marlboro (see Exhibit 6) . The 124 billion Marlborocigarettes sold in the United States that year would stretch to the moon and back 27 times if lined upend to end. Marlboro was also one of the best-selling brands in any category ; in 1992, the brand hadmore revenues in the United States than Campbell Soup ; Kellogg, or Gillette .

Marlboro was also the biggest-selling brand in Germany, Mexico, Switzerland, Saudi Arabia ;Hong Kong, Argentina, and 11 other major markets. Financial World, in its September 1, 1992 issue,named Marlboro as the world's most valuable brand_

I5Patricia Sellers, "The Dumbest Marketing Ploy," Fortune, October 5, 1992,p. 88. Also see Sellers, op. cit., 1994.16Quoted in Sellers, op. cit . ., 1992 . . ' _ . - .

l7Interbrand Group p1c ., Tlie World's Greutest Brands, New York : John Wiley & Sons,1992: -.

O .

9

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001 , . Philip Morris: Marlboro Friday (A) .

Marlboro Friday

Exhibit 11 shows Marlboro's market share over time in the U .S. market. Despite the brand'shistoric strength, its market share slipped steadily from 26 .2% in 1989 to 24.4% in 1992. The rapidgrowth of discount cigarettes was particularly worrisome . In 1991, discount brands and Marlboroboth had a market share close to 25%. By 1992, Marlboro's market share had dropped below 25%,while discountbrands had risen above 30% .

In January 1993, William Campbell, head of Philip Morris USA, announced that Marlboroshipments in 1992 had fallen 5 .6% compared to the previous year . This was the steepest annual dropin the brand's history; in the fourth quarter, Marlboro sales had declined 11 .2% compared to thefollowing year. Although Campbell admitted surprise, he maintained that the growth of discountbrands was slowing and that the fourth quarter decline was primarily due to efforts to reducedistributors'surplusinventory .

First quarter results contained more alarming news. Marlboro shipments were down 8%from first quarter 1992 and the market share of the discount tier continued to surge. In discussingthese results on April 2, Campbell observed : "This market has moved very quickly . We don't see ittoday the way we saw it in January ."18 He then went on to announce a series of stunning changes inPhilip Morris USA's strategy for Marlboro and the other brands in the firm"s product line . Theseannouncements were widely interpreted as representing a watershed event in brand marketing andthus the day on which they occurred came to be designatedd as "Marlboro Friday ."19

1 . Marlboro Pri¢e Promotion In the first of these actions, Philip Morris announced the launch of ea major price promotion, designed to effect a 20% reduction in Marlboro's retail price, lowering theaverage price per pack to consumers from $2 .20 to $1.80. This decision was taken after conducting afour-week test market in Portland, Oregon during the fall of 1992 . The test market showed that aprice cut. of 40 cents per pack gained four share points for Marlboro . Half of this share gain camefrom discount brands, while the other half came from premium brands .

Marlboro did not reduce list prices, but instead effectively cut net retail prices through theuse of coupons and other consumer promotions, such as "buy three, get two free." To help ensurethat the cuts would be passed on to consumers, Philip Morris sought to reduce retailers' inventoriesby reimbursing the retailers for reductions in the value of their inventories caused by the promotionalprice cuts. In order to participate in the buy'down program, retailers agreed to display signsadvertising the retail price cut, to distribute catalogs for a Marlboro promotional program, and topermit. their sales to be monitored weekly . The company hired 2,500 temporary workers to auditretail accounts, effectively doubling its normal salesforce in some territories . Sales reps wereinstructed to visit every major account at least once per week, and authorize checks to cover theretailers' discounts .

2. Marlboro Continuity Program The second action taken on Marlboro Friday involvedexpanding a large-scale continuity program. Spending was greatly' increased on the MarlboroAdventure Team continuity program which had begun in October 1990 . Under this program,Marlboro purchasers earned points enabling them to participate in an "Adventure Tearri' Expeditionand to acquire Westem clothing and outdoor gear featured in an Adventure Team catalog whichincluded such items as charcoal grills, backpacks, jackets, radios, and cigarette lighters . For example,credits received on purchases of 130 packs of Marlboros enabled the buyer to obtain a free Webercharcoal grill.20 Advertising expenditures for Marlboro were left unchanged,

18Shapiro, op . cit ., p~ A10. - - - 1`~The account of Philip Morris' strategy summarized in this section draws on materials found in Sellers, op. cit.,

,p 68-69; Shapiro, op. at.,p Al and A10; and Teinowitz, op. cit ., pp . 24-25. '~~OThe retail list price on a Weber portable charcoal grill was approximately $50 . - .

