prufund structure, investment management and governance … · 2019-10-17 · independent review of...

TRANSCRIPT

INDEPENDENT AKG REVIEW

PRUFUND STRUCTURE,

INVESTMENT MANAGEMENT AND

GOVERNANCE PROCESSES

PREPARED FOR PRUDENTIAL ASSURANCE COMPANY LTD | 27 SEPT 2019

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

Contents 1. Introduction .............................................................................................................................................................................................................................. 1

1.1 Project Background .................................................................................................................................................................................................................1 1.2 AKG’s Assignment ...................................................................................................................................................................................................................1 1.3 AKG’s Review Process and the Scope of its Considerations ...........................................................................................................................1 1.4 Information Sources ................................................................................................................................................................................................................1 1.5 Reliances and Limitations .....................................................................................................................................................................................................2 1.6 Confidentiality ............................................................................................................................................................................................................................2 1.7 Abbreviations .............................................................................................................................................................................................................................3

2. AKG Observations ................................................................................................................................................................................................................. 4 3. Market Context ....................................................................................................................................................................................................................... 6

3.1 Introduction to Governance ..............................................................................................................................................................................................6 3.2 MiFID II Product Governance ............................................................................................................................................................................................6 3.3 Due Diligence Requirements .............................................................................................................................................................................................7 3.4 Considering Outsourced Investment Solutions .......................................................................................................................................................7 3.5 Outcome Oriented Focus ...................................................................................................................................................................................................8 3.6 Transparency of Charges/Terms and Customer Outcomes ............................................................................................................................8 3.7 ‘Smoothed’ Investment Solutions ....................................................................................................................................................................................8

4. PruFund Key Facts .................................................................................................................................................................................................................. 9

4.1 Availability .....................................................................................................................................................................................................................................9 4.2 Types and Series .......................................................................................................................................................................................................................9 4.3 Size ..................................................................................................................................................................................................................................................9 4.4 Charging Structures .............................................................................................................................................................................................................. 10

5. Prudential UK With-Profits Fund Structure .............................................................................................................................................................. 11

5.1 Introduction .............................................................................................................................................................................................................................. 11 5.2 AKG With Profits Fund Assessment........................................................................................................................................................................... 11 5.3 With-Profits Fund (Sterling Ordinary Branch Business) Objective ............................................................................................................. 11 5.4 Principles and Practices of Financial Management (PPFM) ............................................................................................................................. 11 5.5 Prudential With-Profits Committee ............................................................................................................................................................................ 12 5.6 Prudential’s Inherited Estate ............................................................................................................................................................................................ 12

6. Introducing T&IO ................................................................................................................................................................................................................. 14

6.1 Key Facts and Structure ..................................................................................................................................................................................................... 14 6.2 Regions Covered ................................................................................................................................................................................................................... 14 6.3 Key teams and Their Responsibilities ......................................................................................................................................................................... 15 6.4 Regular Communications .................................................................................................................................................................................................. 15

7. T&IO Investment Philosophy and Fund Management Objectives .................................................................................................................. 16

7.1 Introduction .............................................................................................................................................................................................................................. 16 7.2 Asset Allocation Models – PruFund Growth and Cautious Funds ............................................................................................................ 17 7.3 Strategic Asset Allocation review ................................................................................................................................................................................. 18 7.4 Changes Made as a Result of SAA Review ............................................................................................................................................................. 18 7.5 Fund Objectives - PruFund Growth and PruFund Cautious Funds ........................................................................................................... 18 7.6 Fund Objectives – Risk Managed PruFunds ............................................................................................................................................................ 19

8. PruFund Controls and Systems ..................................................................................................................................................................................... 20

8.1 Governance Structure ........................................................................................................................................................................................................ 20 8.2 Controls ..................................................................................................................................................................................................................................... 20 8.3 How Does T&IO Assess Performance? .................................................................................................................................................................... 20 8.4 How Does T&IO Ensure that Managers Possess the appropriate Structure to Achieve Explicit Performance Objectives? ............................................................................................................................................................................................................................................... 21 8.5 Who is responsible for the Performance Review of Funds?.......................................................................................................................... 21

9. Prudential’s Smoothing Mechanics ............................................................................................................................................................................... 22

9.1 Introduction .............................................................................................................................................................................................................................. 22

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

9.2 Some Important Differences in Approach for Series D and Series E Investments ........................................................................... 22 9.3 Smoothing in Action - PruFund ..................................................................................................................................................................................... 22 9.4 What is the EGR? .................................................................................................................................................................................................................. 23 9.5 How Does the EGR Affect the Investment? .......................................................................................................................................................... 23 9.6 How can Unit Price Adjustments Affect the Value of the Investment? .................................................................................................. 23 9.7 PruFund Review Work – Q4 2018 ............................................................................................................................................................................. 24

10. Appraising PruFund Performance and Governance in Action .......................................................................................................................... 26

10.1 Historic PruFund (Life) Unit Price Adjustments ................................................................................................................................................... 26 10.2 Historic PruFund (Pension) Unit Price Adjustments .......................................................................................................................................... 27 10.3 PruFund Cautious Pension Fund Performance ..................................................................................................................................................... 29 10.4 PruFund Growth Pension Fund Performance ....................................................................................................................................................... 30 10.5 PruFund Cautious Life Fund Performance ............................................................................................................................................................... 31 10.6 PruFund Growth Life Fund Performance ................................................................................................................................................................. 32

11. Key Considerations for Advisers ................................................................................................................................................................................... 33 12. Adviser Checklist – PruFund & T&IO ......................................................................................................................................................................... 34 App. A Historic EGRs for PruFund (Pension) ............................................................................................................................................................. 36 App. B Historic EGRs for PruFund (Life) ...................................................................................................................................................................... 38 App. C PruFund Risk Managed Objectives .................................................................................................................................................................. 40 App. D About AKG ............................................................................................................................................................................................................... 41

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

1. Introduction 1.1 PROJECT BACKGROUND

The Prudential Assurance Company Ltd (PAC), the Client, has commissioned AKG Financial Analytics Ltd (AKG) to carry out an

independent review of the investment and risk management approaches, and the associated governance structures and processes,

which underpin the delivery of the PruFund range.

The link with Prudential With-Profits and the intrinsic role played by the M&GPrudential Treasury & Investment Office (T&IO) in

the management and oversight of the assets underlying the PruFund range is also recognised and assessed within this review.

1.2 AKG’S ASSIGNMENT

AKG’s assignment can be broadly summarised as carrying out an independent assessment of the proposition considering and

covering the following key themes and questions:

• Market context, including introduction to governance

• Prudential With-Profits Fund structure

• Introduction to T&IO, including size, resource, key teams and processes

• T&IO’s asset allocation philosophy and overarching fund management objectives

• PruFund controls and systems

• Prudential’s smoothing mechanics explained

• Appraising PruFund performance and governance in action.

We round up this AKG review with a summary of the merits and positioning of the PruFund proposition against some of the key

considerations included in our suggested checklist for advisers.

