presentatie jorij abraham masterclass omnichannelmanagement #kennisenkunde

TRANSCRIPT

© Shopping 2020Jorij Abraham 2

Amsterdam, 26th of May 2015

SHOPPINGTOMORROW HIGHLIGHTS“The best way to predict your future is to create it” – Abraham Lincoln

© Shopping 2020Jorij Abraham 44

Ecommerce Europe represents 25,000+ firms that sell online in EuropeEcommerce Europe is represented by 16 National Assocations

Our Mission:To foster & promote the interest of

e-commerce in Europe

16National

Associations

25.000+NationalMembers

35+European

Business Partners

Advocacy & Communication

Research & Networking

European Trust Certificate

INTRODUCTION

© Shopping 2020Jorij Abraham 66

The “cookie” law is costing Europe € 1.8 billion per yearINTRODUCTION

© Shopping 2020Jorij Abraham 88

Agenda

Why Shopping2020?

Highlighs:• The Market• The Consumer• Technology• Sustainability• Competition

What’s Next?

© Shopping 2020Jorij Abraham 99

Why Shopping2020?

Disintermediation

Google Glasses

3D Printing

Amazonization

Changing consumer

WHY SHOPPING2020?

© Shopping 2020Jorij Abraham 1010

The central research question of Shopping2020

How will the consumer shop in 2020 and what actions should be taken on a national, branch and

company level upon that B2C-operating companies can

successfully respond to this, both nationally and internationally?

WHY SHOPPING2020?

© Shopping 2020Jorij Abraham 1111

A different research approach was chosen than normally. The business, science & political communities were invited to create their own vision

Customer Journey

KeyThemes

FutureTrends

Identifying expert groups, & substantiating trends and

their impact

All trends are combinedwith concrete actions and

recommendations

Determiningresearch questions, expert groups and

desk research

Two research studies among 444 experts and 12,000

consumers

Expert groups define actions based on weighted trends

Desk research(March 1 – June 1)

Expert Trend Analysis(June 13 - Nov. 15)

Wisdom of the Crowds(Oct. 15 – Nov. 25)

Action Plans(Nov. 1 - Dec. 15)

Synthesis(Dec. 15 - March 15, ‘14)

WHY SHOPPING2020?

© Shopping 2020Jorij Abraham 1212

In total, more than 460 experts worked for six months on Shopping2020WHY SHOPPING2020?

© Shopping 2020Jorij Abraham 1313

The 460 experts were divided across 19 themes. Each expert group produced a report of its own. McKinsey supported in writing the synthesis.

ShopperBehavior

Cross-border (e-)Commerce

TechnologicalFuture Touch

PointsEcological Political / Legal

Orientation Selection

Transaction Delivery

BusinessModels

Omni-channelOrganization

Security & FraudThe New Shopping

Street

Smartershopping

Supply Chain

Future Trends

Customer Journey Key Themes

TravelAction Plan

Finance Action Plan

Retail Action Plan

…Action Plan

Action PlanShopping2020

Customer CareCustomer

Data Value Management

Online Business …

Shopping2020Vision

WHY SHOPPING2020?

© Shopping 2020Jorij Abraham 1414

The program organization of Shopping2020

Founding Partners: Scientific Partners:Knowledge Partners:

Program mgt: Jorij AbrahamMar/Com: Inge DemoedResearch: Eveline PoerinkCongress: Marin Wiellersen

Travel Retail Finance

Expert GroupShopperBehavior

Expert Group Cross-Border (e-

)Commerce

Expert Group Technological

Expert Group Future Touch Points

Expert Group Ecological

Expert GroupPolitical /

Legal…… … … …

Expert GroupOnline Business

Expert GroupBusinessmodels

Expert Group Security / Fraud

Expert Group Omni-channel Organization

Expert Group The New Shopping

Street

Expert GroupSupply Chain

………

… …

Expert GroupOrientation

Expert Group Selection

Expert Group Transaction

Expert Group Delivery

Expert Group Customer

Care

Expert GroupCustomer Data

Value ManagementArjen Bonsing …… … … … …

Committee of Recommendation

ProgramBoard

FutureTrends

Key Themes

CustomerJourney

SupportTeam

…Dymfke Kuijpers

…Axel Groothuis

Ed Nijpels (Chairman)Bernard Wientjes (VNO-NCW)Arie van Bellen (Director ECP)Martijn van Dam (MoP PvdA)Jan Kees de Jager (former Minister of Finance)

Cor Molenaar (Erasmus University)Kitty Koelemeijer (Nyenrode University)Walther Ploos van Amstel (Free University)Erik Fledderus (Director TNO)Heleen van Oord (Director DQ&A)

Giovanni Colauto (CEO Bijenkorf)Harry Bruijniks (CEO Euretco)Ronald van Zetten (CEO Hema)Joost Romeijn (CEO Sundio Group)Paul Nijhof (CEO RFS Holding/Wehkamp)Annemarie van Gaal (CEO van Gaal & Co.)

Dick Boer (CEO Ahold)Herna Verhagen (CEO PostNL)Nick Jue (CEO ING NL)Michiel Buitelaar (COO Sanoma Media)Danny van der Eijk (Chairman Achmea)Harry van Dorenmalen (CEO IBM Europe)

Network Partners:

SmarterShopping

Media Partners:

WHY SHOPPING2020?

© Shopping 2020Jorij Abraham 1515

Several results of Shopping2020

360 visitorsfor ShoppingTomorrow

1000+ visitors for ShoppingToday

150+ expert group meetings

25+ external presentations

20,000+ reports downloadedat Shopping2020.nl

20+ company visits

370+ press publications

2,500+ visitors for ShoppingTogether

5,000+ subscriptions tothe Shopping2020 Newsletter

60+ In-CompanyMaster Classes

460 involved experts

150+ participating companies

Supported by 16 branch organizations

1,280 Twitter followers

Research among 12,000 consumers

3,500+ unique visitors p/wat Shopping2020.nl

WHY SHOPPING2020?

© Shopping 2020Jorij Abraham 1616

You can download all reports from Shopping2020.nlWHY SHOPPING2020?

© Shopping 2020Jorij Abraham 17

THE KEY FINDINGSWhen we imagine the future we only see the present.

© Shopping 2020Jorij Abraham 1818

We all say things that we may regret later…THE KEY FINDINGS

© Shopping 2020Jorij Abraham 1919

Video – There’s no need for 4G…THE KEY FINDINGS

© Shopping 2020Jorij Abraham 23

THE MARKET“If I had asked people what they wanted, they would have said faster horses.” Henry Ford

© Shopping 2020Jorij Abraham 2424

83%

17%

Relation online/offline purchases

Offline verkoop

Online verkoop

35%

14%13%

9%

7%

6%

4%

4%4%

1%

1%1%

1% 1%

Market share per segment Food/Nearfood/Health

Home & Garden

Fashion: apperal

Consumer electronics

Insurances

Travel packages

Fashion: shoes & personallifestyleFlight tickets &accommodationsTelecom

Media & Entertainment

Toys (excl. Games)

Event tickets

Books

Sport (hardware)

Source: Desk research GfK 2012* The definition of consumer spending is smaller than applied by Statistics Netherlands and can be found in the full report.

