01 | 2013 | siemens.com/industry industry journal€¦ · ceo siemens industry editor’s note...

TRANSCRIPT

Ind

ust

ry J

ou

rnal

– T

op

ics,

tre

nd

s, a

nd

tec

hn

olo

gie

s fo

r d

ecis

ion

mak

ers

in m

anu

fact

uri

ng

– 0

1 | 2

013

Focus: The future of industry

Real values

New orientation: Industry is enjoying a worldwide boom, thanks to ultramodern software and IT.

Private production

3D printers are capturing the mass market. Industry also relies on these printers to make products in small quantities.

Abundant energy

Russia is one of the world’s largest suppliers of natural gas – and one of the most attractive export markets on earth.

Industry Journal Topics, trends, and technologies for decision makers in manufacturing

01 | 2013 | siemens.com/industry

Th

e f

utu

re o

f in

du

stry

People all over the world are returning to the values of industry.«

»

02 Industry Journal | 01 | 2013 | Editor‘s note

Siegfried Russwurm, CEO Siemens Industry

Editor’s note

Industry Journal | 01 | 2013 | Editor‘s note

Dear readers,

Industry is experiencing a global boom as politicians and the media discuss the comeback of traditional manufacturing and express great appreciation for it. Industrial companies in the United States, Great Britain, Germany, India, and China are finding that there’s a great deal of interest in them and support for their concerns.

The current friendliness toward manufacturing is closely linked to the economic tribulations of the past decade. First the bubble of the »new economy« burst, and then the financial crisis shook the economy to its core. Countries with a strong industrial base coped much better than did economies that had wagered everything on the service sector.

That’s why people all over the world are returning to the values of manufacturing, which day after day makes real products, secures jobs, and serves as a driver for growth, prosperity, and social peace.

Western countries are bringing production capacities back home. And some formerly lowwage countries are increasing value creation by focusing on making valuable products instead of lowprice massproduced goods.

One important factor in this is a technological development that can link productivity and efficiency more than ever before, reducing costs, shortening times to market, and increasing flexibility. I’m referring to the connection of the real and the virtual world of production using ultramodern industrial software combined with increasingly powerful hardware.

This issue of Industry Journal sheds some light on this trend and the resulting opportunities for decision makers in manufacturing. We hope you will find it to be profitable reading.

Best regards,Siegfried Russwurm

03

10Real values

Industry is experiencing a worldwide comeback following the collapse of the new economy and the crash of the financial markets. Major technological progress in IT and software, accompanied by societal changes, has led to a new orientation. As a result, traditional industrialized countries are expanding their domestic production capacities again, and emerging countries are discovering that it’s more profitable to manufacture highquality products than to make and assemble simple massproduced goods. The image of the old economy is improving all over the world.

Markets

Focus: The future of industry20 »Bringing back manufacturing«

Interview with Anthony Foxx, Mayor of Charlotte, North Carolina, about modernization initiatives for manufacturing, the image of this business sector, and competition among cities.

24 Production for the people 3D printers are capturing the mass market.

Customers use them to print spare parts and specialty parts. But companies are also counting on additive production. This is the beginning of a major trend.

30 The manufacturing imperative Countries put their own competitiveness and

economic stability at risk when they neglect their manufacturing industries. An essay by Harvard economist Dani Rodrik.

33 Production comes home Products are increasingly being manufactured

where they are sold. An essay about the reregionalization of the economy by David Bosshart, CEO of Gottlieb Duttweiler Institute of Switzerland.

36 Absolutely camera-ready The new Cars Land at Disney California Adventure

Park south of Los Angeles offers plenty of outdoor fun. It might seem like child’s play, but it requires ultramodern technology.

40 Rising to the top with service Manufacturing companies need reliable service –

a lucrative growth market for the companies that equip industry.

44 Full of energy Russia is one of the world’s largest suppliers of

energy. Its 140 million consumers and its major need for investment in industrial companies and infrastructure offer opportunities for investors. A report on the partner country at the 2013 Hannover Messe.