10

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

Philip Morris: Marlboro Friday (A) 596-001

3. Discount Brand Strategy In the third strategic change, Philip Morris raised the list price of itsleast expensive discount brands and initiated the first major advertising campaign for Basic, one of itsdiscountbrands . . -

Subsequently, on July 20,1993, the Marlboro price cuts were made permanent by convertingthe price promotion into an equivalent list price reduction which was also applied to Philip Morris'other premium brands, including Benson & Hedges, Virginia Slims, Merit, and Parliament . PhilipMorris also announced it would increase prices on its deep discount prices tier brands by $0.06 perpack from $1 .31 to $1.37 while prices on its mid-price tier brands would be decreased $0 .25/pack.Taken togetherthese changes represented a shift in the price structure'of cigarette market from threetiers to two tiers. Smokers were notified of the new prices via a large scale direct mail campaign .

According to the 1993 Philip Morris annual report, the actions started on Marlboro Fridaywere intended to rebuild the company's premium cigarette brands :

Our new pricing strategy and actions had a simple objective: to narrow theprice gap between our premium product and discount competitors to a point whereconsumers would once again base their purchases on brand quality, imagery, andpreference, rather than on price alone . Our goal was to recover our lost premiumbrand share, and thereby to protect the long-term profit and cash-generating powerof these strong brands .

The Aftermath of Marlboro Friday

The actions announced on Marlboro Friday stunned Wall Street. In the six months before theprice cut, Philip Morris' market capitalization had declined by 29% . On Marlboro Friday, PhilipMorris stock fel123°/a, to $49,37 per share from $64 .12 . This was the largest one-day decline in a singlestock since October 19, 1987, and consumed $13

.4 billion in shareholder equity . In later months, thestock would fall to $45 before beginning to rebound.

Overall, -the Dow Jones industrial stock average fell 68 .63 points on Marlboro Friday, asinvestors sold off the stocks of other consumer products manufacturers such as Procter & Gamble,Quaker, and Coca-Cola. Share prices of other tobacco stocks also experienced double-digit decreases .

The company's actions drew a barrage of criticism from industry observers . Somemaintained that the program was an overreaction . As one analyst said, "They used an ax where ascalpel would have been preferable . It destroyed an industry's profitability ."

Otliers criticized the brand's recent management as well as the objectives, execution, andtiming of the new strategy . As Fortune stated,

What really happened is that Philip Morris made an ill-conceived andfoolishly executed decision in an attempt to recover from years of surprisingmismanagement. . . . . Will the $2 billion plan set the Marlboro Man riding highagain? Not necessarily-for the new program is panicky, hodgepodge, andundisciplined?1

Philip Morris defended the plans announced on Marlboro Friday as decisive actions thatwould defend Marlboro's position in the large and lucrative U .S: cigarette market. As LawrenceWexler, senior vice president at Philip Morris said ; .

ZtSellers, op . cit ., p. 68 .

11

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001 Philip Morris: Marlboro Friday (A)

We understand there'll be some short-term pain .in terms of our profitability . .But this is. .an investment in the future . We've seen a lot of other companies, like IBMand GM, constantly try to fight very short-term battles instead of addiessing long-term problems ."

Two questions have persisted about Marlboro Friday. First, did the actions taken by PhilipMorris represent a necessary and effective strategy for preserving Marlboro's brand equity? Second,what were the implications of Marlboro Friday for brands and brand management .

. As Fortune asked, "Did big brands die the day the Marlboro Man fell off his horse?"23

- 22Chakravarty and Feldman, op . cit., p : 106.23Sellers, op . cit ., p . 68 . . .

