powerpoint presentation · pdf filecarillion is extending the main stand at liverpool football...

TRANSCRIPT

2016 Interim Results24 AUGUST 2016

Carillion is extending the main stand at Liverpool Football Club’s world famous Anfield

Stadium under a £75 million contract to increase the stand’s capacity by around 8,500

and the total capacity of the stadium to some 54,000, while keeping the main stand

fully operational for all matches - a project that is now nearing successful completion.

RICHARD HOWSONGROUP CHIEF EXECUTIVE

Introduction

2

Carillion acquired a majority interest in Ask Real Estate in December 2015 and a

Carillion/Ask/Tristan Capital Partners joint venture is developing the impressive £180 million

Greengate project in Manchester of new office accommodation that is also being built by Carillion.

Agenda

Introduction

Financial results

Strategy and prospects

Richard HowsonGroup Chief Executive

Richard AdamGroup Finance Director

Richard HowsonGroup Chief Executive

3

Robust first-half performance

• First-half performance in line with expectations

− led by strong revenue and margin growth in support services

− average net borrowing similar to 2015 full-year average, in line with expectations

− balance sheet remains robust with £1.4bn of committed funding

• Strong work winning performance

– £2.5bn(1)

of new first-half orders and probable orders

– total order book of £17.4bn at 30 June 2016

– record revenue visibility of 98% for 2016

− pipeline of contract opportunities increased to £41.5bn

• Interim dividend increased by 2% to 5.8p

• Expect to make further progress in 2016 – no changes to our full-year expectations

DRIVEN BY STRATEGY AND BUSINESS MODEL

4

(1) Net of £0.2 billion of orders removed as a result of selling Public Private Partnership equity investments.

‘Living our values’ every day in everything we do, is fundamental

to the success of our integrated business model.

RICHARD ADAMGROUP FINANCE DIRECTOR

Financial results

5

Financial highlights

• Strong revenue growth of 10% to £2,487.1m (2015: £2,258.6m)

− led by 8% growth in support services

• Underlying operating profit(1)

up 5% to £121.3m (2015: £115.3m)

– led by 30% growth in support services

• Underlying profit from operations(2)

up slightly to £112.7m (2015: £112.5m)

• Total Group underlying operating margin(3)

4.9% (2015: 5.1%)

− reflects expected lower contributions from PPP equity sales and from Middle East

construction services

• Underlying pre-tax profit(4)

unchanged at £84.5m (2015: £84.5m)

• Underlying earnings per share(5)(6)

up slightly to 16.0p (2015: 15.9p)

6

PERFORMANCE LED BY REVENUE AND MARGIN GROWTH IN SUPPORT SERVICES

(1) Before intangible amortisation of £6.8m (2015: £8.2m) and non-recurring operating items of £10.5m (2015: Nil)

(2) After Joint Ventures net financial expense and taxation charge of £6.9m and £1.7m (2015: £1.3m and £1.5m) respectively and before intangible amortisation and non-recurring operating items

(3) Before Joint Ventures net financial expense and taxation charge, intangible amortisation and non-recurring operating items

(4) After Joint Ventures taxation charge and before intangible amortisation, non-recurring operating items, non-operating items of Nil (2015: £1.5 million), a credit relating to fair value movements on derivative financial instruments of £9.9m (2015: charge of £7.3m ) and a credit arising from changes in the contingent consideration relating to acquisitions of £6.8m (2015: Nil)

(5) Before intangible amortisation, non-recurring operating items, non-operating items, fair value movements in derivative financial instruments and changes in the contingent consideration relating to acquisitions

(6) Based on weighted average number of shares of 430.2m (2015: 430.2m). Period end number of shares 430.3m (2015: 430.3m)

