powerpoint presentationiclgroupv2.s3.amazonaws.com/corporate/wp-content/uploads/sites/... ·...

TRANSCRIPT

Investor Presentation

July 2018

Safe Harbor

2

This Presentation (references to which and to any information contained herein shall be deemed to include information which has been or may be supplied in writing or orally in connection herewith or in connection with any further enquiries) is provided for the sole purpose of providing general information to assist the recipient in deciding whether it wishes to proceed with a further investigation for investing in Israel Chemicals Ltd. and/or its affiliates (hereinafter jointly referred to as the “Company” or “ICL”). This Presentation shall not form the basis of, or be relied upon in connection with, any contract or commitment whatsoever, and it does not purport to be comprehensive or to contain all the information that the recipient may need in order to evaluate the Company and/or its assets.

No representation, warranty or undertaking, express or implied, is given by ICL and/or any member of the ICL Group or their respective directors, officers, employees, agents, representatives and/or advisers as to or in relation to the accuracy, completeness or sufficiency of the information contained in this Presentation or as to the reasonableness of any assumption contained therein. To the maximum extent permitted by law , the Company and its respective directors, officers, employees, agents, representatives and/or advisers expressly disclaim any and all liability which may arise from this Presentation and any errors contained therein and/or omissions therefrom or from any use of this Presentation or its contents or otherwise in connection therewith.

No representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any valuations, forecasts, estimates, opinions and projections contained in this Presentation. In all cases, recipients should conduct their own investigation of any analysis of the Company and/or its assets and the information contained in this Presentation. Nothing in this Presentation constitutes investment advice and any opinions or recommendations that may be contained herein have not been based upon a consideration of financial situation or particular needs of any specific recipient. Any prospective investor interested in buying Company’s securities or evaluating the Company and/or its assets is recommended to seek its own financial and other professional advice.

This Presentation and/or other oral or written statements made by ICL during its presentation or from time to time, may contain forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995 and other applicable securities laws. Whenever words such as "believe," "expect," "anticipate," "intend," "plan," "estimate", “predict” or similar expressions are used, the Company is making forward-looking statements. Such forward-looking statements may include, but are not limited to, those that discuss strategies, goals, financial outlooks, corporate initiatives, existing or new products, existing or new markets, operating efficiencies, or other non-historical matters.

These forward-looking statements and projections are not guarantees of future performance and are subject to a number of assumptions, risks, projections and uncertainties, many of which are beyond the Company’s control, which could cause actual results, performance or achievements to differ materially from those described in or implied by such statements or projections. Because such statements deal with future events and are based on ICL’s current expectations, they could be impacted or be subject to various risks and uncertainties, including those discussed in the "Risk Factors" section and elsewhere in our Annual Report on Form 20-F for the year ended December 31, 2017, and in subsequent filings with the Tel Aviv Securities Exchange (TASE) and/or the U.S. Securities and Exchange Commission (SEC). Although the Company believes that the expectations reflected in such forward-looking statements are based on reasonable assumptions, it can provide no assurance that expectations will be achieved. Except as otherwise required by law, ICL disclaims any intention or obligation to update or revise any forward-looking statements, which speak only as of the date hereof, whether as a result of new information, future events or circumstances or otherwise. Readers, listeners and viewers are cautioned to consider these risks and uncertainties and to not place undue reliance on such information.

Certain market and/or industry data used in this Presentation were obtained from internal estimates and studies, where appropriate, as well as from market research and publicly available information. Such information may include data obtained from sources believed to be reliable, however ICL disclaims the accuracy and completeness of such information which is not guaranteed. Internal estimates and studies, which we believe to be reliable, have not been independently verified. We cannot assure that such data is accurate or complete.

Included in this presentation are certain non-GAAP financial measures, such as Adjusted Operating income and Adjusted Net income, designed to complement the financial information presented in accordance with GAAP because management believes such measures are useful to investors. These non-GAAP financial measures should be considered only as supplemental to, and not superior to, financial measures provided in accordance with GAAP. Please refer to our Annual Report on Form 20-F for the year ended December 31, 2017 filed with TASE and the SEC for a reconciliation of the non-GAAP financial measures included in this presentation to the most directly comparable financial measures prepared in accordance with GAAP.

Corporate Overview

Specialty Fertilizers

6%Potash &

Mg.31%

Advanced Additives

22%

Industrial Products

33%

Food Specialties

6%Specialty Fertilizers

13%

Potash & Mg.23%

Advanced Additives

15%

Industrial Products

22%

Food Specialties

11%

Our Business Segments

Financial Metrics Snapshot(2) Sales and Operating Income By Sub-Segments(2,3)

Essential Minerals

Potash & Magnesium

Specialty Fertilizers

Specialty Solutions

Industrial Products

Advanced Additives

Food Specialties

FY2017 Q1 2018

Sales(3) 5,418 1,404

($,mn)

Adj. Operating Income(4) 652 151

Adj. Net Income(4) 389 106

$5.9bn Market Cap

(02/07/2018)

2.3xLTM Net

Leverage(5)

Leading Global Fertilizer and Specialty Minerals Company

4

FY2017 Sales Mix

39%

Specialty Solutions Essential Minerals

61%48% 52%

FY2017 Operating Income(6)

BBB-

BBB-

Agriculture Industrial

1. A nontransferable Special State Share in ICL, with several rights and upon occurrence restrictions. 2. Includes Fire Safety and Oil Additives. Please refer to page 35. 3. External sales only, excludes intra company sales. 4. Excludes certain expenses and/or income that management believes are not indicative of ongoing operations. 5. Excludes EBITDA from the divested Fire Safety and Oil Additives business. 6. Excludes non-allocated and G&A expenses. 6. Calculated based on average Market Cap. For full year 2017.

(Stable)

(Stable)

YoY

8%

30%

56%

PhosphateCommodities

Phosphate Commodities

16%

Phosphate Commodities

2%

YoY

1%

12%

14%

3.3%Div. Yield (6)

(FY2017)

5

Diversified Company, Integrated Along the Value Chains

5

Unique Business Model, Integrated Along the Mineral Value Chains

6

ResourcesOur Specialty

MineralsOur

ExpertiseSegment Products End Markets

Essential Minerals

Specialty Solutions

Pure PhosphoricAcid

Green Phosphoric Acid

SSP, TSP, DAP, MAP

Potash Fertilizer

StraightsMAP,MPK,Pekacid

Liquid/Water Soluble Fertilizers

Compound NPK

Food Phosphate Additives

Dairy Proteins

Phosphate Acids

Industrial Phosphate Salts

P4 Derivatives

Clear Brine Fluids

Mercury Emission

Bromine Industrial Solutions

Flame Retardants

Polysulphate

Phosphate

Potash

Bromine

Magnesium

UK

China YPH

Negev Desert

Dead Sea

AgricultureMining and Extraction

Formulation

Marketing

R&D

Industrial

Potash

Spain

PolysulphateFertilizers

CRF and SRF

Phosphate

7

ICL Business Model

7

Food

Specialties

Advanced

Additives

Industrial

Products

Specialty

Fertilizers

Phosphate

Potash

Semi-

Specialty

Fertilizers

AGRICULTURE

INDUSTRIAL

EMPLOYEES WORLDWIDE

2017 SALES* BY BUSINESS LINE

53%OF ICL SALES IN 2017

Potash 4,773 K ton

Phosphate Rock 4,877 K ton

Phosphate Fertilizers 2,094 K ton

Potash 5,039 K ton

Phosphate Fertilizers 2,291 K ton

Polysulphate 292 K ton

$3.0Bn 2017 SALES*

$359M 2017 OPERATING INCOME**

2017 PRODUCTION

2017 SALES VOLUME

ICL Essential Minerals Profile

* Before setoffs and inter-segment eliminations. ** Before G&A expenses. Before setoffs and inter-segment eliminations.All numbers are rounded.

