project administration manual - asian development bank · pdf fileactions covering governance,...

TRANSCRIPT

Project Administration Manual

Project Number: 40010-01 Loan and/or Grant Numbers: May 2010

Proposed Loan, Grant, and Technical Assistance Grant Nepal: Rural Finance Sector Development Cluster Program (Subprogram 2)

CONTENTS

Page

Abbreviations

I. Program Description 1

A. Impact and Outcome 1 B. Components and Outputs 1

II. Implementation arrangements 3

A. Program Readiness Activities 3 B. Overall Project Implementation Plan 4

III. Program Management Arrangements 7

A. Program Stakeholders–Roles and Responsibilities 7 B. Key Persons Involved in Implementation 8 C. Project Organization Structure 9

IV. Costs and financing 11

A. The Program Loan 11 B. The Project Grant 11

V. Financial Management 15

A. Financial Management Assessment 15 B. Disbursement 15 C. Accounting and Auditing 16

VI. Procurement and Consulting Services 16

A. Procurement of Goods, Works and Consulting Services 16 B. Procurement Plan 17 C. Consultant's Terms of Reference 21

VII. Safeguards 25

VIII. Performance Monitoring, Evaluation, Reporting and Communication 25

A. Monitoring 28 B. Evaluation 29 C. Reporting 29

IX. Anticorruption Policy 31

Project Administration Manual Purpose and Process

1. The project administration manual (PAM) describes the essential administrative and management requirements to implement the project on time, within budget, and in accordance with Government and Asian Development Bank (ADB) policies and procedures. The PAM should include references to all available templates and instructions either through linkages to relevant URLs or directly incorporated in the PAM.

2. The executing and implementing agencies are wholly responsible for the implementation of ADB financed projects, as agreed jointly between the borrower and ADB, and in accordance with Government and ADB’s policies and procedures. ADB staff is responsible to support implementation including compliance by executing and implementing agencies of their obligations and responsibilities for project implementation in accordance with ADB’s policies and procedures.

3. At Loan Negotiations the borrower and ADB shall agree to the PAM and ensure consistency with the Loan and Grant1 agreement. Such agreement shall be reflected in the minutes of the Loan Negotiations. In the event of any discrepancy or contradiction between the PAM and the Loan and Grant Agreement, the provisions of the Loan and Grant Agreement shall prevail.

4. After ADB Board approval of the project's report and recommendations of the President

changes in implementation arrangements are subject to agreement and approval pursuant to relevant Government and ADB administrative procedures (including the Project Administration Instructions) and upon such approval they will be subsequently incorporated in the PAM.

1 The name of the operational financing document may vary on a project to project basis; this reference

shall be deemed to encompass such variations, e.g., a Framework Financing Agreement, as applicable.

ABBREVIATIONS

ADB – Asian Development Bank ADBL – Agricultural Development Bank Limited CEO – chief executive officer CIB – Credit Information Bureau CTA – Chief Technical Advisor DRT – Debt Recovery Tribunal GBB – Grameen Bikash Bank MIS – management information system MOF – Ministry of Finance NBTI – National Banking Training Institute NGO – nongovernment organization NRB – Nepal Rastra Bank PAM – Project Administration Manual PIU – program implementation unit PMU – program management unit PSC – program steering committee RFSDCP – Rural Finance Sector Development Cluster Program SFDB – Small Farmers Development Bank STI – second tier institution

I. PROGRAM DESCRIPTION

A. Impact and Outcome

1. The expected impact of the Rural Finance Sector Development Cluster Program (RFSDCP) is economic growth and poverty reduction in rural areas through improved rural financial intermediation and enhanced access to affordable rural finance service with special attention to marginal groups and women. The outcome will be improved soundness, efficiency, and outreach of rural finance system through policy, legal, regulatory, and institutional reforms. 2. As the last subprogram of RFSDCP, subprogram II will expect to develop a sound rural finance sector environment that is conducive to promote expansion of rural finance outreach for rural economic development and poverty reduction. The expected outcome of subprogram II is (i) successful transformation of the key rural finance institutions into viable rural finance intermediaries with strong client orientation and pro-poor focus, and (ii) enhanced outreach and efficiency of semi-formal rural finance institutions.

B. Components and Outputs

3. Subprogram II will continue the policy and institutional reform actions which were initiated under subprogram I. After the subprogram I review, modifications of the components were made. The component of the favorable policy environment is merged with the supportive legal and regulatory framework. The component of the product and process innovations is removed. Instead, a new component of the enabling rural finance infrastructure is added. 4. Supportive legal and regulatory framework. The process for establishing an Act and regulatory authority—the second tier institution (STI)—for the supervision of rural finance institutions, which was initiated under subprogram I, will be continued under subprogram II. Key component outputs include: (i) review and update of the Government's Microfinance Policy, 2008; (ii) development of a Microfinance Act; (iii) establishment of STI; and (iv) information dissemination and commencement of licensing and regulation of rural finance institutions. Envisaged STI will be an autonomous regulatory body, which will be governed by the board of directors represented from the Government, Nepal Rastra Bank (NRB), and the private sector. 5. Institutional restructuring and reforms–Agricultural Development Bank Limited. Transforming the Agricultural Development Bank Limited (ADBL) into a viable and effective financial intermediary is a key thrust of RFSDCP. Subprogram I restructuring activities involved voluntary retirement schemes, divestment of the Government shareholding at ADBL to small shareholders2 by 14%, and the initiation of the initial public offering. The key component outputs are the implementation of (i) the ADBL capital restructuring plan, and (ii) the second phase of the ADBL restructuring plan. The aim of the ADBL capital restructuring plan is to bring a private strategic investor into the ownership of ADBL to provide necessary leadership as a competitive modern financial institution. The capital restructuring plan envisages privatizing ADBL by reducing the Government ordinary shareholding to 21% tentatively by July 2011. ADBL privatization will be the first major financial privatization in Nepal. Along with the capital restructuring plan, the second phase ADBL restructuring plan will be for comprehensive reform actions covering governance, transparency, organization, marketing, human resources, 2 The Agricultural Development Bank of Nepal Act, 1967 defines that "a person taking a loan from ADBL in an

amount exceeding NRs10,000 shall be required to have purchased at least one share of ADBL (small shareholders)". Small shareholders could include small farmers, a group of small farmers, a village committee or cooperative institution.

2

business management, portfolio management, management information system (MIS), compliance, treasury, and internal audit. ADBL capital restructuring plan is in Web-linked Document 13. 6. Institutional restructuring and reforms–Small Farmers Development Bank. The ADBL restructuring is well complemented by the institutional reform of Small Farmers Development Bank (SFDB). SFDB is a cooperative bank for small farmer cooperatives, and has a strong grass-roots orientation. The SFDB reform intends to increase the depth of rural finance outreach for greater financial inclusiveness, especially to women. A specific component output is an update and implementation of the SFDB restructuring plan, which covers reconstitution of the board of directors, professionalization of the management, portfolio audit, introduction of a new organization structure, improvement of the internal control, introduction of MIS, and increase of private capital. 7. The SFDB restructuring plan includes strategies to expand microfinance services in the hills and mountain areas. The strategies involves (i) mapping of cooperatives, self help groups,3 and microfinance nongovernment organizations (NGOs) in those areas; (ii) institutional assessment and rating; (iii) technical assistance designing and capacity building; and (iv) onlending support for outreach expansion. SFDB aims to increase credit access to additional 20,000 households in the hills and mountain areas by 2012, of which 60% are women. 8. Institutional restructuring and reforms–Grameen Bikash Bank. Subprogram II envisages the successful completion of the privatization process of the Western Grameen Bikash Bank (GBB) 4 and provides a comprehensive technical advisory and capacity development support to transform it into an effective grass-root financial intermediary.

9. Sector capacity building. RFSDCP supports the establishment of a banking training institute for sector capacity development. The National Banking Training Institute (NBTI), established under subprogram I, will continue to be assisted to raise the standards of professional competence throughout the financial sector including rural and microfinance. An expected output under subprogram II will be the commencement of the professional training courses to a wide range of financial institutions. Specifically, NBTI aims to commence its short- term professional training programs first in Kathmandu, then, in other regions, and eventually long-term diploma and degree programs.

10. Enabling rural finance infrastructure. Subprogram II will support the development of credit information services to class D institutions (microfinance NGOs and cooperatives) by the Credit Information Bureau (CIB). CIB will start providing credit information services to Class D institutions and expand its client data from the present 40,000 to 2 million including small borrowers. To make the debt recovery faster and less costly, a capacity development support will be provided to Debt Recovery Tribunal (DRT). DRT capacity development involves skills development of DRT staff in legal and financial management aspect and office automation.

3 Self-help groups are village-based financial intermediaries usually composed of 10–15 local women. Self-help

groups in Nepal are largely unregistered and carry out voluntary savings and credit activities. 4 GBBs started operations by replicating the Grameen model and there are five GBBs (Eastern, Far-Western,

Central, Mid-Western, and Western GBB).

3

II. IMPLEMENTATION PLANS

A. Program Readiness Activities

11. The progress of the program readiness activities is summarized in Table 1. Overall, substantial part of the program readiness activities have completed and the Program expects no significant delays in the loan and grant effectiveness and program inception.

Table 1: Program Readiness Filter

Key Control Area Yes No N/A Indicators of achievement

Design Stage

1. Clear strategic approach with linkage to government's development strategy and CSP

X Nepal CSP (2010–2012)

2. Project is in government's priority 1 level X Nepal CSP

(2010–2012)

3. Institutional assessment undertaken to assess EA/IA capacity X RRP

4. Action plan for land acquisition and resettlement discussed X

5. Focal Point for the loan appointed by the EA X RRP

6. Draft project implementation and financial manual prepared X PAM

7. Draft result monitoring mechanism developed with collection of baseline data

X RRP/PAM

8. Engineering design for first year of activity prepared X

9. Cofinancing arrangements explored X

Fact-finding

10. Action plan for environment impact assessment and social impact assessment agreed

X RRP

11. Action plan for land acquisition and resettlement agreed X

12. TOR/RFP modality for consultant recruitment discussed X RRP/PAM

13. Cofinancing arrangements confirmed X

14. Draft audit arrangement and Terms of Reference discussed X RRP/PAM

Appraisal Stage

15. Budget and funding for the 1st year of project implementation agreed X RRP

16. Prepared procurement plan X RRP

17. Prepared disbursement plan X

To be prepared during the inception

18. Bid documents for first year of project prepared (Civil works/goods) X

4

Key Control Area Yes No N/A Indicators of achievement

19. EOI for consultant recruitment agreed and shortlisted ready X

To be prepared after the loan effectiveness.

