prdnationwide geelong property watch q2 l 2012

DESCRIPTION

PRDnationwide Geelong Property Watch Q2 l 2012TRANSCRIPT

www.prdresearch.com.au Your home of property knowledge

Second Quarter │2012

GEELONG/LARA AREA Property Watch®

Corio Bay, Geelong

MARKET INDICATORS

Change from Last Year Half Year

HOUSE SALES

HOUSE MEDIAN -

UNIT SALES

UNIT MEDIAN

LAND SALES

LAND MEDIAN

The indicators depicted above are based on the twelve

months ending January 2012.

KEY HIGHLIGHTS

House prices for the twelve months to

January 2012 are flat, whilst unit prices

are up 3.2%.

Vacant land shortages see an 11.6%

growth in the median price, which is in

line with the ten year growth rate of

12.6%.

GEELONG/LARA AREA MARKET OVERVIEW

The following Property Watch report is the result of an investigation into the

historic and current market trends of the Geelong/Lara Area, which encompasses

the metropolitan area of Geelong and surrounding townships including Avalon,

Lara, Leopold and Little River. The coastal townships in the area such as

Torquay, Barwon Heads, Ocean Grove are excluded as they are a distinct market

in themselves.

It might be anticipated that the Geelong/Lara market would follow closely in the

footsteps of the Melbourne market, Geelong itself being a large metropolitan

centre and virtually on Melbourne’s doorstep. The Geelong/Lara area has been

more typical of regional markets however with prices only recently showing signs

of some softening, even though volumes have been trending downwards for

several periods.

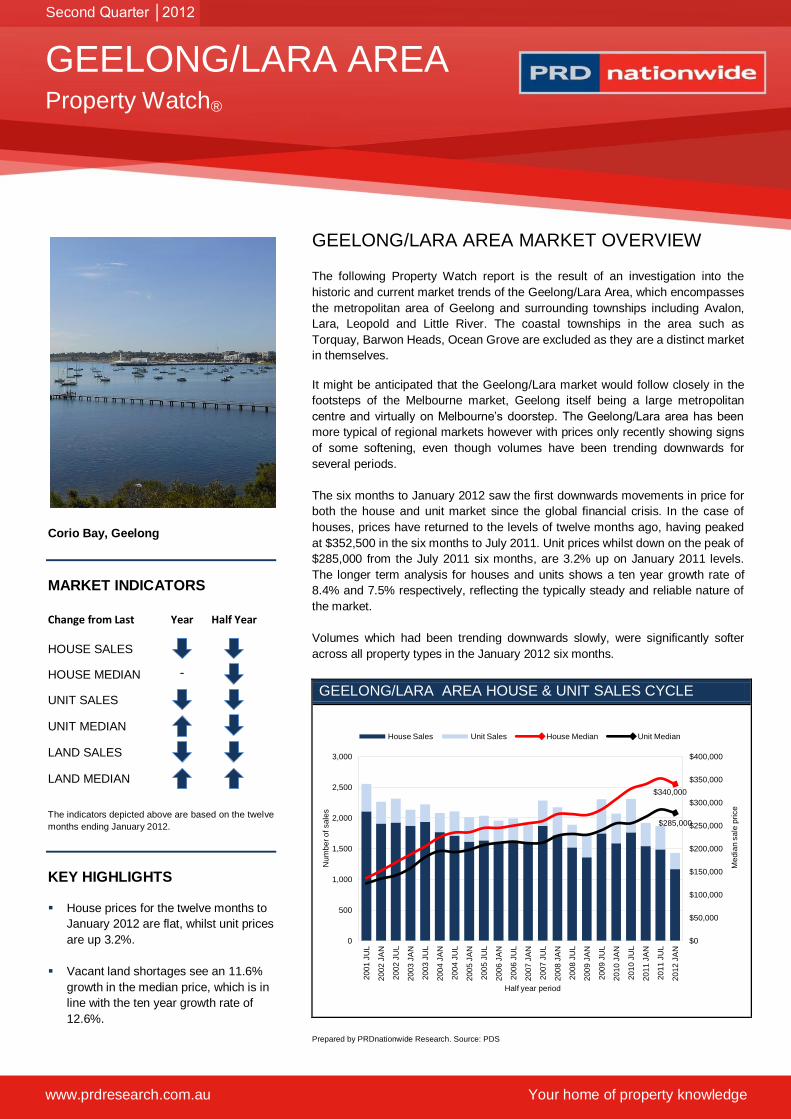

The six months to January 2012 saw the first downwards movements in price for

both the house and unit market since the global financial crisis. In the case of

houses, prices have returned to the levels of twelve months ago, having peaked

at $352,500 in the six months to July 2011. Unit prices whilst down on the peak of

$285,000 from the July 2011 six months, are 3.2% up on January 2011 levels.

