pricing probe in the us dampens sentiment… - icici...

TRANSCRIPT

ICICI Securities Ltd. | Retail Equity Research

December 19, 2016

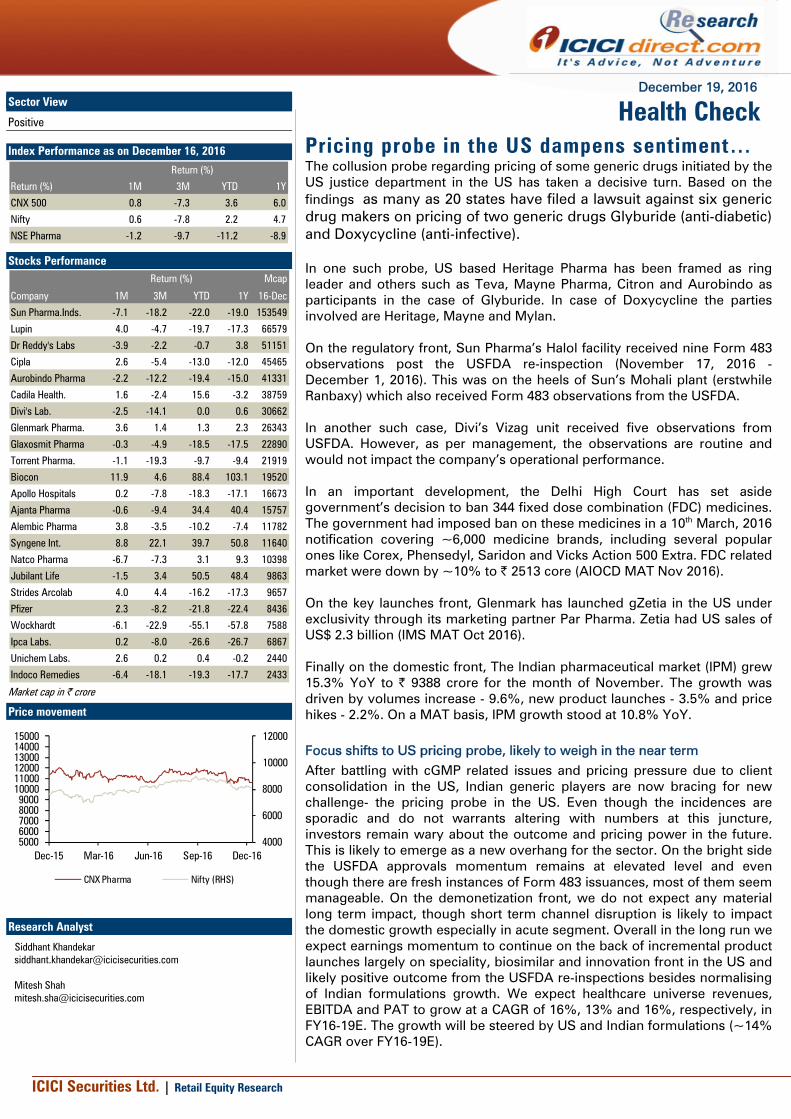

Pricing probe in the US dampens sentiment… The collusion probe regarding pricing of some generic drugs initiated by the US justice department in the US has taken a decisive turn. Based on the findings as many as 20 states have filed a lawsuit against six generic drug makers on pricing of two generic drugs Glyburide (anti-diabetic) and Doxycycline (anti-infective). In one such probe, US based Heritage Pharma has been framed as ring leader and others such as Teva, Mayne Pharma, Citron and Aurobindo as participants in the case of Glyburide. In case of Doxycycline the parties involved are Heritage, Mayne and Mylan. On the regulatory front, Sun Pharma’s Halol facility received nine Form 483 observations post the USFDA re-inspection (November 17, 2016 - December 1, 2016). This was on the heels of Sun’s Mohali plant (erstwhile Ranbaxy) which also received Form 483 observations from the USFDA. In another such case, Divi’s Vizag unit received five observations from USFDA. However, as per management, the observations are routine and would not impact the company’s operational performance. In an important development, the Delhi High Court has set aside government’s decision to ban 344 fixed dose combination (FDC) medicines. The government had imposed ban on these medicines in a 10th March, 2016 notification covering ~6,000 medicine brands, including several popular ones like Corex, Phensedyl, Saridon and Vicks Action 500 Extra. FDC related market were down by ~10% to | 2513 core (AIOCD MAT Nov 2016). On the key launches front, Glenmark has launched gZetia in the US under exclusivity through its marketing partner Par Pharma. Zetia had US sales of US$ 2.3 billion (IMS MAT Oct 2016). Finally on the domestic front, The Indian pharmaceutical market (IPM) grew 15.3% YoY to | 9388 crore for the month of November. The growth was driven by volumes increase - 9.6%, new product launches - 3.5% and price hikes - 2.2%. On a MAT basis, IPM growth stood at 10.8% YoY. Focus shifts to US pricing probe, likely to weigh in the near term After battling with cGMP related issues and pricing pressure due to client consolidation in the US, Indian generic players are now bracing for new challenge- the pricing probe in the US. Even though the incidences are sporadic and do not warrants altering with numbers at this juncture, investors remain wary about the outcome and pricing power in the future. This is likely to emerge as a new overhang for the sector. On the bright side the USFDA approvals momentum remains at elevated level and even though there are fresh instances of Form 483 issuances, most of them seem manageable. On the demonetization front, we do not expect any material long term impact, though short term channel disruption is likely to impact the domestic growth especially in acute segment. Overall in the long run we expect earnings momentum to continue on the back of incremental product launches largely on speciality, biosimilar and innovation front in the US and likely positive outcome from the USFDA re-inspections besides normalising of Indian formulations growth. We expect healthcare universe revenues, EBITDA and PAT to grow at a CAGR of 16%, 13% and 16%, respectively, in FY16-19E. The growth will be steered by US and Indian formulations (~14% CAGR over FY16-19E).

Health CheckSector View

Positive

Index Performance as on December 16, 2016

Return (%) 1M 3M YTD 1Y

CNX 500 0.8 -7.3 3.6 6.0

Nifty 0.6 -7.8 2.2 4.7

NSE Pharma -1.2 -9.7 -11.2 -8.9

Return (%)

Stocks Performance Mcap

Company 1M 3M YTD 1Y 16-Dec

Sun Pharma.Inds. -7.1 -18.2 -22.0 -19.0 153549

Lupin 4.0 -4.7 -19.7 -17.3 66579

Dr Reddy's Labs -3.9 -2.2 -0.7 3.8 51151

Cipla 2.6 -5.4 -13.0 -12.0 45465

Aurobindo Pharma -2.2 -12.2 -19.4 -15.0 41331

Cadila Health. 1.6 -2.4 15.6 -3.2 38759

Divi's Lab. -2.5 -14.1 0.0 0.6 30662

Glenmark Pharma. 3.6 1.4 1.3 2.3 26343

Glaxosmit Pharma -0.3 -4.9 -18.5 -17.5 22890

Torrent Pharma. -1.1 -19.3 -9.7 -9.4 21919

Biocon 11.9 4.6 88.4 103.1 19520

Apollo Hospitals 0.2 -7.8 -18.3 -17.1 16673

Ajanta Pharma -0.6 -9.4 34.4 40.4 15757

Alembic Pharma 3.8 -3.5 -10.2 -7.4 11782

Syngene Int. 8.8 22.1 39.7 50.8 11640

Natco Pharma -6.7 -7.3 3.1 9.3 10398

Jubilant Life -1.5 3.4 50.5 48.4 9863

Strides Arcolab 4.0 4.4 -16.2 -17.3 9657

Pfizer 2.3 -8.2 -21.8 -22.4 8436

Wockhardt -6.1 -22.9 -55.1 -57.8 7588

Ipca Labs. 0.2 -8.0 -26.6 -26.7 6867

Unichem Labs. 2.6 0.2 0.4 -0.2 2440

Indoco Remedies -6.4 -18.1 -19.3 -17.7 2433

Return (%)

Market cap in | crore

Price movement

4000

6000

8000

10000

12000

50006000700080009000

100001100012000130001400015000

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

CNX Pharma Nifty (RHS)

Research Analyst

Siddhant Khandekar [email protected] Mitesh Shah [email protected]

ICICI Securities Ltd. | Retail Equity Research

Page 2

Regulatory approvals

Exhibit 1: Summary of USFDA approvals for Nov, 2016 [5

Company Drug Name Therapeutic Area Innovator company Generic Version of Market SizeAlembic Pharma Irbesartan; Hydrochlorothiazide CVS Sanofi Aventis Avalide NAJubilant Life Darifenacin ER Anti-Infective Allergan Enablex NAAjanta Pharma Lansoprazole Anti-ulcer Takeda Pharms Prevacid NAAurobindo Pharma Risedronate Sodium Osteoporosis Warner Chilcott Actonel US$113 millionAurobindo Pharma Eszopiclone tablets Insomnia Sepracor Lunesta NATorrent Pharma Fluoxetine Hydrochloride CNS APIL Sarafem NAAurobindo Pharma Nylia 7/7/7 (Ethinyl estradiol and norethindrone) OC Janssen Pharma Ortho-Novum 7/7/7-28 NAAurobindo Pharma Cyonanz (Ethinyl estradiol and norethindrone) OC Janssen Pharma Modicon 28 NAAurobindo Pharma Nylia 1/35 (Ethinyl estradiol and norethindrone) OC NA Ortho-Novum 1/35-28 NAGlenmark Pharma Nystatin and Triamcinolone acetonide Dermatology Delcor Assest Mycolog-II US$121 millionTorrent Pharma Olmesartan Medoxomil; Amlodipine; Hydrochlorothiazide CVS Daiichi Sankyo Tribenzor NADr Reddy's Lab Nystatin; Triamcinolone Acetonide Derma G And W Labs Mykacet US$ 37.5 millionLupin Estradiol and Norethindrone Acetate OC JANSSEN PHARMS ORTHO CYCLEN-28 NAAurobindo Pharma Ipratropium Bromide Respiratory Boehringer Ingelheim Atrovent NAAjanta Pharma Amlodipine; Olmesartan Medoxomil Bloodpressure Daiichi Sankyo Azor US$ 174 millionCipla Montelukast Sodium Anti-asthama Merck Singulair NATorrent Pharma Rosuvastatin Calcium Avascular necrosis IPR Crestor NAJubilant Life Rosuvastatin Calcium Avascular necrosis IPR Crestor NAJubilant Life Rosuvastatin Calcium Avascular necrosis IPR Crestor NA

Company Drug Name Therapeutic Area Innovator company Generic Version of Market SizeTorrent Pharma Olmesartan Medoxomil CVS Daiichi Sankyo Benicar NAAurobindo Pharma Hydrochlorothiazide; Olmesartan Medoxomil CVS Daiichi Sankyo Benicar HCT NAJubilant Life Olmesartan Medoxomil CVS Daiichi Sankyo Benicar NAAurobindo Pharma Guaifenesin;Dextromethorphan Hydrobromide Anti-Infective Reckitt Benckiser Mucinex DM NA

Final Approvals

Tentative Approvals

CNS: Central Nervous System; CVS: Cardiovascular,GI: Gastro Intestinal, NA: Not available; Source: USFDA, ICICIdirect.com Research

M&As, Demergers, Tie-ups and JVs Sun Pharma to acquire Biosintez in Russia Sun Pharma entered into an agreement to acquire 85.1% of JSC Biosintez, a Russian pharmaceutical company engaged in manufacture and marketing of pharmaceutical products in Russia and CIS region. Equity consideration for shares acquired is RUB 1,526 million (~| 163 crore). Sun Pharma would also assume a debt of ~US$ 36 million (~| 245 crore) as part of this transaction. JSC Biosintez’s 2015 annual revenue was RUB 3208 million (~| 343 crore). This deal expected to complete by end of 2016. Cipla EU divests stake in Chase Pharmaceuticals to Allergan Cipla announced that Chase Pharma (in which Cipla EU has 16.7% stake) has been acquired by Allergan, plc. Allergan has agreed to pay US$125 million upfront plus potential regulatory and commercial milestones of up to US$875 million to the shareholders of Chase. Cipla acquired a minority stake in Chase in May 2014 via a syndicated venture investment. Aurobindo’s French unit to buy products from Teva Aurobindo Pharma’s French subsidiary Arrow Generiques announced the signing of an agreement to acquire select commercial products in France from Teva. Arrow Generiques will acquire the right, title and interest in products Calcium and Calcium Vitamin D3, including the use of the OROCAL trademark. The transaction is subject to the approval of the European Commission IFC invests | 450 crore for 29% stake in Apollo Health International Finance Corp. (IFC) has invested | 450 crore for a 29% stake in Apollo Health and Lifestyle Ltd (AHLL), a unit of Apollo Hospitals Enterprise Ltd. IFC values AHLL at | 1550 crore. AHLL intends to use this money for expansion of various sub-units.

