q3 2011 sales presentation uklast - carrefour · pdf filerobust supermarket growth ex‐petrol...

TRANSCRIPT

Carrefour Q3 2011 sales

13 October 2011

Flat Q3 sales in a tougher environment

2

Flat sales in Q3:– Decrease in ex‐petrol LFL adjusted for calendar: ‐0.6%

– Including +1.1% impact from new sqm, sales ex‐petrol at constant exchange rates adjusted for calendar were up 0.5% …

– … and down ‐0.8% including a ‐1.3% impact from currencies

France: deterioration in LFL sales largely due to new commercial mix in

hypermarkets

Western Europe: Resilient performance in a negative context: ‐2.2% LFL ex‐

petrol adjusted for calendar in Q3 vs. ‐2.5% in H1

Emerging markets: Continued growth supported by solid performance in Brazil

and expansion in China

3

100

1.1 (1.3)(0.7)

99.2

100.5

Q3 2010sq.m &

acquisitionsLike

for like

Calendarimpact

adjustmentFx impact

Q3 2011const. FXadj. for calendar impact

Q3 2011current FXadj. forcalendarimpact

0.1

Change in Q3 2011 sales, excluding petrol

(Index Q3 2010 = 100; % change)

Slight constant‐currency sales growth driven by expansion

99.4

Q3 2011LfL

adj. for calendar impact

(0.6)

+0.5

(0.8)

4

France

Europe

Latin America

Change in sales excluding petrol adjusted for calendar impact (%)

Asia

0.2

Q1 2011

7.3

2.1

(3.0)

6.4

Q2 2011

(3.0)

(1.0)0.2

13.4

(4.1)

11.0

(3.8)

(0.6)

LFLTotal (constant exchange rates)

7.95.3 (0.3)

Reset in France, resilience in Europe, ongoing growth in Latam, slowdown in Asia

(2.3)(1.9)

(2.6)(3.1)

6.99.9

4.0 (1.9)

Q3 2011

555

Ex‐petrol, ex‐calendar LFL sales down 2.3% with continued outperformance from smaller formats:

– Hypermarkets: Ex‐petrol, ex‐calendar LFL sales down ‐4.4% vs. ‐3.3% in Q2

– Carrefour Market: Ex‐petrol, ex‐calendar LFL sales down ‐0.6% vs +1.3% in Q2

– Convenience stores: 4.3% LFL increase overall with continued excellent performance of stores converted under Carrefour banners (double digit growth)

Action plan underway: progressive commercial mix realignment, reduced out‐of‐stocks, rollout of Carrefour branded products

Q3 2010

1000.4(2.3)

98.1

Change in Q3 2011 sales, ex‐petrol(index Q3 2010 = 100; % change)

Calendarimpact

sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

France: LFL sales deteriorate as action plan launched

097.7

Q3 2011LFL adj. for calendar

666

Resilient performance in a difficult environment

– Hypermarkets ex‐petrol ex calendar Q3 LFL: ‐3.7% improving on ‐4.9% reported in Q2

– Supermarkets ex‐petrol ex calendar Q3 LFL: ‐1.6%, vs. ‐1.3% in Q2

Resilience in food with flat LFL, weak performance in non‐food as discretionary spending continues to be impacted

100 1.2(4.1)97.90.8

Change in Q3 2011 sales, excluding petrol (index Q3 2010 = 100; % change)

