prestel and partner family office forum zurich november 2014 low correlations within portfolio...

TRANSCRIPT

Prestel and Partner Family Office Forum Zurich

November 2014

Low correlations within portfolio building

1 STEPHAN GERWERT /// CHRISTIAN HAMMES

STEPHAN GERWERT /// CHRISTIAN HAMMES 2

STEPHAN GERWERT /// CHRISTIAN HAMMES

SECTION 1 Quick look at theory

SECTION 2 Why?

SECTION 3 Challenges and practical implications when working with correlation

SECTION 4 Investment ideas within the liquid and illiquid portfolio

Agenda

3

STEPHAN GERWERT /// CHRISTIAN HAMMES

SECTION 1

Quick look at theory

STEPHAN GERWERT /// CHRISTIAN HAMMES

Three main aspects

1. Correlation talks about the dependence of at least two variables among each other.

2. Correlation is a general concept not just bound to portfolio-theory.

3. Correlation either positive, negative or zero and range bound from -1 to +1

5

STEPHAN GERWERT /// CHRISTIAN HAMMES

SECTION 2

Why?

STEPHAN GERWERT /// CHRISTIAN HAMMES

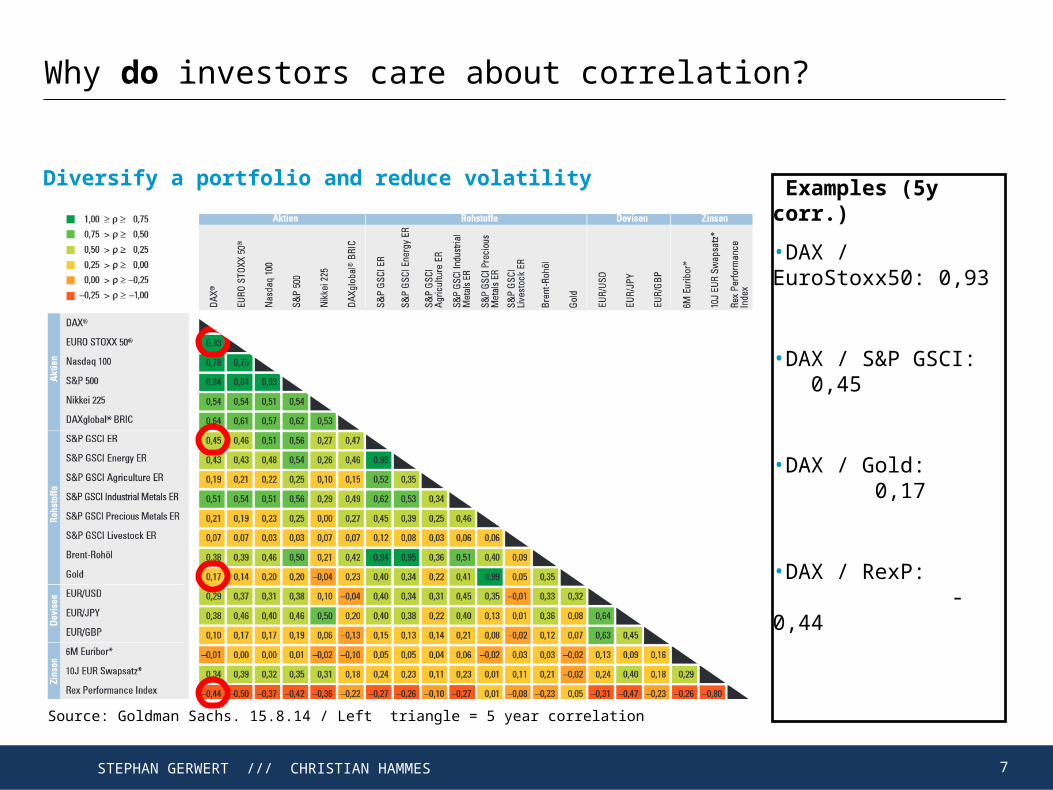

Why do investors care about correlation?

Diversify a portfolio and reduce volatility

Source: Goldman Sachs. 15.8.14 / Left triangle = 5 year correlation

Examples (5y corr.)

•DAX / EuroStoxx50: 0,93

•DAX / S&P GSCI: 0,45

•DAX / Gold: 0,17

•DAX / RexP: -0,44

7

STEPHAN GERWERT /// CHRISTIAN HAMMES

Why should investors care about correlation?

Morphia

US Capital Costs rise

EM Hard Landing

EU Debt

Crisis intensifies

Growth Slowdown

Growth Slowdown

Bond Bubble bursts

Bond Bubble burstsInflationInflation

New Iron Curtain

Abenomics fail

Current Status

Main Scenarios

Side Scenarios

Geopolitical /

Regional Implications

8

Trouble in South China

Sea

STEPHAN GERWERT /// CHRISTIAN HAMMES

SECTION 3

Challenges and practical implications when working with correlation

STEPHAN GERWERT /// CHRISTIAN HAMMES

1. Correlation does not imply causation.

=> Make use of short term deviations where threre is a cause-effect relationship.

What aspects relating to correlation do investors tend to forget?

10

2. The correlation value cannot be interpreted the same for different variables.

=> Expected intermarket relationships should hold true.

3. Correlation among two variables is not a constant and market manipulation is huge.

=> Make use of mean reversion.

4. Tough to measure correlation for illiquid assets.

=> Be pragmatic, use common sense and don´t make a science out of it

5. Constantly high correlation among similar assets are a fact.

=> Focus on fundamentals and relative strength

STEPHAN GERWERT /// CHRISTIAN HAMMES

SECTION 4

Investment ideas within the liquid and illiquid portfolio

STEPHAN GERWERT /// CHRISTIAN HAMMES

Real 10 year return expecations of liquid asset classes

Source: Research Affiliates

GOALGOAL

12

VOLATILITY

STEPHAN GERWERT /// CHRISTIAN HAMMES

The usual suspects

• Liquid portfolio:

Commodities

• Illiquid portfolio:

Hedge Funds (to heterogeneous to go into detail; some are liquid)

Private Equity

Real Estate

Infrastructure

Land and Forestry

Luxury Goods (art, watches, wine, cars)

13

STEPHAN GERWERT /// CHRISTIAN HAMMES

Invest in preparedness, not prediction

• Insurance Linked Securities

• Private Debt

• Factoring

• Microfinance

• Volatility

• Distressed debt

• Smart Beta

• Quantitative strategies

• …

14

Net Return: 7% - 8% p.a.

Volatility: 3% - 4% p.a.

Max. Drawdown: < 5%

STEPHAN GERWERT /// CHRISTIAN HAMMES

THE END

Thank you for your attention.

Q&A