ICICI Securities Ltd. | Retail Equity Research

Page 3

Lupin partners Eli Lilly to market diabetes drug Eglucent Lupin and Eli Lilly (Indian subsidiary) have expanded their partnership in the diabetology therapy in India with the launch of Eglucent, a new brand of Lilly’s rapid-acting insulin analog Lispro. Lupin will market and sell Eglucent through its own specialty field force while Lilly will be responsible for manufacturing and import. Lilly will continue to sell Lispro under the brand name Humalog through its existing channels. Stride Shasun acquires Perrigo API India Stride Shasun acquires Perrigo API India private Limited (Perrigo API) for | 100 crore. The transaction is expected to close by end of 2016. Perrigo API has UAFDA approved API facility at Ambernath, Maharastra. Perrigo API’s FY16 revenues was | 73.8 crore and gross block was | 287.4 crore. Sun Pharma, Moebius Medical tie-up to develop pain product Sun Pharma and Israel-based Moebius Medical have entered into an exclusive worldwide licensing deal to develop novel liposomal non-opiod pain product MM-II for the treatment of pain in osteoarthritis. Sun Pharma to fund further development of MM-II including completion of Phase II and Phase III clinical programs and any required preclinical work necessary for regulatory approval. Moebius Medical will receive upfront, milestone and royalty payment from Sun Pharma. Cipla to set up manufacturing facility for pharmaceuticals in Iran Cipla, through its Netherlands-based subsidiary entered into an agreement with Ahran Tejarat Company to form a joint venture in Iran. As per the agreement, Cipla will hold 75% stake in the JV, while the Iranian partner will own the remaining. Cipla will invest ~Euro 16.9 million (~| 120 crore) in the JV. JV will set up a manufacturing facility for pharmaceutical products in Iran. Price cuts / New Launches / Recalls/Approvals Dr Reddy’s Labs recalls isotretinoin capsules from US Dr Reddy’s Labs has recalled 3,858 prescription packs (115,680 capsules) of Zenatane (isotretinoin capsules USP) 20 mg, 30 capsules due to an out of specification results has been determined for an individual related substance during stability testing. As per the report, all the recalls are fall under a class III recall category. Cadila recalls 20500 bottles of anti- depressant drug in the US Cadila is recalling 20500 bottles of anti- depressant Bupropion Hydrochloride extended release tablets for failed dissolution specifications. This recalls is considered under class III recall category. Glenmark launched gZedia under exclusivity in the US Glanmark Pharma has launched generic version of cholesterol lowering drug Zetia (ezetimibe) under 180 days exclusivity through its partner par Pharma. As per IMS, Zetia has annual sales of US$ 2.3 million in the US. Law suits / Court rulings / Settlements / Regulatory Issues

Sun pharma’s Halol unit receives nine USFDA observations Sun Pharma’s Halol facility receives nine form 483 observations post USFDA re-inspected the plant from November 17, 2016 through December 1, 2016. As per management, none of these observations were repeat observations. The company is preparing its responses to the observations, which will be submitted to USFDA within 15 business days of receipt of the Form-483.

ICICI Securities Ltd. | Retail Equity Research

Page 4

Divi’s Visakhapatnam unit receives five USFDA observations Divis Lab’s Unit-II at Visakhapatnam has received form 483 with five observations post USFDA inspected this plant between November 29, 2016 to December 06, 2016. The company will respond to the USFDA within the time permitted. As per management, the observations are routine and would not impact the company’s operational performance. Sun’s Mohali plant receives seven form 483 observations from USFDA The USFDA inspected Sun Pharma’s Mohali plant between 7 November and 16 November and issued the seven Form 483 observations, citing four deviations from norms in the laboratory system, two in the quality system and one in the production system. This plant is already under USFDA import alert since Sept 2013. Vietnam bans 39 Indian Drug cos for violation of quality standard Aurobindo, cadila are among 39 Indian drug companies that have been blacklisted by Vietnam for quality standard violations. Vietnamese drug regulator has also banned companies in Bangladesh and South Korea. As per Aurobindo, Vietnam annual sales was ~US$ 1 million. However, as per Aurobindo Pharma’s management, the company is not been blacklisted and continues to export to Vietnam. Vietnam regulatory authority has introduced additional step of analysis on importing medicines in vietnam before release of batches. Aurobindo’s annual Vietnam sales is ~US$1 million. 27 medicines sold by top firms fail quality tests in seven states Indian drug regulators of seven states have alleged that 27 medicines sold by 18 major drug companies in India including Abbott India, GSK India, Sun Pharma, Cipla and Glenmark Pharma are of substandard quality, citing grounds such as false labelling, wrong quantity of ingredients, discolouration, moisture formation, failing dissolution test and failing disintegration test. Some of the key brands which were alleged to be substandard are, antipsychotic drug Stemetil and antibiotic drug Pentids from Abbott India, anti-bacterial medicine Althrocin by Alembic Pharma, migraine medication Vasograin by Cadila Pharma, popular cough syrup Ascoril by Glenmark Pharma, worm infection drug Zentel by GSK India, arthritis medication Hydroxychloroquine (HCQS) by Ipca Labs, anti-inflammatory medication Myoril by Sanofi Synthelabo, and Torrent Pharma’s hypertension drug Dilzem. Delhi High Court quashes government ban on over 300 medicines The Delhi High Court has set aside government’s decision to ban 344 fixed dose combination (FDC) medicines. The government had imposed ban on these medicines in a March 10 notification affected around 6,000 medicine brands, including several popular ones like Corex, Phensedyl, Saridon and Vicks Action 500 Extra. The court however had stayed the ban in March. Allergan settles Delzicol patent litigation with Cadila Cadila Healthcare has settled a litigation with US based Allergan regarding latter’s Ulcerative Colitis drug Delzicol. As per the settlement, Cadila will be able to market the generic version (subject to USFDA approval) on 1st March 2020 or earlier under certain circumstances. US antitrust subpoenas companies over generic drug pricing Sun and Taro Pharma including few more foreign Pharma companies received subpoenas from US Department of Justice (DOJ) in connection with a federal antitrust investigation into generic drug pricing. The US DOJ already accused two former generic pharmaceutical executives colluding with other generic manufacturers to fix prices.

ICICI Securities Ltd. | Retail Equity Research

Page 5

U.S. states sue Aurobindo and others for fixing drug prices 20 states filed a lawsuit against Mylan, Teva Pharma, Aurobindo Pharma and three other generic drug makers, saying they conspired over steak dinners and "girls nights out" on pricing of two common generic drugs. According to the complaint, Heritage, Teva, Aurobindo and Citron conspired to raise prices on glyburide; Heritage, Mylan and Mayne conspired to allocate and divide the market for doxycycline. Others

Taro Announces New $250 Million Share Repurchase Authorization Sun Pharma’s subsidiary Taro Pharma announced that its Board of Directors has approved a new US$250 million share repurchase authorization of its ordinary shares. This authorization follows the successful completion of the previous $250 million share repurchase program in August 2016. Fire broke out at Syngene’s campus Fire broke out at Syngene’s one of research facility at BIocon Park in Bangalore on 12th December 2016. There was no injury or loss of life due to this incident. As per the management, this research facility, including office and lab spaces, makes up ~10% of Syngene’s total infrastructure at Biocon Park. The company further added that all its other facilities within the same campus were unaffected due to this incident and continues to operate normally. Flash fire incident occurred at Aurobindo Pharma’s Vizag unit Flash fire incident occurred on 12th December 2016, in Aurobindo’s API Unit at Srikakulam near Vizag, Andhra Pradesh in which two people died and one critically injured. As per management, there is no material impact on the operational of the company due to this incident. The US Congress passes 21st Century Cures Act The US congress has passed the 21st Century Cures Act, which could ignite innovation and bring drugs and medical devices more quickly to market. The legislation, dubbed 21st Century Cures, provides nearly US$5 billion for the National Institutes of Health to accelerate research into major diseases, including US$1.8 billion project on cancer, and US$500 million for the FDA to make its approval process more efficient.