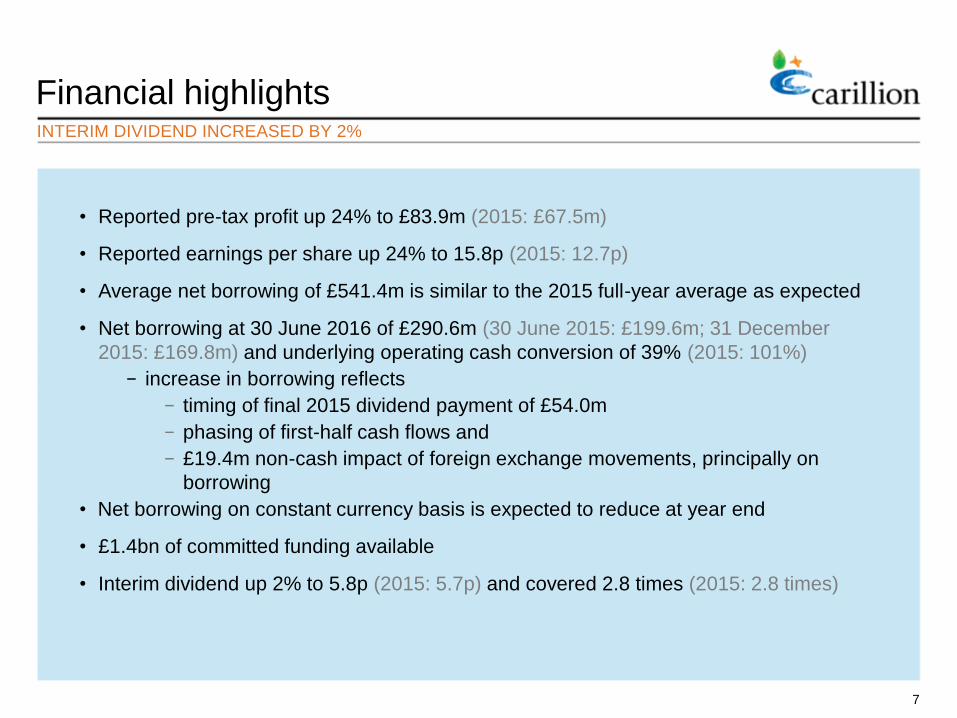

Financial highlights

• Reported pre-tax profit up 24% to £83.9m (2015: £67.5m)

• Reported earnings per share up 24% to 15.8p (2015: 12.7p)

• Average net borrowing of £541.4m is similar to the 2015 full-year average as expected

• Net borrowing at 30 June 2016 of £290.6m (30 June 2015: £199.6m; 31 December

2015: £169.8m) and underlying operating cash conversion of 39% (2015: 101%)

− increase in borrowing reflects

− timing of final 2015 dividend payment of £54.0m

− phasing of first-half cash flows and

− £19.4m non-cash impact of foreign exchange movements, principally on

borrowing

• Net borrowing on constant currency basis is expected to reduce at year end

• £1.4bn of committed funding available

• Interim dividend up 2% to 5.8p (2015: 5.7p) and covered 2.8 times (2015: 2.8 times)

7

INTERIM DIVIDEND INCREASED BY 2%

Income StatementUNDERLYING PROFIT BEFORE TAXATION IN LINE WITH 2015

Underlying Group operating profit

Share of results of Joint Ventures

Underlying profit from operations(1)

Group net interest

Underlying profit before taxation(2)

Intangible amortisation and derivative movements

Non-recurring operating and non-operating items

Profit before taxation

Group taxation

Profit for the period

Non-controlling interests

Profit attributable to Carillion shareholders

Total Group underlying operating margin(3)

90.9

21.8

112.7

(28.2)

84.5

3.1

(3.7)

83.9

(12.2)

71.7

(3.9)

67.8

4.9%

98.4

14.1

112.5

(28.0)

84.5

(15.5)

(1.5)

67.5

(8.3)

59.2

(4.5)

54.7

5.1%

-

-

8

(1) After Joint Ventures net financial expense and taxation charge of £6.9m and £1.7m (2015: £1.3m and £1.5m) respectively and before intangible amortisation of £6.8m (2015: £8.2m) and non-recurring operating items of £10.5m (2015: Nil)

(2) After Joint Ventures taxation charge and before intangible amortisation, non-recurring operating items, non-operating items of Nil (2015: £1.5 million), a credit relating to fair value movements on derivative financial instruments of £9.9m (2015: charge of £7.3m ) and a credit arising from changes in the contingent consideration relating to acquisitions of £6.8m (2015: Nil)

(3) Before Joint Venture net financial expense and taxation charge, intangible amortisation and non-recurring operating items.

