process automation criteria identification and selection

TRANSCRIPT

The Pennsylvania State University

The Graduate School

Department of Labor Studies and Employment Relations

PROCESS AUTOMATION CRITERIA IDENTIFICATION AND SELECTION: A CASE

STUDY IN A PAYROLL COMPANY

A Thesis in

Industrial Relations and Human Resources

by

Fuyu Yi

© 2009 Fuyu Yi

Submitted in Partial Fulfillment of the Requirements

for the Degree of

Master of Science

May 2009

ii

The thesis of Fuyu Yi was reviewed and approved* by the following:

Sumita Raghuram Associate Professor, Labor Studies Employment Relations Thesis Advisor

Sandeep Purao Associate Professor, College of Information Sciences and Technology

Shawn Clark Professor of Practice, College of Information Sciences and Technology

Paul Clark Professor, Labor Studies Employment Relation Head of the Department of Labor Studies and Employment Relations

*Signatures are on file in the Graduate School

iii

ABSTRACT

This research is intended to provide insights to managers making decisions on

automation. With the objective of investigating criteria for business process automation, the

research question is defined as: “What are the criteria used by managers to select processes or

part of a process for automation?” Although there is some development in the practice of

selecting and prioritizing processes for automation, no academic research exists to validate those

criteria used in the prioritization of automating processes. Due to the apparent lack of rigorous

theories, our research utilized a case study strategy to investigate the criteria for business process

automation, which can be helpful in selecting and prioritizing candidates for the automation

process.

This study will generate three major products: a series of process maps; process maps

with varying automation levels; and a list of criteria for process automation. The first product,

process maps, helps managers to better understand their business operation in order to discuss

future improvement. The second product, automation level process maps, provides a discussion

platform for managers to view technology distribution within the company and detect automation

opportunities. The automation criteria, the primary product of this project, will provide new

empirical evidence for critical factors for assessing process automation priorities, contributing to

the efforts of building an automation decision model.

iv

TABLE OF CONTENTS

LIST OF FIGURES ................................................................................................................. v

LIST OF TABLES................................................................................................................... vi

ACKNOWLEDGEMENTS..................................................................................................... vii

Objective.................................................................................................................................. 1

Literature review...................................................................................................................... 2

Definition of Business Process ........................................................................................ 2Definition of Business Process Automation .................................................................... 2Criteria in previous literatures ......................................................................................... 3

Research Methodology ............................................................................................................ 6

3.1 Why case study? ........................................................................................................ 63.2 The Overall Research Plan ........................................................................................ 7

Research Settings and Procedure............................................................................................. 10

Settings ............................................................................................................................ 10Procedure ......................................................................................................................... 11

Findings ................................................................................................................................... 12

Business Process Summary ............................................................................................. 12(1) Selling................................................................................................................. 14(2) On-boarding Process .......................................................................................... 16(3) Operating Process............................................................................................... 19(4) Billing Clients .................................................................................................... 20(5) Taxing................................................................................................................. 21

Process Automation Level Summary .............................................................................. 23Automation Criteria Summary ........................................................................................ 28

Discussion................................................................................................................................ 29

Future Studies .......................................................................................................................... 32

Bibliography ............................................................................................................................ 72

v

List of Figures

Figure 1. Methodology Roadmap............................................................................................ 8

Figure 2. Overall Process Map. ............................................................................................... 13

Figure 3. Selling Process Map................................................................................................. 15

Figure 4. On-boarding Process Map........................................................................................ 17

Figure 5. Operating Process Map ............................................................................................ 19

Figure 6. Billing Clients Process Map..................................................................................... 20

Figure 7. Taxing Process Map................................................................................................. 21

Figure 8 Colored labels of four automation levels .................................................................. 24

Figure 9. Overall Automation Level Map .............................................................................. 24

Figure 10. Automation Level Map–Selling Process................................................................ 25

Figure 11. Automation Level Map–On-boarding Process....................................................... 25

Figure 12. Automation Level Map–Operating Process ........................................................... 26

Figure 13. Automation Level Map—Billing Clients............................................................... 26

Figure 14. Automation Level Map–Taxing Process................................................................ 27

vi

List of Tables

Table 1. The Fitts MABA-MABA List ................................................................................... 33

Table 2 Automation Criteria in previous literatures ................................................................ 33

Table 3. Relevant Situations for Different Research Strategies (Source: Yin, 1994) ............. 41

Table 4. Problems with Selling Process .................................................................................. 41

Table 5. Problems with On-boarding Process ......................................................................... 42

Table 6. Problems with Operating Process.............................................................................. 43

Table 7. Problems with Taxing Process .................................................................................. 44

Table 8. Automation Level Categories.................................................................................... 44

Table 9 Overall Automation Level Table................................................................................ 45

Table 10 Automation Level Table - Selling Process ............................................................... 48

Table 11 Automation Level Table – On-boarding Process ..................................................... 49

Table 12 Automation Level Table - Operating Process .......................................................... 50

Table 13 Automation Level Table – Billing Clients Process .................................................. 52

Table 14 Automation Level Table - Taxing Process ............................................................... 53

Table 15 Ranking of Process Automation Level..................................................................... 54

Table 16. Data analysis of general automation criteria ........................................................... 54

Table 17. Data analysis of automation criteria for on-boarding process................................. 56

Table 18. Data analysis of automation criteria for operating process ..................................... 58

Table 19. Data analysis of automation criteria for billing client's process.............................. 59

Table 20. Data analysis of automation criteria for taxing process .......................................... 60

Table 21. Data analysis of automation criteria for selling process.......................................... 61

Table 22. Automation Criteria List.......................................................................................... 62

vii

ACKNOWLEDGEMENTS

I am very grateful for the cooperation and interest of the professors and the case company

who took part in my automation criteria study. It would not have been possible without their help.

1

Objective

With highly developed business process modeling tools, managers become more aware of

various business processes running in the organization. When examining all those processes,

managers contemplate which process or processes should be automated in order to have their

value-adding processes run faster. Especially when technologies are so developed that almost any

process can be automated, people become less concerned about the technology capability or the

problem of “what can be automated.” Instead, it is more in the manager’s interest to ask: “What

should be automated?” What drives a manager’s decisions on automating a process? How does he

select processes for automation from hundreds or thousands of candidates?

The objective of this research is to investigate the criteria used by managers in selecting

and prioritizing processes as automation candidates. In May 2005, Ultimus announced its

innovative tool for Prioritizing Process Automation to facilitate more informed automation

decision-making. However, until recently there has been a lack of attention in academic research

to study what criteria should be included in such automation decision-making.

To achieve this research objective, we developed a research question (RQ) with two sub-

questions for this thesis project.

RQ: What are the criteria used by managers to select processes or part of a process for

automation?

--1. Is it possible to create a comprehensive process map based on inputs from multiple

stakeholders in a company?

--2. How can we assess automation levels of each process in the process map, based on

inputs from multiple stakeholders in the organization?