ICICI Securities Ltd. | Retail Equity Research

Page 6

Exhibit 2: Patent litigations (12 months) [5

Month Innovator ANDA Filer Brand Name API Used for Dec-15 UCB Inc. InvaGen Pharma Zyrtec-D Cetirizine RespiratoryDec-15 Unimed Pharma Dr. Reddy's Labs Androgel Testosterone Low TestosteroneDec-15 Helsinn Healthcare Dr. Reddy's Labs Aloxi Palanosetron NauseaDec-15 Sanofi-Aventis Glenmark Pharma Multaq Dronedarone Atrial FibrillationDec-15 Otsuka Pharma Ajanta Pharma Abilify Aripiprazole SchizophreniaDec-15 Merz Pharma Taro Pharma Naftin Naftifine Hydrochloride Fungal InfectionJan-16 Dow Pharma Taro Pharma Onexton Cindamycin Phosphate and Benzoyl Peroxide AcneJan-16 Cubist Pharma Dr. Reddy's Labs Cubicin Daptomycin AntibioticFeb-16 Bayer Pharma InvaGen Pharma Xarelto Rivaroxaban Blood ThinnerFeb-16 Bristol Myers Squibb Cipla Reyataz Atazanavir HIVFeb-16 Janssen Products LP Lupin Prezista Darunavir HIVMar-16 Shire Canada Lupin Daliresp Roflumilast RespiratoryMar-16 Daiichi Sankyo Torrent Pharma Benicar Olmesartan Anti-depressantApr-16 Daiichi Sankyo Alembic Pharma Benicar Olmesartan Anti-depressantMay-16 Daiichi Sankyo Aurobindo Pharma Benicar Olmesartan Anti-depressantJun-16 Apicore Aurobindo Pharma Lymphazurin isosulfan blue lymphatic imaging agentJun-16 UCB, Inc. Aurobindo Pharma Vimpat lacosamide partial-onset seizuresJun-16 Gilead Aurobindo Pharma Emtriva emtricitabine HIVJun-16 Janssen Biotech Glenmark Pharma Zytiga abiraterone OncologyJun-16 Sanofi-Aventis Cadila Healthcare Mozobil plerixafor non-Hodgkin's lymphomaJul-16 Sanofi-Aventis Cadila Healthcare Mozobil plerixafor non-Hodgkin's lymphomaJul-16 Roche Cadila Aloxi palonosetron hydrochloride prevention of acute nausea Jul-16 AstraZeneca AB Aurobindo Nexium 24HR esomeprazole magnesium treatment of acid refluxJul-16 Hyperion Therapeutics Lupin Ravicti Glycerol Phenylbutyrate urea cycle disordersJul-16 Gilead Sciences, Inc. Aurobindo Truvada emtricitabine / tenofovir disoproxil fumarate HIVAug-16 Lupin InvaGen Pharma Antara fenofibrate hypercholesterolemiaAug-16 Gilead Sciences Inc Hetero Complera Emtricitabine; Rilpivirine Hydrochloride; TenofoHIVAug-16 Shire LLC Alkem Lab Fosrenol lanthanum carbonate end stage renal diseaseAug-16 AbbVie Inc. Amgen Inc. Humira adalimumab immunosuppressantAug-16 Galderma Laboratories, LP SEEGPharm Metrogel metronidazole rosacea Aug-16 Reckitt Benckiser Inc. Sun Pharma Mucinex guaifenesin / pseudoephedrine hydrochloride bronchial congestionAug-16 Takeda Pharma Dexcel Pharma Prevacid lansoprazole stomach ulcersAug-16 Dexcel Aurobindo Prilosec Omeprazole HeartburnAug-16 Shionogi Inc Hi-Tech Pharmacal Ulesfia benzyl alcohol anti-parasiteAug-16 Nestle Skin Health Perrigo Co. Mirvaso brimonidine DermatologySep-16 Pfizer Aurobindo Toviaz fesoterodine fumarate overactive bladderSep-16 Arena Pharma Lupin Belviq lorcaserin weight lossSep-16 Brigham and Women's Hospital InSun Pharma Sensipar cinacalcet hydrochloride hyper parathyroidismSep-16 Brigham and Women's Hospital InStrides Inc. Sensipar cinacalcet hydrochloride hyper parathyroidismSep-16 Brigham and Women's Hospital InCipla Sensipar cinacalcet hydrochloride hyper parathyroidismSep-16 Eli Lilly and Co., ICOS Corp. Cipla Cialis tadalafil erectile dysfunctionSep-16 Brigham and Women's Hospital InAurobindo Sensipar cinacalcet hydrochloride hyper parathyroidismSep-16 Eli Lilly and Co., ICOS Corp. Alembic Pharma Cialis tadalafil erectile dysfunctionOct-16 Amgen Inc. Ajanta Pharma Sensipar cinacalcet calcium reducerOct-16 Amgen Inc. Dr Reddy's Lab Sensipar cinacalcet calcium reducerOct-16 UCB, Inc. Cadila Healthcare Vimpat lacosamide partial-onset seizuresOct-16 Astellas Pharma Lupin Myrbetriq mirabegron overactive bladderOct-16 Astellas Pharma Cadila Healthcare Myrbetriq mirabegron overactive bladderOct-16 Astellas Pharma Aurobindo Pharma Myrbetriq mirabegron overactive bladderOct-16 AstraZeneca AB Glenmark Pharma Nexium 24HR esomeprazole magnesium treatment of acid refluxOct-16 Celgene Corp. Dr Reddy's Lab Revlimid lenalidomide multiple myelomaOct-16 Otsuka Pharma Zydus Pharma Abilify Aripiprazole SchizophreniaOct-16 Onyx Therapeutics Cipla Kyprolis carfilzomib multiple myelomaOct-16 Eli Lilly Cipla Axiron Hypogonadism TestosteroneOct-16 Galderma Lab Sun Pharma Oracea doxycycline infectionsOct-16 Eli Lilly Cipla Axiron Hypogonadism TestosteroneOct-16 Indoco Remedies Zydus Pharma Abilify Aripiprazole SchizophreniaOct-16 Eli Lilly Cipla Axiron Hypogonadism TestosteroneNov-16 Onyx Therapeutics Dr Reddy's Lab Kyprolis carfilzomib multiple myelomaNov-16 Onyx Therapeutics Cadila Kyprolis carfilzomib multiple myelomaNov-16 Indoco Remedies Zydus Pharma Abilify Aripiprazole SchizophreniaNov-16 UCB Inc Cadila Neupro rotigotine ParkinsonNov-16 Amarin Pharma Dr Reddy's Lab Vascepa icosapent ethy hypertri- glyceridemiaNov-16 Medicis Pharma Dr Reddy's Lab Solodyn minocycline infections

Source: Bloomberg, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 7

IPM grew 15% in November; Chronic drives growth • The Indian pharmaceutical market (IPM) grew 15.3% YoY to | 9388

crore for the month of November. Higher growth was attributable to low base (9.8% in Nov 2015) and high double digit growth in chronic segment.

• The growth was driven by volumes increase – 9.6%, new product launches – 3.5% and price hikes- 2.2%.

• The (Fixed dosage combination) FDCs related market de-grew 30%, impacted ~ 1% to the overall growth.

• Drugs under NLEM list decreased 1.8% to |1005 crore while non-NLEM drugs posted a growth of 17.7% to | 7965 crore. Volume growth in NLEM and Non-NLEM was 10.0% and 5.4% respectively.

• Among companies under I-Direct coverage, Natco, Unichem, Torrent, Sun, Glenmark, Lupin, and Cadila have registered a strong growth of 23.6%, 21.8%, 20.9%, 20.1%, 19.9%, 17.3% and 16.0% respectively.

• Therapy wise, 10 therapies have outpaced the IPM growth. Notable among them with growth rates- Respiratory —31.5%, Anti-diabetic —14.5%, Cardiac – 21.2% and Gynaecology– 21.1%.

• In all, 177 new brands were launched in Nov-16. • On a MAT basis, IPM growth stood at 10.8% YoY to | 107000 crore. • Domestic companies have grown 15.1%, while MNC companies have

grown 16.0% in Nov-2016. Exhibit 3: Domestic formulations - growth trend [

14.5

14.3

13.0

11.5

14.0

11.9 11

.7

11.0 20 11

.3

12.3

11.7

-5

0

5

10

15

20

25

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 4: Companies growth in domestic market in Nov, 2016

8.810.7

12.2

3.1

14.517.9

14.4 11.7 14.314.5

-0.8

10.3

15.211.3 12.2

6.7

-5

0

5

10

15

20

Aja

nta

Ale

mbi

c

Bioc

on

Cadi

la

Cipl

a

DRL

Glen

mar

k

GSK

Phar

ma

Indo

co

Ipca

Lab

s

Lupi

n

Nov

artis

Pfize

r

Sun

Phar

ma

Torre

nt

Unic

hem

(%)

Source: AIOCD data base, ICICIdirect.com Research

Therapy wise performance (| crore) Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)Anti-Infectives 1152 1141 1.0 1307 -11.9Cardiac 950 784 21.2 904 5.1GI 754 658 14.6 778 -3.1Vitamins 613 557 10.0 603 1.6Anti Diabetic 482 421 14.5 480 0.3Respiratory 515 392 31.5 472 9.2Pain 445 372 19.7 455 -2.2Neuro 440 397 10.9 471 -6.6Derma 371 325 14.3 367 1.3Gynaecological 238 197 21.1 242 -1.4Anti-Neoplastics 158 98 61.2 163 -3.0Ophthal 133 122 9.4 138 -3.4Vaccines 112 95 18.0 116 -3.6Hormones 91 83 10.3 93 -1.9Others 83 65 26.8 79 4.8Blood Related 54 42 27.9 61 -11.5Urology 55 33 67.7 59 -6.1Sex Stimulants 35 41 -14.3 55 -36.7Anti Malarials 35 37 -4.2 37 -3.9Stomatologicals 22 20 10.2 23 -4.6 Source: AIOCD data base

Top brands in Indian pharma market Brand Company Therapy Nov' 16 Nov' 15 Gr. (%)Spasmo Prox Wockhardt GI 331.8 289.2 14.8Lantus Sanofi Anti Diabetic 329.3 249.9 31.8Galvus Met Novartis Anti Diabetic 312.3 238.6 30.9Corex Pfizer Respiratory 290.8 291.4 -0.2Augmentin GSK Anti-Infectives 290.6 324.8 -10.5Clavam Alkem Anti-Infectives 274.3 230.4 19.0Volini Sun Pain 245.5 208.3 17.9Pan Sun Pharma GI 231.5 183.6 26.1Becosules Pfizer Vitamins 222.1 248.8 -10.8Voveran Novartis Pain 216.7 170.0 27.5

Source: AIOCD data base Industry acute to chronic therapy ratio percentage…

Acute, 51543, 48.3%

Chronic, 33624, 31.5%

Sub-Chronic, 21634, 20.3%

Source: AIOCD data base; As per AIOCD MAT Nov 2016

ICICI Securities Ltd. | Retail Equity Research

Page 8

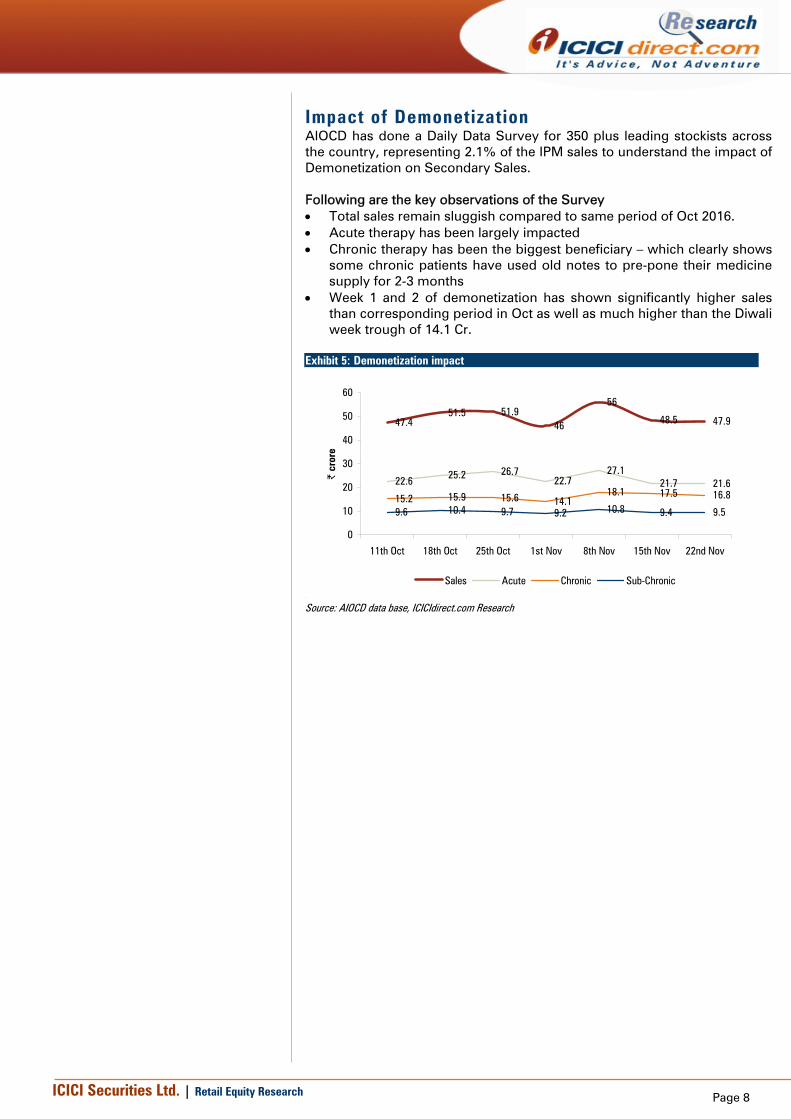

Impact of Demonetization AIOCD has done a Daily Data Survey for 350 plus leading stockists across the country, representing 2.1% of the IPM sales to understand the impact of Demonetization on Secondary Sales. Following are the key observations of the Survey • Total sales remain sluggish compared to same period of Oct 2016. • Acute therapy has been largely impacted • Chronic therapy has been the biggest beneficiary – which clearly shows

some chronic patients have used old notes to pre-pone their medicine supply for 2-3 months

• Week 1 and 2 of demonetization has shown significantly higher sales than corresponding period in Oct as well as much higher than the Diwali week trough of 14.1 Cr.