Loan Negotiation Stage

20. Finalized project implementation and finalized manual X PAM

21. Finalized results monitoring mechanism X RRP

22. Project implementation unit established with appointment of Project Manager and key project staffs

X RRP

23. Request for Proposal issues to shortlisted consultants X To be done after the loan effectiveness.

24. Draft Project Administration Memorandum prepared X PAM

25. Project steering and coordination committees established X RRP

26. Draft bidding documents submitted to ADB (Civil works/goods) X To be done after the loan effectiveness.

CPS = Country Partnership Strategy, PAM = Program Administration Manual, RRP = Report and Recommendation of the President to the Board of Directors. Source: Asian Development Bank estimates.

B. Overall Program Implementation Plan

12. The two cluster subprograms of RFSDCP will be implemented over 5 years. Subprogram I is implemented for November 2006–December 2009.5 Subprogram II will be implemented for 2 years from 2010–2012. The program implementation schedule is in Table 2.

5 RFSDCP subprogram I became effective on 4 November 2006. The program loan of subprogram I was closed on

22 December 2007. The closing date of the project grant of subprogram I was 30 December 2008, but was extended to 31 December 2009.

5

Table 2: Rural Finance Sector Development Cluster Program Implementation Schedule

Component/Activity N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

Preparatory ActionsEstablishment of program management unitEstablishment of program implementation unitsRecruitment of consultants

1. Subprogram I1.1. Creating a Favorable Policy Environment1.1.a. Policy review committee constituted1.1.b. Policy review on emerging rural finance (RF) issues

1.2. Institutional Restructuring and Reforms1.2.a. Agriculture Development Bank Limited (ADBL) restructuring and reforms1.2.a. (i). First Phase ADBL restructuring plan implementation1.2.a. (ii). Procurement and Installation of MIS

1.2.b. Small Farmers Development Bank (SFDB) restructuring and reforms1.2.b. (i). Finalization of the SFDB restructuring plan1.2.b. (ii). Staff capacity development training1.2.b. (iii). Realigning accounting and auditing1.2.b. (iv). Microfinance (MF) business process improvement1.2.b. (v). Implementation of the SFDB restructuring plan1.2.b.(vi). Review of restructuring and reforms

1.3. Grameen Bikash Bank (GBB) Plan Implementation1.3.a. GBB plan implementation1.3.b. GBB plan implementation review

1.4. Supportive Legal and Regulatory Framework1.4.a. Review of Microfinance Act1.4.b. Redrafting the Act1.4.c. Adoption of the regulation and supervision system1.4.d. Development of regulations 1.4.e. Establishment of the supervisory authority1.4.f. Procurement of management information system1.4.g. Development of supervision and regulation manuals1.4.h. Licensing and supervision of MF institutions

1.5. Sector Capacity Building1.5.a. Incorporation of the training institute1.5.b. Training curriculum development1.5.c. Procurement of equipment, etc.1.5.d. Training of trainers1.5.e. Banking and finance training

1.6. Product and Process Innovation1.6.a. Pilot insurance plan development1.6.b. Pilot insurance plan implementation1.6.c. Product development support for RFIs

1.7. Project Implementation Support

Completed Activities

Ongoing Activities

20112006 2007 2008 2009 2010Years

6

Component/Activity N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J

2. Subprogram I Review and Subprogram II Formulation

3. Subprogram IIª2.1 Supportive Legal and Regulatory Framework2.1.a. (i) Drafting the Micro Finance Act2.1.a. (ii) Establishment of Rules, Regulations, and Processes for Supervision and Regulation2.1.a (iii) Incorporation of Regulatory Authority2.1.a (iv) Training and Information Dissemination to Rural and Microfinance Instituitons2.1.a (v) Licensing and supervision of rural and microfinance institutions

2.2 Institutional Restructuring and Reforms2.2.a. ADBL restructuring and reforms 2.2.a.(i) Adoption of the ADBL Capital Restructuring Plan2.2.a (ii) Reduction of the Accumulated losses2.2.a (iii) Implementation of the second phase ADBL Restructuring Plan2.2.a.(iv) Implementation of the ADBL Capital Restructuring Plan2.2.a. (v) Review of the ADBL Financial and Operational Performances2.2.a (vi) Review of the Implementation of the ADBL Capital Restructuring Plan2.2.a. (vi) Performance Review of the Implementation of the Second Phase Restrucutring Plan

2.2.b. SFDB restructuring and reforms2.2.b.(i). Implementation of the SFDB Restructuring Plan2.2.b.(ii). Review of SFDB Financial and Operational Perforamcnes2.2.b.(iii). Development of a SFDB Divestment Plan for an Initial Public Offering2.2.b.(iv). Licensing as a Class B Financial Instituiton

2.3. GBB Plan Implementation2.3.a. Divestment of the NRB Shares at the Far Western GBBs2.3.b. Review of the GBB Financial and Opertional Performances

2.4. Sector Capacity Building2.4 (i) Constituiton of the NBTI Board of Directors2.4 (ii) Apointment of the NBTI Management2.4 (iii) Commencement of Training Programs in Kathmandu area2.4 (iii) Commencement of Training Programs in Other Regions2.4 (iv) Commencement of Diploma and Degree Programs

2.5. Enabling Rural Finance Infrastructure2.5. a Capacity Building at Credit Information Bureau2.5.(i) Marketing Strategy Development for Microfinance Institutions2.5.(ii) Product Development for Microfinance Institutions2.5 (iii) Operation of Microfinance Unit

2.5.b Capacity Building at Debt Recovery Tribunal2.5. (i) Debt Recovery Tribunal Capacity Development Plan 2.5. (ii) Implementation of Debt Recovery Tribunal Capacity Development Plan

2.6. Project Implementation Supportª Tentative; the implementation of Subprogram II is subject to the review of Subprogam I to be carried out in 2009. Source: Asian Development Bank estimates.

2010 2011 2012Years 2006 2007 2008 2009

7

III. PROGRAM MANAGEMENT ARRANGEMENTS

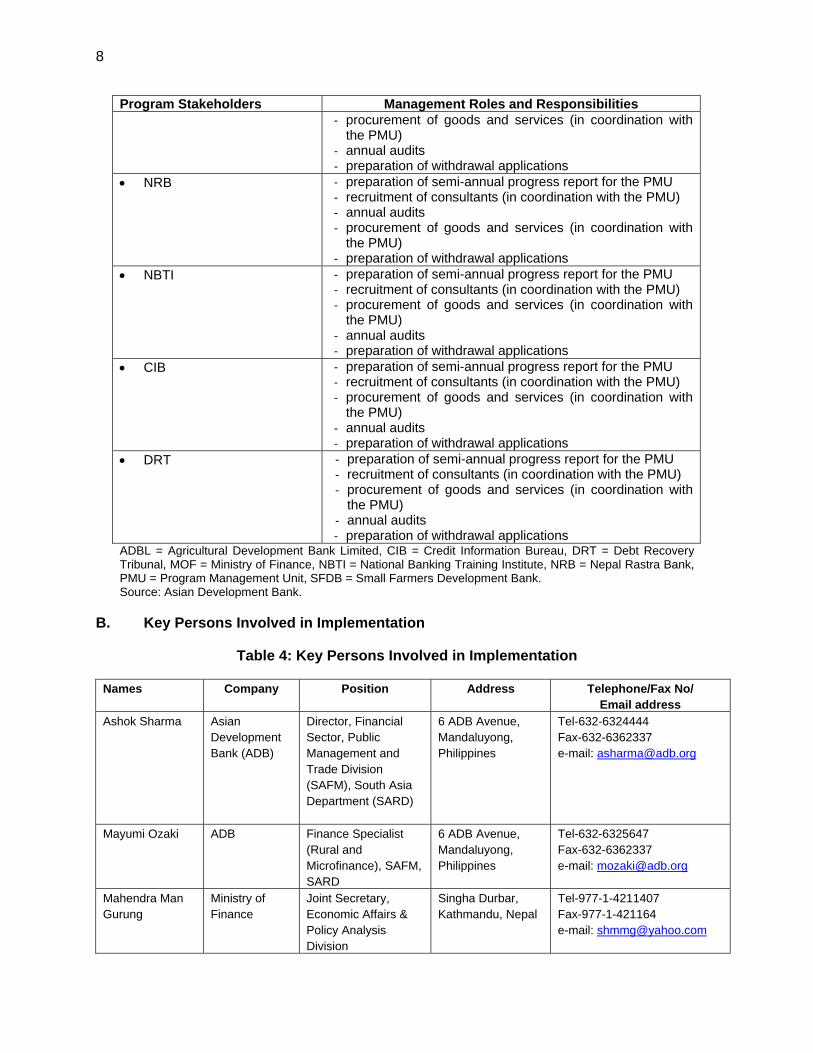

A. Program Stakeholders–Roles and Responsibilities

13. Following the implementation arrangement of subprogram I, the Ministry of Finance (MOF) will be the executing agency for subprogram II and responsible for overall coordination, implementation and monitoring of subprogram II. The program management unit (PMU) established under subprogram I will continue to function as the PMU for subprogram II. 14. ADBL, CIB, DRT, NBTI, NRB and SFDB will be the implementing agencies. ADBL and SFDB will be the implementing agency for the institutional reform and restructuring, CIB and DRT for the enabling rural finance infrastructure, NBTI for the sector capacity building, and NRB for the supportive legal and regulatory framework. For ADBL, NBTI, and NRB the project implementing unit (PIU) established under subprogram I will be continued for subprogram II. CIB, DRT and SFDB will establish the PIU to implement its component. To facilitate the implementation of policy and institutions reforms under its responsibilities, each implementing agency will have a PIU director supported by at least one specialist staff member, with qualifications and experience acceptable to the Asian Development Bank (ADB). The PIUs will (i) ensure smooth implementation of the Project, (ii) produce and submit progress reports on time, and (iii) liaise with the PMU for the implementation of the Project. The PIU directors will report to the program director. 15. Overall implementation of RFSFDP is governed by the program steering committee (PSC) established under subprogram I. PSC is chaired by the MOF Secretary, with membership comprising the chief executive officer of ADBL; chief executive officer of CIB; chairperson of DRT; chief executive officer of NBTI; chief executive officer of SFDB; PMU program director from MOF; senior representatives of the National Planning Commission; and Deputy Governor of NRB. Key functions of the PSC are to (i) provide policy and technical guidance to the PMU and the PIUs, (ii) review the progress of program implementation, (iii) monitor the performance of the PMU and the PIUs, and (iv) ensure program coordination. The PSC meets on a regular basis.