12

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

Philip Morris: Marlboro Friday (A) . 596-001

Exhibit 1 Total Domestic Shipments by Major Cigarette Manufacturers, U .S.Market (billions of cigarettes)

1988 1989 1990 1991 1992

Philip Morris 219.3 219.5 220.6 220.7 214.3-R .J. Reynolds

Brown & Williamson177.3,- 61 .1

149.459.5

154.639.8

- 141 .756.7

1.46 .260 .2

Lorillard 45.6" . 41 .4 - 39.8 37.2 36.5American Tobacco 38.8 36.6 35.5 , 35.8 34.3Liggett & Myers 15.7 . 17 .1 17.7 17.3 215.2Total - 557.8 523.5 522.0 509.4 506.7

Source: Adapted from Marc I. Cohen and Gavin Launder, The Tobacco Handbook. -- New York: Goldman Sachs, April 8, 1994, p . 24.

Exhibit 2 1992 Net Revenues and Operating Contributionfrom U.S. Tobacco Operations of Major Cigarette'Manufacturers'

Net Revenues($ millions) "

OperatingContribution($ millions)

Philip Morris $9,882 . $5,186R.J. Reynolds 6,165 2,112Brown & Williamson NA 510Lorillard 2,185 915American Tobacco 1,443 536Liggett & Myers 606 52

Source: Adapted from data presented in corporate annual reportsand Marc 1. Cohen and Gavin Launder The TobaccoHandbook, New York: Goldman Sachs, April 8, 1994, .-pp:35-58. - - . . . "

All entries in this table refer to sales within the U .S . market only.