Q3 2010 Calendarimpact

sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

Spain: Resilient performance in a tough context

96.7

Q3 2011LFL adj. for calendar

777

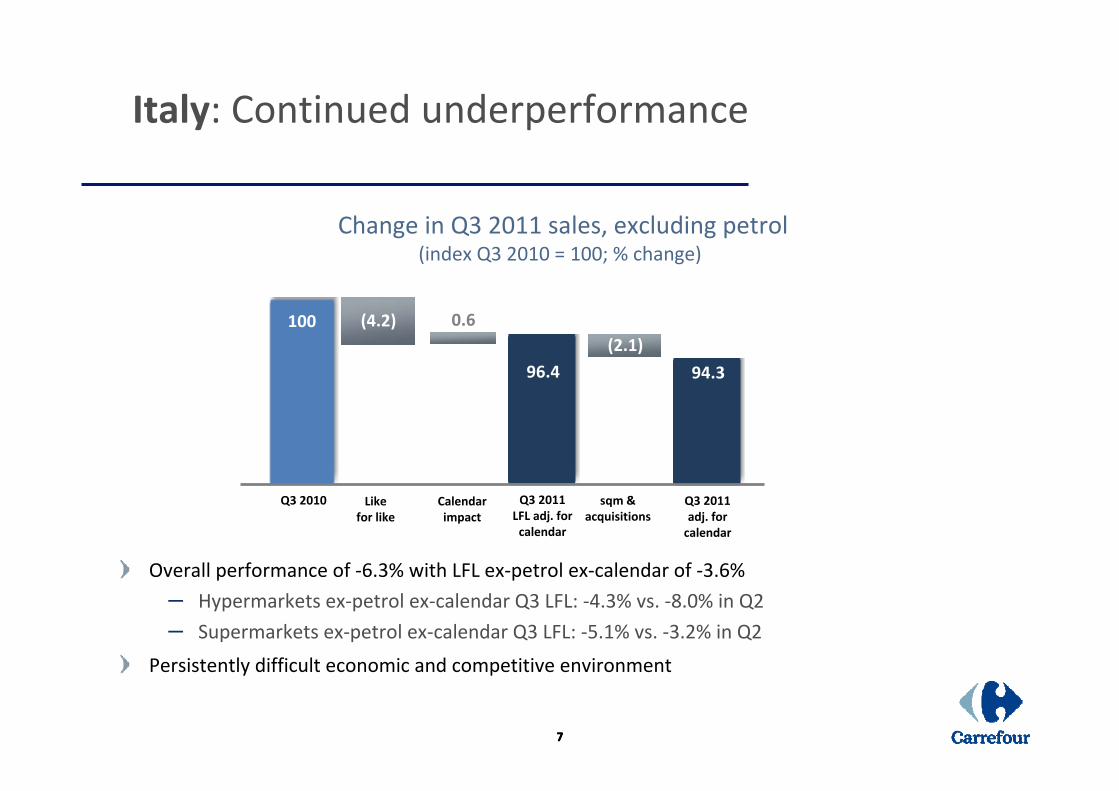

100(2.1)

(4.2)

94.3

0.6

Overall performance of ‐6.3% with LFL ex‐petrol ex‐calendar of ‐3.6%

– Hypermarkets ex‐petrol ex‐calendar Q3 LFL: ‐4.3% vs. ‐8.0% in Q2

– Supermarkets ex‐petrol ex‐calendar Q3 LFL: ‐5.1% vs. ‐3.2% in Q2

Persistently difficult economic and competitive environment

Q3 2010 Calendarimpact

sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

Change in Q3 2011 sales, excluding petrol(index Q3 2010 = 100; % change)

Italy: Continued underperformance

96.4

Q3 2011LFL adj. for calendar

888

100

(3.8)2.7

98.8

(0.1)

Growth in LFL sales (+2.6% ex petrol adjusted for calendar)

Overall sales slightly negative due to the impact of store closures (‐3.8%)

Encouraging growth in hypermarkets: +1.9% ex petrol and adjusted for calendar

Robust supermarket growth ex‐petrol LFL adjusted for calendar: +3.1% vs. +4.0% in Q2

Q3 2010 Calendarimpact

sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

Change in Q3 2011 sales, excluding petrol (index Q3 2010 = 100; % change)

