quarto trim size: 174mm x 240mm - pdfs.semanticscholar.org

TRANSCRIPT

Inte

rnatio

nal Jo

urn

al of P

rod

uc

tivity and

Pe

rform

anc

e M

anag

em

en

tV

olu

me

67 N

um

be

r 7 20

18e

me

raldp

ub

lishin

g.c

om

www.emeraldinsight.com/loi/ijppm

Volume 67 Number 7 2018ISSN 1741-0401

Volume 67 Number 7 2018

International Journal of

Productivity and Performance Management

International Journal of

Productivity and Performance Management

The official journal of the World

Confederation of Productivity Science

Quarto trim size: 174mm x 240mm

Number 7

1089 Editorial advisory board

1090 Editorial

1091 Implementation of environmental management practices in the Ghanaian mining and manufacturing supply chainsSamuel Famiyeh and Amoako Kwarteng

1113 The relationship between management characteristics and firm innovationMahdi Salehi, Mahmoud Lari DashtBayaz and Samaneh Mohammadi Moghadam

1132 Improving public sector service delivery: a developing economy experienceEbenezer Adaku, Kwasi Amoako-Gyampah, Seth Nii Anang Lomotey, Charles Teye Amoatey and Samuel Famiyeh

1147 Impact of workplace bullying on employee outcomes: a study of Indian managerial employeesArpana Rai and Upasna Agarwal

1171 Forced distribution systems and attracting top talentStephanie J. Thomason, Amy Brownlee, Amy Beekman Harris and Hemant Rustogi

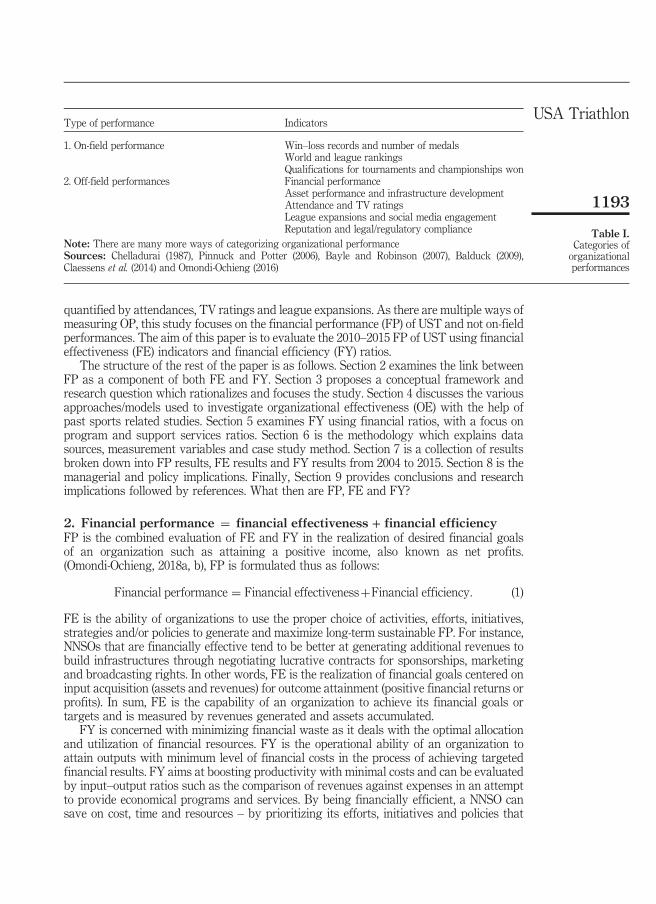

1192 USA Triathlon: a 2010–2015 case study of financial performance using effectiveness indicators and efficiencyPeter Omondi-Ochieng

1214 Performance measurement and management systems as IT artefacts: characterising, contextualising and valuing their effective use in SMEsMarie Marchand and Louis Raymond

1234 Experimenting lean dynamic performance management systems design in SMEsCarmine Bianchi, Graham Winch and Federico Cosenz

Certificate Number 1985ISO 14001

ISOQAR certified Management System,awarded to Emerald for adherence to Environmental standard ISO 14001:2004.

International Journal of Productivity and Performance Managementis indexed and abstracted in:ABI InformBusiness Source Alumni Edition/Complete/Complete:

Government Edition/Corporate/Corporate Plus/Elite/Main Edition/Premier

Cabell’s Directory of Publishing Opportunities in Management and Marketing

Education Research Complete/Education SourceEmerald Management ReviewsErgonomics AbstractsINSPECProQuestPsycINFOSafetyLitTechnicalEducation and Training AbstractsTOC Premier (EBSCO)

International Journal of Productivity and Performance Management addresses new tools, developments and reflective analyses related to approaches designed to improve individual, group and organisational performance in and across all forms of organisations.

Emerald Publishing LimitedHoward House, Wagon Lane, Bingley BD16 1WA, United KingdomTel +44 (0) 1274 777700; Fax +44 (0) 1274 785201E-mail [email protected] more information about Emerald’s regional offices please go to http://www.emeraldgrouppublishing.com/officesCustomer helpdesk :Tel +44 (0) 1274 785278; Fax +44 (0) 1274 785201E-mail [email protected], subscription and missing claims enquiries:E-mail [email protected] +44 (0) 1274 777700; Fax +44 (0) 1274 785201

Missing issue claims will be fulfilled if claimed within six months of date of despatch. Maximum of one claim per issue.Hard copy print backsets, back volumes and back issues of volumes prior to the current and previous year can be ordered from Periodical Service Company. Tel +1 518 537 4700; E-mail [email protected] For further information go to www.periodicals.com/emerald.html

Reprints and permissions serviceFor reprint and permission options please see the abstract page of the specific article in question on the Emerald web site (www.emeraldinsight.com), and then click on the “Reprints and permissions” link. Or contact:E-mail [email protected] Publisher and Editors cannot be held responsible for errors or any consequences arising from the use of information contained in this journal; the views and opinions expressed do not necessarily reflect those of the Publisher and Editors, neither does the publication of advertisements constitute any endorsement by the Publisher and Editors of the products advertised.

No part of this journal may be reproduced, stored in a retrieval system, transmitted in any form or by any means electronic, mechanical, photocopying, recording or otherwise without either the prior written permission of the publisher or a licence permitting restricted copying issued in the UK by The Copyright Licensing Agency and in the USA by The Copyright Clearance Center. Any opinions expressed in the articles are those of the authors. Whilst Emerald makes every effort to ensure the quality and accuracy of its content, Emerald makes no representation implied or otherwise, as to the articles’ suitability and application and disclaims any warranties, express or implied, to their use.

Emerald is a trading name of Emerald Publishing LimitedPrinted by CPI Group (UK) Ltd, Croydon, CR0 4YY

CO-EDITORSDr Luisa Huaccho HuatucoSenior Lecturer in Operations Management, University of York, UKE-mail [email protected] Nicky ShawSenior Lecturer in Operations Management, Leeds University Business School, UKE-mail [email protected]

EDITORIAL ASSISTANTJennifer WebsterE-mail [email protected]

REGIONAL EDITOR – EUROPEDr Cláudia S Sarrico Technical University of Lisbon, Portugal

ISSN 1741-0401© 2018 Emerald Publishing Limited

Quarto trim size: 174mm x 240mm

Guidelines for authors can be found at:www.emeraldgrouppublishing.com/ijppm.htm

EDITORIAL ADVISORY BOARD

Dr Rabiul AhasanUniversity of Oulu, Finland

Professor Jiju AntonyHeriot-Watt University, UK

Umit Sezer BititciHeriot Watt University, UK

Dr Thomas F. BurgessLeeds University Business School, UK

Dr Yu-wang ChenThe University of Manchester, UK

Dr Andre A. de WaalMaastricht School of Management,The Netherlands

Dr Jacky HollowayNorthampton Business School, UK

Dr Kepa MendibilUniversity of Strathclyde, UK

Professor Low Sui PhengNational University of Singapore, Singapore

Professor Zoe RadnorLeicester University, UK

Dr Nick RichSwansea University, UK

Associate Professor Sanjay Kumar SinghAbu Dhabi University, United Arab Emirates

Professor Amrik SohalMonash University, Australia

Professor Karen SpensHanken School of Economics, Finland

Professor Eileen van AkenVirginia Tech, USA

Professor Li ZhengTsinghua University, People’s Republic ofChina

International Journal ofProductivity and Performance

ManagementVol. 67 No. 7, 2018

p. 1089r Emerald Publishing Limited

1741-0401

1089

Editorialadvisory

board

Quarto trim size: 174mm x 240mm

Editorial

Welcome to the seventh issue of IJPPM this year. We have eight thought-provoking anddiverse papers in this issue ranging with studies in Ghana, Iran, India, the USA, Canada andItaly, using a broad variety of methods.

Famiyeh and Kwarteng provide insights into the implementation of environmentalmanagement practices (EMP) in Ghana. They used a survey questionnaire collected from219 managers either in manufacturing or extracting industries. Employing factor analysis, thefindings supported that regulative andmimetic institutional pressure have a significant influenceon EMP whereas normative institutional pressure did not have a significant influence.

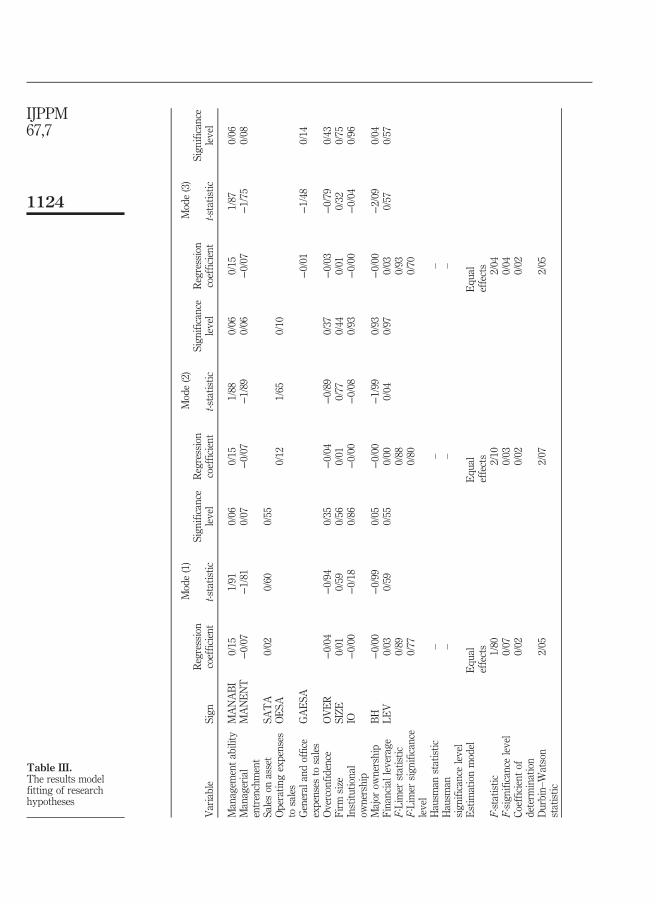

Salehi, Lari Dashtbayaz and Mohammadi study the relationship between managementcharacteristics and firm innovation in Tehran Stock Exchange-listed companies. Using datafrom 125 companies, descriptive-correlational design and panel data regression models wereapplied. They found that managerial entrenchment has a negative effect on innovation,whereas managerial ability could foster innovation; surprisingly neither agency cost noroverconfidence has a significant effect.