~ 7,600

44%

34%

22%

Potash & Magnesium PhosphateSpecialty Fertilizers

2017 FINANCIALS

8

53%47%

Essential Minerals

Specialty Solutions

ICL Specialty Solutions Profile

~ 3,700

2017 PHOSPHATE VALUE CHAIN SALES*

% SALES BY BUSINESS UNIT***

25%

$2.4B SALES*

$554MOPERATING INCOME**

Food Specialties

51%Industrial Products

24%Advanced Additives

EMPLOYEES WORLDWIDE

* Before setoffs and eliminations** Before G&A expenses*** Data excludes the divested Fire Safety and oil Additives businessesAll numbers are rounded

2017 MAIN FINANCIAL RESULTS

27%

40%

19%

14%

2017 IP SALES BREAKDOWN

Brominated FRs

Other Brominated Solutions

Phosphorus Compounds

Specialty Minerals

9

Phosphate Acids26%

Industrial Phosphates

17%

Phosphate Food

Additives 36%

Our Strategic Direction

10

From Core Minerals to Specialties Advanced Crop Nutrition

Our Strategic Direction

11

From Core Minerals to Specialties

Advanced Crop Nutrition

Mineral Asset Base: Potash, Bromine, Phosphate and PolysulphateTM Sites

12

High quality and practically inexhaustible source of potash,

bromine & magnesium

▪ Low cost

▪ Near-infinite reserve life

▪ Logistical advantages: stockpiling ability, proximity to ports and to end markets

Facilitate favorable access to European Ag markets

▪ Logistical advantages: focus on domestic markets, close to ports, hub centre in Europe

▪ Synergies and optimization within production sites

▪ Vast resources of potash in Spain and Polysulphate in the UK

Backbone of our phosphate value chain

▪ Backward integration to Specialty Solutions

▪ Synergies and optimization within production sites

▪ YPH JV: shift to specialties to become the hub of ICL’s specialty businesses in Asia

Potash & Bromine

ICL Dead Sea

Potash & Polysulphate

ICL Iberia, ICL UK

Phosphates

ICL Rotem, YPH JV

Optimization of our Mineral Assets

13

▪ Production process improvement

▪ Early retirement plan

▪ Rock production optimization

▪ Energy efficiency

▪ Maintenance optimization

▪ ~ 50% reduction in workforce

▪ Targeting 1M tonnes by 2020

▪ Significant reduction in loss expected in 2018, profitability expected from 2020

▪ Building access ramp, expand capacity in Suria

▪ New port terminal

ICL Iberia – mine consolidation & logistics upgrade

Operational Excellence In the Dead Sea and Rotem

ICL UK – full shift to Polysulphate in progress

▪ Labor reduction

▪ Process improvement

▪ WPA capacity expansion

YPH JV – Cost efficiency & shift to specialties

Optimization Measures to Reduce Costs and Maintain Production

14

Optimization

~10-15%Reduction in potash cost per tonne over 5 Years

~5M TonneMaintain stable

Potash production

ShiftPhosphate and UK

to Specialty

Specialty

Semi Specialty

Commodity

15

The Evolution of Crop Nutrition

▪ CRF (Controlled Release Fertilizers)

▪ WSNPK (Water Soluble Fertilizers)

▪ Soluble (MAP/MKP)

▪ CN (Calcium Nitrate)▪ NOP (Potassium Nitrate)

NNitrogen

7

PPhosphorous

15

KPotassium

19

Added value

Higher prices

Smaller volumes

Selective distribution

Mineral Attributes

▪ Multi-nutrients

▪ Extended Availability

▪ Natural fertilizer

ICL’s Advantages

▪ Sole producer

▪ Existing infrastructure

▪ Market position

Polysulphate as the Backbone of Our Semi-Specialty Business

A PREMIUM NICHE FERTILIZER WITH UNIQUE BENEFITS

48%S

14%K

17%Ca

6%Mg

15%Other

0

1,000

2,000

3,000

2016 2017 2020 LT potential

K Tonnes

Market Demand Outlook

16

Semi-Specialty Growth Target

Growth

From ~$100M to ~$400MIncrease in Semi-Specialty sales within 5 years

17

Specialty Fertilizers: Building Leadership in Advanced Crop Nutrition Solutions

R&D InfrastructurePrecision

Ag Business

Development

18

Specialty Fertilizers Growth Targets

Growth through Leadership

in Advanced Crop Nutrition

Createbest-in-class

innovative platform

Over $1BNSales within 5 Years

ImproveOperating Margin

19

Our Strategic Direction

20

From Core Minerals to Specialties Advanced Crop Nutrition

280 280

120 120

170 165

77 62

7787

2017 2022

ICL Bromine Value Chain: Global Leadership

21

The Dead Sea provides the highest concentration of Bromine

The Largest Capacity (KMT)(2)

Global Bromine Capacity/producer

ALB (Dead Sea)

ICL (Dead Sea)

Other

USA (ALB & LXS)

China

724

Bromine Prices in China(1)

($/Mt)

714

(1) Source: Bloomberg (2) Source: ICL estimates, MarketsandMarkets

Aug 16 Nov 16 Mar 17 Jul -17 Nov 17 Mar 18Apr 16

▪ New product development including new applications and next generation flame retardants

▪ Value-based pricing approach

▪ Leverage on resource depletion in China and leading market position

▪ Advocacy - FR Standards, SAFR™, Merquel® in China/EU…

▪ Cost reduction initiatives

▪ Global leader in bromine capacity

▪ Backward integrated to the lowest-cost source of bromine

▪ Largest producer of brominated flame retardants, biocides and clear brine fluids

▪ Largest Iso-tank fleet

▪ Near infinite reserve life

Key advantages Growth and margin expansion through…

22

P2O5 Value Chain: Continued Quest For Global Opportunities in Specialty Phosphates

ICL

Innophos

PrayonChinese

Others

(1) Source: market size (acid/salts) via internal analysis, published data & other market reports. Includes Europe, NA and LatAm.(2) Proforma results adjusted for divestments of fire safety and P2S5 businesses. Before setoffs and inter-segment eliminations.

GLOBAL MARKET LEADERSHIPIN SPECIALTY PHOSPHATES(1)

Nth America

50%

Sth America13%

EMEA 28%

Asia/Pac9%

Advanced Additives

Nth America

28%

Sth America13%

EMEA 28%

Asia/Pac32%

Note: Sales and operating income according to Organizational Structure as of Q1 2017. All numbers are rounded.

• Full phosphate chain from rock to salts

• Largest global footprint in specialty phosphates

• Value based pricing approach

• Product Differentiation

• Geographic Expansion: increase footprint in growing emerging markets

• Expand portfolio through innovation based on global trends, tailored solutions

• Cost optimization: “Lean & Reliable”

• Support growth through opportunistic M&A

Food Specialties

GROWTH STRATEGY

KEY ADVANTAGES

Advanced Additives

Food Specialties

• Variety of single, multi blends and

agglomeration technology in food ingredients

• Supported by global trends

GLOBAL SALES FOOTPRINT (2)

Specialty Solutions Segment Long-Term Targets

23

Maintain strength.Provide stability.

