rdi indaba 2015 investor session final

TRANSCRIPT

1February 2015 |

INVESTOR PRESENTATION11 FEBRUARY 2015

2February 2015 |

FORWARD LOOKING STATEMENTS

No regulatory authority has approved or disapproved the information contained in this presentation.

Forward Looking Statements

Except for statements of historical fact, this presentation contains certain "forward-looking information" within the meaning of applicable securities law. Forward-looking

information is frequently characterized by words such as "plan", "expect", "project", "intend", "believe", "anticipate", “potential”, “should”, “likely”, forecast”, "estimate" and

other similar words, or statements that certain events or conditions "may" or "will" occur. Although the Company believes the expectations expressed in such forward-

looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ

materially from those in the forward-looking statements.

Factors that could cause actual results to differ materially from those in forward-looking statements include uncertainties and costs related to the proposed acquisition of

certain properties and assets from Bondeo 140 CC and its associates (“the Transaction”) and the ability of each party to satisfy the numerous conditions precedent in a

timely manner or at all, including, without limitation, completion on a timely basis of financings on satisfactory terms, receipt of shareholder approval, if required, receipt of

all regulatory approvals, including the acceptance of the Section 11 applications and exchange and securities regulatory authority approvals; exploration and development

activities, such as those related to determining whether mineral resources exist on a property; uncertainties related to expected production rates, timing of production and

cash and total costs of production and milling; uncertainties related to the ability to obtain necessary licenses, permits, electricity, surface rights and title for development

projects; operating and technical difficulties in connection with mining development activities; uncertainties related to the accuracy of our mineral resource estimates and

our estimates of future production and future cash and total costs of production and diminishing quantities or grades if mineral resources; uncertainties related to

unexpected judicial or regulatory procedures or changes in, and the effects of, the laws, regulations and government policies affecting our mining operations; changes in

general economic conditions, the financial markets and the demand and market price for mineral commodities such as diesel fuel, steel, concrete, electricity, and other

forms of energy, mining equipment, and fluctuations in exchange rates, particularly with respect to the value of the US dollar, Canadian dollar and South African Rand;

changes in accounting policies and methods that we use to report our financial condition, including uncertainties associated with critical accounting assumptions and

estimates; environmental issues and liabilities associated with mining and processing; geopolitical uncertainty and political and economic instability in countries in which

we operate; and labour strikes, work stoppages, or other interruptions to, or difficulties in, the employment of labour in markets in which we operate our mines, or

environmental hazards, industrial accidents or other events or occurrences, including third party interference that interrupt operation of our mines or development projects.

For further information on Rockwell, Investors should review Rockwell's home jurisdiction filings that are available at www.sedar.com.

3February 2015 |

AGENDA

• WELCOME AND REVIEW OF CORPORATE STRATEGY

• Dr Mark Bristow, Chairman

• CORPORATE REVIEW AND GROWTH PLANS

• James Campbell, CEO

• ROCKWELL’S RESOURCE CENTERED APPROACH TO MINING

• Mulalo Ndwammbi, Senior Production Manager

• REVIEW OF ACQUISITION: DEAL STRUCTURE AND TIMELINES

• John Shelton, CFO

4February 2015 |

REVIEW OF CORPORATE

STRATEGY

DR MARK BRISTOW, CHAIRMAN

5February 2015 |

DIAMOND MINES IN SOUTHERN AFRICA:DIAMOND DISTRIBUTION

MOR alluvial diamond fields:

Large, high value diamonds

Rockwell’s proven track record in the region

MOR alluvial diamond fields:

Large, high value diamonds

Rockwell’s proven track record in the region

6February 2015 |

HIGHLY SEGMENTED VALUATIONS: SMALL CAP CONSOLIDATION OPPORTUNITIES

1

10

100

1,000

10,000

1 10 100 1,000 10,000

Market Value (US$m

) (Log Scale)

Annual Revenue (US$m) (Log Scale)

De BeersAlrosa

Dominium

Rio Tinto (Argyle)

Lucara

Firestone GEM

Petra

Trans Hex

Rockwell

Reinet

Diamcor

Seniors

Mid-tier

Juniors

7February 2015 |

CORPORATE TURNAROUND: STRATEGIC HIGHLIGHTS

2010Strategic review

initiated

2006Rockwell listed on

TSX / JSE

2011New CEO + Private

placement + Diamond Value Management

strategy

2012Internally funded Bulk X-ray plant commissioned at

SHC +Klipdam soldcommissioning

2013New internally

funded Niewejaarskraal plant

commissioning

2015Acquisition of

Bondeo announced

2014New BEE partnership

announced + EMVrenewal plan implemented

8February 2015 |

OUR STRATEGIC DIRECTION

Leverage th benefits of the corporate turnaround

Continue building relationships with all stakeholders: Shareholders, employees and government

Focused on consolidation opportunities against strategic acquisition criteria

Completed agreement to acquire Bondeo

Effectively doubles Rockwell’s business

Quality, high margin early stage assets and fit-for-purpose processing plants

Bondeo leverages Rockwell’s growth potential

Can immediately exceed all-important target of 500k m3 pm of processed quality gravels

Increased optionality in the MOR

Reallocation of available financial, human and intellectual capital to achieve positive returns

“Diamonds for Tomorrow”