Adaku, Amoako-Gyampah, Kwasi, Lomotey, Amoatey and Famiyeh provide anotherstudy in Ghana, this time with the Pension Trust Company. They used extensive data (oldsystem: 14,400 claims and new system: 41,600 claims) in two types of programmes andcompared them statistically. They found that the new system has reduced processing timeby 20 per cent. This is quite an improvement.

Rai and Agarwal investigate the topic of workplace bullying and its influence oninnovative work behaviour. Using data from 835 managerial employees in India, they foundthat workplace bullying is negatively related to workplace innovation and positively relatedto neglect. Based on their findings, they provide useful recommendations to managers.

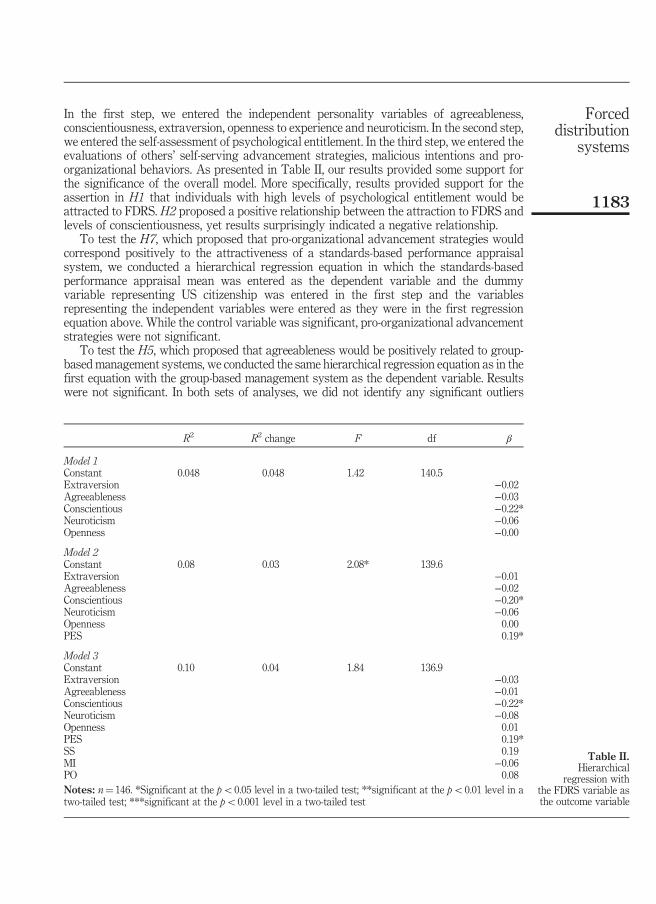

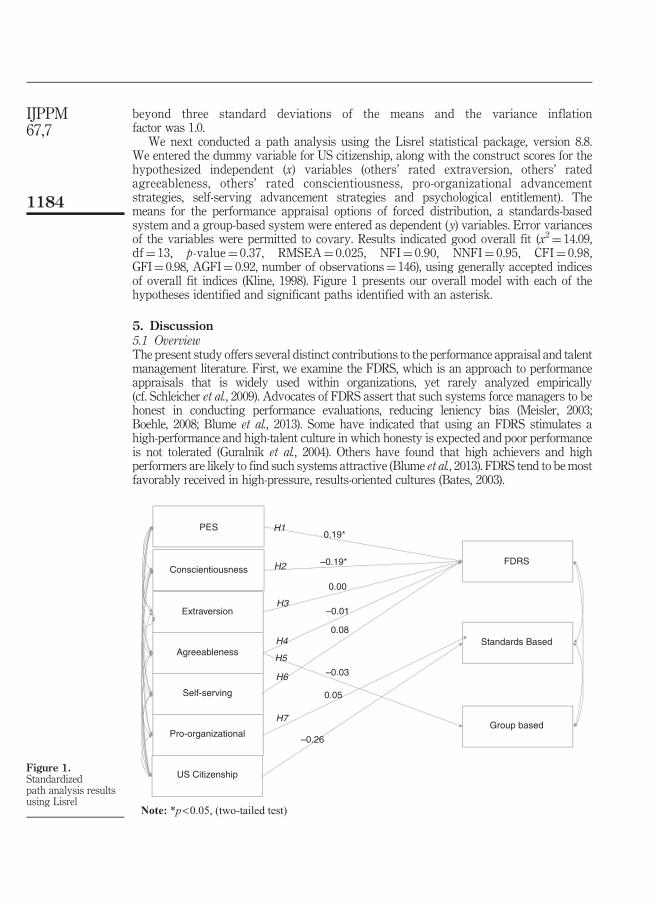

Sticking with the workplace, Thomason, Brownlee, Beekman and Rustogi studiedindividuals’ attraction to different performance appraisal types using a five-factor model ofpersonality types and applying a forced distribution ranking system (FDRS). Theysurveyed 148 students on graduate-level business courses in the USA. Their findingssuggest that FDRS are attractive to those with high levels of psychological entitlement andlow levels of conscientiousness, which contrasts with the existing research.

Ochieng presents a case study of financial performance in the non-profit context ofUS Triathlon. He shows that financial performance is related to both financialeffectiveness and financial efficiency; this is particularly important in contexts wherefinancial resources are unreliable.

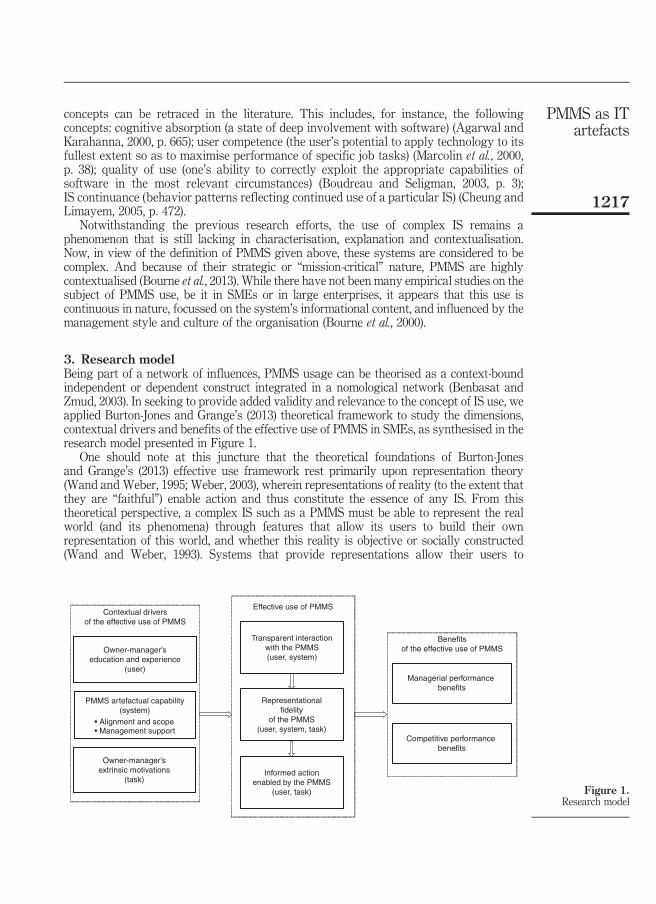

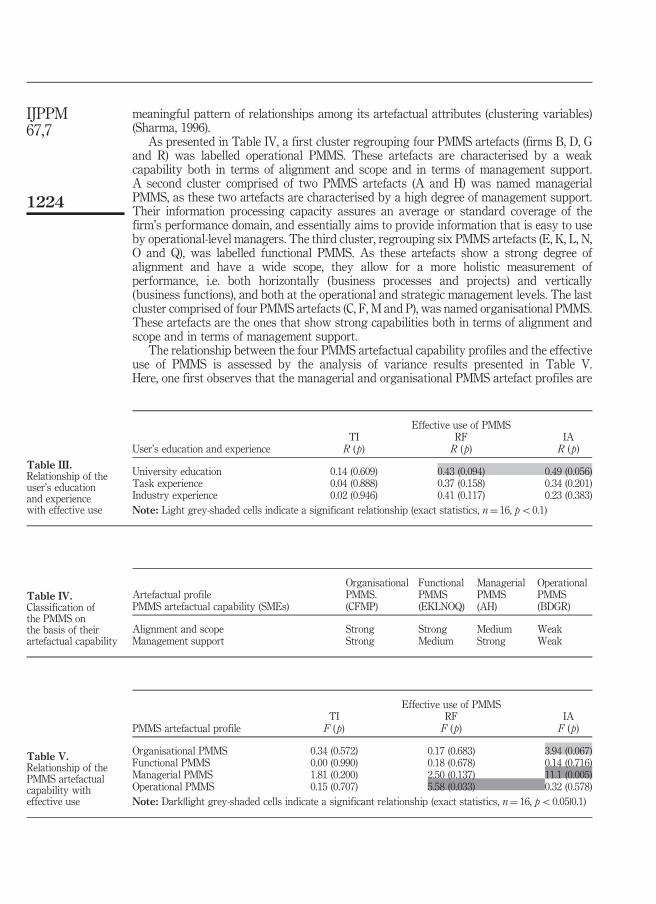

Marchand and Raymond’s article studies performance measurement and managementsystems as IT artefacts using the Burton-Jones and Grange’s (2013) theoretical framework.Their work is applied to 16 SMEs in Canada and findings indicate that transparentinteraction enables representational fidelity, which in turn enables informed action. Thiscontributes to both the performance management and IS literatures.

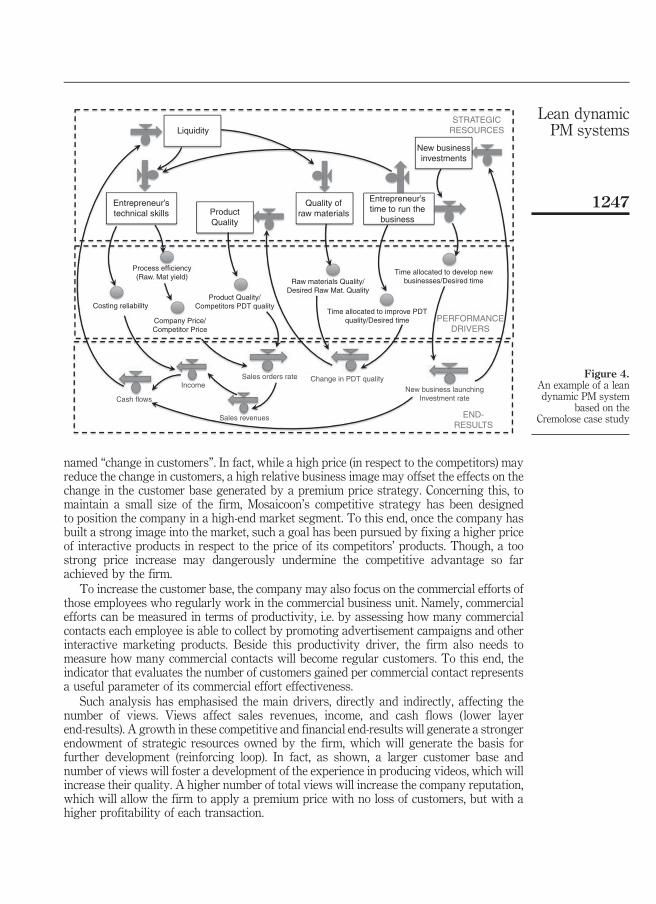

Finally, our reflective practice article by Bianchi, Winch and Consenz presents worksupporting entrepreneurial capabilities by incorporating individual attributes into organisationroutines associated with lean dynamic performance management systems in small and microenterprises in Italy. Their approach contrasts four organisation types: artisan, new companystart-up, established firm and micro-giant company, and utilises system dynamics modelling.