Exhibit 5: Demonetization impact

[

47.451.5 51.9

46

56

48.5 47.9

22.6 25.2 26.722.7

27.121.7 21.6

15.2 15.9 15.6 14.118.1 17.5 16.8

9.6 10.4 9.7 9.2 10.8 9.4 9.5

0

10

20

30

40

50

60

11th Oct 18th Oct 25th Oct 1st Nov 8th Nov 15th Nov 22nd Nov

| cr

ore

Sales Acute Chronic Sub-Chronic

Source: AIOCD data base, ICICIdirect.com Research

ICICI Securities Ltd. | Retail Equity Research

Page 9

Sun Pharmaceuticals

507090

110130150

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Sun Pharma

Source: NSE, ICICIdirect.com Research Exhibit 6: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

14.4

14.1

14.8

14.5

13.2

12.2

10.4

9.6

10.4

10.8 12.024

.8

12.2

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Sun Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 7: Market share in Indian formulations market

8.6 8.6 8.6 8.6 8.6 8.6 8.6 8.6 8.6 8.78.6 8.6 8.7

6.06.57.07.58.08.59.09.5

10.0

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Sun Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 8: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Volini Pain 21.6 21.3 1.4 22.8 -5.1

Rosuvas Cardiac 18.5 12.9 43.7 17.1 8.0

Istamet Anti Diabetic 19.0 12.2 56.0 17.1 10.7

Gemer Anti Diabetic 18.6 12.7 46.3 17.0 8.9

Levipil Neuro 15.6 12.3 26.6 14.5 7.4

Susten Gynaecological 12.4 11.3 9.7 12.1 2.6

Revital H Vitamins 13.9 9.2 51.3 12.4 11.9

Pantocid Gastro Intestinal 12.9 11.1 15.7 9.7 32.4

Pantocid Dsr Gastro Intestinal 11.3 9.4 19.5 11.0 1.9

Storvas Cardiac 9.3 9.4 -1.1 8.5 9.5

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 9: Contribution of therapies to domestic sales (MAT Nov’16)

z

Cardiac29%

Neuro 27%

Gastro Intestinal

19%

Anti-Infectives17%

Derma8%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 10: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Cardiac 163.4 124.1 31.7 151.4 7.9

Neuro 145.7 121.1 20.3 145.0 0.4

Gastro Intestinal 94.9 80.5 18.0 92.3 2.8

Anti-Infectives 82.6 86.0 -3.9 88.4 -6.5

Derma 45.2 32.0 41.1 76.5 -40.9

Anti Diabetic 82.2 62.3 31.8 61.7 33.2

Vitamins 33.9 26.3 28.9 42.4 -20.1

Pain 59.3 53.5 10.8 33.3 77.8

Gynaecological 29.3 27.6 5.9 35.2 -16.8

Respiratory 36.5 29.0 25.6 27.7 31.8

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 3737, 40.3%

Chronic, 4270, 46.0%

Sub-Chronic,

1273, 13.7%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

18%

9%

7%

10%

56%

Top 10 11 to 20 21 to 30 31 to 50 Others

ICICI Securities Ltd. | Retail Equity Research

Page 10

Cipla

Stock Performance

6080

100120140

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Cipla

Source: NSE, ICICIdirect.com Research

Exhibit 11: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

33.6

16.4

16.1

15.1

13.4

11.3

10.5

9.9

10.7

11.4

11.9

12.5

11.7

0

5

10

15

20

25

30

35

40

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Cipla

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 12: Market share in Indian formulations market

4.9 4.9 4.9 4.9 4.9 4.9 4.9 4.9 4.9 4.9 4.9 4.9 4.9

4.0

4.2

4.4

4.6

4.8

5.0

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Cipla

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 13: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Foracort Respiratory 20.8 17.9 16.3 18.7 11.4

Budecort Respiratory 12.2 14.0 -13.1 12.8 -4.8

Duolin Respiratory 17.0 10.5 61.5 14.3 18.7

Asthalin Respiratory 13.6 13.2 3.1 13.0 5.1

Seroflo Respiratory 14.6 11.8 24.0 12.8 13.8

Aerocort Respiratory 9.3 8.4 11.0 8.7 7.5

Montair Lc Respiratory 10.4 8.0 29.0 8.7 18.8

Azee Anti-Infectives 7.3 8.6 -14.4 6.9 6.7

Dytor Cardiac 7.4 5.4 36.3 7.0 4.7

Novamox Anti-Infectives 6.6 8.6 -23.9 6.5 1.8

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 14: Contribution of therapies to domestic sales (MAT Nov’16)

Respiratory31%

Anti-Infectives26%Cardiac

12%

Gastro Intestinal

8%

Urology5%

Other18%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 15: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (% )

Respiratory 155.3 134.0 1 5.9 146.4 6.1

Ant i- Infectives 105.3 111.8 -5.8 111.8 -5.8

Cardiac 58.1 45.8 2 6.8 55.3 5.0

Gastro Intest inal 31.2 29.1 7.3 34.3 -9.0

Urology 24.0 18.1 3 2.4 21.9 9.3

Neuro 15.0 13.8 8.3 14.5 3.0

Ophthal 14.4 12.5 1 5.8 14.3 1.1

Pain 13.7 12.7 7.6 16.0 -14.5

Derma 11.5 9.7 1 8.7 11.8 -2.5

V itamins 8.1 6.9 1 6.4 7.7 4.9

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 2441, 46.6%

Chronic, 2120, 40.5%

Sub-Chronic,

675, 12.9%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

24%

12%

8%12%

44%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 11

Dr. Reddy’s Labs

Stock Performance) Stock Performance

6080

100120140

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Dr. Reddys

Source: NSE, ICICIdirect.com Research Exhibit 16: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

33.7

19.4 20.7 22.0

20.5

18.2

17.2

14.3

15.3

14.1

14.3

15.7

16.4

0

5

10

15

20

25

30

35

40

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Dr. Reddys Lab

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 17: Market share in Indian formulations market

2.3 2.3 2.4 2.4 2.4 2.4 2.4 2.4 2.3 2.3 2.4 2.42.3

0.6

1.1

1.6

2.1

2.6

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Dr. Reddys Lab

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 18: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Omez Gastro Intestinal 8.9 11.4 -22.5 9.0 -1.5

Omez D Gastro Intestinal 9.3 9.1 2.2 9.5 -2.1

Econorm Gastro Intestinal 4.3 4.7 -8.1 3.4 27.2

Nise Pain 5.1 5.8 -11.9 5.2 -1.9

Stamlo Cardiac 5.4 5.7 -5.3 4.6 17.0

Grafeel Anti-Neoplastics 1.9 8.3 -76.9 4.1 -52.9

Razo D Gastro Intestinal 5.1 4.3 17.7 4.7 9.2

Atarax Respiratory 5.5 3.9 38.5 6.2 -11.2

Razo Gastro Intestinal 5.1 3.6 39.5 4.7 7.9

Reditux Anti-Neoplastics 5.1 3.9 30.6 6.7 -22.9

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 19: Contribution of therapies to domestic sales (MAT Nov’16)

Gastro Intestinal

21%

Cardiac14%

Anti-Neoplastics

13%Respiratory9%

Anti-Infectives8%

Other35%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 20: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Gastro Intestinal 42.5 41.9 1.4 41.6 2.0

Cardiac 29.9 28.6 4.4 27.2 10.1

Anti-Neoplastics 30.6 25.0 22.5 36.3 -15.7

Respiratory 21.3 19.2 10.8 21.1 1.0

Anti-Infectives 15.9 17.8 -10.7 18.2 -12.9

Pain 13.7 13.7 0.2 14.1 -2.4

Anti Diabetic 14.6 13.3 9.5 13.0 12.4

Derma 13.2 13.9 -4.7 11.2 17.9

Urology 8.3 8.1 2.8 7.7 7.3

Neuro 7.4 7.1 4.6 7.1 4.1

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 1268, 50.8%

Chronic, 711, 28.5%

Sub-Chronic,

518, 20.7%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

28%

16%

10%

13%

33%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 12

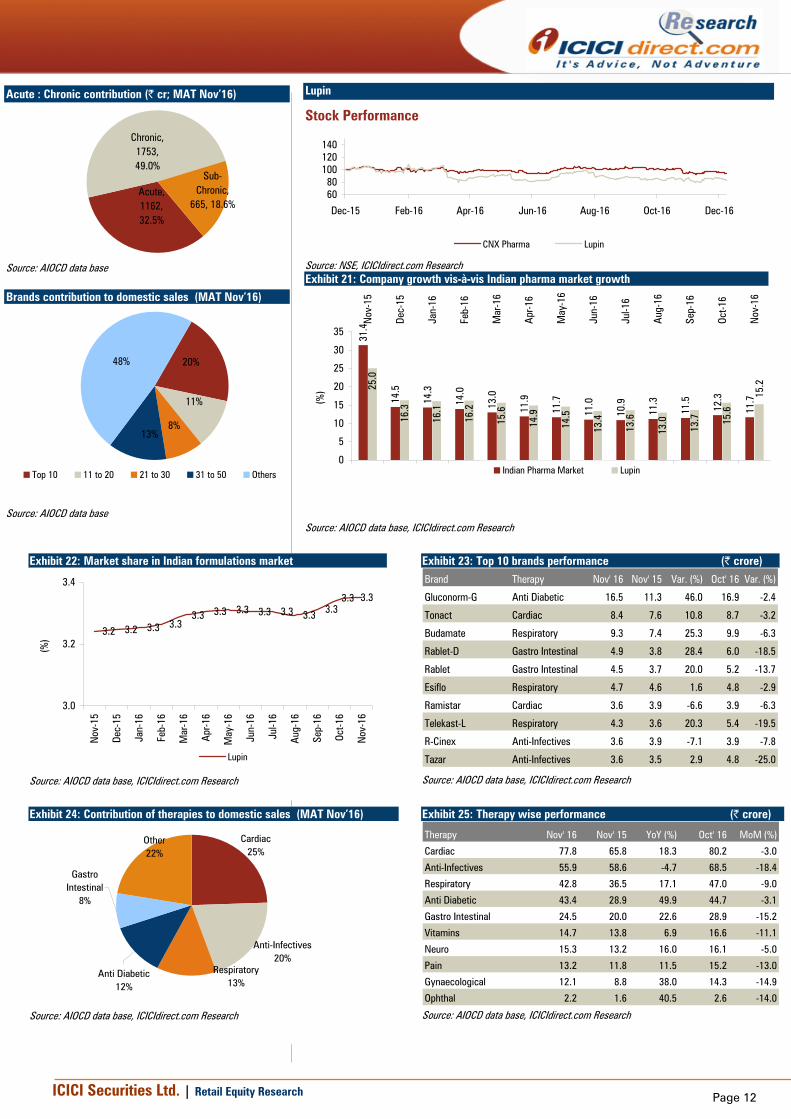

Lupin

Stock Performance

6080

100120140

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Lupin

Source: NSE, ICICIdirect.com Research

Exhibit 21: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

25.0

16.3

16.1

16.2

15.6

14.9

14.5

13.4

13.6

13.0

13.7 15

.6

15.2

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Lupin

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 22: Market share in Indian formulations market

3.2 3.2 3.3 3.33.3 3.3 3.3 3.3 3.3 3.3 3.3

3.33.3

3.0

3.2

3.4

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Lupin

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 23: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Gluconorm-G Anti Diabetic 16.5 11.3 46.0 16.9 -2.4

Tonact Cardiac 8.4 7.6 10.8 8.7 -3.2

Budamate Respiratory 9.3 7.4 25.3 9.9 -6.3

Rablet-D Gastro Intestinal 4.9 3.8 28.4 6.0 -18.5

Rablet Gastro Intestinal 4.5 3.7 20.0 5.2 -13.7

Esiflo Respiratory 4.7 4.6 1.6 4.8 -2.9

Ramistar Cardiac 3.6 3.9 -6.6 3.9 -6.3

Telekast-L Respiratory 4.3 3.6 20.3 5.4 -19.5

R-Cinex Anti-Infectives 3.6 3.9 -7.1 3.9 -7.8

Tazar Anti-Infectives 3.6 3.5 2.9 4.8 -25.0

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 24: Contribution of therapies to domestic sales (MAT Nov’16)

Cardiac25%

Anti-Infectives20%

Respiratory13%

Anti Diabetic12%

Gastro Intestinal

8%

Other22%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 25: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Cardiac 77.8 65.8 18.3 80.2 -3.0

Anti-Infectives 55.9 58.6 -4.7 68.5 -18.4

Respiratory 42.8 36.5 17.1 47.0 -9.0

Anti Diabetic 43.4 28.9 49.9 44.7 -3.1

Gastro Intestinal 24.5 20.0 22.6 28.9 -15.2

Vitamins 14.7 13.8 6.9 16.6 -11.1

Neuro 15.3 13.2 16.0 16.1 -5.0

Pain 13.2 11.8 11.5 15.2 -13.0

Gynaecological 12.1 8.8 38.0 14.3 -14.9

Ophthal 2.2 1.6 40.5 2.6 -14.0

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 1162, 32.5%

Chronic, 1753, 49.0%

Sub-Chronic,

665, 18.6%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

20%

11%

8%13%

48%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 13

Cadila Healthcare

Stock Performance

6080

100120140

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Cadila Healthcare

Source: NSE, ICICIdirect.com Research Exhibit 26: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

35.1

11.3

11.7

12.0

11.6

11.0

10.9

10.2

9.7

9.5 9.