1.3 AKG’S REVIEW PROCESS AND THE SCOPE OF ITS CONSIDERATIONS

AKG has a key focus on the assessment of UK Life Companies from a financial strength perspective. In addition to studying the

core financials of life companies, a further element of AKG’s balanced scorecard approach to assessment is to appraise risk and

governance frameworks. AKG has therefore been able to use its knowledge of these frameworks, and its experience of governed

investment solution reviews, to inform this assessment and review.

AKG has been publishing a set of reports covering both open and closed UK Life Office With Profits Funds since 2006 and has

been analysing with profits funds for over 20 years. This experience has seen AKG’s UK Life Office With Profits Reports become

industry recognised as the key annual reference point for all matters related to with profits funds in the UK and the output

provides a valuable resource for financial advisers, product providers, research groups and other interested parties.

Prudential is covered within AKG’s With Profits output and AKG has therefore been able to use both this knowledge of the

market and the Prudential proposition to further inform this PruFund assessment and review.

Further information about AKG and its services can be found at the end of this report.

1.4 INFORMATION SOURCES

AKG has been supplied with and has utilised a wide range of material as a resource pool for this project, including the following:

• An introduction to The PruFund range of funds (PFBS10000 07/2019)

• PruFund Cautious Fund Factsheet (INVS11397_08_2019)

• PruFund Growth Fund Factsheet (INVS11256_08_2019)

• Risk Managed PruFund Funds (INVS11663 01/2019)

• PruFund Fund Guide Prudential Retirement Account (INVB205504 04/2019)

• Prudential Multi-Asset Funds Governance Report (INVG332905 01/2019)

• Introduction to the M&GPrudential Treasury & Investment Office, 2018 (Presentation)

• Evolution of PruFund (Presentation)

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

Smoothing

• A step by step guide to the PruFund smoothing process (GENM92301 01/2019)

• A step by step guide to the PruFund smoothing process (PRUF624304 02/2019)

With Profits

• Prudential With-Profits Fund Factsheet (BTBQ00068 05/2019)

• Your With-Profits Plan – a guide to how we manage the Fund; PruFund (Pricing Series D) range of funds

(WPG235102 01/2019)

• Your With-Profits Plan – a guide to how we manage the Fund; PruFund (Pricing Series E) range of funds (WPG627603

12/2018)

Latest EGR announcement

The current rates are published at: https://www.pruadviser.co.uk/funds/prufund-egr/ (the rates effective from 27 August 2019

were shown at the time of publication of this report).

Access to key personnel

AKG has also had access to members of various Prudential and T&IO teams in order to provide further context and practical

examples of the investment approach, structure and processes.

Additional Prudential material

Additional material from Prudential has been considered in the compilation of this report and some of this material is referenced

directly within the body of this report.

1.5 RELIANCES AND LIMITATIONS

Much of the information upon which AKG’s report and comments are based has been supplied directly by The Client. AKG has

made every effort to ensure the accuracy of the content of this report and to ensure that the information contained is as current

as possible at the date of issue, but AKG (inclusive of its directors, officers, staff and shareholders and any affiliated third parties)

cannot accept any liability to any party in respect of, or resulting from, errors or omissions. AKG personnel are available to expand

upon the comments in this report, if required.

Whilst many aspects underlying AKG’s comments are likely to change only slowly, the financial services industry is a competit ive

and dynamic marketplace, with new products/funds and developments being announced regularly. As a result, AKG cannot

guarantee that any particular comment will remain appropriate at any future date. Future developments in the market could have

significant impact upon the comments.

AKG information, comments and opinion, as expressed in the form of its analysis and ratings, do not establish or seek to establish

suitability in any individual regard and AKG does not provide, explicitly or implicitly, through this report and its content, or any

other assessment, rating or commentary, any form of investment advice or fiduciary service.

Actuaries must comply with standards produced by The Institute and Faculty of Actuaries (IFoA) and the Financial Reporting

Council (FRC). The FRC is responsible for setting Technical Actuarial Standards (TASs) and the IFoA is responsible for setting

and maintaining ethical standards, or Actuarial Profession Standards (APSs).

In AKG’s opinion, the work involved in this review does not fall within the scope of any of the TASs set by the FRC.

1.6 CONFIDENTIALITY

This report has been produced for the Client’s consideration. AKG is happy for the Client to reproduce all or part of this report

in any internal or external published material, subject to prior written agreement of the content, context, duration and volume

of such reproduction and of any reference, explicit or implicit, to AKG’s involvement in producing this report.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

1.7 ABBREVIATIONS

ABI Association of British Insurers

AMC Annual Management Charge

CIP Centralised Investment Proposition

CIS Collective Investment Scheme

COBS Conduct of Business Sourcebook

DCPSF Defined Charge Participating Sub-Fund

EGR Expected Growth Rate

FCA Financial Conduct Authority

FCR Financial Condition Report

FTSE Financial Times Stock Exchange

IMA Investment Management Agreement

ISA Individual Savings Account

MiFID Markets in Financial Instruments Directive

M&GP M&GPrudential Limited

PAC The Prudential Assurance Company Ltd

PHKL Prudential Hong Kong Limited

PPFM Principles and Practices of Financial Management

PPMG Prudential Portfolio Management Group

PS Policy Statement

SAA Strategic Asset Allocation

SAIF Scottish Amicable Insurance Fund

TAA Tactical Asset Allocation

T&IO Treasury & Investment Office

TR Thematic Review

UPA Unit Price Adjustment

WPSF With-Profits Sub-Fund

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

2. AKG Observations Proposition

• Prudential is focusing on targeting new business opportunities for PruFund across a range of life, pension and investment

wrappers.

• The PruFund range is long-standing but continues to evolve. For example, it is important for advisers to keep abreast of the

relevant type or series of PruFund within which their clients hold investments, particularly when it comes to investment

performance review and announcements relating to EGRs and UPAs.

• In January 2019 the names and objectives of each Risk Managed PruFund were changed and a new Risk Managed PruFund,

5 was launched. This change has been communicated to advisers. Prudential states that the changes reflected regulatory and

client requirements to be more specific on the client’s investment journey, but Prudential confirms that the underlying

investment process and philosophy remains unchanged.

• The team from the Prudential Portfolio Management Group (PPMG) now form part of the newly created M&GPrudential

T&IO. It is important for advisers to recognise that this change has taken place and to keep abreast of T&IO’s activities and

developments.

• From an investment solution perspective, financial advisers are quickly able to see which parts of the investment process are

being outsourced to T&IO, through the use of PruFunds, and hence which responsibilities remain with them.

• Adviser responsibilities revolve around the suitability of the fund, tax wrapper and product features (such as smoothing), the

assessment of an investor’s risk appetite and then contextual financial planning issues; with T&IO picking up the core

investment tasks, including asset allocation.

• Given the nature and composition of the PruFund range, and its associated mechanisms, T&IO has a requirement for an

industrial strength, multi-faceted investment management, risk and governance framework.

• AKG can see, through T&IO’s structure, processes and the range of application of its teams, that this requirement is taken

seriously and that appropriate measures are put in place to continue this governance underpin.

• The Prudential With-Profits Fund and the PruFund range are subject to an additional layer of scrutiny, review and process

through the work of the independent With-Profits Committee and the required publication of a PPFM.