2

Literature review

Definition of Business Process

There are many different ways in the literature to define a business process. A definition

from the workflow perspective given by Amit Sheth (1997) is “a series of actions, changes, or

functions that bring about an end or result.” However, such a definition neglects a vital element of

a process – the human, which has also been widely discussed as a vital concern in automation

(Parasuraman, 2008). In this paper, we use a relatively comprehensive definition given by

Davenport and Short (1990). A business process is “the logical organization of people, materials,

energy, equipment and procedures into work activities designed to produce a specified end

result.” This process definition covers all the elements (people, materials, energy, equipment and

procedures) in a business process without any bias towards either activities or people. Such a

definition opens multiple doors for searching for criteria used in automation decisions.

Definition of Business Process Automation

Automating business processes is also known as Automated Workflow (Gary et al, 1997).

The emphasis of workflow automation has largely been on automating administrative tasks and

other mostly routine processes; however, there is increased research interest in automating more

complex, mission-critical, and coordination-centric processes (Amit Sheth, 1997). With highly

developed technologies and diverse capabilities, automation has been given more possibilities and

more expectations. Automating low-level repeatable processes is not enough to maintain a highly

3

effective office operation. However, processes requiring more coordination and collaboration

require an adaptive way to approach workflow automation.

To include all types of technical capabilities, this thesis defines “Business Process

Automation” as the replacement of one or more manual parts of a business process with

automated ones, usually through the use of advanced technologies. In this definition, the word

“automation” was selected very carefully because it implies essentially what Information

Technology is doing.

Criteria in previous literatures

Based on our literature review, there is a lack of understanding about how to make a

rational automation decision; however, we can learn from practical experience, and also follow

clues in other research areas during our exploration of automation criteria.

In the process prioritizer tool developed by Ultimus, four groups of factors are used to

compute a candidate process’s Priority Index (Baker, 2005). The four groups are process features,

technical features, human factors and business alignment by BPM sponsor’s priorities. Process

features determine whether the process is suitable for automation. Then each process’s technical

suitability for automation is explored. Human factors decide whether automating a process will fit

the organizational culture. Finally, the automation candidate process is evaluated by its extent of

alignment with strategic business concerns. The four groups cover a wide range of factors, but

what specific criteria are evaluated under each group is not clear.

In assessing the automation suitability of a process, the traditional method is always to

automate routine processes, and leave processes that require more complex human skills (human-

centric processes), such as coordination, communication, collaboration, and complex decision-

making, manual (Ayachitula, Buco, Diao, & Fisher, 2007). In differentiating a routine process

4

from a human-centric process, Ayachitula et al (2007) used the number of tasks, number of

shared tasks, number of cross-role links, and number of business items as four criteria to evaluate

process complexity.

A more famous approach for making automation decisions in the human-machine

interaction discipline is Fitts list (1951) that states what “men are better at” and what “machines

are better at” (MABA-MABA). Human-machine interaction is a very different research area from

our study. The former concerns closed-system functionality design in a time-critical system, such

as in aircraft, medical and robotic systems, while our research is about allocating human and

automation processes in business organizations with less time pressure. However, these two

research areas share process features that are suitable for automation. The Fitts MABA-MABA

(see Table 1) list outlines features that shall be identified in processes considered for automation.

But, as pointed out by Price (2005), data needed for a Fitts list are context-dependent; therefore

they are not the ideal criteria, which should be completely context-independent (Botta & Bahill,

2007).

--Table 1 here—

Human-machine interaction has produced a huge range of literature since 1950, dealing

with the behavioral, social and organizational impact of automation (Grudin, 2006). Aside from

culture (Baker, 2005; Tedre, Sutinen, Kahkonen, & Kommers, 2006), other human factors are

examined when determining the automation degree in human-machine system design, such as

mental workload, situation awareness, complacency, and skill degradation (Parasuraman,

Scheridan, & Wickens, 2000). Those human concerns could constitute useful criteria to gain a

desired human performance improvement and avoid the serious consequences of human sacrifice.

Above all, beyond process features, technical features or human factors, automating a

process must be in line with organizational priorities. Organizational priorities such as company

growth or customer satisfaction should be the final judge of a process automation decision

5

because it is the overall goal of any organization-wide decision. For example, organizational

critical success factors (CSFs) are derived to select and prioritize processes for re-engineering

(Kettinger, Teng, & Guha, 1997). Since company resources are limited, any new

investment/development decision should provide maximum contributions to the company

strategy (Abendshien, 2001).

In addition to all the desired benefits mentioned above, we should also consider different

costs and risks of automating processes as a constraint criterion in most decisions/prioritizations

(Botta & Bahill, 2007). Cost not only implies money, but also includes resources like time, labor,

opportunities, and so on (Botta & Bahill, 2007). Technology costs and risks have been found

through extensive research examining prioritization models of process re-engineering (Kettinger,

Teng, & Guha, 1997), technology investment (Abendshien, 2001), and human-machine

interaction design (Parasuraman, Scheridan, & Wickens, 2000).

Other than academic research, a large number of automation benefits, such as

accountability and compliancy (Manila, 1996), responsiveness to customers (Statton-Smith, 1986;

Goldenberg, 1995), and greater control (Kennedy, 1988), can be found in popular magazines and

Internet articles. In summary, all the factors related to automation are listed in the table 2.

--Table 2 here—

6

Research Methodology

Research questions of this thesis follow from a review of the literature.

RQ: What criteria do managers use to select processes or part of a process for

automation?

1. Is it possible to create a comprehensive process map based on input from multiple

stakeholders in a company?

2. How can we assess automation levels of each process in the process map (based on

input from multiple stakeholders in the organization)?

A research method has been carefully developed to respond to these questions. This

section summarizes the research process including research strategy selection and research plan

development. Based on careful consideration of research requirements and resources available, a

case study has been designed as the research methodology. The following sections will elaborate

on the choice of the case study and the development of the case study plan.

3.1 Why case study?

To answer the research question, case study has been chosen as the research methodology

rather than Experiment, survey, Archival analysis, or History that represents the main research

strategies in Yin’s book (2003). The considerations behind this choice include the form of the

primary research question, when events or issues involved in answering the primary research

question took place, and whether or not any control existed over these events or issues.

7

Different aspects of the five research strategies have been compared in Table 3, according

to Yin (2003).

--Table 3 here—

Based on the Yin’s summary, there several reasons suggest case study as the most

appropriate strategy for this research,

1. Form of research question. Although the research question is an assessment of “what?”,

no previous studies have directly touched this problem, so an exploratory case study would be

most appropriate to investigate criteria behind a manager’s automation decision without any

contamination from a researcher’s preset expectations and biases.

2. The research question is about a contemporary issue and researchers have no control of

the issues and environment.

3. There no clear candidate criteria are found in the literature for the context of this

research question. Therefore, contextual conditions should be covered for the research

exploration. In this situation, case study is the most desirable strategy to investigate automation

criteria hiding in the big context, while any other strategies have some limitations. For instance, it

would be awkward to list all potential criteria in a survey, and it would also be possible to

mislead a participant.