Where are we in 2012: € 65.9 billion in Dutch consumer spending of which 17% is purchased online in the Netherlands

THE MARKET

Offline purchases

© Shopping 2020Jorij Abraham 2525

Online grows explosively over the next seven years in the NetherlandsTHE MARKET

Online; 20%

Offline; 80%

2013

Online; 28%

Offline; 72%

2017

Online; 36%

Offline; 64%

2020

Source: GfK Expert Research, September 2013 among 444 Experts

© Shopping 2020Jorij Abraham 2727

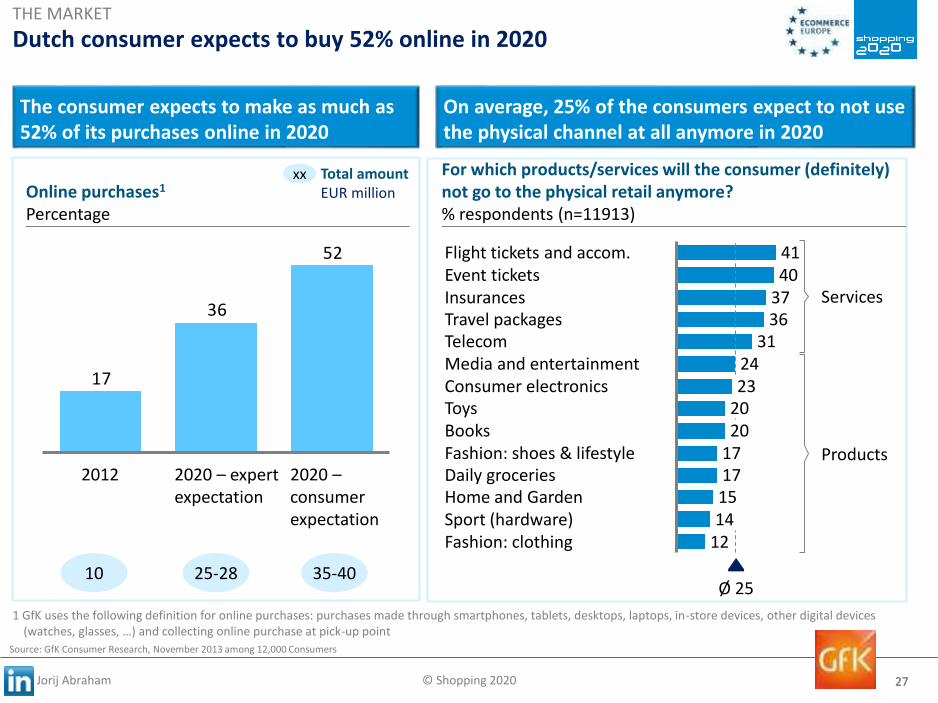

Dutch consumer expects to buy 52% online in 2020 THE MARKET

Source: GfK Consumer Research, November 2013 among 12,000 Consumers

52

36

17

2020 –consumer expectation

2020 – expert expectation

2012

Total amountEUR million

10 25-28

On average, 25% of the consumers expect to not use the physical channel at all anymore in 2020

Ø 25

Fashion: clothing 12Sport (hardware) 14Home and Garden 15Daily groceries 17Fashion: shoes & lifestyle 17Books 20Toys 20Consumer electronics 23Media and entertainment 24Telecom 31Travel packages 36Insurances 37Event tickets 40Flight tickets and accom. 41

Online purchases1

Percentage

For which products/services will the consumer (definitely) not go to the physical retail anymore?% respondents (n=11913)

xx

35-40

The consumer expects to make as much as 52% of its purchases online in 2020

1 GfK uses the following definition for online purchases: purchases made through smartphones, tablets, desktops, laptops, in-store devices, other digital devices (watches, glasses, …) and collecting online purchase at pick-up point

Services

Products

© Shopping 2020Jorij Abraham 2828

17%

50% 53% 53% 57%49%

36%

21% 20% 23%

10% 10% 8%13%

1%

+19%

+31% +23% +23% +14%

+14%

+15%

+26%+20% +11%

+17% +17%+14%

+9%

+13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

status 2012 groei t/m 2020

36%

81%76% 76%

71%

63%

51%47%

40%34%

27% 27%22% 22%

14%

THE MARKET

Status 2020Status 2012

The growth of online differs significantly per segment in the Netherlands: Travel is in the lead, Food grows fast

Source: GfK Expert Research, September 2013 among 444 Experts

Online market share per market segment in 2020

© Shopping 2020Jorij Abraham 3030

65.9 64.6

70.173.6

11.012.6

19.4

26.9

54.952.0 50.7

46.6

0

10

20

30

40

50

60

70

80

2012 2013 2017 2020

Total consumer spending (corrected for inflation)

Totale markt

Online

Offline

€b

illio

ns

+12%

-15%

+145%

Online replaces Offline but total spending only grows marginallyTHE MARKET

© Shopping 2020Jorij Abraham 3131

112

126

122

113

112

110

110

108

108

107

106

105

104

104

90

80 90 100 110 120 130

Totaal

Telecom

Home & Garden

Food/Nearfood/Health

Media & Entertainment

Losse vliegtickets & accommodaties

Tickets voor e venementen

Fashion: schoenen & personal lifestyle

Consumentenelektronica

Pakketreizen

Sport

Fashion:kleding

Speelgoed

Verzekeringen

Boeken

THE MARKET

The growth per market segment differs significantly. For most of them, growth is limited.

Total

Telecom

Home & Garden

Food/Near food/Health

Media & Entertainment

Flight tickets & accommodations

Event tickets

Fashion: shoes & personal lifestyle

Consumer electronics

Travel packages

Sport (hardware)

Fashion: apparel

Toys (excl. Games)

Insurances

Books

Source: GfK Expert Research, September 2013 among 444 Experts

Growth per market segment (online & offline) in relation to 2012

© Shopping 2020Jorij Abraham 32

THE CONSUMER“There is only one boss. The customer. And he can fire everybody in the company from the chairman on down, simply by spending his money somewhere else...”

© Shopping 2020Jorij Abraham 3333

In 2020, there will be (almost) no digital illiterates anymore…

Source: Gary Swartz, The Impulse Economy Photo’s: iStock

THE CONSUMER

© Shopping 2020Jorij Abraham 3434

The consumer of 2020 will be more powerful than ever…THE CONSUMER

I know

• more about the product….

• the lowest prices…

• where it’s available...

