protecting the pensions of today’s and tomorrow’s participants

TRANSCRIPT

0

Protecting the Pensions of Today’s and

Tomorrow’s Participants

1

Agenda for August 13, 2005Agenda for August 13, 2005

• Introductory Remarks

• Pension Fund Status and Adopted Changes

• Questions and Answers – after lunch

• Dave LaughtonUnion Trustee Co-Chair

• Ed GrodenPension Fund

• Trustees and Pension Fund

2

Current Environment

Current Environment

People are living longer and retiring earlier.

The number of active participants is declining.

Employer contribution hours are declining.

The number of retirees is increasing.

Three year stock market free-fall from 2000 through 2002 hurt Funds throughout the US…and the world.

Increasing Retirees…

10,000

15,000

20,000

25,000

30,000

35,000

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Retirees Actives

Current Environment

Current Environment

…Decreasing Actives

3

4

As Actives have declined…

25,000

26,000

27,000

28,000

29,000

30,000

31,000

32,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

48

50

52

54

56

58

60

62

64

66

ActivesHours

(Millions of H

ours)Current

EnvironmentCurrent

Environment

…so have Contribution Hours

5

NETTIPF Pensioners are retiring earlier…

61

35

9

59

45

16

Avg Age atRetirement

% of New Retirees< 60

% of New Retirees< 55

10 Years Ago Last Year

Current Environment

Current Environment

Current Environment

Current Environment

…and collecting larger benefits over longer periods of time.

$905

$2,884

Average Monthly Benefit

10 Years Ago Last Year

The average The average NETTIPF pension NETTIPF pension benefit rose 219% benefit rose 219% over the past 10 over the past 10 yearsyears

6

7

What’s the Impact?What’s the Impact?What’s the Impact?In every year since 1992, In every year since 1992,

NETTIPF benefit NETTIPF benefit paymentspayments

have been have been greatergreater than than contribution contribution incomeincome..

Current Environment

Current Environment

Contributions Received vs. Benefits Paid

$0$50

$100$150$200$250$300$350$400

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

(in millions $)

8

9

How has the NETTIPF Pension continued to operate with

expenses outpacing income?

By spending reserves and By spending reserves and

relying on investment relying on investment

income to make up the gap. income to make up the gap.

Deficit Spending Is Not Sustainable

-$95.9

-$121.3-$133.0

-$152.0

-$72.1-$56.8

-$38.3-$29.7-$23.6-$21.9

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

(in millions $)

Excess of NETTIPF Fund Benefits Paid over Employer Contributions Received

10

11

NETTIPF Employers No Longer Making Contributions

Consolidated Freightways: BANKRUPTRed Star: CLOSEDSuperValu: SOLD / WITHDRAWNAPA: SHUT DOWN

70% of current retirees last worked for an employer who no longer is making

contributions to the Fund.

How Employer Bankruptcies Impact the Fund

Filed Bankruptcy: September 2, 2002

Pension FundEmployer Withdrawal Liability

• $8 million• Expect to collect $2 million — $6 million

shortfall

CONSOLIDATED FREIGHT

12

13

Consequences of Rising Liabilities and Shrinking Assets

Funding DeficiencyFailure to meet minimum funding level required by federal law.

Deteriorating Funding StatusFully Funded = 100% NETTIPF ratio has dropped to 55%NETTIPF Goal: 90% by 2030

14

…many established …many established Pension Funds face a Pension Funds face a

similar similar —— if not worseif not worse ——situation.situation.

NETTIPF is not alone …NETTIPF is not alone …

15

Many Multiemployer Plans are modifying future accrual rates in response to the funding crisis…

Western Conference of Teamsters Pension TrustCentral States Southeast and Southwest Areas Health and Pension Funds NYS Teamsters Benefit Funds

16

…while others have found they can no longer go it alone.

Company No. of EmployeesBethlehem Steel 95,000LTV Steel 82,000TWA 36,500National Steel 35,000Pillowtex 23,000Grand Union Co. 17,000Anchor Glass Container Corp. 14,000Polaroid Corp. 11,000Outboard Marine Corp. 10,000Reliance Insurance Company 8,800Bradlees 8,000Consolidated Freightways 8,000Durango Apparel 7,000Kaiser Aluminum 5,000

Funds taken over by the federal Pension Benefits Guarantee Corp. (PBGC)

17

The PBGC’s maximum payment for a multi-employer pension is $35.75 per month for each year of credited service.

