portfolio theory and the capital asset pricing model 723g28 linköpings universitet, iei 1

TRANSCRIPT

1

Portfolio Theory and the Capital Asset Pricing Model

723g28Linköpings Universitet, IEI

2

We have learned from last chapter risk and return: (that for an individual investor)Combining stocks into portfolios can reduce standard deviation, below the level obtained from a simple weighted average calculation.

Rational investors maximize the expected return given risks. Or minimize risks given expected return.

3

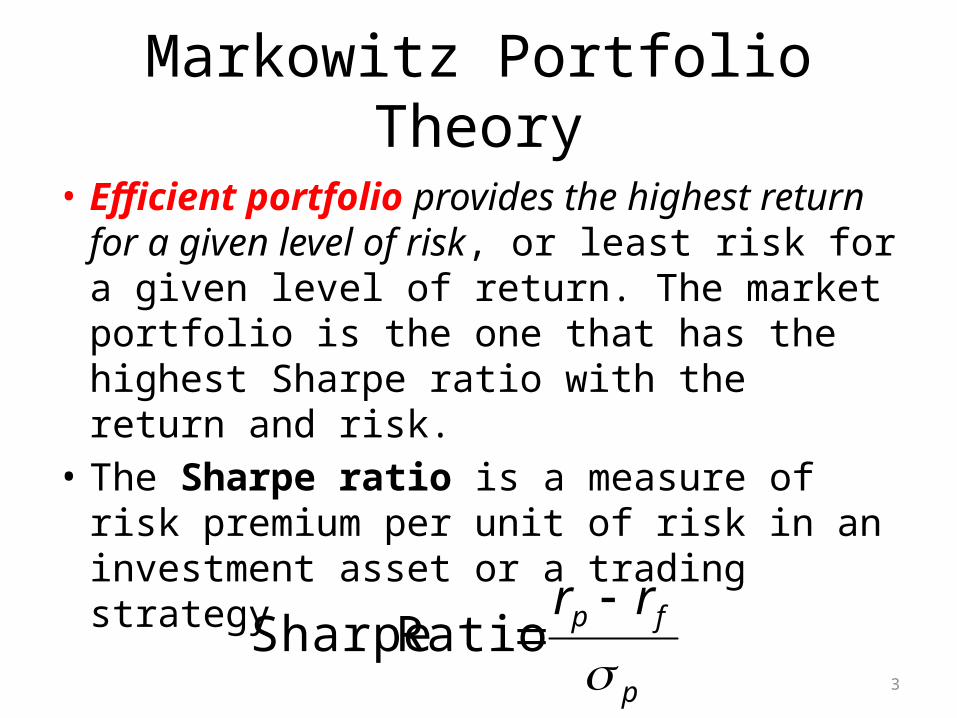

Markowitz Portfolio Theory

• Efficient portfolio provides the highest return for a given level of risk, or least risk for a given level of return. The market portfolio is the one that has the highest Sharpe ratio with the return and risk.

• The Sharpe ratio is a measure of risk premium per unit of risk in an investment asset or a trading strategy

p

fp rr

Ratio Sharpe

4

Effect of diversification on variance

Assuming the following:• N independent assets, i.i.d. with covariance=0,• σ= std of the return• r= expected return• Equally weighted portfolio, Then, we have: the more the assets are in, the lower the standard deviation σ. σ portfolio =