As you can see, again another varied and interesting content to our seventh issue.We hope you enjoy!

Nicky E. Shaw and Luisa Delfa Huaccho Huatuco

International Journal ofProductivity and PerformanceManagementVol. 67 No. 7, 2018pp. 1090-1090© Emerald Publishing Limited1741-0401DOI 10.1108/IJPPM-07-2018-0258

1090

IJPPM67,7

Quarto trim size: 174mm x 240mm

Implementation of environmentalmanagement practices in the

Ghanaian mining andmanufacturing supply chains

Samuel Famiyeh and Amoako KwartengGhana Institute of Management and Public Administration, Accra, Ghana

AbstractPurpose – The purpose of this paper is to understand the driving forces of environmental managementpractices in mining and manufacturing firms using data from Ghana.Design/methodology/approach – Prior exploratory factor analysis and structural equation modeling,based on questionnaire survey data, were used to study the driving forces of environmental managementpractices in the extractive and manufacturing firms using institutional theory.Findings – Environmental management practices by organizations in Ghana are driven by regulatory andthe mimetic pressures. Normative pressure has no significant effect on environmental management practices.The authors found no difference between the extractive and the manufacturing sectors as far as the resultsare concerned.Research limitations/implications – The results indicate the importance of regulatory bodies indeveloping good environmental policies that are implemented and monitored in order to achieve improvedenvironmental performance. Effective implementation of environmental policies is likely to motivate other firmsto mimic the actions of implementing organizations. One limitation of this work is the use of data from Ghana. Itis important for other researchers to assess these relationships using data from a wider geographical area.Practical implications – The results indicate that organizations implement environmental managementpractices as a result of coercive and mimetic pressures. In practice, it is therefore important for the regulatorybodies, such as the Environmental Protection Agency Ghana, to be very innovative in developing goodenvironmental regulations that are monitored to ensure implementation by all polluting sources. This isbecause the results indicate that the monitoring of regulations by regulatory bodies seems to be connected tothe implementation of these regulations. Such implementation is also expected to be benchmarked by otherfirms, thereby influencing the “greening” agenda in Africa.Originality/value – The study illustrates and provides some insights, and builds on the literature in thearea of green supply chain strategies for a developing country’s environment. This is one of the few studiesthat investigate the driving forces of environmental management implementation using the institutionaltheory based on data from the African business environment.Keywords Ghana, Productivity, Environmental, Coercive, Mimetic, NormativePaper type Research paper

1. IntroductionPoorly regulated manufacturing and industrial activities have resulted in seriousenvironmental problems such as global warming, ozone layer depletion, increasing wasteand pollution levels all over the world (Shukla et al., 2009; King and Lenox, 2001). Despite therapidly increasing research on companies’ environmental strategies and environmentalmanagement practices, the motivation for proactive implementation still remains unclear(Delmas and Toffel, 2004). It has been established that green practices have a positive impacton sustainability for all stakeholders (Balasubramanian and Shukla, 2017). Past researchersfocusing on investigating why organizations have implemented environmental managementpractices have concluded these initiatives are either due to pressures from regulation andcompetition (Christmann, 2000; Dean and Brown, 1995; Delmas, 2003) or sometimes thesepressures arise from non-governmental organizations (Lawrence and Morell, 1995). In thisstudy, institutional theory is used as a framework to show that governments, regulators,workers, professional associations, customers and competitors impose coercive, normative

International Journal ofProductivity and Performance

ManagementVol. 67 No. 7, 2018

pp. 1091-1112© Emerald Publishing Limited

1741-0401DOI 10.1108/IJPPM-04-2017-0095

Received 19 April 2017Revised 2 July 2017

7 August 201717 August 2017

Accepted 26 August 2017

The current issue and full text archive of this journal is available on Emerald Insight at:www.emeraldinsight.com/1741-0401.htm

1091

Environmentalmanagement

practices

Quarto trim size: 174mm x 240mm

and mimetic pressures on organizations to implement environmental management initiatives(Carroll and Delacroix, 1982), using data from Ghana.

Apart from the numerous legal regulations that establish environmental practices suchas the environmental assessment regulations, 1999, L.I.1652 (EPA Ghana, 1999); firms facepressures from different stakeholders regarding the implementation of environmentalmanagement practices, including downstream customers who prefer to buy eco-friendlyproducts (Hu and Hsu, 2010; Shukla et al., 2009). The 1999 environmental assessmentregulations 24 (1) set out by the Environmental Protection Agency (EPA) Ghana clearlystate that all organizations operating in Ghana who have their preliminary environmentalreports of environmental impact statement approved shall submit to the Agency anEnvironmental Management Plan (EMP) in respect of their operations within 18 months ofbeginning operations and thereafter every three years (EPA Ghana, 1999). The question is,apart from such formal command and control policies set up and monitored forimplementation by firms in Ghana that drive the implementation of environmentalmanagement systems, what other forces drive the implementation of environmentalmanagement practices by firms in Ghana? The purpose of this study is to answer thispressing question using data from the Ghanaian business environment.

There have been some works related to environmental management such as Tuttle andHeap (2007), Prado-Lorenzo and García-Sánchez (2010), Björklund and Forslund (2013)and Wang and Sarkis (2013) on the integration of environmental and economic issues. Tuttleand Heap (2007) provided some evidence concerning the emerging consensus, onthe importance to integrate environmental issues with economic and business issues todrive improvements in productivity and environmental impacts. Their results indicate thisintegration is very effective when environmental issues are planned as part of a total review ofthe life-cycle of products and their manufacturing and delivery processes. Prado-Lorenzo andGarcía-Sánchez (2010) investigated the effect of operation size, environmental conditions andmanagement on municipal sewerage services using data from sewerage services in somemunicipalities in Spain. The results indicated that operation size and environmentalconditions have a significant impact on efficiency, however, the management type, public orprivate, does not impact the degree of efficiency. A related work by Björklund and Forslund(2013) investigated the purposes of having environmental performance management systems(EPMS) in logistics management and how these performance measures can influence the focusof the supply chain using data from Swedish firms. They found target setting as the mostcommon purpose of implementing EPMS into logistics management. Wang and Sarkis (2013),using data from the USA, investigated whether companies’ environmental and social supplychain activities impact on financial performance. In their findings, they indicated thatintegrated sustainable supply chain management, i.e., including social and environmentalsupply chain management efforts, is positively associated with corporate financialperformance measured by return on assets and return on equity.

According to To and Tang (2014), the motivations and perceived benefits of theimplementation of ISO 14001 by organizations were studied in Macao SAR and theyidentified the main factors driving the implementation of EMS were the promotion ofenvironmental awareness among internal employees, regulatory compliance and thereduction of waste from operations. The above examples indicate some of the research workon the issue under investigation; however, most of the research findings are based on datafrom the developed world and that of Asia. This clearly indicates the need for researchinvestigating the driving forces of environmental management practices in organizationsfrom the developing economies especially, the Sub-Saharan Africa given the pressingenvironmental issues there.

The literature presents some research in the area of environmental management inSub-Saharan Africa. These include environmental literacy by Owusu et al. (2017),

1092

IJPPM67,7

small-scale mining and environmental management by Aryee et al. (2003) and extent ofstakeholder influence on environmental performance by Mensah (2014). Mensah (2014)examined the extent to which primary and secondary stakeholders influence theenvironmental performance of hotels in the Accra Metropolis of Ghana, and found thatprimary stakeholders such as customers and board of directors have significant influenceon the environmental performance of hotels while size of hotel moderates the effect ofstakeholders on the environmental performance of hotels. Our study is similar; however,different from that of Mensah (2014) in that the main theory underlying his work wasstakeholder theory and his emphasis was specific to the hotel sector. The current studyexamines the drivers of environmental management implementation using institutionaltheory as well as data from more than one industrial sector. Industries in less developedeconomies face difficult challenges because of the lack of technology, human resources,expertise, strong institutions and competition. Thus, studies that contribute to theknowledge drivers of environmental management practices of organizations in such hostileenvironments should interest researchers. The contribution of this study to the literature isvery important in that, we, first, examine the applicability of our proposed model of driversof environmental management in a less developed Sub-Saharan African country.In addition, we contribute to fostering the development of a growing body of greensupply chain management knowledge in developing countries.

The rest of the paper is structured into five main parts. First, we present the literaturereview and the research hypothesis, together with the conceptual model. This is followed bythe research method and the data collection procedures. We then present the data analysisand the main findings. We finally present the discussion, conclusions, limitations and areasfor future research in the last section.

2. Theoretical background and research hypotheses2.1 Institutional theoryInstitutional theory suggests that organizations are social systems, and is often used as atheoretical framework to explain why organizations adopt practices, policies and procedures(DiMaggio and Powell, 1983; Meyer and Rowan, 1977 cited in Scott, 2001). Institutional theorydescribes how organizations should behave (Hatch, 1997; Powell and DiMaggio, 1991; Scott,1995) and the actions to be taken in response to environmental pressures (Grewal andDharwadkar, 2002; Hoffman, 1997; Scott, 2001) that are beyond their control (Hoffman, 1977).

The theory suggests that an organization’s choices and actions are influenced by socialbehaviors, norms and values within the environment in which they operate (Selznick, 1957).This means that organizations are constrained by their environment and sometimes have toadopt and adhere to rules and practices created because of environmental pressure, whichmay not be the organization’s original intent. Meyer and Rowan (1977) stressed that to gainlegitimacy and enhance their survival; organizations have to conform to institutionalpressures within their operating environment. It is important therefore for organizations torespond to pressures from the environment, not only for the sake of resources andcustomers but also for political power and institutional legitimacy in order to achieve social,as well as economic, rewards (Carroll and Delacroix, 1982). Institutional isomorphism,according to DiMaggio and Powell (1983), occurs through three main mechanisms, namely,coercive pressure, normative pressure and mimetic pressures. We have therefore used thesethree mechanisms as our main constructs that underlie our investigation.

2.2 Literature review and the development of hypotheses2.2.1 Coercive pressures and firm’s environmental management practices. Scott (1987)claimed that organizational behavior is influenced by two primary mechanisms: imposition

1093

Environmentalmanagement

practices

and inducement. The imposition mechanism is enacted through regulatory institutionswhile inducement mechanism works through other organizations that constrain theorganization and direct its behavior (Oliver, 1991). Organizations, for instance, are forced tocomply with laws enacted by regulatory institutions by making the necessary changes intheir structure and processes in order to avoid the potential costs, uncertainty and legalliabilities for noncompliance (Clemens and Douglas, 2006; DiMaggio and Powell, 1983).