I determine

• what I read, see, hear and do

• where, when and how I make my

purchases

I make

• or break

• your product/service

© Shopping 2020Jorij Abraham 3636

Slimmed-down alternativeBargain hunter

Source: McKinsey

Example: Canceling existing travel plansApplies to:Leisure spending

Example: Going to a three-star alternative instead of a luxurious hotelApplies to: insurances, medical/health, communication

Example: Using the Internet to find the best priceApplies to:Groceries, Electronics, Toys and Games, Clothing

A

B

Decreasing volume C

E D

Lowering prices

THE CONSUMER

Consuming less seems to be a trend that will remain after the crisis

Control spending

Replace if necessary

Do-It-Yourself

Example: Staying at friends o family instead of a hotelApplies to: Home furnishing

Example: Postponing travel plansApplies to: Home Furnishing, Electronics, Cars

© Shopping 2020Jorij Abraham 3737

Consumers look for product information on a wide range of websites, but more than 50% limit their search to one web shop

THE CONSUMER

17

52

14

17

4+2

31

# of web shops visited until choice is made

There are more channels available to find information and consumers use them all

However, 87% of the consumers limit their search to a maximum of three web shops

SOURCE: GfK; Expert Report "Cross-Border (e-)Commerce"

Consultation of channels by consumersPercentage of respondents

# of web shops visited until purchasePercentage of respondents

41

56

63

78

81

81

81

93

© Shopping 2020Jorij Abraham 3838

% of research per channel

The consumer starts (en ends) its search increasingly often at one place

SOURCE: McKinsey iConsumer U.S. 2012

12

15

10

18

17

19

19

15

22

16

14

13

23

18

13

Pet supplies

9Clothing

10

Furniture 10

Office supplies 11

Jewelry 12

Footwear 12

Sporting goods 13

Home décor 14

Computer HW & SW 16

Electronics 21

Video games 22

Music 31

Toys 31

DVD/Video 34

Books 42

Am

azo

n-o

wn

ed

Go

ogl

e-o

wn

ed

NOT EXHAUSTIVE

THE CONSUMER

© Shopping 2020Jorij Abraham 3939

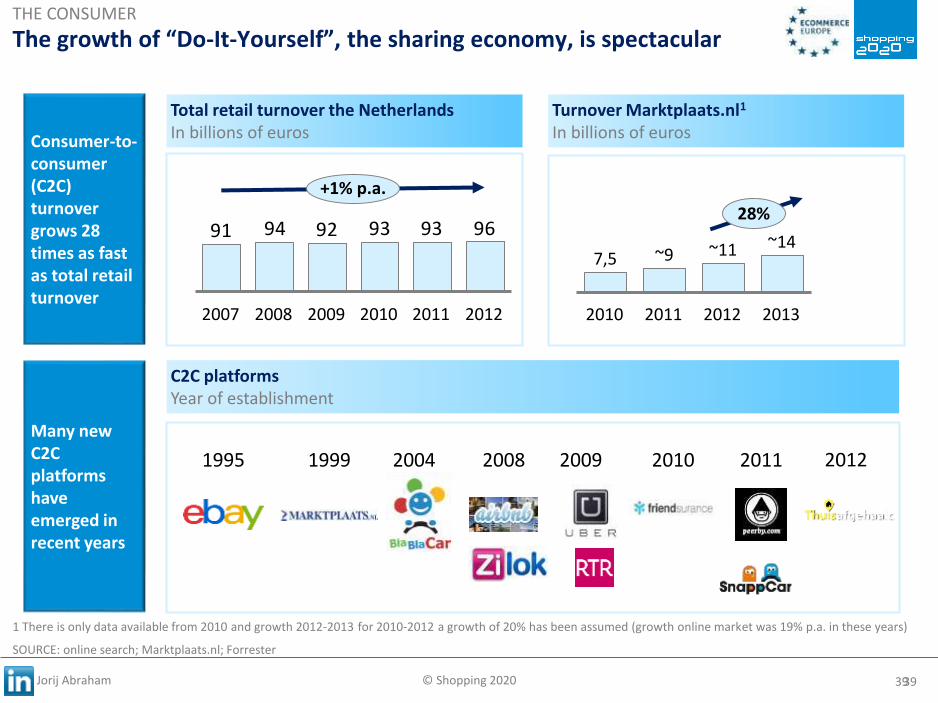

The growth of “Do-It-Yourself”, the sharing economy, is spectacular

SOURCE: online search; Marktplaats.nl; Forrester

969393929491

2007

+1% p.a.

20122011201020092008

Consumer-to-consumer (C2C) turnover grows 28 times as fast as total retail turnover

Total retail turnover the NetherlandsIn billions of euros

Many new C2C platforms have emerged in recent years

C2C platformsYear of establishment

20041995 1999 2008 2009 2010 2011 2012

THE CONSUMER

1 There is only data available from 2010 and growth 2012-2013 for 2010-2012 a growth of 20% has been assumed (growth online market was 19% p.a. in these years)

2010 2012 20132011

~97,5 ~11 ~14

Turnover Marktplaats.nl1

In billions of euros

28%

© Shopping 2020Jorij Abraham 4040

Why buy something if you can share almost everything?THE CONSUMER

© Shopping 2020Jorij Abraham 4444

One million Germans have shared a car last yearThe market grew with 37,4% in 2014 (51% in 2013)

http://www.carsharing.de/presse/pressemitteilungen/pressemitteilung-vom-16032015

© Shopping 2020Jorij Abraham 4545

The sharing economy can have a huge impact in a very short period of timeLyft caused a reduction of 30% in taxi turnover in the Bay Area in 2013

THE CONSUMER

Source: http://en.wikipedia.org/wiki/Lyft www.sanjose.com/2013/10/23/ridesharing_service_lyft_disrupts_silicon_valley/

© Shopping 2020Jorij Abraham 4646

Pley, 75.000 toysets hired and countingAllowing consumers to save 75% on the cost of buying Lego

THE CONSUMER

© Shopping 2020Jorij Abraham 4747

Borrow my doggy, matching dog owners & borrowersDog owners pay € 44,99 p/y, borrowers € 9,95 p/y

THE CONSUMER

© Shopping 2020Jorij Abraham 4848

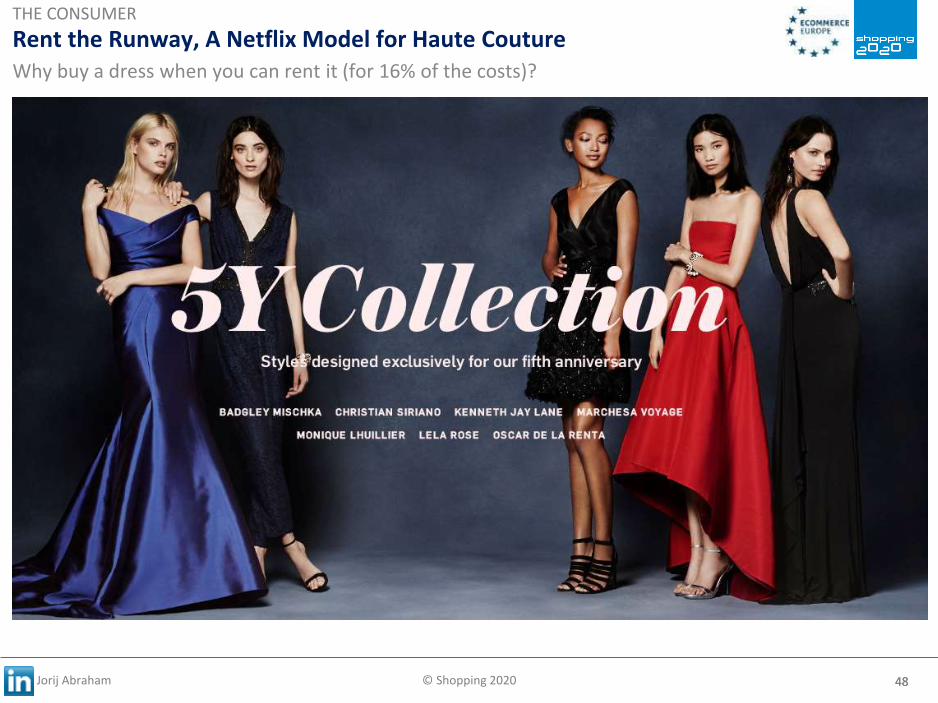

Rent the Runway, A Netflix Model for Haute CoutureWhy buy a dress when you can rent it (for 16% of the costs)?