Table 3: Program Stakeholders–Roles and Responsibilities

Program Stakeholders Management Roles and Responsibilities MOF - organizing the program steering committee meetings

- submission of semi-annual progress report - management and replenishment of imprest account - submission of annual audit report - recruitment of consultants

ADBL - implementation of the restructuring plan - coordination for the implementation of the capital

restructuring plan - preparation of semi-annual progress report for the PMU - recruitment of consultants (in coordination with the PMU) - procurement of goods and services (in coordination with

the PMU) - annual audits - preparation of withdrawal applications

SFDB - implementation of the restructuring plan - implementation of the strategies for hills and mountains - preparation of semi-annual progress report for the PMU - recruitment of consultants (in coordination with the PMU)

8

Program Stakeholders Management Roles and Responsibilities - procurement of goods and services (in coordination with

the PMU) - annual audits - preparation of withdrawal applications

NRB - preparation of semi-annual progress report for the PMU - recruitment of consultants (in coordination with the PMU) - annual audits - procurement of goods and services (in coordination with

the PMU) - preparation of withdrawal applications

NBTI - preparation of semi-annual progress report for the PMU - recruitment of consultants (in coordination with the PMU) - procurement of goods and services (in coordination with

the PMU) - annual audits - preparation of withdrawal applications

CIB - preparation of semi-annual progress report for the PMU - recruitment of consultants (in coordination with the PMU) - procurement of goods and services (in coordination with

the PMU) - annual audits - preparation of withdrawal applications

DRT - preparation of semi-annual progress report for the PMU - recruitment of consultants (in coordination with the PMU) - procurement of goods and services (in coordination with

the PMU) - annual audits - preparation of withdrawal applications

ADBL = Agricultural Development Bank Limited, CIB = Credit Information Bureau, DRT = Debt Recovery Tribunal, MOF = Ministry of Finance, NBTI = National Banking Training Institute, NRB = Nepal Rastra Bank, PMU = Program Management Unit, SFDB = Small Farmers Development Bank. Source: Asian Development Bank.

B. Key Persons Involved in Implementation

Table 4: Key Persons Involved in Implementation

Names Company Position Address Telephone/Fax No/ Email address

Ashok Sharma Asian Development Bank (ADB)

Director, Financial Sector, Public Management and Trade Division (SAFM), South Asia Department (SARD)

6 ADB Avenue, Mandaluyong, Philippines

Tel-632-6324444 Fax-632-6362337 e-mail: [email protected]

Mayumi Ozaki ADB Finance Specialist (Rural and Microfinance), SAFM, SARD

6 ADB Avenue, Mandaluyong, Philippines

Tel-632-6325647 Fax-632-6362337 e-mail: [email protected]

Mahendra Man Gurung

Ministry of Finance

Joint Secretary, Economic Affairs & Policy Analysis Division

Singha Durbar, Kathmandu, Nepal

Tel-977-1-4211407 Fax-977-1-421164 e-mail: [email protected]

9

Names Company Position Address Telephone/Fax No/ Email address

Vishnu Nepal

Nepal Rastra Bank

Executive Director, Microfinance Department

Baluwatar, Kathmandu, Nepal

T-977-1-4413136 F-977-1-4412224 e-mail: [email protected]

Shyam Singh Panday

Agricultural Development Bank Limited

Chief Executive Officer

Ramshah Path Kathmandu Nepal

Tel-977-1-4262690/4252359/4252360 Fax-977-1-4262929 e-mail: [email protected]

Jalan Kumar Sharma

Sana Kisan Bikas Bank Limited

Chief Executive Officer

Subidhanagar Kathmandu P.O. Box 21956 Nepal

Tel-977-1-4111828/4111752 Fax-977-1-4111901 e-mail: [email protected]

Anil Chandra Adhikari

Credit Information Bureau

Chief Executive Officer

Heritaze Plaza, 4th Floor, Kamaladi Kathmandu Nepal

Tel-977-1-4222855/4263073 Fax-977-1-4230868 e-mail: [email protected]

Gokul Prasad Burlakoti

Debt Recovery Tribunal

Chairperson

Kamalpokhari Kathmandu Nepal

Tel-977-1-4441432 Fax-977-1-4441418 e-mail: [email protected]

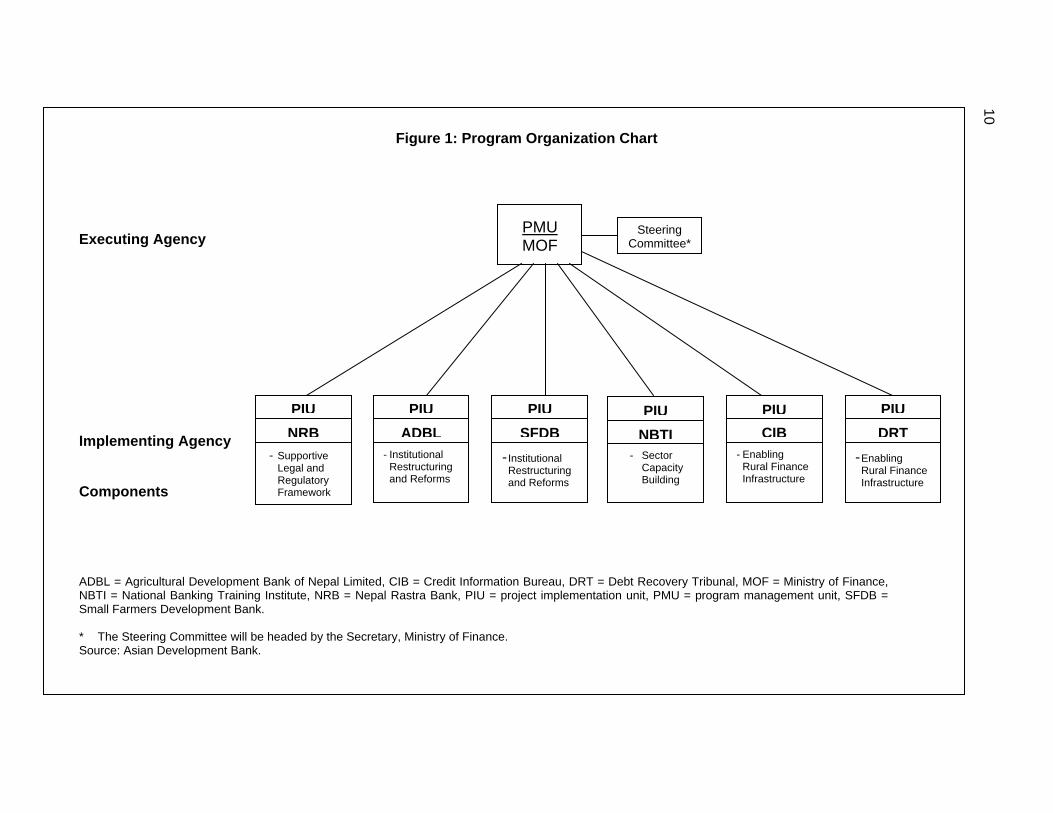

C. Program Organization Structure

16. The program organization structure is in Figure 1.

10

10

Figure 1: Program Organization Chart

Executing Agency

Implementing Agency

Components

ADBL = Agricultural Development Bank of Nepal Limited, CIB = Credit Information Bureau, DRT = Debt Recovery Tribunal, MOF = Ministry of Finance, NBTI = National Banking Training Institute, NRB = Nepal Rastra Bank, PIU = project implementation unit, PMU = program management unit, SFDB = Small Farmers Development Bank. * The Steering Committee will be headed by the Secretary, Ministry of Finance. Source: Asian Development Bank.

PMU MOF

Steering Committee*

PIU

NRB

- Supportive Legal and Regulatory Framework

PIU

ADBL

PIU PIU

NBTI- Sector

Capacity Building

CIB- Enabling

Rural Finance Infrastructure

- Institutional Restructuring and Reforms

PIU

SFDB

- Institutional Restructuring and Reforms

PIU

DRT

- Enabling Rural Finance Infrastructure

11

IV. COSTS AND FINANCING

A. The Program Loan

17. The total approved amount for the RFSDCP cluster was $91 million comprising a program loan of $56 million for subprogram I and $35 million for subprogram II. Under subprogram I, ADB provided a loan of $56 million from its Asian Development Fund resources. The Government used the entire program loan proceeds of subprogram I to recapitalize ADBL through cash subscription of additional preference shares equivalent of NRs3.7 billion. The program loan amount for subprogram II is increased to $60.4 million, thus increasing the total amount for the RFSDCP cluster to $116.4 million. 18. For subprogram II, ADB will provide a loan of $60.4 million from its Asian Development Fund resources with a term of 24 years, including a grace period of 8 years. The loans will have an annual interest rate of 1.0% during the grace period and 1.5% thereafter, as well as other terms and conditions set forth in the Loan Agreement. B. The Project Grant

19. The project cost is estimated at the equivalent of $14.2 million. The Government and counterpart contributions include counterpart staff salaries, office expenses, training, local travel, and other costs.

1. Cost Estimates by Expenditure Category

Table 5: Cost Estimates by Expenditure Category ($ '000)

Item

Total Cost Total Cost (%) A. Investment Costsa 1. Equipment a. Office Equipment 180.00 1.27 b. MIS Package 5,445.00 38.33 Subtotal 5,625.00 39.60 2. Training 292.50 2.06 3. Consulting Services a. International 1,721.70 12.12 b. National 2,313.20 16.29 Subtotal 4,034.90 28.41 4. Credit Line 2,400.00 16.90 5. Taxes and Duties 657.50 4.63 Total Investment Costs 13,009.90 91.60 B. Recurrent Costs 1. Management Support 400.00 2.82 Total Recurrent Costs 13,409.90 94.41 C. Contingencies Physical Contingenciesb 550.50 3.87 Price Contingenciesc 243.50 1.71 Total 14,203.90 100.00

MIS = management information system. a October 2009 prices. b 5% on all expenditure accounts except credit line. c 1.0% falling to 0% on foreign exchange and 8.0% falling to 6.5% on local currency. Source: Asian Development Bank estimates.

