presentation hsbc u.s. road show

TRANSCRIPT

Meeting with Investors Meeting with Investors

May 08May 08

2

Forward-looking Statements

This presentation contains forward-looking statements. These statements do

not represent historical fact, but rather reflect the beliefs and expectations

of Braskem’s management. The words “anticipate”, “wish”, “expect”,

“estimate”, “intend”, “forecast”, “plan”, “predict”, “project”, “target” and

similar words are intended to identify these statements. Although Braskem

believes that the expectations and assumptions reflected in these forward-

looking statements are reasonable and based on information currently

available to management, Braskem cannot guarantee future results or events.

The forward-looking statements included in this presentation are valid only

on the date on which they are made (March 31, 2008), and the Company does

not undertake any obligation to update them in light of new information or

future developments.

Braskem is not responsible for any transaction or investment decision taken

based on the information in this presentation.

3

Agenda

� Overview

� Key Differentiators

� Key Financial & Operational Figures

� Upside Drivers

3

4

Agenda

� Overview

� Key Differentiators

� Key Financial & Operational Figures

� Upside Drivers

4

5

• #2 Ebitda Margin in the Americas (1Q08 LTM)

Braskem # 1 Petrochemical Company in Latin America

• #1 Petrochemical Company in LATAM

Resins Production Capacity (kton)

5

0

1,000

2,000

3,000

CPS* Solvay EcopetrolMexichemBraskem

3,440

1,515

682521 438

692

Dow

Source: Braskem/ CMAI

1Q08 LTM FINANCIALS

• Net Revenue: US$ 10.2 bi

• EBITDA: US$ 1.6 Bi

• Assets: US$ 12.1 bi

• EV: US$ 8.0 bi

*CPS: Companhia Petroquímica do Sudeste – 60% of Unipar and 40% of Petrobras

0%

5%

10%

15%

20%

Mexichem Nova Chemical

Unipar

15%

DOW Westlake Ultrapar

Median

Braskem

3,500

6

Strong and consistent growth via Organic and Acquisitions Routes

Source: Braskem

1994 1996 1998 2000 2002 2004 2005 2006 2007

Organic

Acquisitions

1,000

2,000

3,000

4,000

5,000

US$ 1,357 MM

US$ 2,375 MM

US$ 9,712 MM

1,2281,234

1,528 1,734

3,045 3,225

3,621

5,551

• Revenues ► CAGR (’94-’07) – 16.3%

• Production capacity ► CAGR (’94-’07) – 12.3%

New PP Plant

start-up

New PE Plant

start-up

Creation ofBraskem

PP DBNEthylene DBN

PVC DBN

PolitenoAcquisition

Copesul / IPQAcquisition

3,145

KtonRevenues

6

7

• # 3 Resins Producer in Americas - petrochemical “pure-play”(kton)

7

0%

5%

10%

15%

20%

Mexichem Solvay Westlake DowUnipar

18%

LG Ultrapar Nova Chemical

Median

Braskem

• #2 Global Ebitda Margin - petrochemical “pure-play” (03-07 average)

Source:Braskem / CMAI March 2008

PVC

PEPP

FormosaDow

615

6464

5,774

5,0955,095

LyondellBasell Braskem

3,440

ShintechIneos

2,8132,813

1,833

4,646

1,8151,815

1,110

515515

978978

761

1,2101,210

2,949

926926

2,1612,040

730730

1,515

CPS

3rd 7th

7851,235

Large Scale combined with superior profitability

8

AgendaAgenda

� Overview

� Key Differentiators

� Key Financial & operational Figures

� Upside Drivers

8

99

Braskem has most of its operations in the leading economy in LATAM…

• Brazil: 1/3 of LATAM GDP • LATAM GDP (US$ billion) *

Brazil: 1,838

México: 1,353

Argentina: 524

Venezuela: 335

Colombia: 320

Others: 1,070

Total: 5,440

Colombia 6%

Mexico

25%

Argentina

10%

Venezuela 6%

Brazil

33%

Others

20%

Source: The Economist (Mar2008)