In the coercive view of institutional theory, the emphasis is placed on the conformity tolay down rules and rewards for good behavior as well as punishment for non-conformance(DiMaggio and Powell, 1983). Thus, coercive pressures may be considered as a force, apersuasion for firms to take certain actions which they did not intend to, due to pressuresarising from government regulations or laws (DiMaggio and Powell, 1983); customers(Teo et al., 2003). Grewal and Dharwadkar (2002) claimed that firms are often forced intoadopting practices or actions to avoid punishment; and sanctions (Scott, 1995).

One of the key stakeholders that influence the adoption of environmental managementpractices is governmental institutions. In Ghana, such government bodies in charge ofenvironmental issues are the EPA; the ministry responsible for environment, science andtechnology; Minerals Commission; Forestry Commission; etc. These bodies are basicallyinvolved in regulating environmental issues by setting up the rules and regulations for andto monitor all polluting sources. These regulatory agencies are therefore responsible forpromulgating and enforcing these regulations, a form of coercive power. Many countries,especially in Europe, have strict environmental regulations that prohibit hazardousproducts and promote recycling and products take-back (Tibben-Lembke, 2002; Fergusonand Browne, 2001).

Researchers have established the enforcement of legislation and regulations as amotivating factor for firms’ implementation of environmental practices (Carraro et al., 1996;Delmas, 2002; Majumdar and Marcus, 2001; Rugman and Verbeke, 1998). Delmas (2002)indicated one of the key players for companies to adopt ISO 14001, is the government. In asurvey by Delmas in 2000 among European and US firms, a substantial number ofmanagers indicated they adopt measures such as ISO 14001 in their operations in their questto satisfy regulatory compliance. To and Tang (2014), in a study in Macao SAR, identifiedthe top driving forces for the adoption of environmental management practices were theencouragement of environmental issues among workers, the effective management ofoperations in order to stay in compliance and reduction of waste in operations.

Heras-Saizarbitoria et al. (2011) conducted an extensive study of the driving forces andthe benefits of implementing ISO 14001 by surveying 214 Spanish companies. They foundthat the most highly rated benefit was compliance with environmental laws and regulations,followed by environmental effectiveness improvement, less environmental problems andimproving customer satisfaction. Williamson et al. (2006) used empirical research into theenvironmental practices of 31 manufacturing small- and medium-sized enterprises (SMEs)and found that “business performance” and “regulation” considerations drive theenvironmental behavior of the enterprises.

Jennings and Zandbergen (1995) were among the first researchers who applied theinstitutional theory to explain the adoption of environmental management practices in theorganization, and indicated coercive forces, prescribed in the form of regulations andregulatory enforcement, have been the main driving forces of environmental management.Based on data from the wine industry in New Zealand, Dodds et al. (2013) found that thestrong drivers for environmental sustainability initiatives are organizations concern aboutthe state of the environment and social responsibility, followed by requirements forexporting and protection of agricultural land. Zailani et al. (2012) using data from 132 EMS-ISO-14001 – certified manufacturing firms in Malaysia, found a strong relationship between

1094

IJPPM67,7

environmental regulations and incentive as a driver of eco-design initiatives inorganizations surveyed. These regulations and incentives also seem to driveenvironmental performance of the firms. In a study by Tate et al. (2011), concerning thedriving forces of supplier adoption of environmental practices in the USA based oninstitutional theory analysis, they identified supplier adoption of environmental practices ismore likely in the presence of coercive, normative and mimetic pressures. Cordano (1993) isof the view that the increasing levels of penalties, fines and legal costs have driven theimportance for companies to comply with environmental regulations. Lampe et al. (1991)also indicate the need for firms to stay ahead of environmental regulations in order to avoidvery expensive capital refits.

Building on regulatory or coercive pressure from institutional theory, the followinghypothesis is proposed:

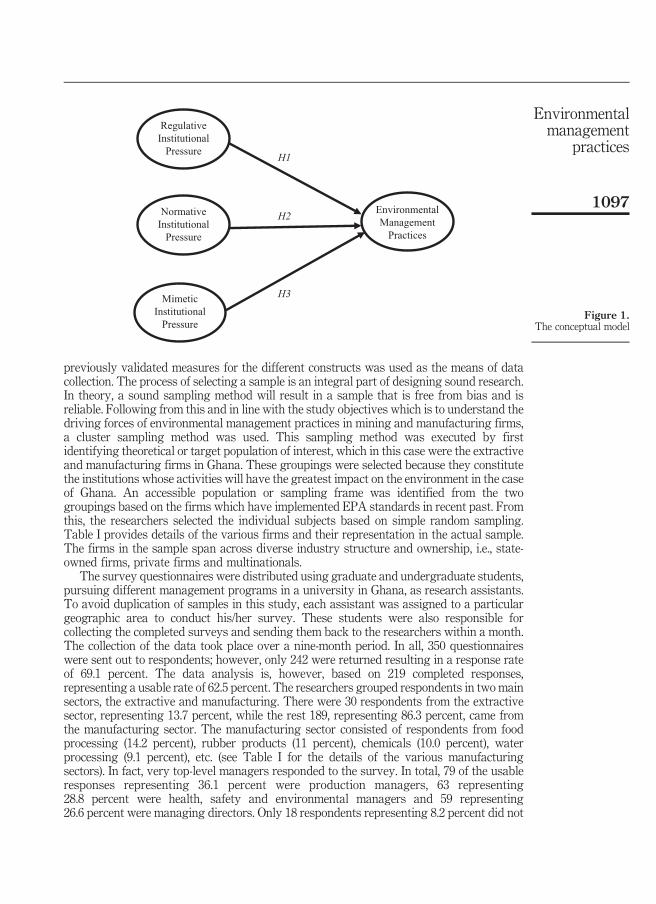

H1. Regulatory or coercive institutional pressure will influence the implementation ofenvironmental management practices by firms in Ghana.

2.2.2 Normative pressures and firm’s environmental management practices. Normativepressure refers to pressure that stems from professionalization, which has to do with thecollective efforts by individuals of similar occupation to describe the ways and processes oftheir work and also establish a legitimate cognitive base for their occupational autonomy(Cheng and Yu, 2008; DiMaggio and Powell, 1983; Larson, 1991). A study conducted byKollman and Prakash (2002) in two countries in Europe and the USA indicated why countrieshave different rates of EMS certification. They found out that the decision on whether to go forcertification and the kind of standard, either ISO 14001 or EMAS, was basically influenced bythe pressures from stakeholders in the various industry associations, in addition to regionalchamber of commerce, suppliers and regulators. In a survey of 63 Brazilian companies fromthe chemical, mechanical and electronic industries, Gavronski et al. (2008) identified foursources driving the implementation of environmental management practices: reaction topressures from the external stakeholders; proactive in expectation of future business concerns;legal concerns; and internal influences. Heide and John (1992) argued that when personnelwithin an organization aim to achieve the results of the same expectations, these expectationswill become shared norms, which in turn influence organization attitudes toward themaintenance of relationship networks, and curtail behaviors that promote individual goals.Firms are pressured to conform to the shared norms and assure personnel in the field of itscommitment to maintain procedural legitimacy (Zsidisin et al., 2005). In a survey of 209manufacturers of Pearl River Delta in China, by Ye et al. (2013), the results indicated thatinstitutional pressures including government pressure, customer pressure and competitorpressure have a statistically significant positive influence on top managers’ posture towardreverse logistics implementation. Using data from the hotel sector in Ghana, Mensah (2014)indicated that customers, as well as the board of directors, had a more significant influence onthe environmental performance of hotels. However, this relationship seems to be moderatedby the size of the hotel. Zailani et al. (2012), based on data from firms in Malaysia, indicated astrong relationship between customer pressures and design of ecologically friendly products.

Competitive pressures sometimes force firms to implement environmental programs(e.g. environmentally friendly programs, green products and environmental marketingprograms) without studying the impacts it would have on the firm ( Jennings andZandbergen, 1995). Building on the normative pressure from the institutional theoryperspectives, the following hypothesis is proposed:

H2. Normative institutional pressure will influence the implementation of environmentalmanagement practices by firms in Ghana.

1095

Environmentalmanagement

practices

2.2.3 Mimetic pressures and firm’s environmental management practices. In addition tocoercive and normative pressures, firms may also be under pressure to mimic practices thatsuccessful leading firms have adopted. Moreover, in an effort to establish qualitymanagement standards, firms are forced to respond to customer requirements andmaintain customer–supplier relationships (Anderson et al., 1999). According to DiMaggioand Powell (1983), a mimetic process occurs when an organization models itself on otherthriving organizations within an uncertain environment. Organizations tend to modelthemselves after other organizations they believe are well managed and able to survive in acompetitive environment.

Corporate managers, for fear of regulations and customer dissatisfaction, are more likelynot to take actions that are detrimental to the reputation of the company, especially whenmarkets become more competitive, and the issue of customer satisfaction becomes relativelymore important (Bansal and Clelland, 2004; Singhapakdi et al., 2001). This is normally verysuitable when consumers place a premium on environmentally friendly products. In suchsituations, it is imperative for competing firms to mimic or benchmark themselves byimplementing environmental or green management practices in order to stay in thecompetition. In developing a new theoretical proposition regarding how suppliers who arenot early adopters are influenced to adopt environmental practices, Tate et al. (2011)concluded that supplier adoption of environmental practices is more likely if coercive,normative and mimetic institutional forces are in play. In a work focusing on theinstitutional perspective on the adoption of green information systems and technology,Chen et al. (2011) concluded that the mimetic and coercive pressures significantly drivegreen information system and technology adoption. They indicated, in particular, outcome-based imitation and imposition-based coercion represent major institutional processes.According to Chu et al. (2017), mimetic pressures drawn from the concept of institutionalpressure have a positive significant impact on the performance of top managers, this impacttends to significantly affect the practices of green supply chain management and firmperformance. Firms turn to follow the footsteps of successful competitors; this statementwas found to be true by Yang (2016) who in his research found that firms mimic theenvironmental practices that successful leading firms have adopted in order to enhancetheir corporate image. Building on mimetic pressure from institutional theory, the followinghypothesis is proposed:

H3. Mimetic institutional pressure will influence the implementation of environmentalmanagement practices by firms in Ghana.

Figure 1 summarizes the hypotheses of this study in a conceptual model. The hypothesizedrelationships between the constructs are all indicated as positive (+).