£m 2016 2015

+24%

+21%

+24%

Underlying Group operating profit

Depreciation and other non-cash items

Working capital(1)

Dividends received from Joint Ventures

Underlying cash flow from operations

Pension deficit contributions

Non-recurring operating items

Interest and taxation

Net capital expenditure

Other

Foreign exchange movements

Acquisitions and disposals

Dividends

Reduction in net borrowing

Net borrowing at 1 January

Net borrowing at 30 June

Underlying operating cash conversion

£m

98.4

(0.1)

6.1

8.7

113.1

(22.2)

(2.2)

(22.7)

(1.1)

(1.8)

63.1

2.3

(34.9)

(52.8)

(22.3)

(177.3)

(199.6)

101%

Cash flow AVERAGE NET BORROWING SIMILAR TO FULL-YEAR 2015

90.9

17.5

(70.5)

5.7

43.6

(22.3)

(5.9)

(24.2)

(14.8)

(4.5)

(28.1)

(19.4)

(18.1)

(55.2)

(120.8)

(169.8)

(290.6)

39%

2016 2015

(1) Including £35.4m (2015: £14.1 million) from the sale of Public Private Partnership Equity investments (excess of proceeds over profit)

9

Average net borrowing

2016

£541.4m £538.9m

FY 2015

• Net borrowing increased at the half year

due to timing of paying the £54.0m prior

year final dividend

• 2016 half year also impacted by

– working capital movement due to

phasing of cash flow items across

period end

– £19.4m FX movements

• Full-year expectations unchanged

– net borrowing on constant

currency basis to reduce by year

end

– full-year profit 100% cash-backed

• £1.4bn of committed funding to support

strategy for growth

10

Balance sheetROBUST BALANCE SHEET WITH £1.4 BILLION OF FUNDING TO SUPPORT STRATEGIC OBJECTIVES

148.9

1,646.6

160.5

1,956.0

(231.8)

(401.7)

(61.4)

1,261.1

(290.6)

970.5

(541.4)

140.5

1,628.1

166.1

1,934.7

(378.7)

(317.6)

(51.3)

1,187.1

(169.8)

1,017.3

(538.9)

June 2016

December2015

(1)

Property, plant and equipment

Intangible assets

Investments

Inventories, receivables and payables

Net retirement benefit liability (net of tax)

Other

Net operating assets

Net borrowing

Net assets

Average net borrowing

June2015

(1)

132.5

1,640.3

156.7

1,929.5

(352.0)

(355.9)

(87.6)

1,134.0

(199.6)

934.4

(486.5)

£m

• £1.4bn of available funding to support delivery of strategic objectives

(1) Restated for the retrospective adjustment provisional amounts recognised on the acquisition of the Outland Group in 2015.

11

PERFORMANCE LED BY STRONG GROWTH IN SUPPORT SERVICES

Segment results

• Directors’ valuation of PPP investment portfolio at a 9% discount rate decreased to £27m

(31 December 2015: £52m) due to the sale of £48m of equity at an average discount rate of just under 7%

Support services

Public Private Partnership (PPP) projects

Middle East construction services

Construction services (excluding Middle East)

Total

£m 2016 2015

1,336.0

143.8

320.3

687.0

2,487.1

1,238.5

82.5

326.5

611.1

2,258.6

+8%

+74%

-2%

+12%

+10%

REVENUE

Support services

Public Private Partnership (PPP) projects

Middle East construction services

Construction services (excluding Middle East)

Group costs and Joint Venture interest and tax

Underlying profit from operations

£m 2016

75.9

19.7

11.7

20.7

128.0

(15.3)

112.7

58.3

26.4

18.9

19.3

122.9

(10.4)

112.5

+30%

-25%

-38%

+7%

+4%

+47%

-

UNDERLYING OPERATING PROFIT(1)

2016 2015

5.7

13.7

3.7

3.0

4.9(2)

4.7

32.0

5.8

3.2

5.1(2)

OPERATING MARGIN %

2015

(1) Before intangible amortisation of £6.8m (2015: £8.2m) and non-recurring operating items of £10.5m (2015: Nil)

(2) After Group unallocated costs of £6.7m (2015: £7.6m)

• Strong organic revenue growth of 10% to £2,487.1m (2015: £2,258.6m)

• Underlying operating profit(1)

up 5% to £121.3m (2015: £115.3m)