In conclusion, case study offers the most appropriate strategy to explore the answer to the

research question in this thesis.

3.2 The Overall Research Plan

In this study, we draw on earlier literatures to define a business process and business

process automation, which built a discussion platform for further investigation of automation

criteria. Although no academic research has been found about automation criteria, a process-

8

prioritizing tool has been found in practice and provides a starting point for our research. Based

on four groups of factors identified in process prioritizing, extensive research has been found

either to extend automation criteria under each group or provide proof or supplemental factors to

make the automation decision.

Based on multidisciplinary literature, we can develop a significant list of automation

criteria and validate all the criteria in future studies. Without previous studies directly discussing

the topic in this paper, exploratory case study offers the best research strategy for the study. The

case was carefully selected to meet research requirements and validity considerations. We

developed four steps to complete this case study (see figure 1):

Figure 1. Methodology Roadmap

9

1) Systematic interviews. This step includes the kick-off interview, eight individual

interviews, one group interview and two follow-up interviews. All individual interviews are

structured interviews during which the researcher asks all participants a standard set of questions.

The group interview was conducted in a semistructured way: participants were asked to look at

process maps one by one, but for each process no standard questions were asked.

2) Process Modeling. This study uses the process-modeling tool Blueprint, a software

developed by Lombardi Software, Inc., a provider of Business Process Management (BPM)

software and services. Blueprint is a tool for processing documentation and workflow

diagramming. This study used Blueprint to map business processes because Blueprints include as

Inline editing, collapsible sub-processes, and linked common processes, which make process

mapping simple enough so that the user has more energy and time to explore automation criteria.

3) Exploring automation criteria through a group interview. After participants revised the

process map during the first section of the group interview, they were asked to talk about the

criteria they used in deciding the current automation level of each process. This section was also

conducted in a semistructured way, and again, no standard questions were designed in advance.

New questions popped up throughout the discussion.

4) Analyzing results. Automation criteria are derived from interview notes using content

analysis. Those criteria are then compared with those found in earlier literature. The analysis

contributes to the understanding of managers' concerns in decisions about automation and

provides information for future studies.

10

Research Settings and Procedure

Settings

The case study has been carried out in a payroll outsourcing company in central

Pennsylvania. Payroll outsourcing is a highly growing industry dominated by three players—

ADP, Paychex, and Ceridian Employer Services. According to an IDC study (IDC, 2008/06), the

three companies dominated a 44-percent share of US payroll outsourcing market; while those

small, regional companies like the company in this case study primarily operate at the very local

level. The competition in this market is furious, and it is in the interest of those small companies

to stand at the edge of technology to maintain and even expand their businesses.

The case companyhas 12 employees, including a CEO, 3 people in the operations

department (one of them takes all technical responsibilities as IT manager), 2 people in the tax

department, 2 in the conversion department and 4 in the sales department. Tax, conversion, and

IT all come under the umbrella of operations. Although each person has a distinct title, they all

share some general responsibilities, like operating payroll, answering phone calls from clients,

and other office tasks, which enables the company to provide better customer service and a

flexible work environment.

Although this company provides outsourcing services, it has outsourced some of its own

functions to other companies as well. For example, it outsourced its own payroll to Pay Choice,

and its website design and hosting are outsourced to Focal Tech.

The IT environment is relatively simple; the company uses a core system—licensed

software bought from Pay Choice—to run payrolls. Other software the company uses include

Microsoft Operating System, Microsoft Office, and Norton Anti-Virus.

11

Procedure

This case study includes four steps: systematic interviews, process modeling, group

interview and data analysis.

The first step of this study includes an initial interview and eight individual interviews.

The first interview took place at the company office with the CEO and Senior Vice President for

Operations at 9:00 a.m. on December 14, 2007. The goal of this meeting was to discuss the

overall structure of this company.

Next, structured interviews were conducted with the CEO, Senior Vice President for

Operations, two operations people, the tax manager, tax employee, conversion manager, and sales

manager. Interview questions included task allocation within department, detailed steps of the

work processes, time distribution on various steps, input and output of each step and process, time

schedule for a typical workday, workload, and personal feelings about current work.

After the Blueprint software had mapped out the results, we conducted an interview with

the CEO and Operations Manager to verify the process map and, most importantly, to discuss

automation criteria. Following this interview, two additional individual interviews were

conducted with the conversion manager and the tax manager to investigate detailed steps in

conversion validation and tax processing, respectively.

The fourth step is the data analysis phase. We derived an automation criteria list from

interview notes using content analysis. All the automation criteria were compared with the earlier

literature to investigate what factors influence automating a process or prioritizing processes as

automation candidates.

12

Findings

This study has three major outcomes: the process map of the case organization, the

process automation levels and the list of criteria in explaining the current automation levels of

different processes. The three findings are concluded in three parts: Business Process Summary,

Process Automation Level Summary, and Automation Criteria Summary. Business Process

Summary includes a process map and a brief description of and current problem for each process.

Based on these process maps, steps with different automation levels have been marked with

different colors in the Process Automation Level Summary. Next, the five business processes

have been ranked according to their automation levels in a table. To explain the current

automation rankings, 21 criteria were found during discussion with the case company . Those

criteria are summarized in the last part of this section.

Business Process Summary

The case company has five business processes: selling, on-boarding, operating, billing

clients and taxing. Two levels of sub-processes have been developed under each process except

for billing clients, which is totally automated.

13

Figure 2. Overall Process Map.

The business of the case company begins with the selling process that turns prospect

clients into real clients. To illustrate the map above, we imagine company ABC in central

Pennsylvania. ABC has previously outsourced its payroll to company Slow-Motion. Since ABC

is a local company with only 30 employees (meeting the criteria of a prospective client), the case

company is very interested in developing business with this company. Therefore, a sales person

responsible for ABC's area will make phone contact with his company.

After making many efforts, this sales person gains a chance to meet with ABC’s HR

manager and finally succeeds in getting a contract with the payroll company . Then this sales

person will collect all required documents, such as company and employee information from

ABC and deliver them to the The payroll company office, which triggers the on-boarding process.

14

The on-boarding process starts at the point when the sales person hands client documents

to the on-boarding manager. With these documents, the on-boarding manager starts building a

client shell for ABC in the Pay Choice system. In addition, on-boarding people are also

responsible for processing the first payroll.

The operating people will then take the responsibility of processing periodic payroll for

ABC according to its pay schedule (monthly for example). After processing the March payroll for

ABC, an ACH (Automated Clearing House) file will be generated to charge ABC. Ata this point,

the payroll operation is completed.

Billing clients is totally automated once the ACH file has been submitted to the online

billing center. The amount of the service fee will be transferred from ABC’s bank account to the

payroll company ’s bank account electronically.