Granted extensive package of prospective ground in the MOR: >50,000 ha

9February 2015 |

CORPORATE REVIEWJAMES CAMPBELL, CEO

10February 2015 |

WHAT ROCKWELL DOES BEST: PRODUCE HIGH VALUE GEM QUALITY DIAMONDS

145cts: Old Saxendrift Tailings (Oct. ‘12)

70cts: Saxendrift Ext.(Aug. ‘12) 287cts: Saxendrift Ext. (Nov. ‘13)

49.3cts; 135.8cts; 54.0cts: SHC / Saxendrift

(Dec. ‘14)

116cts: Saxendrift Ext. (Aug. ‘13)

138cts; 169cts; 126cts: SHC/ Saxendrift

Extension (Sep. ‘13)

11February 2015 |

AGENDA

OUR EXCITING FUTURE:

THE SEVEN REASONS

1. PEOPLE

2. PRODUCT

3. PROPERTIES

4. PRODUCTION

5. PARTNERSHIPS

6. POTENTIAL

7. PROSPECTS

CONCLUSION

Recent recoveries at Saxendrift 56 carats (upper) and

103 carats (lower)

Five +115 carat rough diamonds

recovered by Rockwell: Middle

Orange, Aug. – Nov. 2013

12February 2015 |

EXPERIENCED LEADERSHIP

James Campbell,

CEO

John Shelton,

CFO

Richard Mhlontlo,

Group HR & IR

Glenn Norton,

Group Technical

Jeffrey Brenner,

Group Sales & Marketing

Stéphanie Leclercq,

IR & Corporate Development

Frans Bezuidenhout,

GM: MOR

Wikus De Winnaar,

Mine Manager: NJK

Petronella Mohale,

Mine Geologist

George Stevens,

Mine Manager: Saxendrift

Mahlodi Malowa,

Mine Geologist

Mulalo Ndwammbi,

Mine Manager: SHC

Penelope Mohale,

Mine Geologist

Ben Nell,

Tirisano Contracts Manager

Kurt Petersen,

Consulting Metallurgist

Board of Directors:

Dr Mark Bristow

(Chairman)

Stephen Dietrich

Willem Jacobs

Richard Linnell

Richard Menell

Johan van’t Hof

Board of Directors:

Dr Mark Bristow

(Chairman)

Stephen Dietrich

Willem Jacobs

Richard Linnell

Richard Menell

Johan van’t Hof

13February 2015 |

SUPERB PRODUCT: THE ALANA ~ AN EXCEPTIONAL GEM QUALITY DIAMOND RECOVERED AT SHC

Exploration pitting at

SHC: A method used to

evaluate the quality of

gravel to be mined

Exploration pitting at

SHC: A method used to

evaluate the quality of

gravel to be mined

James Campbell (CEO) and

Wikus de Winnaar (GM: MOR

Operations) at a trench such

as the one where the Alana

was eventually found

James Campbell (CEO) and

Wikus de Winnaar (GM: MOR

Operations) at a trench such

as the one where the Alana

was eventually found

SOLD – MARCH 2014!!

The 109 carat Alana stone:

Fancy yellow, no visual

flaws and octahedral shape

SOLD – MARCH 2014!!

The 109 carat Alana stone:

Fancy yellow, no visual

flaws and octahedral shape

At the cutting factory the stone was analyzed in 3D to identify the best cuts and value for recovery from the stone

At the cutting factory the stone was analyzed in 3D to identify the best cuts and value for recovery from the stone

The SHC processing plant: Gravel is screened and prepped before processing through the Bulk X-ray sorters

The SHC processing plant: Gravel is screened and prepped before processing through the Bulk X-ray sorters

Liberating the gravelsLiberating the gravels

Mining the gravels

Large boulders act as trap sitesLarge boulders act as trap sites

Loading and hauling the gravelLoading and hauling the gravel

The people on the team

Penelope Mohale (Mining Geologist) and MulaloNdwammbi (Mining Manager: SHC): Responsible for geology and mining when the Alana was recovered.

Penelope Mohale (Mining Geologist) and MulaloNdwammbi (Mining Manager: SHC): Responsible for geology and mining when the Alana was recovered.

Location of the AlanaLocation of the Alana

Locating the right mining area

Large stone plots : Used to determine the possible location of large stones

Large stone plots : Used to determine the possible location of large stones

Mining the gravels Geological daily report: Description of the gravel containing the AlanaGeological daily report: Description of the gravel containing the Alana

Mulaloexamines the pit the day before the discovery

Mulaloexamines the pit the day before the discovery

The Alana: 169 carats (13 September

2013)

The Alana: 169 carats (13 September

2013)

Looking for the Alana

Finding the Alana (August

2013)

Recovering the Alana

(September 2013)

Polishing the Alana

Selling the Alana (March

2014)