• Underlying pre-tax profit(2)

unchanged at £84.5m (2015: £84.5m)

• Underlying earnings per share(3)

up slightly at 16.0p (2015: 15.9p)

• Reported earnings per share up 24% to 15.8p (2015: 12.7p)

• Average net borrowing broadly unchanged at £541.4m (31 December 2015: £538.9m)

Financial results summaryPERFORMANCE LED BY REVENUE AND MARGIN GROWTH IN SUPPORT SERVICES

(1) Before intangible amortisation of £6.8m (2015: £8.2m) and non-recurring operating items of £10.5m (2015: Nil)

(2) After Joint Ventures taxation charge of £1.7m (2015: £1.5m) and before intangible amortisation, non-recurring operating items, non-operating items of Nil (2015: £1.5 million), a credit relating to fair value movements on derivative financial instruments of £9.9m (2015: charge of £7.3m) and a credit arising from changes in the contingent consideration relating to acquisitions of £6.8m (2015: Nil)

(3) Before intangible amortisation, non-recurring operating items, non-operating items, changes in fair value movements in derivative financial instruments and changes in the contingent consideration relating to acquisitions

12

Strategy andprospectsRICHARD HOWSONGROUP CHIEF EXECUTIVE

13

Mobile technology plays a key role in enabling Carillion to deliver large,

complex support services contracts successfully and efficiently.

Good first-half performance

• Consistent delivery demonstrates robust strategy and integrated business model

• Continuing growth in support services

– contributed some 60% of operating profit in first half of 2016

• Work-winning remains strong

– £2.5bn(1)

of new and probable orders in first half versus £1.0bn in first half of 2015

– total value of orders plus probable orders at 30 June 2016 of £17.4bn

• Investments in Public Private Partnerships performing well

• Construction in UK, Middle East and Canada in line with expectations, supported by a

highly selective approach

• Expect Group to make further progress in 2016 with no changes to our full-year

expectations

DRIVEN BY ROBUST STRATEGY AND BUSINESS MODEL

14

(1) Net of £0.2 billion of orders removed as a result of selling Public Private Partnership equity investments.

Our integrated, scaleable business model

15

CONTINUES TO DRIVE PERFORMANCE AND ADD VALUE

Resources What we do

• Centralised operating

platform

• Strong risk

management

• First-class supply

chain management

• Embedding

sustainability into

everything we do

• Building long-term

partnerships with

customers, partners

and suppliers

• Living our Values

• High standards of

corporate governance

Key outputsHow we do it

• Growing a sustainable

business and creating

value for all our

stakeholders

• Financial strength

• Excellent people

• First-class expertise

• Leadership in Health &

Safety

• Leadership in

sustainability

Value created and shared with our stakeholders and also reinvested in our business

Delivering on our strategyGROWING SUPPORT SERVICES

16

Support Services

Public Private Partnership projects(2) (3)

Construction (including Middle East)

(2) Includes construction of PPP projects

Revenue

(1) 1999 UKGAAP; 2015 and 2016 IFRS

15% 80%

5%

£1.8bn(1)1999

2015

H1 2016

£4.6bn(1)

£2.5bn(1)

55% 41%4%

40%54%

6%

29% 60%

11%

£56.2m1999(2)

2015(2)

H1 2016(2)

£259.0m

£128.0m

57% 24%19%

25%60% 15%

Underlying operating profit(1)

Margin(4) 5.3%

(3) Includes construction of PPP projects

(2) 1999 UKGAAP; 2015 and 2016 IFRS

(1) Before intangible amortisation of £6.8m (2015: £8.2m) and non-recurring operating items of £10.5m (2015: Nil)

(4) Before Joint Ventures net financial expense and taxation charge, intangible amortisation and non-recurring operating items

Margin(4) 4.9%

Margin(4) 2.3%

2016 first-half revenue by geography TOTAL GROUP REVENUE £2.5 BN, UP 10%

17

646 1,077

UK(1)

£1,844m - 74%(2015: £1,600m - 71%)

22

199

Canada(2)

£262m - 11%(2015: £281m - 12%)

41

61

Middle East and North Africa

£381m - 15%(2015: £378m - 17%)

