pump primer list the functions of money & the desirable characteristics of moneylist the...

TRANSCRIPT

Pump PrimerPump Primer

• List the functions of money & List the functions of money & the desirable characteristics of the desirable characteristics of moneymoney

Unit IV: Economics of the Financial Market

“ECONOMICS for Christian Schools”

By Alan J. Carper

Bob Jones University Press. 1998

Chapter Chapter 1010

““Money & Money & Banking”Banking”

Objectives:Objectives:• Explain the definitions of money used in the Explain the definitions of money used in the

United States.United States.• Describe the properties of money.Describe the properties of money.• List the functions of money & the desirable List the functions of money & the desirable

characteristics of moneycharacteristics of money• Identify the different kinds of moneyIdentify the different kinds of money• Name the four designations given to Name the four designations given to

measurements of the money supplymeasurements of the money supply• Describe the banking activity of goldsmiths that Describe the banking activity of goldsmiths that

led to an expansion of the money supplyled to an expansion of the money supply• Describe a commercial bankDescribe a commercial bank• Describe the existing dual banking systemDescribe the existing dual banking system• List the functions of commercial banksList the functions of commercial banks• Explain the concept of near-monies.Explain the concept of near-monies.

Biblical Integration:Biblical Integration:

• We are to be good stewards of the We are to be good stewards of the money God has given unto us. (Luke money God has given unto us. (Luke 16:11) 16:11)

• Money is a tool to be used for His Money is a tool to be used for His service to provide for one's family, service to provide for one's family, feed the needy & spread the gospel.feed the needy & spread the gospel.

Money?Money?

• Proverbs 23: 4-5 - The uselessness of seeking riches

• Luke 16:11 – the necessity of being good stewards of the money we have

• 2 Cor. 8:9 – the source of true riches.

Proper Use of Money:Proper Use of Money:

• “The proper use of money allows man to provide for his family, to purchase clothing for the destitute, to obtain food for the hungry, to care for the sick, and to spread the gospel to the nations of the world. Money is a tool to be used for God’s service.”

(Carper, 129)

IntroductionIntroduction• The properties of money, the functions of The properties of money, the functions of

money the definitions of money are important money the definitions of money are important concepts for you to understand.concepts for you to understand.

• Money has existed for a long time, and a wide Money has existed for a long time, and a wide range of commodities have served as money range of commodities have served as money in different countries and at different times.in different countries and at different times.

• Before money, economies used a barter Before money, economies used a barter system.system.– The principle problem with a barter system is the The principle problem with a barter system is the

double coincidence of wantsdouble coincidence of wants required for success. required for success.• Double coincidence of wants means that you must find Double coincidence of wants means that you must find

someone who wants what you want to trade and has what someone who wants what you want to trade and has what you want!you want!

• Time-consuming and limiting!Time-consuming and limiting!

MoneyMoney• Properties of any commodity used as Properties of any commodity used as

money:money:– PortabilityPortability– UniformityUniformity– DurabilityDurability– Stability in valueStability in value– AcceptabilityAcceptability

• Commodities that have served as money:Commodities that have served as money:– Cigarettes and chocolate bars in prisoner war Cigarettes and chocolate bars in prisoner war

campscamps– Wampum (sm. Beads woven into colorful strips Wampum (sm. Beads woven into colorful strips

by the Indians)by the Indians)

• Functions of Money:Functions of Money:– Medium of exchangeMedium of exchange

• Eliminates the need of the double Eliminates the need of the double coincidence of wantscoincidence of wants

– Store of valueStore of value• Permits money to be held for use at a later Permits money to be held for use at a later

timetime

– Unity of Account, or standard-of-valueUnity of Account, or standard-of-value• There is an agreed-to measure for starting There is an agreed-to measure for starting

the prices of goods and services. (This the prices of goods and services. (This simplifies price comparisons.)simplifies price comparisons.)

““Money”Money”Activity 34 & 35Activity 34 & 35

by by Advanced Placement Economics Advanced Placement Economics

Teacher Resource ManualTeacher Resource Manual. . National Council on Economic National Council on Economic

Education, New York, N.YEducation, New York, N.Y

Activity 34: MoneyActivity 34: Money

• Use the table to evaluate how well each item Use the table to evaluate how well each item would perform the functions of money in would perform the functions of money in today’s economy. today’s economy.