5

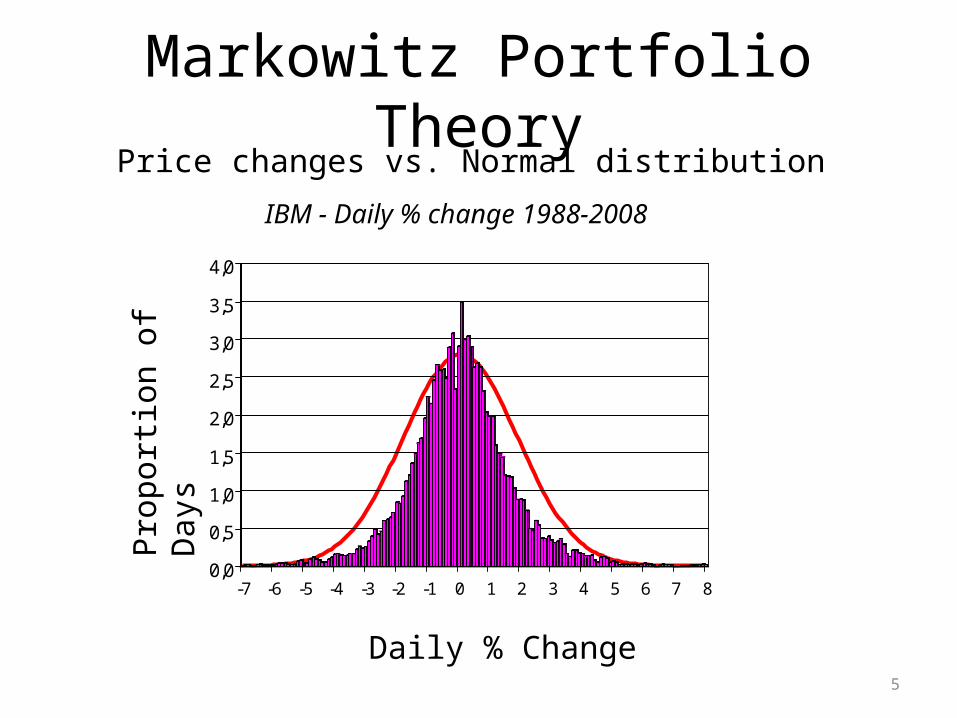

Markowitz Portfolio TheoryPrice changes vs. Normal distribution

IBM - Daily % change 1988-2008

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

-7 -6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8

Pro

port

ion

of D

ays

Daily % Change

6

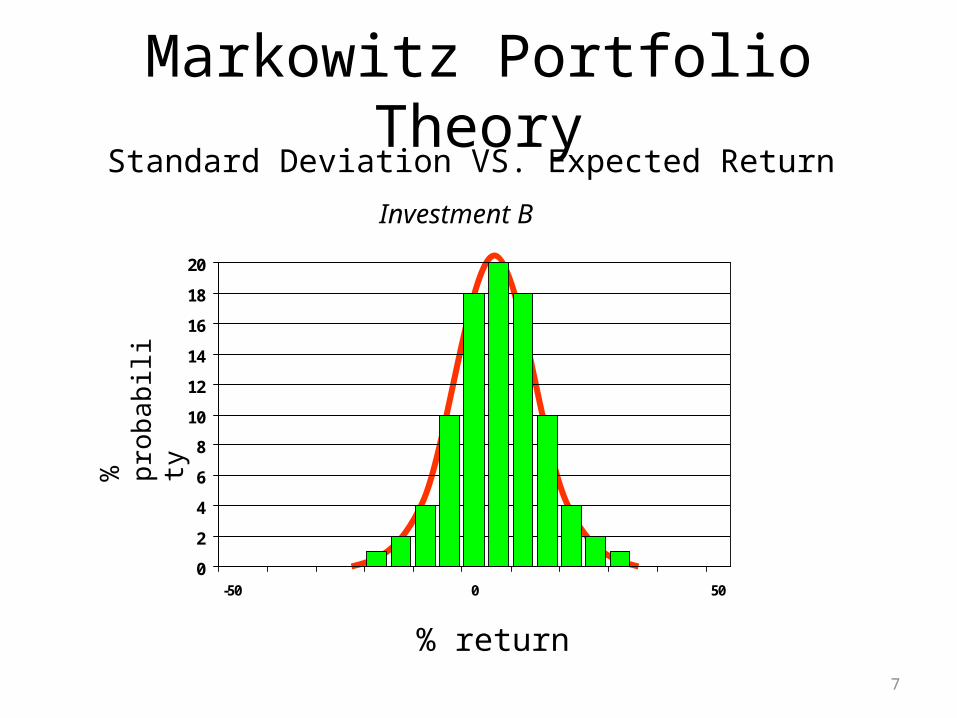

Markowitz Portfolio TheoryStandard Deviation VS. Expected Return

Investment A

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

%

prob

abili

ty

% return

7

Markowitz Portfolio TheoryStandard Deviation VS. Expected Return

Investment B

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

%

prob

abili

ty

% return

8

Markowitz Portfolio TheoryStandard Deviation VS. Expected Return

Investment C

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

%

prob

abili

ty

% return

9

0.00 5.00 10.00 15.00 20.00 25.000

1

2

3

4

5

6

7

8

9

10

Campbell Soup

40% in Boeing

Boeing

Standard Deviation

Exp

ecte

d R

etur

n (%

)