12

2. Allocation and Withdrawal of Grant Proceeds

Table 6: Allocation and Withdrawal of Gran Proceeds

Asian Development

Bank

Participating Financial

Institutions

Government of

Nepal

Total

Institutions $'000 % $'000 % $'000 % $'000 % A. Institutional Restructuring and Reforms

1. Agricultural Development Bank Limited 5,159.3 89.5 42.5 0.7 565.6 9.8 5,767.4 40.6 2. Small Farmers Development Bank 2,911.3 85.7 400.0 11.8 85.3 2.5 3,396.6 23.9

Subtotal 8,070.7 88.1 442.5 4.8 650.9 7.1 9,164.0 64.5 B. Supportive Legal and Regulatory Framework 1. Nepal Rastra Bank 347.5 79.2 42.5 9.7 48.9 11.1 438.9 3.1

C. Sector Capacity Building 1. National Banking Training Institute 1,287.4 91.7 42.5 3.0 73.8 5.3 1,403.7 9.9 D. Enabling Rural Finance Infrastructure

1. Credit Information Bureau 1,899.5 90.0 0.0 0.0 211.1 10.0 2,110.5 14.9

2. Debt Recovery Tribunal 371.5 76.6 42.5 8.8 71.0 14.6 485.0 3.4 Subtotal 2,271.0 87.5 42.5 1.6 282.0 10.9 2,595.5 18.3

E. Project Management Support 1. Ministry of Finance 123.5 20.5 0.0 0.0 478.3 79.5 601.8 4.2

Total 12,100.0 85.2 569.9 4.0 1,534.0 10.8 14,203.9 100.0 Source: Asian Development Bank estimates.

3. Expenditure Accounts by Financier

Table 7: Expenditure Accounts by Financier

Asian Development

Bank

Participating Financial

Institutions

Government of Nepal

Total

$'000 % $'000 % $'000 % $'000 % I. Investment Costs A. Equipment 1. Office Equipment 24.5 11.3 169.9 78.7 21.6 10.0 216.0 1.5 2. MIS Package 5,745.8 90.0 0.0 0.0 638.4 10.0 6,384.3 44.9 Subtotal 5,770.3 87.4 169.9 2.6 660.0 10.0 6,600.2 46.5 B. Training 330.9 90.0 0.0 0.0 36.8 10.0 367.7 2.6 C. Consulting Services

1. International 1,827.2 100.0 0.0 0.0 0.0 0.0 1,827.2 12.9 2. National 2,171.5 85.0 0.0 0.0 384.6 15.0 2,556.1 18.0 Subtotal 3,998.8 91.2 0.0 0.0 384.6 8.8 4,383.4 30.9 D. Credit Line 2,000.0 83.3 400.0 16.7 0.0 0.0 2,400.0 16.9

Total Investment Costs 12,100.0a 88.0 569.9 4.1 1,081.4 7.9 13,751.3 96.8 II. Recurrent Costs A. Management Support 0.0 0.0 0.0 0.0 452.6 100.0 452.6 3.2 Total Recurrent Costs 0.0 0.0 0.0 0.0 452.6 100.0 452.6 3.2

Total 12,100.0 85.2 569.9 4.0 1,534.0 10.8 14,203.9 100.0 MIS = management information system. a Inclusive of taxes and duties. Source: Asian Development Bank estimates.

13

4. Expenditure Accounts by Components

Table 8: Expenditure Accounts by Components

Total Costs Item

Total Cost ($ million) (%)

Base Cost A. Institutional Restructuring and Reforms

1. Agricultural Development Bank of Nepal 5.40 38.03 2. Small Farmers Development Bank 3.30 23.24 B. Supportive Legal and Regulatory Framework 0.40 2.82 C. Sector Capacity Building 1.30 9.15 D. Enabling Rural Finance Infrastructure

1. Credit Information Bureau 2.00 14.08 2. Debt Recovery Tribunal 0.50 3.52 E. Project Management Support 0.50 3.52

Total Base Cost 13.40 94.37 1. Physical Contingencies 0.60 4.23 2. Price Contingencies 0.20 1.41

Total Cost To Be Financed 14.20 100.00 Source: Asian Development Bank estimates.

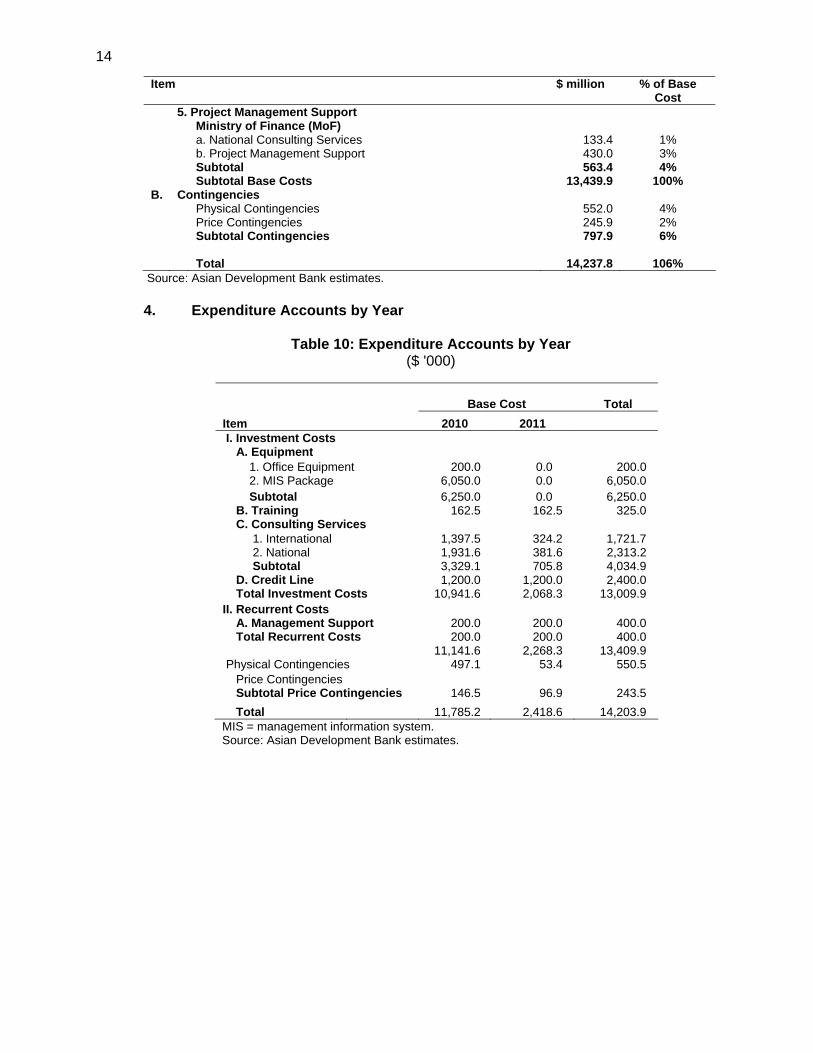

Table 9: Cost Estimates by Component, Institution and Expenditure Category Item $ million % of Base Cost A. Base Cost 1. Institutional Restructuring and Reform Agricultural Development Bank Limited (ADBL) a. Equipment 3,800.0 28% b. International Consulting Services 560.4 4% c. National Consulting Services 1,052.8 8% Subtotal 5,413.2 40% Small Farmers Development Bank (SFDB) a. Equipment 250.0 2% b. International Consulting Services 329.2 2% c. National Consulting Services 345.6 3% d. Credit Line 2,400.0 18% Subtotal 3,324.8 25% 2. Support Legal and Regulatory Framework Nepal Rastra Bank (NRB) a. Equipment 100.0 1% b. International Consulting Services 89.0 1% c. National Consulting Services 217.8 2% Subtotal 406.8 3% 3. Sector Capacity Building National Banking Training Institute (NBTI) a. Equipment 50.0 0% b. Training 325.0 2% c. International Consulting Services 743.2 6% d. National Consulting Services 175.3 1% Subtotal 1,293.5 10% 4. Enabling Rural Finance Infrastructure Credit Information Bureau (CIB) a. Equipment 2,000.0 15% Subtotal 2,000.0 15% Debt Recovery Tribunal (DRT) a. Equipment 50.0 0% b. National Consulting Services 388.2 3% Subtotal 438.2 3%

14

Item $ million % of Base Cost 5. Project Management Support Ministry of Finance (MoF) a. National Consulting Services 133.4 1% b. Project Management Support 430.0 3% Subtotal 563.4 4% Subtotal Base Costs 13,439.9 100% B. Contingencies Physical Contingencies 552.0 4% Price Contingencies 245.9 2% Subtotal Contingencies 797.9 6% Total 14,237.8 106%

Source: Asian Development Bank estimates.

4. Expenditure Accounts by Year

Table 10: Expenditure Accounts by Year ($ '000)

Base Cost Total

Item 2010 2011 I. Investment Costs A. Equipment 1. Office Equipment 200.0 0.0 200.0 2. MIS Package 6,050.0 0.0 6,050.0 Subtotal 6,250.0 0.0 6,250.0 B. Training 162.5 162.5 325.0 C. Consulting Services 1. International 1,397.5 324.2 1,721.7 2. National 1,931.6 381.6 2,313.2 Subtotal 3,329.1 705.8 4,034.9 D. Credit Line 1,200.0 1,200.0 2,400.0 Total Investment Costs 10,941.6 2,068.3 13,009.9 II. Recurrent Costs A. Management Support 200.0 200.0 400.0 Total Recurrent Costs 200.0 200.0 400.0 11,141.6 2,268.3 13,409.9 Physical Contingencies 497.1 53.4 550.5 Price Contingencies Subtotal Price Contingencies 146.5 96.9 243.5

Total 11,785.2 2,418.6 14,203.9 MIS = management information system. Source: Asian Development Bank estimates.