14February 2015 |

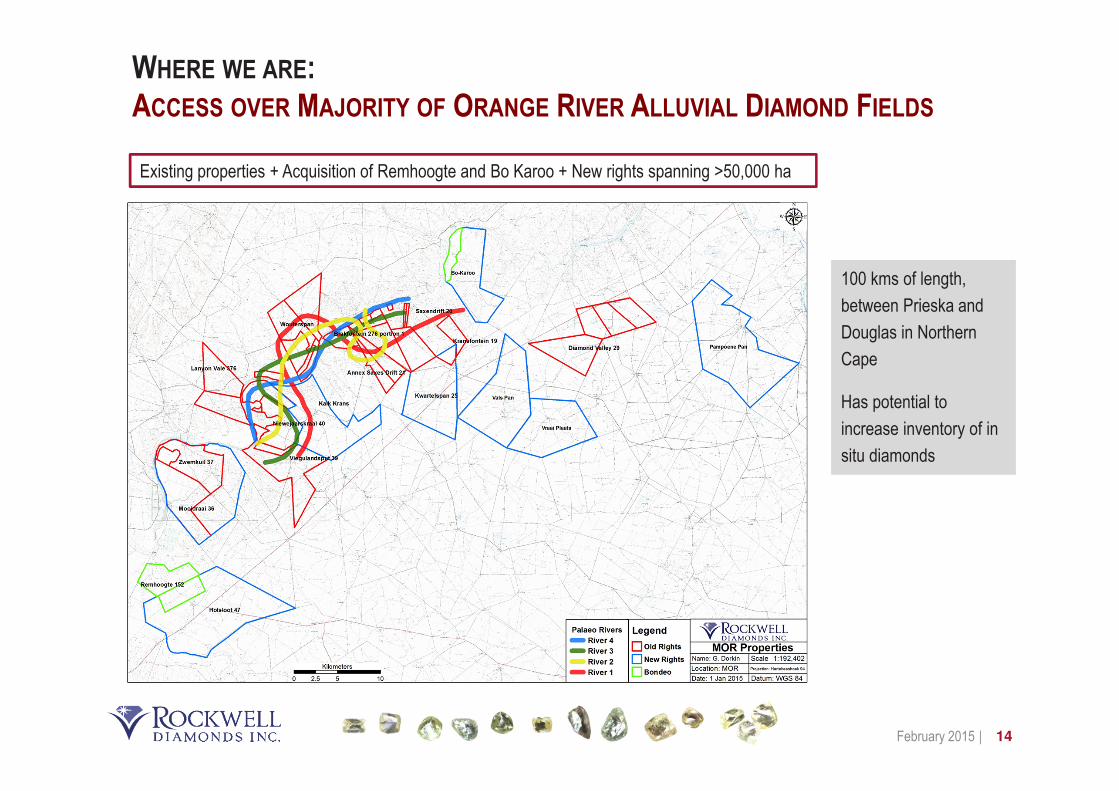

WHERE WE ARE:ACCESS OVER MAJORITY OF ORANGE RIVER ALLUVIAL DIAMOND FIELDS

Existing properties + Acquisition of Remhoogte and Bo Karoo + New rights spanning >50,000 ha

100 kms of length,

between Prieska and

Douglas in Northern

Cape

Has potential to

increase inventory of in

situ diamonds

100 kms of length,

between Prieska and

Douglas in Northern

Cape

Has potential to

increase inventory of in

situ diamonds

15February 2015 |

PLAN SHOWING THE GEOLOGY OF THE MIDDLE ORANGE PROJECTS

Independence you can trust

FIG

UR

E 1

2

Source: Trans Hex Group

LEGEND:

This diagram and the information therein are copyrighted. It may not be reproduced

or transmitted in any form or by any means without prior written permission

from Venmyn Rand (Pty) Ltd. Trading as Venmyn.

THexSaxendrift'06Fig12.cdr

Road

Gravel Road

River

Powerline

Mid Orange Mine/Project

Farm Boundary

Gravel Assemblage Terrace

SCALE:

0 2 4 km2

TEXT

BRAKFONTEIN276

ANNEX SAXES D

RIFT 21

Orange River

SAXENDRIFT 20

VIEGULANDS PUT 39

NIEWEJAARSK RAAL 40

KRANSFONTEIN 19

MOOIDRAAI 36

ZWEM KUIL 37

REMHOOGTE 152

BLAAUWBOSCH DRAAI 141

KWARTELS PAN 25

SAXENDRIFT MINE

KWARTELSPAN PROJECT

NIEWEJAARSKRAAL MINE

ZWEMKUIL-MOOIDRAAI PROJECT

REMHOOGTE-HOLSLOOT PROJECT

TA4

TA3

TA2

TA1

TB3

TB2

TB1

TC4

TC3

TC2

TC1

Terrace A

Terrace B

Terrace C

HOLSLOOT47

THO - Middle Orange Projects

SPV 1

SPV 2

SPV 3

ANNEX BRAKFONTEIN EAST 22

BONDEO ACQUISITION: PROPERTIES CONTIGUOUS TO EXISTING MOR PROPERTIES

30 kms

16February 2015 |

* Based on the Company’s approved internal budgets for F2015

** LOM based on NI43-101 report, excludes any future exploration potential

STATUS OPERATIONGRADE* (CARATS /

100M3)

PROCESSINGRATE

(M3/MONTH)

CARAT

VALUE*(US$)