THE CONSUMER

© Shopping 2020Jorij Abraham 4949

Marleen cooks, local cooks cook for youTHE CONSUMER

© Shopping 2020Jorij Abraham 51

TECHNOLOGYWe're not a retailer competing in Silicon Valley. We're building an Internet technology company inside the world's largest retailer.” - Wallmart

© Shopping 2020Jorij Abraham 5252

The Internet has become something gigantic…

Source: www.internetlivestats.com/

© Shopping 2020Jorij Abraham 5353

Towards 2020, hundreds of new technologies will come our way…TECHNOLOGY

SOURCE: Gartner Hype Cycle 2014

© Shopping 2020Jorij Abraham 5454

The pace of innovation and adoption of technology is increasing exponentially

SOURCE: McKinsey

Nintendo WiiiPadiPhoneNetflixBlackBerryiPod

Number of days until sale of one million items

TECHNOLOGY

2874

~300+

~360+

~13

~180

© Shopping 2020Jorij Abraham 5555

We truly believe in omnichannel, because the customer is

omnichannel. Adriaan Thierry

E-VP Marketing, Formats & E-Commerce

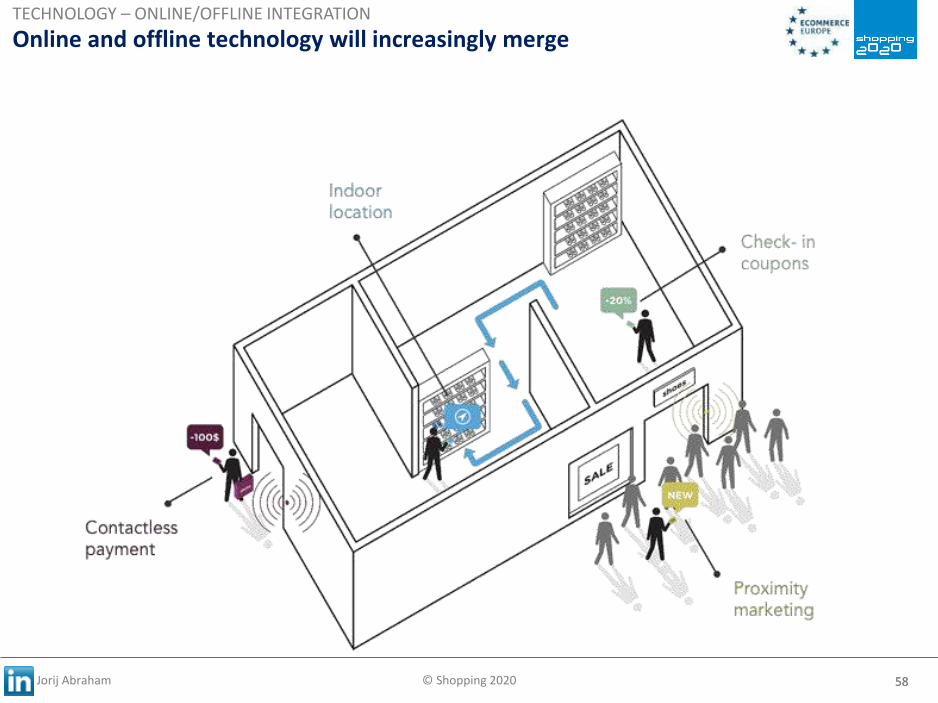

Online and offline technology will increasingly mergeTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 5656

The borders between online and offline are disappearingTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

Source: Todd Pollak, Industry Director Retail, Google

44% researches

online & buys

online

51% researches

online & buys

instore

17% visits a store

& buys online

32% researches

online, visits a

store & buys

online

© Shopping 2020Jorij Abraham 5757

Online shopping evokes functional associationsBricks & mortar more social attributes

http://blog.gfk.com/2014/11/what-next-for-the-shopping-mall-the-blended-shopping-experience/

TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 5858

Online and offline technology will increasingly mergeTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 6060

Mycom uses tablets to sell the ‘long tail’ and offer better serviceIt allowed the retail chain of 23 stores to acquire Dixons with 128 store

TECHNOLOGY – ONLINE/OFFLINE INTEGRATIE

© Shopping 2020Jorij Abraham 6464

Online & offline will increasingly merge to provide informationTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

Source: Estimote iBeacon (http://youtu.be/sUIqfjpInxY)

© Shopping 2020Jorij Abraham 6666

Starbucks is testing iBeacon to recognize customers when they enter a store, to serve them immediately and to enable them to pay automatically

TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

http://www.onemorething.nl/2014/01/vier-elementen-voor-een-betaalsysteem-van-apple-die-nu-al-in-je-iphone-zitten/

© Shopping 2020Jorij Abraham 6767

Rebecca Minkoff uses touch screens to facilitate the in store experienceBy not only showing off new products but also making the dressing room a positive experience

TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 7373

Online & offline will increasingly merge…for purchasesTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

Source: http://www.youtube.com/watch?v=oUD57MpHAE8

© Shopping 2020Jorij Abraham 7575

Bloomingdale offered a 3D body scanner in 70 stores for the perfect fitThe scanner failed. Women found it to confronting and jeans were offered only in 15 sizes

http://www.me-ality.com/fit-solutions

TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 8181

Audi uses digital media to get the showroom in the shopping streetTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

Source: http://www.audi.co.uk/audi-innovation/audi-city.html

© Shopping 2020Jorij Abraham 8383

Mini Concept Store proves you can create an experience without techTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 8484

Holograms will increastingly be part of the in store experience TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 8686

Holograms even get their own fan base like Hatsune MikuTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 8888

32%

31%

22%

10%

3% 15%

10%

33%

21%

9%

5%3%4%

Laptop Desktop Tablet

Smartphone Interactive/Internet television Glasses (e.g. Google Glasses)

Smart watches Other devices

Distribution of online purchase channels in 2020 (%)

Base: all experts who have given their vision on the total marketand have evaluated a specific segment (n= 268)

2013 2020

TECHNOLOGY – MEDIA/BODY INTEGRATION

The tablet and mobile phone displace the laptop/PC The importance of I-TV and Smartware (watches, glasses) is increasing

© Shopping 2020Jorij Abraham 8989

In India mobile is so popular traditional web shops are shut downMyntra draws as much as 80% of its traffic and 70% of sales from its mobile app

http://timesofindia.indiatimes.com/tech/tech-news/Myntra-to-shut-website-from-May-1/articleshow/46818792.cms

© Shopping 2020Jorij Abraham 9090

However in the US the desktop / mobile ratio is less favorableThe costs of supporting mobile does not yet delivery direct sales