15

5. Fund Flow Diagram

Figure 2: Funds Flow Chart for Imprest Account

V. FINANCIAL MANAGEMENT A. Financial Management Assessment

20. While the legal and institutional arrangements of the Government's public financial management are adequate, its implementation capacity is accessed weak. However, the Government had initiated a comprehensive public financial management reform program and various achievements were made reducing the overall vulnerability in the public financial management. All the formal financial institutions in Nepal are supervised by NRB and under the rigorous inspections with various financial reporting requirements. NRB's supervisory capacity has improved over the years under the Government's Financial Sector Reform Program. B. Disbursement

1. The Program Loan

21. In accordance with the provisions of ADB’s Simplification of Disbursement Procedures and Related Requirements for Program Loans, 6 the proceeds of the program loan will be disbursed to the Government as the Borrower. The proceeds of the program loan will be utilized to finance the full foreign exchange costs (excluding local duties and taxes) of imports produced in, and procured from, ADB’s member countries, other than those specified in the list of ineligible items and imports financed by other bilateral and multilateral sources. No supporting import documentation will be required if, during each year that loan proceeds are expected to be disbursed, the value of total imports minus imports from nonmember countries, ineligible

6 ADB. 1998. Simplification of Disbursement Procedures and Related Requirements for Program Loans. Manila.

$5,159,300

$371,500

Ministry of Finance

$2,911,300 Credit Information

Bureau

Debt Recovery Tribunal

Asian Development Bank

Nepal Rastra Bank

$347,500

$1,899,500

$123,500

Imprest Account

$1,287,400

Withdrawal Application

Replenishment

Agricultural Development Bank Limited

Small Farmers Development Bank Limited

National Banking Training Institute

Source: Asian Development Bank.

16

imports, and imports financed under other official development assistance, is equal to or greater than the amount of the grant and loan expected to be disbursed during such year. The Government will certify its compliance with this formula with its withdrawal request. The policy loan proceeds will be disbursed based on the certification provided by the Government, which confirms that the requirements for the policy loan have been met. ADB will have the right to audit the use of the loan proceeds, and to verify the accuracy of the Government’s certification.

2. The Project Grant

22. Immediately after the effectiveness date of the grant, an imprest account denominated in US dollars will be established at NRB. The imprest account will be operated and maintained in accordance with ADB’s Handbook on Loan Disbursements (January 2007). ADB will advance into the imprest account 6 months of estimated expenditures, or 10% of the grant amount, whichever is lower. The Government uses the imprest account to pay contractors, suppliers, and others for ADB’s share of eligible project expenditures incurred in local and foreign currency. ADB’s statement of expenditure procedure will be used to reimburse eligible expenditures, and to liquidate and replenish the imprest account for individual payments not exceeding $50,000. The second generation imprest accounts opened by ADBL and NBTI will continue to be used to receive the funds from the project imprest account. C. Accounting and Auditing

23. Accounts, auditing, and reporting. The PMU will maintain separate records and accounts for the imprest fund and project expenditure in accordance with sound accounting principles, and will have such accounts and records audited annually by auditors acceptable to ADB. Auditors satisfactory to ADB will audit the use of the imprest account, the second generation imprest accounts, and statement of expenditures procedures. The Government is requested to submit the audited financial statements for project accounts and imprest funds to ADB not more than 6 months following the end of the fiscal year. Independent auditors acceptable to ADB will audit ADBL, CIB, DRT, NBTI, NRB, and SFDB accounts annually. The Government will ensure that audited accounts will be submitted to ADB within 6 months of the end of financial year. Audited financial and operational information will be made available on the websites of respective institutions. The audit reports will include a separate opinion on the use of imprest accounts and the statement of expenditure procedure. 24. The PMU will submit reports to ADB on the use of the loan proceeds, project administration, and financial management. The reports will be submitted quarterly and annually. The reports will cover (i) information on project expenditures, (ii) project progress by component and by institutions, (iii) activities by consultants, (iv) progress in policy and institutional reform actions, and (v) any outstanding issues and concerns. The project completion report will be submitted to ADB within 3 months of project completion.

VI. PROCUREMENT AND CONSULTING SERVICES

A. Procurement of Goods, Works and Consulting Services

25. The procurement of goods, related services, and works financed by the grant will follow procedures outlined in the ADB’s Procurement Guidelines (February 2007 as amended from time to time). Goods and equipment for an MIS package for ADBL and CIB, estimated to cost $500,000 equivalent or more per contract, will be procured using international competitive bidding. Goods and equipment contracts estimated to cost between $100,000 and $500,000 will be procured through national competitive bidding. Goods and equipment to be procured through national competitive bidding include all types of office furniture, computer (stand-alone),

17

computer peripherals, and office equipment. Contracts that cost $100,000 or less may be procured through shopping. Before commencement of national competitive bidding, ADB and the Government will review the Government’s procurement procedures to ensure consistency with ADB requirements. Any necessary modifications or clarifications to the Government’s procedures will be documented in the procurement plan. 26. Consulting services will be procured in accordance with ADB’s Guidelines on the Use of Consultants (February 2007 as amended from time to time). The Project will finance approximately 59 person-months of international consulting services and 330 person-months of national consulting services. Where firms are to be engaged, the quality- and cost-based selection method with 80:20 of quality and cost ratio will be used for selecting consultants. For the consultant recruitment package over $1 million will be recruited using full technical proposals; for packages over $600,000 and below $1 million, simplified technical proposals; for ones below $600,000, biodata technical proposals. Details of the consultant recruitment packages are in the procurement plan. B. Procurement Plan

1. Project Procurement Thresholds

27. Except as the ADB may otherwise agree, the following process thresholds shall apply to procurement of goods and works.

Table 11: Procurement of Goods and Works

Method Threshold International Competitive Bidding for Works More than $1,000,000 International Competitive Bidding for Goods More than $500,000 National Competitive Bidding for Works Less than $1,000,000 above $100,000 National Competitive Bidding for Goods Less than $500,000 above $100,000 Shopping for Works Less than $100,000 Shopping for Goods Less than $100,000 List here any other methods of procurement approved for use (see Section III of the Procurement Guidelines)

Not Applicable

Source: Asian Development Bank.

2. ADB Prior or Post Review 28. Except as ADB may otherwise agree, the following prior or post-review requirements apply to the various procurement and consultant recruitment methods used for the Project.

Table 12: Procurement of Goods and Works

Procurement Method Prior or Post International Competitive Bidding Works Prior International Competitive Bidding Goods Prior National Competitive Bidding Works Post National Competitive Bidding Goods Post Shopping for Works Post Shopping for Goods Post

Recruitment of Consulting Firms Quality and Cost-Based Selection Prior

Recruitment of Individual Consultants Individual Consultants Selection Prior

Source: Asian Development Bank.

18

3. Goods and Works Contracts Estimated to Cost More than $1 Million

29. The following table lists goods and works contracts for which procurement activity is either ongoing or expected to commence within the next 18 months.

Table 13: Goods and Works Contracts General Description Estimated

Contract Value

Procurement Method

Prequalification Of Bidders

Advertisement Date

MIS Package for ADBL $3.75 million ICB No By 15 July 2011 MIS Package for CIB $2 million ICB No By 15 July 2010 ADBL = Agricultural Development Bank Limited, CIB = Credit Information Bureau, ICB = international competitive bidding, MIS = management information system. Source: Asian Development Bank.

4. Consulting Services Contracts Estimated to Cost More than $100,000

30. The following table lists consulting services contracts for which procurement activity is either ongoing or expected to commence within the next 18 months.

19

Table 14: Consulting Services Contracts

General Description

Contract Value

Recruitment Method

Advertisement Date

International or National Assignment

Comments

Consultants for Supportive Legal and Regulatory Framework (NRB)

$0.3 million

QCBS (80:20), BTP

3nd Quarter 2010

International: (i) Rural Finance

Regulation Specialist, 3 pm;

National: (i) Rural Finance

Regulation Specialist (12 pm)

(ii) Audit and Accounting Specialist, (12 pm)

(iii) MIS Specialist,(6pm)

Consultants for Institutional Restructuring and Reforms (ADBL)

$1.6 million

QCBS (80:20), FTP/ICS

3nd Quarter 2010

International: (i) Chief Technical

Advisor, (8 pm); (ii) Strategic

Divestment Specialist, (12 pm)

National: (i) Strategic

Divestment Specialist, (12 pm);

(ii) Human Resource Specialist, (12 pm);

(iii) Accounting and Financial Management Specialist, (12 pm);

(iv) IT Project Manager, (24 pm);

(v) Security and Network Officer, (18 pm);

(vi) CBS Implementation Officer, (18pm);

(vii) Marketing Specialist, (12pm);

(viii) Risk Management Specialist (12 pm)

(ix) Treasury Specialist (12 pm);

(x) Training Specialist (12 pm);

(xi) Trade Finance Specialist (12 pm)

ICS for international consultants; QCBS through a firm for national consultants

20

General Description

Contract Value

Recruitment Method

Advertisement Date

International or National Assignment

Comments

Consultants for Institutional Restructuring and Reforms (SFDB)

$0.67 million

QCBS (80:20), STP/ICS

3nd Quarter 2010

International: (i) Microfinance

Institutions Development Specialist (12 pm).

National: (i) Microfinance and

Banking Operations Specialist (24pm);

(ii) Training Specialist (12 pm);

(iii) MIS Specialist (12 pm)

ICS for international consultant; QCBS for National Consultants

Consultants for Sector Capacity Building (NBTI)

$0.92 million

ICS 3nd Quarter 2010

International: (i) Chief Executive

Officer (24 pm) National: (i) NGO Institutional

Development Specialist (12 pm)

(ii) Banks and Financial Institutions Training Specialist (12 pm)

Consultants for Enabling Rural Finance Infrastructure (DRT)

$0.39 million

ICS 2nd Quarter 2010

National: (i) MIS Specialist (6

pm) (ii) Legal Officer (12

pm) (iii) Financial Officer

(12 pm) (iv) MIS Assistance

(24 pm)

Consultant for Project Management Support (MOF)

$0.13 million

ICS 2nd Quarter 2010

National: (i) Project

Coordinator (18 pm)

ADBL = Agricultural Development Bank Limited, BTP = biodata technical proposal, CBS = core banking system, DRT = Debt Recovery Tribunal, FTP = full technical proposal, ICS = individual consultant selection, IT = information technology, MIS = management information system, MOF = Ministry of Finance, NBTI = National Banking Training Institute, NGO = non Government organization, NRB = Nepal Rastra Bank, QCBS = quality and cost-based selection, SFDB = Small Farmers Development Bank, STP = simplified technical proposal. Source: Asian Development Bank.