Markowitz Portfolio Theory Expected Returns and Standard Deviations vary given different

weighted combinations of the stocks

10

A two asset portfolio constructed with % of both assets, allow short selling of one assets

0.05 0.07 0.09 0.11 0.13 0.15 0.17 0.19 0.210.015

0.017

0.019

0.021

0.023

0.025

0.027

Series1

Market volatility

Market

Capital Market Line

11

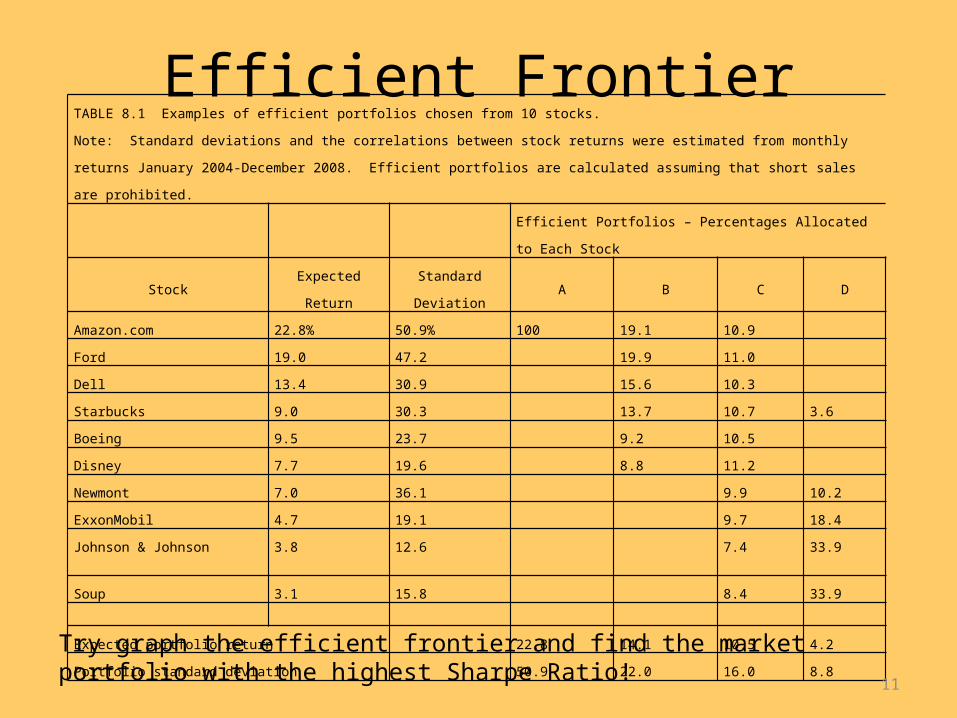

Efficient FrontierTABLE 8.1 Examples of efficient portfolios chosen from 10 stocks.

Note: Standard deviations and the correlations between stock returns were estimated from monthly returns January 2004-December 2008. Efficient

portfolios are calculated assuming that short sales are prohibited.

Efficient Portfolios – Percentages Allocated to Each Stock

Stock Expected Return Standard Deviation A B C D

Amazon.com 22.8% 50.9% 100 19.1 10.9

Ford 19.0 47.2 19.9 11.0

Dell 13.4 30.9 15.6 10.3

Starbucks 9.0 30.3 13.7 10.7 3.6

Boeing 9.5 23.7 9.2 10.5

Disney 7.7 19.6 8.8 11.2

Newmont 7.0 36.1 9.9 10.2

ExxonMobil 4.7 19.1 9.7 18.4

Johnson & Johnson 3.8 12.6 7.4 33.9

Soup 3.1 15.8 8.4 33.9

Expected portfolio return 22.8 14.1 10.5 4.2

Portfolio standard deviation 50.9 22.0 16.0 8.8

Try graph the efficient frontier and find the market portfolio with the highest Sharpe Ratio!