That equals $1,072 per month for a person with 30 years of service.

Takeover by the PBGC is a last resort.

Takeover by the Takeover by the PBGC is a last resort.PBGC is a last resort.

18

Strengthen the Fund to Strengthen the Fund to protect protect futurefuture pensions.pensions.

GoalsGoals

Protect Protect allall benefits benefits alreadyalreadyearned.earned.

Change Change onlyonly what’s what’s necessary.necessary.

19

1. Reduce Fund’s Administrative Costs

With the move of the Fund Office to Burlington, we’ve reduced annual overhead expenses by about $400,000.

Action PlanAction Plan

20

2. Meet Investment Targets

Actuaries project that the Fund must earn an 8.5% annual return on assets in order to maintain benefits and meet future obligations.

Action PlanAction Plan

21

3. Do Not Change Structure of the Plan

Action PlanAction Plan

Fund Trustees did not change the way the Fund operates, including:

Preserve the highest yearly accruals in the industry.Preserve the right to Early Retirement at age 55 with 15 years of Pension Credit.Preserve All Types of Pensions, Lump Sums,Disability Pensions, Death Benefits, Survivor Pensions for married and unmarried, All Optional Forms of payment, earning of Pension Credit, etc.

22

4. Implement Benefit Modifications

Action PlanAction Plan

After extensive study and discussion, Fund Trustees deemed modifications necessary to safeguard pensions of current and future retirees:

Change only what’s necessary.Protect past accruals.Preserve Special Service and 30-Year Full Service Pensions.Provide a $1,000 “Supplemental” Benefit for qualifying retirees.

23

5. Request relief under IRC Section 412(e)

Action PlanAction Plan

Helps Funds such as NETTIPF continue to meet their ERISA minimum funding requirements.

24

Pensions accrued for pension credit earned prior to July 31, 2005, do NOT change.

All Pensions Accrued Remains As Is

Plan ModificationsPlan Modifications

25

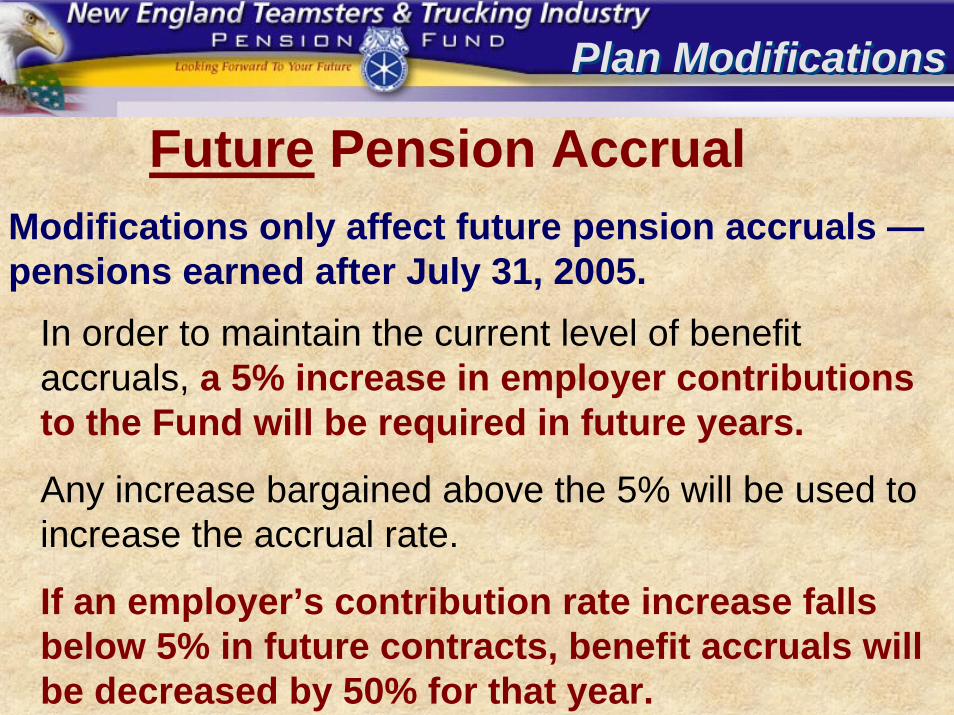

Modifications only affect future pension accruals —pensions earned after July 31, 2005.