3. Material and methods3.1 Data collection and samplingIn this study, we targeted the use of respondents involved in decision making at the top ofthe organization and also in decisions making related to the environment. Theserespondents are referred to as key informants because they normally report on relationshipsbetween their organizations and other organizations and are not reporting on their personalfeelings or behavior (Van Weele and van Raaij, 2014). Miles and Arnold (1991) applaud theuse of informants in the collection of research data, as they are of the view that informantssuch as top managers, managing directors, production managers were always willing andable to provide insight into their own underlying business orientations through a writtenself-administered survey instrument. These respondents were therefore responding onbehalf of their organizations and not their personal emotions. A questionnaire made up of

1096

IJPPM67,7

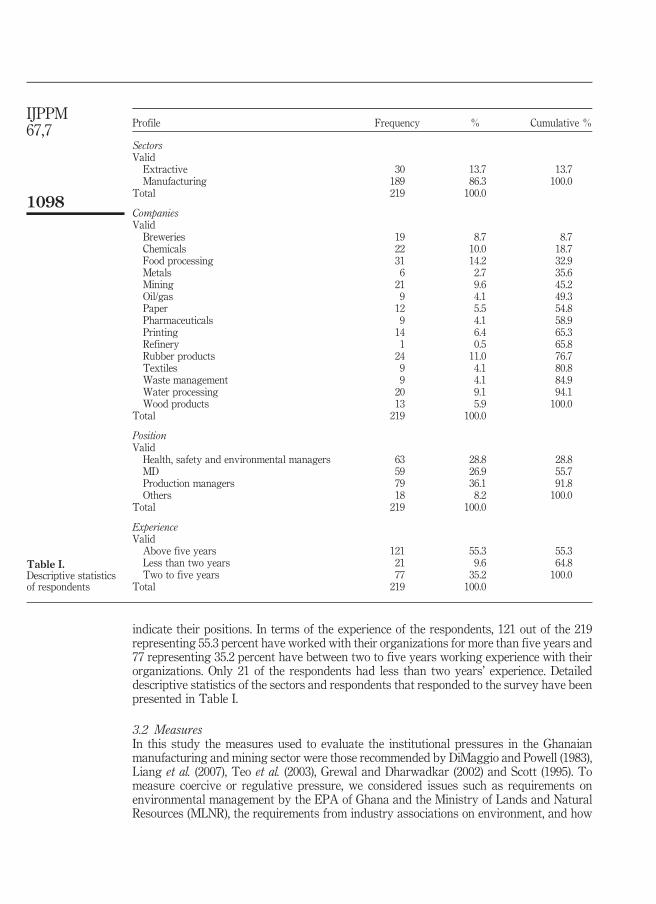

previously validated measures for the different constructs was used as the means of datacollection. The process of selecting a sample is an integral part of designing sound research.In theory, a sound sampling method will result in a sample that is free from bias and isreliable. Following from this and in line with the study objectives which is to understand thedriving forces of environmental management practices in mining and manufacturing firms,a cluster sampling method was used. This sampling method was executed by firstidentifying theoretical or target population of interest, which in this case were the extractiveand manufacturing firms in Ghana. These groupings were selected because they constitutethe institutions whose activities will have the greatest impact on the environment in the caseof Ghana. An accessible population or sampling frame was identified from the twogroupings based on the firms which have implemented EPA standards in recent past. Fromthis, the researchers selected the individual subjects based on simple random sampling.Table I provides details of the various firms and their representation in the actual sample.The firms in the sample span across diverse industry structure and ownership, i.e., state-owned firms, private firms and multinationals.

The survey questionnaires were distributed using graduate and undergraduate students,pursuing different management programs in a university in Ghana, as research assistants.To avoid duplication of samples in this study, each assistant was assigned to a particulargeographic area to conduct his/her survey. These students were also responsible forcollecting the completed surveys and sending them back to the researchers within a month.The collection of the data took place over a nine-month period. In all, 350 questionnaireswere sent out to respondents; however, only 242 were returned resulting in a response rateof 69.1 percent. The data analysis is, however, based on 219 completed responses,representing a usable rate of 62.5 percent. The researchers grouped respondents in two mainsectors, the extractive and manufacturing. There were 30 respondents from the extractivesector, representing 13.7 percent, while the rest 189, representing 86.3 percent, came fromthe manufacturing sector. The manufacturing sector consisted of respondents from foodprocessing (14.2 percent), rubber products (11 percent), chemicals (10.0 percent), waterprocessing (9.1 percent), etc. (see Table I for the details of the various manufacturingsectors). In fact, very top-level managers responded to the survey. In total, 79 of the usableresponses representing 36.1 percent were production managers, 63 representing28.8 percent were health, safety and environmental managers and 59 representing26.6 percent were managing directors. Only 18 respondents representing 8.2 percent did not

H1

H2

H3

RegulativeInstitutional

Pressure

NormativeInstitutional

Pressure

MimeticInstitutional

Pressure

EnvironmentalManagement

Practices

Figure 1.The conceptual model

1097

Environmentalmanagement

practices

indicate their positions. In terms of the experience of the respondents, 121 out of the 219representing 55.3 percent have worked with their organizations for more than five years and77 representing 35.2 percent have between two to five years working experience with theirorganizations. Only 21 of the respondents had less than two years’ experience. Detaileddescriptive statistics of the sectors and respondents that responded to the survey have beenpresented in Table I.

3.2 MeasuresIn this study the measures used to evaluate the institutional pressures in the Ghanaianmanufacturing and mining sector were those recommended by DiMaggio and Powell (1983),Liang et al. (2007), Teo et al. (2003), Grewal and Dharwadkar (2002) and Scott (1995). Tomeasure coercive or regulative pressure, we considered issues such as requirements onenvironmental management by the EPA of Ghana and the Ministry of Lands and NaturalResources (MLNR), the requirements from industry associations on environment, and how

Profile Frequency % Cumulative %

SectorsValidExtractive 30 13.7 13.7Manufacturing 189 86.3 100.0

Total 219 100.0

CompaniesValidBreweries 19 8.7 8.7Chemicals 22 10.0 18.7Food processing 31 14.2 32.9Metals 6 2.7 35.6Mining 21 9.6 45.2Oil/gas 9 4.1 49.3Paper 12 5.5 54.8Pharmaceuticals 9 4.1 58.9Printing 14 6.4 65.3Refinery 1 0.5 65.8Rubber products 24 11.0 76.7Textiles 9 4.1 80.8Waste management 9 4.1 84.9Water processing 20 9.1 94.1Wood products 13 5.9 100.0

Total 219 100.0

PositionValidHealth, safety and environmental managers 63 28.8 28.8MD 59 26.9 55.7Production managers 79 36.1 91.8Others 18 8.2 100.0

Total 219 100.0

ExperienceValidAbove five years 121 55.3 55.3Less than two years 21 9.6 64.8Two to five years 77 35.2 100.0

Total 219 100.0

Table I.Descriptive statisticsof respondents

1098

IJPPM67,7

the competitive environment requires organizations to initiate environmental managementpractices in order to be competitive as recommended by DiMaggio and Powell (1983), Lianget al. (2007) and Teo et al. (2003). Specifically, regulative pressures were measured usingquestions like our company adopts environmental management practices for the reasonsthat: please indicate (1¼ strongly disagree; 5¼ strongly agree):

(1) the EPA of Ghana requires our firm to plan and implement environmentalmanagement practices (REG1);

(2) the industry associations in Ghana requires our firm to plan and implementenvironmental management practices (REG2);

(3) the MLNR requires our firm to plan and implement environmental managementpractices (REG3);

(4) the competitive conditions of our firm require our firm to plan and implementenvironmental management practices (REG4); and

(5) the international environmental regulation requires that our firm plan andimplement environmental management practices (REG5).

To measure the normative pressure, we considered issues like the extent of environmentalmanagement practices adopted by suppliers, customers and the extent to which governmentpromotion of environmental management practices influences the adoption of environmentalmanagement practices. This scale is largely consistent with the dimensions recommended byTeo et al. (2003) and Liang et al. (2007). Specifically, normative pressures were measured usingquestions like: our company adopts environmental management practices due to: pleaseindicate (1¼ strongly disagree; 5¼ strongly agree):

(1) the extent of environmental management practices adopted by suppliers (NORM1);

(2) the extent of environmental management practices adopted by customers (NORM2);

(3) the extent to which the government of Ghana promotes environmental managementpractices (NORM3); and

(4) the extent to which the global community promotes environmental managementpractices (NORM4).

Following Teo et al. (2003), the mimetic pressure construct was measured in terms of theperceived extent to which competitors have benefited from the implementation ofenvironmental management practices. This construct was measured by asking respondentsto assess themselves based on how they think competitors in the industry have benefitedfrom the adoption of environmental management practices. Respondents were also to assesshow their competitors are perceived as favorites in the same industry by suppliers andcustomers due to their adoption of environmental management practices (Liang et al., 2007;Teo et al., 2003). Specifically, mimetic pressures were measured using questions like: ourcompetitors who planned and implemented comprehensive environmental managementpractices; please indicate (1¼ strongly disagree; 5¼ strongly agree):

(1) have benefited (MIME1);

(2) are favorably perceived by others in the same industry (MIME2);

(3) are favorable perceived by their suppliers in the same industry (MIME3); and

(4) are favorably perceived by their customers in the same industry (MIME4).

Environmental management practices were measured according to Zhu et al. (2008). Thiswas with reference to senior- and middle-level managers’ commitment to environmental

1099

Environmentalmanagement

practices

management practices, cross-functional cooperation for environmental improvements,environmental compliance and auditing programs and ISO 14001 certification orenvironmental permit from the EPA Ghana. Specifically, environmental managementpractices were measured using questions like: indicate the extent to which your organizationhas implemented the following: please indicate (1¼ strongly disagree; 5¼ strongly agree):

(1) our senior managers are committed to environmental management (EMP1);

(2) our middle-level managers are committed to environmental management (EMP2);

(3) our organization has a cross-functional cooperation for environmentalimprovements (EMP3);

(4) our organization is committed to environmental compliance and auditingprograms (EMP4);

(5) our organization has ISO 14001 Certification (EMP5); and

(6) our organization has EPA Ghana Certification (EMP6).

3.3 Analytical techniquesThe relationships between the hypothesized model, namely, institutional pillars; regulative,normative, mimetic constructs and the environmental management practices wereexamined through the use of structural equation modeling (SEM). These were testedusing AMOS software version 23. In this study, we conducted an exploratory factor analysis(EFA) on the items using the SPSS software. The factor analysis indicated how distinct(discriminant validity) the constructs are and that each measures a single thing (convergentvalidity), and that they are reliable (reliability). This can all be achieved in the confirmatoryfactor analysis (CFA). Where the pre-validated instrument used is being applied to adifferent data set or within a different context or environment, EFA could be repeated beforeperforming the CFA (Gaskin, 2016). Thus, it was decided to conduct an EFA prior to thetesting of our structural model since the items were adapted and going to be used in adifferent environment (Osborne and Fitzpatrick, 2012; Gaskin, 2016). An EFA with themaximum likelihood extraction method and the Promax with Kaiser normalization wasused in the study. The rotation converged with five iterations. The objective of this was toextract the latent factors of the institutional theory and environmental managementpractices (Sadikoglu and Zehir, 2010; Gunday et al., 2011). All the items under the respectiveconstructs were reflective in nature and for that reason; they were all modeled as such.Apart from that AMOS application does not lend itself easily to formative constructs and forthat, the default model was used (Gaskin, 2016). A CFA was therefore performed on all theitems and constructs based on their reliabilities and validities by evaluating the Cronbach’sα coefficients, outer loadings, average variance extracted (AVE), and composite reliabilities(CR) (Sadikoglu and Zehir, 2010).

4. Results4.1 Exploratory factor analysisIn this study, we started with 4 constructs and 21 items. After five iterations, the results ofthe EFA analysis converged with same four constructs, however, 5 out of the 21 items weredeleted due to poor loadings. The final model, therefore, consisted of 4 constructs and 16items, three for institutional pillars and one for environmental management practices. Theextracted institutional theory constructs were labeled as regulatory, normative and mimeticpressures. Similarly, four items loaded to a coherent factor and was labeled environmentalmanagement practices accordingly. The pattern matrix for the EFA is presented in Table II.

1100

IJPPM67,7

Table II also presents the eigenvalues as well as the percentage variance of the factorsextracted and total variance explained.

