presents drafting the world’s greatest special needs trust · presents drafting the world’s...

TRANSCRIPT

3/22/17

1

Presents

Drafting the World’s GreatestSpecial Needs Trust

With

Michele Fuller, Kevin Urbatsch, Ray Falcon,Nancy Chudacoff, Travis Finchum, and Robert Mascali

Today’s Program

• Introduction

• Third Party SNT provisions

• (d)(4)(A) SNT provisions

• Provisions common to both types of SNTs

• Questions

ASNP Program Materials

• Agenda

• ASNP’s “Drafting Guide for Drafting the World’s Best Special Needs Trust”

• David Lillesand’s Annotated one-page (d)(4)(A) SNT

• Article: Professor Jeffrey Pennell’s Deconstructing the SNT

• Draft Third Party SNT

• Draft Self-Settled (d)(4)(A) SNT

• ASNP Brochure – Memo of Intent

3/22/17

2

Types of Special Needs Trusts

Third-Party • Using Assets of Others

First Party or Self-Settled• (d)(4)(A) (a/k/a Payback SNT)

• (d)(4)(B) (Miller Trust)

• (d)(4)(C) (a/k/a Pooled Trust)

Drafting Depends on Type of SNT

First Party SNT• Federal specific legal requirements

• State specific legal requirements

• Don’t be creative

Third Party SNT• Less legal requirements = More flexibility and creativity

• Exceptions• “Sole benefit” if want parent to qualify for long term Medicaid

• Setting up SNT for spouse

Third-Party Special Needs Trust

For SSI purposes, the Social Security Administration defines in the POMS SI 01120.200(B)(17) a third party trust as

"a trust established by someone other than the beneficiary as grantor.”

It defines a grantor in the POMS SI 01120.200(B)(2) as

"the individual who provides the trust principal (or corpus).”

3/22/17

3

Third Party SNT Requirements

SSI regulations impose two requirements for third party SNTs:

1. The beneficiary cannot have authority to revoke the trust; and

2. The beneficiary cannot direct the use of trust assets for his or her support and maintenance under the terms of the trust

42 USC §1382b(e)(3)(A), 20 CFR §416.1201(a)(1); POMS SI 01120.200(D)(2)

Third Party SNT Drafting

Common drafting error, focusing only on preserving public benefit eligibility

Missing main planning concerns of parents (replacing what the parent does):• Caregiving – instructions for hiring and utilizing caregivers

• Advocacy – preserving opportunities

• Housing – live in home? facility? board & care?

Collecting the parents/grandparents knowledge of person with a disability • Memorandum of Intent

Third Party SNT ProvisionsNC

1. Introductory provisions• Naming the SNT

• Trust Funding

2. Trust intent

3. Testamentary or Living SNT

4. Revocable or Irrevocable

3/22/17

4

Drafting the Third Party SNT

Living (inter vivos) versus Testamentary• If for spouse, must be testamentary trust (cannot use Living

SNT)

Revocable versus Non Revocable• Beneficiary with disability must never have right to revoke

trust

• Others may have that right (e.g. Parents)

Third Party SNT ProvisionsKU

• Describing Beneficiary’s disability

• Defining the term “Special Needs”

• Using a Memorandum of Intent

• Provisions for Care Manager and Advocate

• Providing Specific Instructions on Distributions• Maintaining contact with family

• Social/cultural activities

• Sporting

Defining “Disability” in Trust

• Generally, I use a general definition in document

• May want to provide a more thorough definition• If doing so, should only do so after fully discussing with

client, if using a general definition from internet be prepared for upset client when definition does not match their child’s condition

• My belief is better to provide detailed description of disability in Memorandum of Intent, easier to update and let parent define their child’s condition

3/22/17

5

Defining the Term “Special Needs”

• Most SNTs define the term to include a laundry list of goods and services that can be purchased• Is it necessary?

• Is it helpful?

• Be careful of placing too many limitations

• Be careful of allowing too many options (i.e., the shopping list)

Memorandum of Intent• In third party planning, most critical document for

customized plans• Add in specifics of person with disability• Keep updated (reminder to do it on person’s birthday)

• Prepare trust provision to have SNT Management Team review and utilize when interpreting “intent”

• Send Memo of Intent guidelines to client

• Refer clients to “Life Planning for Adults with Developmental Disabilities: A Guide for Parents and Family Members” by Professor Judith Greenbaum

Advocate/Care Manager• Oftentimes, the client is planning for their loved one with special

needs and the client is the one providing all the care, advocacy, love, and support

• Planning for the loss of this essential person is one of the most critical areas, especially in providing advocacy, as one of our members recently stated:

• “People with disabilities are repeatedly denied constitutional due process rights, reasonable accommodations under the law, and their basic needs. I think many criminals are given those and if they are not there is a significant legal response. Folks with disabilities are often given significantly less, and often victimized and punished for being a “burden” when they have committed no crime.”• Patti Dudek

3/22/17

6

Considerations for Advocacy and Care Management

• The SNT Trustee does not have legal authority to manage a beneficiary’s life, however, the drafter can provide them authority to manage or pay for that type of advocacy

• Great topic for a Memorandum of Intent

Drafting for Care Management and Advocacy

• Drafters should focus on Settlor’s desires for:• Coordinating and evaluating existing care to make sure it is

being done efficiently and thoroughly;• Applying to obtain services the person with a disability may

require if no one else can do so;• Determining if Beneficiary is receiving all services and public

benefits;• Visiting the Beneficiary to inspect and review home care;• Speaking with the Beneficiary’s medical personnel to make

sure health care is appropriate and care plans are being followed; or

• Advocating for services and care if in the opinion trust management team, it is not.

ASNP Drafting Guide’s Options

Option One: Provides a discretionary standard on when to hire a Care Manager or Advocate

Option Two: General provision allowing trustee to hire professionals as needed

3/22/17

7

SNT Disbursement Provisions to Enhance Quality of Life

When drafting a third party SNT, one of the best ways to make you a hero for your client is discussing specialized services that will enhance the quality of life of a child with a disability

Usually can determine in an intake form by asking such questions as:

• Does child attend annual camp

• Does child attend religious services

• Does child participate in Special Olympics or other athletic events

• Does child enjoys concerts, movies, or other social activities

• Is visiting family a priority

ASNP Drafting Guide:Some Provisions

There are provisions that can be customized for your client’s specific situation:

• Recreation and Social Activities

• Family Activities

• Payment for Vacations

Third Party SNT ProvisionsRF

1. Third party SNT taxation provisions

2. Termination provisions• Loss of public benefits• Substantial gainful employment• No longer disabled

• Uneconomical to administer• Death

3. General or Limited Power of Appointment

4. Remainder beneficiaries• Setting up contingent SNT for heirs

3/22/17

8

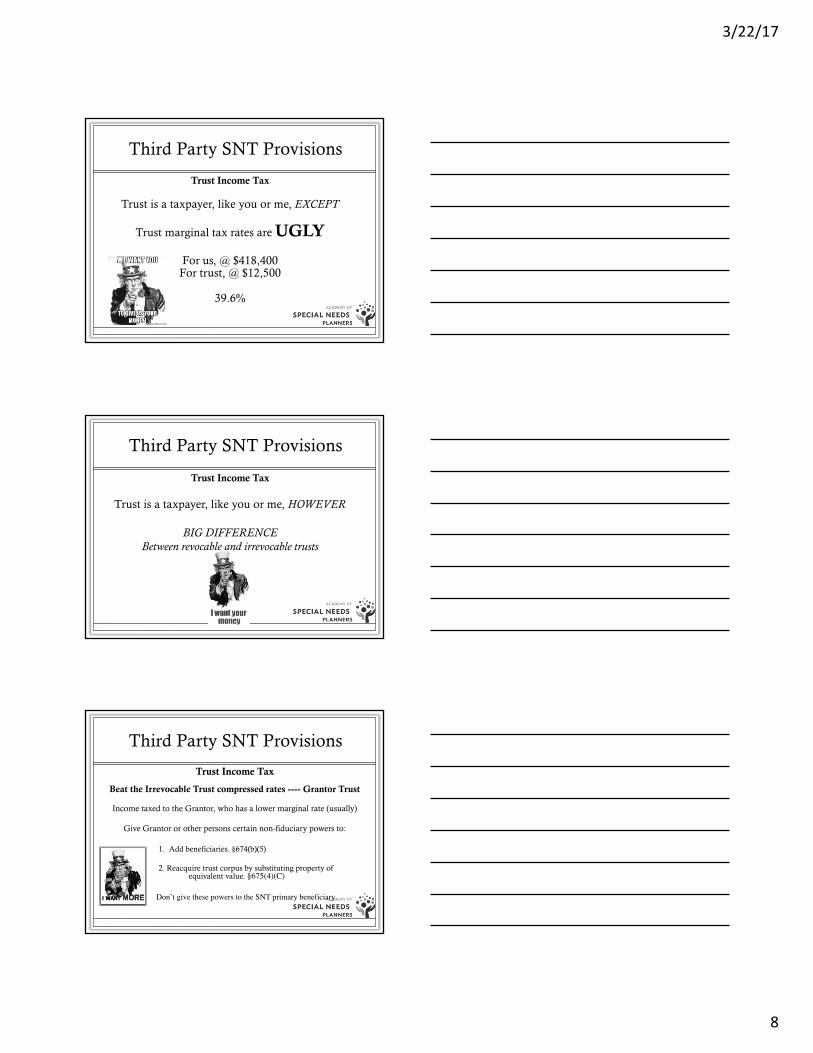

Third Party SNT Provisions

Trust Income Tax

Trust is a taxpayer, like you or me, EXCEPT

Trust marginal tax rates are UGLY

For us, @ $418,400For trust, @ $12,500

39.6%

Third Party SNT Provisions

Trust Income Tax

Trust is a taxpayer, like you or me, HOWEVER

BIG DIFFERENCEBetween revocable and irrevocable trusts

Third Party SNT Provisions

Trust Income Tax

Beat the Irrevocable Trust compressed rates ---- Grantor Trust

Income taxed to the Grantor, who has a lower marginal rate (usually)

Give Grantor or other persons certain non-fiduciary powers to:

• 1. Add beneficiaries. §674(b)(5)

2. Reacquire trust corpus by substituting property of equivalent value. §675(4)(C)

•Don’t give these powers to the SNT primary beneficiary

3/22/17

9

Third Party SNT Provisions

Third party SNT taxation!Do it Right!

I’m STILL broke!!

Third Party SNT Provisions

Qualified Disability Trust

I. Applies to a non-grantor complex trust (not only SNTs)

II. Allows trust a $4,050 personal income tax exemption

1041 Royal StNOLA

Third Party SNT Provisions

Qualified Disability Trust

To be treated as a QDT, the trust must be

1. Irrevocable2. Sole benefit of beneficiary3. Beneficiary is under the age of sixty-five4. All current beneficiaries have been determined

disabled by the SSA

I.R.C. §642(b)(2)(C)(ii); 42 U.S.C. §1396p(c)(2)(B)(iv).

3/22/17

10

Third Party SNT Provisions

Trust Termination provisions

DEATH

‘Nuff Said

Oh, and don’t forget to provide for contingent beneficiaries. . . .

Third Party SNT Provisions

Trust Termination provisions

Loss of Public Benefits

1. Cure the trust flaws (trustee or trust protector)

2. Kick out to beneficiary (or treat as support trust?)

3. The Moral Imperative – kick to someone else . . . and pray.

SSI office

Third Party SNT Provisions

Trust Termination provisions

No longer disabled

• Trustee determines beneficiary is not disabled per SSA definition

• Period of SGA -- Meet own needs for X months

CAUTION: some disabilities may return, such as mental illness

Trustee should have discretion to retain assets in trust

3/22/17

11

Third Party SNT Provisions

Trust Termination provisions

Uneconomical to Administer

Give trustee discretion to terminate and distribute

THEN NOW

Third Party SNT Provisions

Final Expenses

Trustee should have discretion to pay beneficiary’s:

A. Last debts properly due from beneficiary

B. Funeral expenses

C. Taxes

IF not enough cash outside the SNT to cover

Third Party SNT Provisions

Then What?

Final distribution of remaining assets

1. Give beneficiary the option to say where remainder goes• Limited/Special Power of Appointment (NOT general POA)

• By will or inter vivos writing

2. Residuary Clause – do a Gap analysis

3. Ultimate contingent – intestacy provision

3/22/17

12

Third Party SNT Provisions

Then What?

Final distribution of remaining assets

Contingent Beneficiary has Disabilities?

Provide for share to remain in SNT!

-- On terms of current SNT, or

-- With new terms and disposition

Third Party SNT Provisions

Then What?

Final distribution of remaining assets

Contingent Beneficiary is too young? ”Minority Trust” !

Discretionary until age milestone/s

Distribution on attaining age/s

Whaddaya mean I have to wait ‘til I’m 30 for my Buggati ?

Third Party SNT ProvisionsMF

1. Establishing third party SNT for spouse

2. Gifting provisions for charity, family or friends

3. Commingling Provision

3/22/17

13

Establishing a Third Party SNT for Spouse

• When do you use this provision? providing for an ill spouse in the event the well-spouse predeceases

• Provides structure and oversight if someone cannot (for whatever reason) handle the property

• Preventative LTC planning

• Post Medicaid planning when one spouse is in a nursing home or receiving some other type of Medicaid benefit

Benefit to the Spouse

• Integral part of a comprehensive Medicaid crisis plan

• Medicaid crisis plans are completely thwarted without implementation of planning in the event the well-spouse predeceases

• Provides safety and protection for the NH spouse

• For spouses in the home on waiver, in home support benefits, or PACE, they need the exempt resources to pay for additional caregiving, home repairs, taxes, to age in place.