• AKG can see that interaction between the teams which form T&IO and the wider teams within Prudential does take place

and that they work together to achieve their collective goals. They also show an understanding of how investors will be

engaging with PruFund solutions in the market, including usage within pension, onshore/offshore bond and ISA wrappers.

• M&GPrudential is a business going through a period of change and transition, including corporate structure, business

integration and personnel. It is important that momentum is maintained in relation to the operation, management and delivery

of the PruFund proposition which remains central to the future success of the business.

• The core PruFund Growth and PruFund Cautious Funds have both been operating in the market for some time now and

have displayed strong track records in terms of performance against stated objectives and delivering EGRs.

• This performance presents a positive endorsement of the investment approach, risk management, product design and

governance structure.

• The shape of the performance charts also underlines how Prudential’s smoothing process has successfully taken some of the

investment bumps out of the equation for investors.

• It is important to reiterate to investors that their investment in PruFund can go down.

• Another key performance indicator is the historic requirement for the application of a UPA. UPAs reflect the actual

performance of the underlying assets and the smoothing process. Information tables contained in this report confirm UPA

activity for the PruFund Cautious and PruFund Growth Funds. These make positive viewing in terms of the limited number

of occasions where Prudential has had to employ UPAs, be they positive or negative adjustments.

• EGRs are published and displayed on Prudential’s websites for financial advisers and customers on a quarterly basis. This

provides another example of where Prudential’s approach to running PruFunds is open to public scrutiny.

• The direction of travel for Prudential’s EGRs has been downward for a period, underlining the challenging investment markets,

secular changes and economic backdrop of recent times.

• Prudential and T&IO continues to seek to address key investment issues, outlook and methodology with the adviser

community via a range of communication channels.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

• Prudential will need to keep product governance considerations in mind as it continues with the evolution of the PruFund

proposition, acting, where relevant, to establish commensurate processes and systems. This will include ongoing research to

monitor the types of customer engaging with PruFund and associated suitability testing.

Financial Strength of the Fund

• The company has the largest with profits portfolio in the UK, and it continues to write new with profits business in volumes

that dwarf all others in the market. The company has continued its focus on the with profits market and it remains committed

to with profits and the long term returns of a multi-asset strategy. The inherent strength of its With-Profits Fund remains

apparent.

Company Financial Strength

• As one of the UK's largest and strongest life companies, PAC continues to show significant resilience in the wake of very

challenging economic, legislative and regulatory conditions. It has retained focus and increased its market share, whilst

continuing to demonstrate its appetite for key segments of the UK market, specifically the Pre- and Post-Retirement space.

• As at 31 December 2018, PAC's estimated Solvency II own funds of the shareholder business and the With Profits Funds

were £12.0bn and £8.4bn respectively, against capital requirements of £7.4bn and £4.7bn, giving coverage ratios of 163%

and 179%.

• PAC is currently wholly owned by M&GPrudential Limited (M&GP) which is wholly owned by Prudential public limited

company. M&GP acquired the beneficial title to the entire issued share capital of PAC from Plc with effect from 23 November

2018.

• As publicly announced, it is the intention for the UK and Europe business of the Plc group of companies to demerge under

M&GP (as a legal entity) and for M&GP to subsequently list on the London Stock Exchange. M&GP is expected to list on

the London Stock Exchange as M&G plc on 21 October 2019.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

3. Market Context 3.1 INTRODUCTION TO GOVERNANCE

There is no ‘one-size-fits-all’ definition of what constitutes good governance. AKG has therefore prepared the following

overarching paragraph over time to set the scene, having reviewed various sources from a number of different spheres of business

and governmental activity.

In general terms, governance can be regarded as the combination of competent processes and structures within an organisation that ensures it meets its objectives in a legal, ethical and honest way. Most importantly, governance must be transparent. An organisation is accountable for its governance and must be able to demonstrate the same.

This overarching definition then needs to be interpreted further in the context of financial services in general, the specific role

that the governance function in question is seeking to play and the associated roles of key market participants, including advisers,

providers and asset managers.

In doing so, there are several key terms which then spring to mind when you consider what governance in financial services might

stand for, including:

Key Terms Relating to the Concept of Governance

Accountability Responsibility Duty of care

Inquisitive Challenging Assessment

Demonstrable Effective Adaptable

Structure Framework Process

Connectivity Communication Recordable

Responsive Participatory Effective

Transparent Auditable Independent

Requirement for customers to be treated fairly and for good customer outcomes to be targeted

When assessing governance functions and structures the reviewer should therefore have these key terms in mind, specifically the

end customer requirements, and seek to monitor and appraise financial services governance functions against these key

competencies and objectives.

AKG’s review of the governance approach and framework adopted within the PruFund proposition therefore seeks to assess

against some of these key competencies and objectives.

3.2 MIFID I I PRODUCT GOVERNANCE

Reason for better governance

MiFID II has introduced significant product governance requirements and hence, whether directly or indirectly affected, companies

across the UK financial services sector now have cause to consider their approach and processes when designing, distributing and

recommending products and funds in future.

Providers will need to demonstrate to distributors that they fully understand the products and its features, so that advisers can

explain these adequately to the end investor. The overarching aim for this work, as ever, should be to achieve best practice within

these companies and to target positive outcomes for consumers in a transparent manner.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

Range of considerations on governance

AKG has listed below various considerations for firms when it comes to MiFID II’s governance requirements:

• Better acquisition and demonstration of knowledge and intelligence relating to a company’s target customers and

their requirements.

• Carry out quantitative and qualitative market research on consumer objectives when designing and testing appetite

for new products and funds.

• Ensure solutions are going to the right customers through a detailed management information and reporting capability.

• Investigate and report instances where funds are not being used by the right customer.

• Enhance management information and reporting capability in relation to distributors. Improve the exchange and flow

of data between companies, intermediaries and third parties to help each party meet their respective requirements.

• Realise there will be a greater requirement for governance and associated reporting to follow the product cycle. Be

prepared to continue to test the rationale relating to product/fund fit for consumers.

• Senior management teams must ensure governance is embedded in internal processes, with relevant and appropriate

levels of resource and expertise.

PROD rules

FCA PROD rules are outlined at https://www.handbook.fca.org.uk/handbook/PROD/3/?view=chapter. Distributors and

manufactures need to pay close heed to these. If advisers haven’t digested and acknowledged these PROD rules they should do

so.

Prudential will also need to keep many of these product governance considerations in mind as it continues with the evolution of

the PruFund proposition, acting, where relevant, to establish commensurate processes and systems. This will include ongoing

research to monitor the types of customer engaging with PruFund and associated suitability testing.

3.3 DUE DILIGENCE REQUIREMENTS

In February 2016, the FCA published TR16/1: Assessing suitability: Research and due diligence of products and services, a report

which set out the high-level findings of the FCA’s thematic review of the research and due diligence processes carried out by

advisory firms on the products and services recommended by them to retail customers.

The review included, for example, exploring how:

• firms selected products, funds, platforms and discretionary investment management services

• created panels and CIPs

• considered options for individual clients.