The Kaiser–Meyer–Olkin (KMO) measure of the sampling adequacy was found to be0.883, which was greater than 0.5 indicating that the sample size is adequate for the givennumber of variables used for the factor analysis (Hutcheson and Sofroniou, 1999). Table IIIpresents the KMO and Bartlett’s test of sphericity values. Table IV presents the descriptivestatistics of the constructs used in the study.

4.1.1 Summary of EFA. The results of the EFA indicate: factor 1 as a regulative, factor 2as a normative, factor 3 as a mimetic and factor 4 as environmental management practices.

FactorItems 1 2 3 4

NORM1 0.835NORM2 0.911NORM3 0.875NORM4 0.866EMP2 0.877EMP3 0.958EMP4 0.732EMP5 0.704REG1 0.800REG3 0.942REG4 0.980REG5 0.810MIME1 0.921MIME2 0.801MIME3 0.893MIME4 0.779Eigenvalues 6.559 2.825 2.005 1.539% variance extracted 38.638 16.169 10.932 8.818Cumulative % 74.558Notes: Extraction method: maximum likelihood; rotation method: promax with Kaiser normalization;rotation converged in five iterations

Table II.EFA pattern matrix

Descriptive statistics n Minimum Maximum Mean SD

NORMATIVE 219 1 5 2.259 0.805ENVMGT 219 1 5 3.817 0.644REGULATIVE 219 1 5 4.000 0.644MIMETIC 219 1 5 3.530 0.807

Table IV.Descriptive statistics

of constructs

Kaiser–Meyer–Olkin measure of sampling adequacy 0.883

Bartlett’s test of sphericityApprox. χ2 4,936.850df 120Sig. 0.000

Table III.KMO and Bartlett’s

test of sphericity

1101

Environmentalmanagement

practices

4.2 Confirmatory factor analysisThe factor structure was tested and scales validated by conducting a CFA (Hair et al., 2010).The model consisted of 4 constructs with 16 indicator elements, see Figure 2. All theconstructs in the model consisted of four items each. Figure 2 presents the constructs andtheir items which were the basis for the CFA. Prior to the assessment of the structuralrelationships between the constructs, we assessed the quality and the fitness of themeasurement models as recommended when using CB–SEM. The study, therefore,examined the reliability of the items used, convergent and discriminant validity as well asthe general goodness of fit of the model. To conduct this quality and goodness of fitanalysis, we used the “Master Validity Tool,” an AMOS Plugin tool developed by Gaskinand Lim (2016a).

To establish convergent validity, we considered the outer loadings as well as the AVEfor items and constructs, respectively. All items had very high loadings on their respectiveconstructs, ranging between 0.7 and 0.9, indicating very high convergent validity, all above0.7 (Fornell and Larcker, 1981). Table IV, therefore, indicates that the AVE’s for allconstructs were ranging between 0.673 and 0.795, larger than the recommended thresholdvalue of 0.5 (Fornell and Larcker, 1981; Hu and Bentler, 1999). For discriminant validity,

e10.87

0.93

0.95

0.81

0.84

0.91

0.87

0.86

0.88

0.85

0.90

0.78

0.86

0.37

0.22

0.23 0.53

0.48

0.23

0.93

0.72

0.75

REG1

REG3REGULATIVE

NORMATIVE

MIMETIC

ENVMGT

REG4

REG5

NORM1

NORM2

NORM3

NORM4

MIME1

MIME2

MIME3

MIME4

EMP2

EMP3

EMP4

EMP5

e2

e4

e5

e6

e7

e8

e9

e10

e11

e12

e13

e14

e15

e16

0.37

e3

Figure 2.Constructs usedin the model anditems – confirmatoryfactor analysis

1102

IJPPM67,7

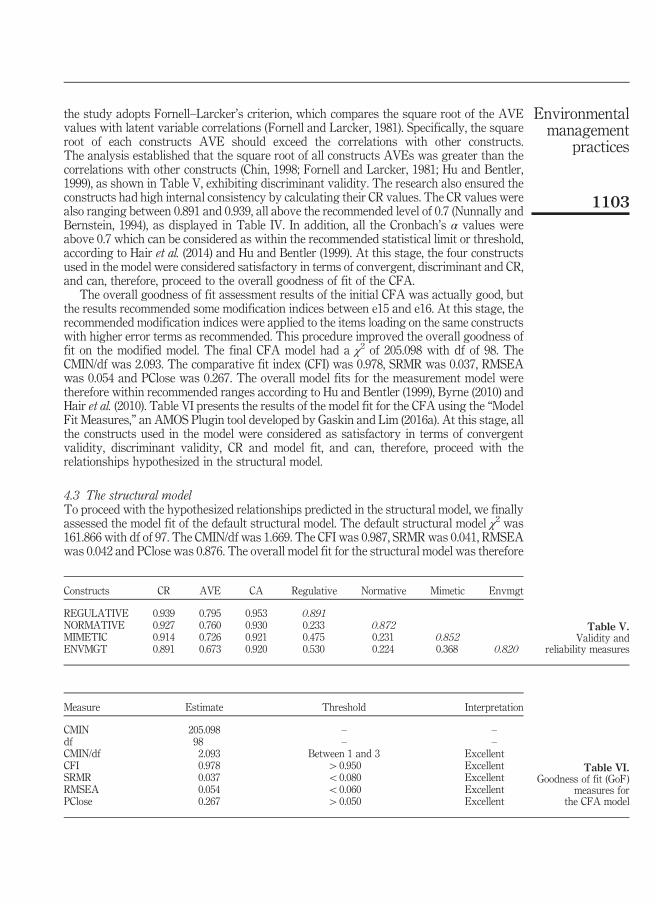

the study adopts Fornell–Larcker’s criterion, which compares the square root of the AVEvalues with latent variable correlations (Fornell and Larcker, 1981). Specifically, the squareroot of each constructs AVE should exceed the correlations with other constructs.The analysis established that the square root of all constructs AVEs was greater than thecorrelations with other constructs (Chin, 1998; Fornell and Larcker, 1981; Hu and Bentler,1999), as shown in Table V, exhibiting discriminant validity. The research also ensured theconstructs had high internal consistency by calculating their CR values. The CR values werealso ranging between 0.891 and 0.939, all above the recommended level of 0.7 (Nunnally andBernstein, 1994), as displayed in Table IV. In addition, all the Cronbach’s α values wereabove 0.7 which can be considered as within the recommended statistical limit or threshold,according to Hair et al. (2014) and Hu and Bentler (1999). At this stage, the four constructsused in the model were considered satisfactory in terms of convergent, discriminant and CR,and can, therefore, proceed to the overall goodness of fit of the CFA.

The overall goodness of fit assessment results of the initial CFA was actually good, butthe results recommended some modification indices between e15 and e16. At this stage, therecommended modification indices were applied to the items loading on the same constructswith higher error terms as recommended. This procedure improved the overall goodness offit on the modified model. The final CFA model had a χ2 of 205.098 with df of 98. TheCMIN/df was 2.093. The comparative fit index (CFI) was 0.978, SRMR was 0.037, RMSEAwas 0.054 and PClose was 0.267. The overall model fits for the measurement model weretherefore within recommended ranges according to Hu and Bentler (1999), Byrne (2010) andHair et al. (2010). Table VI presents the results of the model fit for the CFA using the “ModelFit Measures,” an AMOS Plugin tool developed by Gaskin and Lim (2016a). At this stage, allthe constructs used in the model were considered as satisfactory in terms of convergentvalidity, discriminant validity, CR and model fit, and can, therefore, proceed with therelationships hypothesized in the structural model.

4.3 The structural modelTo proceed with the hypothesized relationships predicted in the structural model, we finallyassessed the model fit of the default structural model. The default structural model χ2 was161.866 with df of 97. The CMIN/df was 1.669. The CFI was 0.987, SRMR was 0.041, RMSEAwas 0.042 and PClose was 0.876. The overall model fit for the structural model was therefore

Constructs CR AVE CA Regulative Normative Mimetic Envmgt

REGULATIVE 0.939 0.795 0.953 0.891NORMATIVE 0.927 0.760 0.930 0.233 0.872MIMETIC 0.914 0.726 0.921 0.475 0.231 0.852ENVMGT 0.891 0.673 0.920 0.530 0.224 0.368 0.820

Table V.Validity and

reliability measures

Measure Estimate Threshold Interpretation

CMIN 205.098 – –df 98 – –CMIN/df 2.093 Between 1 and 3 ExcellentCFI 0.978 W0.950 ExcellentSRMR 0.037 o0.080 ExcellentRMSEA 0.054 o0.060 ExcellentPClose 0.267 W0.050 Excellent

Table VI.Goodness of fit (GoF)

measures forthe CFA model

1103

Environmentalmanagement

practices

within the recommended ranges according to Hu and Bentler (1999), Byrne (2010), Hair et al.(2010). Table VII presents the results of the model fit for the default structural model usingthe “Model Fit Measures,” an AMOS Plugin tool developed by Gaskin and Lim (2016b).At this stage, we can confirm that the default model satisfies all the recommended qualitycriteria and now suitable to assess the relationships hypothesized in the structural model.The default model is presented in Figure 3.

4.4 The hypothesized relationshipsAfter meeting all the prescribed quality criteria for the measurement as well as the defaultmodels the last step in the CB–SEM is to analyze the structural model. These results arepresented in Table VIII. The table presents the effect of the three exogenous constructs, theinstitutional pillars on the single endogenous construct, environmental managementpractices. This estimate represents the β value (coefficient value associated withenvironmental management practices). This value assesses the relationship between a givenexogenous variable and it respective endogenous variables holding all other exogenous

e1

0.75

0.86 0.87

0.93

0.95

0.810.66

0.70

0.83 0.84

0.910.76

0.87

0.750.86

0.77

0.88

0.14

0.09

0.48

0.310.75

0.72

0.93

0.860.75

0.86

0.52

0.570.23

0.44

0.23

0.72

0.800.90

0.780.60

0.85

0.90

REG1

REGULATIVE

NORMATIVE

MIMETIC

ENVMGT

EMP5

EMP4

EMP3

EMP2

e17

e16

e15

e14

e13

REG3

REG4

REG5

NORM1

NORM2

NORM3

NORM4

MIME1

MIME2

MIME3

MIME4

e2

e3

e4

e5

e6

e7

e8

e9

e10

e11

e12

Figure 3.The default modelshowing theconstructs and theirhypothesizedrelationships

Measure Estimate Threshold Interpretation

CMIN 161.866 – –df 97 – –CMIN/df 1.669 Between 1 and 3 ExcellentCFI 0.987 W0.950 ExcellentSRMR 0.041 o0.080 ExcellentRMSEA 0.042 o0.060 ExcellentPClose 0.876 W0.050 Excellent