Source: comScore, 2015 US Digital Future in Focus, March 26 2015

© Shopping 2020Jorij Abraham 9696

IKEA helps you try furniture before you buyTECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 9999

Everywhere where products are available, the consumer will make purchases: from the TV, on the street…

TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 100100

Voice control is still a challenge but doubling in usage every yearBut we are learning agents to also hear emotions and lip-read

TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

http://www.nu.nl/gadgets/3783453/spraakbesturing-wereld-verovert.html

0

1

2

3

4

5

6

7

8

9

2010 2011 2012 2013

# billion of voice commands

© Shopping 2020Jorij Abraham 101101

We may work with fingernail sized devices…TECHNOLOGY – ONLINE/OFFLINE INTEGRATION

© Shopping 2020Jorij Abraham 104104

Media are coming closer to our bodies; we will be online continuouslyTECHNOLOGY – MEDIA/BODY INTEGRATION

Source: https://vimeo.com/46304267

© Shopping 2020Jorij Abraham 106

© Shopping 2020Jorij Abraham 108108

In 2020, not every customer will come to the (web) shop…

1980

1990

2000

2010

2020

www.hongkiat.com/blog/30-futuristic-phones-we-wish-were-real/

TECHNOLOGY – MEDIA/BODY INTEGRATION

© Shopping 2020Jorij Abraham 109109

http://www.slideshare.net/vangeest/exponential

-organizations-h

© Shopping 2020Jorij Abraham 115115

Expectation is that in 2020 we will own 6,5 connected devices

Source: Cisco Internet Business Solutions Group, april 2011

TECHNOLOGY – MEDIA/BODY INTEGRATION

© Shopping 2020Jorij Abraham 116116

The Pyramid of TechnologyTechnology is moving toward becoming natural

http://www.nextnature.net/2014/08/pyramid-of-technology/

© Shopping 2020Jorij Abraham 117117

Source: Hapilabs.com

The product is becoming more and more digitalTECHNOLOGY – PRODUCT DIGITIZATION

© Shopping 2020Jorij Abraham 118118

Shoes coach you how to sport better

Source: Steven van Belleghem

TECHNOLOGY – PRODUCT DIGITIZATION

© Shopping 2020Jorij Abraham 119119

The diaper tells you when it needs to be changed

http://www.nst.com.my/latest/japan-sensor-will-let-diaper-say-baby-needs-changing-1.480875

TECHNOLOGY – PRODUCT DIGITIZATION

© Shopping 2020Jorij Abraham 120120

Create your own chair & work healthyTECHNOLOGY – PRODUCT DIGITIZATION

© Shopping 2020Jorij Abraham 123123

3D scanning & printing is changing the entire production chain

Source: http://www.3ders.org/articles/20120620-tool-less-production-of-moulds-using-3d-printing-technology.htmlhttp://www.youtube.com/watch?v=RPvxShlrm58&list=PLUWBnRobGU6gMcaXFRKwYa_F_OKILjA4L

TECHNOLOGY – 3D PRINTING

© Shopping 2020Jorij Abraham 125125

3D Printing can have an impact of $ 550 billion worldwide

http://www.mckinsey.com/insights/business_technology/disruptive_technologieshttp://www.mckinsey.com/insights/manufacturing/3-d_printing_takes_shape?cid=other-eml-nsl-mip-mck-oth-1402http://www.explainingthefuture.com/3dprinting.html

Less (local) stock

TECHNOLOGY – 3D PRINTING

Production of lighter& ‘impossible’ products

Quicker design & production process

Mass one-on-oneproduction

© Shopping 2020Jorij Abraham 126126

Even traditional retail chains like Hema have started offering 3D printingWhile sales is still minimal, this was also the case for photo printing. Now Hema market leader.

TECHNOLOGY – 3D PRINTING

© Shopping 2020Jorij Abraham 130130

Appie, from shopping list to primary online ordering toolTECHNOLOGY – BIG DATA

Albert Heijn prefills 80 to 90% of its mobile app shopping list for its customers

Bron: www.emerce.nl/nieuws/ahnl-maakt-zich-reeks-online-vernieuwingen

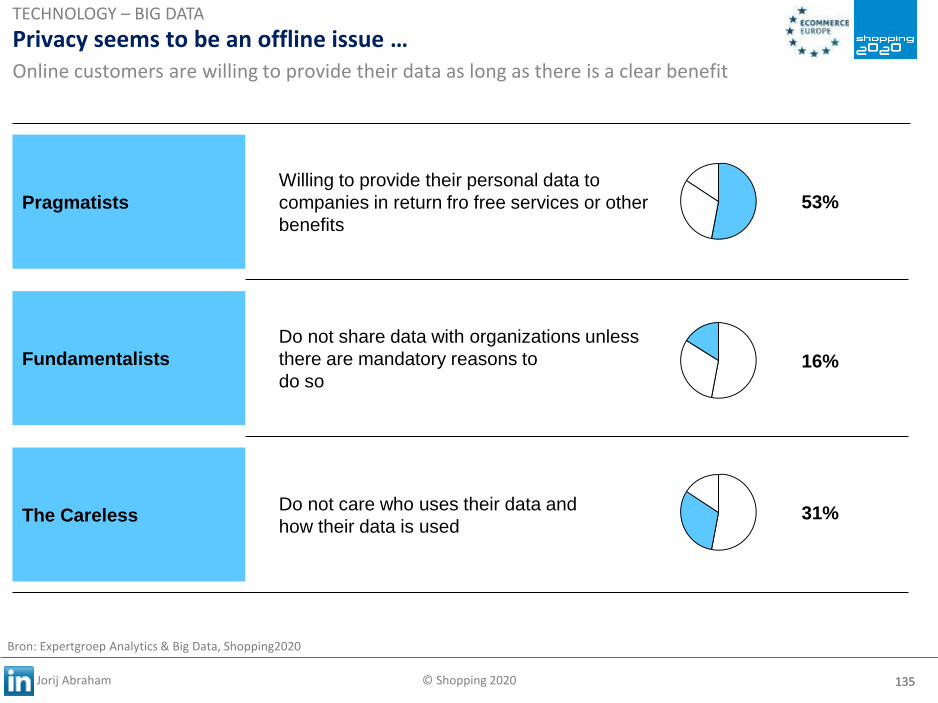

© Shopping 2020Jorij Abraham 135135

Privacy seems to be an offline issue …

Pragmatists

Willing to provide their personal data to

companies in return fro free services or other

benefits

Fundamentalists

Do not share data with organizations unless

there are mandatory reasons to

do so

The CarelessDo not care who uses their data and

how their data is used

53%

16%

31%

Online customers are willing to provide their data as long as there is a clear benefit

Bron: Expertgroep Analytics & Big Data, Shopping2020

TECHNOLOGY – BIG DATA

© Shopping 2020Jorij Abraham 136136

RadioShack is selling its customer data of 67 million customersRadioShack filled for bankruptcy and is trying to sell its (intellectual) assets of 1740 stores

TECHNOLOGY – BIG DATA

http://www.sltrib.com/home/2453366-155/radioshack-is-looking-to-sell-customer

© Shopping 2020Jorij Abraham 176

SUSTAINABILITY

© Shopping 2020Jorij Abraham 177177

Vacancy in 2020 is 10%, if the current trend continues

SUSTAINABILITY

The shopping street is changing, the high vacancy rate is becoming an increasingly larger problem

In the UK, the vacancy rate has already reached 15%

“Big chains won't return to high street because of rise of online shoppers”Mary Portas Review

09

5,5

10

6,0

11

6,3

12

7,5

2015

10,0

2020

5,0

2008

+5,9% p.a.