(*) PPP – Purchasing Power Parity

10

…and is exposed to a dynamic market with strong growth rates…

• Domestic demand for resins

Source: Abiquim – domestic sales + imports

PEPPPVC

2,880

3,435 3,3773,694

2001 2004 2005 2006

4,048

2007

1,695

990

692

1,833

1,114

1,964

1,228

856

6.0%CAGR

10%

9%

749

• USA Demand for resins

(Kton)

23,276

25,90424,749

25,020

2001 2004 2005 2006

24,306

2007

6,350

6,081

6,287

12,826

6,142

12,601

5,563

0.7%CAGR

-3%1%

5,907

12,318

Source: NAD - CMAI

1111

…with high level of consolidation

• 2 Top producers share

• High Demand Growth and Elasticity

01-07 CAGR Resin Growth 01-07 GDP Elasticity

Brazil: 6.0% Brazil: 2x

USA: 0.7%

• Number of Producers

BRAZIL USA

Source: Braskem / CMAI

PEPP PVC

1212

9

42 2

PP PVCPE

100% 100%93%

30%51%42%

12

% Capacity Share

Region Company PE PP PVC

South America Braskem 46% 44% 32%

Unipar 23% 31% 0%

North America DOW 22% 4% 1%

NOVA 7% 0% 0%

Mexichem 0% 0% 4%

Westlake 6% 0% 8%

Northeast Asia LG Chemical 5% 2% 6%

Western Europe Solvay 0% 0% 15%

Braskem has unmatched regional capacity share in core products…

12

Source: Braskem / CMAI

131313

…with Growing & Sustained Leadership in Brazil…

Source: Braskem/Abiquim Dec 07

• PP Market Share • PVC Market Share

• PE Market Share

40% 38%49%

51% 55% 37%

9% 7% 14%

42% 41%

48% 50%

10% 9%

0%

20%

40%

60%

80%

100%

2001 2003 2005 2006 2007

BRASKEM PEER IMPORTS

57%48% 54%

29%32% 27%

14% 20% 19%

52% 53%

28% 30%

20% 17%

0%

20%

40%

60%

80%

100%

2001 2003 2005 2006 2007

BRASKEM PEER IMPORTS

29% 31%

52%

55% 50%

32%

16% 19% 16%

33% 37%

53% 46%

15% 17%

0%

20%

40%

60%

80%

100%

2001 2003 2005 2006 2007

BRASKEM PEER IMPORTS

141414

Source: Braskem / IBGE

…and Diversified customer basis in the fast-growing Brazilian market

% of Resin Sales% of Resin Sales

FOOD PACKAGING

CONSUMERGOODS

CIVIL CONSTRUCTION

RETAIL

AGRICULTURE

COSMETICS ANDPHARMACEUTICALS

CLEANINGMATERIAL

INFRASTRUCTURE

ELECTRIC AND ELECTRONIC

AUTOMOTIVE

OTHERS

17%

17%

23%

10%3%

2%4%

5%

3%

8%

8%

INDUSTRIALINDUSTRIAL + 6%

Growth by Sector in 2007Growth by Sector in 2007

CONSTRUCTION CONSTRUCTION

AUTOMOBILESAUTOMOBILES

HOME APPLIANCESHOME APPLIANCES

FERTILIZERSFERTILIZERS

CONSUMER GOODSCONSUMER GOODS

PLASTIC PACKAGINGPLASTIC PACKAGING + 4%

+ 5%

+ 5%

+ 5%

+ 15%

+6%

151515

Innovation and Technology as key value drivers

• Over US$ 160 million in R&D assets

• 200 researchers

• 8 pilot plants

• 187 patents filed

• Focus on nanotechnology and intelligent packaging

• 18% of resins sales derive from products launched in the last three years

• Partnership with universities and R&D centers in Brazil and abroad

Source: Braskem

161616

Spreads on Asian pricesSpreads on Asian pricesPVC: Braskem premium over internationalPVC: Braskem premium over international

PP: Braskem Premium over InternationalPP: Braskem Premium over InternationalPE: Braskem Premium over InternationalPE: Braskem Premium over International