Table VII.Goodness of fitmeasures (Gof )for the default model

1104

IJPPM67,7

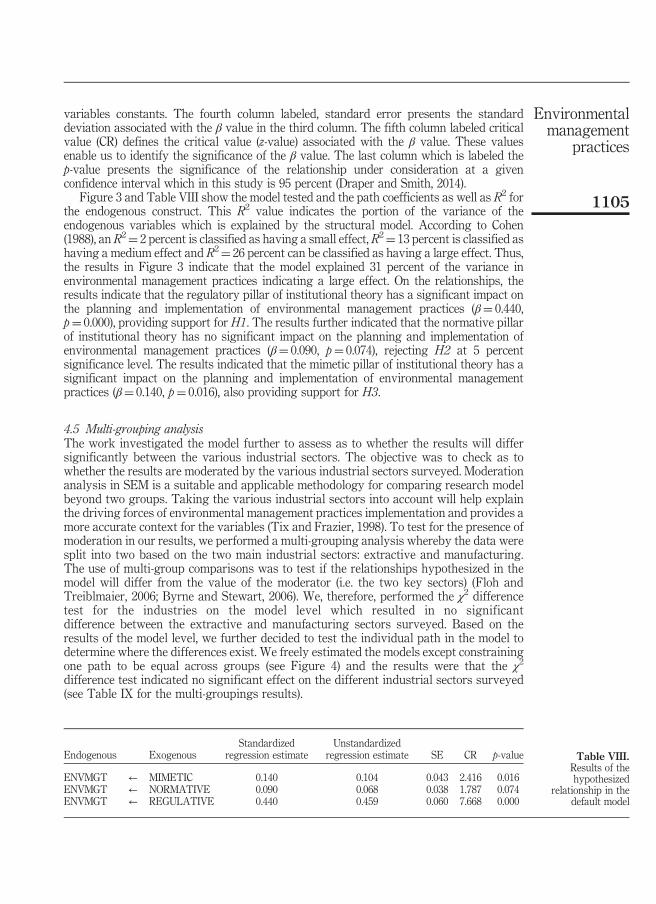

variables constants. The fourth column labeled, standard error presents the standarddeviation associated with the β value in the third column. The fifth column labeled criticalvalue (CR) defines the critical value (z-value) associated with the β value. These valuesenable us to identify the significance of the β value. The last column which is labeled thep-value presents the significance of the relationship under consideration at a givenconfidence interval which in this study is 95 percent (Draper and Smith, 2014).

Figure 3 and Table VIII show the model tested and the path coefficients as well as R2 forthe endogenous construct. This R2 value indicates the portion of the variance of theendogenous variables which is explained by the structural model. According to Cohen(1988), an R2¼ 2 percent is classified as having a small effect, R2¼ 13 percent is classified ashaving a medium effect and R2¼ 26 percent can be classified as having a large effect. Thus,the results in Figure 3 indicate that the model explained 31 percent of the variance inenvironmental management practices indicating a large effect. On the relationships, theresults indicate that the regulatory pillar of institutional theory has a significant impact onthe planning and implementation of environmental management practices (β¼ 0.440,p¼ 0.000), providing support for H1. The results further indicated that the normative pillarof institutional theory has no significant impact on the planning and implementation ofenvironmental management practices (β¼ 0.090, p¼ 0.074), rejecting H2 at 5 percentsignificance level. The results indicated that the mimetic pillar of institutional theory has asignificant impact on the planning and implementation of environmental managementpractices (β¼ 0.140, p¼ 0.016), also providing support for H3.

4.5 Multi-grouping analysisThe work investigated the model further to assess as to whether the results will differsignificantly between the various industrial sectors. The objective was to check as towhether the results are moderated by the various industrial sectors surveyed. Moderationanalysis in SEM is a suitable and applicable methodology for comparing research modelbeyond two groups. Taking the various industrial sectors into account will help explainthe driving forces of environmental management practices implementation and provides amore accurate context for the variables (Tix and Frazier, 1998). To test for the presence ofmoderation in our results, we performed a multi-grouping analysis whereby the data weresplit into two based on the two main industrial sectors: extractive and manufacturing.The use of multi-group comparisons was to test if the relationships hypothesized in themodel will differ from the value of the moderator (i.e. the two key sectors) (Floh andTreiblmaier, 2006; Byrne and Stewart, 2006). We, therefore, performed the χ2 differencetest for the industries on the model level which resulted in no significantdifference between the extractive and manufacturing sectors surveyed. Based on theresults of the model level, we further decided to test the individual path in the model todetermine where the differences exist. We freely estimated the models except constrainingone path to be equal across groups (see Figure 4) and the results were that the χ2

difference test indicated no significant effect on the different industrial sectors surveyed(see Table IX for the multi-groupings results).

Endogenous ExogenousStandardized

regression estimateUnstandardized

regression estimate SE CR p-value

ENVMGT ← MIMETIC 0.140 0.104 0.043 2.416 0.016ENVMGT ← NORMATIVE 0.090 0.068 0.038 1.787 0.074ENVMGT ← REGULATIVE 0.440 0.459 0.060 7.668 0.000

Table VIII.Results of thehypothesized

relationship in thedefault model

1105

Environmentalmanagement

practices

5. Discussion and conclusionsIn this study, we have provided some empirical evidence on the driving forces ofenvironmental management practices into organizations using institutional theory. Theresults from our study highlight relationship between the three institutional pillars, i.e.,regulative, normative and mimetic the planning and implementation of environmentalmanagement practices in Ghanaian firms. The findings indicate that firms in Ghanaincorporate environmental management practices into their operations due to forces exertedfrom the regulatory bodies as well as benchmark the initiatives of other organizations in thesame industry which have successfully planned and implemented environmentalmanagement practices into their operations. These findings corroborate those of Delmas(2002), Tate et al. (2011), Williamson et al. (2006), To and Tang (2014) and Heras-Saizarbitoriaet al. (2011). In a survey by Delmas (2001) among European and US firms, a substantialnumber of managers indicated they adopt measures such as ISO 14001 environmentalmanagement systems in their operations in the quest to satisfy regulatory compliance.Heras-Saizarbitoria et al. (2011) also conducted an extensive literature review concerning the

e11

1

1

1

1

1

1

1

1

1

1

1

1

11

1

1

1

1

1

1

v1_2

a1_2

a2_2

a3_2

a4_2

a5_2

a6_2

a7_2

a9_2

vvv3_2

ccc3_2

b2_2

b1_2

ccc2_2

vvv2_2

ccc1_2

b3_2

vvv1_2

vv1_2

a12_2

a11_2

v13_2

v14_2

v15_2a_2

v16_2

a10_2

a8_2

v2_2

v3_2

v4_2

v5_2

v6_2

v7_2

v8_2

v9_2

v10_2

v11_2

v12_2

e2

e3

e4

e5

e6

e7

e8

e9

e10

e11

e12

e14

e13

e15

e16

e17

REG1

REG3

REG4

REG5

NORM1

NORM2

NORM3

NORM4

MIME1

MIME2

MIME3

MIME4

REGULATIVE

NORMATIVE

MIMETIC

ENVMGT

EMP5

EMP4

EMP3

EMP2

Figure 4.Default multi-groupings model

Path df CMIN p-values

Unconstrained model 15 9.011 0.877Regulative – Envt Mgt Pract 1 1.034 0.309Normative – Envt Mgt Pract 1 0.094 0.759Mimetic – Envt Mgt Pract 1 2.556 0.110

Table IX.Multi-groupingsresults

1106

IJPPM67,7

motivations for and benefits of implementing ISO 14001 environmental managementsystems and surveyed 214 Spanish companies. They found that the most highly ratedbenefit was compliance with environmental laws and regulations, followed byenvironmental effectiveness improvement, less environmental problems and improvingcustomer satisfaction. Williamson et al. (2006) used empirical research into theenvironmental practices of 31 manufacturing SMEs and found that “businessperformance” and “regulation” considerations drive the environmental behavior of theenterprises. Also, in a study to understand the transaction cost and institutional drivers ofsupplier adoption of environmental practices in the USA, Tate et al. (2011) found thatinstitutional theory analysis reveals that supplier adoption of environmental practices ismore likely if coercive, normative and mimetic institutional forces are in play.

In addition to coercive pressures, the results also indicated that organizations in Ghanaalso mimic practices that successful leading firms have adopted in terms of environmentalmanagement practices. This finding is consistent with that of Anderson et al. (1999),Henriques and Sadorsky (1996) and Khanna and Anton (2002). Our results also confirmthose of DiMaggio and Powell (1983) and Jennings and Zandbergen (1995). DiMaggio andPowell (1983) posit that a mimetic process occurs when an organization models itself onother organizations in an uncertain environment. Organizations tend to model themselvesafter other organizations they believe are well managed and able to survive in a competitiveenvironment. According to Jennings and Zandbergen (1995), firms sometimes implementprograms (e.g. environmentally friendly programs, green products and environmentalmarketing programs) without studying the impacts, but rather due to competitive pressure.

The results, however, contradict with the findings of Kollman and Prakash (2002) whoexamined why the UK, Germany and US companies adopt an EMS. They found in the USAthat the decision of whether to pursue certification and which standard to certify against(ISO 14001 or the European Union’s Eco-Audit and Management Scheme) was stronglyinfluenced by stakeholder pressures from industry associations in addition to regionalchambers of commerce, suppliers and regulators.

Our results indicate consistency across the various industrial, i.e., manufacturing and theextractive sectors surveyed based on the multi-grouping analysis. This is might be due tothe fact that both the manufacturing and the extractive sectors are highly regulated by theEPA Ghana based on Act, 203, 1994 and the L.I 1652, 1999. Over the years, the Ghanaianbusiness environment has been regulated by the Environmental Protection Council (EPC).The main objective then was to advise the government on environmental issues. However,since 2004, the EPC was converted to the EPA, operating as a public agency that can sueand be sued, thereby strengthening environmental regulations in the country.

6. Implications, limitations and future researchThe results indicate that organizations implement environmental management practices asa result of coercive and mimetic pressures. The implication is that it is important forregulatory bodies such as the EPA Ghana to actually develop effective and efficientenvironmental policies that are implemented and monitored in order to achieve improvedenvironmental performance. This is because the finding has indicated that one of the maindriving forces of environmental management practices implementation is the regulatorypillar. It is important therefore for the EPA Ghana to plan and guide the effectiveimplementation of policies as well as monitoring on all sectors including manufacturing andthe extractive sectors. Another implication from the findings of this work is the need forregulatory bodies to continually monitor polluting firms to make sure they are planning andimplementing policies related to the environment since the effective implementation of thesepolicies will motivate other firms to mimic the actions of the implementing firms. The resultsalso indicate the importance of educating industrial associations on the importance of

1107

Environmentalmanagement

practices

integrating environmental issues into manufacturing and service delivery to enable them toplay an active role in achieving sustainable development.

One limitation of this work is the use of data only from Ghana. It is important for otherresearchers to assess these relationships using data from other geographical areas. In anattempt to operationalize the environmental management practices construct, the researchdeveloped and used only one construct based on previously validated items. The inclusionof other constructs could be interesting for future research. This could provide valuableknowledge about the link between these institutional pillars and other categories ofenvironmental management practices to obtain a more in-depth view of the relationship.Future studies can also consider the relationship between the three institutional pillars andcorporate social responsibility initiatives.

References

Anderson, S.W., Daly, J.D. and Johnson, M.F. (1999), “Why firms see IS 9000 certification: regulatorycompliance or competitive advantage”, Production and Operations Management, Vol. 8 No. 1,pp. 28-43.

Aryee, B.N.A., Ntibery, B.K. and Atorkui, E. (2003), “Trends in the small-scale mining of preciousminerals in Ghana: a perspective on its environmental impact”, Journal of Cleaner Production,Vol. 11 No. 2, pp. 131-140.