Taxing is a relatively separate process from payroll operation. Taxes are deducted from

paychecks for ABC’s employees during the operating process, but that tax money is actually held

by the payroll company until the taxes are due. As the tax due date approaches, The payroll

company assumes the liability to pay taxes to the taxing authorities on behalf of ABC.

The following paragraphs include more detailed information for each business process.

Each business process has its own map at the beginning, followed by a brief description of its

workflow and current problems indicating future improvement opportunities.

(1) Selling

The sales people are not settled in one office but are scattered at different places. A major

task for sales people is to make phone calls to prospective clients and to try to gain a first meeting

with them. The detailed steps are illustrated in Figure 3 and described afterwards.

15

Figure 3. Selling Process Map

The sales manager will first define the characteristics of prospective clients and do

market research about them and will buy a database of the prospect's information. The sales

manager then will assign sales people in charge of the prospective client's specific area. After the

sales manager completes the first two steps, sales people start their work by making phone calls

to prospects.

The first phone call to a prospective client is called a “cold call”, which could end in one

of three situations: a successful appointment, a warm call, or a rejection.

If the prospect responds very positively and agrees to schedule an appointment with the

payroll company , this sales person will ask the appointment person to schedule it in the online

calendar. The appointment may or may not end up with a final contract. But if the prospective

client agrees to sign a contract, the business becomes a new client. The sales person then collects

16

documents containing company and employee information and delivers it to the payroll company

, along with the first payroll data, most of the time.

If the prospect says “ *** is not here, could you call us later?”, or something to the same

effect, the sales person makes a “warm call” at a later time, which may end in one of the three

situations again.

If the response is a total rejection, the sales person will still make a “warm call” after

about six months, because they don’t want to give up on any prospects. The person in charge of

the prospect company might change his or her mind or that person might have been replaced after

several months, which could create a new selling opportunity.

Current problems existing in selling process are illustrated in Table 4 at the end of this

paper.

--Table 4 here—

(2) On-boarding Process

The on-boarding process sets up a company shell and employee profile for new clients. In

addition, the on-boarding person is also responsible for running the first payroll for this new

client. The First Payroll Process will be described in this section following the process of building

new client shell. Detailed steps are illustrated in Figure 4 below.

17

Figure 4. On-boarding Process Map

To build a new client shell, the on-boarding person first receives client documents from

sales people who have direct connection with clients. The employee information usually comes

from the prior payroll company that this client previously associated with. However, most of the

time it arrives on paper rather than in an electronic format, due to the competitor’s unwillingness

to make the transition an easy one. When the on-boarding person gets all the information needed,

she will enter the data into the Pay Choice system. That completes the process of building a new

client shell.

After the client shell has been set up, the on-boarding person needs to run the first

payroll. The first payroll is run in the same way as the subsequent ones, except that the on-

boarding person needs to do more error-checking. As described by the on-boarding person

interviewed, “When operations get it (payroll data), they need to be able to just process them and

18

get them out of the door, (but) I need to check them to make sure everything’s correct before it

goes to operation.”

Processing the first payroll starts when the sales people hand over the first payroll data to

the on-boarding people. Before processing the actual payroll, the on-boarding person needs to

check the year-to-date report for this client. Take the ABC company for example, who has been

associated with Slow-Motion before contracting with the payroll company . The year-to-date

report contains all the payroll information before ABC terminated contract with Slow-Motion

within the year. Validation of the year-to-date report has two purposes: 1) making sure previous

payroll records are correct, which will influence the yearly report at the end of a year; and 2)

providing a good reference for the first payroll, because it is unlikely big differences will arise

between first payroll numbers and the year-to-date report.

After checking the year-to-date information, the on-boarding person always chose to

process the entire payroll first and validate it at the end.

Then, they will hand the checks and reports to the sales people. And the sales people will

deliver them to the client and explain the reports to them. This is a very important part of client

service as a competitive advantage, because big payroll companies usually don’t have the time for

such service.

When there are no setups to do, the on-boarding people may help out with operations to

process payrolls if needed.

Current problems existing in on-boarding process are illustrated in Table 5 at the end of

this paper.

--Table 5 here—

19

(3) Operating Process

Figure 5. Operating Process Map

The operating process starts when clients fax in payroll data. Clients have three ways of

sending data to the payroll company —fax, ftp, or phone, among which phone is the least used

method. In addition, clients can also send special notes for each payroll processing through e-

mail.

Most of the time, clients will fax payroll data. When information arrives by fax, a payroll

staff member will retrieve it if the information is payroll related. This person will start to type the

information into the Pay Choice system. Upon finishing entering data, he or she will go over it

again validating it against the fax received. Then, the payroll will be sent to the printers. This

same person or some other operation person will pick them up at the printers and wrap payrolls

for mailing. At the wrap station (a table specially set up for wrapping outgoing mail), there is a

20

schedule of payrolls that are coming in this week. When the payroll is wrapped, the operating

person will check it off the list. The periodic payroll is completed at this point.

Current problems existing in operating processes are illustrated in Table 6 at the end of

this paper.

--Table 6 here—

(4) Billing Clients

The Billing Clients process happens daily and is totally automated. Once a payroll has

been processed, the operation person will generate an ACH file to charge this client. At the end of

a business day, all ACH files generated during the day will be sent to the person in charge of it.

At the payroll company , it is the tax manager. The tax manager will then submit all the ACH

files to an online billing center. This online billing center will transfer the amount due from the

client’s bank account to the payroll company ’s account. All the transactions are processed

electronically.

Figure 6. Billing Clients Process Map

21

(5) Taxing

There are three types of taxes—federal, state and local. All those taxes have already been

deducted from employees' paychecks and held by The payroll company during the Operating

Process. When the tax due date approaches, the payroll company pays the amount to the tax

authorities on behalf of the clients. Both federal and state tax payments can be made through

Internet, while local tax payment needs to be processed manually by mailing checks to local tax

authorities. Considering the fact that townships scattered all over Pennsylvania collect their taxes

separately, the local tax payment is a very complicated and time-consuming process.

Figure 7. Taxing Process Map

For a new client's federal taxes, the tax person needs the client number at the payroll

company from the on-boarding manager to apply for a personal information number (pin)

number. Each client has a unique pin for federal taxes in the federal tax payment system called

the Electronic Filing Tax Payment System for Internal Revenue Services (EFTPIRS). Once the

22

pin is assigned to the client, the tax person can use it to pay tax on behalf of the client in the

future. Since the payment frequency of federal taxes varies from client to client and the payroll

company assumes the liability instead of its clients, the tax person pays federal tax semi-weekly,

usually on Wednesdays and Fridays, or the payroll company will be charged for late tax

payments.

The rest of the process of paying the federal tax is quite simple. The tax person usually

checks the due dates daily and exports a file with companies whose due days are two days later.

Since the Pay Choice system is in a different computer than the one where the EFTPIRS is

installed, the tax person needs to import this file into EFTPIRS and then submit the payment

through the Internet.