W

13 _

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001 -14 -

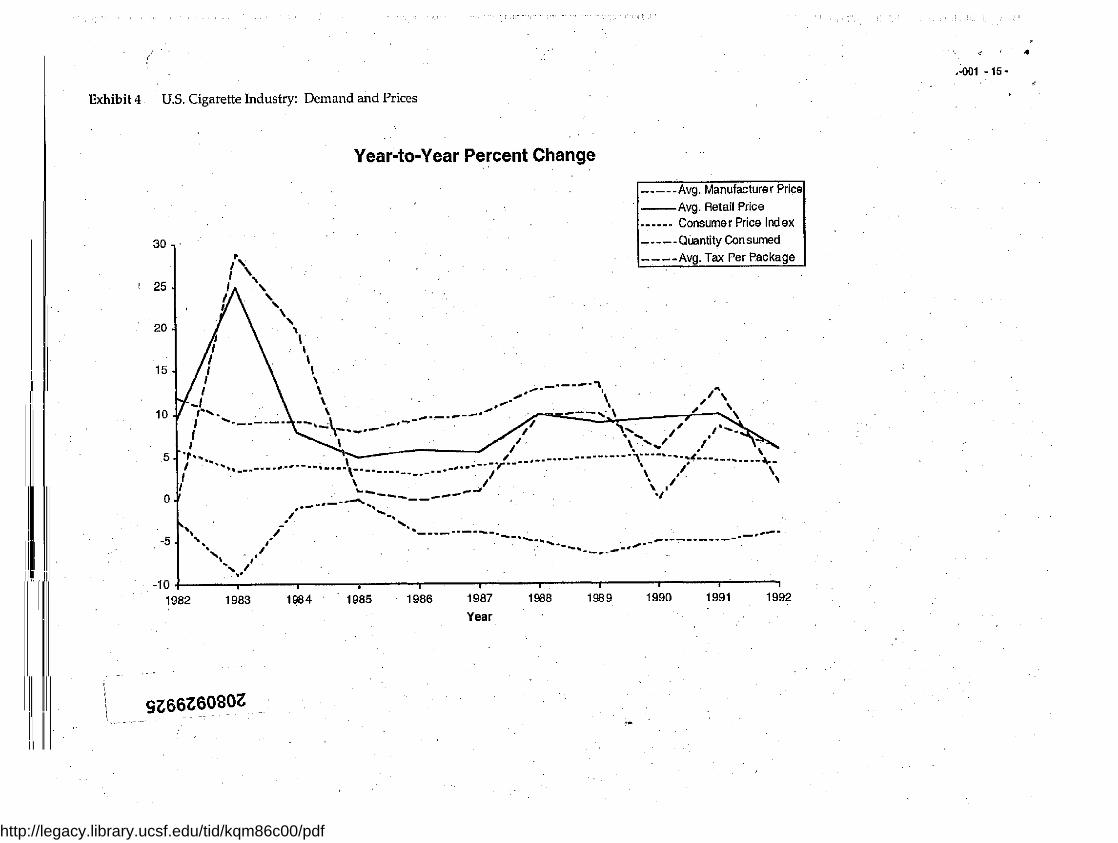

Exhibit 3 Percent Annual Changes in Manufacturer Prices, Retail Prices, Consumer Price Index, and Consumption in the U.S. Cigarette Market, 1982-1993

1982 - 1983 1984 1985 1986 .1987 1988 1989 . 1990 1991 1992

Average retail price per pack $0.72 $0.87 $0.94 $0.99. $1 .05 $1 .11 $1 .22 $1 .33 $1 .46 $1 .61 $1 .72

% Annual Change in :

Average manufacturer price - 11 .4% 8.9'0 . 9.1% 8.2% 9.6% 12.2% 12.8'/e 1 .4% 9.0% 7.3%aAverage retail price 9.3% 20.8% 8.0% 5.3% 6.1% 5.7% . 9.9% 9.0% 9.8% 10.3% 6.8%Consumer price index 6.2% 3.2% 4.3% 3.5% 1 .9% . 3.7% 4.1 % 4.8% 5.4'/0 4.2% 3.0%Average Federal and State Tax per package° 1 .4% 24.2% 17.2% 1 .9% . 0.9% 2.2% 10.4% 10.5% 7.7% 12.8% 2 .4%

Total U .S. consumption : . .

Billions of cigarettesb 634.0 600.0 . 600.4 . 594.0 583.8 575.5 562.5 540.0 525.0 510.0 500.0Millions of dollars' . . $23,525 $26,840 $28,750 $30,250 $31,800 $33,560 $34,700 $37,400 . $39,500 $42,850 $45,790

% Annual Change in unit consumption . -0.9% -5.4"/e 0.1% 1 .1% -1 .7% -1 .5% -2.2% -4.0% -2.8% -2.9% -2.0%

Adapted from Marc I. Cohen and G2vin Launder, The Tobacco Handbook, New York: Goldman Sachs Co., April 8, 1994 .

eUnited States Department of Ayriculture, Economic Research Service, Tobacco Situation and Outlook Report, April 1994 and September 1992 .

United States Department of Agriculture, Agricultural Marketing Service, Annual Report on Tobacco Statistics, 1993, 1988, 1983 .

°Calculated from data presented in U .S. Department of Health and Human Services, Preventing Tobacco Use Among Young People : A Report of the Surgeon General, WashingtonD.C .: Superintendent of Documents, U .S. Government Printing Office, 1994, p . 268 . .

Note :

A change in manufacturer price does not necessarily imply a change in retail price, as the two prices are set independently .

The consumption data provided in this exhibit may differ from the data on domestic shipments presented in Exhibit 1 due to cigarettes imported into the United States, as well aschanges in retailer and wholesaler inventories .

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

.•001 -15-

1

Exhibit 4 U.S. Cigarette Industry: Demand and Prices

Year-to-Year Percent Change

i 25

20

15

10

5

0

30

_.__.Avg . Manufacturer Price-Avg . Retail Price. . . ... Consumer Price Index_ _-piiantityConsumed----Avg. Tax Per Package

_ . ._- ---•- i •~------ =+~ ---- ., - •- - l-•-----•-------

---------------,-10

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 -

. Year

9Z66Z6080Z

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001 Philip Morris: MariboroFriday(A)

Exhibit 5 Total Cigarette Brand Introductions; 1970-1992

Before 1970 1970-1979 1980-1984 1985-19891990-1992

Philip Morris 30 - 17 18 43 24R.J. Reynolds 12 22 17 2 0Brown & Williamson 26 14 . 17 . 35 23Loriltard . 12 24 22 19 17American Tobacco - 18 . 18 11 23 37 -Liggett & Meyers 22 11 17 12 2Total 120 106 102 134 - 103

Source:' Adapted from 1993 Maxwell Tobacco Fact Book, Raleigh, North Carolina : Tobacco- Reporter, pp. 1-18 to 1-29 , . .