Outgrowthe market

Expandmargins

Financial Overview

-

200

400

600

800

1,000

1,200

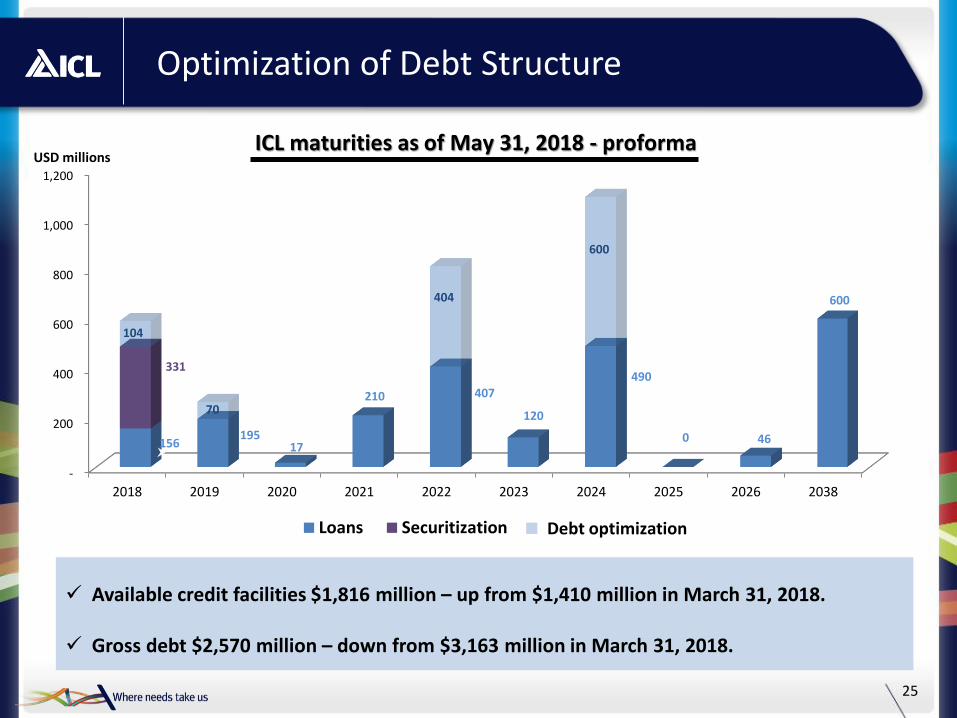

2018 2019 2020 2021 2022 2023 2024 2025 2026 2038

156195

17

210 407

120

490

0 46

600

331

104

70

404

600

Loans Securitization

ICL maturities as of May 31, 2018 - proforma

Optimization of Debt Structure

25

✓ Available credit facilities $1,816 million – up from $1,410 million in March 31, 2018.

✓ Gross debt $2,570 million – down from $3,163 million in March 31, 2018.

USD millions

Debt optimization

Investing in Our Future and Creating Financial Flexibility

Net debt ($ million)

2016 2017 Q1 2018

Net Debt/EBITDA

$3,268$3,037

$2,269

3.12.9

2.3*

From Core

Minerals to

Specialties

Advanced

Crop

Nutrition

Support M&A and growth

Infrastructure development

and improvements

Capital allocation approach

Financial flexibility for future growth

From on-going operating cash flow generation

Maintain balance between LT value creation, investment grade rating

and shareholder’s return

26

* LTM EBITDA, excluding EBITDA contribution of divested businesses

Key Takeaways

Low Cost Dead Sea Production, Geographically

Advantaged Asset Base

Diversified Company, Integrated Along the Value

Chains

Prudent Capital Allocation Management

Focus on Core Minerals and Advanced Crop Nutrition

27

Thank You

Appendix

30

Our Businesses Are Positioned to Benefit from Growing Global Trends

Environmental Regulations & Sustainability

Ind

ust

rial

P

rod

uct

s

TrendRenewable

Energy & Energy storage

Electric / Smart Vehicles & Home

Automation

Growing Middle Class in Emerging

Markets

Ad

van

ced

A

dd

itiv

es

Foo

d

Spe

cial

tie

s

Limited Clean Water Supply

Food Security

Co

nve

nti

on

al

Fert

ilize

rs

Spe

cial

ty

Fert

ilize

rs

Effective Tax Rate

See Q1 2018 press release for a reconciliation of Adjusted operating income to operating income

31

$ million Q1 18 2017

Adjusted income before tax 137 528

Normalized tax rate (including resource tax) 23% 26%

Normalized tax expenses 32 136

Carryforward losses not recorded for tax purposes 3 19

35 151

26% 29%

Other items (mainly exchange rate impact) (2) 1

Adjusted income tax 33 156

Actual Effective tax rate 24% 30%

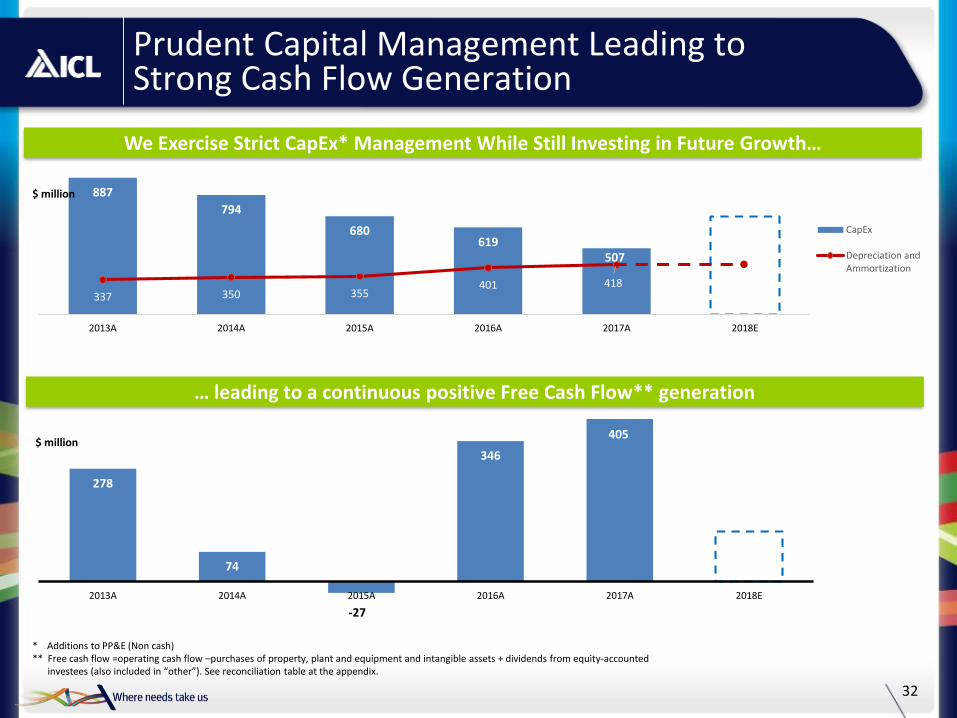

… leading to a continuous positive Free Cash Flow** generation

887

794

680619

507

337 350 355401 418

2013A 2014A 2015A 2016A 2017A 2018E

CapEx

Depreciation andAmmortization

Prudent Capital Management Leading to Strong Cash Flow Generation

We Exercise Strict CapEx* Management While Still Investing in Future Growth…

* Additions to PP&E (Non cash)** Free cash flow =operating cash flow –purchases of property, plant and equipment and intangible assets + dividends from equity-accounted

investees (also included in “other”). See reconciliation table at the appendix.