320

76%

8%

16%

16%

84%

121

Support services

Public Private Partnership

(PPP) projects

Construction services

Support services

Construction services

Support services

Public Private Partnership

(PPP) projects

Construction services

(1) Includes £10.8m (2015: £22.0m) of revenue generated outside the UK, Middle East and

North Africa and Canada

(2) Includes £3.4m (2015: £9.8m) of revenue generated in the Caribbean

35% 58%

7%

Order book and probable orders

18

REVENUE VISIBILITY OF 98% FOR 2016

• 80% of orders plus probable orders in support services

and PPP projects (31 December 2015: 80%)

• Order book of £15.0bn, plus probable orders of £2.4bn

totalling £17.4bn (31 December 2015: £17.4bn)

• Strong revenue visibility(2)

for 2016 of 98%

(31 December 2015: 84% for 2016)

• In addition, we have been awarded framework

agreements with a total potential value of over £2bn

Support services £13.0bn 75%(31 December 2015: £12.7bn: 73%)

Public Private Partnership(PPP) projects £0.9bn 5%(31 December 2015: £1.2bn: 7%)

Middle East construction services £0.6bn 3%(31 December 2015: £0.8bn: 5%)

Construction services (excludingthe Middle East) £2.9bn 17%(31 December 2015: £2.7bn: 15%)

£2.5bn(1)

(30 June 2015: £1.0bn)

Total orders plus probable orders

£17.4bn(31 December 2015: £17.4bn)

17% 75%

5%

3%

(1) Net of £0.2 billion of orders removed as a result of selling Public Private Partnership equity investments

(2) Based on expected revenue and secure and probable orders, which exclude variable work, frameworks and re-bids

New first-half orders and probable orders

£2.5bn of first-half orders and probable orders

19

Support services

• Petroleum Development Oman

– £240m 4.5 year extension

• Northern Ireland Housing Executive

– up to £366m over 10 years

• Canada support services

– power and oil sectors over £140m(1)

Public Private Partnership projects

• Financial close on Irish Schools Bundle 5(2)

- £4.5m of equity and construction,

services and concession revenue of

over £190m over 27 years

SIGNIFICANT SUCCESSES IN 2016

(1) Includes the Maritime Link power transmission project announced in July 2016

(2) Classified as a probable order at 31 December 2015 and became a secure order in July 2016

UK construction

£2.5bn of first-half orders and probable orders

20

SIGNIFICANT SUCCESSES IN 2016

Middle East construction

• Lambeth College - £167m

• Manchester Central - £158m

• Gateshead Quays - £168m

• Milburngate, Durham - £130m

• Embankment West, Salford - £120m

• Angel Gardens, Manchester - £85m

• Paradise Circus, Birmingham - £40m

(one phase of several prospective phases)

Al Futtaim Carillion

• Bee’ah, Dubai(1)

- £60m (Carillion’s share: £30m)

(1) Classified as a probable order at 31 December 2015 and became a secure order in H1 2016

Substantial high-quality pipeline SIGNIFICANT OPPORTUNITIES FOR FURTHER PROGRESS

21

Support services £12.1bn 29%(2015: £12.1bn: 29%)

Public Private Partnership

(PPP) projects £2.3bn 6%(2015: £2.4bn: 6%)

Middle East

construction services £16.0bn 38%(2015: £16.0bn: 39%)

Construction services (excluding

the Middle East) £11.1bn 27%(2015: £10.9bn: 26%)

Pipeline opportunities

£41.5bn(31 December 2015: £41.4bn)

41.5£bn

33.135.2

37.539.2

20132012 2014 2015 20162011

12.1

2.3

16.0

11.1

31 December 30 June

41.4

Growth market sectors

22

UK, CANADA, MIDDLE EAST

Support services Public Private Partnerships

£1.3bn2016 revenue

Constructionservices

£13.0bnOrder book

£12.1bnPipeline

£0.2bn2016 revenue

£0.9bnOrder book

£2.3bnPipeline

£1.0bn2016 revenue

£3.5bnOrder book

£27.1bnPipeline

Managing the potential impacts of Brexit

• Carried out extensive work to assess potential impact prior to Referendum

• Put robust plans in place to manage impacts of Brexit

• No significant operations in mainland Europe

• Sourcing of labour from EU countries

• Some sourcing of commodities and materials from EU countries

• Exchange rate impacts on prices

• Overall, well positioned to manage potential impacts

WELL POSITIONED WITH ROBUST PLANS IN PLACE

23

Well positioned to make further progress

24

LED BY GROWTH IN SUPPORT SERVICES

• Robust strategy and business model

• Performance led by revenue and margin

growth in support services

• Strong work-winning performance

• Substantial, high-quality order book &

probable orders worth £17.4bn

• Record full-year revenue visibility(1)