• If an item seems to fulfill the function, put a If an item seems to fulfill the function, put a ““++” sign in the box; ” sign in the box;

• If it does not fulfill a function in your opinion, If it does not fulfill a function in your opinion, place a “place a “––” sign in the box.” sign in the box.

• Put a “Put a “??” Sign in the box if you are unsure ” Sign in the box if you are unsure whether the item fulfills the functions of whether the item fulfills the functions of moneymoney

• The item with the most + signs would be the The item with the most + signs would be the best form of money for you. best form of money for you.

• In the space below the table, list the top six In the space below the table, list the top six forms of money, according to your evaluation.forms of money, according to your evaluation.

Item Medium of Exchange Store of Value Standard of Value

Salt

Large stone wheels

Cattle

Gold

Copper coins

Beaver pelts

Personal checks

Savings account passbook

Prepaid phone card

Debt card

Credit card

Cigarettes

Playing cards

Bushels of wheat

$1 bill

$100 bill

- - - - + - - - -

+ + ++ + + - - -

+ + + - - -? + +

+ + ++ - + - - -

- - - - - -

+ + + + + +

My top six items: Gold, copper coins, personal checks, debit card, $1 bill and $100 bill

2.2. After you finish the evaluation in Question 1, After you finish the evaluation in Question 1, rate the various items in the table below. rate the various items in the table below.

– Evaluate how well they meet the characteristics Evaluate how well they meet the characteristics of money.of money.

– Again, if an item seems to fit a characteristic, use Again, if an item seems to fit a characteristic, use a “a “++” sign;” sign;

– If the item does not seem to fit a characteristic, If the item does not seem to fit a characteristic, use a “use a “--” sign;” sign;

– If there is a difference of opinion or if you are If there is a difference of opinion or if you are uncertain, use a “uncertain, use a “??”.”.

– The item with the most “The item with the most “++” signs would best fit ” signs would best fit the characteristics of money.the characteristics of money.

– In the space below the table, list your six top In the space below the table, list your six top items.items.

Item Portability Uniformity Acceptability Durability Stability in Value

Salt

Large stone wheels

Cattle

Gold

Copper coins

Beaver pelts

Personal checks

Savings account passbook

Prepaid phone card

Debt card

Credit card

Cigarettes

Playing cards

Bushels of wheat

$1 bill

$100 bill

+ + +

+

+

++++

++

++

+

+

++

+

+

++

?

+

+

+

+ +

+ +

+

+

+++

+

++

++

++

++

+?

??

?

?

?

- -

- - - - - - -

- -

+

-

- -

- -

- - -

-

- -

-

- - -

-

- -

My top six items: Gold, copper coins, personal checks, debit card, $1 bill and $100 bill

3.3. Why might factors such as ease of Why might factors such as ease of storage, difficulty in counterfeiting storage, difficulty in counterfeiting and security of electronic transfer and security of electronic transfer of funds also be characteristics that of funds also be characteristics that you might use in evaluating money?you might use in evaluating money?

For an item to be a good medium of exchange, you would want to minimize the costs of holding or storing it. Counterfeiting and security affect the item’s underlying value and might affect acceptability.

CheckCheck

• A check is an authorization to pay A check is an authorization to pay a designated amount of money a designated amount of money out of an established account.out of an established account.

(Carper, 136)

Negotiable Check:

(1) In writing

(2) Signed by the maker

(3) Payable to the bearer or to the order of a specific person

(4) Ordering the bank to pay a specified sum of money

(5) Bearing a date no older than six months.

(Carper, 136)

ChecksChecks• “Many corporations will use a stamp signature

instead of signing each individual check.”

• “On most checks the writer writes out the amount of the check in both words and in numerals. If the two do not agree, the written amount in words is the legal amount of the check.”

• “Checks older than six months are considered “stale” dated and by law cannot be cashed. It is also illegal to “post” date a check (date a check for time in the future).”