LIFE OF

MINE

(YEARS)**

STEADY STATE UNIT

COST

INPRODUCTION

SAXENDRIFT / SAXENDRIFT EXT. 0.45 - 0.51 180,000 2,300 3 US$9.0/m3

NIEWEJAARSKRAAL 0.6 130,000 2,600 >10 US$12.0/m3

PROCESS AT

SAXENDRIFTSAXENDRIFT HILL COMPLEX 0.4 - 2,400 0.5 -

JV IN RAMP

UPKWARTELSPAN 0.76 36,000 2,400 1.5 -

EVALUATIONWOUTERSPAN:PEA COMPLETED

0.62 350,000 2,300 >10 -

ROYALTY

MINING

TIRISANO: 6X ROYALTY MINING

CONTRACTS0.45 - 0.63 160,000 668 >18 -

DIVERSIFIED PRODUCTION:CURRENT AND ACQUIRED OPERATIONS + DEVELOPMENT OPPORTUNITIES

ACQUISITION

TARGET

REMHOOGTE / HOLSLOOT:Produced >7,300 cts of high quality diamonds: Sample grade of 0.8 cphm3 value at US$3,000 – US$4,000 /ctExploration Targets of 11 - 12 M m3 of gravels at target grade of 0.4 – 1.5 cphm3

Processing capacity increases by ~200,000m3 p.m.

BROWNFIELD

PROJECT

BO-KAROO:Many areas at same elevation levels as Saxendrift / NiewejaarskraalExtensive Exploration Targets: Historical sample grades of 0.2 – 0.4 cphm3 + diamond values of US$3,000 – US$4,000/ct

17February 2015 |

* Indicative quarterly revenue and +50 carat stone production based on technical reports

PAST

(Actual)

PAST

(Actual)

CURRENT

(Actual)

CURRENT

(Actual)FUTURE: ORGANIC

(Plan)

FUTURE: ORGANIC

(Plan)

MINES

(000

M3 /MONTH)

MINES

(000

M3 /MONTH)

QUARTERLY

REVENUE*

QUARTERLY

REVENUE*

# +5

0 CARAT

STO

NESPER

YEAR*

# +5

0 CARAT

STO

NESPER

YEAR*

99

110,000m3 360,000m3 480,000m3

MONTHLY

MOR

THROUGHPUT

MONTHLY

MOR

THROUGHPUT

Time

Rev

enue

Time

Rev

enue

Time

Rev

enue

44442727

FUTURE: POST

ACQUISITION (Plan)

FUTURE: POST

ACQUISITION (Plan)

700,000m3 growing to 1,000,000m3

Rev

enue

48+2248

+22

110

SX SHC NJK WP RH

Time

180

80 100

SX SHC NJK WP RH

200

130 150

SX SHC NJK WP RH

200 200 150 150

150 150

SX SHC NJK WP RH

WHERE WE ARE GOING

18February 2015 |

DIAMOND VALUE MANAGEMENT: IMPACTS EVERY PART OF ROCKWELL’S BUSINESS

Dia

mon

d Va

lue

Man

agem

ent D

isci

plin

esD

iam

ond

Valu

e M

anag

emen

t Dis

cipl

ines

Operations ManagementOperations

Management

Mining Mining

Mineral Resource

Management

Mineral Resource

Management

Earthmoving

Renewal Plan

Earthmoving

Renewal Plan

Processing Processing

Fit-for-purpose

Technologies

Fit-for-purpose

Technologies

MetallurgyMetallurgy

FundingFundingShareholder Value

management

Shareholder Value

management

MarketingMarketingBeneficiation

Joint Venture

Beneficiation

Joint Venture

Chairman’s visit: December 2014

19February 2015 |

FLEET OPTIMIZATION PLAN AT SAXENDRIFT / SHC: IMPROVE THROUGHPUT AND REDUCE MAINTENANCE EXPENSES

Challenge

♦ Escalating vehicle maintenance costs and inadequate fleet availabilities

♦ Declining overall plant utilization (OPU)

Objective

♦ Improve earthmoving availabilities to increase mining volumes

♦ Reduce maintenance costs

♦ Sweat invested processing capacity

Investigation

♦ Review of status quo with expert consultant (Kenn Smart)

♦ Fleet unmatched to current and future mining requirements

♦ Reorganization of maintenance and asset management practices

Challenge

♦ Escalating vehicle maintenance costs and inadequate fleet availabilities

♦ Declining overall plant utilization (OPU)

Objective

♦ Improve earthmoving availabilities to increase mining volumes

♦ Reduce maintenance costs

♦ Sweat invested processing capacity

Investigation

♦ Review of status quo with expert consultant (Kenn Smart)

♦ Fleet unmatched to current and future mining requirements

♦ Reorganization of maintenance and asset management practices

Implementation

♦ Eqstra selected as EMV provider

♦ Reviewing financing options

♦ Managed maintenance lease

♦ Guaranteed availability (85%)

♦ No upfront capex

♦ 10-15% maintenance cost reduction

♦ Rebuild of existing equipment internally funded

Implementation

♦ Eqstra selected as EMV provider

♦ Reviewing financing options

♦ Managed maintenance lease

♦ Guaranteed availability (85%)

♦ No upfront capex

♦ 10-15% maintenance cost reduction

♦ Rebuild of existing equipment internally funded

20February 2015 |

BONDEO ACQUISITION:INVESTMENT HIGHLIGHTS

• Accretive on operating and financial metrics

• Acquisition of complementary alluvial diamond properties and associated plant and equipment in South Africa

• Contiguous assets to existing properties, enlarging operating and asset base as well as property portfolio