For state taxes, the process is very similar to federal taxes except for some minor

differences. For example, the client does not need a pin number to submit the payment, but the

tax person need to get permission to pay the state taxes on the client’s behalf before they actually

process the state tax. The tax person can either apply for permission from the state government

website or request it from some other organization that already holds it. Once the rights are

released to the payroll company Payroll, the tax person can login onto the state tax website and

pay taxes for multiple clients at the same time.

For local taxes, most payments are made manually by mailing checks to the local taxing

authorities at the end of a quarter. Thus, it is not an everyday task but can be very cumbersome

when it is coming close to the end of a quarter. The tax people print out checks and reports, wrap

it with forms sent by the tax bureau if there are any, and then send them by mail.

Current problems existing in the taxing process are illustrated in Table 7 at the end of this

paper.

--Table 7 here—

23

Process Automation Level Summary

The automation level varies among the five business processes and their sub-processes.

Based on the understanding of the five business processes presented in the previous section,

knowledge of the current automation levels enables decision makers to reflect on the automation

criteria in use and think about possibilities of further automation. In this section, we define four

levels of automation and mark them on the process map. The four levels include Manual, Partial

Automation, Predominant Automation, and Total Automation. We differentiate them according to

which parts of the process have been automated. A process usually includes three components:

input, operation, and output. Based on the principle that automating the operation of a process

increases the automation level much more than automating the format of input/output, a process

with IT operation is always more automated than a process with manual operation. The four

automation levels are defined below:

--Table 8 here—

A manual process is defined as a process with no electronic information. Partial

Automation refers to a process transferring data from paper to electric, or transporting data

manually from one device to another, such as data entry and transporting data by removable disk.

Predominant Automation refers to an automation level between Partial Automation and Total

Automation, where the Information System is usually involved in the operation system but some

manual pieces still exist. Total Automation means all human input involved in a process involves

no more than clicking buttons. The categorization of the four automation levels is illustrated in

the table 8 and label for each automation level is colored in automation level maps in following

paragraphs (colored labels are illustrated in Figure 8).

24

Figure 8 Colored labels of four automation levels

To illustrate automation levels on process maps, each process is presented by a map and a table.

In the automation level maps (Figure 9 – Figure 14), varying automation levels have been

differentiated by color. In addition to the map, details of input, operation and output of all non-

manual processes are summarized in tables (Table 9 – Table 14). Input and output are labeled by

material name. Operation name is consistent with the name of the process it belongs to, which

begins with a verb. At last, the automation rankings of the five business processes illustrate the

overall order of automation levels. It can be viewed as a summary of the automation conditions

(Table 15).

Figure 9. Overall Automation Level Map

-- Table 9 here--

25

Figure 10. Automation Level Map–Selling Process

-- Table 10 here—

Figure 11. Automation Level Map–On-boarding Process

-- Table 11 here--

26

Figure 12. Automation Level Map–Operating Process

-- Table 12 here--

Figure 13. Automation Level Map—Billing Clients

-- Table 13 here--

27

Figure 14. Automation Level Map–Taxing Process

-- Table 14 here—

-- Table 15 here--

28

Automation Criteria Summary

To investigate automation criteria, content analysis is used to analyze group interview

notes. Interview notes are listed sentence by sentence in tables. Because managers were asked to

give automation criteria for each business process in the company, interview notes about

automation criteria are organized by five business processes from Tables 16 to Table 21. For each

sentence from the notes, the researcher’s interpretation of this sentence is followed in the column

next to it.

--Table 16 here—

--Table 17 here—

--Table 18 here—

--Table 19 here—

--Table 20 here—

--Table 21 here—

Criteria are drew from those interpretations and marked in bold font, though some

sentences cannot generate any criteria but still kept in the table to keep complete original

information. Based on content analysis of all interview notes, 27 criteria are derived and then

listed in Table 22, which is the primary outcome of this study. In Table 22, the criteria are also

compared with those found from previous literatures.

--Table 22 here—

29

Discussion

1) It is possible to identify and codify criteria from determining the automation potential of

a business process. Similar to the decision model for selecting and prioritizing processes

for business process improvement, can also automation decision be rationalized by

analyzing a list of criteria. The list of criteria in this paper are very useful as a first step in

building a decision model, but this paper is limited in differentiating criteria for each

process and even sub-processes. Furthermore, the weights of processes on criteria are not

identified in this research due to limited time.

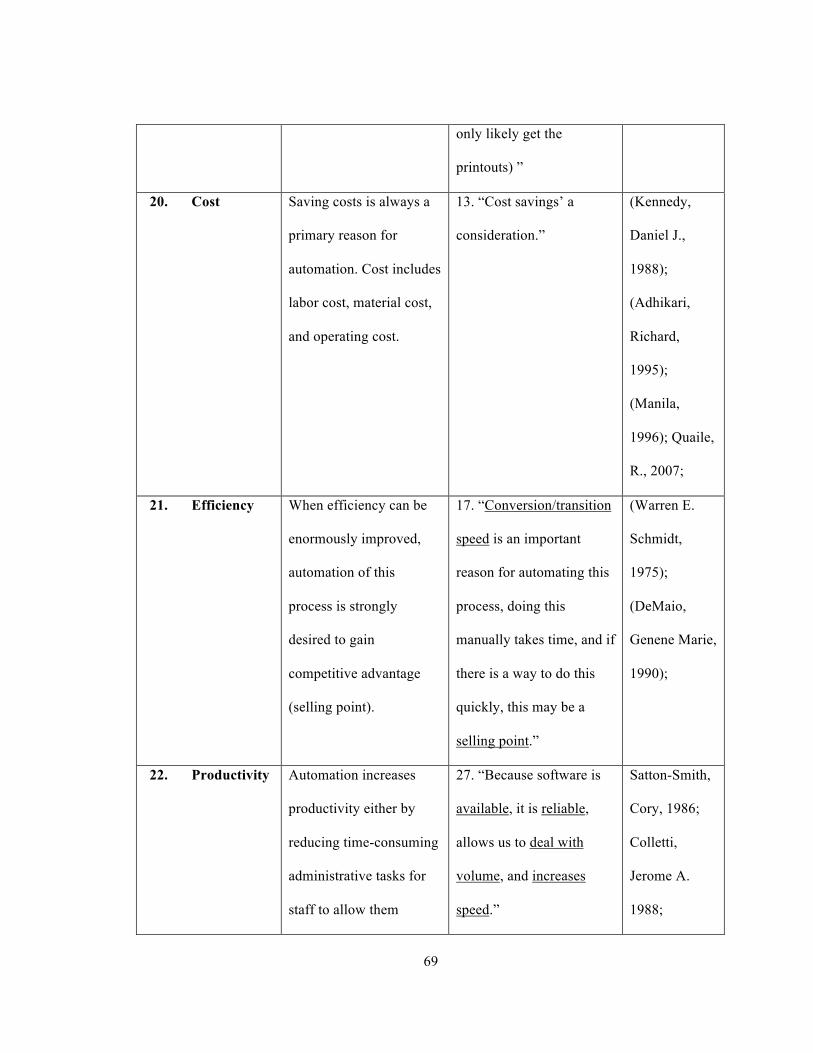

2) This study found criteria that support earlier literatures, such as business strategy,

competitive advantage, efficiency, productivity, and technology reliability. Those criteria

basically cover concerns of business alignment (business strategy and competitive

advantage), automation benefits (efficiency and productivity), technical features

(reliability and easy operation), people (available trained workers), and cost. Automation

decision is multifactor decision making. To gain the most benefits of automation, a

company will not automate a process just because it is more strategically important or

just because it has the best benefit-cost balance, but a company will try to balance many

more factors including technology possibilities and people.