8

11.1

10.7

0

5

10

15

20

25

30

35

40

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Cadila Healthcare

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 27: Market share in Indian formulations market

4.2 4.2 4.2 4.2 4.2 4.2 4.2 4.2 4.2 4.1 4.1 4.24.2

3.0

3.4

3.8

4.2

4.6

5.0

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Cadila Healthcare

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 28: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Skinlite Derma 14.0 13.2 5.9 15.1 -7.4

Atorva Cardiac 9.7 11.3 -14.2 8.5 13.3

Mifegest Kit Gynaecological 8.5 8.3 2.8 4.5 89.6

Deriphyllin Respiratory 12.0 8.7 38.6 10.0 20.7

Pantodac Gastro Intestinal 9.0 8.2 10.3 9.8 -7.9

Zyrop Blood Related 5.6 4.2 34.3 10.9 -48.7

Aten Cardiac 4.8 5.4 -10.8 5.1 -6.5

Amlodac Cardiac 5.1 5.4 -5.7 5.1 -0.9

Thrombophob Pain 5.4 4.8 13.5 6.1 -11.5

Sovihep Anti-Infectives 7.3 2.6 178.9 6.9 7.1

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 29: Contribution of therapies to domestic sales (MAT Nov’16)

Other39%

Gynaecological10%

Respiratory10%

Gastro Intestinal

12%

Anti-Infectives14%

Cardiac15%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 30: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Cardiac 57.2 51.9 10.3 55.9 2.3

Anti-Infectives 56.6 48.1 17.7 63.7 -11.2

Gastro Intestinal 44.5 41.4 7.5 46.4 -4.0

Respiratory 45.1 36.7 23.0 40.9 10.1

Gynaecological 34.5 33.1 4.1 31.6 9.0

Pain 37.0 29.6 25.1 38.2 -3.1

Derma 28.3 25.4 11.2 29.8 -5.0

Anti-Neoplastics 26.7 14.9 79.0 34.0 -21.5

Vitamins 16.5 13.2 24.9 17.1 -3.6

Hormones 8.2 7.0 17.2 8.9 -7.6

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 1162, 32.5%

Chronic, 1753, 49.0%

Sub-Chronic,

665, 18.6%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

20%

11%

8%13%

48%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 14

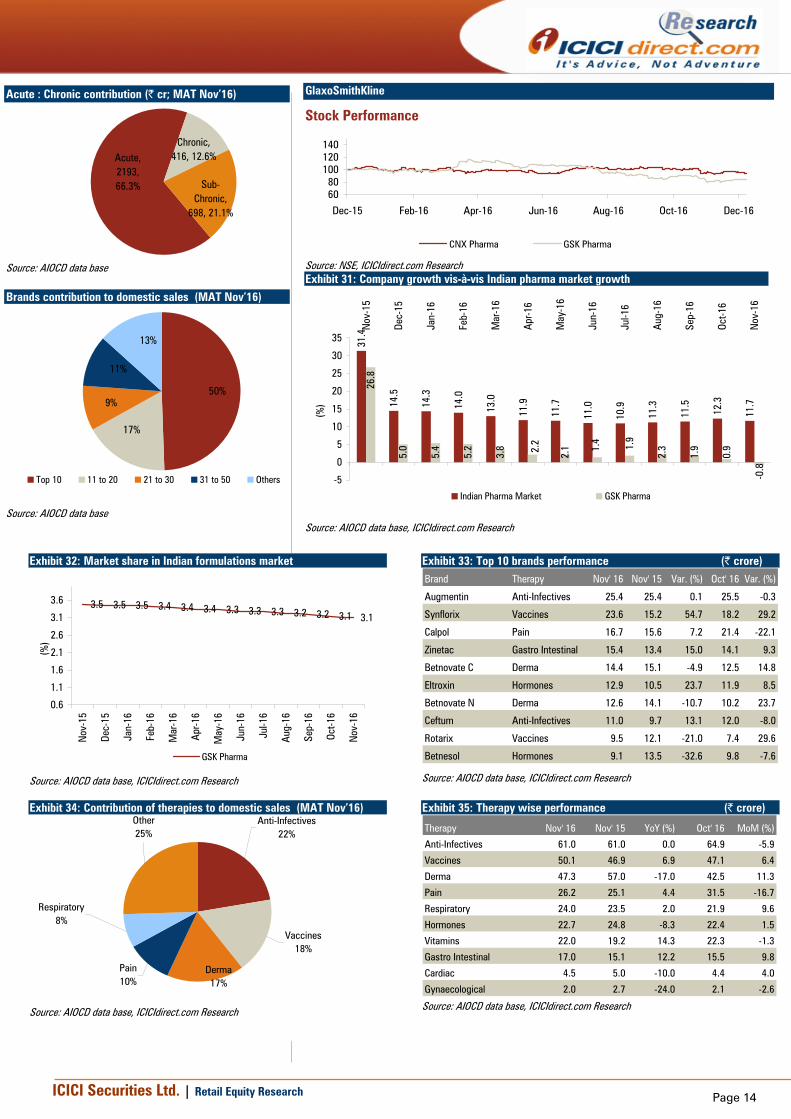

GlaxoSmithKline

Stock Performance

6080

100120140

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma GSK Pharma

Source: NSE, ICICIdirect.com Research

Exhibit 31: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

26.8

5.0

5.4

5.2

3.8

2.1

2.3

1.9

0.92.

2 1.4 1.9

-0.8

-5

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market GSK Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 32: Market share in Indian formulations market

3.5 3.5 3.5 3.4 3.4 3.4 3.3 3.3 3.3 3.2 3.2 3.1 3.1

0.6

1.1

1.6

2.1

2.6

3.1

3.6

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

GSK Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 33: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Augmentin Anti-Infectives 25.4 25.4 0.1 25.5 -0.3

Synflorix Vaccines 23.6 15.2 54.7 18.2 29.2

Calpol Pain 16.7 15.6 7.2 21.4 -22.1

Zinetac Gastro Intestinal 15.4 13.4 15.0 14.1 9.3

Betnovate C Derma 14.4 15.1 -4.9 12.5 14.8

Eltroxin Hormones 12.9 10.5 23.7 11.9 8.5

Betnovate N Derma 12.6 14.1 -10.7 10.2 23.7

Ceftum Anti-Infectives 11.0 9.7 13.1 12.0 -8.0

Rotarix Vaccines 9.5 12.1 -21.0 7.4 29.6

Betnesol Hormones 9.1 13.5 -32.6 9.8 -7.6

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 34: Contribution of therapies to domestic sales (MAT Nov’16) Anti-Infectives

22%

Vaccines18%

Derma17%

Pain 10%

Respiratory8%

Other25%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 35: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Anti-Infectives 61.0 61.0 0.0 64.9 -5.9

Vaccines 50.1 46.9 6.9 47.1 6.4

Derma 47.3 57.0 -17.0 42.5 11.3

Pain 26.2 25.1 4.4 31.5 -16.7

Respiratory 24.0 23.5 2.0 21.9 9.6

Hormones 22.7 24.8 -8.3 22.4 1.5

Vitamins 22.0 19.2 14.3 22.3 -1.3

Gastro Intestinal 17.0 15.1 12.2 15.5 9.8

Cardiac 4.5 5.0 -10.0 4.4 4.0

Gynaecological 2.0 2.7 -24.0 2.1 -2.6

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 2193, 66.3%

Chronic, 416, 12.6%

Sub-Chronic,

698, 21.1%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

50%

17%

9%

11%

13%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 15

Wockhardt

Stock Performance

050

100150200250300350400

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Wockhardt

Source: NSE, ICICIdirect.com Research Exhibit 36: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

32.9

20.4

19.1

17.5

7.8

15.3

12.5

10.3

6.6

6.1

5.6 6.6

6.7

0

5

10

15

20

25

30

35N

ov-1

5

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Wockhardt

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 37: Market share in Indian formulations market

2.32.3 2.3 2.3 2.3

2.32.3

2.22.2 2.2 2.2 2.2 2.2

2.12.22.22.22.22.22.32.32.32.32.3

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Wockhardt

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 38: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Spasmo Proxyvon PluGastro Intestinal 40.1 28.9 38.4 31.8 26.0

Practin Vitamins 6.5 6.0 8.4 6.8 -3.7

Tryptomer Neuro 5.3 4.6 15.4 4.2 24.5

Bro Zedex Respiratory 5.1 5.4 -5.3 4.6 12.5

Methycobal Vitamins 4.3 3.4 28.6 4.2 4.0

Zedex Respiratory 4.2 4.0 4.1 3.9 8.3

Biovac V Vaccines 3.2 3.3 -3.5 3.5 -9.6

Biovac A Vaccines 4.2 2.8 51.2 4.4 -2.5

Wosulin Anti Diabetic 2.4 2.1 14.1 2.7 -8.5

Ace Proxyvon Pain 2.0 2.8 -29.8 2.2 -9.6

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 39: Contribution of therapies to domestic sales (MAT Nov’16)

Other33%

Anti Diabetic7% Neuro

8%

Respiratory12%

Vitamins 15%

Gastro Intestinal

25%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 40: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Gastro Intestinal 41.8 30.1 38.9 33.5 25.1

Vitamins 16.6 15.0 10.7 17.0 -2.4

Respiratory 17.5 16.8 4.4 16.8 4.1

Neuro 9.3 7.8 19.4 8.5 9.4

Anti Diabetic 7.8 7.2 8.2 7.4 5.2

Anti-Infectives 7.5 8.0 -6.9 9.1 -17.9

Derma 7.5 6.9 8.6 8.0 -6.1

Pain 6.0 6.9 -13.5 6.4 -6.1

Vaccines 8.2 6.1 34.9 8.5 -3.0

Hormones 2.5 2.2 14.2 3.4 -25.8

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Sub-Chronic

152, 11.1%

Chronic, 283,

20.6%Acute, 943,

68.4%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

55%

15%

8%

8%

14%

Top 10 11 to 20 21 to 30 31 to 50 Others

ICICI Securities Ltd. | Retail Equity Research

Page 16

Glenmark Pharmaceuticals

Stock Performance

6080

100120140160180200

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Glenmark

Source: NSE, ICICIdirect.com Research

Exhibit 41: Company growth vis-à-vis Indian pharma market growth

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3 12.3

26.8

25.4

24.9

24.5

23.4

21.5

19.8

17.7

15.9

15.5

15.4

16.2

14.511

.5

11.7

-4

4

12

20

28

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Glenmark Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 42: Market share in Indian formulations market

2.32.3

2.42.4

2.42.4 2.4 2.4 2.4

2.4 2.4 2.42.4

2.32.32.32.32.32.42.42.42.42.42.4

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Glenmark Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 43: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Telma Cardiac 15.1 13.9 8.9 13.1 15.8