The longer term analysis for houses and units shows a ten year growth rate of

8.4% and 7.5% respectively, reflecting the typically steady and reliable nature of

the market.

Volumes which had been trending downwards slowly, were significantly softer

across all property types in the January 2012 six months.

GEELONG/LARA AREA HOUSE & UNIT SALES CYCLE

Prepared by PRDnationwide Research. Source: PDS

$340,000

$285,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

0

500

1,000

1,500

2,000

2,500

3,000

20

01

JU

L

20

02

JA

N

20

02

JU

L

20

03

JA

N

20

03

JU

L

20

04

JA

N

20

04

JU

L

20

05

JA

N

20

05

JU

L

20

06

JA

N

20

06

JU

L

20

07

JA

N

20

07

JU

L

20

08

JA

N

20

08

JU

L

20

09

JA

N

20

09

JU

L

20

10

JA

N

20

10

JU

L

20

11

JA

N

20

11

JU

L

20

12

JA

N

Me

dia

n s

ale

pri

ce

Num

be

r o

f sa

les

Half year period

House Sales Unit Sales House Median Unit Median

PRDnationwide does not give any warranty in relation to the accuracy of the information contained in this report. If you intend to rely upon the information contained herein, you must take note that the information, figures and projections have been provided by various sources and have not been verified by us. We have no belief one way or the other in relation to the accuracy of such information, figures and projections. PRDnationwide will not be liable for any loss or damage resulting from any statement, figure, calculation or any other information that you rely upon that is contained in the material. Prepared by PRDnationwide Research © All medians and volumes are calculated by PRDnationwide

Research. Use with written permission only. All other responsibilities disclaimed. © 2012

Your home of property knowledge www.prdresearch.com.au

Research Analyst │Mark Corboy P (0400) 520 717 E [email protected]

PRDnationwide Geelong │Principal Alex Campbell P (03) 52 222 566 F (03) 52 222 604 E [email protected]

The current shortage

of Vacant Land has

seen the median price

grow 11.6% in the last

twelve months.

HOUSE PRICE POINTS

Prepared by PRDnationwide Research. Source: PDS

VACANT LAND PRICE POINTS

Prepared by PRDnationwide Research. Source: PDS

In the case of Houses and Units softening sales levels appear to be largely due

to weaker buyer sentiment. Media speculation regarding the state of the economy

generally and particularly in relation to manufacturing, which has a significant

presence in the Geelong economy with Ford and Alcoa both major employers,

appears to have dampened buying sentiment. Peter Fort of Geelong PRD notes

that enquiry levels remain strong, particularly at the lower price points. Enquiry

levels from out of town investors, particularly Melbourne investors, is especially

high reaching 50% of enquiry for some properties. Mr Fort says that well priced

properties in the mid to lower range are selling strongly. Enquiry levels in the

higher price brackets are also quite strong, but buyers appear to be slower to act

at these levels.

Despite lower buyer sentiment, the house price points table indicates that the

higher priced brackets are increasing their share of total sales. Sales under

$300,000 dominated the market for the twelve months to January 2009 with 59%

of all sales, however as at January 2012 they now represent only 30% of the

market. Sales over $600,000 have doubled from 4% of the market to 8% over the

same period.

