portfolio models mgt 4850 spring 2007 university of lethbridge

Post on 21-Dec-2015

218 views

TRANSCRIPT

Portfolio Models

MGT 4850

Spring 2007

University of Lethbridge

Introduction

• Portfolio basic calculations

• Two-Asset examples– Correlation and Covariance– Trend line

• Portfolio Means and Variances

• Matrix Notation

• Efficient Portfolios

Review of Matrices• a matrix (plural matrices) is a rectangular

table of numbers, consisting of abstract quantities that can be added and multiplied.

Adding and multiplying matrices

• Sum

• Scalar multiplication

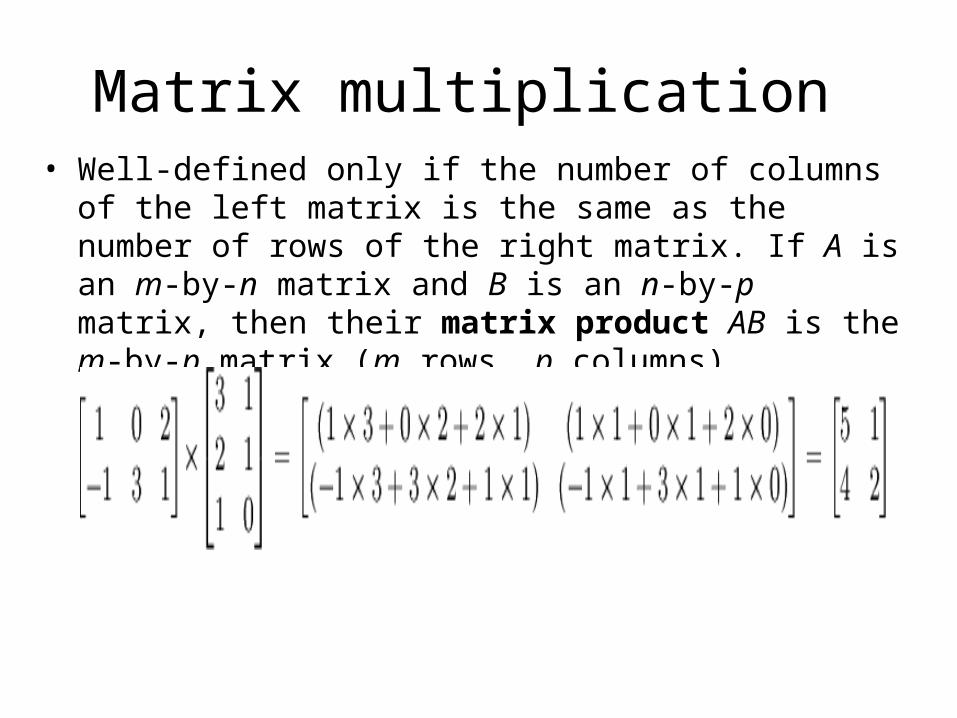

Matrix multiplication • Well-defined only if the number of columns of the left

matrix is the same as the number of rows of the right matrix. If A is an m-by-n matrix and B is an n-by-p matrix, then their matrix product AB is the m-by-p matrix (m rows, p columns).

Matrix multiplication

• Note that the number of of columns of the left matrix is the same as the number of rows of the right matrix , e. g. A*B →A(3x4) and B(4x6) then product C(3x6).

• Row*Column if A(1x8); B(8*1) →scalar

• Column*Row if A(6x1); B(1x5) →C(6x5)

Matrix multiplication properties:

• (AB)C = A(BC) for all k-by-m matrices A, m-by-n matrices B and n-by-p matrices C ("associativity").

• (A + B)C = AC + BC for all m-by-n matrices A and B and n-by-k matrices C ("right distributivity").

• C(A + B) = CA + CB for all m-by-n matrices A and B and k-by-m matrices C ("left distributivity").

The Mathematics of Diversification

• Linear combinations

• Single-index model

• Multi-index model

• Stochastic Dominance

Return

• The expected return of a portfolio is a weighted average of the expected returns of the components:

1

1

( ) ( )

where proportion of portfolio

invested in security and

1

n

p i ii

i

n

ii

E R x E R

x

i

x

Two-Security Case

• For a two-security portfolio containing Stock A and Stock B, the variance is:

2 2 2 2 2 2p A A B B A B AB A Bx x x x

portfolio variance

• For an n-security portfolio, the portfolio variance is:

2

1 1

where proportion of total investment in Security

correlation coefficient between

Security and Security

n n

p i j ij i ji j

i

ij

x x

x i

i j

Minimum Variance Portfolio

• The minimum variance portfolio is the particular combination of securities that will result in the least possible variance

• Solving for the minimum variance portfolio requires basic calculus

Minimum Variance Portfolio (cont’d)

• For a two-security minimum variance portfolio, the proportions invested in stocks A and B are:

2

2 2 2

1

B A B ABA

A B A B AB

B A

x

x x

The n-Security Case (cont’d)

• A covariance matrix is a tabular presentation of the pairwise combinations of all portfolio components– The required number of covariances to

compute a portfolio variance is (n2 – n)/2

– Any portfolio construction technique using the full covariance matrix is called a Markowitz model

Single-Index Model

• Computational advantages

• Portfolio statistics with the single-index model

Computational Advantages

• The single-index model compares all securities to a single benchmark– An alternative to comparing a security to each

of the others

– By observing how two independent securities behave relative to a third value, we learn something about how the securities are likely to behave relative to each other

Computational Advantages (cont’d)

• A single index drastically reduces the number of computations needed to determine portfolio variance– A security’s beta is an example:

2

2

( , )

where return on the market index

variance of the market returns

return on Security

i mi

m

m

m

i

COV R R

R

R i

Multi-Index Model

• A multi-index model considers independent variables other than the performance of an overall market index– Of particular interest are industry effects

• Factors associated with a particular line of business

• E.g., the performance of grocery stores vs. steel companies in a recession

Multi-Index Model (cont’d)

• The general form of a multi-index model:

1 1 2 2 ...

where constant

return on the market index

return on an industry index

Security 's beta for industry index

Security 's market beta

retur

i i im m i i in n

i

m

j

ij

im

i

R a I I I I

a

I

I

i j

i

R

n on Security i

Basic Mechanics of Portfolio calculations

• Two Asset Example p.132

• Continuously compounded monthly returns – mean variance std deviation

• Covariance and variance calculations p.133

• Correlation coefficient as the square root of the regression R2

• Portfolio mean and variance p.135

Portfolio Mean and Variance

• Matrix notation; column vector Γ for the weights transpose is a row vector ΓT

• Expected return on each asset as a column vector or E its transpose ET

• Expected return on the portfolio is a scalar

(row*column)

Portfolio variance ΓTS Γ (S var/cov matrix)