• Potentially high value gem quality diamonds

• Economies of scale with potential to reduce volatility of quarterly production: Potential to increase MOR throughput

to 1,000,000m3 per month

• Increased optionality: Leverage financial / human / intellectual capital across broader operational base

21February 2015 |

BONDEO ACQUISITION:PERFECT COMPLEMENT TO EXISTING ASSET BASE

c.0.9 million m3 of gravel processed since start-up (May to Dec 2014)

♦ 7,307 carats of high quality diamonds produced

♦ Sample grade of 0.8 cpcm3

High carat values: US$3,000 to US$4,000 / ct at sale of ~5,000 cts

Remhoogte Mine / Holsloot Project:

♦ Exploration targets of 11 to 12 M m3 of gravel with target grades of

0.4 to 1.5 cphm3

♦ Better colours than Rockwell’s current MOR assortment with largest

stone of 178 carats

Fit-for-purpose processing plants: Processing ~200,000 m3 p.m.

♦ Remhoogte (commissioned June 2014): Bourevestnik Bulk X-ray for

coarse gravels + 4x rotary pan plant for fine gravels

♦ Remhoogte (commissioned November 2014): Rotary pan plant with

four pans

♦ Holsloot (recently commissioned): Desanding system, Bourevestnik

Bulk X-ray for coarse gravels + DMS

Includes acquisition of brownfields Bo-Karoo exploration project

c.0.9 million m3 of gravel processed since start-up (May to Dec 2014)

♦ 7,307 carats of high quality diamonds produced

♦ Sample grade of 0.8 cpcm3

High carat values: US$3,000 to US$4,000 / ct at sale of ~5,000 cts

Remhoogte Mine / Holsloot Project:

♦ Exploration targets of 11 to 12 M m3 of gravel with target grades of

0.4 to 1.5 cphm3

♦ Better colours than Rockwell’s current MOR assortment with largest

stone of 178 carats

Fit-for-purpose processing plants: Processing ~200,000 m3 p.m.

♦ Remhoogte (commissioned June 2014): Bourevestnik Bulk X-ray for

coarse gravels + 4x rotary pan plant for fine gravels

♦ Remhoogte (commissioned November 2014): Rotary pan plant with

four pans

♦ Holsloot (recently commissioned): Desanding system, Bourevestnik

Bulk X-ray for coarse gravels + DMS

Includes acquisition of brownfields Bo-Karoo exploration project

22February 2015 |

BENEFICIATION JOINT VENTURE:SIGNIFICANT VALUE ADD

ROUGH

77 ct makeable, Saxendrift Extension

(2012)

145 ct makeable, old Saxendrift tailings

(2012)

105 ct Type II A, Middle Orange (2009)

169 ct yellow, Saxendrift Hill Complex

(2013)

128 ct yellow, Middle Orange (2011)

POLISHED

37 ct J color round brilliant, VS2

30 ct stone being polished. Additional

pieces to be polished

35 ct D color internally flawless

Sold for $230,000/ct109 ct vivid yellow 81 ct vivid yellow

BENEFI-CIATION

VALUE ADD

+34% on initial roughsale price

Currently being polished

+62% on initial roughsale price

+61% on initial roughsale price

+126% on initial roughsale price

Diacore profit share agreement (>2.8 carat stones)

• Market related prices for diamonds sold into JV + 50% profit share on polished price

• 10% revenue uplift in F2014: US$4.1m

Diacore profit share agreement (>2.8 carat stones)

• Market related prices for diamonds sold into JV + 50% profit share on polished price

• 10% revenue uplift in F2014: US$4.1m

23February 2015 |

5

6

7

8

9

10

11

12

13

14

15

16

17

18

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

F2011 F2012 F2013 F2014 F2015

Rev

enue (incl. b

eneficiation (US$m

)

Ave

rage va

lue per carat (US$

Revenue (including beneficiation)

Average price per carat (US$)

4 per. Mov. Avg. (Average price per carat (US$))

Holpan on C&M Klipdam sold

Number of MOR mines

Acquired Saxendrift Ext.

1 2 3

10 successive quarters of revenue growth

CORPORATE TURNAROUND:

FINANCIAL HIGHLIGHTS

24February 2015 |

FIVE PRODUCTION YEAR PLAN:CRITICAL MASS AND SCALE IN MOR

1. Projected production and revenue for own operations: These are based on the Company’s latest internal budget information and the technical reports.

2. Projected production and revenue for properties being acquired from Bondeo: These are based on the information disclosed in the Company News Release published on February 05, 2015.