Industry Journal | 01 | 2013 | Contents04

Management

Themes

Innovation

56 66

06 Big picture Kalex uses PLM software

by Siemens to build worldcham pion racing motorcycles.

08 Spotlights Efficient steam turbines, eleva

tor controls, maintenance for copper mines, Inventors of the Year, TIA Portal, and Simatic S71500.

42 What is the job of a maintenance manager? Integral Plant Maintenance increases the productivity of industrial plants.

50 People to watch: Esther Duflo

The MIT professor uses unconventional methods to solve the problems of the world’s poorest people.

76 Bookshop Books worth reading: Makers,

Jugaad Innovation, Just Start, Extreme Trust.

78 Imprint

56 The most dedicated employees in the world

Two international consulting firms have measured employee engagement. This survey will help companies use engagement management to increase productivity.

62 Knowledge as a business model Nathan Myhrvold is a physicist, economist, and former executive at Microsoft who advocates the privatization of knowledge. His U.S. company Intellectual Ventures markets more than 40,000 patents and ranks among the world’s major patent brokers.

66 The charm of the swarm It’s not the highestranking member of the

swarm that determines its direction, it’s the one with the best information – a model for future decentralized production and logis tical systems.

72 The place for really big questions Scientists at CERN, the European Organiza tion for Nuclear Research in Geneva, Switzerland, are hunting for the smallest elements. The Large Hadron Collider, which cost €3 billion, is one of the most complex machines in the world.

Industry Journal | 01 | 2013 | Contents 05

Big PictureTechnology for world champions

Kalex motorcycles are always at the head of the pack. Stefan Bradl of Germany became world champion in the Moto2 class on a Kalex in 2011, Pol Espargaró of Spain (pictured here) took a Kalex to second place in 2012, and Sandro Cortese of Germany – the current world champion in the Moto3 class – will ride a Kalex in the Moto2 for the first time in 2013. Kalex is a German company specializing in the development, design, and production of custom motorcycles and parts. Located in Bobingen, a town in Bavaria, Germany, Kalex uses the NX CAD/CAM/CAE solution from Siemens PLM Software. Cortese will be competing in 2013 for the new Dynavolt Intact GP team, which is based in Memmingen, Germany, and which was created specifically for him. The team’s main sponsor is the Chinese battery manufacturer Dynavolt.

Industry Journal | 01 | 2013 | Big Picture06

07Industry Journal | 01 | 2013 | Big Picture

Spotlights

The new version of the Totally Integrated Automation (TIA) Portal, the integrated engineer ing framework from Siemens, makes the imple mentation of automation solutions even more efficient. Version V12 of the TIA Portal now enables the seam less integration and planning of drive technology. Safety features were also enhanced, including those for the new Simatic S71500 controller. Security measures were impro ved to safeguard business

secrets, protect against copying, and control access.

The new generation of Simatic S71500 controllers also ushers in major improvements in engineering. The medium and highend controllers integrate many standard motioncontrol, security, and safety features, including the new con figurable diagnostic feature for the system status and integration into the TIA Portal for easier engineering and reduced planning costs.

More enhancements to TIA Portal and Simatic S7-1500

Efficient steam turbine

Siemens has developed an industrial steam turbine that boasts much greater efficiency and starts up nearly twice as fast as previous mod els. The result: Biogas facilities, com binedcycle power plants, and smaller coalfired power plants can produce more energy than ever before. Facilities like solar thermal plants that do not produce energy continuously also benefit.

An optimized turbine blade design and better insulation of the turbine stages make these gains possible. The new turbines also feature a symmetrical outer casing that warms up more evenly than before. The use of new materials and the materialsaving design improve the warmup stage while also extending the turbine’s useful life.

Every year, millions of tourists visit one of America’s bestknown icons: the Statue of Liberty in New York. Thanks to a comprehensive overhaul in 2012, Lady Liberty now complies with the latest safety standards. The project included replacing the 30yearold emer gency elevator, which ensures that safety personnel like paramedics and firefighters can quickly reach

New heights for Lady Liberty

the observation platform located in the crown.