$ million

$ million

278

74

-27

346

2013A 2014A 2015A 2016A 2017A 2018E

405

32

405

150-200

~70

0-50

33

Strategic CAPEX Financed Through Operating Cash Flow

Investing in our future and creating financial flexibility to support growth

US$ million

Essential Minerals Segment

ICL Essential Minerals - Organizational Structure

35

Business Development

HR

Finance

Sales, Marketing& Logistics

Alon Gil

23 years in ICL

SpecialtyFertilizers

Eli Amon

26 years in ICL

Phosphate

Yakov Kahlon

22 years in ICL

Potash & Magnesium

Noam Goldstein

31 years in ICL

President, ICL Essential Minerals Segment

Ofer Lifshitz

21 years in ICL

ICL Essential Minerals Division

Agriculture

Potash PhosphateSpecialty Fertilizers

Commodity Semi-specialty Specialty

36

37

Growing

population

Dietary

shifts

Arable land

per capitaBiofuels

More grains

Increased yields

More fertilizers

More people want more…Demand for fertilizers is closely linked to the demand

for food and fuel crops

Global Fertilizer Demand

38

MeatConsumption

Population

Fertilizerconsumption

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

Ind

ex, r

elat

ive

to 1

96

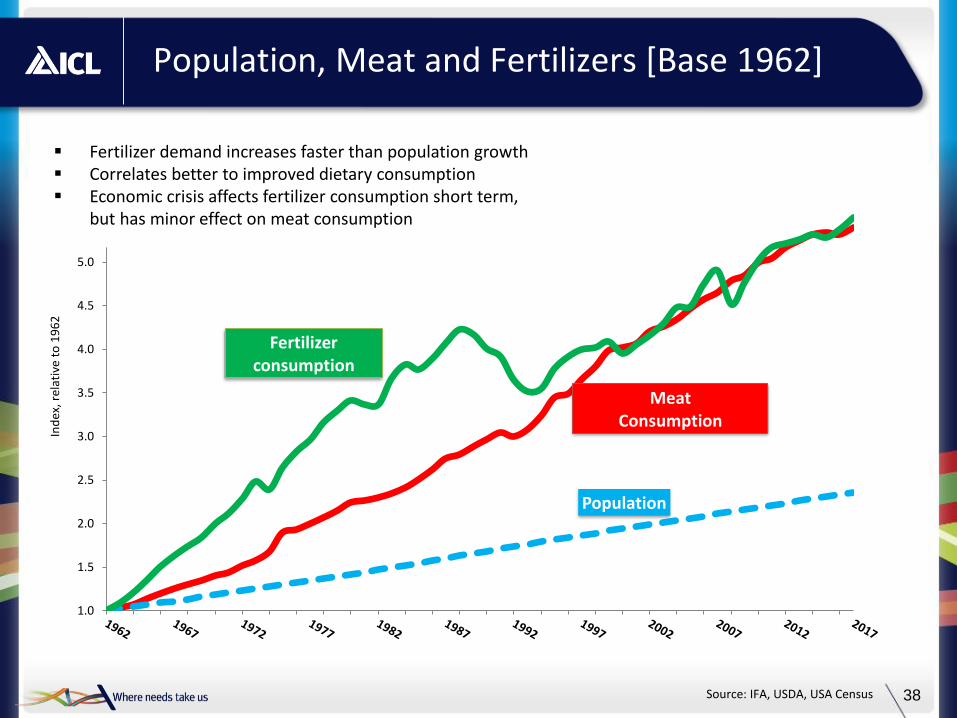

2Population, Meat and Fertilizers [Base 1962]

▪ Fertilizer demand increases faster than population growth ▪ Correlates better to improved dietary consumption▪ Economic crisis affects fertilizer consumption short term,

but has minor effect on meat consumption

Source: IFA, USDA, USA Census

39

Cereals 37%

Oilseeds 20%

Tot. Other43%

Wheat 6.2%

Rice 12.6%

Maize 14.9%

Other Cereals 3.7%

Soybean 9.0%Oil Palm

7.2%

Other Oilseeds 3.5%

Fibre Crops2.8%

Sugar Crops 7.7%

Roots/Tubers3.8%

Fruits6.6%

Vegetables10.0%

Oth Crops11.8%

Source: IFA- Assessment of Fertilizer Use by Crop at the Global Level

Total Fertilizer Use by Crop at Global Level

Cereals and OilseedsAccount for 62% ofFertilizer Consumption

40

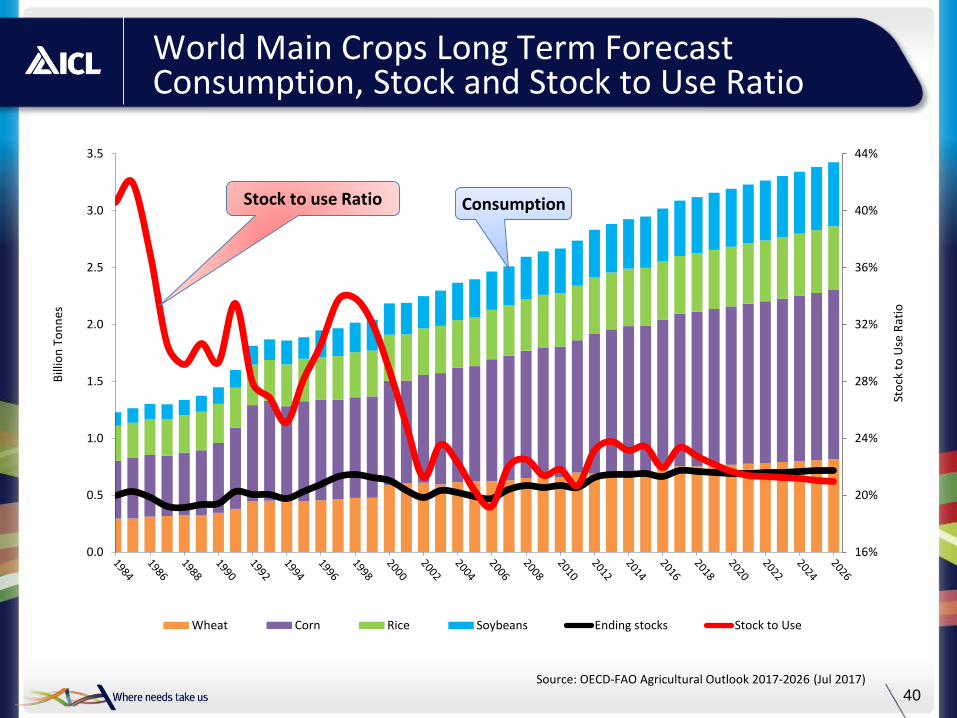

World Main Crops Long Term ForecastConsumption, Stock and Stock to Use Ratio

Source: OECD-FAO Agricultural Outlook 2017-2026 (Jul 2017)