Belgium: Further evidence of turnaround

102.6

Q3 2011LFL adj. for calendar

999

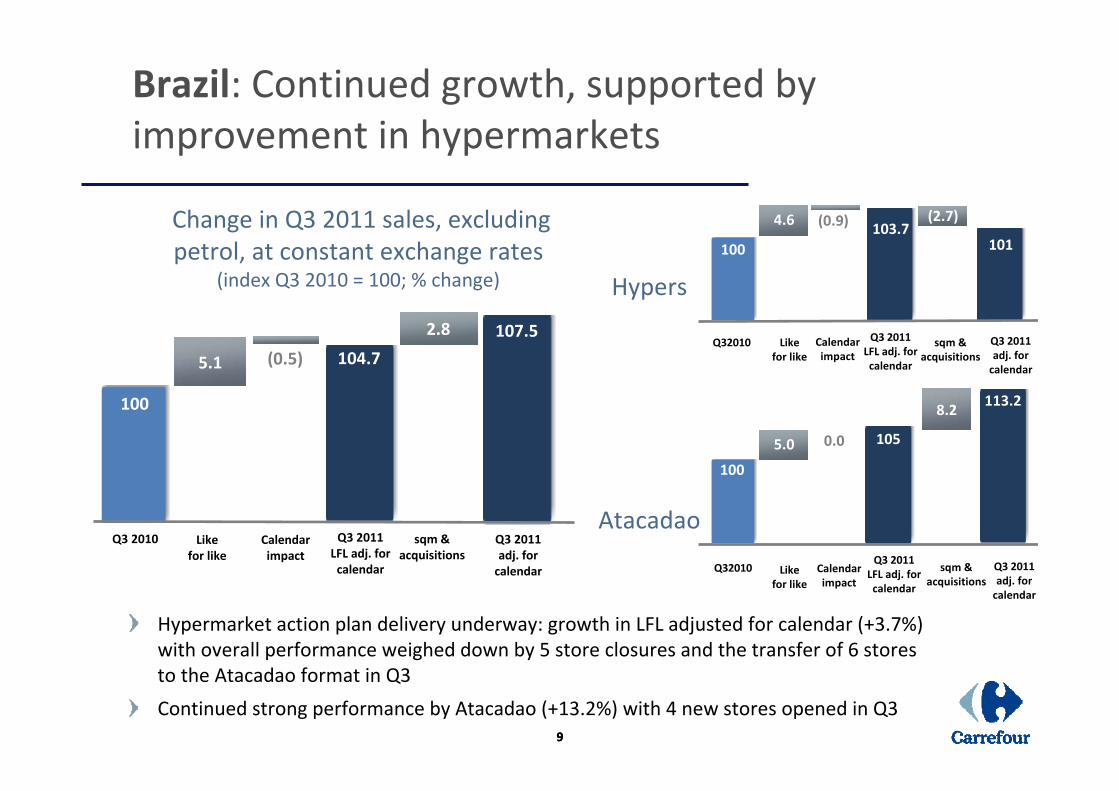

Hypermarket action plan delivery underway: growth in LFL adjusted for calendar (+3.7%) with overall performance weighed down by 5 store closures and the transfer of 6 stores to the Atacadao format in Q3

Continued strong performance by Atacadao (+13.2%) with 4 new stores opened in Q3

100

5.1

107.5

(0.5)

Change in Q3 2011 sales, excluding petrol, at constant exchange rates

(index Q3 2010 = 100; % change)

2.8

100

5.0

113.2

0.0

Q32010 Calendarimpact

sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

Atacadao

Hypers

100

4.6

101

(0.9)

Q32010 Calendarimpact

sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

8.2

Q3 2010 Calendarimpact

sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

(2.7)