of 98%

• Increased pipeline of contract opportunities

of £41.5bn

• Well positioned to manage potential impacts

of Brexit

• Expect to make further progress in 2016 with

no changes to full-year expectations

(1) Based on expected revenue and secure and probable orders, which exclude variable work, frameworks and re-bids

Appendices

25

Carillion has a £91 million contract for Helical Bar to deliver Phase 1

of the Bart's Square mixed-use development in the City of London on

a site that includes the area formerly occupied by Barts Hospital.

Facts about Carillion

26

Support services

Public Private Partnership (PPP) projects

• Carillion has the skills and resources to provide all the services needed to manage and maintain property, road, rail and utility infrastructure networks

• We provide facilities management and other support services for thousands of public and private sector buildings

• We provide management and maintenance services for some 17,000 kilometres of road in the UK and Canada

• In the UK, we provide services for public utility networks, including the broadband network for Openreach for whom we are also a key delivery partner in the roll out of super-fast fibre access

• In Canada, we provide power transmission and distribution services and remote site accommodation services

• In the Middle East we provide facilities management services for property estates and highways maintenance services

• We have been a leader in PPP projects since the inception of the UK’s Private Finance Initiative in the early 1990’s

• Since then, we have financially closed 65 PPP contracts in the UK and Canada for hospitals, schools, prisons, military accommodation, roads and railways

• We have sold PPP equity investments generating proceeds of some £667 million and a pre-tax profit of around £256 million

• In the Middle East, we are developing opportunities for PPP projects to support customer investment programmes

Carillion is a leading integrated support services company employing some

46,000 people across the UK, in the Middle East and Canada

Facts about Carillion

27

Middle East construction services

Construction Services(excluding the Middle East)

• We have around 40 years experience of operating in the Middle East, where we have built an outstanding reputation for quality and reliability

• We operate in the UAE, Oman, Qatar, the Kingdom of Saudi Arabia and Egypt

• We have built many of the region’s iconic landmark projects, including Dubai Festival City, the Grand Mosque in Oman, the Yas Hotel, (centre piece of Abu Dhabi’s Formula 1 Grand Prix circuit) and the Royal Opera House in Oman

• Our history in construction spans almost two centuries, as Carillion brings together the heritage of Tarmac, Mowlem and Alfred McAlpine

• Carillion has continued to deliver outstanding projects, such as the new Government Communication Headquarters in Cheltenham, 17 major hospitals, some 160 new schools, several prisons and numerous motorway, trunk road and rail projects

• In Canada, where we have operated for around 50 years, we have also built a reputation for delivering high-quality projects, particularly Public Private Partnership projects, where we have financially closed nine major projects, notably in the healthcare sector.

Carillion is a leading integrated support services company employing some

46,000 people across the UK, in the Middle East and Canada

Revenue and profit summary

28

65.6 10.3 75.9

12.3 7.4

19.7

4.5 7.2

11.7

15.2 5.5

20.7

128.0

(6.7)

121.3

(6.9)

(1.7)

112.7

Support servicesGroupShare of joint venturesTotal

Public Private Partnership projectsGroupShare of joint venturesTotal

Middle East construction servicesGroupShare of joint venturesTotal

Construction services (excluding the Middle East)GroupShare of joint venturesTotal

Total revenue and operating profit

Group eliminations and unallocated items

Operating profit (before Joint Ventures net financial expense and taxation)

Share of Joint Ventures net financial expense

Share of Joint Ventures taxation

Underlying profit from operations

£m 20152016

+30%

-25%

-38%

+7%

+5%

-

2015

1,203.1 132.9

1,336.0

0.7143.1 143.8

200.1 120.2 320.3

682.7 4.3

687.0

2,487.1

2016

Underlying operating profit(1)Revenue

1,158.679.9

1,238.5

0.681.982.5

194.4132.1326.5

607.73.4

611.1

2,258.6

48.8 9.5

58.3

22.6 3.8

26.4

16.1 2.8

18.9

18.5 0.8

19.3

122.9

(7.6)