16%

20%

24%

28%

32%

36%

40%

44%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Sto

ck t

o U

se R

atio

Bill

ion

To

nn

es

Wheat Corn Rice Soybeans Ending stocks Stock to Use

Stock to use Ratio Consumption

Global Fertilizer Consumption

4%

9%

Global market share

41

-

20

40

60

80

100

120

140

19

67/6

8

19

69/7

0

19

71/7

2

19

73/7

4

19

75/7

6

19

77/7

8

19

79/8

0

19

81/8

2

19

83/8

4

19

85/8

6

19

87/8

8

19

89/9

0

19

91/9

2

19

93/9

4

19

95/9

6

19

97/9

8

19

99/0

0

20

01/0

2

20

03/0

4

20

05/0

6

20

07/0

8

20

09/1

0

20

11/1

2

20

13/1

4

20

15/1

6

20

17/1

8

20

19/2

0

20

21/2

2

million m

tnutr

ient

Source: IFA – Medium Term Outlook for World Agriculture and Fertilizer Demand (May 2017)

35.7%

26.3%25.1%

31.6%

16.7%

19.8%

25.5%

22.6%

14%

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

36%

38%

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

19

60

/61

19

62

/63

19

64

/65

19

66

/67

19

68

/69

19

70

/71

19

72

/73

19

74

/75

19

76

/77

19

78

/79

19

80

/81

19

82

/83

19

84

/85

19

86

/87

19

88

/89

19

90

/91

19

92

/93

19

94

/95

19

96

/97

19

98

/99

20

00

/01

20

02

/03

20

04

/05

20

06

/07

20

08

/09

20

10

/11

20

12

/13

20

14

/15

20

16

/17

20

18

/19

ConsumptionProductionStockStock to Use

Sources: USDA, June 2018

World Grains Production & Consumption: Current Stock-to-use Ratio

42Grains and Pulses: Barley, Corn, Millet, Mixed Grain, Oats, Rice, Rye, Sorghum, Wheat

Billion Tonnes

43

Fertilizer Prices

Potash Prices

FOB Vancouver standard KCl

US$/t spotUS$/t spot

Average DAP FOB Tampa

Average GTSP, FOB North Africa

Phosphate Prices

* Source: Fertilizer Week

FOB NOLA granular KCl

0

100

200

300

400

500

600

700

200

250

300

350

400

450

500

550

600

650

23%

20%

12%

26%

18%

Canpotex Uralkali APC BPC ICL

26%

17%

22%

7%

12%

Russia Belarus Canada Jordan ICL

ICL’s Market Share in Fast Growing Markets

India Brazil China

3.8 Mt 8.8 Mt 6.8 Mt

Total Im

po

rt 20

16

29%

17%6%

22%

13%

Canpotex Uralkali SQM BPC ICL

44

4.5 Mt 9.2 Mt 7.5 Mt Total Im

po

rt 20

17

10%

25%

25%

16%

20%

4%

APC BPC Canpotex ICL Uralkali K+S

5%

20%

23%

9%

29%

14%

SQM BPC Uralkali K+S Canpotex ICL

20%

23%

31%

12%

9%5%

Uralkali BPC Canpotex ICL APC Others

Strategic Geographic AdvantageClear Service Advantage to Developed and Emerging Markets

Distance Destination (Days)

Country of Departure

Mine-to-Port (km) (1) China India Brazil

Israel ~200 23 11 22

UK ~30 34 22 20

Spain ~85 27 15 17

Germany ~350 34 23 20

Russia / Belarus ~600 39 27 25

Canada West Coast ~1,700 35 47 43

China

India

IL

Europe

Brazil

US

Short mine-to-port distances and proximity to emerging markets

1 Israel based on average from Dead Sea to Port of Eilat and Ashdod; Germany based on Werra to Port of Hamburg and Bremerhaven; Canada based on Saskatchewan to Port of Vancouver; Russia based on Starobin to Port of Klaipeda; Spain based on Cabanasas Mine to Port of Barcelona; UK based on Cleveland Potash, Saltburn-by-the-Sea to Teesport Commerce Park

2 Source: ICL estimates, Netpas

• Shorter mine-to-port distances and shorter shipping routes to emerging markets results in lower costs both for land and maritime transportation, as well as faster time to markets

45

46

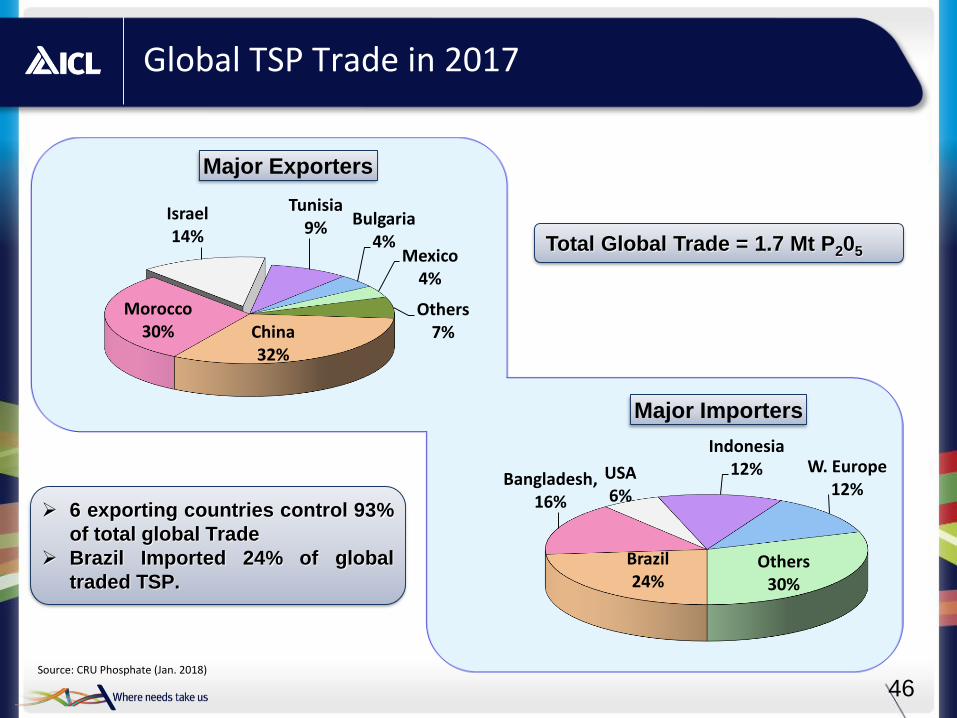

Global TSP Trade in 2017

China32%

Morocco30%

Israel14%

Tunisia9% Bulgaria

4%Mexico

4%

Others7%

Major Exporters

Brazil24%

Bangladesh, 16%

USA6%

Indonesia12% W. Europe

12%

Others30%

Major Importers

Total Global Trade = 1.7 Mt P205

Source: CRU Phosphate (Jan. 2018)

➢ 6 exporting countries control 93%

of total global Trade

➢ Brazil Imported 24% of global

traded TSP.