Strong pricing power Over 30% spread on international prices

%%

%%

Source: CMAI / Braskem

PPPP

PEPE + 34%

+ 33%

PVCPVC + 42%

%%

%%

27%

34%

jan/

05m

ar/0

5m

ai/0

5

jul/0

5

set/0

5no

v/05

jan/

06m

ar/0

6m

ai/0

6

jul/0

6

set/0

6no

v/06

jan/

07m

ar/0

7m

ai/0

7

jul/0

7

set/0

7no

v/07

jan/

08m

ar/0

8

Spread PEAD Braskem / International US$

Average 27%

42%33%

jan/

05m

ar/0

5m

ai/0

5

jul/0

5

set/0

5no

v/05

jan/

06m

ar/0

6m

ai/0

6

jul/0

6

set/0

6no

v/06

jan/

07m

ar/0

7m

ai/0

7

jul/0

7

set/0

7no

v/07

jan/

08m

ar/0

8

Spread PP Braskem / International US$

Average 30%

42%

52%

jan/

05m

ar/0

5m

ai/0

5

jul/0

5

set/0

5no

v/05

jan/

06m

ar/0

6m

ai/0

6

jul/0

6

set/0

6no

v/06

jan/

07m

ar/0

7m

ai/0

7

jul/0

7

set/0

7no

v/07

jan/

08m

ar/0

8

Spread PVC Braskem / International US$

Average 42%

17

AgendaAgenda

� Overview

� Key Differentiators

� Key Financial & Operational Figures

� Upside Drivers

17

18

Production growth with higher operating reliability

PE PP PVC

1Q084Q07

ETHYLENE

93%

95%

Source: Braskem

Resin ProductionResin Production KtonKton

1Q07

86%

96%

Capacity Utilization Capacity Utilization %%

ALL-TIME RECORDS

� Production in the last 12 months of 2,827 Kton

� Quarterly PVC production of 130 Kton in 1Q08

1Q084Q071Q07 1Q084Q071Q07 1Q084Q071Q07

88% 89%91%

96% 96%96%94%

104%

92%

702

1Q084Q07

704

LTM1Q08

LTM 1Q07

2,786 2,827

+1%

700

1Q07

19

Leadership position in robust domestic market: Demand +10%

Source: Braskem / Abiquim

Domestic Sales 1Q08 vs. 1Q07Domestic Sales 1Q08 vs. 1Q07 %% Resin Market Share 1Q08Resin Market Share 1Q08

+13%

+ 5 %+7%+ 6%

+10%

PVCPPResin

BraskemPE

Brazilian market*

Other

Imports

49%49%

22%

29%

*Domestic sales + Imports

20

648

4Q07 1Q08PricesFixed Costs/ SG&A

Volume Foreign Exchange

Source: Braskem

(32)

FX impacton costs

FX impacton revenue

Raw Materials

(263)

188

(136)

Other

Evolution of EBITDA Commercial strategy and reduction in fixed costs minimize impacts from higher Naphtha prices

Evolution of EBITDA Commercial strategy and reduction in fixed costs minimize impacts from higher Naphtha prices

583

83

(115)

11219

(89)