115.3

(1.3)

(1.5)

112.5

+8%

+74%

-2%

+12%

+10%

(1) Before intangible amortisation and non-recurring operating items

69 49

247

805

51

122

26

0

100

200

300

400

500

600

700

800

900

2016 2017 2018 2019 2020 2021 2022 2023 2024

£1.4bn of available fundingMATURITY PROFILE FOLLOWING RENEWAL OF UK BORROWING FACILITIES

29

£m

15

Total revenue by sector/geography

30

UK public sector

UK regulated sector

UK private sector

International

0.5

0.4

0.6

1.040%

24%

16%

20%

Total revenue first-half 2016

£2.5bn (2015: £2.3bn)

Risk management STRONG AND RESILIENT PROCESSES

31

Carillion plc Board

Board sub-committees

Business Integrity Committee

SustainabilityCommittee

Major Projects Committee

Audit Committee

Corporate Oversight and Direction

Group Chief Executive’s Leadership Team

OtherFunctional Heads

Group RiskManagement

Operations

Business UnitManaging Directors

Contract RiskManagers

Business UnitRisk Management

PeerReviews

Assurance

Internal Audit

External Audit

External Benchmarking

Market sectors

32

UK

Support services

Public Private Partnerships

£1.1bnH1 2016 revenue

Constructionservices

£0.6bnH1 2016 revenue

£0.1bnH1 2016 revenue

• Defence

• Roads

• Rail

• Airports

• Private sector ‘relationship customers’

• Mixed-use developments

• Increased Government spending especially on infrastructure

• Infrastructure services

– Rail and roads

– Power distribution

– Airports

• Property FM services

– Public sector

– Health

– Local Authorities

– Defence

– Ministry of Justice

– Private sector

• Targeting further projects

– Integrated solutions

– Healthcare/hospitals

– Schools/academies

– Highways

• £54m of equity still to be invested in 4 financially closed projects

Market sectors

33

CANADA

Support services

Public Private Partnerships (PPP)

£0.2bnH1 2016 revenue

Construction services

£41mH1 2016 revenue

£22mH1 2016 revenue

• PPP driven

• Key sectors

– Health

– Roads

– Rail

– Airports

– Power

• Further project opportunities

• Major programmes with total capital value of some $60bn

– Ontario

– British Columbia

– Alberta

– Saskatchewan

• £7m of equity still to be invested in 2 financially closed projects

• Highways maintenance

• Acquisition of Outland Group in 2015 broadens services offering to include remote site accommodation and associated services

• Power transmission & distribution

• FM

– Health (PPP projects)

– Defence

– Education

– Municipalities

• Oil & Gas/natural resource industries

• Medium-term growth from expansion into new Provinces

Market sectors

34

MIDDLE EAST

Construction services

Public Private Partnerships (PPP)

£0.3bnH1 2016 revenue

Support services

£61mH1 2016 revenue

£nilH1 2016 revenue

• Property FM

– Health

– Airports

– Commercial

• Infrastructure services

– roads and rail

• Energy services

• Oil & gas sector services

• Opportunities for growth over medium term

– Dubai

– Oman

– Qatar

• Medium term

– Abu Dhabi 2030 Plan

– Saudi Arabia

• UK Export Finance is a key differentiator for Carillion

• Increasing potential for PPP projects in Middle East and other international regions e.g.

– Oman

– Bahrain

Directors’ valuation of equity in financially closed Public Private Partnership projects

35

VALUATION REDUCED BY £19M AFTER £48M OF EQUITY SALES

Discount rate

0

20

40

60

80

5% 6% 7% 8% 9% 10% 11% 12%

Net

pre

sen

t valu

e (

£m

)

£44m(1)

£27m(2)

Net present value at 30 June 2016

£27m (31 December 2015: £46m)