• Prevents having to do planning to re-qualify:• Half-loaf or annuity

What to Include in Estate Plan

• A third-party SNT MUST be established by Will

• If your state is simple probate, terms of the will can establish the spousal testamentary SNT

• If there is a revocable living trust-there must be a “pour back” provision to have the assets go through probate in order to establish the SNT • The method of establishment and funding is state-specific

3/22/17

14

Third-Party SNT Gifting

• A third-party trust is not administered under the sole benefit rule

• A fundamental difference between first and third party

• When drafting consider putting guidelines for the trustee and limits on what can be disbursed• Can the trustee gift to self ?• Cults? Religious organizations? • Limit amount of gift? duration? scope?• Gift even if running out of money? Set floor in document

• Good points to be addressed in the Memorandum of Intent

• In absence of direction leaving it up to the Trustee

3p SNT Gifting provisions

Third-Party SNT Gifts

3/22/17

15

Third-Party SNT Gifts

Comingling in a Third-Party SNT

Comingling in a Third-Party SNT

• Do not place the Beneficiary’s assets into a third-party SNT

• Many non-professional trustees dislike multiple accounts

• The Beneficiary’s assets are COUNTABLE while in the third-party trust

• First-party money does not poison the third-party trust-but after a while may take a forensic accountant to unravel

3/22/17

16

Break Time

Please return in 30 minutes

Third Party SNT ProvisionsNC

1. “Sole benefit” trust if Settlor needs Medicaid

2. Adding POMS Third Party requirements

3. Funding a Pooled SNT

Drafting the Third Party SNT

Following POMS• SSA eligibility workers use this to evaluate whether snt

qualifies

• Make sure Third Party SNT meets all SSA requirements of:• POMS SI 01120.200 - Trusts

3/22/17

17

Third Party SNT ProvisionsKU

1. Multiple SNT beneficiaries

2. Drafting for receipt of IRA proceeds

Multiple SNT Beneficiaries

• Unlike first party SNT, a third party SNT can have multiple beneficiaries

• Typical planning scenarios are when:• Family has more than one child with a disability; or

• Family wants to create a Pot Trust or Children’s Trust with their entire inheritance

SNT Drafting for Multiple Beneficiaries

• Must ensure the trust distribution provision takes into account Settlor’s intent:• If two or more children with disabilities, how will Trustee

decide to allocate resources among children, e.g., if one has substantially more needs than another

• If only one child has disability, must make sure that the Trustee has appropriate discretionary distribution standard for the child with a disability

3/22/17

18

ASNP’s Guide on Drafting for Multiple Beneficiaries

Option One: Basic provisions on naming multiple beneficiaries when only one child has special needs

Option Two: Common Trust for all children and grandchildren with disabilities

IRA Accumulation Provisions

• If do not feel comfortable planning in this area, RUN, don’t walk to ASNP website and review Melanie Marmion’s program titled “SNTs & Retirement Benefits” that is available under 10th Annual Conference Materials

• Next, Natalie Choate’s book “Life and Death Planning for Retirement Benefits” is essential

Drafting SNT to Receive IRAs

• An SNT can be a “Designated Beneficiary” of an IRA if drafted correctly

• This allows an IRA to continue in existence and provide tax deferral benefits

• If no Designated Beneficiary the IRA must be distributed within 5 years after the owner's death. IRC §401(a)(9)(B)(ii)

• Bad tax result because the beneficiary will incur significant ordinary income tax during those 5 years and lose the benefit of deferred income tax

3/22/17

19

SNT as Designated Beneficiary• Trust has no life expectancy and regulations state that trust cannot be a

designated beneficiary. Treas Reg §1.401(a)(9)–4, A-5(a)

• The beneficiaries of a named trust will be recognized as designated beneficiaries if the following requirements are met (Treas Reg §1.401(a)(9)–4, A-5(b)):

1. Trust is valid under state law;

2. Trust is irrevocable, by its terms, on the participant's death;

3. Trust beneficiaries are individuals who are identifiable from the trust instrument; and

4. Plan administrator is provide a copy of the trust instrument and a list of all of the beneficiaries of the trust) See Treas Reg §1.401(a)(9)–4, A-6

Two General Types of Trusts May be Designated Beneficiary

• Conduit Trust is a safe harbor – the language of this trust allows for Required Minimum Distributions (RMD)s to flow through trust directly to beneficiary• IRS uses age of lifetime beneficiary to determine RMD

• RMDs from conduit affects SNT beneficiary’s public benefits

• Accumulation Trust allows for RMDs to be paid to trust, but not require immediate distribution• IRS uses age of oldest beneficiary to determine RMD,

including contingent remainder beneficiaries

• Issue arises if contingent beneficiary is not a natural person, e.g, a charity or is older than SNT beneficiary