The general sentiment from the FCA in the paper is that due diligence processes need to be robust, repeatable and recordable.

And crucially that the suitability of solutions should be gauged at both a customer level and at an adviser business level.

This certainly still carries relevance for advisers now.

3.4 CONSIDERING OUTSOURCED INVESTMENT SOLUTIONS

With a proliferation of outsourced investment solutions for advisers to select from there has been an increasing focus on how

these solutions are operated.

What is the management style? How do they select managers/stocks? What is their structure? What size are their teams? Who

is responsible for what? What processes do they have in place to underpin the delivery of the multi-asset fund or portfolio?

Performance and cost will continue to present themselves as differentiators for outsourced investment solutions, although AKG

believes that over time the ability of a fund or portfolio to meet its core, stated objectives and to operate within its stated

parameters will be of ultimate importance to advisers and investors.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

The quality of the underpinning governance structure and the risk management processes employed has also become a key

differentiator.

3.5 OUTCOME ORIENTED FOCUS

Two of the most obvious and enduring investment requirements for many customers when considering their retirement strategies

remain:

• The delivery of a sustainable income for life in retirement, and/or

• The preservation of capital sums accumulated.

There appears to be a greater, and welcome, focus on targeting goals and outcomes for the end investor when considering these

retirement income planning needs. Putting a target percentage on the amount of income required and/or the growth required

on a capital sum are logical steps for the adviser and the customer.

Advisers might wish to align with Prudential’s EGR structure when setting outcome-oriented planning strategies for customers.

3.6 TRANSPARENCY OF CHARGES/TERMS AND CUSTOMER OUTCOMES

There is a concerted focus within the industry on ensuring that customers receive suitable recommendations and achieve good

outcomes. Within this, the clarity and transparency of terms and conditions for investment and pension propositions will be key

watchwords moving forward.

Items including the following will come under the microscope:

• Are the fund/portfolio objectives and parameters clearly explained for the investor?

• Is the company marketing the product, fund or portfolio solution doing enough to make the investment charges,

methodology, terms and conditions clear and transparent?

• For example, is the total cost of investment made clear rather than just headline charges being displayed?

• What asset/fund types are being utilised within portfolios?

Asset managers will continue to come under pressure in terms of making their objectives, terms, conditions and performance

clearer to customers.

3.7 ‘SMOOTHED’ INVESTMENT SOLUTIONS

Given some of the concerns flagged by advisers about investment market volatility, AKG’s 2018 Pension Freedoms paper also

sought to gauge adviser appetite for smoothed product/fund solutions.

The research showed that 17% of advisers surveyed were already utilising these solutions for clients while 32% were sometimes

advising on these solutions.

A further 35% say that they would potentially use smoothed product/fund solutions with the caveat that such solutions need to

improve/simplify further beforehand.

Providers of ‘smoothed’ product/fund solutions in the retail wealth management market are acknowledged as being Prudential,

LV= and Aviva.

These providers need to continue to evolve their propositions and ensure that they are marketed appropriately. Unless some

form of guarantee is specifically in play providers of ‘smoothed’ product/fund solutions need to ensure that customers understand

that the value of their units in the fund may go up as well as down. Customers must not have the perception that smoothing

provides some form of implicit guarantee.

Continued improvements in the way in which smoothing techniques and functionality is described, to both advisers and customers,

should also be targeted.

Providers and advisers both have responsibility in terms of best ensuring that customers understand the risk/reward profile of the

funds and the likely investment performance characteristics.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

4. PruFund Key Facts 4.1 AVAILABILITY

The following table illustrates PruFund range availability for Prudential’s key products. It underlines Prudential’s focus on targeting

business opportunities across a range of pension and investment wrappers:

Prudential PruFund Growth Fund

Prudential PruFund Cautious Fund

Prudential Risk Managed PruFund Funds

Prudential Retirement Account

Flexible Retirement Plan #

Prudential ISA

Prudential Investment Plan

Prudential International Investment Bond *

Trustee Investment Plan

*Available with currency options for PruFund Growth Fund and PruFund Cautious Fund (Sterling, Euro, US Dollar).

# The Flexible Retirement Plan (FRP) closed to new business on 17 September 2018. Existing FRP customers can still make changes to their plan.

4.2 TYPES AND SERIES

The PruFund range is long-standing but continues to evolve. It is important for advisers to keep abreast of the relevant type or

series of PruFund within which their clients hold investments, particularly when it comes to investment performance review and

announcements relating to EGRs and UPAs.

For example, there are now two series of PruFund within Prudential’s Retirement Account, which have different investment date

cycles. Customers are invested in either series as follows:

• All investments made on or before 25 August 2017.

• All investments made after 25 August 2017 (including fund switches and regular premium contributions).

4.3 SIZE

Sector PruFund £bn

Life funds Growth 9.1

Growth & Income 0.1

Cautious 5.7

Risk Managed 1.1

Pension funds Growth 13.4

Cautious 5.5

Risk Managed 4.8

Sub-total 39.6

Offshore 4.2

Total 43.8

Source: M&GPrudential (as at 31 December 2018)

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

4.4 CHARGING STRUCTURES

Using Prudential Retirement Account by way of example, charges are outlined within the Key Features Document.

• Product charge - This is an annual charge calculated as a percentage of the customer’s total Retirement Account value

and Prudential deducts 1/12th of the yearly charge each month on the charge date. Prudential applies a discount to

the customer’s product charge which varies according to the value of their Retirement Account. The yearly Product

Charge before any discounts is 0.45%.

• Investment charge - This is a daily charge by the fund manager for the management and administration of funds. For

PruFunds, it is described as an Annual Management Charge (AMC) in the PruFund Fund Guide. In addition to this

charge, there may be further costs incurred, which can vary over time, and are detailed in the customer’s personal

illustration as Further Costs.

Investment charges are covered in greater detail within the PruFund Fund Guide. Prudential takes an AMC for looking after the

customer’s investment, from each of the funds they invest in. The charge is taken by the deduction of 1/365th of the applicable

AMC from the fund each day. Any further costs shown are expenses which are borne by the fund.

The basic AMC for PruFund Cautious and PruFund Growth is 0.65%. These Fund charges and Further Costs are confirmed on

page 9 of the PruFund Fund Guide. Further information about Further Costs is also provided on page 6. Given the focus on costs

and transparency it is important for Prudential to make this information available to advisers and customers.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

5. Prudential UK With-Profits Fund

Structure 5.1 INTRODUCTION

Both the PruFund proposition and the work of T&IO are intrinsically linked with the running of the main Prudential With-Profits

Fund (£82.4 billion as at 31 March 2019) - https://www.pru.co.uk/pdf/BTBQ00068.pdf.

It is therefore useful and important for financial advisers to understand how the Fund’s risk and governance structure and

investment process works.

5.2 AKG WITH PROFITS FUND ASSESSMENT

AKG's comprehensive 2018 UK Life Office With Profits Reports, contained analysis and assessment of with profits funds that

were active in the UK market at the end of December 2018, including Prudential.