Telma H Cardiac 15.5 10.9 42.5 12.8 21.0

Ascoril Plus Respiratory 11.4 10.1 13.0 11.1 3.4

Candid Derma 7.1 6.3 12.3 9.2 -22.7

Candid-B Derma 8.0 7.3 10.0 9.7 -17.6

Telma Am Cardiac 7.8 6.0 28.3 6.8 14.1

Ascoril Ls Respiratory 5.4 5.3 1.2 5.5 -3.1

Onabet Derma 4.1 3.0 34.7 4.7 -13.0

Zitamet Plus Anti Diabetic 4.0 0.8 392.0 3.7 8.2

Zita Plus Anti Diabetic 3.0 2.7 8.6 2.8 4.0

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 44: Contribution of therapies to domestic sales (MAT Nov’16) Derma29%

Cardiac22%

Respiratory16%

Anti-Infectives13%

Anti Diabetic7%

Other13%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 45: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Derma 63.5 53.8 18.0 67.1 -5.5

Cardiac 53.7 41.9 28.3 46.4 15.9

Respiratory 41.4 36.6 13.0 39.1 5.7

Anti-Infectives 30.6 26.6 14.9 34.8 -12.0

Anti Diabetic 14.7 17.7 -16.8 13.9 5.4

Gastro Intestinal 8.6 4.3 97.3 8.6 -0.6

Vitamins 5.1 4.7 8.7 5.0 1.8

Gynaecological 6.8 4.1 65.3 6.6 3.0

Pain 4.0 4.0 2.0 4.2 -4.1

Ophthal 2.9 3.1 -8.4 3.3 -12.4

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 1044, 40.9%

Chronic, 912, 35.7%

Sub-Chronic,

596, 23.4%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

36%

12%9%

13%

30%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 17

Torrent Pharmaceuticals

Stock Performance

4080

120160200

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Torrent Pharma

Source: NSE, ICICIdirect.com Research Exhibit 46: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

32.9

17.5

7.8

20.4

19.1 15

.3

12.5

10.3

6.6

6.1

5.6 6.6

6.7

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Torrent Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 47: Market share in Indian formulations market

2.3 2.3 2.3 2.3 2.3 2.3 2.3 2.2 2.2 2.2 2.2 2.22.2

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Torrent Pharma

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 48: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Shelcal Vitamins 18.7 12.8 45.8 17.8 4.5

Chymoral Forte Pain 11.1 7.9 40.6 11.1 0.0

Nikoran Cardiac 8.8 6.7 31.6 8.0 10.0

Dilzem Cardiac 6.1 4.7 28.0 5.5 10.2

Nebicard Cardiac 6.5 4.9 32.6 5.9 9.9

Azulix-Mf Anti Diabetic 6.6 4.5 45.8 5.5 19.2

Nexpro Rd Gastro Intestinal 5.6 4.2 31.9 5.6 -0.1

Shelcal Ct Vitamins 4.9 3.4 43.2 4.5 7.9

Nexpro Gastro Intestinal 4.7 3.7 27.9 4.8 -0.6

Alprax Neuro 3.1 3.2 -3.4 3.6 -12.5

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 49: Contribution of therapies to domestic sales (MAT Nov’16) Cardiac

29%

Neuro 16%Vitamins

16%

Gastro Intestinal

15%

Pain 8%

Other16%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 50: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Cardiac 62.3 52.0 19.9 58.8 6.0

Neuro 33.6 29.9 12.3 33.7 -0.4

Vitamins 36.6 26.1 40.1 34.1 7.5

Gastro Intestinal 29.7 25.5 16.1 30.3 -2.1

Pain 17.6 13.1 34.4 17.7 -0.7

Anti Diabetic 14.5 10.9 33.2 13.3 9.5

Anti-Infectives 6.8 8.2 -17.3 7.7 -12.7

Derma 6.9 4.8 42.8 6.8 1.4

Gynaecological 2.8 3.1 -9.1 2.8 1.6

Urology 0.9 0.8 20.3 1.0 -5.2

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 561, 23.6%

Chronic, 1210, 50.9% Sub-

Chronic, 604, 25.4%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

33%

14%9%

12%

32%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 18

Ipca Laboratories

Stock Performance

5075

100125150

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Ipca

Source: NSE, ICICIdirect.com Research Exhibit 51: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

28.7

9.1

7.9

6.6

5.9

5.0 5.9 6.7 8.

4 11.1

11.6

10.3

10.7

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Ipca Lab

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 52: Market share in Indian formulations market

1.3 1.3 1.3 1.3 1.3 1.3 1.3 1.3 1.3 1.3 1.3 1.3 1.3

0.0

0.5

1.0

1.5

2.0

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Ipca Lab

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 53: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Zerodol Sp Pain 8.3 7.3 14.6 8.7 -4.6

Zerodol P Pain 5.4 4.9 8.8 6.6 -18.8

Hcqs Anti Malarials 5.8 4.8 20.5 5.6 4.4

Larinate Anti Malarials 4.6 5.2 -10.5 7.7 -39.6

Rapither-Ab Anti Malarials 3.1 3.3 -5.2 6.0 -48.8

Lariago Anti Malarials 2.4 2.9 -16.9 4.1 -40.9

Glycinorm M Anti Diabetic 3.4 2.9 18.1 3.3 4.3

Folitrax Anti-Neoplastics 2.6 2.4 5.6 2.7 -4.7

Lumerax Anti Malarials 2.3 2.5 -7.5 4.3 -46.5

Zerodol Pain 2.2 2.3 -5.7 2.5 -12.3

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 54: Contribution of therapies to domestic sales (MAT Nov’16) Other24%

Anti-Infectives6%

Gastro Intestinal

8% Cardiac17%

Anti Malarials20%

Pain 25%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 55: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Pain 27.6 25.3 9.0 31.5 -12.3

Anti Malarials 20.2 21.7 -6.9 31.2 -35.3

Cardiac 18.8 17.5 7.5 18.3 2.7

Gastro Intestinal 7.6 7.4 2.7 8.6 -11.0

Anti-Infectives 7.1 5.9 20.1 8.4 -15.3

Anti Diabetic 6.0 5.3 13.0 5.9 2.2

Anti-Neoplastics 4.6 3.7 25.0 4.7 -2.0

Respiratory 5.2 4.9 5.8 5.3 -1.9

Neuro 5.0 3.2 57.1 4.9 3.7

Derma 4.4 3.0 45.5 4.3 1.9

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 893, 66.3%

Chronic, 366, 27.2%

Sub-Chronic, 89,

6.6%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

37%

16%11%

13%

23%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 19

Biocon

Stock Performance

60100140180220

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16CNX Pharma Biocon

Source: NSE, ICICIdirect.com Research

Exhibit 56: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

24.9

6.4

5.4

5.1

5.4

5.1 5.5

5.4

8.8

7.6

7.3

5.4

5.0

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Biocon

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 57: Market share in Indian formulations market

0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.3 0.30.3

0.0

0.2

0.4

0.6

0.8

1.0

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Biocon

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 58: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Insugen Anti Diabetic 7.8 7.1 10.4 7.2 8.4

Basalog Anti Diabetic 5.6 4.9 15.5 5.1 10.2

Erypro Blood Related 4.7 1.2 304.3 3.9 20.6

Canmab Anti-Neoplastics 2.5 0.8 230.1 1.3 85.6

Abraxane Anti-Neoplastics 0.3 0.3 -1.0 1.0 -67.1

Insugen R Anti Diabetic 1.5 1.4 3.4 1.7 -15.1

Blisto Mf Anti Diabetic 1.4 1.5 -11.2 1.1 21.9

Biomab Egfr Anti-Neoplastics 0.6 0.5 14.0 0.3 97.1

Psorid Anti-Neoplastics 0.7 0.8 -11.9 0.9 -20.9

Insugen N Anti Diabetic 0.6 0.7 -13.0 0.6 4.0

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 59: Contribution of therapies to domestic sales (MAT Nov’16)

Other 4%

Derma3%Cardiac

5%Blood Related

9%

Anti-Neoplastics

22%

Anti Diabetic57%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 60: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Anti Diabetic 18.0 16.8 6.9 16.8 7.2

Anti-Neoplastics 5.9 4.1 42.7 5.4 9.0

Blood Related 4.9 1.2 309.9 4.1 18.7

Cardiac 1.4 1.4 0.1 1.4 2.2

Derma 0.8 0.9 -9.7 0.8 3.7

Anti-Infectives 1.0 0.7 47.8 0.7 43.4

Others 0.2 0.2 -13.4 0.2 -5.7

Gastro Intestinal 0.2 0.3 -4.7 0.1 94.9

Vitamins 0.1 0.1 -10.9 0.1 29.9

Pain 0.1 0.1 12.6 0.1 12.1

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 74, 20.8%

Chronic, 252, 70.9%

Sub-Chronic, 30,

8.3%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

79%10%

5%

5%

1%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 20

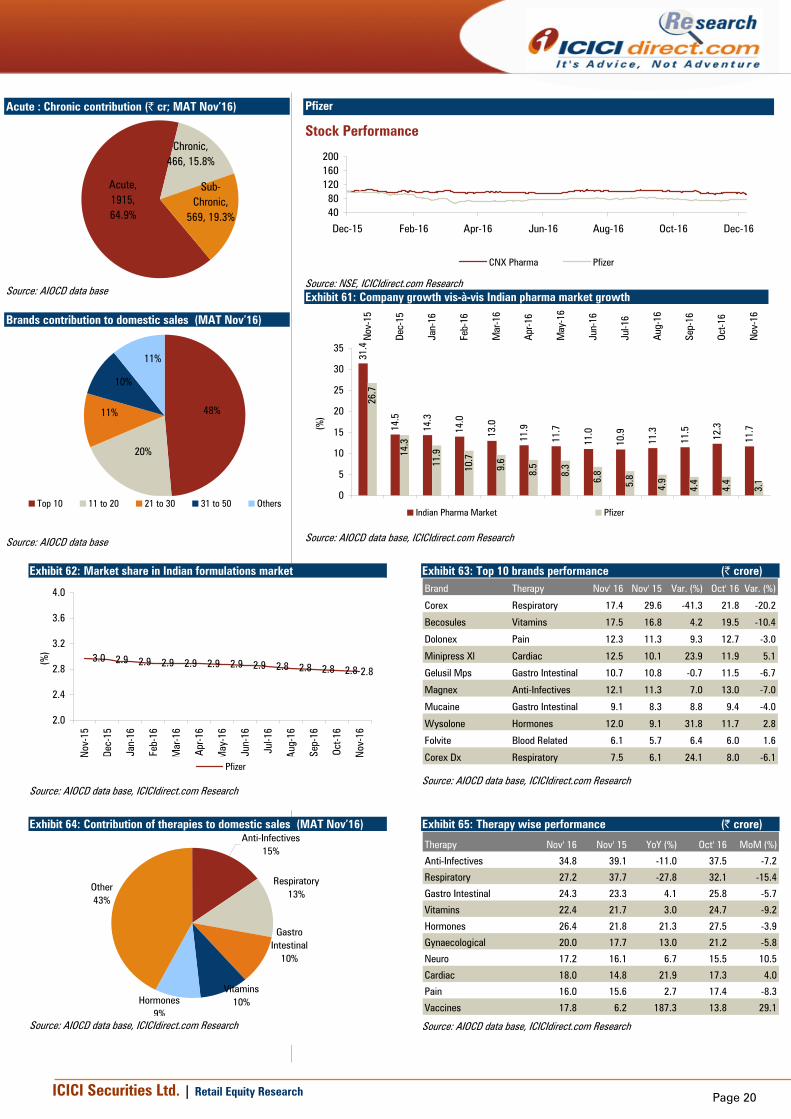

Pfizer

Stock Performance

4080

120160200

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Pfizer

Source: NSE, ICICIdirect.com Research Exhibit 61: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

26.7

14.3

11.9

10.7

9.6

8.5

8.3

6.8

5.8

4.9

4.4

4.4

3.1

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Pfizer

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 62: Market share in Indian formulations market