Siemens developed the control and monitoring software for the elevator system. Project partner Tower Elevator Systems used the Siemens TIA Portal to program the software, which saved costs by accelerating the engineering, testing, and troubleshooting phases.

The new SST111 multistage industrial steam turbine

126 years old but equipped with the latest technology: the Statue of Liberty in New York

Industry Journal | 01 | 2013 | Spotlights08

Siemens has expanded its portfolio of complex product testing and simulation software through the acqui sition of LMS International in Belgium. LMS, with its 1,200 employees, is a software partner and key supplier to leading global enterprises in the automotive and aerospace sectors.

The company develops software platforms that simulate and test mechatronic systems in automobiles and airplanes. They makes it pos sible to virtually test and optimize

Software for complex simulations

the vibrational patterns, acoustic properties, and fatigue strength of all components – with no need for expensive prototypes or com plex physical test environments.

LMS is the ideal addition to the Siemens PLM portfolio, allowing Siemens to expand its dominant position in the market for simulation and analysis software. Shared customers include big names like Daimler, General Motors, Nissan, Volkswagen, Boeing, Mercury Marine, Ericsson, and even NASA.

Service in the Andes Siemens has taken over plant and equipment maintenance in the Andina mine operated by Chilean mining company Codelco, the world’s largest producer of copper. The job begins with the crushers that break down the copper ore and includes the conveyors, mills, flotation basins, and filtration equipment. The fiveyear contract includes the molybdenum equipment, the shafthoisting installation, and the piping system. The Andean mine supplies some 248,000 metric tons of copper annually.

The maintenance services are billed by agreedupon metrics such as production volume, system availability, safety, and environmental impact. Siemens also follows Codelco’s riskbased maintenance concept. The Andina mine is now the third Codelco mine in Chile, after Radomiro Tomic and Minera Gaby, for which Siemens manages technical maintenance.

Copper mine owned by Chilean mining giant Codelco.

Scrap is to be minimized at all costs in the stainless steel production process. One area where scrap is generated is in the rolling mill when wornout rolls are replaced. Siemens employee HansJoachim Felkl developed a new process for replacing rolls that can increase the output by at least seven percent for coldrolling mills. The 58yearold was honored as Inventor of the Year for his developments to increase throughput in tandem lines.

Since 1995, Siemens has yearly awarded the distinction Inventor

of the Year to excellent researchers and developers in its workforce. The twelve recip ients honored in 2012 account for 734 indivi dually issued patents. Overall, Siemens applied for 4,600 patents in 2012.

The other honoree in the Industry Sector is Manuela Lüftl, an engineer who played a key role in developing an improved generation of contactors – special devices that are essential for switching motors in automation technology.