3) Like any organizational decisions, automation decision is expected to be in line with

strategic concerns, including business strategy, competitive advantage, market share, and

company size. If automation can contribute to or be compatible to any of those strategic

concerns, a company will have a strong desire to increase automation, vice versa. Those

concerns may overlap depending on specific situations. For example, it may be because

30

of a large inefficient workforce that a bigger company's size requires more automation, or

it may be because of increasing market share that a bigger company needs automation to

handle increased workload. Above all, this is a proactive approach to the automating

processes, with which companies make automation decision from their own needs and

strategies.

4) External factors such as client size, type, needs, automation level and a competitor’s

automation level are also very important in automation decisions. Those automation

concerns are either reaction to clients or peer pressure from competitors, thus it is a more

reactive approach to automation. Client size, client type and its automation level may be

mediated by client needs, because automation is always intended to better serve a client’s

needs. In this paper, however, the mediation relationship has not been examined.

5) Value-add for processes are very different, thus whether automation can contribute to the

value-add of a process is a very important concern. For example, the value-add of the

selling process in this case study is to build a relationship with clients. The human touch

is appreciated very much in this process. Thus, the automation level is somewhat

constrained by this criterion. If a process values productivity and efficiency, then

automation is desired to increase them.

6) Process features such as availability of electronic data and computability of a process are

either enablers or constraints for automation. For example in this case study, automating

the data entry step of the on-boarding process is not possible because previous payroll

data are not available in electronic format—no matter how time-consuming this step is or

how strongly managers want to automate it.

31

7) Similar to process features, technical features can also be either enablers or constraints.

They include technology availability, quality, maturity, reliability and operation ease. A

few decades ago, those technical features may have played more of a constraining role

than enabler, because technologies were not well developed. But nowadays there are

extensive technology capabilities that can automate almost any process. Furthermore,

many small companies even start up around a software package covering many business

processes, like the company in this case study. In such a scenario, well-developed

technologies encourage automation by providing a package of automated processes

before managers consider which one should be automated.

8) Cost is another constraining concern, including labor cost, technology cost, and cost of

change. Cost of change has been emphasized in this case study because it starts from a

blank slate and little cost of change is a big advantage of this company to introduce a

whole package of software to automate many processes at the same time. Other costs in

the literature, such as labor costs and technology costs, are not mentioned in this study,

considering this is not a labor-intensive environment and monetary cost may not be a big

concern for growing companies when they’re looking for potential benefits in the future.

9) Compliance with government regulations is a criterion that we have not expected to find

in the literature. Just like manipulating the free market, government can exert its special

influence to encourage automation as a public policy, which is a strong driving force for

automation besides automation benefit/cost tradeoff.

32

Future Studies

The criteria found in this study are a valuable first attempt to build a pool of criteria for

automation decision-making. But this study is limited to exploring further weights of various

criteria on automation decisions. In addition, different processes have different concerns for

automation, but this paper did not categorize criteria specific for one process or one type of

process because of an inefficient amount of processes studied. It will be in the interest of future

studies to explore the possibility of building a list of common criteria to assess automation

potential of processes in general, or whether it’s better to categorize criteria and build a unique

decision model for a specific type of process such as customer facing processes. But in this case,

there will be more considerations about how to categorize processes appropriately in order to be

examined by the same group of criteria.

In addition, although this research does not particularly differentiate between types of

organizations in the discussion of automation criteria, it is believed that there will be different

criteria or different weights on the same criteria within different types of organizations. Future

studies on automation criteria are expected to make efforts to explore more criteria in different

types of organizations. In this way, companies can borrow experiences of best practices in

automation decision making from similar organizations.

33

Table 1. The Fitts MABA-MABA List

Men are better at

Detecting small amounts of visual, auditory or chemical energy

Perceiving patterns of light or sound

Improvising and using flexible procedures

Storing information for long periods of time, and recalling appropriate parts

Reasoning inductively

Exercising judgment

Machines are better at

Responding quickly to control signals

Applying great force smoothly and precisely

Storing information briefly, erasing it completely

Reasoning deductively

Table 2 Automation Criteria in previous literatures

Criteria Description Citation

Business alignment “Identify the extent of its alignment with the

priorities of BPM sponsors”

Baker, 2005; Kettinger,

Teng, & Guha, 1997

Competitive

advantage

Competitive advantage is the critical impetus

to automate a process.

Goldenberg, Barton,

1995

Process features “Determine if each candidate process has the

right characteristics to be suitable for

automation”

Baker, 2005

34

Technical features “Explore each process' technical suitability for

automation”

Baker, 2005

Continuous process

improvement

It’s easier to implement process

improvements on automated processes than

manual ones.

Captaris: Top ten

reasons to automate

workflow

Execution

Complexity

The complexity involved in performing the

tasks that make up the service process,

typically characterized by the number of

tasks.

Ayachitula, Buco, Diao,

& Fisher, 2007

Decision Complexity A sub-category of

execution complexity, quantifies decision

making according to the number of branches

in the decision, the degree of guidance, the

impact of the decision, and the visibility of the

impact.

Ayachitula, Buco, Diao,

& Fisher, 2007

Coordination

Complexity

The complexity

resulting from coordinating between multiple

roles,

either within a task or between tasks, and

depend on how business items are transferred

and processed.

Ayachitula, Buco, Diao,

& Fisher, 2007

Business Item

Complexity

The complexity involved in providing data

into the service process, and is quantified

through how the values were obtained.

Ayachitula, Buco, Diao,

& Fisher, 2007

35

Culture “Decide whether automation of each will be

advantageous within the culture of the

organization”

Baker, 2005

Mental workload The evidence suggests that well-designed

information automation can change human

operator mental workload to a level that is

appropriate for the system tasks to be

performed.

Parasuraman, Sheridan,

& Wickens, 2000

Situation awareness Automation of decision-making functions

may reduce the operator’s awareness

Parasuraman, Sheridan,

& Wickens, 2000

Complacency If automation is highly but not perfectly

reliable in executing decision choices, then

the operator may not monitor the automation

and its information sources and hence fail to

detect the occasional times when the

automation fails.