(Carper, 136)

Measuring the Money Measuring the Money SupplySupply

• How much money exists in the How much money exists in the United States?United States?– This is not an easy question to answer, This is not an easy question to answer,

since money represents purchasing since money represents purchasing power and it greatly depends on how it power and it greatly depends on how it is measured. is measured. • M-IM-I• M-2M-2

M-1M-1• Economists refer to first method of measuring the Economists refer to first method of measuring the

money supply as M-1 money supply as M-1 (1)(1)““currency outside the U.S. Treasury, Federal currency outside the U.S. Treasury, Federal

Reserve Banks, and the vaults of depository Reserve Banks, and the vaults of depository institutions; institutions;

(2)(2)traveler's checks of nonbank issuers; traveler's checks of nonbank issuers; (3)(3)demand deposits at commercial banks (excluding demand deposits at commercial banks (excluding

those amounts held by depository institutions, the those amounts held by depository institutions, the U.S. government, and foreign banks and official U.S. government, and foreign banks and official institutions) less cash items in the process of institutions) less cash items in the process of collection and Federal Reserve float; and collection and Federal Reserve float; and

(4)(4)other checkable deposits (OCDs), consisting of other checkable deposits (OCDs), consisting of negotiable order of withdrawal (NOW) and automatic negotiable order of withdrawal (NOW) and automatic transfer service (ATS) accounts at depository transfer service (ATS) accounts at depository institutions, credit union share draft accounts, and institutions, credit union share draft accounts, and demand deposits at thrift institutions. Seasonally demand deposits at thrift institutions. Seasonally adjusted M1 is constructed by summing currency, adjusted M1 is constructed by summing currency, traveler's checks, demand deposits, and OCDs, each traveler's checks, demand deposits, and OCDs, each seasonally adjusted separately.” (“seasonally adjusted separately.” (“Money StockMoney Stock…”)…”)

M-2M-2• A broader measure of the money supply is referred to as A broader measure of the money supply is referred to as

M-2:M-2:– Includes M-1 money plus all money available to spend Includes M-1 money plus all money available to spend

after a short delay: after a short delay:

(1)(1)Savings deposits (including money market deposit Savings deposits (including money market deposit accounts); accounts);

(2)(2)Small-denomination time deposits (time deposits in Small-denomination time deposits (time deposits in amounts of less than $100,000), less individual amounts of less than $100,000), less individual retirement account (IRA) and Keogh balances at retirement account (IRA) and Keogh balances at depository institutions; and depository institutions; and

(3)(3)Balances in retail money market mutual funds, less IRA Balances in retail money market mutual funds, less IRA and Keogh balances at money market mutual funds. and Keogh balances at money market mutual funds. Seasonally adjusted M2 is constructed by summing Seasonally adjusted M2 is constructed by summing savings deposits, small-denomination time deposits, and savings deposits, small-denomination time deposits, and retail money funds, each seasonally adjusted separately, retail money funds, each seasonally adjusted separately, and adding this result to seasonally adjusted M1.” and adding this result to seasonally adjusted M1.” (“(“Money StockMoney Stock…”)…”)

M-3M-3• The broadest measure of the money supply is known as The broadest measure of the money supply is known as

M-3 – no longer published by Federal Reserve as of M-3 – no longer published by Federal Reserve as of March 16, 2006.March 16, 2006.

• Includes M-1 & M-2Includes M-1 & M-2(1)(1)““Balances in institutional money market mutual funds; Balances in institutional money market mutual funds; (2)(2)Large-denomination time deposits (time deposits in Large-denomination time deposits (time deposits in

amounts of $100,000 or more); amounts of $100,000 or more); (3)(3)Repurchase agreement (RP) liabilities of depository Repurchase agreement (RP) liabilities of depository

institutions, in denominations of $100,000 or more, on institutions, in denominations of $100,000 or more, on U.S. government and federal agency securities; and U.S. government and federal agency securities; and

(4)(4)Eurodollars held by U.S. addressees at foreign Eurodollars held by U.S. addressees at foreign branches of U.S. banks worldwide and at all banking branches of U.S. banks worldwide and at all banking offices in the United Kingdom and Canada. Large-offices in the United Kingdom and Canada. Large-denomination time deposits, RPs, and Eurodollars denomination time deposits, RPs, and Eurodollars exclude those amounts held by depository institutions, exclude those amounts held by depository institutions, the U.S. government, foreign banks and official the U.S. government, foreign banks and official institutions, and money market mutual funds. institutions, and money market mutual funds. Seasonally adjusted M3 is constructed by summing Seasonally adjusted M3 is constructed by summing institutional money funds, large-denomination time institutional money funds, large-denomination time deposits, RPs, and Eurodollars, each adjusted deposits, RPs, and Eurodollars, each adjusted separately, and adding this result to seasonally separately, and adding this result to seasonally adjusted M2.” (“adjusted M2.” (“Discontinuance of M3Discontinuance of M3 “) “)