5,3

Vacant points of sale1, %

SOURCE: Locatus, Expert Reports “The New Shopping Street"

1 Extrapolated in 2015 and 2020 on the basis over average annual growth 2008-2012; vacancy is defined as a vacant building that is intended for sale. Buildings that used to be shops but are now used differently will not be included.

© Shopping 2020Jorij Abraham 178178

American shopping mall traffic declines with 50% from 2010 to 2013Due to over offering, a return to down town and rise of online shopping (6%)

© Shopping 2020Jorij Abraham 180180

Number of parcelsMillion

Value per deliveryEUR

Online retail turnover in the NetherlandsBillions of euros

Increasing parcel traffic requires new solutions

11,3

6,54,64,13,63,02,51,8

+12% p.a.1

+21% p.a.

77101

118123123140156155 -5% p.a.2

-5% p.a.

202020152012111009082007

575

250180

+18% p.a.

202020152013

1 Based on growth in accordance with the experts in the GfK Expert Report2 Decrease of 2007-2012 extrapolated 3 based on approx. 9-10 million households in 2020

SOURCE: GfK Expert Research; Expert Report "Cross-border (e-)Commerce“; parcelbox4u.com; PostNL

ROUGH ESTIMATE

~1.5 million parcels delivered per day ~60 small parcels per year per household3 in 2020 35% of current parcel traffic is air traffic at the

moment

X

SUSTAINABILITY

© Shopping 2020Jorij Abraham 189

MARKET CONCENTRATION & CROSS BORDER ECOMMERCE“Start with the customer and work backwards.“ Jeff Bezos, CEO Amazon

© Shopping 2020Jorij Abraham 190190

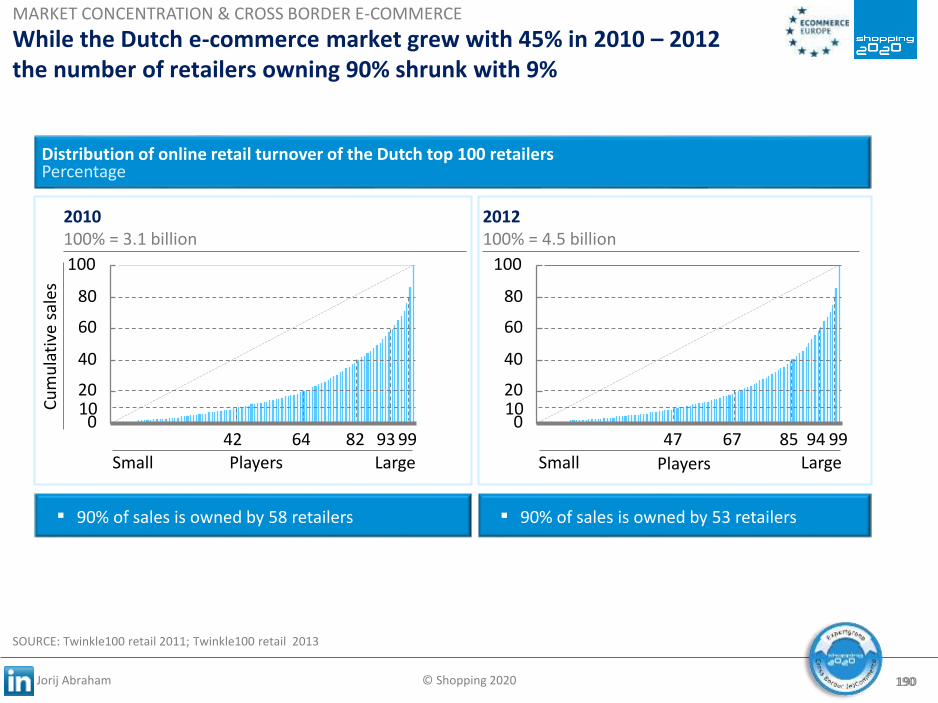

Distribution of online retail turnover of the Dutch top 100 retailersPercentage

While the Dutch e-commerce market grew with 45% in 2010 – 2012the number of retailers owning 90% shrunk with 9%

0

20

40

60

80

100

0

20

40

60

80

100

64 82 93 67 85 9499 99

▪ 90% of sales is owned by 58 retailers

SOURCE: Twinkle100 retail 2011; Twinkle100 retail 2013

10 10

42 47

2010100% = 3.1 billion

2012100% = 4.5 billion

Players Players

Cu

mu

lati

ve s

ales

▪ 90% of sales is owned by 53 retailers

Small Large Small Large

MARKET CONCENTRATION & CROSS BORDER E-COMMERCE

© Shopping 2020Jorij Abraham 191191

Big is becoming beautifull (again). One Winner Takes All.

Books

Insurance

Fashion

Hotels

Fast Food

MARKET CONCENTRATION & CROSS BORDER E-COMMERCE

© Shopping 2020Jorij Abraham 196196

The number of European consumers that buy online with foreign players increases quickly

SOURCE: EC (2013) Consumer Attitudes Towards Cross Border Trade and Consumer Protection

15

10

78

7

+21% p.y.

86

444

+19% p.y.

20122011201020092008

Consumers that bought products online outside of their own country in the last 12

Within the EU

Outside of the EU

Percentage

MARKET CONCENTRATION & CROSS BORDER E-COMMERCE

© Shopping 2020Jorij Abraham 200200

Consumers are buying increasingly more cross border.Larger countries are leading the way.

SOURCE: Civic Consulting (2011); “Consumer market study on the functioning of eCommerce” in EC (2012) Bringing eCommerce benefits to customers

In which countries did you buy products/services online (%, 2011)?

Austria

Belgium

Denmark

Finland

France

Germany

Italy

Luxembourg

Netherlands

Portugal

Spain

Sweden

U.K.