SNT Drafting Issues

• Drafting SNT so all contingent beneficiaries are natural persons

• Drafting SNT so oldest beneficiary is person with a disability

• Make sure even a Power of Appointment in trust limits allowable appointees to natural persons younger than beneficiary

3/22/17

20

Drafting Solutions in ASNP Guide

Option One: Not leaving IRAs to person with a disability, leave it to other beneficiaries and even up with other assets

Option Two: Basic accumulation trust provisions, must make sure there are no charities as contingent remainder beneficiaries

Option Three: Trigger sub-Accumulation trust. Creates sub-trust for IRA proceeds in event trust is a beneficiary

Option Four: Creates a conduit trust and attempts to limit RMDs to only one month a year

Interested in Joining ASNP’s Special Needs Trust Planning Guide

Planning Team?

Join the Group by Signing our Form

Lunch Time

Please return in 60 minutes

3/22/17

21

(d)(4)(A) Special Needs Trusta.k.a. Payback Trusts

TF

Authorized by 42 U.S.C. §1396p(d)(4)(A) and has the following requirements:• Must be disabled• Must be established by INDIVIDUAL, parent, grandparent,

legal guardian, or court

• Must be for the sole benefit of the beneficiary

• Beneficiary must be under the age of 65 when established and funded

• Must provide that on the death of the beneficiary, the trustee must repay Medicaid if funds remain in the trust at the beneficiary's death

First Party SNT ProvisionsTF

1. Introductory provisions

2. Defining disability

3. Proper SNT establishmenta. “Self”

b. Parent/Grandparent (Seed)

c. Court

d. Guardian

First Party SNT ProvisionsTF

4. Under age 65 – when established and funded

5. Irrevocable

3/22/17

22

First Party SNT Must be Irrevocable

Federal statute does not expressly require a (d)(4)(A) SNT to be irrevocable

However, SSA does: • POMS SI 01120.201(D)(1); and

• POMS SI 01120.203(D)(1), Step 7

First Party SNT ProvisionsTF

6. Funding with Beneficiary’s assets – Seed necessary?

7. Defining the term “Special Needs” for first party SNTs

8. Administrative costs authorized prior to Payback - limit

First Party SNT ProvisionsTF

9. Early termination – SI 01120.199

10. Payback provisions – to “ALL State Medicaid agencies”

3/22/17

23

First Party SNT ProvisionsNC

1. “Sole Benefit” requirement

2. POMS checklist for first party SNTs

First Party SNT ProvisionsRF

1. Powers of Appointment

2. Taxation provisions for first party SNT

First Party SNT Provisions

Powers of Appointment

General: contingent beneficiaries can be anyone, including the powerholder, powerholder’s estate, powerholder’s creditors or creditors of the powerholder’s estate.

Limited/Special: contingent beneficiaries can be anyone EXCEPT the powerholder, powerholder’s estate, powerholder’s creditors or creditors of the powerholder’s estate.

3/22/17

24

First Party SNT Provisions

Powers of Appointment

Why do we care?

PWD may change mind about contingent beneficiaries.

POA allows PWD to change beneficiaries.

First Party SNT Provisions

Powers of Appointment

Ѭ State regulations may not allow PWD to designate contingent beneficiaries

Ѭ General POA may cause estate inclusionя -- large settlement may exceed lifetime federal exemption

я -- state estate tax exemption may be small

First Party SNT Provisions

Taxation provisions

Grantor Trust Redux

Beneficiary is considered the grantor if:

• No adverse parties must give permission for disbursements §674

• Beneficiary has power of substitution §675(4)(C)

CAUTION: some Medicaid agencies have held that the power of substitution is akin to the right to revoke trust

3/22/17

25

First Party SNT Provisions

Taxation provisions

Grantor Trust Redux

Beneficiary is considered the grantor if:

Ø Trustee has power to pay insurance premiums on life insurance on beneficiary. §677(a)

Ø Beneficiary has power of substitution

Ø Beneficiary has non-testamentary limited POA over assets left after Medicaid payback

First Party SNTMF

1. Prepayment of funeral

2. No commingling

3. No funding after age 65

4. Drafting to avoid SSA’s use of English Feudal common law

Prepaying for Funerals

• POMS specifically prohibit paying for funeral expenses after the Beneficiary’s death

• Draft guidelines and instructions to the Trustee as to POMS limits and exemptions for arranging an irrevocable pre-paid funeral contract

• If owned by the Trust, no limits

• Must be done PRIOR to the Beneficiary’s death

3/22/17

26

NO Comingling

• Common fiduciary mistake is accepting third-party assets• Subjects the assets to avoidable payback

• May jeopardize the exempt nature of the SNT if others have a right to trust assets