3.0 2.9 2.9 2.9 2.9 2.9 2.9 2.9 2.8 2.8 2.8 2.8 2.8

2.0

2.4

2.8

3.2

3.6

4.0

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Pfizer

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 63: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Corex Respiratory 17.4 29.6 -41.3 21.8 -20.2

Becosules Vitamins 17.5 16.8 4.2 19.5 -10.4

Dolonex Pain 12.3 11.3 9.3 12.7 -3.0

Minipress Xl Cardiac 12.5 10.1 23.9 11.9 5.1

Gelusil Mps Gastro Intestinal 10.7 10.8 -0.7 11.5 -6.7

Magnex Anti-Infectives 12.1 11.3 7.0 13.0 -7.0

Mucaine Gastro Intestinal 9.1 8.3 8.8 9.4 -4.0

Wysolone Hormones 12.0 9.1 31.8 11.7 2.8

Folvite Blood Related 6.1 5.7 6.4 6.0 1.6

Corex Dx Respiratory 7.5 6.1 24.1 8.0 -6.1

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 64: Contribution of therapies to domestic sales (MAT Nov’16)

Other43%

Hormones9%

Vitamins 10%

Gastro Intestinal

10%

Respiratory13%

Anti-Infectives15%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 65: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Anti-Infectives 34.8 39.1 -11.0 37.5 -7.2

Respiratory 27.2 37.7 -27.8 32.1 -15.4

Gastro Intestinal 24.3 23.3 4.1 25.8 -5.7

Vitamins 22.4 21.7 3.0 24.7 -9.2

Hormones 26.4 21.8 21.3 27.5 -3.9

Gynaecological 20.0 17.7 13.0 21.2 -5.8

Neuro 17.2 16.1 6.7 15.5 10.5

Cardiac 18.0 14.8 21.9 17.3 4.0

Pain 16.0 15.6 2.7 17.4 -8.3

Vaccines 17.8 6.2 187.3 13.8 29.1

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 1915, 64.9%

Chronic, 466, 15.8%

Sub-Chronic,

569, 19.3%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

48%

20%

11%

10%

11%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 21

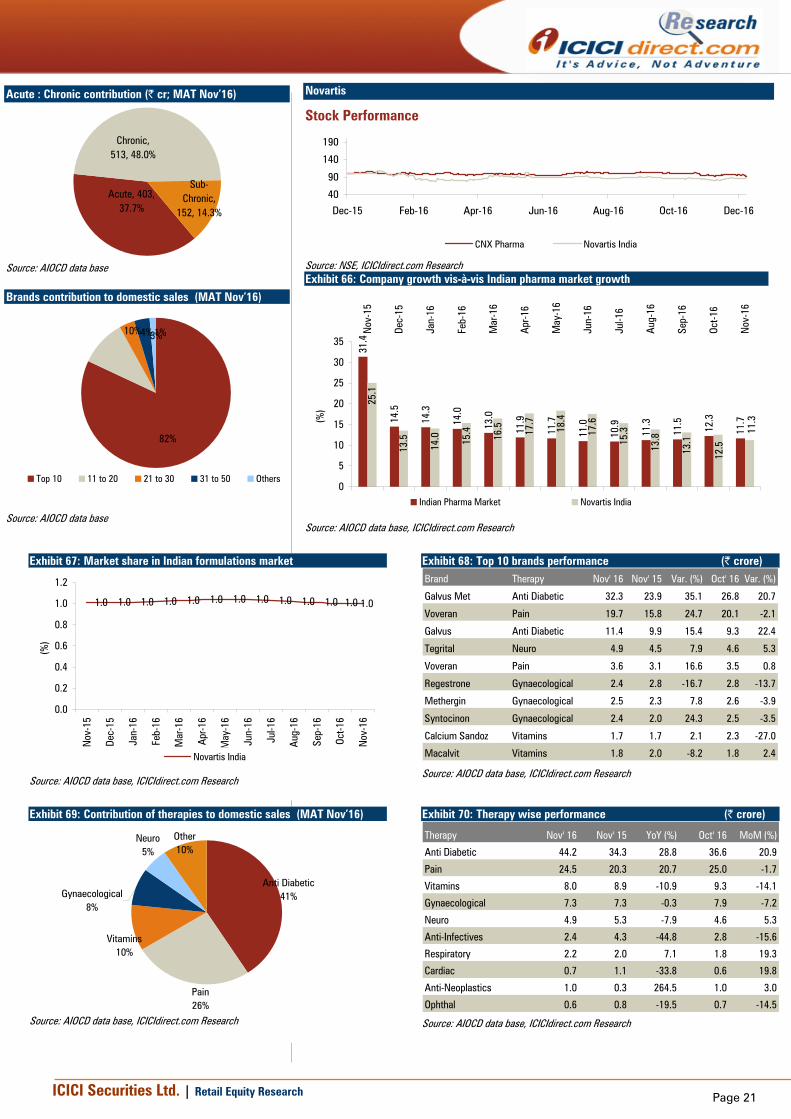

Novartis

Stock Performance

40

90

140

190

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Novartis India

Source: NSE, ICICIdirect.com Research

Exhibit 66: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

25.1

13.5

14.0 15

.4 16.5 17.7

18.4

17.6

15.3

13.8

13.1

12.5

11.3

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Novartis India

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 67: Market share in Indian formulations market

1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.0 1.01.0

0.0

0.2

0.4

0.6

0.8

1.0

1.2

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Novartis India

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 68: Top 10 brands performance (| crore) Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Galvus Met Anti Diabetic 32.3 23.9 35.1 26.8 20.7

Voveran Pain 19.7 15.8 24.7 20.1 -2.1

Galvus Anti Diabetic 11.4 9.9 15.4 9.3 22.4

Tegrital Neuro 4.9 4.5 7.9 4.6 5.3

Voveran Pain 3.6 3.1 16.6 3.5 0.8

Regestrone Gynaecological 2.4 2.8 -16.7 2.8 -13.7

Methergin Gynaecological 2.5 2.3 7.8 2.6 -3.9

Syntocinon Gynaecological 2.4 2.0 24.3 2.5 -3.5

Calcium Sandoz Vitamins 1.7 1.7 2.1 2.3 -27.0

Macalvit Vitamins 1.8 2.0 -8.2 1.8 2.4

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 69: Contribution of therapies to domestic sales (MAT Nov’16)

Anti Diabetic41%

Pain 26%

Vitamins 10%

Gynaecological8%

Neuro 5%

Other10%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 70: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Anti Diabetic 44.2 34.3 28.8 36.6 20.9