12

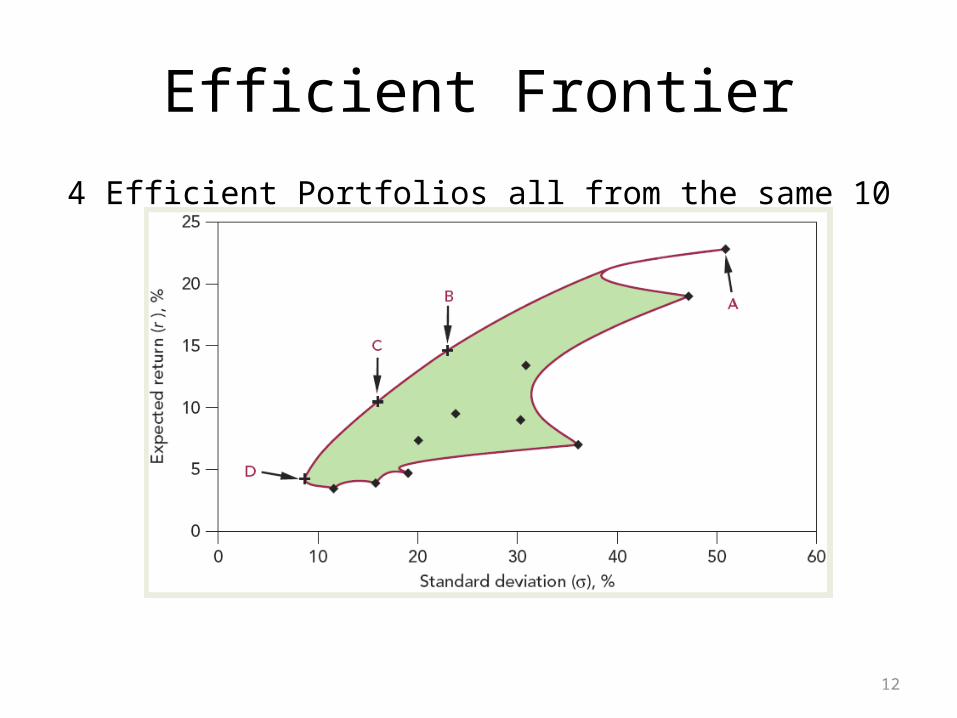

Efficient Frontier

4 Efficient Portfolios all from the same 10 stocks

13

Efficient Frontier

Standard Deviation

Expected Return (%)

Lending or Borrowing at the risk free rate (rf) allows us to exist outside the

efficient frontier.

rf

Lending

BorrowingS

T

The red line is the Capital Market Line, where you can hold a combination of the risk free assets and the market portfolio and get any returns you like.