Plan ModificationsPlan Modifications

Future Pension Accrual

In order to maintain the current level of benefit accruals, a 5% increase in employer contributions to the Fund will be required in future years.

Any increase bargained above the 5% will be used to increase the accrual rate.

If an employer’s contribution rate increase falls below 5% in future contracts, benefit accruals will be decreased by 50% for that year.

26

Plan ModificationsPlan Modifications

Future Pension AccrualsContracts in effect on 7/31/2005 will automatically satisfy the 5% maintenance of benefits requirement during the remainder of the contract.

For example, if your current contract calls for only a 4% annual increase in the employer contribution rate to the Pension Fund, this 4% will be accepted as satisfying the Fund’s maintenance of benefit requirement until the contract is scheduled to expire and the employer contribution can be negotiated for 5% increases in future years.

27

Plan ModificationsPlan Modifications

Future Pension Accruals

So long as future contracts are negotiated that continue to include 5% annual employer contribution rate increases, participants will not see their future service accruals reduced.

28

Preserve the Special Service and 30-Year Full Service

Pensions…

Plan ModificationsPlan Modifications

…by implementing a minimum retirement age of 57

29

Can still retire at any age.

Special Service Pensions

Will continue to “move up the chart” to reflect additional years of age and pension credit, as long as covered employment continues.

Plan ModificationsPlan Modifications

1. Participants who qualify for any Special Service Pension on 7/31/2005

30

Can still retire at any age under the Plan C schedule.

Special Service Pensions

Will move to the Plan D schedule upon attaining 30 years of pension credit, but no earlier than age 57, as long as covered employment continues.

Plan ModificationsPlan Modifications

2. Participants working under a Plan D contract, but who have earned 25 years but less than 30 years of pension credit on 7/31/2005

31

May not retire under a Special Service Pension earlier than age 57.

Special Service Pensions

Future eligibility for a Special Service Pension will be based on contribution rates and years of pension credit.

Plan ModificationsPlan Modifications

3. Participants who do not qualify for any Special Service Pension on 7/31/2005

Good chance that Regular Accrual Pension will exceed Special Service Pension

32

Yearly accruals under the Fund are the highest in the industryRegular Accrual Pensions may provide a bigger pension than Special ServiceComparison charts on the following pages use the UPS contract with a future accrual of $248/month for each future year.

Regular Accrual Pensions

Plan ModificationsPlan Modifications

33

Growth in Pension Value

$0

$2,000

$4,000

$6,000

$8,000

$10,000

55 /24

56 /25

57 /26

58 /27

59 /28

60 /29

61 /30

62 /31

63 /32

64 /33

Age and Credit at Retirement

Mon

thly

Pen

sion

Regular Accrual Pension Plan D Plan C

Current Age = 44 / Current Credit = 13

Age

Credit

34

Growth in Pension Value

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000

55 /28

56 /29

57 /30

58 /31

59 /32

60 /33

61 /34

62 /35

63 /36

64 /37

Age and Credit at Retirement

Mon

thly

Pen

sion

Regular Accrual Pension Plan D Plan C

Current Age = 50 / Current Credit = 23

Age

Credit

35

Growth in Pension Value

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000

55 /30

56 /31

57 /32

58 /33

59 /34

60 /35

61 /36

62 /37

63 /38

64 /39

Age and Credit at Retirement

Mon

thly

Pen

sion

Regular Accrual Pension Plan D Plan C

Current Age = 50 / Current Credit = 25

Age

Credit

36

Growth in Pension Value

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000

55 /30

56 /31

57 /32

58 /33

59 /34

60 /35

61 /36

62 /37

63 /38

64 /39

Age and Credit at Retirement

Mon

thly

Pen

sion

Regular Accrual Pension Plan D Plan C

Current Age = 52 / Current Credit = 27

Age

Credit

37

Growth in Pension Value

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000

55 /24

56 /25

57 /26

58 /27

59 /28

60 /29

61 /30

62 /31

63 /32

64 /33

Age and Credit at Retirement

Mon

thly

Pen

sion

Regular Accrual Pension Plan D Plan C

Current Age = 54 / Current Credit = 23

Age

Credit

38

Growth in Pension Value

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000

55 /25

56 /26

57 /27

58 /28

59 /29

60 /30

61 /31

62 /32

63 /33

64 /34

Age and Credit at Retirement

Mon

thly

Pen

sion

Regular Accrual Pension Plan D Plan C

Current Age = 55 / Current Credit = 25

Age

Credit

39

A participant who qualifies for a 30-Year Full Service Pension on 7/31/2005 can still retire at any age, based on pension accrual to retirement age.