MEDIUM TERM GROWTH TARGET: Process 1,000,000m3 of quality gravels p.m. from multiple faces

OBJECTIVE: Enhance quarterly earnings visibility

0

1

2

3

4

5

6

7

8

9

10

F2014A F2015E F2016E F2017E F2018E F2019E

Production plans (million m3)

Remhoogte

Wouterspan

Niewejaarskraal

SHC

Saxendrift + Extension

0

50

100

150

200

250

F2014A F2015E F2016E F2017E F2018E F2019E

Value of diamond sales (US$m)

Remhoogte

Wouterspan

Niewejaarskraal

SHC

Saxendrift + Extension

25February 2015 |

SUPPLY

ANDDEMAND

PRICING

Demand expected to exceed supply: Within next 10 yrs despite global

economic woes

Supply and demand growth: (Goldman Sachs)

Rough demand: 11% CAGR to 2017

Rough supply: 5.2% CAGR to 2017

By 2020: Declining production among many existing mines

Current projects under development: 25% of production capacity

in 2020

After 2020: Global rough diamond production could go into decline

Demand expected to exceed supply: Within next 10 yrs despite global

economic woes

Supply and demand growth: (Goldman Sachs)

Rough demand: 11% CAGR to 2017

Rough supply: 5.2% CAGR to 2017

By 2020: Declining production among many existing mines

Current projects under development: 25% of production capacity

in 2020

After 2020: Global rough diamond production could go into decline

Source: Dundee Capital Markets, Bain & Co

2013 2015F 2017F 2019F 2021F 2023F 2024F

Forecasted demand

Forecasted production

100

125

150

175

75

Rough diamond supply and demand 2013-2024, 2013= 100 Index; 2013 price

Note: Rough diamond demand has been transformed from polished diamond demand using historical rough

diamond/polished diamond ratio

Source: Euromonitor, Kimberley Process; Idex; Tacy Ltd and Chaim Evan-Zohar; publication analysis; expert interviews; Bain

analysis

Annual retail diamond sales: up ~4% in 2014

US retail sales deflationary due to decrease in gold and diamond prices:

Leading to increased consumer demand

Large and special diamonds sold on auction in 2014: Increased

demand with higher prices with all major Auction houses

Increased interest at auctions: Supports +10ct diamond prices

Lower polished inventories (post Festive season sales) + rough

diamond supply by major producers: Buoy demand in H2 2015 to

stabilize diamond prices

Annual retail diamond sales: up ~4% in 2014

US retail sales deflationary due to decrease in gold and diamond prices:

Leading to increased consumer demand

Large and special diamonds sold on auction in 2014: Increased

demand with higher prices with all major Auction houses

Increased interest at auctions: Supports +10ct diamond prices

Lower polished inventories (post Festive season sales) + rough

diamond supply by major producers: Buoy demand in H2 2015 to

stabilize diamond prices0

20

40

60

80

100

120

140

160

180

200

Ind

ex

Historic Rough Prices

DCM Rough Estimate

Polished Prices

+5% CAGR +13% CAGR

+2.5% CAGR Est

0

20

40

60

80

100

120

140

160

180

200

Ind

ex

Historic Rough Prices

DCM Rough Estimate

Polished Prices

+5% CAGR +13% CAGR

+2.5% CAGR Est

POSITIVE LONG TERM DIAMOND MARKET FUNDAMENTALS:SUPPLY AND DEMAND / PRICING

Source: De Beers

Source: Company

26February 2015 |

SHORT TERM PRIORITIES

COMPLETE BONDEO

ACQUISITION• Short term opportunities for efficiencies: Efficient allocation resources across broader asset base

SAXENDRIFT HILL

COMPLEX

• Process remaining resource at Saxendrift Hill Complex through Saxendrift processing infrastructure

• Relocate portions of EMV fleet to Niewejaarskraal

NIEWEJAARSKRAAL• Operate plant at current design capacity of 130,000m3 p.m. after moving SHC fleet

• Relocate SHC plant assets to increase capacity to 200,000m3 p.m.

INTEGRATEREMHOOGTE/HOLSLOOT

• Standardize operations to Rockwell’s MOR operational template

• Apply Rockwell’s MOR-specific geological and technical skill including longer term planning

• Evaluate option to integrate existing processing plants

• Transfer current employees to Rockwell employment to ensure continuous production

• Implement fit-for-purpose modifications at Remhoogte and Holsloot operations

EXPLORATIONPROGRAMME

• Define Mineral Resource at Remhoogte/Holsloot by end February 2016

• Exploration at Bo Karoo to evaluate potential as a possible replacement for Saxendrift

REGIONAL GEOLOGY

STRATEGY• Regional geological strategy expanded following granting of >50,000 ha of new mining and prospecting rights

• Identify new targets for follow up and economic assessment

27February 2015 |

OUR SPECIAL POSITIONING

•Experienced leadership team with ≈100yrs diamond experience + Engaged board of directors•Young professional team including 12 geologists and metallurgists

PEOPLE

•Produced nine large (+100 carat) , high value diamonds in Middle Orange since September 2013

•Quality of production profile enhanced with acquisition of Remhoogte

•Resources have high quality diamonds: Average values >US$2,000/ct vs global average of ~US$100/ct

PRODUCT

•Access over majority of Orange River alluvial diamonds fields: Existing properties + Acquisition of

Remhoogte and Bo-Karoo + New rights spanning >50,000 haPROPERTIES

•Acquisition delivers current mid-term target of 500,000m3 /month: Better quarterly earnings visibility

•New medium term production target increases to potentially 1,000,000m3 after acquisitionPRODUCTION

•Beneficiation partnership with Diacore (+10 carat stones): 50% profit share in sale of polished diamonds