21

5. Goods and Works Contracts Estimated to Cost Less than $1 Million and Consulting Services Contracts Less than $100,000

31. The following table groups smaller-value goods, works, and consulting services contracts for which procurement activity is either ongoing or expected to commence within the next 18 months.

Table 15: Goods and Works Contracts and Consulting Services Contracts General Description Value of Contracts

(cumulative) Number of Contracts

Procurement/ Recruitment Method

Office Equipment for NRB/STI $50,000 1 Shopping Office Equipment for ADBL $50.000 1 Shopping Office Equipment for NBTI $50,000 1 Shopping Office Equipment for DRT $50.000 1 Shopping ADBL = Agricultural Development Bank Limited, DRT = Debt Recovery Tribunal, NBTI = National Banking Training Institute, NRB = Nepal Rastra Bank, STI = Second Tier Institution. Source: Asian Development Bank. C. Consultant's Terms of Reference

32. Terms of reference of the international consultants are summarized as below. Terms of reference of national consultants will be developed jointly with the executing and implementing agencies during the inception.

1. Chief Technical Advisor (CTA) for Agricultural Development Bank Limited (International, 8 person-months)

33. The Chief Technical Advisor (CTA) shall have at least 15 years of experience in management, administration, and sound knowledge as well as experiences in development of banks and financial institutions, and must have knowledge on comprehensive aspects of modern banking operations. Familiarity with agricultural finance and involvement as team leader/member in transformation of a Government-owned development bank into a viable and sustainable commercial bank would be an advantage. Working experience in Asia is desirable. She/he will take full responsibility for the successful implementation of the second phase ADBL Restructuring Plan. Reporting directly to the chief executive officer (CEO) and Board of Directors of the ADBL, CTA will undertake:

(i) Support the management and board of directors of ADBL in the implementation of all aspects of the second phase ADBL restructuring plan and ensure the expected ADBL restructuring plan targets and milestones are achieved in a timely manner. Identify any shortfalls in the implementation and devise appropriate remedial measures in consultation with the management and board of directors.

(ii) Advise ADBL management and board of director the complete process to implement the ADBL Capital Restructuring Plan to achieve the expected milestones and targets in view of building appropriate capital base for ADBL’s sustainable and expanded operations.

(iii) Review the ADBL annual business plan and evaluate the financial and operational achievements against the business plan in consultation with ADBL management. Make appropriate dissemination and presentation to the board of director and other key stakeholders to lead to further operational performance improvement of ADBL.

22

(iv) In coordination with the ADBL management and staff, lead the process for developing the annual business plan with realistic targets and milestones. Assist the ADBL management to disseminate the targets of the business plan for effective implementation and monitoring of the plan.

(v) In consultation with the ADBL management and board of directors, review the operational performance of divisions and offices at ADBL, identify skills deficiencies and capacity constraints and develop appropriate training and human resource development plan in coordination with the Human Resource Department.

(vi) In coordination with the ADBL management, periodically review various policies and strategies in use at ADBL, identify areas for updating in view of prevailing laws and regulations and industry best practices. Coordinate with the ADBL management, update and disseminate the new strategies and policies.

(vii) In coordination with the ADBL management and together with the Internal Control Division, monitor ADBL’s compliance with the legal and regulatory requirements and advice appropriate remedial measures if any deficiencies are found.

(viii) Assist and supervise the development, procurement, and commissioning of the core banking system and, in coordination with the Information Technology Division, organize appropriate training and capacity development programs for staff.

(ix) Any other relevant tasks as reasonably requested by the ADBL management, board of directors and ADB.

2. Strategic Divestment Specialist for Agricultural Development Bank Limited (International, 12 person-months)

34. The Strategic Divestment Specialist shall have more than 10 years commercial banking experience as well as in-depth involvement in divestment and privatization of banks and financial institutions. Experience in reform and restructuring of state-owned financial institutions is essential. She/he will take full responsibility for successful implementation of the ADBL Capital Restructuring Plan. Familiarity of the financial sector in South Asia is preferable. Working closely with the CTA, ADBL, MOF, NRB and under the guidance of the PMU director and the Steering Committee, the specialist shall:

(i) Advise ADBL management and board of directors on the complete process to implement the ADBL Capital Restructuring Plan to achieve the expected milestones and targets in view of ADBL's sustainable and expanded operations.

(ii) Assist ADBL and other related agencies (especially MOF and NRB) in the overall coordination for the divestment process to a strategic investor, and prepare and monitor a detailed and time-bound action plan.

(iii) Advise the MOF and NRB during the divestment process and during negotiations.

(iv) Assist in identification and design of specific advisory needs such as legal advice.

(v) Substantially contribute to the updating of the privatization material including the Information Memorandum and other documents as necessary.

(vi) Develop and implement the marketing activities leading to the offering of ADBL, including preparation of press material and participation in marketing trips as required by MOF and NRB.

(vii) Assist the Selection Committee in the process of evaluation of technical aspects of proposals, etc. (viii) Assist ADBL and other related agencies (especially MOF and NRB) with any other tasks reasonably requested by ADBL, MOF and NRB, including post-divestment activities.

23

3. Microfinance Institutions Development Specialist for Small Farmers Development Bank (International, 12 person-months)

35. The Microfinance Institutions Development Specialist shall have more than 10 years of experience in operation, management, and development of banks and financial institutions. Working experience in and knowledge on micro and rural finance and savings and credit cooperatives are essential. Working experience in Nepal or South Asia is desirable. Reporting to and working with the management of the SFDB, the specialist shall:

(i) Support the management of SFDB in the implementation of the second SFDB Restructuring Plan to ensure that the expected targets and milestones are achieved in a timely manner. Identify any shortfall in achieving the target and propose appropriate remedial measures. Assist the SFDB management to achieve the intended capital and ownership restructuring plan with the purpose of ensuring the proper representation and control by member small farmer cooperatives in the management of SFDB.

(ii) Periodically review the progress of the SFDB business plan to ensure the specified financial and operational targets are met. If any shortfall, advice appropriate remedial actions in consultation with the SFDB management.

(iii) Lead the process of annual business plan development with realistic targets and objectives through the wide consultation with member small farmer cooperatives.

(iv) Assisting the SFDB management and staff, and conduct periodical external relation and communication activities specifically to ensure member farmer cooperatives understand the rights and obligations as the owner of SFDB.

(v) Periodically review the all operational aspects and divisions of SFDB and advice measures to improve their performance. If needed, develop appropriate training and human resource capacity development plan in consultation with the SFDB management.

(vi) In coordination with the SFDB management, identify areas for capacity development needs for member small farmers cooperatives and carry out necessary training and capacity development programs for them.

(vii) Any other tasks as reasonably requested by the SFDB management, board of directors, and ADB.

4. Chief Executive Officer, National Banking Training Institute (International, 24 person-months)

35. The CEO shall have as a minimum a master's degree, or its equivalent from a recognized professional institution, in a field relevant to NBTI's business scope; a post-graduate teaching qualification would be an advantage. The CEO also shall have (a) either, not less than 15 years experience in banking of which at least 5 years shall have been as an operational manager and experience as an instructor in a field relevant to banking, financial services and rural finance; or (b) not less than 15 years teaching experience in a field or fields of relevance to banking, financial services, and rural finance at a graduate school. She/he shall be computer literate at an advanced level and must have demonstrably good management skills and the ability to run a team of strong academics. The CEO is accountable to the NBTI Board of Directors for the profitable management of the Institute. The responsibilities of the CEO include, but are not restricted to:

(i) Implementation of the Board of Directors decisions; (ii) Preparation of the Institute’s business plan and annual budget; (iii) Planning and management of NBTI’s day-to-day business activity; (iv) Proactive supervision of NBTI’s activities and those of affiliated institutions;

24

(v) Evaluation of the performance of NBTI and affiliated institutions against business plan targets;

(vi) Formulation and application of remedial action where necessary; (vii) Appointment, development, promotion and, where appropriate, dismissal of NBTI

employees; (viii) Half-yearly assessment of the quality of performance of NBTI employees; (ix) Engagement of outside expertise for special events and short courses designed

to ensure awareness of change in banking, financial services, and rural finance; (x) Representing NBTI as authorized by the Board of Directors; (xi) Reporting to the Board of Directors on the activities of NBTI; (xii) Arrangement of the meetings of the Board of Directors; (xiii) Preparation of NBTI’s annual report; and (xiv) Such other activities for the advancement of NBTI’s interests as the Board of

Directors may reasonably propose.

5. Rural Finance Regulation Specialist (International, 3 person-months)

36. The International Rural Finance Regulation Specialist will have more than 15 years of demonstrated extensive international experience in regulatory issues relating to banking system, particularly in rural credit and microfinance areas. Previous Nepal financial sector-related experience is desirable. Reporting to the Deputy Governor, NRB, the Rural Finance Regulation Specialist will undertake the following:

(i) Based on the agreed draft legal framework and plan for the second tier supervisory authority for rural and microfinance institutions, develop the implementation and business plan of the proposed supervision and regulation system or agency with detailed functions, business process, roles and responsibilities, outsourcing, financing plan, funding requirements, and staffing.

(ii) Ensuring that all recommendations are congruent with the proposed legislation, prepare draft regulations and reporting requirements, formats and procedures for licensed microfinance institutions, and policies and procedures for inspection, defining inter alia: (a) in specific numerical terms the requirements for risk weighted capital

adequacy, provisioning requirements, statutory reserve requirements, loan to deposit ratios, single borrower and other exposure limits;

(b) the format, frequency, and deadlines for reporting; (c) the frequency of inspections and the procedure to be followed; and (d) analysis of inspection reports by the regulatory agency and arrangements

for compliance. (iii) Prepare a microfinance supervision manual, incorporating:

(a) a statement of supervision policies; and (b) a guide for supervisory staff identifying staff responsibilities, timing of

activities and documentation requirements associated with each activity for: the submission, review and analysis of microfinance institution inspection reports; the conduct of on-site inspections; and the actions to be taken in cases of non-compliance.

(iv) Prepare terms of references for staff of the proposed supervisory and regulatory institution or agency.