THE BANKING SYSTEMTHE BANKING SYSTEM

The Federal Reserve regulates and influences the activities of the commercial banks, thrift institutions, and money market funds, whose deposits make up the nation’s money.

THE BANKING SYSTEMTHE BANKING SYSTEM

Financial Institutions

• ““Is the collection of organizations that assist house-Is the collection of organizations that assist house-holds in channeling their money to businesses and holds in channeling their money to businesses and government.”government.”

• ““CommercialCommercial BanksBanks are “full service” institutions are “full service” institutions offering a wide range of services for both individuals offering a wide range of services for both individuals and businesses. Account for nearly half of all assets and businesses. Account for nearly half of all assets held by financial institutions. Also, it is important to held by financial institutions. Also, it is important to know that all commercial banks are chartered.” know that all commercial banks are chartered.”

(Carper 140, 143)

THE BANKING SYSTEMTHE BANKING SYSTEM

• Commercial BanksCommercial Banks

– A A commercial bankcommercial bank is a firm that is licensed by the is a firm that is licensed by the

Comptroller of the Currency in the U.S. Treasury (or Comptroller of the Currency in the U.S. Treasury (or

by a state agency) to accept deposits and make loans. by a state agency) to accept deposits and make loans.

– About 7,400 commercial banks operate in the United About 7,400 commercial banks operate in the United

States in 2006.States in 2006.

– Because of mergers, this number is down from 13,000 Because of mergers, this number is down from 13,000

a few years ago.a few years ago.

THE BANKING SYSTEMTHE BANKING SYSTEM

Types of DepositsTypes of Deposits

– A commercial bank accepts three types of A commercial bank accepts three types of

deposits:deposits:

• Checkable depositsCheckable deposits

• Savings depositsSavings deposits

• Time depositsTime deposits

THE BANKING SYSTEMTHE BANKING SYSTEM

Profit and Prudence: A Balancing ActProfit and Prudence: A Balancing Act– The goal of a commercial bank is to maximize the The goal of a commercial bank is to maximize the

long-term wealth of its stockholders.long-term wealth of its stockholders.– To achieve this goal, a bank must be prudent in the To achieve this goal, a bank must be prudent in the

way it uses its depositors’ funds and balance way it uses its depositors’ funds and balance security for the depositors against profit for its security for the depositors against profit for its stockholders.stockholders.

THE BANKING SYSTEMTHE BANKING SYSTEM

Cash AssetsCash Assets–A bank’s A bank’s cash assets cash assets consist of its reserves and consist of its reserves and funds that are due from other banks as payments for funds that are due from other banks as payments for checks that are being cleared.checks that are being cleared.–A bank’s A bank’s reservesreserves consist of currency in the bank’s consist of currency in the bank’s vaults plus the balance on its reserve account at a vaults plus the balance on its reserve account at a Federal Reserve Bank.Federal Reserve Bank.–The Fed requires the banks and other financial The Fed requires the banks and other financial institutions to hold a minimum percentage of institutions to hold a minimum percentage of deposits as reserves, called the deposits as reserves, called the required reserve required reserve ratioratio..

THE BANKING SYSTEMTHE BANKING SYSTEM

Interbank LoansInterbank Loans–When banks have excess reserves, they can lend When banks have excess reserves, they can lend them to other banks that are short of reserves in an them to other banks that are short of reserves in an interbank loans market.interbank loans market.–The interbank loans market is called federal funds The interbank loans market is called federal funds market and the interest rate on interbank loans is the market and the interest rate on interbank loans is the federal funds ratefederal funds rate..–The Fed’s policy actions target the federal funds The Fed’s policy actions target the federal funds rate.rate.