Minimum variance portfolio

14

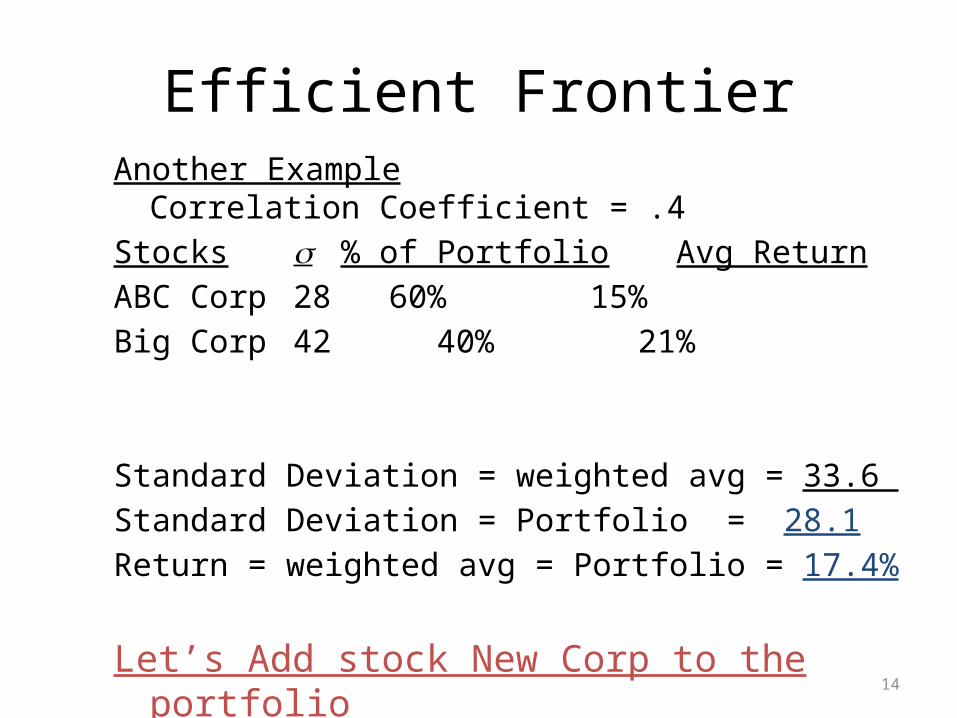

Efficient FrontierAnother Example Correlation Coefficient = .4Stocks s % of Portfolio Avg ReturnABC Corp 28 60% 15%Big Corp 42 40% 21%

Standard Deviation = weighted avg = 33.6 Standard Deviation = Portfolio = 28.1 Return = weighted avg = Portfolio = 17.4%

Let’s Add stock New Corp to the portfolio

15

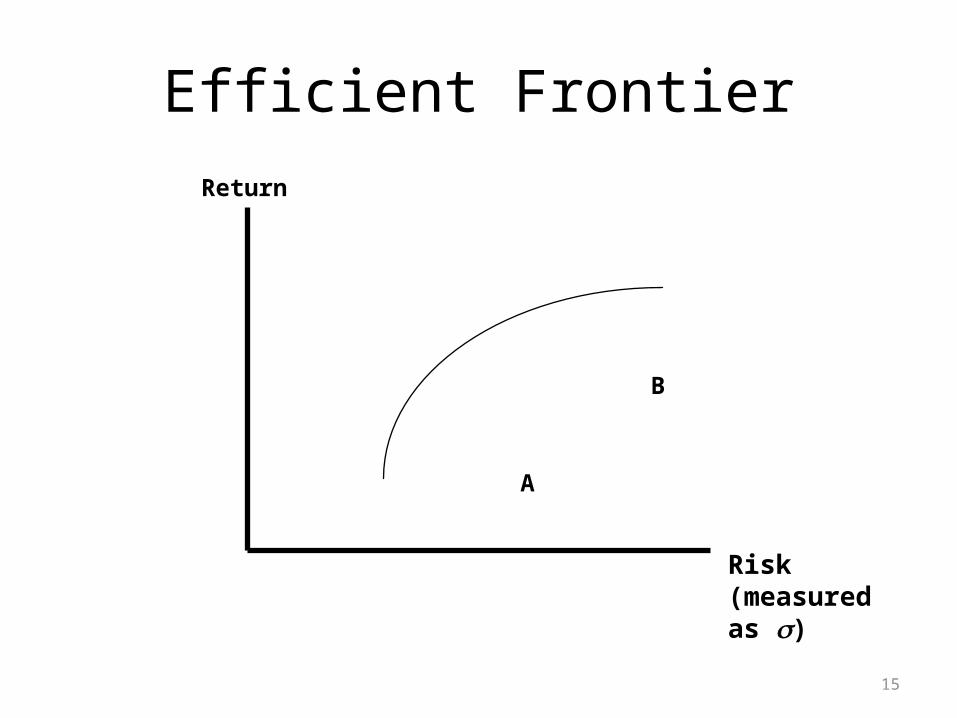

Efficient Frontier

A

B

Return

Risk (measured as s)

16

Efficient Frontier

A

B

Return

Risk

AB

17

Efficient Frontier

A

BN

Return

Risk

AB

18

Efficient Frontier

A

BN

Return

Risk

ABABN

19

Efficient Frontier

A

BN

Return

Risk

AB

Goal is to move up and left.