Prudential has licensed the distribution of an excerpt derived from AKG’s 2018 With Profits Reports. A link to this document is

provided here: https://www.pruadviser.co.uk/pdf/GENM11347.pdf.

The excerpt covers the full set of assessment pages for Prudential with a brief contextual introduction and AKG’s comment on

PAC.

5.3 WITH-PROFITS FUND (STERLING ORDINARY BRANCH BUSINESS) OBJECTIVE

Prudential states that the aim is to seek to secure the highest total return (allowing for the effect of taxation and investment

expenses) whilst maintaining an acceptable overall risk level for the Fund and protecting the relative interests of all groups of

policyholders.

The policy for with-profits business is to invest in a highly diversified portfolio of UK and overseas assets. All investment

management approaches, governance structures and risk management processes stem from this overarching objective for the

main Fund.

5.4 PRINCIPLES AND PRACTICES OF FINANCIAL MANAGEMENT (PPFM)

All firms that carry out with profits business are required to publish a PPFM that applies to the management of with profits funds.

The Prudential PPFM aims to help a knowledgeable observer (e.g. a financial adviser) to understand how it manages its With-

Profits business, including:

• how Prudential determines pay-out values,

• Prudential’s investment strategy, and

• how Prudential manages business risks.

The PPFM covers all With-Profits policies issued in the UK by companies in or acquired by the Prudential Group i.e. PAC, Scottish

Amicable Life plc, Scottish Amicable Life Assurance Society, Prudential (Abbey National) Limited and Prudential International

Assurance plc. It also covers the With-Profits annuity policies transferred from the Equitable Life Assurance Society to PAC.

The Principles define the overarching standards adopted in managing PAC's With-Profits business and describe the approach

used in responding to longer-term changes in the business and economic environment. The Practices describe the approach used

in responding to changes in the business and economic environment in the shorter-term, hence they will change more frequently

than Principles.

The latest version of the PPFM was published in August 2019. Financial advisers can find the document online at:

https://www.pru.co.uk/pdf/WPGB0014.pdf.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

The requirement to produce and publish a PPFM brings with it an additional layer of public scrutiny and imposed transparency

to the Prudential With-Profits Fund, and the PruFund range.

5.5 PRUDENTIAL WITH-PROFITS COMMITTEE

In addition to internal committees, the With-Profits Committee provides an independent assessment of the way in which

Prudential manages its With-Profits business, how it balances the rights and interests of policyholders and shareholders, and

whether Prudential complies with the PPFM.

Advisers can access the Terms of Reference for the Prudential With-Profits Committee online via this link:

http://www.pru.co.uk/pdf/PRUAG01216.pdf.

The Committee comprises at least three members, all of whom are independent of Prudential. The current Prudential With-

Profits Actuary is Peter Needleman (Willis Towers Watson plc).

Name Background

Ronnie Bowie (Chair) Senior Partner, Hymans Robertson; Past President, Institute and Faculty of Actuaries

Chris Daykin Former Government Actuary; Past President, Institute of Actuaries

Bruno Geiringer Former Partner, Pinsent Masons LLP

David Keeler Former Consulting Actuary, Towers Watson

Julius Pursaill Governor of the Pensions Policy Institute

5.6 PRUDENTIAL’S INHERITED ESTATE

The Inherited Estate is the surplus money that has built up within the With-Profits Fund over time and essentially provides the

‘buffer’ to support the with profits smoothing component. Here are some key pieces of information:

The company has two inherited estates, one in the WPSF and one in SAIF. The inherited estate in the WPSF is effectively the

working capital for PAC. It has built up over many years and neither policyholders nor shareholders can have any expectation

that they will receive any distribution of it.

In March 2007 the company announced that it was considering a possible reattribution of the WPSF inherited estate. However,

after extensive assessment, the company decided in June 2008 that it would not proceed with a reattribution as it believed that

the current operating model was in the best long-term interests of both policyholders and shareholders.

There is no specific target for the size of the WPSF inherited estate. It currently supports the WPSF with profits business by

providing benefits associated with smoothing and guarantees, permitting investment flexibility and meeting regulatory

requirements. It also supports business in SAIF and the DCPSF (including the ex-Equitable Life with profits annuity portfolio), for

which it receives a charge.

The inherited estate may also be used for other purposes as determined by the Directors. Currently, this includes the additional

tax payable by the long term fund as a result of shareholders' distribution from the WPSF (and this use is expected to continue),

expenses written off between 1997 and the end of 2011 and any cost of shareholder transfers in respect of business issued by

Scottish Amicable Life plc in excess of the difference between charges deducted and expenses incurred.

However, since 2012, new business in the WPSF has been priced such that it is expected to be financially self-supporting over

the lifetime of the business at the point the pricing assumptions are set. Where the business is not expected to be financially self-

supporting at the point the pricing assumptions are set, shareholders will make an appropriate contribution to the WPSF, as

happened for 2014.

The inherited estate also met the cost of the pensions mis-selling review. In 1998, the company gave WPSF policyholders an

assurance that this would not impact bonus or investment policy and if it did, appropriate shareholder resources would be made

available. Following completion of the review, the assurance does not apply to post-2003 new business. Since the investment

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

policy for WPSF policies is the same whether or not the assurance applies, its withdrawal has had no effect on policyholder

returns.

The WPSF inherited estate now has a different investment strategy to the remainder of the WPSF. Early in 2008, the company

tactically de-risked part of the inherited estate, by selling a portion of the equity investments into high grade bonds and cash. As

a result, the inherited estate was mainly invested in fixed interest securities and cash at the end of 2010 and this continued to be

the case at the end of each of the years 2011 to 2017.

In 2012, the FSA provided guidance to the company to clarify two questions raised by Prudential in relation to FSA policy

statement PS12/4. The guidance clarifies that Prudential is not generally required, when writing new business and managing its

with profits fund, to take account of any current policyholders’ interest in the prospect of a distribution (or greater distribution)

from Prudential’s inherited estate.

Also, while Prudential’s with profits fund remains open and the inherited estate remains fully utilised in supporting current and

expected future new business, policyholders do not have any expectation of a distribution of the inherited estate, other than

through the normal process of the smoothing of their returns and in Prudential meeting guarantees in adverse investment

conditions. Prudential believes that no group of in-force policyholders has made any contribution to the inherited estate.

With the transfer of in-force Hong Kong branch business and future such business to Prudential Hong Kong Ltd (PHKL) it was

also considered appropriate to transfer a portion of the WPSF inherited estate to PHKL and this took place as part of the transfer

effective from 1 January 2014. The share of the WPSF inherited estate transferred to the PHKL with profits fund took into account

PHKL's anticipated requirement for capital to fund the writing of new business in that fund after the transfer.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

6. Introducing T&IO 6.1 KEY FACTS AND STRUCTURE

The Prudential Portfolio Management Group (PPMG) now forms part of the newly created M&GPrudential T&IO -

https://www.pruadviser.co.uk/funds/tio/.

T&IO remains one of the largest and most well-resourced multi-asset teams in the UK, managing approximately £175 billion (as

at 30 June 2019) across a growing range of highly competitive multi-asset investment solutions and annuities, on behalf of

Prudential UK & Europe.