Total

13

20

48

40

29

20

29

19

21

41

28

34

…

24

…

2

3

4

1

31

4

4

3

1

2

3

2

8

4

3

2

3

3

5

…

5

3

4

8

3

6

4

Italy

4

38

8

7

3

11

4

5

…

3

2

3

6

6

Nether-lands

2

0

1

1

1

3

2

0

2

0

0

2

3

2

Poland

1

2

2

2

5

4

7

2

4

21

…

3

8

5

Spain

1

1

22

22

1

2

2

1

1

1

1

…

2

2

SwedenUnited KingdomAustria

2

…

1

2

15

4

4

19

15

1

5

2

3

5

Belgium

0

0

…

5

2

4

2

1

2

1

2

15

2

2

Denmark

90

26

32

38

41

…

36

78

43

18

22

32

21

27

GermanyFrance

5

42

5

5

…

9

26

43

11

16

27

9

17

14

Country of origin

Country where products/services were purchased

MARKET CONCENTRATION & CROSS BORDER E-COMMERCE

Percentage > 10%

© Shopping 2020Jorij Abraham 213

COMPETITION“Start with the customer and work backwards.“ Jeff Bezos, CEO Amazon

© Shopping 2020Jorij Abraham 214214

The global e-commerce market is exploding, especially in AsiaCOMPETITION

© Shopping 2020Jorij Abraham 217217

The American are coming… and so are the ChineseCOMPETITION

© Shopping 2020Jorij Abraham 221221

The top 10 webshops of GermanyTurnover in millions €

Bron: Statista, http://twinklemagazine.nl/nieuws/2014/09/amazon-tekent-voor-30-procent-omzet-duitse-top-100/index.xml

COMPETITION

© Shopping 2020Jorij Abraham 224224

Amazon is still leading the way and setting the standardWith selection (the everything store), lowest prices, best convenience & great confidence

COMPETITION

© Shopping 2020Jorij Abraham 239239

Ebay offers (near-)instant commerce; ordering & delivering in 60 minutesCOMPETITION

© Shopping 2020Jorij Abraham 240240

Google is migrating from “search” to “find” to “buy” platformGoogle is slowly expanding its vertical searches for hotels, flights, goods, insurances

COMPETITION

© Shopping 2020Jorij Abraham 245245

Alibaba sold for $ 9.3 billion on Singles Day (11th of November)A rise of 60% compared to 2013

COMPETITION

© Shopping 2020Jorij Abraham 247247

Will market places rule the world in 2020?The “everything store strategy” results in conversion ratio’s up to 20%

# of countries active Growth 2013

13 22%

1*(just bought US 11Main)

50%

13 45%

The 3rd party strategy is a cash cow; as sales growth their costs remain the same

Market share

2 – 20%

55 – 60%

20 – 30%

* Although Alibaba offers an international site it is not focused on a specifica market

COMPETITION

1 200%25%

© Shopping 2020Jorij Abraham 252

SUPPLY CHAIN & DELIVERY

© Shopping 2020Jorij Abraham 253253

Supply chain and delivery will become increasingly complex

(R)Etail /

Reseller

Product brandEur. DC / Reg. DC

Retail Distribution center

Retail chain stores

Specialist store

Manufacturer

Wholesale Store replenishment

Between stores

Consignment/VMI

Cross dock

Concession / shop in shop

Private

label

Wholesale

(R)Etail /

Reseller

Product brandEur. DC / Reg. DC

Retail Distribution center

Retail chain stores

Specialist store

Manufacturer

Wholesale Store replenishment

Between stores

Consignment/VMI

Cross dock

Concession / shop in shop

Private

label

Home delivery from online retailer

Home delivery from small retailer

Wholesale

Online store replenishment

(R)Etail /

Reseller

Product brandEur. DC / Reg. DC

Retail Distribution center

Retail chain stores

Specialist store

Manufacturer

Wholesale Store replenishment

Between stores

Consignment/VMI

Cross dock

Concession / shop in shop

Private

label

Home delivery from online retailer

Home delivery from small retailer

Pick up points

Pick up in store

From store to door/pick in store

Pick up at pick up point Home delivery from

small retailer

Wholesale

Online store replenishment

(R)Etail /

Reseller

Product brandEur. DC / Reg. DC

Retail Distribution center

Retail chain stores

Specialist store

Manufacturer

Wholesale Store replenishment

Between stores

Consignment/VMI

Cross dock

Concession / shop in shop

Private

label

Home delivery from online retailer

Home delivery from small retailer

Pick up points

Pick up in store

From store to door/pick in store

Pick up at pick up point Home delivery from

small retailer

Concession Pick up at pick up point Home delivery from market place DC

C2C

Wholesale

Online store replenishment

Market place

E-fullfilmentcenter (r)etailer(s)

C2C

Brand direct

(R)Etail /

Reseller

Market place

Product brandEur. DC / Reg. DC

Retail Distribution center

Retail chain stores

Pick up points

Mono brand stores

Specialist store

Home

E-fullfilmentcenter (r)etailer(s)

E-fullfilmentcenter product brand(s)

Market place DC

Manufacturer

Manufacturer

Wholesale

Consignment/VMI

Cross dock

Concession

Pick up in store

Store replenishment

Online store replenishment

Pick up in store

Pick up at pick up point

Concession / shop in shop

Online store replenishment

Home delivery from online retailer

Direct delivery from product brand

From store to door/pick in store

From store to door/pick in store

Between stores

Store replenishment

Pick up at pick up point

Pick up at pick up point Home delivery from market place DC

Home delivery from small retailer

Wholesale

Private

label

Brand direct

(R)Etail /

Reseller

Market place

3D printing

Product brandEur. DC / Reg. DC

Retail Distribution center

Retail chain stores

Pick up points

Mono brand stores

Specialist store

Home

E-fullfilmentcenter (r)etailer(s)

E-fullfilmentcenter product brand(s)

Market place DC

Manufacturer

Manufacturer

Wholesale

Consignment/VMI

Cross dock

Concession

Pick up in store

Store replenishment

Online store replenishment

Pick up in store

Pick up at pick up point

Concession / shop in shop

Online store replenishment

Home delivery from online retailer

Direct delivery from product brand

From store to door/pick in store

From store to door/pick in store

Between stores

Store replenishment

Pick up at pick up point

Pick up at pick up point

Print shop

3d printing at home3d printing at print shop

Home delivery from market place DC

Home delivery from small retailer

Wholesale

C2C

Private

label

SUPPLY CHAIN & DELIVERY

Source: Shopping2020 Expert Group Purchasing & Supply Chain

© Shopping 2020Jorij Abraham 254254

The new norm: delivery for free where and when the consumer wantsHow do you charge delivery costs now and what is your expectation for the future?

12%

51%11%

26%

Bezorgkosten worden als apart item doorbelast in de bestelling.

Bezorging wordt geheel gratis aangeboden. De bezorgkosten zijn versleuteld in deverkoopprijs van het product.Een deel van de bezorgkosten wordt in rekening gebracht, een deel versleuteld in deverkoopprijs van het product.Bezorgkosten worden als apart item doorbelast, tenzij een minimum orderbedrag wordtbehaald waarna de bezorgkosten vervallen

21%

22%

11%

46%2014(n= 123)

(n= 113)2020

Source: Dutch GfK Shopping2020 Expert Study Nov. 2014 Vraag: Hoe verrekent uw bedrijf momenteel de bezorgkosten en hoe verwacht u dat dit in 2020 gebeurt? ((excl. Do not know)

SUPPLY CHAIN & DELIVERY

© Shopping 2020Jorij Abraham 255255

Amazon and other giants set the standard with next & same day deliverySUPPLY CHAIN & DELIVERY

© Shopping 2020Jorij Abraham 256256

Inventory management & transparancy and shorter delivery times towards consumers will have the biggest impact on the supply chain

Basis: alle respondenten uit bedrijven met online en/of

offline winkels (n= 164)

Source: Dutch GfK Shopping2020 Expert Study Nov. 2014. Question: to what extent is your business impacted by the following developments.