THE BANKING SYSTEMTHE BANKING SYSTEM

Securities and Loans Securities and Loans –Securities held by banks are bonds issued by the Securities held by banks are bonds issued by the U.S. government and by other large, safe, U.S. government and by other large, safe, organizations. organizations. –A bank earns a moderate interest rate on securities, A bank earns a moderate interest rate on securities, but it can sell them quickly if it needs cash.but it can sell them quickly if it needs cash.–Loans are the funds that banks provide to Loans are the funds that banks provide to businesses and individuals and include outstanding businesses and individuals and include outstanding credit card balances.credit card balances.–Loans earn the highest interest rate but cannot be Loans earn the highest interest rate but cannot be called in before the agreed date.called in before the agreed date.

THE BANKING SYSTEMTHE BANKING SYSTEM

Bank Deposits and Assets: The Relative Bank Deposits and Assets: The Relative MagnitudesMagnitudes

– In 2007, checkable deposits at commercial banks In 2007, checkable deposits at commercial banks in the United States, included in M1, are about 7 in the United States, included in M1, are about 7 percent of total commercial bank deposits. percent of total commercial bank deposits.

– The other 63 percent of deposits are savings The other 63 percent of deposits are savings deposits and small time deposits, which are part of deposits and small time deposits, which are part of M2.M2.

Financial InstitutionsFinancial Institutions

• Functions include:Functions include: – (1)(1) Accepting Deposits. (Primary Accepting Deposits. (Primary

source of source of money for loans)money for loans)– (2)(2) Extending LoansExtending Loans

(3) Provision of Miscellaneous Services(3) Provision of Miscellaneous Services

(Carper 140, 141)

Creating A BankCreating A Bank

1.1. Obtain a CharterObtain a Charter- - Apply to the “Comptroller of the Apply to the “Comptroller of the Currency” (federal charter) or state Currency” (federal charter) or state treasurer’s office (state charter)treasurer’s office (state charter)

2.2. Raise Financial CapitalRaise Financial Capital- - selling sharesselling shares

3.3. Buying EquipmentBuying Equipment4.4. Accepting DepositsAccepting Deposits

(Blade et al. 524)

5.5. Establishing A Reserve AccountEstablishing A Reserve Account- - “The bank’s required reserves equal “The bank’s required reserves equal the required reserve ratio multiplied by the the required reserve ratio multiplied by the amount of deposits.”amount of deposits.”-- “Excess reserves equal actual reserves “Excess reserves equal actual reserves minus required reserves. The bank can loan minus required reserves. The bank can loan only its excess reserve.”only its excess reserve.”

6.6. Clearing ChecksClearing Checks

7.7. Buying Government SecuritiesBuying Government Securities

-- “Government securities provide a bank with “Government securities provide a bank with an an income and are a safe asset that is easily income and are a safe asset that is easily converted converted back into reserves when necessary.”back into reserves when necessary.”

8.8. Making LoansMaking Loans

-- Generates the primary income for the Generates the primary income for the institution (I.e., interest).institution (I.e., interest).

(Blade et al. 524)

THE BANKING SYSTEMTHE BANKING SYSTEM

• Thrift InstitutionsThrift Institutions–Three types of thrift institutions are savings and Three types of thrift institutions are savings and loan associations, savings banks, and credit unions. loan associations, savings banks, and credit unions. –A A savings and loan associationsavings and loan association (S&L) is a financial (S&L) is a financial institution that accepts checkable deposits and institution that accepts checkable deposits and savings deposits and that makes personal, savings deposits and that makes personal, commercial, and home-purchase loans.commercial, and home-purchase loans.–A A savings banksavings bank is a financial institution that accepts is a financial institution that accepts savings deposits and makes mostly consumer and savings deposits and makes mostly consumer and home-purchase loans. home-purchase loans.

THE BANKING SYSTEMTHE BANKING SYSTEM

–A A credit unioncredit union is a financial institution owned by a is a financial institution owned by a social or economic group, such as a firm’s social or economic group, such as a firm’s employees, that accepts savings deposits and makes employees, that accepts savings deposits and makes mostly consumer loans.mostly consumer loans.–Like commercial banks, thrift institutions hold Like commercial banks, thrift institutions hold reserves and must need minimum reserve ratios set reserves and must need minimum reserve ratios set by the Fed.by the Fed.