T&IO’s role is to function as the in-house investment strategist and ‘manager of managers’, responsible for monitoring and

reviewing performance and for day-to-day allocation of monies to the group’s various fund management specialists: including

M&G Investment Managers, M&G Real Estate, Prudential Portfolio Managers America, Eastspring Asset Management and

Infracapital; as well as external specialists in private equity, hedge funds and infrastructure.

T&IO has a team of over 60, including experienced investment professionals with specialist expertise in capital market research,

investment strategy design, liability management, alternative investments and portfolio management.

The structure chart for T&IO is illustrated below:

Source: M&GPrudential

6.2 REGIONS COVERED

To help inform investment decisions, T&IO, has access to the skills of a large number of investment professionals both in the UK

and around the world. The Prudential Group has over 800 investment professionals worldwide, investing £657bn as at December

2018.

T&IO works with other Prudential Group fund managers to achieve its regional and asset type diversification.

• M&G Investments – UK and Europe (Equities and corporate bonds)

• Eastspring Investments – Far East, Emerging Markets and Japan (Equities, emerging markets and corporate bonds)

• PPM America – US (Equities and corporate bonds)

• M&G Real Estate (Property)

• Infracapital (Infrastructure)

• Various third-party specialists for alternatives (for example, the Q1 T&IO Update references investment in a fund

through Primary Wave, one of the largest independent music publishing, marketing and talent management firms in

the US).

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

6.3 KEY TEAMS AND THEIR RESPONSIBILITIES

There are four core teams in T&IO involved in managing the money and supporting PAC in the delivery of the PruFund

proposition to the market.

It is important for financial advisers to get a feel for the roles and duties of the teams involved in running a managed fund solution.

The table below looks at the composition of and the key activities carried out by core T&IO teams:

Source: M&GPrudential

These teams work together to enable the day-to-day running of the multi-asset portfolios underlying the PruFund proposition

and delivering client support to PAC.

The teams also need to interact with other key stakeholders in the wider Prudential business, including the PAC Board, the With-

Profits Committee and the product development and distribution teams. It is vital for the ongoing delivery of the PruFund

proposition that this collaboration between business units continues effectively.

6.4 REGULAR COMMUNICATIONS

PAC and T&IO publish regular investment updates for the adviser community to provide a sense of its views on the economy

and key investment markets – UK and worldwide.

Key investment activity and asset allocation positioning is also covered in these updates for advisers. These are typically published

on a quarterly basis. A link to the Q1 2019 update from T&IO is provided below.

Q1 2019 T&IO Update

https://www.pruadviser.co.uk/knowledge-literature/knowledge-library/treasury-investment-office-q1-2019/

PAC and T&IO also run a series of webinars and seminars for advisers to further enhance understanding of its investment beliefs

and processes. Links to the April and June 2019 Market Insights videos are provided below for reference.

https://www.pruadviser.co.uk/knowledge-literature/knowledge-library/prudential-market-insights-april-2019/?icid=banner_articles

https://www.pruadviser.co.uk/knowledge-literature/knowledge-library/prudential-market-insights-june-2019/#investments

Prudential Multi-Asset Investment Update – August 2019

https://www.pruadviser.co.uk/content/pruadviser/homepage/knowledge-literature/knowledge-library/prudential-multi-asset-

investment-august-2019.html

Investment Week - Industry Voice: The anatomy of long-term asset allocation

In this feature Parit Jakhria, Head of Long- Term Investment Strategy, explains how his team operates to determine its long-term

investment strategy.

https://www.investmentweek.co.uk/investment-week/sponsored/3019615/the-anatomy-of-long-term-asset-allocation

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

7. T&IO Investment Philosophy and

Fund Management Objectives 7.1 INTRODUCTION

Source: M&GPrudential

T&IO states that it believes in the following key investment approaches:

• A long-term approach to investing

• Diversification, by both asset category and geography

• Active management

• The importance of valuation

• Illiquidity and credit premiums.

The T&IO team states that it seeks to add value through:

• Strategic asset allocation

• Mandate design

• Tactical asset allocation (working closely with the macro team in M&G Investments)

• Underlying manager alpha

• Efficient implementation.

As a result of these beliefs and approaches, PruFund portfolios will therefore have some common characteristics:

• Active equity portfolios generally have a slight value bias

• Fixed income portfolios have a credit bias

• Property portfolios have a bias towards high quality assets in core locations

• Private assets represent a sizeable proportion of portfolios

• Portfolios will evolve as new asset classes and opportunities are embraced.

Advisers should understand and be comfortable with the asset allocation approach followed by their outsourced investment

partners and the associated fund management objectives.

T&IO invests globally in a range of assets including equities, property, fixed interest and where applicable alternative assets. By

pooling together a large number of investors they put themselves in a strong position to be able to achieve this diversification.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

The PruFunds each have different asset allocations and fund aims. Within each high-level asset type (for example international

equities or fixed interest) the amount held in different types of that asset is driven by the proportion held in the main Prudential

With-Profits Fund, which could change on a daily basis. The PAC Board sets the long-term asset allocation positions of each

PruFund, based on recommendations from T&IO. However, the way in which asset allocation positions are applied for each of

the funds can be different.

7.2 ASSET ALLOCATION MODELS – PRUFUND GROWTH AND CAUTIOUS FUNDS

Strategic asset allocation breakdown as at 30 June 2019:

PruFund Growth Fund

Source: PruFund Growth Fund Factsheet

PruFund Cautious Fund

Source: PruFund Cautious Fund Factsheet

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

7.3 STRATEGIC ASSET ALLOCATION REVIEW

Advisers should also seek to understand the asset allocation review processes undertaken by their outsourced investment partners

and how any associated changes are made.

An annual review of the SAA within multi-asset portfolios is carried out formally by the T&IO’s Long Term Investment Strategy

(LTIS) team and approved by the PAC Board. The analysis and modelling required is complex. The LTIS team must factor in

capital constraints and hedging requirements as well as metrics like volatility, economic growth and asset class correlation, whilst

also estimating the long-term equilibrium returns and risks that are the foundation of portfolio construction.

The diagram below provides a high-level overview of the SAA process.

Source: M&GPrudential T&IO

The medium and long-term capital market assumptions are based on structural factors like demographics, economic growth,

monetary and fiscal policy, debt levels and political risks. These are then combined with the short-term outlook based on valuations

to give the full picture of asset class returns. These returns and risk assumptions are input into a proprietary economic scenario

generator, GeneSiS, to give the full range of possible outcomes for individual asset classes as well as overall portfolios. This

complete range of assumptions and possible outcomes are tested for thousands of portfolios to give an optimal portfolio in terms

of risk and return.

T&IO views evolve to reflect the changing economic landscape, so for instance a proprietary Demographics and Economic

Growth model has been built to help inform views on long-term risk and return assumptions.

7.4 CHANGES MADE AS A RESULT OF SAA REVIEW

Despite their long-term outlook, the regular review of PruFund SAA breakdown and positioning forms a key part of ongoing

process and governance at T&IO.

A link to the Q1 2019 update from T&IO is provided below.