(1) Average discount rate for disposals in 2016

(2) Directors’ valuation

• Potential for approximately £62m of further equity

investments

36

Financially closed PPP projects

Roads

A13

Aberdeen Western Peripheral

Health

Royal Ottawa Hospital, Canada

North Battleford Hospital, Canada

Stanton Hospital, Canada

Royal Liverpool Hospital

Midland Metropolitan Hospital

PPP projectFinancial

Close Date StatusConcession Period Years

EquityInvested

to date (£m)Equity

Share (%)

TotalCommittedEquity (£m)

Non-RecourseDebt (£m)

2000

2014

2004

2015

2015

2013

2015

Operational

In Construction

Operational

In Construction

In Construction

In Construction

In Construction

30

33

20

33

33

35

33

7.5

-

0.7

-

-

-

-

7.5

20.2

0.7

3.5

3.9

15.2

13.3

25

33

50

50

50

50

50

Continued

45.5

74.3

-

43.2

30.3

74.8

25.0

At 30 June 2016

37

Financially closed PPP projects

PPP projectFinancial

Close Date StatusConcession Period Years

EquityInvested

to date (£m)Equity

Share (%)

TotalCommittedEquity (£m)

Non-RecourseDebt (£m)

1995

2015

2007

2008

2009

2009

2010

2010

Operational

In Construction

Operational

Operational

Operational

Operational

Operational

Operational

30

28

25

25

25

25

25

25

-

-

0.4

0.4

0.5

1.0

0.5

0.8

11.8

-

5.6

0.4

0.4

0.5

1.0

0.5

0.8

73.5

100

42.5

4

8

8

8

8

8

-

10.0

2.0

4.2

3.6

9.4

4.7

3.2

330.2

At 30 June 2016

Education

University of Greenwich

Priority Schools Midlands

South Tyneside and

Gateshead Schools BSF

Nottingham Schools BSF

Durham Schools BSF

Tameside Schools BSF

Rochdale Schools BSF

Wolverhampton Schools BSF

TOTAL

Middle East construction servicesREVENUE BY COUNTRY

38

90

110

18

Dubai

Abu Dhabi

Oman

Egypt

Qatar & Saudi

32%

6%

34%

102

28%

2016 Revenue

£320m

2015 Revenue

£327m

68

127

30

31%

9%

39%

102

21%

Acquisitions and disposals

• Acquisition of the Outland Group is the second instalment of the consideration payable

• Investments income of £1.5m relates to the repayment of sub-debt invested in PPP joint ventures

39

Acquisition of the Outland Group

Acquisition of Ask Real Estate Limited

Investments

Acquisition of the Rokstad Corporation

Transaction costs

Other

£m 2016

(15.0)

(4.0)

1.5

-

(0.6)

-

(18.1)

(8.2)

-

(16.9)

(2.6)

(6.9)

(0.3)

(34.9)

2015

Non-underlying items

• Change in fair value of contingent consideration relates to a reduction in the amount payable on the acquisition of the Rokstad Corporation

• Construction Workers Compensation Scheme represents Carillion’s share of the compensation and associated costs that we expect to pay to workers who have been impacted by the use of the database vetting system operated by The Consulting Association

40

Fair value movement in derivatives

Intangible amortisation

2016

9.9

(6.8)

3.1

(7.3)

(8.2)

(15.5)

2015

20152016

Change in fair value of contingent consideration

Construction Workers Compensation Scheme

Acquisition costs

6.8

(10.5)

-

(3.7)

-

-

(1.5)

(1.5)

Intangible amortisation and derivative movements

Non-recurring operating and non-operating items

£m

£m

Cautionary Statement

This presentation may contain indications of likely future developments and other forward-

looking statements that are subject to risk factors associated with, among other things, the

economic and business circumstances occurring from time to time in the countries, sectors and

business segments in which the Group operates. These and other factors could adversely

affect the Group's results, strategy and prospects. Forward-looking statements involve risks,

uncertainties and assumptions. They relate to events and/or depend on circumstances in the

future which could cause actual results and outcomes to differ materially from those currently

anticipated. No obligation is assumed to update any forward-looking statements, whether as a

result of new information, future events or otherwise.

2016

Interim Results

42

‘Living’ our values shapes the way we do business – how we work

with each other, our customers, our suppliers, our partners and all

those with whom we interact when delivering our services.

In 2015, Carillion acquired the Outland Group, a leading provider of remote-

site accommodation services that operates across Canada to support a variety

of private and public sector customers who need to work remote locations.