Phosphate Green Phosphoric Acid

SSP, TSP

Pure Phosphoric Acid

Food additives

Controlled & slow release fertilizers

Liquid & water soluble

fertilizers

Industrial phosphate Salts and acids

Phosphate - Operational Advantages

The operational advantages of Phosphate, starting

with the P2O5 value chain

Phosphate Specialty Fertilizers Specialty solutions47

Key Takeaways

P2O5 value chain in Israel and in China

Significant potash presence in emerging markets

Significant growth potential in semi-specialty and specialty fertilizers

Low production cost at the Dead Sea

Experienced management team

48

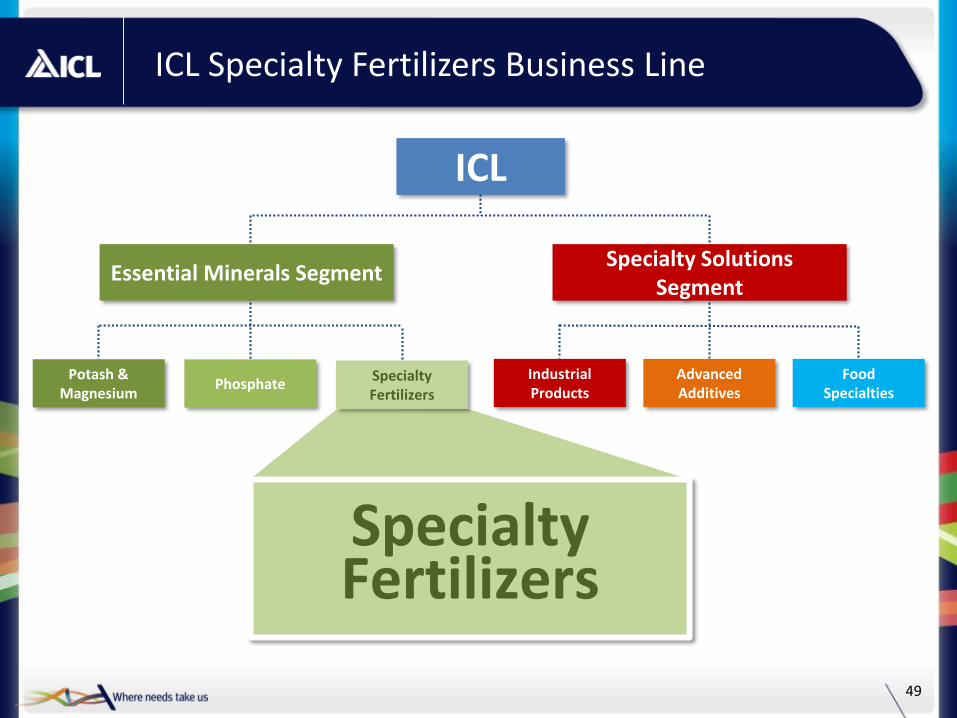

ICL Specialty Fertilizers Business Line

ICL

Essential Minerals SegmentSpecialty Solutions

Segment

Specialty Fertilizers

PhosphatePotash &

Magnesium Food

Specialties Advanced Additives

Industrial Products

Specialty Fertilizers

49

EMPLOYEES WORLDWIDE

~ 900

OPTIMAL PLANT NUTRITION: LESS IS MORE!

* FY2017** Before setoffs and eliminations.*** Before G&A expenses.

Foliar Fertilizer

Controlled Release Fertilizers

$692M$56M

SALES**

OPERATING INCOME***

FY2017 RESULTS

REVENUE BY MARKET SEGMENT*

Horticulture & Turf

28%

Chemicals & other

10%Specialty Ag.

62%

ICL Specialty Fertilizers Profile

50

47%

25%

17%

11%Europe

Americas

ASIAPAC

MEAI

REVENUE BY GEOGRAPHIES*

Fertigation/ Soluble Fertilizers

51

ICL’s Leadership in the Specialty Fertilizers Market

2010

2011

04

2011

05

2012

Xcalibur

(USA)

11

2012

09

20141993

52

Global Players by Product Categories

Coated Fertilizers Solubles / Straights Liquids

SRF CRFSoluble

NPK

MAP/

MKPSOP/CN NOP

Bulk

Liquids

Foliar

Liquids

ICL-SF ^ ^ ^ ^ ^ ^

Compo ^ ^ ^ ^

Haifa Chemicals ^ ^ ^ ^

YARA ^ ^ ^

SQM ^ ^ ^ ^

Kingenta ^ ^ ^ ^

Haifa SQM YARA KingentaCompoICL-SF

ICL Specialty Fertilizers: Our Strengths

▪ Leader in Key Markets

▪ Access to P and K resources, unique access to Polysulphate

▪ Wide Portfolio with well established brands & unique products

▪ Profound agronomic knowledge & strong professional sales force

▪ Advanced P and K chemistry

▪ Advanced and flexible manufacturing technologies

▪ Efficient Supply Chain

▪ Leveraging on supporting global trends

53

54

Our Core Markets and Products Today

Turf & LandscapeGolf courses, sports fields & landscape

Liquid Fertilizers

Growing Media Grass Seeds

Water Soluble Fertilizers (WSF)

Controlled Release Fertilizers (CRF)

Straights (MAP / MKP / Pekacid)

Plant Protection Products

Adjuvants Water Conservation Agents

Liquid Fertilizers

Slow Release Fertilizers

Specialty AgricultureFruit, vegetables & arable crops

Turf & LandscapeGolf courses, sports fields & landscape

Ornamental HorticultureNursery stock, perennials, pot & bedding plants

69%OF 2017 SALES

19%OF 2017 SALES

12%OF 2017 SALES

55

Our Core Markets and Products / Turf

Most stadiums of “La Liga” use ICL products (fertilizers& seeds)

Camp Nou

56

Our Core Markets and Products / Turf

Wimbledon

57

Our Core Markets and Products / Turf

Cardiff

57

58

Specialty Fertilizers and Bio Solutions Became An Important Part of the Ag Input market

Others, 32%

Traditional Fertilizers,63%

Specialty Fertilizers3.5%

~$150bn

Nontraditional application of nutrients (i.e. Soluble, Liquids and Coated)

Advanced bio solutions for plant nutrient and protection

Bio Solutions1.5%

Micro Nutrients1%

Nutrients consumed in small quantities2

N,P,K and Secondary

nutrients1

1 Calcium, Magnesium and Sulfate2 iron, cobalt, chromium, copper, iodine, manganese, selenium, zinc and molybdenum

Specialty Fertilizers market / ~$9bn

Global Trends Driving Shift Towards Specialty Fertilizers

Population growth, urbanization &

reduction in arable land per capita

Regulatory Pressure

ChangingFood Chain

Environmental Trends

New Grower Practices

59

60

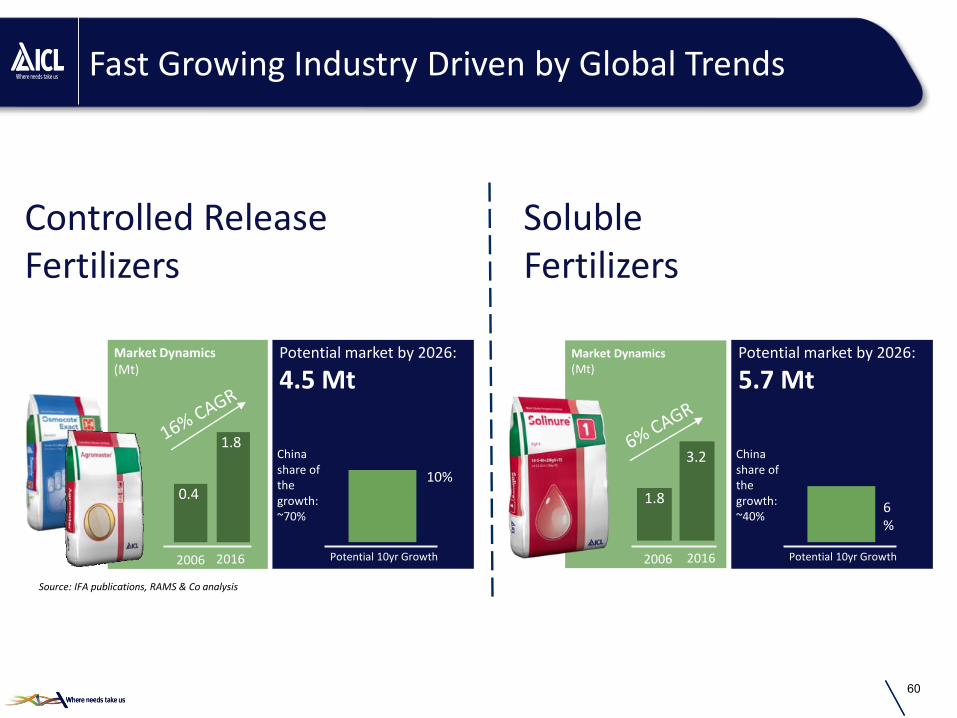

Fast Growing Industry Driven by Global Trends

Controlled Release Fertilizers

SolubleFertilizers

Market Dynamics(Mt)