Q1 2019 T&IO Update

https://www.pruadviser.co.uk/knowledge-literature/knowledge-library/treasury-investment-office-q1-2019/

7.5 FUND OBJECTIVES - PRUFUND GROWTH AND PRUFUND CAUTIOUS FUNDS

In November 2004 Prudential introduced the PruFund Growth Life Fund, a ‘new-style’ with profits fund offering smoothed

investment returns and an increased level of transparency. The investment mix of the PruFund Growth Fund is the same as the

main part of the WPSF.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

In November 2009, the PruFund Cautious Life Fund was launched. The PruFund Growth Pension Fund and the PruFund Cautious

Pension Fund were launched in November 2008 and November 2009 respectively.

Each of the funds aims to protect the investor against some of the ups and downs of the investment markets by using a smoothing

process. This is designed to provide less volatile and more stable returns over the medium to long term in line with each fund’s

objective and allowable equity parameters. The funds in the PruFund range offer different levels of risk and potential return for

the investor.

The following overarching objective for the PruFund Growth Fund is taken directly from the fund factsheet.

PruFund Growth Fund – The Fund aims to maximise growth over the medium to long term by investing in shares, property, fixed interest and other investments. The fund currently invests in UK and international equities, property, fixed interest securities, index-linked securities and other specialist investments.

Prudential recently announced to advisers and customers that the investment aim for the PruFund Cautious Fund was being

updated with effect from 29 July 2019. The table below confirms this change.

Investment Aim pre 29 July 2019 – PruFund Cautious Fund Investment Aim wef 29 July 2019 – PruFund Cautious Fund

The Fund aims for steady and consistent growth through a cautious approach to investing. The Fund currently invests around 70% in a well-diversified portfolio of fixed interest securities and holdings of cash and money market instruments. The balance is invested in UK and International shares, property and alternative assets.

The fund aims for steady and consistent growth over the medium to long term (5 to 10 years or more) through a cautious approach to investing. The fund invests in UK and international equities, property, fixed interest securities, index-linked securities, cash and other specialist investments. The fund will aim to invest 50-75% in fixed interest securities, index-linked securities and cash, although we may occasionally move outside this range to meet the fund objectives.

Prudential states that there will be no change to the fund’s risk rating, as provided by Prudential.

The rationale given for the change is that Prudential believes the current investment aim constrains the choice of investments

open to the fund, as it limits investments in shares, property and alternative assets to around 30%. However, Prudential may in

future wish to invest more in these assets and, without increasing the fund’s risk rating, try to achieve a better return for

policyholders.

Prudential states that there is no change to the way in which the fund is managed and that the investment aim update will not

impact on the fund’s EGR.

7.6 FUND OBJECTIVES – RISK MANAGED PRUFUNDS

In November 2011, four Risk Managed PruFunds (Life and Pension versions) were introduced (originally differentiated as 0-30%,

10-40%, 20-55%, and 40-80%, based on the equity proportion). In the first instance, they stated to the investor that there was a

minimum and maximum equity exposure framework for each Fund.

In January 2019 the names and objectives of each of the four existing funds were changed and a new fund was launched: PruFund

Risk Managed 5 Fund. Prudential states that the changes reflected regulatory and client requirements to be more specific on the

client’s investment journey, but Prudential confirms that the underlying investment process and philosophy remains unchanged.

An explanatory note was produced for intermediaries to provide additional details about the changes. This document briefly

outlines the rationale for the change from the previous equity exposure parameters to the volatility parameters and displays the

old and new investment objectives of each fund alongside each other for adviser reference. The new investment objectives are

also confirmed in Appendix C.

https://www.pru.co.uk/pdf/GENB955201.pdf

The Prudential potential risk and reward indicators are indicated for each of the funds and show that these have stayed the same

following the change from equity exposure parameters to volatility parameters.Prudential states that these risk ratings are based

on their expectation of future volatility (the chance of short-term fluctuations up and down in the value of a fund). The ratings

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

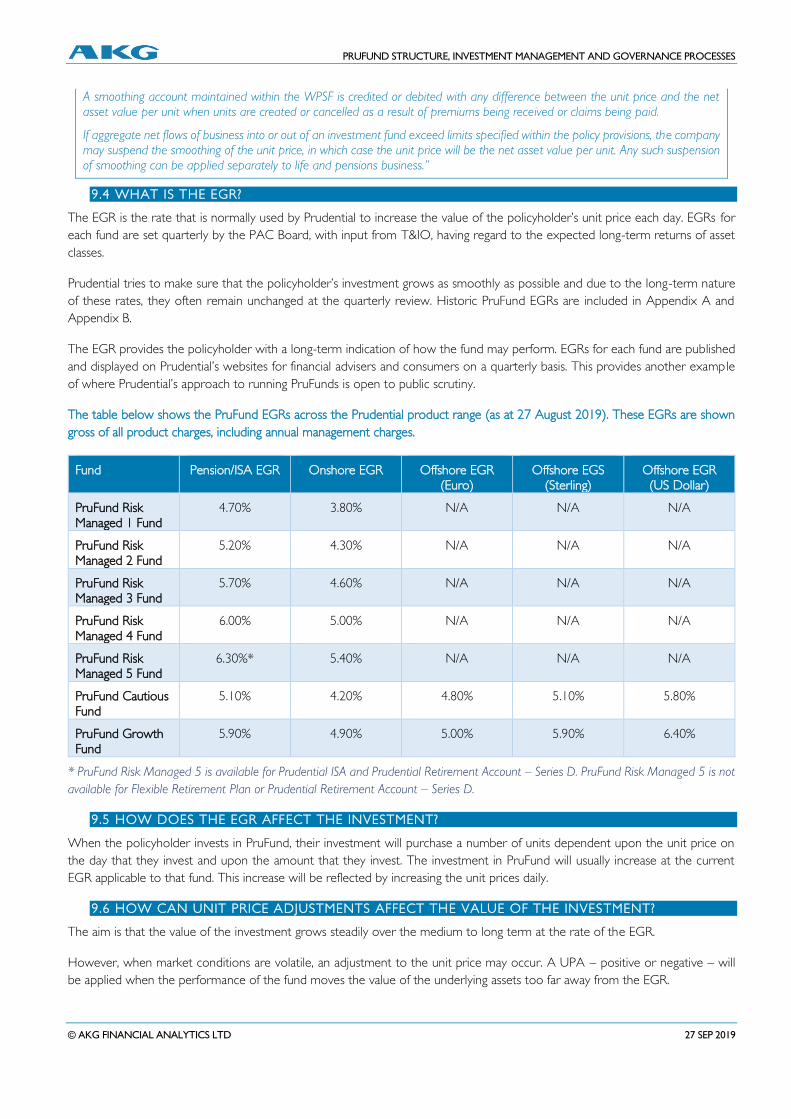

do not take into account other types of investment risks faced such as the effects of inflation. Funds are rated on a scale of 1-6

with 1 being the lowest risk rating and 6 being the highest. Risk ratings are regularly reviewed and may change in the future.