WHY?

ABN

20

Efficient FrontierThe ratio of the risk premium to the standard deviation is the Sharpe ratio.In a competitive market, the expected risk premium varies in proportion to portfolio standard deviation. P denotes portfolio. Along the Capital Market Line one holds the risky assets and a risk free loan.

p

fp rr

Ratio Sharpem

fm

p

fp rrrr

21

Capital Asset Pricing Model

CAPM

2

( )i f i m f

imi

m

r r r r

22

Security Market LineStock Return

.

rf

Market Portfolio

Market Return = rm

BETA

risk

1.0

Risk Free Return =

(Treasury bills)

2,0

ri

𝑟 𝑖=2 (𝑟𝑚−𝑟 𝑓 )

23

Efficient FrontierReturn

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

24

Capital Market LineReturn

Risk

.

rfRisk Free Return =

(Treasury bills)

Market Portfolio

Market Return = rm

Tangent portfolio

25

Security Market LineReturn

.

rf

Market Portfolio

Market Return = rm

BETA1.0

Risk Free Return =

(Treasury bills)

Market Risk Premium: Example

0

2

4

6

8

10

12

14

0 0,2 0,4 0,6 0,8 1

Beta

Exp

ecte

d R

etu

rn (

%)

Let,

4%

12%

Market Risk Premium = 8%

f

m

r

r

Example:

4%fr

8%market risk premium Market Portfolio (market return = 12%)

According to CAPM, the expected return on the asset is

( ) 4% 1.2 (8%) 13.6%f m fr r r r

27

Security Market Line: depicts the CAPMReturn

BETA

rf

1.0

SML

SML Equation = rf + β( rm - rf )

Security Market Line

28

Expected Returns

Stock Beta (β) Expected Return [rf + β(rm – rf)]

Amazon 2.16 15.4Ford 1.75 12.6Dell 1.41 10.2Starbucks 1.16 8.4Boeing 1.14 8.3Disney .96 7.0Newmont .63 4.7ExxonMobil .55 4.2Johnson & Johnson .50 3.8Soup .30 2.4

These estimates of the returns expected by investors in February 2009 were based on the capital asset pricing model. We assumed 0.2% for the interest rate r f and 7 % for the expected risk premium r m − r f .