• Increases leverage to diamond prices: Added ~10% to F2014 revenue

•Supportive shareholder base

PARTNERSHIPS

• Improving performance due to strategic turnaround programme

•Focused on consolidation opportunities

•Granted new prospecting and mining rights in MORPOTENTIAL

•Positive industry fundamentals: Supply deficit forecast after 2018

•Strong demand for investment diamondsPROSPECTS

28February 2015 |

ROCKWELL’S RESOURCE CENTERED

APPROACH TO MININGMULALO NDWAMMBI, SENIOR PRODUCTION MANAGER

29February 2015 |

REGIONAL GEOLOGY

30February 2015 |

GRAVELS

31February 2015 |

12 MONTH MINE PLAN

Saxendrift

Niewejaarskraal

NJK

32February 2015 |

DRILLING

GeophysicsResistivity and lithology's

Structural GeologyEnlisted Mike De Wit and John WardPriority rating scheme

GeophysicsResistivity and lithology's

Structural GeologyEnlisted Mike De Wit and John WardPriority rating scheme

33February 2015 |

RESOURCE CONTOURING

34February 2015 |

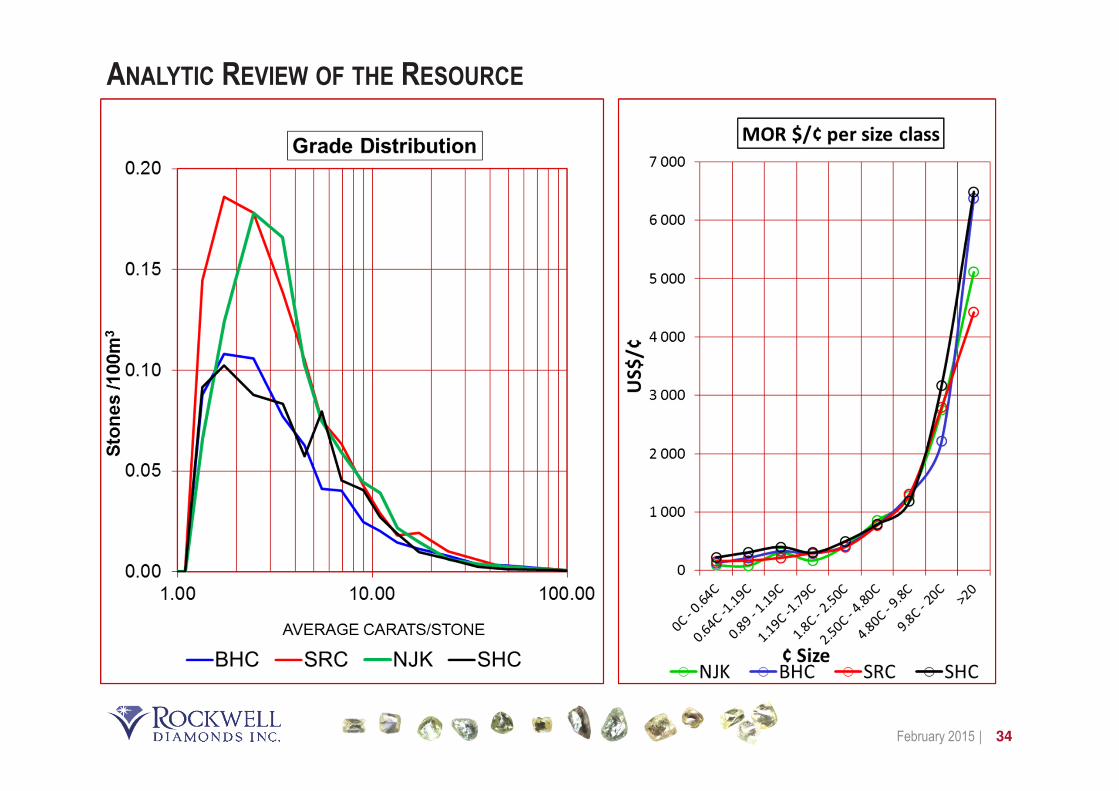

ANALYTIC REVIEW OF THE RESOURCE

35February 2015 |

MINING METHOD

Drilling and Blasting

Rehabilitation

Stripping

Processing

Loading and Hauling

Dozing and Liberating

36February 2015 |

METALLURGY

In-Field Screen

Waste +75mm

ROM

Scrubbing and Screening

Wet Plant

DMSRotary Pans

BV

Concentration

Final product

FlowsortBV

Recovery

37February 2015 |

SECURITY

• Off-site camera surveillance

• Covert and overt cameras

• Routine polygraph testing

• Application of industry intelligence

• Reports directly to CEO

38February 2015 |

CONCLUSION

�Planning is based on

� Clear understanding of the resource

� Depositional Environment

� Value Distribution

� Size Distribution

� Alluvial’s Volume Based

� Allocation of EMV & sequencing

� Fit for purpose equipment

� Diamond Clusters

�Production results analyzed

� Historical data

� Determine recovery efficiency

� Expected trends

� Guidance to ensure balance resource depletion

39February 2015 |

REVIEW OF ACQUISITION: DEAL

STRUCTURE AND TIMELINES

JOHN SHELTON, CFO

40February 2015 |

THE BONDEO DEAL

Acquisition of: R million

Mining and prospecting rights - Remhoogte / Holsloot 80

(these are contiguous properties)

Exploration rights - Bo Karoo 5

3 mineral processing plants 28

2 Properties (Social assets and staff housing) 7

Assets under lease 126

Assets vendor financed 39

Total to be financed 285 Equivalent = C$29 million

41February 2015 |

THE BONDEO DEAL

R million

Total to be financed 285

Financed as follows:

Vendor financed (10 months) 39

Bond on properties 7

EMV refinanced 88 70% of acquisition value assumed

Other 151

Total (to be financed as a combination of equity and debt) 285

42February 2015 |

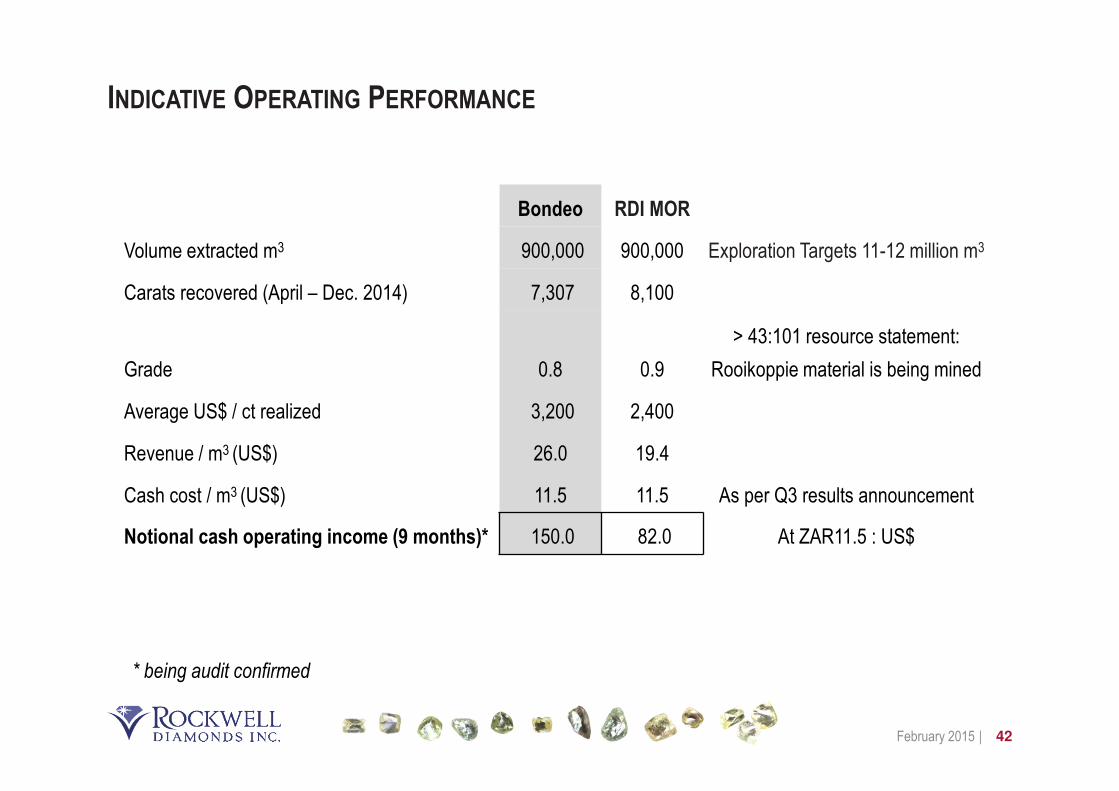

INDICATIVE OPERATING PERFORMANCE

Bondeo RDI MOR

Volume extracted m3 900,000 900,000 Exploration Targets 11-12 million m3

Carats recovered (April – Dec. 2014) 7,307 8,100

Grade 0.8 0.9

> 43:101 resource statement:

Rooikoppie material is being mined

Average US$ / ct realized 3,200 2,400

Revenue / m3 (US$) 26.0 19.4

Cash cost / m3 (US$) 11.5 11.5 As per Q3 results announcement

Notional cash operating income (9 months)* 150.0 82.0 At ZAR11.5 : US$

* being audit confirmed

43February 2015 |

INDICATIVE IMPACT ON ROCKWELL'S BALANCE SHEET

Including Bondeo at:

Nov-14 100% equity 50% equity 25% equity

Target

Equity 42 71 56 49

Long term debt 6 6 21 28

Net current debt 1 1 1 1

Total equity and liabilities 49 78 78 78

Debt : equity 17% 10% 39% 59%

• Preferred option: 50% equity and 50% debt

• Additional R140m of debt is sustainable given the properties’ cash flow generation potential

• Split as R88m in leases and debt of R52m, of which R38m is vendor provided

• An additional R30m in working capital facilities would be sought

44February 2015 |

QUESTIONS

Four +100 carats recovered in Middle Orange River in August/September 2013

45February 2015 |

43-101 MINERAL RESOURCE SUMMARY

# Due to a lack of reliable data on SHC, the 5mm bottom cut-off size (“bcos”) values are not included at Indicated Mineral Resource classification.Diamond values (under “Value”) for BHC, SHC, KPC and Niewejaarskraal are based on a two-year moving average (from + 10,000ct from the BHC terrace on Saxendrift mine at 5mm bcos). Diamond values for SRC are based on the 5mm bcos sales data for FY2013 only. Diamond values for Wouterspan are based on extrapolation of FY2011 data at 5mm bcos.Tirisano data is at 29 February, 2012NOTE: the Indicated Mineral Resources on the BHC terrace of the Saxendrift mine are inclusive of the Mineral Reserves.