1.8

3.2

Market Dynamics(Mt)

0.4

1.8

2006 2016 Potential 10yr Growth

Potential market by 2026:

4.5 Mt

10%

China share of the growth: ~70%

2006 2016 Potential 10yr Growth

Potential market by 2026:

5.7 Mt

6%

China share of the growth: ~40%

Source: IFA publications, RAMS & Co analysis

ICL’s Main Growth Drivers in Specialty Agriculture –

Reduce cost of production

Expand Product Portfolio

Establish production in attractive

markets

New cost efficient coating generation

New production plants with focus on emerging markets

Grow with R&D and new Strategic

Partners

61

Leveraging Precision Ag to Grow sales

Digitization of Farms -Sensing, Analytics and Connectivity

Solutions

Prediction Models:•Pest Out•Water Stress•Yield

Weather•Sensing•Prediction

Crop Soil Sensors•Moisture•pH•Temperature

Aerial Imagery•Drones•Satellites

Equipment•Autonomous•Task Assist or

Replacement

Software Platforms•ERP•Farm

Management•Agronomy

Digital Ag:Reduce

Inputs & Increase Yield

a

Big data insights

New productsNew customers

More sales

62

Digital Package to Enhance Sales

Mobile App

Remote sensing of nutrient deficiencies

Data analytics used to offer tailored

products

In-soil temperature

sensor

Integration of data to an

Ag platform

Prescription tool: what fertilizer to

apply when?

63

64

Key Takeaways

ICL Specialty FertilizersAn attractive investment opportunity

Fast Growing Industry Driven by Global

TrendsLeader in Key Markets

Well Positioned for Growth with Wide

Portfolio

Efficient Supply Chain,Strong Professional

Sales ForceEstablished Brands

End User Inspired Innovation, Leveraging

on Precision Ag

Specialty Solutions Segment

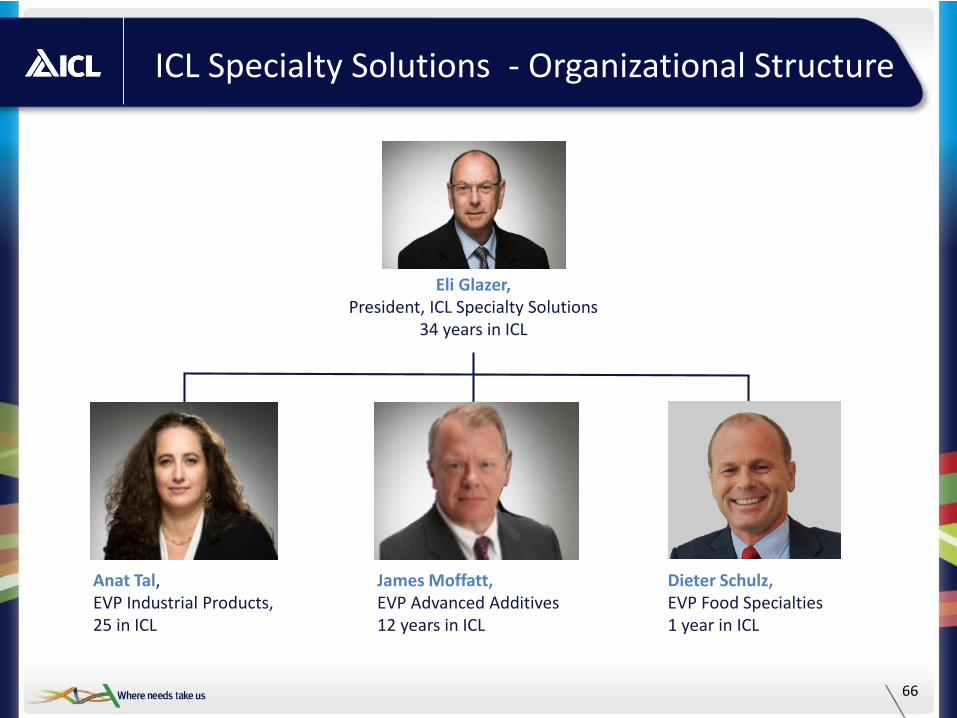

ICL Specialty Solutions - Organizational Structure

66

Anat Tal,EVP Industrial Products,25 in ICL

James Moffatt, EVP Advanced Additives12 years in ICL

Dieter Schulz, EVP Food Specialties1 year in ICL

Eli Glazer, President, ICL Specialty Solutions

34 years in ICL

1,2511,034 1,120 1,193

457555 553 568

526 613659 596

FY 2014 FY 2015 FY 2016 FY 2017

Industrial products Advanced additives Food specialties

Specialty Business Provide Balance

67

Specialty Solutions Sales*** ($M)

Segment Operating Income ($M)** & ***

Adjusted to organizational structure as of Q1 2017 * Total prior to elimination of inter-business lines’ sales**Excluding G&A, unallocated expenses and eliminations*** Proforma adjusted for divestment of fire safety and P2S5 businesses

2,202* 2,332*2,234* 2,357*

371

451

534 554

FY 2014 FY 2015 FY 2016 FY 2017

68

$1.2Bn 2017 SALES*

$303M 2017 OPERATING INCOME**

~1,600EMPLOYEES WORLDWIDE

Industrial Products: Impressive Performance Driven by Value Based Strategy and Cost Reduction

Note: Sales and operating income according to Organizational Structure as of Q1 2017. All numbers are rounded.* Before setoffs and inter-segment eliminations.** Before G&A expenses.