(v) Organize information dissemination seminars on the proposed draft Act and regulations for staff of NRB, key Government agencies, and microfinance institutions.

(vi) Based on the Manual and Reporting formats, prepare a training course on microfinance institution supervision for staff of the regulatory agency who will

25

assume responsibility in due course, including materials on rationale for policies and procedures including reference to legislation and best practices in the field.

(vii) Develop the capacity development plan for staff of the second tier institution and organize appropriate training programs.

(viii) Other relevant tasks as reasonably requested by NRB, the management, and board of director of the second tier institution and ADB.

VII. SAFEGUARDS

37. The Program expects no negative impacts on environment, resettlement and indigenous people.

VIII. PERFORMANCE MONITORING, EVALUATION, REPORTING AND COMMUNICATION

Table 16: Program Design and Monitoring Framework

Design Summary

Performance Targets/Indicators

Data Sources/Reporting Mechanisms

Assumptions and Risks

Impact Economic growth and poverty reduction in rural areas

Access to credit by rural poor increases from 1 million in 2008 to 1,170,000 by 2012. Access to financial services in the disadvantaged hills and mountain areas increases from 10,000 in 2008 to 30,000 by 2012. Women's access to finance increases from 200,000 in 2008 to 283,000 by 2012.

Economic reform program assessment Baseline study and impact monitoring report Nepal Rastra Bank (NRB) reports Program completion report Asian Development Bank (ADB) evaluation reports Program impact study

Assumptions Stable and favorable macroeconomic conditions Risk Changes in policy environment that discourage further financial sector reform and liberalization

Outcomea Inclusive rural finance system that is more sound and efficient, and has wider outreach

Credit outreach of Agricultural Development Bank Limited (ADBL) increases from 200,000 accounts in January 2010 to 250,000 (of which 20% are women) by 2012. Credit outreach of Small Farmers Development Bank (SFDB) increases from 140,000 accounts in 2008 to 360,000 (of which 60% are women) by the end of 2013. At least 60 cooperatives start providing microcredit in the hills and mountain areas by the end of 2011. National Banking Training Institute (NBTI) provides training to approximately 400 rural finance practitioners annually from 2010. Pending cases at the Debt Recovery Tribunal reduced from 830 in 2008 to 530 by end 2012.

Program reports Program reviews (semiannual, annual, and midterm) Audit reports ADBL reports ADB review missions Program completion report Program performance evaluation report NRB reports Reports of financial institutions Parliamentary briefings Reports of the government auditor general

Assumptions The government’s commitment to market-based economic policy Autonomy and independence of NRB, the central bank The government’s commitment to maintain the financial sector reform policy Risks Unsound political interference by the government in financial institutions Insufficient regulatory enforcement by NRB

26

Design Summary

Performance Targets/Indicators

Data Sources/Reporting Mechanisms

Assumptions and Risks

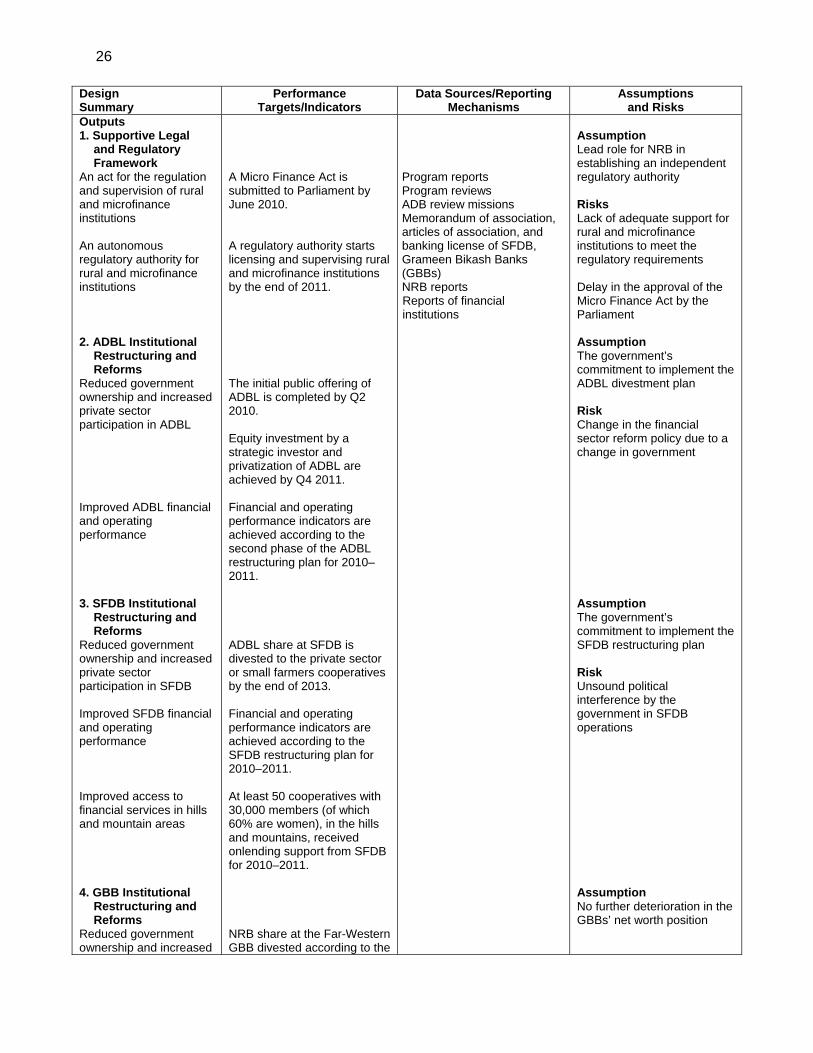

Outputs 1. Supportive Legal

and Regulatory Framework

An act for the regulation and supervision of rural and microfinance institutions An autonomous regulatory authority for rural and microfinance institutions 2. ADBL Institutional

Restructuring and Reforms

Reduced government ownership and increased private sector participation in ADBL Improved ADBL financial and operating performance 3. SFDB Institutional

Restructuring and Reforms

Reduced government ownership and increased private sector participation in SFDB Improved SFDB financial and operating performance Improved access to financial services in hills and mountain areas 4. GBB Institutional

Restructuring and Reforms

Reduced government ownership and increased

A Micro Finance Act is submitted to Parliament by June 2010. A regulatory authority starts licensing and supervising rural and microfinance institutions by the end of 2011. The initial public offering of ADBL is completed by Q2 2010. Equity investment by a strategic investor and privatization of ADBL are achieved by Q4 2011. Financial and operating performance indicators are achieved according to the second phase of the ADBL restructuring plan for 2010–2011. ADBL share at SFDB is divested to the private sector or small farmers cooperatives by the end of 2013. Financial and operating performance indicators are achieved according to the SFDB restructuring plan for 2010–2011. At least 50 cooperatives with 30,000 members (of which 60% are women), in the hills and mountains, received onlending support from SFDB for 2010–2011. NRB share at the Far-Western GBB divested according to the

Program reports Program reviews ADB review missions Memorandum of association, articles of association, and banking license of SFDB, Grameen Bikash Banks (GBBs) NRB reports Reports of financial institutions

Assumption Lead role for NRB in establishing an independent regulatory authority Risks Lack of adequate support for rural and microfinance institutions to meet the regulatory requirements Delay in the approval of the Micro Finance Act by the Parliament Assumption The government’s commitment to implement the ADBL divestment plan Risk Change in the financial sector reform policy due to a change in government Assumption The government’s commitment to implement the SFDB restructuring plan Risk Unsound political interference by the government in SFDB operations Assumption No further deterioration in the GBBs’ net worth position

27

Design Summary

Performance Targets/Indicators

Data Sources/Reporting Mechanisms

Assumptions and Risks

private sector participation at GBBs 5. Sector Capacity

Building NBTI training programs in finance, banking, and rural and microfinance subjects for a wide range of financial institutions 6. Enabling

Infrastructure for Rural Finance

Credit information services to microfinance institutions by Credit Information Bureau Debt Recovery Tribunal capacity development

NRB Act by end-2010 NBTI established and training operations begin by Q2 2010. Regional training began by Q2 2010. Long-term accredited diploma and degree programs begin by Q4 2011. Credit Information Bureau begins credit information services to microfinance institutions by Q1 2011. Debt Recovery Tribunal capacity development support is provided by the end of 2011.

Risk Unsound political interference by the government in GBB operations Assumption Enough demand for training programs at NBTI Risk Declining interest among participating financial institutions to maintain NBTI after the program implementation period Assumption Enough demand from microfinance institutions for credit information service Risk Lack of strong enforcement of debt recovery laws and regulations

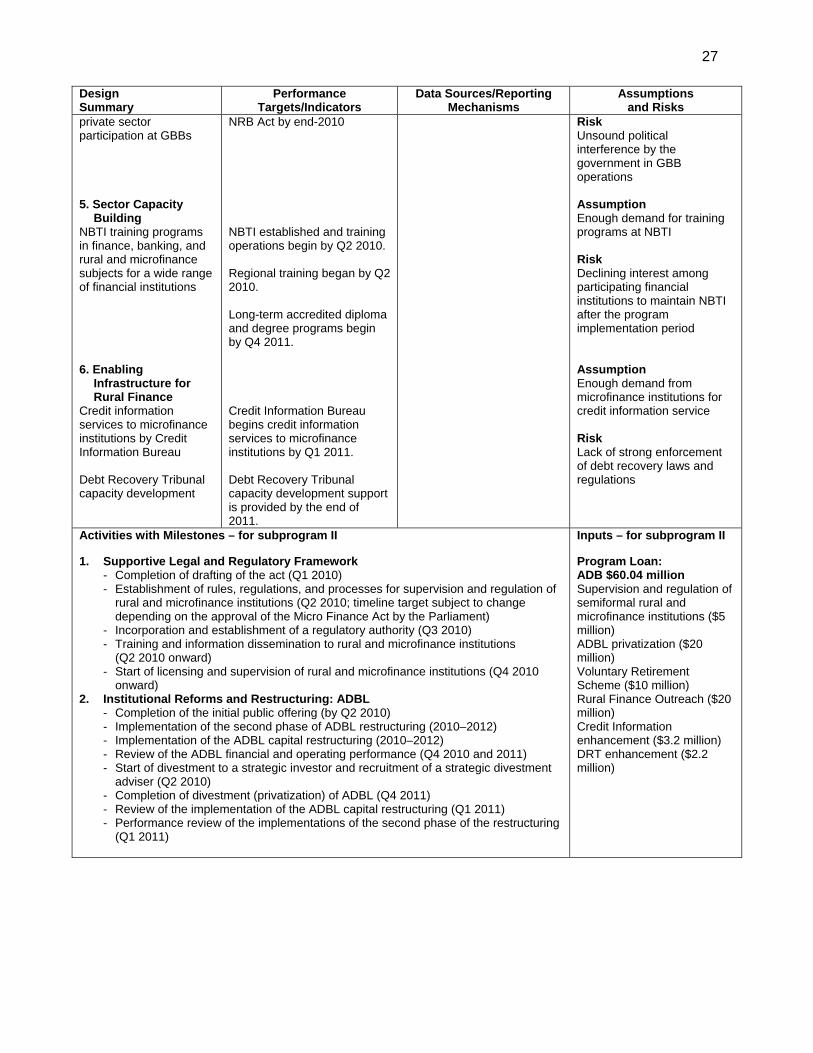

Activities with Milestones – for subprogram II 1. Supportive Legal and Regulatory Framework