Contractual Savings Contractual Savings Institutions Institutions

• Institutions who operate under contract Institutions who operate under contract to receive regular payments or to receive regular payments or premiums, invest the funds, and return premiums, invest the funds, and return stipulated amounts prescribed by the stipulated amounts prescribed by the contract – insurance companies and contract – insurance companies and pension funds.pension funds.

(Carper 138, 139)

Finance Companies Finance Companies

• Make consumer loans (tend to offer Make consumer loans (tend to offer higherhigher rates than commercial banks)rates than commercial banks)

(Carper 138, 139)

Investment Investment Companies Companies

• Mutual funds and other investment Mutual funds and other investment companies pool shareholders money companies pool shareholders money to purchase stock & return profit to to purchase stock & return profit to the shareholders.the shareholders.

(Carper 138, 139)

THE BANKING SYSTEMTHE BANKING SYSTEM

THE FEDERAL RESERVE THE FEDERAL RESERVE SYSTEMSYSTEM

• The Federal Reserve SystemThe Federal Reserve System–The The Federal Reserve SystemFederal Reserve System is the central bank of is the central bank of the United States. the United States. –A A central bankcentral bank is a public authority that provides is a public authority that provides banking services to banks and regulates financial banking services to banks and regulates financial institutions and markets. institutions and markets. –The Fed’s main task is to regulate the interest rate The Fed’s main task is to regulate the interest rate and quantity of money to achieve low and and quantity of money to achieve low and predictable inflation and sustained economic growth.predictable inflation and sustained economic growth.

Activity 35: “What’s All This About Activity 35: “What’s All This About the Ms?”the Ms?”

1.1. What are the three basic functions of money?What are the three basic functions of money?

2.2. Why is it important for the Fed to know the size and Why is it important for the Fed to know the size and rate of growth of the money supply? rate of growth of the money supply?

(A)(A) What are the effects if the money supply grows What are the effects if the money supply grows too slowly?too slowly?

(B)(B) What are the effects if the money supply grows What are the effects if the money supply grows too rapidly?too rapidly?

Medium of exchange, a standard of value (unit of account), and a store of value.

The size of the money supply and the rate at which it is growing can have a significant impact on the economic well being of the country.

If the money supply is growing too slowly, the likelihood of recession increases because the demand for money will increase, driving interest rates up. As interest rates rise, investment declines, slowing the growth rate of real output.

If the money supply is growing too quickly, it could lead to inflation.

3.3. Name a type of money that serves primarily as Name a type of money that serves primarily as a medium of exchange.a medium of exchange.

4.4. Name a type of money that serves primarily as Name a type of money that serves primarily as a store of value.a store of value.

5.5. With the use of credit cards becoming more With the use of credit cards becoming more prominent and the availability of credit broader prominent and the availability of credit broader than ever, why are credit cards not included in than ever, why are credit cards not included in the Ms?the Ms?

Currency, coin, debit cards or checkable deposits

Savings account or money market mutual fund account.

Credit cards are short-term loans. Credit-card bills are not directly subtracted from checking accounts. Instead the credit-card holder pays the bill from a checking or NOW (negotiable order of withdrawal ) account. Not only should loans NOT be counted as money, but if they were and the payment were also counted, one economic transaction would be double-counted in the money supply.

6.6. Why is it difficult for the Fed to get an accurate Why is it difficult for the Fed to get an accurate measure of the money supply?measure of the money supply?

7.7. Why must the fed continue to develop new Why must the fed continue to develop new ways to track the money supply?ways to track the money supply?

