policy evaluation and robustness with the … yoo.pdf · policy evaluation and robustness with the...

TRANSCRIPT

Policy Evaluation and Robustness with theMacroeconomic Model Data Base

Jinhyuk Yoo

Goethe University Frankfurt, IMFS

January 16, 2014

MMB Team (IMFS) 1st Workshop, London January 16, 2014 1 / 21

Outline I

1 Introduction

2 Policy Evaluation and Robustness

3 Conclusion

MMB Team (IMFS) 1st Workshop, London January 16, 2014 2 / 21

Outline I

1 Introduction

2 Policy Evaluation and Robustness

3 Conclusion

MMB Team (IMFS) 1st Workshop, London January 16, 2014 3 / 21

The state of macro modelling 2015

Criticism and debate following macroeconomists’ failure to providesufficient warning of the risk of financial crisis

New modelling approaches: Financial sector and banking, moneyand credit, labor markets, international linkages, instruments andeffects of monetary, fiscal and macroprudential policies

Need of a level-playing field on which models can compete interms of empirical benchmarks and robustness of policyrecommendations

MMB Team (IMFS) 1st Workshop, London January 16, 2014 4 / 21

Macroeconomic Model Data Base 2.0

A tool that can be useful for research and policy analysis usingstructural macroeconomic models (in development since 2007)

in the spirit of...

leading economists - among them Nobel prize winners PaulSamuelson and Franco Modigliani - warned of the danger of an’intellectual monopoly’ in economics and demanded a ’pluralisticspirit in economic science that respects different approaches andencourages critical and tolerant dialogue’.

MMB Team (IMFS) 1st Workshop, London January 16, 2014 5 / 21

Systematic approach to model comparison

Many models, few comparisons, why?

The standard approach to model comparison is cumbersome andrequires a lot of resources, multiple research teams, each workingwith its own model, multiple meetings, limited set of exercises

- Brookings Institution:1988-89-93, Bryant, Currie, Frenkel, Masson,Portes (eds.) (1989); Bryant, Hooper, Mann (eds.) (1993)

- NBER: Taylor (ed.) (1999)

- IMF: Coenen et al. (2010), 17 authors, 7 models.

MMB Team (IMFS) 1st Workshop, London January 16, 2014 6 / 21

Wieland et al.(2012), Journal of Economic Behavior and Organisation

Formal exposition of comparative approach (augmenting modelswith common policy rules and common, comparative variables)

A macroeconomic model archive

A computational platform (Matlab, Dynare) that allows individualresearchers to conduct comparisons relatively easily, frequentlyand on a large scale

MMB Team (IMFS) 1st Workshop, London January 16, 2014 7 / 21

Macroeconomic model data base: new release 2.0(2014 March)

New Version offers:- new user-friendly interface- new models with financial frictions or banking sector (61 models as

of now)- many new functions for comparative and exploratory model analysis

Software requirements

- Matlab

- Dynare 4: www.dynare.org

- Model Base files: www.macromodelbase.com

MMB Team (IMFS) 1st Workshop, London January 16, 2014 8 / 21

Outline I

1 Introduction

2 Policy Evaluation and Robustness

3 Conclusion

MMB Team (IMFS) 1st Workshop, London January 16, 2014 9 / 21

Exercise 1: Implications for monetary policytransmission

Consequences of economic activity and inflation in response to anunexpected change in policy rate?

It is hard to identify effects that monetary policy alone causes.

A solution: build a structural macroeconomic model and conduct a policyexperiment.

Implications drawn from the model are model-specific by construction.

Let’s do a comparative exercise with four models from Modelbase togauge the extent of differences between models regarding to monetarypolicy transmission.

A monetary policy shock is defined as a surprise deviation from systemicpolicy behavior.

MMB Team (IMFS) 1st Workshop, London January 16, 2014 10 / 21

Choices of models and a policy rule

The models chosen:I Taylor (1993) G7 countries model (G7 TAY93), used in original

design of the Taylor rule.I Smets and Wouters (2007) US model (US SW07), one of the

best-known (New Keynesian) models.I De Graeve (2008) US model (US DG08), (New Keynesian) model

enriched with a macro-financial linkage.I Meh and Moran (2010) US model (NK MM10), (New Keynesian)

model with banking sector.

A common policy rule used: Smets and Wouters (2007) rule.

Let’s do the exercise now!

MMB Team (IMFS) 1st Workshop, London January 16, 2014 11 / 21

Comparative performance of models under monetarypolicy shock

0 5 10 15 20-0.45

-0.4

-0.35

-0.3

-0.25

-0.2

-0.15

-0.1

-0.05

0

Output Gap

0 5 10 15 20-0.18

-0.16

-0.14

-0.12

-0.1

-0.08

-0.06

-0.04

-0.02

0

Inflation

0 5 10 15 20-0.2

0

0.2

0.4

0.6

0.8

Interest Rate

0 5 10 15 20-0.45

-0.4

-0.35

-0.3

-0.25

-0.2

-0.15

-0.1

-0.05

0

Output

US_SW07

US_DG08

G7_TAY93

NK_MM10

IRF Mon. Pol. Shock: SW rule

MMB Team (IMFS) 1st Workshop, London January 16, 2014 12 / 21

Exercise 2: Interactions of monetary andmacroprudential policies

Motivation: which policies should address financial imbalances?Model: Kannan, Rabanal and Scott (2012), Monetary and

macroprudential policy rules in a model with house price booms, B.E. Journal in

Macroeconomics: Contributions, Vol. 12,1

Brief overview on model structureI Two types of households: patient HHs and impatient HHs.I Households decide on consumption, housing investment, saving

and work.I Banks take deposits from savers and lend them to borrowers.I Following the spirit of BGG financial accelerator, the lending deposit

spread positively depends on households’ leverage (LTV ratios).I The spread also relies on mark-up charged over funding and a

macro-prudential instrument.