- Completion of drafting of the act (Q1 2010) - Establishment of rules, regulations, and processes for supervision and regulation of

rural and microfinance institutions (Q2 2010; timeline target subject to change depending on the approval of the Micro Finance Act by the Parliament)

- Incorporation and establishment of a regulatory authority (Q3 2010) - Training and information dissemination to rural and microfinance institutions

(Q2 2010 onward) - Start of licensing and supervision of rural and microfinance institutions (Q4 2010

onward) 2. Institutional Reforms and Restructuring: ADBL

- Completion of the initial public offering (by Q2 2010) - Implementation of the second phase of ADBL restructuring (2010–2012) - Implementation of the ADBL capital restructuring (2010–2012) - Review of the ADBL financial and operating performance (Q4 2010 and 2011) - Start of divestment to a strategic investor and recruitment of a strategic divestment

adviser (Q2 2010) - Completion of divestment (privatization) of ADBL (Q4 2011) - Review of the implementation of the ADBL capital restructuring (Q1 2011) - Performance review of the implementations of the second phase of the restructuring

(Q1 2011)

Inputs – for subprogram II Program Loan: ADB $60.04 million Supervision and regulation of semiformal rural and microfinance institutions ($5 million) ADBL privatization ($20 million) Voluntary Retirement Scheme ($10 million) Rural Finance Outreach ($20 million) Credit Information enhancement ($3.2 million) DRT enhancement ($2.2 million)

28

Activities with Milestones – for subprogram II 3. SFDB Institutional Reform and Restructuring

- Implementation of the SFDB restructuring plan (2010–2012) - Review of SFDB financial and operating performance (Q4 2010) - Development of the SFDB divestment plan for an initial public offering (Q1 2011) - Cooperative business plan development and capacity development support in the

hills and mountains (Q3 2011) - Self-help group mapping and conversion into cooperatives (Q4 2011) - Onlending support to microfinance nongovernment organizations and cooperatives

(2010–2011) 4. GBB Institutional Reform and Restructuring

- Divestment of NRB shares in the Far Western GBB (Q3 2010) - Completion of the privatization of Western GBB (Q4 2011) - Review of GBB financial and operating performance (Q4 2010)

5. Sector Capacity Building - Incorporation and establishment of NBTI (Q1 2009) - Start of training programs in Kathmandu area (Q2 2010) - Start of training programs in other regions (Q4 2010) - Start of diploma and degree programs (Q4 2011)

6. Enabling Infrastructure for Rural Finance - Staff capacity development and institutional training for microfinance institutions

(Q3–Q4 2010) - Operation of microfinance unit at Credit Information Bureau (Q4 2010) - Recruitment of legal officer, financial officer, MIS specialist, and MIS assistant (Q2–

Q4 2010) for DRT - Development of DRT operating manuals (Q4 2010–Q1 2011) - DRT staff training and workshop (Q4 2010–Q2 2011)

Inputs – for subprogram II Project Grant: ADB $12.1 million Office equipment ($0.2 million) MIS equipment ($5.7 million) International consulting services ($1.8 million) National consulting services ($2.1 million) Training ($0.3 million) Credit line ($2.0 million) Technical Assistance Grant: ADB $200,000 Inputs in: Consultant remuneration ($180,000) Consultant International and Local travel ($8,000) Consultants reports ($1,000) Miscellaneous Administration and Support Costs ($1,000) Contingency ($10,000)

a Sex disaggregated data will be monitored through the existing management information system in each implementing agency.

Source: Asian Development Bank.

A. Monitoring

38. The project performance management system established under subprogram I will continue to be used. The performance management reports will comprise (i) component activities and outputs, (ii) project expenditures and disbursement, (iii) consultant inputs and activities, (iv) procurement, and (v) any outstanding issues. ADBL and SFDB will submit financial reports covering (i) loan portfolio growth and performance; (ii) liability growth and management, especially of savings deposits; (iii) financial performance indicators, including capital adequacy ratio, collection rate, operating profit ratio, and nonperforming loan ratio; (iv) details of the number of borrowers by gender, poverty classification, type of services, and size of transactions; (v) information on the performance of staff, measured by financial volume, number of customers, and earnings ratios; (vi) information on planned and actual levels of activities; and (vii) annual financial statements. 39. ADB and the Government will conduct semiannual reviews throughout the implementation of subprogram II. The review will evaluate the (i) program scope, (ii) implementation arrangements, (iii) implementation of ADBL's restructuring plan, (iv) progress on the policy reform agenda, and (v) capacity building measures. ADB and the Government also will undertake the midterm review to evaluate physical and financial progress, implementation procedures, procurement and performance of consultants, including that of the attached technical assistance.

29

B. Evaluation

40. The Government will submit the program completion report to ADB within 3 months of the program completion. ADB will conduct the program completion mission to assess the overall output and outcome of the policy and institutional reform and derive recommendations to the Government and the sector institutions on actions to further develop the rural finance sector. C. Reporting

41. The sample reporting formats are as follows:

Format for Project Performance Management Report

1. Summary

2. Component Outputs

2.1 Supportive Legal and Regulatory Framework 2.2 Institutional Restructuring and Reforms

2.2.1 Agricultural Development Bank Limited 2.2.2 Small Farmers Development Bank 2.2.3 Grameen Bikash Banks

2.3 Sector Capacity Building 2.4 Enabling Rural Finance Infrastructure

3. Program Management

3.1 Project Expenditures 3.2 Procurement 3.3 Consultant Inputs

3.4 Highlights of Audit Report of ADBL, SFDB 3.5 Disbursement

4. Issues and Recommended Actions

30

Format for Program Performance Monitoring Report: Financial Report

Infrastructure Branch Offices Personnel

Financing Structure Total Assets Total Equity Total Debt Deposits per Voluntary Savings Gross Loan Portfolio Deposits -to-Total Assets Capital Adequacy Ratio

Outreach Number of Active Borrowers Number of Active Women Borrowers Number of Loans Outstanding Number of Active Loan Accounts Loans Outstanding Number of Savers Number of Saving Accounts Number of Women Savers Savings Outstanding Number of Active Women Borrowers per Total Active Borrowers Average Loan Balance per Active Borrower Percentage of Women Savers-to-Total Active Savers

Financial Performance Average total assets Average total equity Adjusted Return-on-Assets Adjusted Return-on-Equity Operational Self-Sufficiency Financial Self-Sufficiency Collection Rate

Operating Efficiency Adjusted Operating Expense Adjusted Personnel Expense Average Gross Loan Portfolio Average Number of Active Borrowers/Clients Average Number of Active Loans/Deposits Adjusted Operating Expense-to-Average Gross Loan Portfolio Adjusted Personnel Expense-to-Average Gross Loan Portfolio Average Salary per Capital Adjusted Cost per Borrower Adjusted Cost per Loan Operating Profit Ratio

Productivity Total Number of Staff Total Number of Loan Officers Borrowers per Staff Loans per Staff Borrowers per Loan Officer Loans per Loan Officer Savers per Staff Savings Accounts per Staff Personnel Allocation Ratio

31

Risk Portfolio at Risk > 30 days Portfolio at Risk > 90 days Nonperforming Ratio Adjusted Loan Loss Reserve Loan Written Off during the year Portfolio at Risk >30 days-to-Gross Loan Portfolio Portfolio at Risk >90 days-to-Gross Loan Portfolio Non Earning Liquid Assets-to-Total Assets

Format for Program Progress Report

Second Tranche Actions

October 2006–December 2008 Status Action to be Taken

IX. ANTICORRUPTION POLICY

42. ADB’s Anticorruption Policy7 was explained to, and discussed with, the Government, ADBL, CIB, DRT, NBTI, NRB, and SFDB. Consistent with its commitment to good governance, accountability, and transparency, ADB reserves the right to investigate, directly or through its agents, any alleged corrupt, fraudulent, collusive, or coercive practices relating to RFSDCP. To support these efforts, relevant provisions of ADB’s Anticorruption Policy are included in the grant regulations and the bidding documents for the Project. In particular, all contracts financed by ADB in connection with RFSDCP shall include provisions specifying the right of ADB to audit and examine the records and accounts of ADBL, CIB, DRT, NBTI, NRB and SFDB and as well as all contractors, suppliers, consultants, and other service providers as they relate to RFSDCP.

43. Specifically, RFSDCP has been designed to reduce vulnerability to corruption by seeking to ensure that: (i) the board of financial institutions are aware of the possibility of corruption and mismanagement in their own institutions, and can demonstrate how they are dealing with these problems; (ii) adequate steps to enhance corporate governance are taken in all relevant institutions; (iii) all relevant institutions and the Government give assurances that they will abide by transparency and disclosure stipulations, as specified by NRB; and (iv) rigorous monitoring mechanisms are put in place to ensure that proper accounting is made continually of, among others, mandated actions and full fund flow management.

7 ADB. 2007. Anticorruption and Integrity: Policies and Strategies. Manila.

32

44. Further, during program implementation, ADB will review regularly the reports of audit authorities to assess (i) the nature of financial and administrative irregularities, (ii) pilferage of funds, and (iii) how the financial institutions have responded to the findings. During regular review missions, governance and anticorruption risks assessments will be updated as necessary.