8. PruFund Controls and Systems 8.1 GOVERNANCE STRUCTURE

Given the nature and composition of the PruFund range, T&IO has a requirement for an industrial strength, multi-faceted

investment management, risk and governance framework.

Whilst they are able to make use of the global investment insight provided by asset management companies within the Group

to inform their investment views, they also have the role of monitoring and managing these experts.

In this respect T&IO undertakes the “manager of managers” role and has created a thorough governance framework to support

their work.

T&IO has governance responsibility for each of these Prudential Group fund management companies, and they in turn manage

the stock selection for underlying internal funds and mandates used.

8.2 CONTROLS

The Manager Oversight Team regularly monitors internal and external managers against their benchmarks and mandate and will

report any material issues. Investment Management Agreements (IMAs) govern how a strategy/mandate should be implemented

by each of the fund managers. Managers will be given different mandates across asset classes and the degree of flexibility permitted

may vary.

The Manager Oversight Team is responsible for the investment due diligence and ongoing monitoring of internal and external

managers. This entails very close interaction through:

1. Best practice monitoring (monthly) – In addition to monitoring whether daily limits are being breached or not, the team

looks at key exposures in funds on a monthly basis to see if anything untoward is taking place.

2. Strategy and performance review (quarterly) – T&IO holds quarterly meetings with the managers, either in person for

those based in London and by video conference for the managers located overseas. Each manager submits a Data

Request Book prior to the quarterly meeting, which provides performance data, risk metrics and attribution for the

quarter. The Data Request Book forms the basis of the meeting, enabling T&IO to pinpoint areas that require further

discussion.

3. Investment due diligence (annually) – Annual site visits are conducted to assess each fund manager on their suitability

and alignment with the strategy. Investment due diligence covers both quantitative and qualitative factors. Quantitative

factors include measures of performance and holdings analysis. Qualitative analysis incorporates People, Process,

Philosophy and Infrastructure.

4. IMA review (at least annually) – Manager IMAs are reviewed as part of the annual investment due diligence process to

ensure that the mandate and guidelines remain fit for purpose.

This T&IO manager oversight process is brought to life by head of this team, Ciaran Mulligan, in an interview aired in December

2018:

https://www.pruadviser.co.uk/knowledge-literature/knowledge-library/governance-of-multi-asset-portfolios-december-2018/

8.3 HOW DOES T&IO ASSESS PERFORMANCE?

T&IO states that its primary concern is that managers perform to mandate – which may from time to time lead to positive or

negative relative return at the fund total level when compared to either peer group or benchmarks

T&IO’s governance and control framework helps to support this monitoring and assessment. In addition, the standard measures

of fund/mandate versus benchmark and fund/mandate versus peer group are also monitored.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

8.4 HOW DOES T&IO ENSURE THAT MANAGERS POSSESS THE APPROPRIATE STRUCTURE TO ACHIEVE EXPLICIT PERFORMANCE OBJECTIVES?

By having in place a process of clearly articulating a mandate at outset and measuring the performance relative to that mandate

on an ongoing basis, T&IO states that it can work towards ensuring that the portfolios remain fit for purpose and possess the

appropriate structure to achieve the objectives.

Adherence to the mandate is therefore the key here, and these are formally reviewed and re-agreed with the Executive

Investment Committee (EIC) on an annual basis.

8.5 WHO IS RESPONSIBLE FOR THE PERFORMANCE REVIEW OF FUNDS?

Financial advisers should also find out more about an asset manager’s internal approach to performance controls.

The ultimate responsibility for the performance of the PruFund range rests with the PAC Board, which has created an investment

subcommittee to formally discharge this duty.

The EIC is supported in its duties by T&IO, who produce investment reporting for the funds, and will draw to the attention of

the board any matters of immediate concern. Performance of these funds relative to peer group is highly visible, and there is a

high degree of scrutiny applied to performance data in many areas of the business throughout the year.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019

9. Prudential’s Smoothing Mechanics 9.1 INTRODUCTION

Prudential states that PruFunds aim to provide more stable growth than might be expected from investing directly in the stock

market. Each PruFund fund has a different asset mix and fund objective. These funds are designed to deliver smoothed growth

by:

• Investing in many different investment areas, such as UK and International Equities, Property, Fixed Interest and Cash.

By spreading investments Prudential can help to reduce the risk of the investment experiencing the extreme ups and

downs associated with any single investment type.

• Applying a unique smoothing process. The process has two elements:

o Expected Growth Rates, which normally apply on a day-to-day basis; and

o Unit price adjustments, applied when the formula requires Prudential to do so.

Advisers should ensure they are comfortable with how smoothing works and be able to support customer understanding of the

concept, with assistance from Prudential material where required.

9.2 SOME IMPORTANT DIFFERENCES IN APPROACH FOR SERIES D AND SERIES E INVESTMENTS

Series E of PruFund was launched in August 2017 and is available to Prudential Retirement Account customers only. In Series E,

the period a customer’s investment will be in the holding account reduces from up to 3 months (standard practice for customers

in earlier versions of PruFund, including Series D) to up to 1 month.

Investments into Series E of PruFund take place on the PruFund Investment Date (25th of each month or the first working day

after the 25th) rather than quarterly in February/May/August /November (standard practice for customers in earlier versions of

PruFund, including Series D).

The comparison between the smoothed and unsmoothed unit price is checked on a monthly basis for Series E, whereas the

practice for earlier versions of PruFund, including Series D, is to do the comparison check on a quarterly basis.

Prudential stated that it introduced these changes as part of managing the guarantees offered by the With-Profits Fund through

the Holding Account while seeking to retain the fund’s investment flexibility and ensuring the fair treatment of all policyho lders.

It is crucial that Prudential’s marketing and communications material makes these distinctions clear to advisers and that advisers

therefore understand the different terms and treatment for customers invested in different series of PruFund.

9.3 SMOOTHING IN ACTION - PRUFUND

Vital reading for advisers in this regard is Prudential’s step-by-step guide to the PruFund smoothing process:

• For investments into PruFund funds held in: Prudential Investment Plan, Prudential ISA, Prudential International Investment

Bond, Flexible Retirement Plan and Trustee Investment Plan - https://www.pruadviser.co.uk/pdf/GENM92301.pdf.

• For investments, top-ups and monthly premiums into PruFund funds on Prudential Retirement Account from 25 August

2017 - https://www.pruadviser.co.uk/pdf/PRUF624304.pdf.

The following text from Prudential explains how the smoothing mechanism works in relation to the PruFund Growth Fund (Series

D).

“On a quarter date, if the net asset value per unit is more than 5% above or below the unit price, the unit price is repeated ly adjusted by half the difference between the unit price and the net asset value per unit until the net asset value per unit is within 5% above or below the unit price.

Between quarter dates, the net asset value per unit is averaged over the previous five working days to give the average net asset value per unit. If the net asset value per unit and the average net asset value per unit are both 10% (or more) above or below the unit price, the unit price will be increased or decreased immediately so that it is 2.5% below or above the net asset value per unit.

PRUFUND STRUCTURE, INVESTMENT MANAGEMENT AND GOVERNANCE PROCESSES

© AKG FINANCIAL ANALYTICS LTD 27 SEP 2019