HansJoachim Felkl developed a new process for replacing rolls

Manuela Lüftl improved a device for switching motors in industry

Inventors of the Year

09Industry Journal | 01 | 2013 | Spotlights

Comeback of manu- facturing

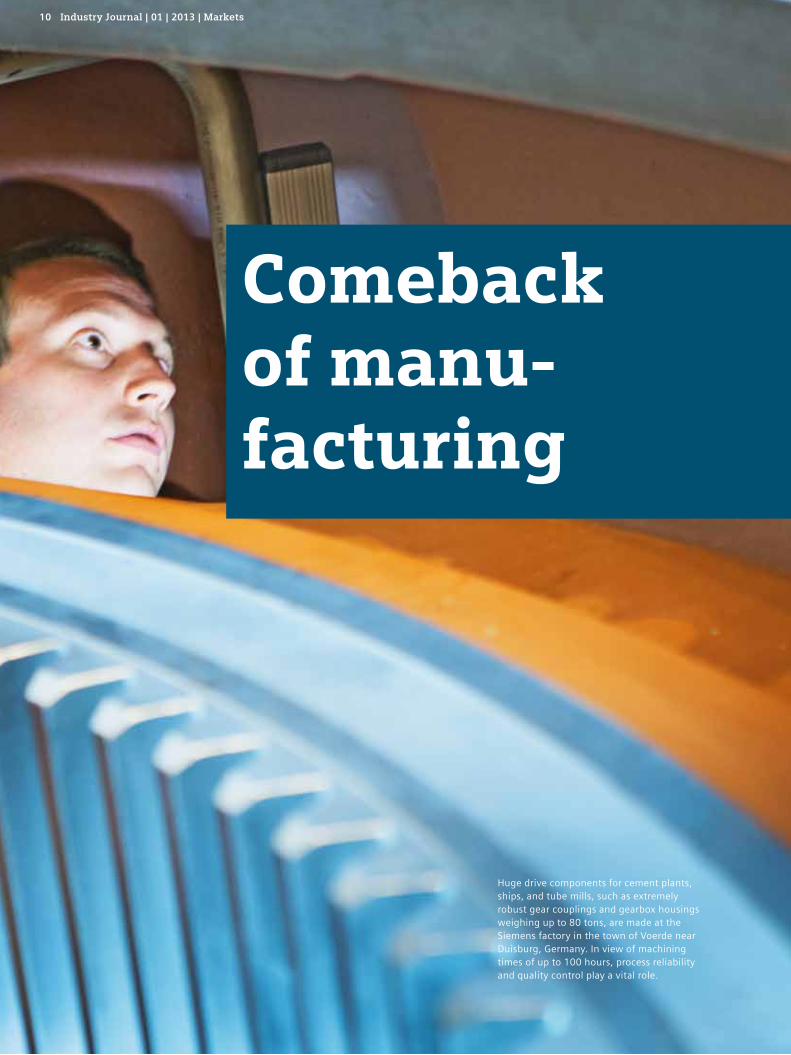

Huge drive components for cement plants, ships, and tube mills, such as extremely robust gear couplings and gearbox housings weighing up to 80 tons, are made at the Siemens factory in the town of Voerde near Duisburg, Germany. In view of machining times of up to 100 hours, process reliability and quality control play a vital role.

Industry Journal | 01 | 2013 | Markets10

Berlin, the capital of Germany, is full of industrial buildings. As the result of a precipitous decline in Berlin’s industry, they often stand empty or offer homes to architects and artists. In 1920, nearly 600,000 people poured through the plant gates at companies like Borsig, Schering, AEG, and SiemensSchuckert every morning. But most companies either left or were dismantled after the Second World War. The number of industrial workers fell to 100,000 – and Berlin sought its salvation in sectors like the media, tourism, and software.

The city is now planning a comeback as a location for industry. The Berlin Senate, the executive body that governs the city, has been working with associations, trade unions, and companies to develop the »Industrial City Berlin 2010–2020« master plan, and now hopes to double the number of industrial jobs in just

a few years. »Creative cities with service economies need an industrial base,« says Governing Mayor Klaus Wowereit.

Berlin is in good company as it falls back in love with the manufacturing sector again. Governments all over the world are developing programs to promote industry. U.S. President Barack Obama recently announced a proposal to create a National Network for Manufacturing Innovation, with 15 research institutions located all over the country that will encourage innovation in industry.

Wellknown American industry organizations have also joined the National Manufacturing Renaissance Campaign to promote highquality industrial manufacturing. And companies all over the country are starting to bring back manufacturing that they once outsourced to lowwage countries.

Industry is experiencing a worldwide renaissance following the collapse of the

new economy and the crash of the financial markets. Technological progress in

manu facturing, accompanied by societal changes, has led to a new orientation.

Traditional industrialized countries are expanding their domestic production

capacities again, and emerging countries are discovering that it’s more profitable

to manufacture high-quality products than to make cheap, simple, mass-produced

goods. The image of the »old economy« is improving all over the world. Industry

is suddenly sexy again.