Brazil: Continued growth, supported by improvement in hypermarkets

104.7

Q3 2011LFL adj. for calendar

103.7

Q3 2011LFL adj. for calendar

105

Q3 2011LFL adj. for calendar

101010

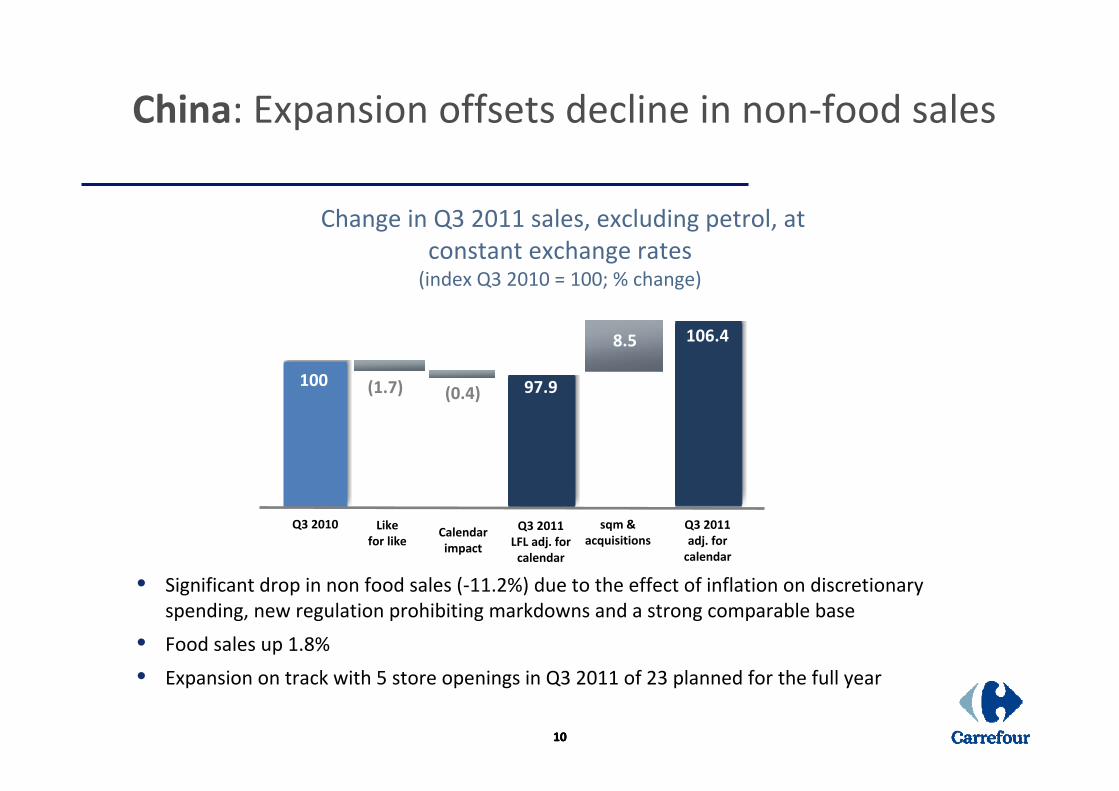

• Significant drop in non food sales (‐11.2%) due to the effect of inflation on discretionary spending, new regulation prohibiting markdowns and a strong comparable base

• Food sales up 1.8%

• Expansion on track with 5 store openings in Q3 2011 of 23 planned for the full year

100

8.5

(1.7)

106.4

Q3 2010 sqm &acquisitions

Likefor like

Q3 2011adj. for calendar

Change in Q3 2011 sales, excluding petrol, at constant exchange rates (index Q3 2010 = 100; % change)

China: Expansion offsets decline in non‐food sales

97.9

Q3 2011LFL adj. for calendar

(0.4)

Calendarimpact

111111

Carrefour Planet: Rollout on track

50 Carrefour Planet at end Sept. 2011– France: 15

– Spain: 27

– Belgium: 6

– Italy: 1

– Greece: 1

On track to operate 82 Carrefour Planet in Europe at year‐end

12

Outlook

Macroeconomic conditions likely to remain challenging in the coming months within an increasingly uncertain environment

Unchanged priorities:

– Specific Action Plan in France

– Adapting to the new context in Southern Europe

– Transformation Plan and cost cutting delivery

– Pursue growth ambitions in key emerging markets, rollout of Carrefour Planet and Carrefour‐branded products

2011 Current Operating Income guidance broadened to a range of ‐15% to ‐20% vs. restated 2010, ex DIA

Carrefour Q3 2011 sales

13 October 2011