• Common fiduciary mistake: allowing SS income to be assigned to the trust• Accepting resources from the Beneficiary if over $2,000 is ok

• When drafting these provisions-provide guidance to the trustee and other resources for administration

No Funding After age 65

No Funding After 65

• Hard line rule-any assets added to the trust are counted as resources

• Depending on circumstances-draft for exceptions• Litigation recovery-structures that began prior to age 65

• Spousal support-if began before age 65 also exempt

3/22/17

27

Drafting to Avoid Feudal Law

Feudal Doctrine of Worthier Title

• Bane of every law student’s existence• Method of inheritance in feudal England: preference for

transfer of title by decent rather than devise or purchase

• Way for land to stay in family and avoid feudal duty

• Taking title by inheritance was viewed as “worthier” than through a legal instrument

• Differs by state• UTC states-generally statutorily abolished

• Review your state statutes

• Review Regional Counsel Opinions for prior cases

SSA Reliance on DWT

3/22/17

28

SSA Reliance on DWT

• To be an exempt asset-d4A must be irrevocable

• Easy to draft around this issue

• Problem language? • If there are any remaining assets after the payback, the

Trustee shall distribute these assets to the heirs (or estate) of the beneficiary

SSA Application of DWT

• SNTs that name “heirs at law” or the “estate of the beneficiary” as remainder beneficiaries, when determining the SNT is revocable, and therefore a countable resource

• Simplistic application of merger doctrine: this language renders the trust revocable under the feudal doctrines described in general above because the beneficiary is the sole beneficiary of the trust under the merger doctrine

• If the trust is for the “sole benefit” of the beneficiary and there are no other intervening interests, then all the interests are held by the beneficiary. The interests thus merge and the beneficiary holds all legal and equitable title to the trust assets.

Drafting around the DWT

• Pay particular attention to the remainder beneficiary portion

• Name specific people or classes of people (my children, my nieces and nephews)

• Where the Settlor’s heirs are unknown, for example, they may marry and have children at some point, gift a known person $10, then to heirs-at-law.

• Consider adding in state statutory provision which abolishes DWT-may save you an appeal later

3/22/17

29

First Party Special Needs TrustRM

• Medicare Set Aside Trust provisions

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Taking Medicare’s Interest into Account

Initial Reporting: • Carrier Responsibility

Pre-Settlement: • Lien Status Verification• Public Benefit Analysis / Conversation

Settlement:• Final Demand Letter and payment within 60 days• Establish Trust / MSA Approval

Post-Settlement: • MSA / MCA Administration • Trust Administration (SNT, PT, SPT, Family)

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Initial Reporting = Carrier Responsibility

The Medicare Secondary Payor Mandatory Reporting Provisions makes the Carrier responsible for reporting all

payments of S, J, or A over $1,000.00* to the CMS Coordinator for Benefits Contractor.

*This amount also represents the settlement threshold for reimbursement of Conditional Payments

Section 202 of the SMART ACT

3/22/17

30

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Responsibilities of Attorneys

Upon taking a case where the beneficiary is a Medicare or Medicaid recipient the parties are required to place the

appropriate agency on notice (depending Comp or Liability), this also includes *Advantage Organizations

(MAO).*Circuit Opinions Differ

Please note these agencies have no responsibility to contact the attorney or client.

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Pre-Settlement MSA / SNT or BOTH

If a beneficiary is currently receiving Medicare and the gross settlement is over $25,000, or the total amount is over $250,000 and the beneficiary could be Medicare eligible within 30 months, or has end stage renal disease

If a beneficiary is currently receiving Medicaid and chooses to preserve these benefits you will need to discuss Special Needs Trust options

3/22/17

31

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Settlement = Attorney Responsibility

MSA Allocation Submission* and Approval• Submit MSA Allocation to CMS with Final Settlement

Agreement and a statement as to how the MSA will be Funded and Administered

* OK City (Comp) CMS Portal / Atlanta (Liability)

Establishment of a Special Needs Trust• Take into consideration age of beneficiary• Consider options for Trust Administration

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Post Settlement = Attorney and Beneficiary

Self Administered MSA• The Self Administered MSA requires the beneficiary to

possess sound money management abilities, excellent judgment, keen organizational skills, and expertise in medical billing and fee schedules.

Self Administered SNT• A Self Administered SNT is simply not an option. The

beneficiary may never act as trustee of their own SNT. In addition it is not a wise decision to engage a family member for these fiduciary responsibilities.

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Post Settlement = Attorney and Beneficiary

Professionally Administered MSA• Safety, security and knowledge are all elements that a

professional Medicare Set-Aside Administrator should possess, but be careful when choosing your MSA Administrator to ensure they have specific experience in MSA Administration.