29

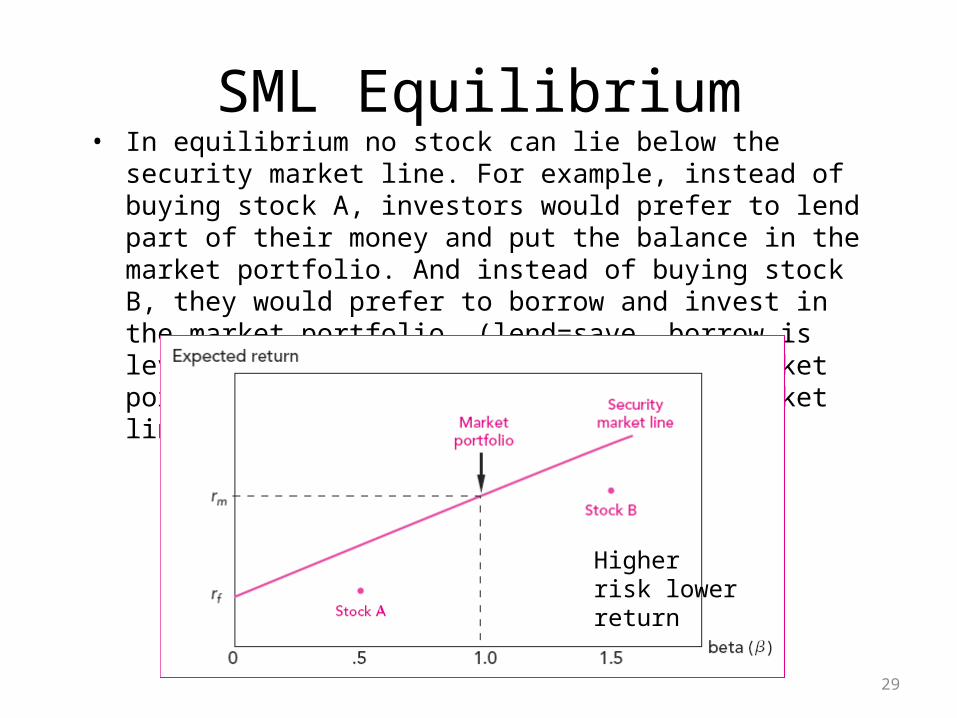

SML Equilibrium• In equilibrium no stock can lie below the security market line. For

example, instead of buying stock A, investors would prefer to lend part of their money and put the balance in the market portfolio. And instead of buying stock B, they would prefer to borrow and invest in the market portfolio. (lend=save, borrow is leveraging.) risk free assets and the market portfolio can span the whole Security market line)

Higher risk lower return

30

Testing the CAPM

Average Risk Premium 1931-2008

Portfolio Beta1.0

SML20

12

0

Investors

Market Portfolio

Beta vs. Average Risk Premium: low beta portfolio fared better than high beta

portfolio 1931-2008

31

Testing the CAPM

Portfolio Beta1.0

SML

12

8

4

0

Investors

Market Portfolio

Beta vs. Average Risk Premium

Average Risk Premium 1966-2008

32

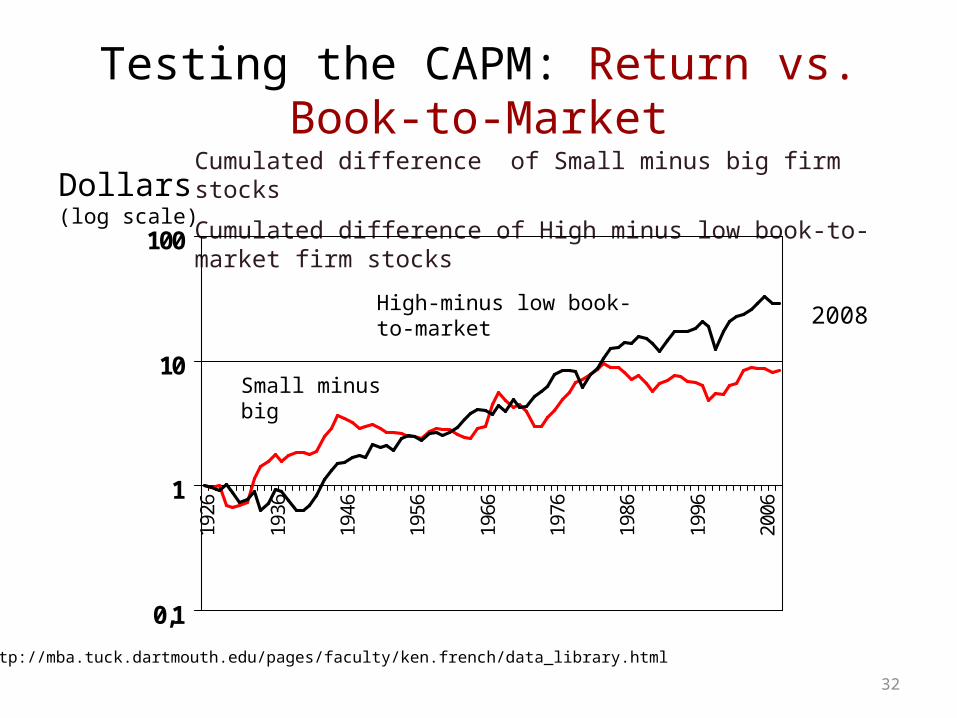

Testing the CAPM: Return vs. Book-to-Market

0,1

1

10

10019

26

1936

1946

1956

1966

1976

1986

1996

2006

High-minus low book-to-market

Dollars(log scale)

Small minus big

http://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

2008

Cumulated difference of Small minus big firm stocks

Cumulated difference of High minus low book-to-market firm stocks