Note: This table lists the new brands, and product varieties introduced by the six major cigarette, manufacturers . Some of these brands were later discontinued or modified through actions such as repackaging, reintroductions, or name changes

: . - - - - ,

Exhibit 6 Market Share and Advertising Expenditures of Major CigaretteBrands, 1991-1992

. -'Unit Market Share

AdvertisingExpenditures($ miltions)

Brand Owner 1991 1992 1991 1992

Marlboro -Winston

PMRJR

25.8% .7 .5

24.4% -6.8

$101 .646.0

$85.914.3 -

Basic' . PM - 0.0 2.3 0.0 . 0.0GPC' B&W - 2.1 4.2 W0 0.0Newport , -Doral' -

LorillardRJR

4.74.6

4.84.4

- 43.61 .2

35.98 .1

SalemCamel

RJR .RJR -

5.44.0

4.94.1 -

9.733.8

9.523.0

Kool B&W 4.6 ' 4.3 19.5 5.7Benson & Hedges PM . 3.2 3.1 - 16.1 9.4Merit PM 3.1 3 0 11 .0 . 31 .2Total, above brands .

.

. 65.0 66.3,

282.5 . 223.0All other brands . 35. 33.7 196.0 147.0

Grand total 100.0% 100.0% $478.5 - $370 .0

Source: Adapted from Ira Teinowitz, "Marlboro Friday, SuAen Sunday for Smokes,"Advertising Age, August 28, 1994, pp. 28-29; and Ira Teinowitz, "Risky Promos, 'Price Cuts Assure Smokes' Shakeout," Advertising Age, September 29, 1993,p . .16 .

aDenotes discount brands .

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

Philip Morris : Marlboro Friday (A) 596-001

I Exhibit 7 Total Domestic Cigarette Advertising and Promotional Expendituresa,1986-1990

- Share of Expenditures f%)Type of Advertisinp/promotion 1986 1987 1988 1989 1990

Newspapers - 5.0 3.7 3.2 2.1 1 .8 :Magazines . 14 .3 12 .3 10.8 10.5 ' 8.2 .Outdoor- . . 12 .7 - 10.5 - 9.7 9.9 9.4Transit - 1 .5 1 .4 1 .4 1.4 1 .5Total media advertising (33 .5) . (27 .9) . - (25.1) (23.9) (20 .9)Point-of-purchase 5.7 - 5.9 . 6.8 - . 6.7 . 7 .6Promotional allowances 26.4 . 27 .2 26.9 27.6 25.6Sampling distribution . . 4.1 . 2 .1 2.3- 1 .6 2.5Speciaity item distribution . 8.8 15.2 _ 5.6 - - 7.3 . - 7.7 .Public entertainment 3.0 2.8 . 2.7 2.5 ~ 3.1Direct mailEndorsements and testimonials

7.9 7.3 1 .3 - 1 :3 1.3

Coupons and retail value-addedAll others

-10 .6

-11 .6

. 26.72.4

. 26.5 .

. 2.529.6

1 .6(Total promotion) (66.5) - (72.1) (74.9) ~ . (76.1) (79.1)

Total advertising and promotion . . 100.0% 100.0% ; : 100.0% 100.0% . 100.0%,

Total ezpenditures ($ millions) $2,383.357 $2,580.504 $3,274.853 $3,616 .993 $3,992.008

Source: Adapted form data reported in U .S. Department of Health and Human Services, Preventing Tobacco .Use Among Young People: A Repoit of the Surgeon General, Washington, D .C . : Superintendent ofDocuments U .S. Government Printing Office, 1994, pp . 164-165. The original source is : Federal TradeCommission, Report .to Congress for 1990 : Pursuant to the Federal Cigarette Labelling and Advertising-Act, Washington, D .C . : FTC, 1992 .

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001 Philip Morris : Marlboro Friday (A)

Exhibit 8 Social, Economic, and Demographic Characteristics of CigaretteSmokers

Percent of AdultsU.S. Population Cigarette Smokers

Gender :Male 47.7% 52.3%Female .52 .3 47.7

Total 100.0% . 100.0% . .