• (Reversionary)

Professionally Administered SNT• Since Medicaid programs differ from state to state, the Trustee

of a Special Needs Trust should have comprehensive knowledge of specific rules regarding program eligibility, otherwise the beneficiary could risk disqualification from these vital programs.

• (Reversionary)

3/22/17

32

The materials contained herein are not to be considered legal advice but informational in nature. Copyright 2015 The Centers

Post Settlement = Attorney and Beneficiary

Self Administered MSA• The Self Administered MSA requires the beneficiary to

possess sound money management abilities, excellent judgment, keen organizational skills, and expertise in medical billing and fee schedules.

Self Administered SNT• A Self Administered SNT is simply not an option. The

beneficiary may never act as trustee of their own SNT. In addition it is not a wise decision to engage a family member for these fiduciary responsibilities.

Break Time

Please return in 30 minutes

Provisions Common to Both SNTsRF

• Trustee provisions• Identifying initial trustee

• Replacement of Incapacitated Trustee

• Successor trustee (independent or interested)

• Removal of trustee

• Exculpatory clauses

• Professional trustee provisions

• Default of designation

3/22/17

33

Provisions Common to Both SNTs

Trustee provisions

Initial trustee

1. Individual trustee

2. Corporate trustee

3. Co-trustees

Provisions Common to Both SNTs

Trustee provisions

Temporary Removal of Trustee

Incapacity/Disability

I. Medical certification (two docs, one a specialist)

II. By Court of competent jurisdiction

Provide for Interim Trustee to serve during period of incapacity

Provisions Common to Both SNTs

Trustee provisions

Permanent Removal of Trustee

I. By Grantor (only third party SNTs)

II. By Trust Protector

III. By Court of competent jurisdiction (for cause)

Cause? Gross negligence, insolvency, failure to act, inability to manage financial assets, willfulness

3/22/17

34

Provisions Common to Both SNTs

Trustee provisions

Successor trustee

1. Name the bench in the agreement

2. If more than one trustee, let remaining ones serve without replacing dead or disabled trustee

3. Allow last-serving trustee to appoint own successor

4. Trust protector or committee appoints successor

5. Court with jurisdiction makes appointment

Provisions Common to Both SNTs

Trustee provisions

Exculpatory Clause

1. Only liable for gross negligence and intentional acts – all trustees

2. Only liable for gross negligence and intentional acts – individual

trustees 3. No liability for failing to ID benefit

4. No liability for failing to maintainbenefits

Provisions Common to Both SNTs

Trustee provisions

Corporate fiduciary

1. Provide for scheduled fees as permissible compensation

2. Required language allowing self-dealing

3. Consider only replacing a corporate fiduciary with a corporate fiduciary

4. Have corporate fiduciary review draft

3/22/17

35

Provisions Common to Both SNTs

Trustee provisionsDefault of Designation

What happens when there are no named trustees left?

Provide mechanism for filling the vacancy!

Α Grantor (if alive)

Β Trust Protector

Γ Trust Advisory Council

Δ CourtWest Coast Trustee doing chair

Yoga exercises while working

Provisions Common to Both SNTsKU

1. Trust Advisory Committee/Trust Protector

2. Hiring professionals

3. Distribution provisions• Supplemental

• Discretionary

4. Making SNT distributions

Specific Provisions in SNT DraftingKU

1. Regular contact with Beneficiary

2. Reporting to SSA and others

3. Null and void clauses

4. Allocating disbursements among multiple SNTs

3/22/17

36

Setting Up the SNT Management Team

Need to consider possible decades of SNT administration

Establish lifetime trust management team• Trustee – Individual or Professional

• Trust Advisory Committee• Good check and balance on Trustee

• Remove and replace Trustee

• Trust Protector• Backup to Trust Advisory Committee

• Allowed to modify SNT terms to keep current with changes in law

Helpful Provision:What Can’t a SNT Pay For?

A SNT CANNOT give cash directly to Beneficiary (this includes gift cards unless strict definition)

If SNT pays for food, shelter or medical care already being provided by SSI or Medicaid it will reduce (or eliminate) public benefits.• Shelter is defined as food, gas, electricity, water, sewer,

heating fuel, garbage removal, real estate taxes, rent or mortgage

Drafting the SNTDistribution Standard

Knowing the Right Distribution Standard• Supplemental – No payments if reduce or eliminate public

benefits

• Discretionary – Allows Trustee to make disbursements even if affects public benefits

WARNING – State Specific

WARNING – Health, Education, Maintenance and Support Standard Could be Hazardous to Your SNT

3/22/17

37

Making SNT Distributions

• A provision that outlines how to make SNT distributions is not legally necessary, but it can be helpful for an SNT trustee who may not be aware of how SNT administration can still jeopardize public benefits eligibility