20% CAGR IN OPERATING INCOME

200 225286 303

16%

22%26% 25%

0%

5%

10%

15%

20%

25%

30%

50

100

150

200

250

300

350

2014 2015 2016 2017

Operating income Operating income margin

Flame Retardants

41%

Brominated organic

intermediates & Industrial

34%

Clear brine fluids

15%

Biocides7%

Mercury Control

4%

2017 BROMINE DEMAND BY INDUSTRYMARKET UTILIZATION RATES: 70-80%

FINANCIAL RESULTS

ICL-IP Product Supply Chains

69* RM sourced from 3rd parties

Specialty

Minerals

plants:Israel

France*

Bromine compounds plants:

IsraelNetherlands

China

Phosphorus compounds plants:

GermanyUSA

MgClSaltsKCl

Purchased

Customers

Produced

ICL-IP Market Leadership

in Flame Retardants

in Bromine capacity

in Bromine compounds plant

in Bromine Iso-tank fleet

in Brominated biocides

in Phosphorus FRs

in Clear Brine Fluids

in Self-extinguishing Hydraulic fluids

in Solid MgCl

in Magnesia for Nutraceutical market70

Global Trends and Major End Markets

PopulationRegulation & EnvironmentalStandard of living

FURNITURE & TEXTILETRANSPORTATION

WATER TREATMENT

CONSTRUCTION

INTERMEDIATES FOR FOOD,

PHARMA, AGRO and Other OIL & GAS

POWER PLANTS

ELECTRONICS

71

Regulation

New target 1-7Yet to

follow 1.3

Existing 1-30 30

Major Trends and ICL Solutions

72

Trends

Clean AirMercury Emissions Control

MERQUEL®

ICL’s Solutions

Comparison of Hg Emission limits (µgr/m3)

73

Renewable energy Energy storage

Electrolytes for Bromine Flow battery

Trends ICL’s Solutions

Major Trends and ICL Solutions

74

Trends ICL’s Solutions

Electric car/ Autonomous car

New generation polymeric FRs

Major Trends and ICL Solutions

75

Trends ICL’s Solutions

Major Trends and ICL Solutions

Home automation New generation polymeric FRs

76

Trends ICL’s Solutions

Water shortage and treatment

New Biocides

Major Trends and ICL Solutions

Live

77

Note: Sales and operating income according to Organizational Structure as of Q1 2017.All numbers are rounded.(1) Before G&A expenses.(2) Proforma results adjusted for divestments of fire safety and P2S5 businesses

SALES DISTRIBUTIONS 2017

78

$568M 2017 SALES(2)

$85M 2017 OPERATING INCOME(1)

~900

EMPLOYEES WORLDWIDE

KEY ADVANTAGES

• Full phosphate chain from rock

to salts

• Largest global footprint in

specialty phosphates

GROWTH STRATEGY

Advanced Additives Benefits from Vast Global Footprint and Backward Integration

Phosphate Acids59%

Industrial phosphates

38%

P44%

• Geographic Expansion

• Product Differentiation

• Cost optimization /

“Lean & Reliable”

• Support growth through opportunistic M&A

FINANCIAL RESULTS

We Have Built a World-Class Advanced Additives Portfolio

79

Phosphate Salts and Acids Paints and Coatings

Description • Technical Phosphates & Related Specialties; food and technical grade Phosphoric Acids

• Specialty phosphates and blends, selected organic chemistry

Key Applications • Metal treatment, water treatment, cleaners, oral care, cola drinks, asphalt modification, others

• Corrosion Inhibition, Flash Rust Inhibitors, Tannic Stain Inhibitors

Example Customers & Distributors

• P&G, Henkel, Colgate, Coca-Cola, Pepsi, Chemetall

• Univar, Brenntag

• Sherwin Williams, Behr Paint

• Specialty Distributors based on mutual exclusivity

• High-growth new applications in Meat and Dairy

• Expand portfolio through tailored solutions

• Increase footprint in growing emerging markets

• Support growth through opportunistic M&A

Food Specialties Growth Driven by Global and Portfolio Expansion, Supported by Market Trends

80

2017 BUSINESS LINE BREAKDOWN

$596M2017 SALES(1)

$51M2017 OPERATING INCOME(2)

~850EMPLOYEES WORLDWIDE

(1) Before setoffs and inter-segment eliminations.(2) Before G&A expenses.All numbers are rounded.

MARKET TRENDS

• Growing middle class in emerging markets

• Demand for longer shelf- life

• “On the go”

• Health and Nutrition(gluten free, reduced salt, etc)

GROWTH STRATEGY

GLOBAL SALES FOOTPRINT*

Spices

6%

Dairy Proteins

25%Food

Phosphates, Blends,

Multi-blends

69%

Description • $200M in 2016 sales

• Providing solutions for modifying texture and stability of food products, including meat substitutes

• $280M in 2016 sales

• Produces milk and whey proteins for food ingredients

• Provides integrated solutions based on dairy proteins and phosphate additives

• $180M in 2016 sales

• ICL leavening acids impact the appearance, texture and volume of bakery products

Key Applications • Continued development of applications for low-sodium salts (SALONA™) from the Dead Sea

• Development of new products based on milk proteins

• Novel product applications by exploiting synergies betweenfood phosphates, proteins, starches and fibers

Recent Acquisitions • In 2014, completed acquisition of the HagesudGroup, a German producer of premium spice blends and food additives for meat processing

• In 2015, completed acquisition of ProlactalGmbH, a leading European producer of dairy proteins

Key Customers

Vast Product Portfolio Serving a Variety of End Markets

81

Meat, Poultry and Seafood:

Dairy and Dairy Protein: Bakery and Other:

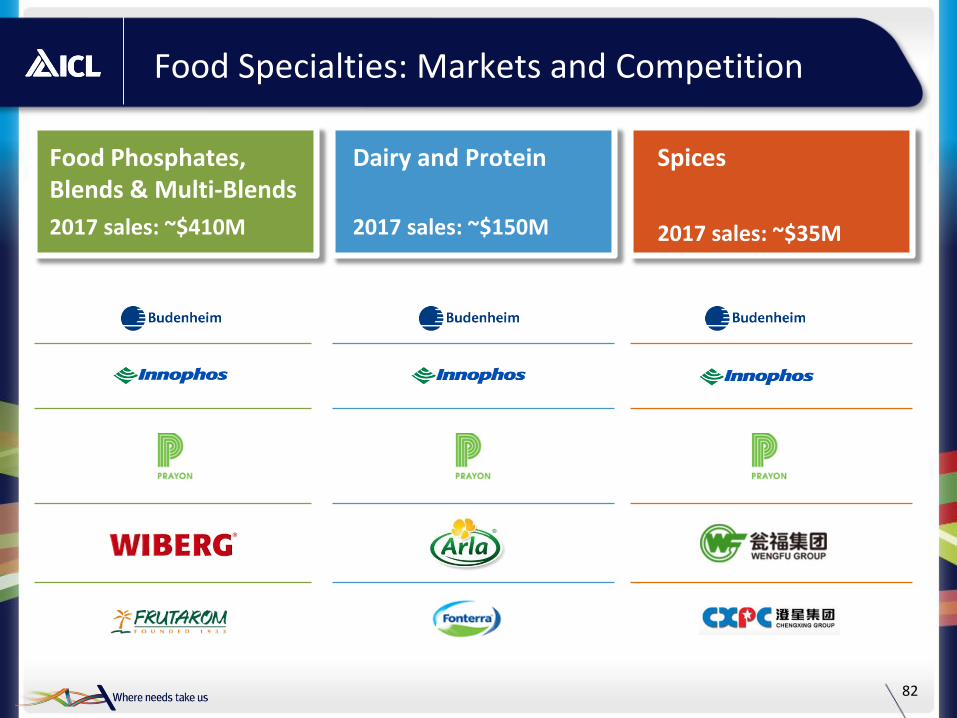

Food Specialties: Markets and Competition

82

Food Phosphates, Blends & Multi-Blends

2017 sales: ~$410M

Dairy and Protein

2017 sales: ~$150M

Spices

2017 sales: ~$35M

Main Takeaways for Specialty Solutions Division

83

Backward integration to Bromine and Phosphate

The only Global player with worldwide presence

Innovation capabilities

Growing sales and margins despite competitive market environment

Clear, proven, value based strategy

Thank You