Pain 24.5 20.3 20.7 25.0 -1.7

Vitamins 8.0 8.9 -10.9 9.3 -14.1

Gynaecological 7.3 7.3 -0.3 7.9 -7.2

Neuro 4.9 5.3 -7.9 4.6 5.3

Anti-Infectives 2.4 4.3 -44.8 2.8 -15.6

Respiratory 2.2 2.0 7.1 1.8 19.3

Cardiac 0.7 1.1 -33.8 0.6 19.8

Anti-Neoplastics 1.0 0.3 264.5 1.0 3.0

Ophthal 0.6 0.8 -19.5 0.7 -14.5

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 403, 37.7%

Chronic, 513, 48.0%

Sub-Chronic,

152, 14.3%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

82%

10%4%3%1%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 22

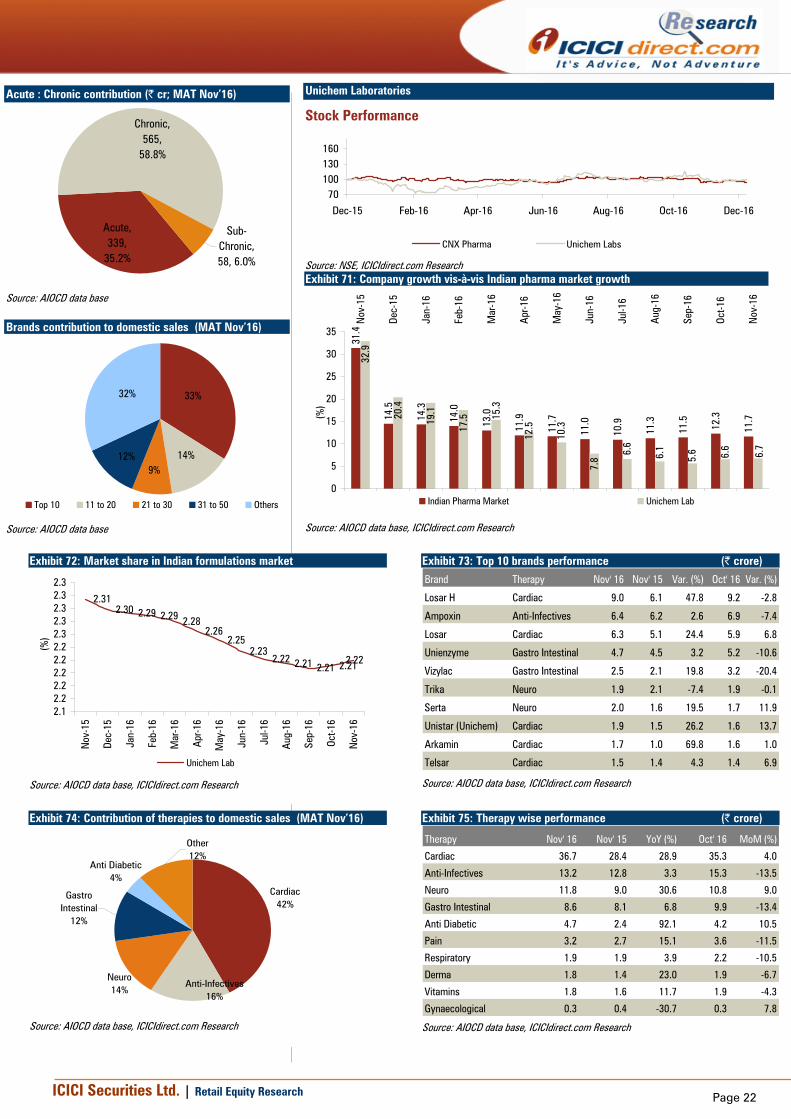

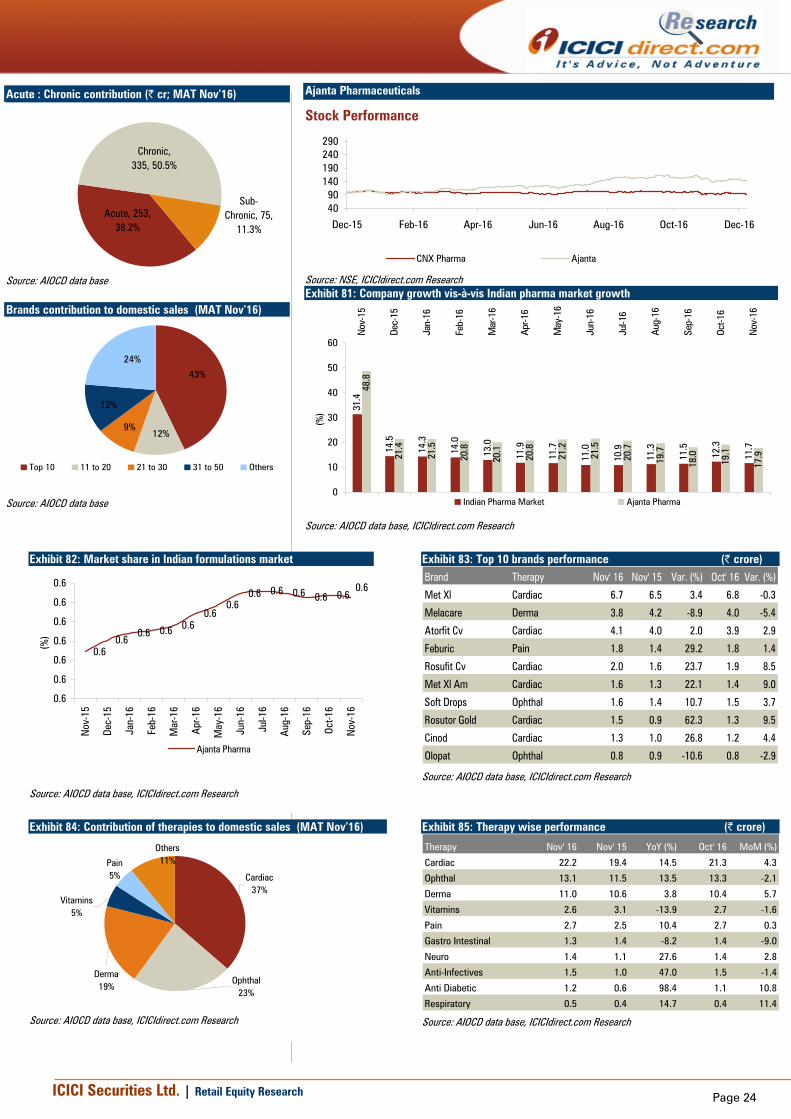

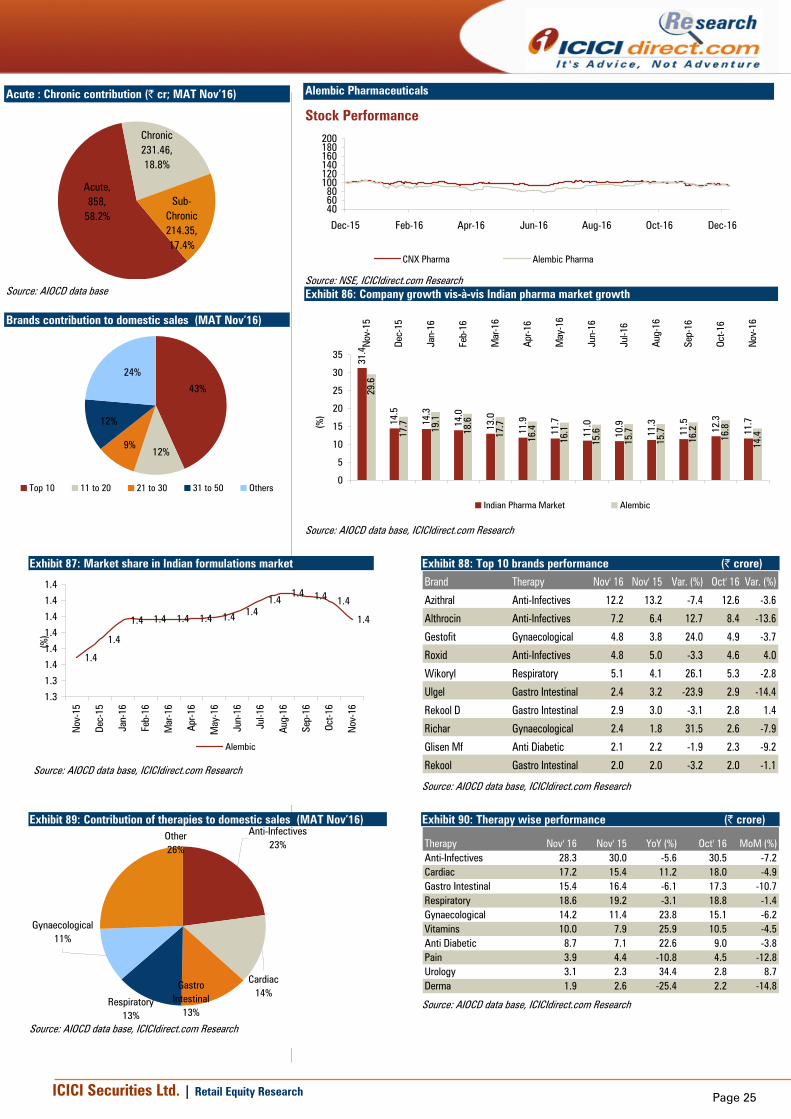

Unichem Laboratories

Stock Performance

70100130160

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

CNX Pharma Unichem Labs

Source: NSE, ICICIdirect.com Research

Exhibit 71: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

32.9

19.1

17.5

7.8

20.4

15.3

12.5

10.3

6.6

6.1

5.6 6.6

6.7

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Unichem Lab

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 72: Market share in Indian formulations market

2.312.30 2.29 2.29 2.28

2.262.25

2.232.22 2.21 2.21 2.212.22

2.12.22.22.22.22.22.32.32.32.32.3

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Unichem Lab

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 73: Top 10 brands performance (| crore)

Brand Therapy Nov' 16 Nov' 15 Var. (%) Oct' 16 Var. (%)

Losar H Cardiac 9.0 6.1 47.8 9.2 -2.8

Ampoxin Anti-Infectives 6.4 6.2 2.6 6.9 -7.4

Losar Cardiac 6.3 5.1 24.4 5.9 6.8

Unienzyme Gastro Intestinal 4.7 4.5 3.2 5.2 -10.6

Vizylac Gastro Intestinal 2.5 2.1 19.8 3.2 -20.4

Trika Neuro 1.9 2.1 -7.4 1.9 -0.1

Serta Neuro 2.0 1.6 19.5 1.7 11.9

Unistar (Unichem) Cardiac 1.9 1.5 26.2 1.6 13.7

Arkamin Cardiac 1.7 1.0 69.8 1.6 1.0

Telsar Cardiac 1.5 1.4 4.3 1.4 6.9

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 74: Contribution of therapies to domestic sales (MAT Nov’16)

Other12%

Anti Diabetic4%

Gastro Intestinal

12%

Neuro 14%

Anti-Infectives16%

Cardiac42%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 75: Therapy wise performance (| crore)

Therapy Nov' 16 Nov' 15 YoY (%) Oct' 16 MoM (%)

Cardiac 36.7 28.4 28.9 35.3 4.0

Anti-Infectives 13.2 12.8 3.3 15.3 -13.5

Neuro 11.8 9.0 30.6 10.8 9.0

Gastro Intestinal 8.6 8.1 6.8 9.9 -13.4

Anti Diabetic 4.7 2.4 92.1 4.2 10.5

Pain 3.2 2.7 15.1 3.6 -11.5

Respiratory 1.9 1.9 3.9 2.2 -10.5

Derma 1.8 1.4 23.0 1.9 -6.7

Vitamins 1.8 1.6 11.7 1.9 -4.3

Gynaecological 0.3 0.4 -30.7 0.3 7.8

Source: AIOCD data base, ICICIdirect.com Research

Acute : Chronic contribution (| cr; MAT Nov’16)

Acute, 339,

35.2%

Chronic, 565,

58.8%

Sub-Chronic, 58, 6.0%

Source: AIOCD data base

Brands contribution to domestic sales (MAT Nov’16)

33%

14%9%

12%

32%

Top 10 11 to 20 21 to 30 31 to 50 Others

Source: AIOCD data base

ICICI Securities Ltd. | Retail Equity Research

Page 23

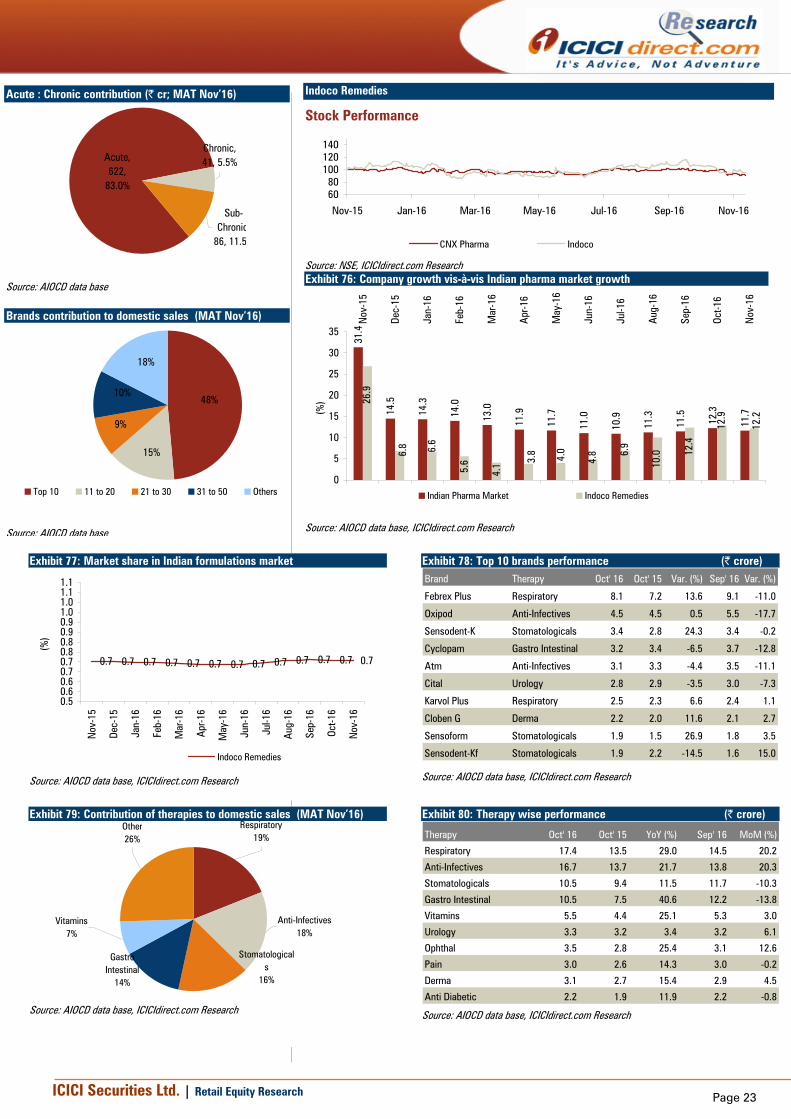

Indoco Remedies

Stock Performance

6080

100120140

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

CNX Pharma Indoco

Source: NSE, ICICIdirect.com Research

Exhibit 76: Company growth vis-à-vis Indian pharma market growth

31.4

14.5

14.3

14.0

13.0

11.9

11.7

11.0

10.9

11.3

11.5

12.3

11.7

5.6

4.1

12.2

12.9

12.4

10.06.

9

4.84.0

3.86.

6

6.8

26.9

0

5

10

15

20

25

30

35

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr

-16

May

-16

Jun-

16

Jul-1

6

Aug

-16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indian Pharma Market Indoco Remedies

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 77: Market share in Indian formulations market

0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7 0.7

0.50.60.60.70.70.80.80.90.91.01.01.11.1

Nov

-15

Dec-

15

Jan-

16

Feb-

16

Mar

-16

Apr-1

6

May

-16

Jun-

16

Jul-1

6

Aug-

16

Sep-

16

Oct-1

6

Nov

-16

(%)

Indoco Remedies

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 78: Top 10 brands performance (| crore) Brand Therapy Oct' 16 Oct' 15 Var. (%) Sep' 16 Var. (%)

Febrex Plus Respiratory 8.1 7.2 13.6 9.1 -11.0

Oxipod Anti-Infectives 4.5 4.5 0.5 5.5 -17.7

Sensodent-K Stomatologicals 3.4 2.8 24.3 3.4 -0.2

Cyclopam Gastro Intestinal 3.2 3.4 -6.5 3.7 -12.8

Atm Anti-Infectives 3.1 3.3 -4.4 3.5 -11.1

Cital Urology 2.8 2.9 -3.5 3.0 -7.3

Karvol Plus Respiratory 2.5 2.3 6.6 2.4 1.1

Cloben G Derma 2.2 2.0 11.6 2.1 2.7

Sensoform Stomatologicals 1.9 1.5 26.9 1.8 3.5

Sensodent-Kf Stomatologicals 1.9 2.2 -14.5 1.6 15.0

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 79: Contribution of therapies to domestic sales (MAT Nov’16) Respiratory

19%

Anti-Infectives18%

Stomatologicals

16%

Gastro Intestinal

14%

Vitamins 7%

Other26%

Source: AIOCD data base, ICICIdirect.com Research

Exhibit 80: Therapy wise performance (| crore)