R$ million

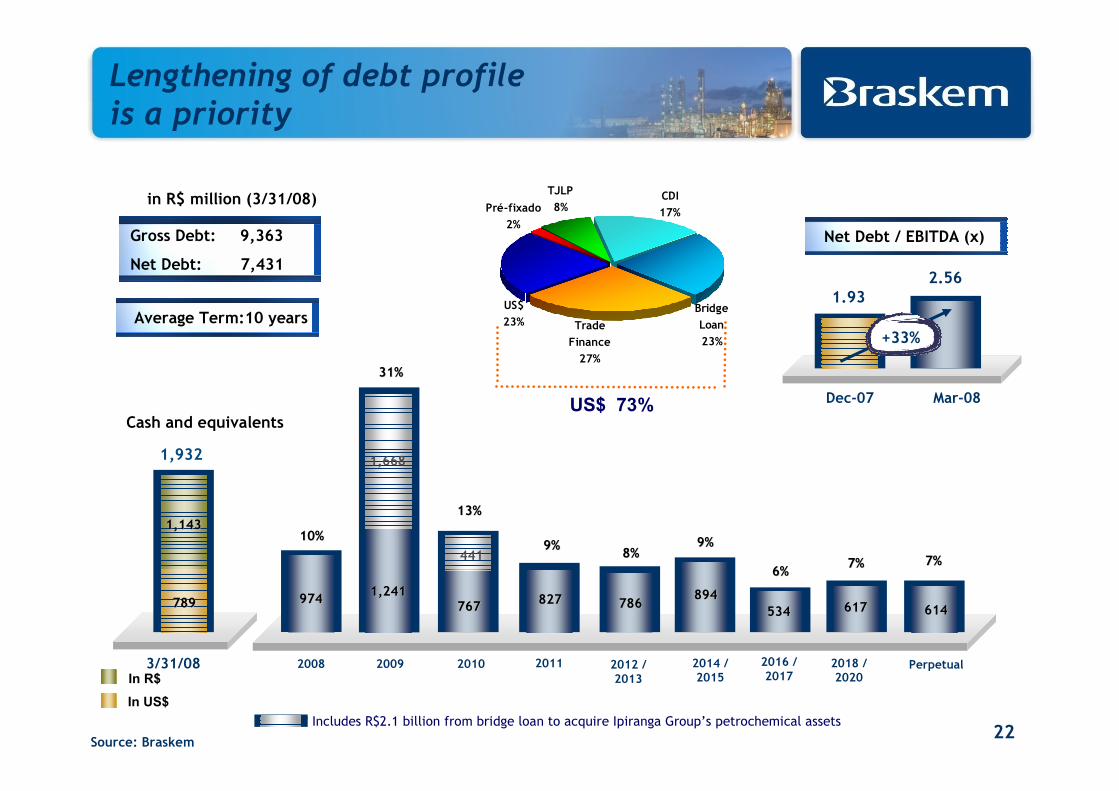

21

Key Financial Figures

R$ million

Source: Braskem * Pro Forma Figures

21

1Q08 (A) 4Q07 (B) 1Q07*(C)

Change %

(A)/(B)

Change %

(A)/(C)

Sales 4,410 4,809 4,424 (8) (0)

EBITDA 583 648 853 (10) (32)

Margin 13.2% 13.5% 19.3% -0.3 p.p. -6.1 p.p.

Net Income before Minority 120 25 275 379 (56)

Minority Interest (37) 2 (148) - (75)

Net Income 83 27 127 204 (35)

ST+LT Debt 9,363 8,382 8,948 12 5

Cash (1,932) (2,259) (2,090) (14) (8)

Net Debt 7,431 6,123 6,859 21 8

Net Debt/EBITDA 2.56 1.93 2.28 33 12

22

2016 /2017

Source: Braskem

Lengthening of debt profileis a priority

in R$ million (3/31/08)

3/31/08

1,932

Gross Debt: 9,363

Net Debt: 7,431

2008

In US$

In R$

Cash and equivalents

2009 2010 2011 2012 /2013

2014 /2015

2018 /2020

Perpetual

13%13%

9%9%8%8%

6%6%7%7% 7%7%

US$ 73%

* Includes R$2.1 billion from bridge loan to acquire Ipiranga Group’s petrochemical assets

9%9%

Average Term:10 years

31%31%

974974

10%10%

1,2411,241

1,668

767767 827827 786786894894

534534 617617 614614

1,1431,143

789789

441

2.56

Dec-07 Mar-08

1.93

+33%

Net Debt / EBITDA (x)

Pré-fixado

2%

Bridge

Loan

23%

US$

23% Trade

Finance

27%

CDI

17%

TJLP

8%

23

AgendaAgenda

� Overview

� Braskem Key Differentiators

� Key Financial Figures

� Upside Drivers

23

2424

� R$ 200 million on annual and recurring basis in the EBITDA

24

NPV of US$ 1.1 billion in total synergies from Ipiranga acquisition

R$ million

200

TotalSynergies

69

Commercial Financial

9

Industrial

73

SupplyLogistics

25

Others

Source: Braskem

1410

Synergies in 2008 (R$ 108 million)

Total Synergies

25

Accelerated Synergies in 1Q08:R$ 136 million in annual and recurring gains

R$ million

Source: Braskem

Commercial

Industrial

Supply

Logistics

Synergies 1Q08

16

42

7

10

2008

39

29

16

13

Financial ex-Ebitda 59

Financial 2 7

Others 1 4

Actual Goal

Annualized

Impact on EBITDA 77 108

80

262626

�R$ 100 million estimated annual & recurring gains:

�R$ 30 million in production costs

�R$ 70 million in general and administrative expenses

�R$ 67 million already captured in 1Q08 on annualized and recurring basis

�Renegotiation of contracts: insurance, IT and telecom

�Supply chain integration: reduction in inventory levels of maintenance and production items

�Optimization of the organizational structure

Additional gains of R$ 100 million with Fixed Costs Reduction Program

272727

Strategic alignment with Petrobras

� Superior Industry Structure in Brazil: Consolidation around 2 large competitors (Braskem & CPS).

� New Geographic growth opportunities: linked to Petrobras’extensive footprint in Brazil and abroad

� Synergies:

� potential for operational integration with Petrobras refineries

� Innovation & Technology: partnership with Petrobras Research Center

� High corporate governance standards: New shareholders agreement

28

Ethylene global supply & demand balanceHigh capacity utilization rate in 2008

Source: CMAI, March of 2008

Supply Demand Utilization Rate

131140

149 154

119124

131 136

88%88%88%88%89%89%

91%91%

0

20

40

60

80

100

120

140

160

180

2008 2009 2010 2011

75

80

85

90

95

100

Utilization Rate %MM ton

160

142

89%89%

2012

75

80

85

90

95

100

1 2 3 4 5

28

29

Global supply & demandHigh Ethylene Utilization Rate in South America

EthyleneMM tons

159

Supply2012

9

Saudi Arabia Others

9

Supply2007

126

IranChina

8

Qatar

43

EHYTLENE UTILIZATION RATE (EHYTLENE UTILIZATION RATE (’’0707--’’12)12)

WORLD WORLD ≥≥≥≥≥≥≥≥ 88%88%

SOUTH AMERICA SOUTH AMERICA ≥≥≥≥≥≥≥≥ 92%92%

NORTH AMERICA NORTH AMERICA ≥≥≥≥≥≥≥≥ 85%85%

29

Source: CMAI

30

Significant resins production capacity increase…

Source: Braskem

Braskem Capacity Additions (2008-12)

* JV with Pequiven (49%) and Sojitz (2%)30

Product Capacity Investment Advantage Start-up(K ton) (US$ MM)

PP Paulínia 350 350 Diversification - Refinery Gas 2008

Green PE 200 NA Ethanol – 100% Renewable 2010

PP Venezuela* 450 900 Propane at competitive cost 2010

PVC Alagoas 200 350 Leadership and innovation 2010

PE Venezuela* 1,100 2,600 Ethane at competitive cost 2012

PP Bahia 300 NA Strengthen Market leadership 2012

Total 2,600

NA: Not Available

31

…Resulting in even larger scale and increased competitiveness

NaphthaFeedstock from Refinery

Ethanol

Camaçari - BA

Triunfo - RS

Paulínia - SP

Venezuela

9%9%

57%57%34%34%32%32% 55%55%

4%4%9%9%

Natural GasPolyethylene Polypropylene PVC

2008 2012 FYE

4.9 million

1,815

1,110

515515

3.4million

715

1,635

2,565

+43%

� Larger scale � Increased Competitiveness

31

Source: Braskem

32

PP Paulínia: Proven capacity in project management

� Start up in April 2008

� Spheripol technology

� Global scale: 350 Kton/year

� Located in the largest consumer market in Latin America

� Feedstock: Propylene from refinery

� Investments of R$ 700 million

333333

Braskem: High upside potential

Commitment to SustainabilityCommitment to Sustainability

� Dominance in the domestic market with superior profitability

� Exposure to the fast-growing domestic market

� NPV of US$ 1.4 billion derived from synergies and reduced fixed

costs

� Growth projects with increased profitability and high ROCE

� Proven expertise to implement greenfield projects

� Strategic alignment with Petrobras

� Innovation and Technology as key value drivers: green polymer

� Experienced management team focused on value creation

Visit our website: Visit our website: www.braskem.com.br/riwww.braskem.com.br/ri

Meeting with Investors Meeting with Investors

May 08May 08