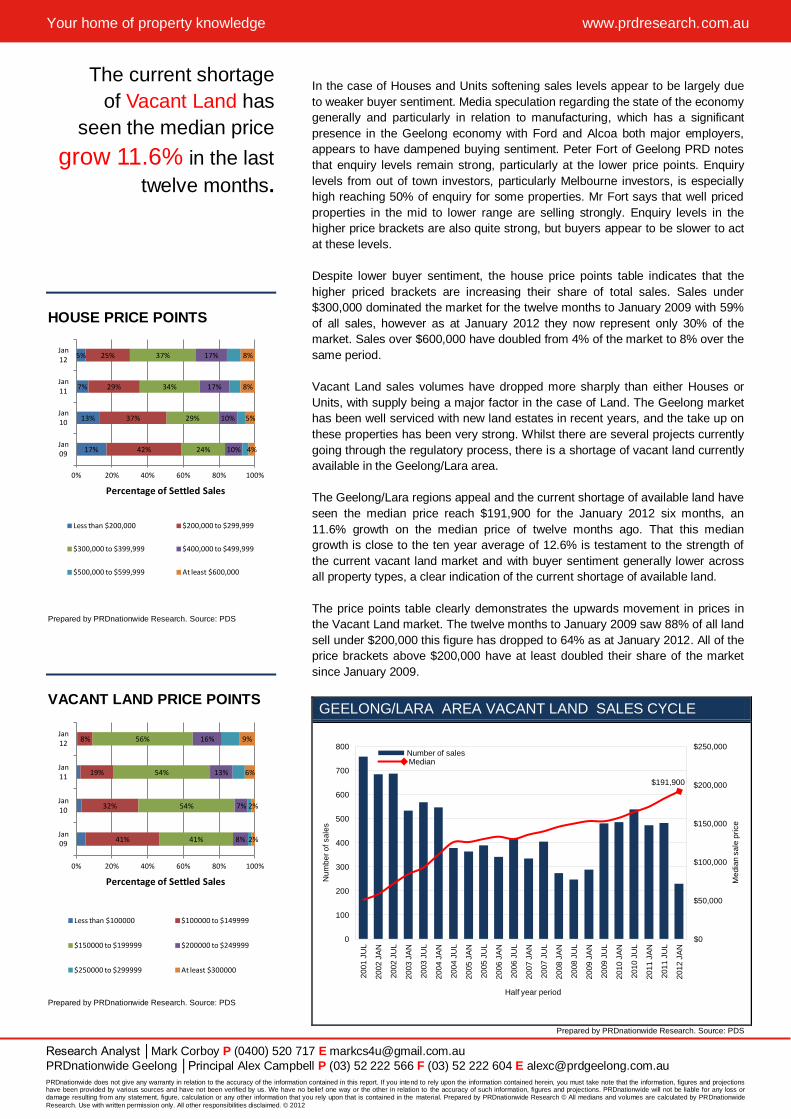

Vacant Land sales volumes have dropped more sharply than either Houses or

Units, with supply being a major factor in the case of Land. The Geelong market

has been well serviced with new land estates in recent years, and the take up on

these properties has been very strong. Whilst there are several projects currently

going through the regulatory process, there is a shortage of vacant land currently

available in the Geelong/Lara area.

The Geelong/Lara regions appeal and the current shortage of available land have

seen the median price reach $191,900 for the January 2012 six months, an

11.6% growth on the median price of twelve months ago. That this median

growth is close to the ten year average of 12.6% is testament to the strength of

the current vacant land market and with buyer sentiment generally lower across

all property types, a clear indication of the current shortage of available land.

The price points table clearly demonstrates the upwards movement in prices in

the Vacant Land market. The twelve months to January 2009 saw 88% of all land

sell under $200,000 this figure has dropped to 64% as at January 2012. All of the

price brackets above $200,000 have at least doubled their share of the market

since January 2009.

GEELONG/LARA AREA VACANT LAND SALES CYCLE

Prepared by PRDnationwide Research. Source: PDS

17%

13%

7%

5%

42%

37%

29%

25%

24%

29%

34%

37%

10%

10%

17%

17%

4%

5%

8%

8%

0% 20% 40% 60% 80% 100%

Jan 09

Jan 10

Jan 11

Jan 12

Percentage of Settled Sales

Less than $200,000 $200,000 to $299,999

$300,000 to $399,999 $400,000 to $499,999

$500,000 to $599,999 At least $600,000

41%

32%

19%

8%

41%

54%

54%

56%

8%

7%

13%

16%

2%

2%

6%

9%

0% 20% 40% 60% 80% 100%

Jan 09

Jan 10

Jan 11

Jan 12

Percentage of Settled Sales

Less than $100000 $100000 to $149999

$150000 to $199999 $200000 to $249999

$250000 to $299999 At least $300000

$191,900

$0

$50,000

$100,000

$150,000

$200,000

$250,000

0

100

200

300

400

500

600

700

800

20

01

JU

L

20

02

JA

N

20

02

JU

L

20

03

JA

N

20

03

JU

L

20

04

JA

N

20

04

JU

L

20

05

JA

N

20

05

JU

L

20

06

JA

N

20

06

JU

L

20

07

JA

N

20

07

JU

L

20

08

JA

N

20

08

JU

L

20

09

JA

N

20

09

JU

L

20

10

JA

N

20

10

JU

L

20

11

JA

N

20

11

JU

L

20

12

JA

N

Me

dia

n s

ale

pri

ce

Nu

mb

er

of

sa

les

Half year period

Number of sales Median