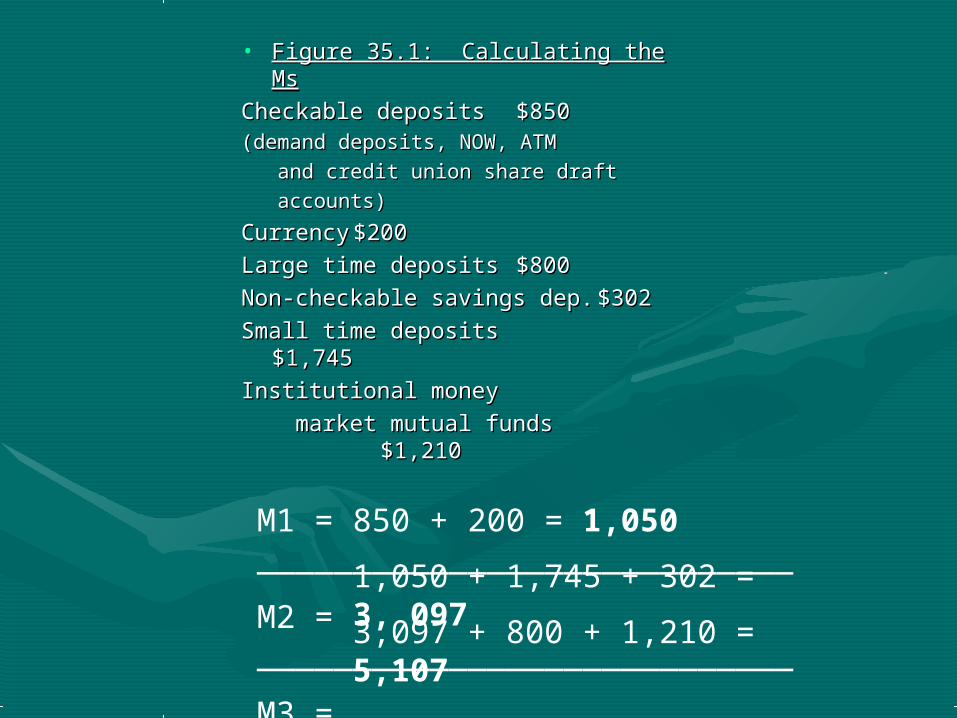

8.8. Use the data in Figure 35.1 to calculate M1, Use the data in Figure 35.1 to calculate M1, M2, and M3. Assume that all items not M2, and M3. Assume that all items not mentioned are zero. Show all components for mentioned are zero. Show all components for your answers.your answers.

Because of the volume of transactions in the United states, which can range into the trillions on a daily basis, getting an accurate measure of each transaction can be an arduous task. The inputs are constantly changing as banks make new loans and people repay loans ahead of schedule.

Because of technological innovation in the financial services industry and profit maximizing behavior on the part of commercial banks, the Fed must find new measures for tracking the money supply to assist with monetary policy.

• Figure 35.1: Calculating the MsFigure 35.1: Calculating the Ms

Checkable depositsCheckable deposits $850$850(demand deposits, NOW, ATM (demand deposits, NOW, ATM

and credit union share draft and credit union share draft

accounts)accounts)

CurrencyCurrency $200$200

Large time depositsLarge time deposits $800$800

Non-checkable savings dep.Non-checkable savings dep. $302$302

Small time depositsSmall time deposits $1,745 $1,745

Institutional moneyInstitutional money

market mutual funds market mutual funds $1,210$1,210

M1 = ____________________________

M2 = ____________________________

M3 = ____________________________

850 + 200 = 1,050

1,050 + 1,745 + 302 = 3, 0973,097 + 800 + 1,210 = 5,107

Works CitedWorks Cited

Blade, Robin, and Michael Parkin. Blade, Robin, and Michael Parkin. Foundations of Economics: Foundations of Economics: Instructor’s ManualInstructor’s Manual. 2nd ed. Boston: Pearson Education, Inc., . 2nd ed. Boston: Pearson Education, Inc., 2007. 2007.

Carper, Alan. Carper, Alan. Economics for Christian SchoolsEconomics for Christian Schools. Greenville: Bob Jones . Greenville: Bob Jones University Press, 1998. University Press, 1998.

““Discontinuance of M3.”Discontinuance of M3.” Federal ReserveFederal Reserve. 9 Mar . 9 Mar 2006. 21 Mar 2006. 21 Mar 2008. 2008. http://www.federalreserve.gov/Releases/H6/20060309/h6.txt

““Money Stock Measure.”Money Stock Measure.” Federal Reserve StatisticalFederal Reserve Statistical ReleaseRelease. 20 Mar . 20 Mar 2008. 21 Mar 2008. 2008. 21 Mar 2008. http://www.federalreserve.gov/releases/h6Current/

"The New King James Version." "The New King James Version." Logos Bible SoftwareLogos Bible Software. CD_ROM. . CD_ROM. ed.ed. 20042004..