17%

37%

41%

33%

14%

13%

26%

26%

31%

20%

26%

24%

23%

22%

27%

44%

13%

10%

15%

40%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Alle voorraad beschikbaar en transparant voor alle kanalen(online en offline)

Off shore productie kosten stijgen

Off shore productie leadtimes belemmeren flexibiliteit

Geen standaardisatie in supply chains waardoor track &trace moeilijk is

Levertijden naar online klanten moet steeds korter

Geen invloed Enigszins invloed Redelijk wat invloed Veel invloed

SUPPLY CHAIN & DELIVERY

© Shopping 2020Jorij Abraham 257257

Retailers will prefer to work with logistical intermediairies offering all possible delivery models

Basis: alle respondenten uit bedrijven met online

winkels die fysieke producten verkopen (n= 128)

20%

10%

15%

19%

17%

11%

26%

25%

21%

20%

37%

33%

15%

12%

21%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Fulfilment netwerken van retailplatformen met eigenvervoersoplossingen

Samenwerken met logistieke bemiddelaars die in opdrachtvan consumenten het vervoer regelen met koeriers

Samenwerken met logistieke bemiddelaars die iedereen(consumenten, taxi`s, koeriers) kunnen inschakelen om het

vervoer af te handelen voor de ontvanger

Zeer onwaarschijnlijk Onwaarschijnlijk Neutraal Waarschijnlijk Zeer waarschijnlijk

SUPPLY CHAIN & DELIVERY

Source: Dutch GfK Shopping2020 Expert Study Nov. 2014. Question: What is the (un)likelyhood your company will work with the following delivery models in 2020 (excl. Do not know)

© Shopping 2020Jorij Abraham 258258

DHL is investing significantly in pick-up stationsIn Germany already 2.750 pick-up stations have been installed by DHL

SUPPLY CHAIN & DELIVERY

Source: Shopping2020 Expert Group Purchasing & Supply Chain

© Shopping 2020Jorij Abraham 259259

Deliver is becoming ubiquitosThuisbezorgd.nl already delivers 1 million orders each month. Volvo offers car delivery.

SUPPLY CHAIN & DELIVERY

© Shopping 2020Jorij Abraham 260260

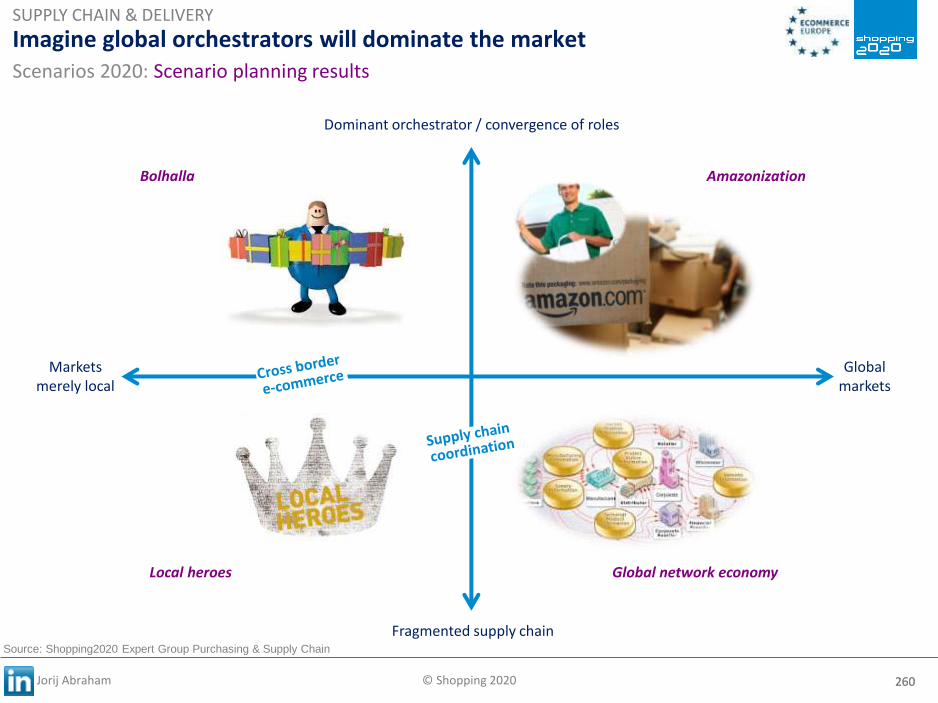

Imagine global orchestrators will dominate the market

Global markets

Markets merely local

Dominant orchestrator / convergence of roles

Fragmented supply chain

Bolhalla

Local heroes

Amazonization

Global network economy

Scenarios 2020: Scenario planning results

SUPPLY CHAIN & DELIVERY

Source: Shopping2020 Expert Group Purchasing & Supply Chain

© Shopping 2020Jorij Abraham 261261

1 hour delivery standard

Delivery times long

3D printing explodes

3D Printing remains niche

Printing at producer

Long tail / Make-To-Order at producer

Print in store/at home

Long tail / Assemble in store

Imagine 3D printing and 1 hour delivery become the new standardScenarios 2020: Scenario planning results

SUPPLY CHAIN & DELIVERY

Source: Shopping2020 Expert Group Purchasing & Supply Chain

© Shopping 2020Jorij Abraham 262262

Imagine 1 hour delivery in a world with very few storesScenarios 2020: Scenario planning results

1 hour delivery standard

Delivery times long

Number of stores decreases significantly

Number of stores stabilizes

Drop shipments

Showrooms full of experience

City hubs

Pick (up) in store

SUPPLY CHAIN & DELIVERY

Source: Shopping2020 Expert Group Purchasing & Supply Chain

© Shopping 2020Jorij Abraham 320

WHAT’S NEXT?“It’s not the crisis, it’s not the web, it’s the consumer stupid.” Ed Peerenbolte

© Shopping 2020Jorij Abraham 321321

In the next 7 years consumers will…

52

36

17

2020 – consumer expectation

2020 – expert opinion

2012

Buy up to 50%+ online

10

25-28

35-40

Market in billion €xx

Will share more products

Buy instantly & less in the (web)shop Buy more from international marketplaces

THE KEY FINDINGS

© Shopping 2020Jorij Abraham 330330

Will Europe be following Austria’s footsteps?

85% of the e-commerce turnover in Austria is bought from (r)etailers of which

the head office is in another country.

WHAT'S NEXT

© Shopping 2020Jorij Abraham 332332

What can we learn from the Scary Five?

Ultimate User Focus

New Business Models Speed!!!

WHAT'S NEXT

Think Big! Go X-Border

© Shopping 2020Jorij Abraham 421421

Shopping2020 transformed from research to permanent programWHAT'S NEXT

© Shopping 2020Jorij Abraham 426426

In 2015 Shopping2020 is transforming from program to platformHow can we solve a specific challenge in order to prepare ourselves fro the future?

Common vision(2013)

Conversion attribution

Creating social

awareness

The Last Mile

Shared Roadmap(2014)

2017

2018

2019

WHAT'S NEXT

© Shopping 2020Jorij Abraham 428428

Are you a retail, finance or travel organization? Join us in 2015!

Just sent us an email.

RSVP [email protected]

© Shopping 2020Jorij Abraham 431431

Questions? Want to participate? Please contact me!

Jorij Abraham

Director Research & Advice

M: +31 6 52 84 00 39