Parasuraman, Sheridan,

& Wickens, 2000

Skill degradation If the decision-making function is consistently

performed by automation, there will come a

time when the human operator will not be as

skilled in performing that function.

Parasuraman, Sheridan,

& Wickens, 2000

Increased

productivity

Automation increases productivity either by

reducing time-consuming administrative tasks

for staff to allow them focusing on more

value-added tasks or by equipping them with

Satton-Smith, Cory,

1986; Colletti, Jerome

A. 1988; Adhikari,

Richard, 1995; Buehrer,

36

more timely information to perform more

productively.

Senecal and Pullins,

2005; Manila, 1996;

Goldenberg, Barton,

1995; Crux automation:

reasons to automate

Increased

capacity/volume

Automation can increase capacity by handling

much more volume than people given the

same time period. Therefore automation can

either replace people to deal with large

volume or enable small number of staff to

handle volume that requires many more

people before.

Warren E. Schmidt,

1975; Richardson,

1991; Adhikari,

Richard, 1995;

Captaris: Top ten

reasons to automate

workflow; Crux

automation: reasons to

automate

Labor costs The more labor costs involved in a process,

the more savings are expected by automating

this process.

Kennedy, Daniel, 1988;

Adhikari, Richard,

1995; Manila, 1996;

Mark Lewis, 2005;

Captaris: Monte

Enbysk, 2008; Top ten

reasons to automate

workflow

Availability of labor The shortage of trained operators is also a Christopher A Bailey,

37

strong impetus to automate a process. 2005

Processing

time/speed/efficiency

Saving time entails two meanings: 1.

Automating routine processes increase the

efficiency of the automated process per se. 2.

Automating routine processes frees time up

for other strategic processes.

Warren E. Schmidt,

1975; Buehrer, Senecal

and Pullins, 2005;

Colletti, Jerome A.

1988; Steve A

Rosenthal, 2007;

DeMaio, Genene Marie,

1990; Steve A

Rosenthal, 2007;

Captaris: Top ten

reasons to automate

workflow

Accountability &

compliancy

The machine is much more objective than

people, therefore, accountability &

compliancy is expected to be enforced by

automation. In addition, automation is

expected to be less prone to corruption in

government.

Manila, 1996; Captaris:

Top ten reasons to

automate workflow

Connection of

customers and

suppliers

It is easier to serve customers and suppliers

through automated system.

Monte Enbysk, 2008;

Captaris: Top ten

reasons to automate

workflow

Responsiveness to Automation can increase responsiveness to Satton-Smith, Cory,

38

customer customers and suppliers, for example, the

availability of updated info enables reps to

respond more quickly to customers’ questions

1986; Goldenberg,

Barton, 1995

Timely and accurate

information

Automation can provide timely, easy access to

accurate information. For example, sales force

automation enable sales reps to make more

persuasive presentations by widening their

range of information.

Satton-Smith, Cory,

1986; DeMaio, Genene

Marie, 1990;

Goldenberg, Barton,

1995; Captaris: Top ten

reasons to automate

workflow

Maintenance of

operational

knowledge

Automated systems retain operational

knowledge without dependence on people,

especially in industries without high turnover

rates.

Captaris: Top ten

reasons to automate

workflow

Single source for

workflow

Automation offers a single source for

workflow, which reduces potential errors

produced by multiple sources.

Monte Enbysk, 2008;

Captaris: Top ten

reasons to automate

workflow

Immediate

communication

Automation enables immediate

communication

Richardson, 1991;

DeMaio, Genene Marie,

1990; Goldenberg,

Barton, 1995

Accelerate the flow of

information

Automation accelerates the flow of

information

Richardson, 1991

39

Accuracy/ precision Automation can produce more accurate

outcomes than humans, such as regional

maps.

Warren E. Schmidt,

1975; Richardson, 1991

Highly complex and

repetitive

computation

Only computers can do such highly complex

and repetitive computation. Such cases are

very common in engineering processes.

Warren E. Schmidt,

1975; Richardson, 1991

Make output

professional

Professionalism requires more standardized

and consistent output, which can only be

produced by an automation system.

DeMaio, Genene Marie,

1990

Greater control Automation enables managers to have greater

control over business processes. For example,

treasury automation enables a firm to achieve

greater control over the balances in its various

bank accounts.

Kennedy, Daniel, 1988;

Colletti, Jerome A.

1988

Better tracking

capabilities

It is much easier and faster to track historical

records with automation than with a manual

process.

Steve A Rosenthal,

2007; Monte Enbysk

(2008, Microsoft)

Sufficient training Training proved most effective in increasing

usage of technology

Buehrer, Senecal and

Pullins, 2005

Employee satisfaction

and motivation

Highly productive employees are expected to

feel more sense of achievement and therefore

feel more satisfied.

Goldenberg, Barton,

1995

Reliability The fewer uncontrolled variables in a process,

the higher the quality and more uniform the

Parasuraman, Sheridan,

& Wickens, 2000;

40

products. Richardson, 1991;

Mark Lewis, 2005;

Crux automation:

reasons to automate; J.

D. Lee and N. Moray,

1992

Predictability A reliable automation system can also

increase predictability of a process, such as

delivery dates and product quality, which is

especially important for the transportation

industry.

Richardson, 1991

Affordable The more affordable the automation

technology is, the more likely to automate a

process.

Manila, 1996; Monte

Enbysk, 2008

Easy to use The easier it is to use automation technology,

the more likely to automate a process

Monte Enbysk, 2008

41

Table 3. Relevant Situations for Different Research Strategies (Source: Yin, 1994)

Strategy Form of

research

question

Requires

control over

behavioral

events?

Focuses on

contemporary

events

Boundaries between

phenomenon and

context

Experiment How, why Yes Yes Deliberately divorces

a phenomenon from

its context

Survey Who, what,

where, how

many, how much

No Yes No, but the ability to

investigate the

context is extremely

limited

Archival

analysis

Who, what,

where, how

many, how much

No Yes/no

History How, why No No No

Case study How, why No Yes Not clearly evident

Table 4. Problems with Selling Process

Problem Description Challenge for Improvement

Challenges in

building client trust

It is challenging for sales people to

choose appropriate methods

throughout the interaction with

Since payroll usually takes 30

percent or more of the entire

budget of a company, the

42

prospective clients. prospective client needs enough

confidence in the payroll

company to handle their payroll

and expose their confidential

information such as bank

accounts.

Table 5. Problems with On-boarding Process

Problem Description Challenge for Improvement

Incompatible data

formats from clients

“The spreadsheet for my system has to

be in a specific order, so if a company

sends me over an Excel spreadsheet

that does not have the exact format

that I need, I end up spending more

time converting the files to the way I

needed than to just enter the

employees all by myself, just enter

them all by hand.”

“We sell on the point that our

on-boarding process is very

simple, you know, just give us

your report, and we take care of

it. For them, it’s so easy; it’s a

little more complicated for me”

Time consuming at

on-boarding step

On average, each company takes six

hours for set up.