MMB Team (IMFS) 1st Workshop, London January 16, 2014 13 / 21

Credit spread in Kannan et al. (2012)

RLt

Rt= vtF (

BBt

PDt D

Bt

)τt

vt: financial shock, down if greater bank competition, or reduction in perceived risk.Bt: debt of home-owners, PD

t DBt : housing value, BB

t

PDt DB

t: loan to value ratio, F (·)

increasing in leverage.τt: macroprudential instrument τt = f(BB

t ), i.e. loan provisions, bank capitalrequirement

Credit accelerator at work:

Relaxation of lending standards, lending rates down, increase in housingprices and investment, collateral value increase, households take outmore loans and so on.

MMB Team (IMFS) 1st Workshop, London January 16, 2014 14 / 21

Four policy regimes

KRS baseline interest rate rule

it = 0.7it−1 + 0.3[i∗ + 1.3(πt−1 − π∗) + 0.5qt−1] (1)

KRS baseline & leaning rule

it = 0.7it−1 + 0.3[i∗ + 1.3(πt−1 − π∗) + 0.5qt−1 + 0.1bt−1]

KRS baseline (1) & macroprudential policy rule

τt = 0.1bt−1

Taylor’s ruleit = i∗ + 1.5(πat − π∗) + 0.5qt

i: policy rate, π: the annualized q-to-q rate of inflation, π∗: inflation targetq: output gap, πa: the annualized y-on-y rate of inflation,b: the credit growth

MMB Team (IMFS) 1st Workshop, London January 16, 2014 15 / 21

Effects of a financial shock across policy regimes

0 5 10 15 20-0.1

0

0.1

0.2

0.3

0.4Real GDP

0 5 10 15 20-0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4Inflation

0 5 10 15 20-0.5

0

0.5

1

1.5

2Policy Rate

0 5 10 15 20-1

0

1

2

3

4

5

6Nominal Debt Growth

KRS baseline interest rate rule

KRS baseline & leaning rule

KRS baseline & macroprudential rule

Taylor´s rule

a larger set of variables

MMB Team (IMFS) 1st Workshop, London January 16, 2014 16 / 21

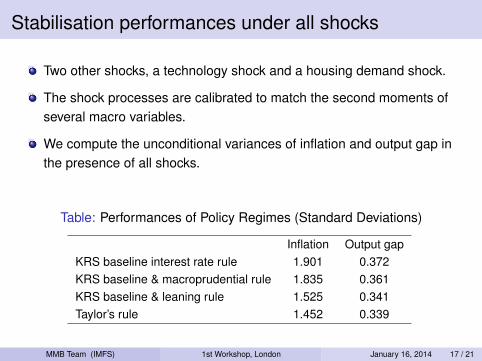

Stabilisation performances under all shocks

Two other shocks, a technology shock and a housing demand shock.

The shock processes are calibrated to match the second moments ofseveral macro variables.

We compute the unconditional variances of inflation and output gap inthe presence of all shocks.

Table: Performances of Policy Regimes (Standard Deviations)

Inflation Output gapKRS baseline interest rate rule 1.901 0.372KRS baseline & macroprudential rule 1.835 0.361KRS baseline & leaning rule 1.525 0.341Taylor’s rule 1.452 0.339

MMB Team (IMFS) 1st Workshop, London January 16, 2014 17 / 21

Implications

The stabilization performance of the economy facing credit boomcan be improved either by monetary policy leaning against creditmarket development or by including macroprudential policy.

However, the original Taylor rule performs quite well even withoutadding macroprudential policy.

MMB Team (IMFS) 1st Workshop, London January 16, 2014 18 / 21

Outline I

1 Introduction

2 Policy Evaluation and Robustness

3 Conclusion

MMB Team (IMFS) 1st Workshop, London January 16, 2014 19 / 21

Conclusion

MacroModelBase is an open platform for comparativemacro-financial modelling and policy evaluation.

Comparative exercises across competing reference models oracross policy prescriptions improve policy advice.

More to come: including more macro models with financial sector,forecasting and effects of alternative expectation formations,robustness analysis for policy rules

MMB Team (IMFS) 1st Workshop, London January 16, 2014 20 / 21

Appendix: Efffects of a financial shock

0 5 10 15 20-0.1

0

0.1

0.2

0.3

0.4Real GDP

0 5 10 15 20-0.5

0

0.5

1

1.5Inflation

0 5 10 15 20-0.5

0

0.5

1

1.5

2Policy Rate

0 5 10 15 20-2

0

2

4

6Nominal Debt Growth

0 5 10 15 20-1

-0.5

0

0.5

1

1.5Residential Investment

0 5 10 15 20-0.1

0

0.1

0.2

0.3

0.4Consumption

0 5 10 15 20-0.1

0

0.1

0.2

0.3

0.4Nominal House Price

0 5 10 15 20-2

-1.5

-1

-0.5

0

0.5Lending Rate

0 5 10 15 200.1

0.2

0.3

0.4

0.5Shock Process

KRS baseline interest rate rule

KRS baseline & leaning rule

KRS baseline & macroprudential rule

Taylor´s rule

Back

MMB Team (IMFS) 1st Workshop, London January 16, 2014 21 / 21