Age :18-34 years old 37.3% 42.0%35-54 years old 34.7 38.755 or older 28.0 _19.3-

Total 100.0% 100.0%

Graduated College: - . 19.6% 13.1 %

Occupation :Prof essionaUexecutive/mahagerial 17.1% 13.40/6Clerical/salesftechnical 19.3 18.0

.Precision/crafts/repair 7 .1 9.8

-Other employed 19.1 . , ~ 23.4

Not employed 37.4 - 35.4

Total 100.0%.100.0%

Annual Household Income :000 or more$75 12.6% . 8.9%,

, 50,000-74,999~ . 17.7 . 15 .730,000-49,999 . 26.8 - .

-27.2

. 10,000-29,999 32 .1 .1 8

35 .113 1Less than $10,000

. Total0.

- 100.0% . '.

100.0%

Daily Newspapers :Read any 58.7% 54.5Read one daily 46.7 44.0

Subscribe to cable television 59 .8 , 58 .9

Source: Calculated from data presented in Mediamark Research Shopping &Tobacco Products Report, Spring 1993, p . 144

1,8 .

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

Philip Morris ; Marlboro Friday (A) -

Exhibit 9 Unit Market Share of Discount Cigarette Brands, U .S. Market

596-001

Market Share

40 %

--------------------------------------------------------- -35% - -- - --

30% - - - - - - - - - - - - - - - - - - - - --- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

__- ----------------------------- _----- _------- _________25% -

20% _________________ .___-_______._________________ :-_____

------------------------------------- --15% - ---- -

10% -----------------'-'------------ - - - - - - - - - - - - - -- - - - - - - - - - - -~

--------------------------------------5%

0%1981 1982 19813 1984 1985 1986 1987 1988 1,989 1990 1991 1992

Year .

Source:Adaptedfromdatapresentedin1993Maawe//TotxaccoFactBook,Relegh,NorthCardina SPECCOMMInternaEmal,- 1994. p.16 . . . . . . . . . . .

19

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf

596-001

Exhibit 10 Selected Philip Morris Brand Names and Categories

Philip Morris: Marlboro Friday (A)

Category Brand

Cigarettes:Premium brandsDiscount brands

Beer-

Grocery Products:Baked goodsCoffee and tea 'Soft drink mixesCerealsCondiments and saucesConfections and dessertsDry groceryFrozen productsCheeseOther dairy productsOther food products

Source: Annual reports

Marlboro, Bensen & Hedges, Virginia Slims, Merit, Parliament- Cambridge, Basic, Alpine, Players, Bucks, Bristol - .

Miller, Meister Brau, Molson, Sharp's

Esteimann's, Oroweat, BoboliMaxwell House, Sanka, Brim, Yuban, Maxim, Crystal LightCountry Time, Kool-Aid, Tang, Capri SunPost, A1pha Bits, Grape-Nuts, Raisin Brand, Honeycomb, Bran'nolaBull's Eye Barbecue Sauces, Miracle Whip, Seven SeasToblerone Chocolate Bars, Jell-O 'Log Cabin Syrups,.Stove Top, Shake 'N Bake, - , - -Lendei s Bagels, CoollNhip, Tombstone PizzaVelveeta, Cracker Barrel, Light n LivelyPhiladelphia Cream Cheese, Temp-Tee, Breakstone's, Bryers YogurtDiGiorno Pasta & Sauces, Oscar Meyer, Claussen Pickles, Cheez Whiz

Exhibit 11 Marlboro- UnitMarket Share in the U.S. Market,1980-1992

1980 17.7%.

1984 21.61985 .22.51986 ' 23.11987 23.61988 _ 24.61969 26.21990 25.8 .1991 25.81992 24.4

Source: Calculated from datareported in John C .Maxwell, Jr., "PM's MarketShare.Gains, RJR's Due to .Rise; Top Remain Same,"Tobacco International,December 26, 1990, p. 15

, and 1993 Maxwell Tobacco- Fact Book, 1-38-1-43

20

http://legacy.library.ucsf.edu/tid/kqm86c00/pdf