For small companies, most

documents are kept on paper;

for bigger companies, electronic

documents may not be available

due to the competition's

43

unwillingness to make the

transition easy.

Time consuming at

the validation step

A ten-employee company could take

her 20 minutes to finish checking

everything, while the actual payroll-

processing step takes only minutes.

Since the company shell and

first payroll is only entered once

at the beginning of each new

client relationship, careful

validation is a critical step to

ensure that future payrolls could

be processed smoothly.

Miscommunication “I don’t think I have ever had received

such great paperwork that I never have

to call the client. And I always have to

call the clients for something.”

Mistakes are unavoidable when

data are processed manually

several times.

Table 6. Problems with Operating Process

Problem Description Challenge for Improvement

Time consuming at

data entry step

In the absence of any errors data entry

could take as little as a couple of

minutes, to as long as an hour.

For small companies, most of

documents are kept on paper;

fax is the primary method to

collect payroll data.

Time consuming to

deal with unexpected

errors

Problems happen all the time, so the

operating person needs to go back and

search the error source and correct it,

or if there is nothing wrong with either

Mistakes are unavoidable when

data are processed manually

several times.

44

data entering or software, this person

needs to call the client to check if they

have sent the wrong data.

Table 7. Problems with Taxing Process

Problem Description Challenge for Improvement

Inconsistence of tax

rates

Whether to use the tax rate based on

where the business is located or based

on where the employee lives, if the

two are different.

Government policies differ from

one town to another

Time consuming for

local tax payments

Local taxes cannot be paid

electronically, instead, can only be

paid by mailing checks to many small

local tax authorities.

Small townships scattered all

over Pennsylvania collect their

taxes separately

Table 8. Automation Level Categories

45

Table 9 Overall Automation Level Table

Automation

Level

Process Name Input Operation Output

Selling –

Assign tasks to

salesmen

Database of

prospect clients

Assign tasks to

salesmen in face,

by phone, or email

Task assignment to

each salesman

Onboarding –

Gather basic

client data

Basic client data in

paper, or electronic

format at client

company

Gather basic client

data mostly by

hand, from

salesmen, or ftp

server, or from fax

machine.

Basic client data in

paper, or electronic

format at the

payroll company

Onboarding –

gather first

payroll data

First payroll data

in paper, or

electronic format

at client company

gather first payroll

data mostly by

hand, from

salesmen, or ftp

server, or from fax

machine.

First payroll data

in paper, or

electronic format

at the payroll

company

Partial

Automation

Operating –

gather periodic

payroll data

Periodic payroll

data in paper, or

electronic format

at client company

gather periodic

payroll data mostly

by hand, from

salesmen, or ftp

server, or from fax

machine.

Periodic payroll

data in paper, or

electronic format

at the payroll

company

46

Selling –

Schedule the

appointment

online

Appointment

information on

paper

Schedule the

appointment online

Appointment

scheduled online

Onboarding –

Build client

shell

Basic client data in

paper, or electronic

format at the

payroll company

Build client shell

in the Pay Choice

system

Client shell stored

in the Pay Choice

system

Onboarding –

Process first

payroll

First payroll data

in paper, or

electronic format

at the payroll

company

Process first

payroll in the Pay

Choice system

First payroll data

stored in the Pay

Choice system

Operating –

Print out

weekly client

list

Client information

in the Pay Choice

system

Print out weekly

list of clients

whose pay period

is in the same

week

Client list on the

paper

Operating –

Process

periodic

payrolls

Periodic payroll

data in paper, or

electronic format

at the payroll

company

Process periodic

payrolls in Pay

Choice system

Periodic payroll

data stored in the

Pay Choice system

Predominant

Automation

Taxing – Tax updates Update tax Updated tax

47

Update tax

information

information in

mails/emails

information information in the

Pay Choice system

Taxing –

Process local

tax payments

Tax payment

information in the

Pay Choice system

Process local tax

payments

Tax payment

checks

Billing clients –

Collect ACH

files of clients

due daily

ACH file

generated by the

Pay Choice system

Collect ACH files

of clients due daily

ACH files in the

computer

responsible for

billing clients

Billing clients –

Login billing

center online

User name and

password of the

payroll company

Login billing

center online

Successfully login

to the the payroll

company ’s online

billing panel

Billing clients –

Submit all

ACH files

ACH files in the

computer

responsible for

billing clients

Submit all ACH

files

Online requests for

billing clients

Total

Automation

Billing clients –

Charge clients

bill

Online requests for

billing clients

Charge clients bills

by transferring

money from

clients to the

payroll company

Transaction

completed between

clients and the

payroll company

48

Taxing –

Process Federal

Tax Payments

Tax information of

clients whose taxes

are due

Process Federal

Tax Payments

through EFTPIRS1

Transaction

completed between

Federal tax bureau

and the payroll

company

Taxing –

Process State

Tax Payments

Tax information of

clients whose taxes

are due

Process State Tax

Payments through

state online system

Transaction

completed between

State tax bureau

and the payroll

company

Table 10 Automation Level Table - Selling Process

Automation

Level

Process Name Input Operation Output

Access to

prospects

database

User name and

password of the

payroll company

Access to

prospects

database

Successfully

login to the

database

Partial

automation

Group prospects

by location

List of prospects

in the database

Group prospects

by location

List of prospects

grouped by

location

Totally

automated

Login online

calendar

User name and

password of the

payroll company

Login online

calendar

Successfully

login to online

calendar

1

Electronic Filing Tax Payment System For Internal Revenue Services

49

Set up

appointments on

calendar

Appointment

information

either in paper or

electronic format

Set up

appointments on

calendar

Appointments set

up in the online

calendar

Save

appointments

online

Appointments set

up in the online

calendar

Save

appointments

online

Appointments

saved in the

online calendar

Table 11 Automation Level Table – On-boarding Process

Automation

Level

Process Name Input Operation Output

Receive basic

client data

Client documents

in paper at client

company

Receive basic

client data

through fax or

manually

Client documents

in paper at the

payroll company

Partial

Automation

Receive first

payroll data

First payroll data

at client

company

Receive first

payroll data

through fax or

manually

First payroll data

at the payroll

company

Predominate

automation

Enter client

company

information

Client company

information in

paper

Enter client

company

information into

Pay Choice

system

Client company

profile in the

system

50

Enter client

employee

information

Client employee

information in

paper

Enter client

employee

information into

Pay Choice

system

Client employee

profile in the

system

Print out checks

and reports

Payroll

information in

the system

Print out checks

and reports

Checks and

reports

Login the system User name and

password of the

payroll company

Login the system Successfully

login to Pay

Choice system

Create a new

client

Client company

information in

paper

Create a new

client

A new client

profile

uncompleted in

the Pay Choice

system

Save the client

profile

Client profile in

the Pay Choice

system

Save the client

profile

Client profile in

the Pay Choice

system

Total automation

Save first payroll First payroll in