30-Year Full Service Pensions

A participant who does not qualify for a 30-Year Full Service Pension on 7/31/2005 may not collect a 30-Year Full Service Pension before they reach the new minimum age of 57.

Plan ModificationsPlan Modifications

40

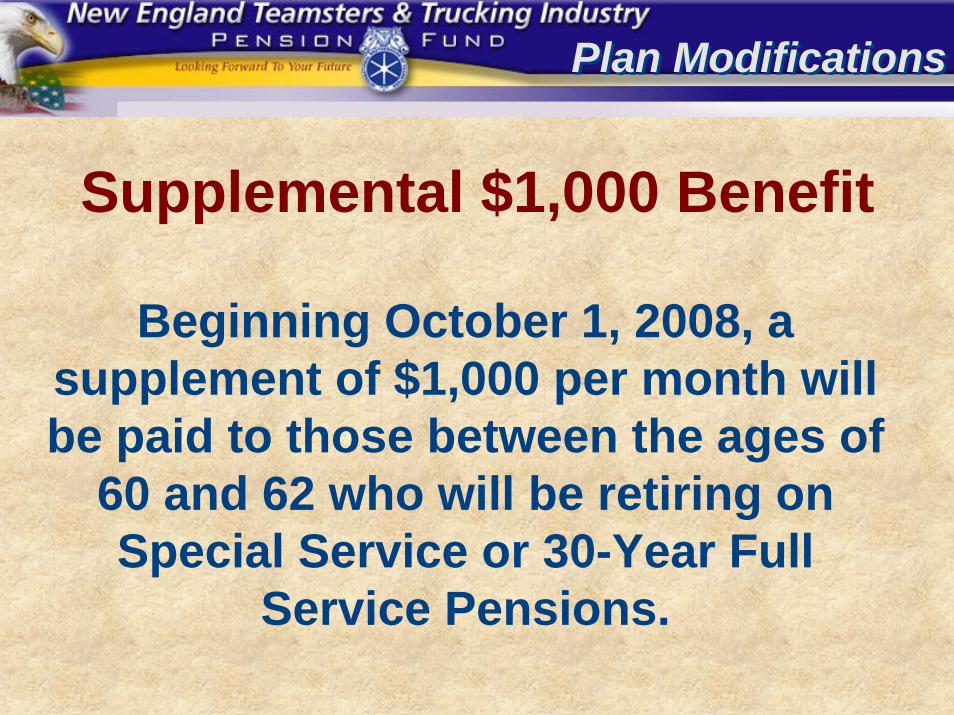

Supplemental $1,000 Benefit

Plan ModificationsPlan Modifications

Beginning October 1, 2008, a supplement of $1,000 per month will be paid to those between the ages of

60 and 62 who will be retiring on Special Service or 30-Year Full

Service Pensions.

41

Goal: Achieve 90% Funding by 2030

Modification GoalsModification Goals

5% annual increases in employer contributions for maintenance of benefits will increase the total dollar amount of employer contributions each year and help shrink the growing gap between contribution income and benefit expenses.

Getting there will require increasing the Fund’s Asset Base

42

Modification GoalsModification Goals

Through a combination of reducing future benefit accruals and implementing the 57-year minimum retirement age, we will slow the growth rate in the Fund’s liabilities and help ensure that there will be sufficient assets to cover expected benefit payouts.

Goal: Achieve 90% Funding by 2030

Getting there will require slowing the Fund’s liability growth

43

Goal: Achieve 90% Funding by 2030

Modification GoalsModification Goals

Getting there will require a change in participant behavior.

Minimum retirement age for full pension and supplemental incentive will, over time, encourage participants to retire later and lead to greater balance in Fund’s demographics.

44

Goal: Achieve 90% Funding by 2030

Modification GoalsModification Goals

Getting there will ensure the retirement security of today’sand tomorrow’s NETTIPF pensioners.