• The ASNP Drafting Guide includes a checklist that should be performed each time Trustee is making an SNT distribution then provides some sample methods on how to make such a distribution if the person is on public benefits

Regular Beneficiary Contact

• When advising SNT trustees during administration, one of the biggest surprises is how little many of the trustee’s communicate or visit with the Beneficiary

• Beneficiaries when contacted oftentimes have unmet needs the trust could be providing

• The ASNP Drafting Guide provides a provision that requires a trustee to visit (or hire an agent) to visit the Beneficiary on a regular basis

Maintaining Beneficiary’s Public Benefits

• One of my pet peeves is reviewing an SNT that requires a Trustee to obtain all the beneficiary’s public benefits and do all the reporting to public benefit agencies

• Issue is that Trustee oftentimes does not have the legal right to do so because the government will only deal with beneficiary directly or their legal representative who is in charge of their person

• During SNT administration the Trustee must then decide to comply with trust terms (which may be impossible) seek court intervention to instruct on how to proceed, or be in breach of trust

3/22/17

38

Better SNT Provision on Public Benefits

Better SNT provision included in ASNP’s Drafting Guide requires Trustee to cooperate with Beneficiary in obtaining and maintaining public benefits, but does not require them to obtain or maintain benefits

Null and Void Clauses

The SSA does not recognize either null and void provisions or exculpatory clauses in a trust

NOTE: While exculpatory clauses, use clauses, trustee discretion and restrictions on distributions, etc., do not affect a trust's countability, they do have an impact on how the various components are treated. For example, a prohibition in a discretionary irrevocable trust that limits the trustee to distributing no more than $10,000 to an individual has no effect on whether or not the trust is countable, but does affect the amount that is countable.

Allocating Among Multiple SNTs

• A person with a disability can have multiple SNTs, it could be a (d)(4)(A) SNT and one third party SNT

• In one case, I had a client who had 5 third party SNTs and 1 first party SNT, the 5 included funding from each set of grandparents, one from mother’s separate property, one from father’s separate property, and one jointly from mother and father, each with their own trustee and different remainders

• An allocation clause was essential to make sure disbursements were made from the appropriate trust

3/22/17

39

Multiple SNTs Allocation

The ASNP Drafting Guide includes a provision that requires that first distributions come from first party SNT, then if there are multiple third party SNTs, an allocation among each of them

Common SNT Phrases

The ASNP Drafting Guide includes a section on commonly used public benefit and person with a disability phrases that can be included in the definition sections of an SNT

Provisions Common to Both SNTsMF

1. Spendthrift provisions

2. Real estate provisions

3. Funding an ABLE account

3/22/17

40

Spendthrift Provisions

• Common SNT provision-prevents Beneficiary from transferring or selling their interest in the trust

• Even if Beneficiary received regular recurring income from the trust-creditors cannot reach it• In best practice SNT administration, this wouldn’t happen anyway

• Does your state recognize spendthrift protection?

• If not, SSAs directive is to recognize the value of the Beneficiary’s right to income as a countable resource because it can be sold

Spendthrift Provisions

• Drafter should include a spendthrift provision

• Prevents Beneficiary from legally assigning interest

• Prevents creditors from attachment to future disbursements

• Clarifies legal rights of the Beneficiary, relationship to creditors, and authority of Trustee to deny claims

Real Estate Provisions

3/22/17

41

Real Estate Provisions

• Dealing with real estate is one of the most difficult propositions for an SNT Trustee

• Drafting considerations:• What type of SNT is it?

• Family wishes (see Memo of Intent for further guidance that doesn’t belong in the legal document);

• Specific condition of the Beneficiary-keep in mind prognosis and how aging may affect future needs

• The expertise of the Trustee(s)

Real Estate Provisions

• Role of drafter is to create written guidance in light of the type of SNT

• Identify purchase options: rent, own, lend?

• Management and maintenance: who’s responsible?

• Sustainability?

• Public assistance? Section 8? In home supports? Roommates?

• Answer the what if ’s

Funding an ABLE Account

3/22/17

42

Funding an ABLE Account

Valid disbursement from an SNT

• Empowers Beneficiary

• Improves relationship with Trustee

• Reduces Trustee fees

• May prevent ISM reduction for SSI recipients

ABLE Account Provisions

Drafting considerations:

• Ability of the Beneficiary to handle money: limit the scope of how much the Trustee can fund? Or up to annual max? Frequency?

• Can the trust afford it?

• The type of SNT: third-party funds now subject to payback

• Insert guidance for SSA regarding disregard of ABLE disbursements for QDE as income even if for shelter

• OR just rely on the discretion and judgment of the Trustee

• Add provisions to help Trustee make decisions

Questions?