Balasubramanian, S. and Shukla, V. (2017), “Green supply chain management: an empiricalinvestigation on the construction sector”, Supply Chain Management: An International Journal,Vol. 22 No. 1, pp. 58-81.

Bansal, P. and Clelland, I. (2004), “Talking trash: legitimacy, impression management, andunsystematic risk in the context of the natural environment”, Academy of Management Journal,Vol. 47 No. 1, pp. 93-103.

Björklund, M. and Forslund, H. (2013), “The purpose and focus of environmental performancemeasurement systems in logistics”, International Journal of Productivity and PerformanceManagement, Vol. 62 No. 3, pp. 230-249.

Byrne, B.M. (2010), Structural Equation Modeling with AMOS: Basic Concepts, Applications, andProgramming, 2nd ed., Routledge, New York, NY.

Byrne, B.M. and Stewart, S.M. (2006), “Teacher’s corner: the MACS approach to testing for multigroupinvariance of a second-order structure: a walk through the process”, Structural EquationModeling, Vol. 13 No. 2, pp. 287-321.

Carraro, C., Katsoulacos, Y. and Xepapadeas, A. (Eds) (1996), Environmental Policy and MarketStructure, Kluwer, Boston, MA.

Carroll, G.R. and Delacroix, J. (1982), “Organizational mortality in the newspaper industries ofArgentina and Ireland: an ecological approach”, Administrative Science Quarterly, Vol. 27 No. 2,pp. 169-198.

Chen, A.J., Watson, R.T., Boudreau, M. and Karahanna, E. (2011), “An institutional perspectiveon the adoption of green IS & IT”, Australasian Journal of Information Systems, Vol. 17 No. 1,pp. 5-27.

Cheng, H.-L. and Yu, C.-M.J. (2008), “Institutional pressures and initiation of internationalization:evidence from Taiwanese small and medium-sized enterprises”, International Business Review,Vol. 17 No. 3, pp. 331-348.

Chin, W.W. (1998), “Commentary: issues and opinion on structural equation modeling”,MIS Quarterly,Vol. 22 No. 1, pp. vii-xvi.

Christmann, P. (2000), “Effects of “best practices” of environmental management on cost advantage:the role of complementary assets”, Academy of Management Journal, Vol. 43 No. 4,pp. 663-680.

1108

IJPPM67,7

Chu, S.H., Yang, H., Lee, M. and Park, S. (2017), “The impact of institutional pressures on green supplychain management and firm performance: top management roles and social capital”,Sustainability, Vol. 9 No. 5, pp. 764-785.

Clemens, B. and Douglas, T.J. (2006), “Does coercion drive firms to adopt ‘voluntary’ green initiatives.Relationships among coercion, superior firm resources, and voluntary green initiatives”, Journalof Business Research, Vol. 59 No. 4, pp. 483-491.

Cohen, J. (1988), Statistical Power Analysis for the Behavioral Sciences, 2nd ed., Academic Press,New York, NY.

Cordano, M. (1993), “Making the natural connection: justifying investment in environmentalinnovation”, Proceedings of the International Association for Business and Society, pp. 530-537.

Dean, T.J. and Brown, R.L. (1995), “Pollution regulation as a barrier to new firm entry: initialevidence and implications for future research”, Academy of Management Journal, Vol. 38 No. 1,pp. 288-303.

Delmas, M. (2001), “Stakeholders and competitive advantage: the case of ISO 14001”, Production andOperations Management, Vol. 10 No. 3, pp. 343-358.

Delmas, M. (2002), “The diffusion of environmental management standards in Europe and the UnitedStates: an institutional perspective”, Policy Sciences, Vol. 35 No. 1, pp. 91-119.

Delmas, M. (2003), “In search of ISO: an institutional perspective on the adoption of internationalmanagement standards”, Working Paper No. 1784, Stanford Graduate School of Business,Stanford, CA.

Delmas, M. and Toffel, M.W. (2004), “Stakeholders and environmental management practices: aninstitutional framework”, Business Strategy and the Environment, Vol. 13 No. 4, pp. 209-222.

DiMaggio, P.J. and Powell, W.W. (1983), “The iron cage revisited: Institutional isomorphism andcollective rationality in organizational fields”, American Sociological Review, Vol. 48 No. 2,pp. 147-160.

Dodds, R., Graci, S., Ko, S. and Walker, L. (2013), “What drives environmental sustainability in theNew Zealand wine industry?: an examination of driving factors and practices”, InternationalJournal of Wine Business Research, Vol. 25 No. 3, pp. 164-184.

Draper, N.R. and Smith, H. (2014), Applied Regression Analysis, Vol. 326, John Wiley & Sons,New York, NY.

EPA Ghana (1999), available at: http://extwprlegs1.fao.org/docs/pdf/gha78169.pdf (accessedFebruary 11, 2017).

Ferguson, N. and Browne, J. (2001), “Issues in end-of-life product recovery and reverse logistics”,Production Planning & Control, Vol. 12 No. 5, pp. 534-547.

Floh, A. and Treiblmaier, H. (2006), “What keeps the e-banking customer loyal? A multigroup analysisof the moderating role of consumer characteristics on e-loyalty in the financial service industry”,Journal of Electronic Commerce Research, Vol. 7 No. 2, pp. 97-110.

Fornell, C. and Larcker, D.F. (1981), “Evaluating structural equation models with unobservablevariables and measurement error”, Journal of Marketing Research, Vol. 18 No. 1, pp. 39-50.

Gaskin, J. (2016), “Exploratory factor analysis”, Gaskination’s StatWiki, available at: http://statwiki.kolobkreations.com (accessed January 10, 2017).

Gaskin, J. and Lim, J. (2016a), “Master validity tool”, AMOS Plugin, Gaskination’s StatWiki.

Gaskin, J. and Lim, J. (2016b), “Model fit measures”, AMOS Plugin, Gaskination’s StatWiki.

Gavronski, J., Ferrer, G. and Paiva, E.L. (2008), “ISO 14001 certification in Brazil: motivations andbenefits”, Journal of Cleaner Production, Vol. 16 No. 1, pp. 87-94.

Grewal, R. and Dharwadkar, R. (2002), “The role of the institutional environment in marketingchannels”, Journal of Marketing, Vol. 66 No. 3, pp. 82-97.

Gunday, G., Ulusoy, G., Kilic, K. and Alpkan, L. (2011), “Effects of innovation types on firmperformance”, International Journal of Production Economics, Vol. 133 No. 2, pp. 662-676.

1109

Environmentalmanagement

practices

Hair, J.F., Black, W.C., Babin, B.J. and Anderson, R.E. (2010), Multivariate Data Analysis, 7th ed.,Prentice Hall, NJ.

Hair, J.F., Hult, G.T.M., Ringle, C.M. and Sarstedt, M. (2014), A Primer on Partial Least SquaresStructural Equation Modeling (PLS-SEM), Sage, Thousand Oaks, CA.

Hatch, M.J. (1997), Organizational Theory: Modern, Symbolic, and Postmodern Perspectives,Oxford University Press, New York, NY.

Heide, J.B. and John, G. (1992), “Do norms matter in marketing relationships?”, Journal of Marketing,Vol. 56 No. 2, pp. 32-44.

Henriques, I. and Sadorsky, P. (1996), “The determinants of an environmentally responsive firm: anempirical approach”, Journal of Environmental Economics and Management, Vol. 30 No. 3,pp. 381-395.

Heras-Saizarbitoria, I., Landin, G.A. and Molina-Azorin, J.F. (2011), “Do drivers matter for the benefitsof ISO 14001?”, International Journal of Operations & Production Management, Vol. 31 No. 2,pp. 192-215.

Hoffman, A.J. (1997), From Heresy to Dogma: An Institutional History of Corporate Environmentalism,New Lexington Press, San Francisco, CA.

Hoffman, M.L. (1977), “Moral internalization: current theory and research”, Advances in ExperimentalSocial Psychology, Vol. 10, Academic Press, pp. 85-133.

Hu, A.H. and Hsu, C.W. (2010), “Critical factors for implementing green supply chain practice: anempirical study of electrical and electronic industries in Taiwan”,Management Research Review,Vol. 33 No. 6, pp. 586-608.

Hu, L. and Bentler, P.M. (1999), “Cutoff criteria for fit indexes in covariance structure analysis:conventional criteria versus new alternatives”, Structural Equation Modeling, Vol. 6 No. 1,pp. 1-55.

Hutcheson, G. and Sofroniou, N. (1999), The Multivariate Social Scientist, Sage Publications, London.

Jennings, P.D. and Zandbergen, P.A. (1995), “Ecologically sustainable organizations: an institutionalapproach”, Academy of Management Review, Vol. 20 No. 4, pp. 1015-1052.

Khanna, M. and Anton, W.Q. (2002), “Corporate environmental management: regulatory and market-based pressures”, Land Economics, Vol. 78 No. 4, pp. 539-558.

King, A.A. and Lenox, M.J. (2001), “Does it really pay to be green? An empirical study of firmenvironmental and financial performance”, Journal of Industrial Ecology, Vol. 5 No. 1, pp. 105-116.

Kollman, K. and Prakash, A. (2002), “EMS-based environmental regimes as club goods: examiningvariations in firm level adoption of ISO 14001 and EMAS in UK, US, and Germany”, PolicySciences, Vol. 35 No. 1, pp. 43-67.

Lampe, M., Ellis, S.R. and Drummond, C.K. (1991), “What companies are doing to meet environmentalprotection responsibilities: balancing legal, ethical, and profit concerns”, Proceedings of theInternational Association for Business and Society, Vol. 2, pp. 1053-1073.

Larson, A. (1991), “Partner networks: leveraging external ties to improve entrepreneurial performance”,Journal of Business Venturing, Vol. 6 No. 3, pp. 173-189.

Lawrence, A.T. and Morell, D. (1995), “Leading-edge environmental management: motivation,opportunity, resources, and processes”, in Collins, D. and Starik, M. (Eds), Special ResearchVolume of Research in Corporate Social Performance and Policy, Sustaining the NaturalEnvironment: Empirical Studies on the Interface Between Nature and Organizations, JAI Press,Greenwich, CT, pp. 99-126.

Liang, H., Saraf, N., Hu, Q. and Xue, Y. (2007), “Assimilation of enterprise systems: the effect ofinstitutional pressures and the mediating role of top management”,MIS Quarterly, Vol. 31 No. 1,pp. 59-87.

Majumdar, S.K. and Marcus, A.A. (2001), “Rules versus discretion the productivity consequences offlexible regulation”, Academy of Management Journal, Vol. 44 No. 1, pp. 170-179.

1110

IJPPM67,7

Mensah, I. (2014), “Stakeholder pressure and hotel environmental performance in Accra, Ghana”,Management of Environmental Quality: An International Journal, Vol. 25 No. 2, pp. 227-243.

Meyer, J.W. and Rowan, B. (1977), “Institutionalized organizations: formal structure as myth andceremony”, American Journal of Sociology, Vol. 83 No. 2, pp. 340-363.

Miles, M.P. and Arnold, D.R. (1991), “The relationship between marketing orientation andentrepreneurial orientation”, Entrepreneurship Theory and Practice, Vol. 15 No. 4, pp. 49-65.