»

»Industry is a guarantor of growth and social stability.«Thomas Menze, Senior consultant, ARC Advisory Group

11Industry Journal | 01 | 2013 | Markets

Even upandcoming India, the service provider, has a new economic policy that calls for increas ing industry’s current share of GDP by more than fifty percent before 2025.

Unusual esteem

From Michigan to Manchester, Delhi to Detroit, Beijing to Berlin – industry is in vogue all over the world. It is being courted and is enjoying unusual esteem in the eyes of political leaders and society at large. This follows years of pro cla mations – at least in the Western world – that the next stage would be a service society that would create intellectual property instead of cumbersome machinery.

The new economy arose during this phase of euphoria in the service sector. Internet business models mushroomed, with enormous expectations for returns. There was a goldrush mentality. Dotcom companies were unreservedly viewed as cool and, above all, as the new economy – the future.

In contrast, industry meant the old economy – the past. It apparently did only what it had always done: make machines and drives, auto bodies and motors, fuel and chemicals, drugs and flour. With no perks like a soccer table in the office, no bosses wearing hoodies, and no rosecolored glasses. To young people, a job in industry was about as attractive as a glass of iced tea on Grandma’s porch.

Factories were seen as relics of another time. The United States and Great Britain sold their industrial base or shifted it to lowwage countries. In the United Kingdom today, only about one employed person in ten works in industry. Industrial manufacturing’s share of gross value creation declined from 19 percent in 1998 to 11 percent in 2010. American states with previously strong sectors like steel, consumer electronics, and machine manufacturing saw their industrial value creation fall from 17 to 13 percent during the same period. Almost six million industrial jobs disappeared during the first decade of this century.

The same thing is happening in Europe. EU Industry Commissioner Antonio Tajani has submitted a strategy paper calling for industry’s share of gross domestic product (GDP) to increase from 16 to 20 percent by 2020. He is pressing for »a third industrial revolution.« And EU Energy Commissioner Günther Oettinger is urging a »reindustrialization of Europe.«

The emerging countries with their strong economies have also recognized this global trend. China, according to its current fiveyear plan, will no longer emphasize cheap assembly or the manufac turing of simple, massproduced goods. Instead, the country will increasingly emphasize sophisticated manufacturing of highquality products by select hightech industrial sectors.

One reason for this is to compensate for the increasing loss of China’s position as the »world’s workshop.« China also knows that this kind of manufacturing promises greater value creation, growth, and prosperity in the future.

Spain

GermanyGreat Britain

U.S.

Industry, value added (% of GDP)

Source: World Bank*2002, **2009

1998|2010

17|13 23|2318|11

19|13**Mexico 21|18

Russia

17*|15

Brazil

16|15Australia

15|9

India15|15

South Africa

19|15

Sweden22|16

Japan

22|19

Indonesia25|25

China32|30

Vietnam17|20

Industry Journal | 01 | 2013 | Markets12

»The reputation of what are known as ‘bluecollar jobs’ has suffered a great deal compared with ‘whitecollar jobs’ in the U.S.,« confirms Martin H. Richenhagen. He is a German and the CEO of AGCO, an agricultural equip ment company with annual revenue of US$8 billion headquartered in the small town of Duluth, Georgia. But the trend is shifting, he says.

Global rethinking

That’s because global rethinking began after the collapse of the new economy and then the financial markets. Entire national economies are again looking to industry – the second sector – with its unspecta cular but steady growth and its creation of real value and secure jobs.

Gene Sperling, Director of the National Economic Council and Assistant to the President for Economic Policy, has described the decline of industrial employment in the U.S. as a national problem of the first order. But they are already well on their way to solving that problem: American industry has grown by more than ten percent annually and has created 500,000 jobs since early 2010.

Germany doesn’t need such a fundamental rethinking. It has always believed in its industry and in a strong »Mittelstand,« its small and mediumsized companies. Germany was still being mocked as a stodgy European problem case in the 1990s, but today the rest of the world envies Germany’s large share of the world’s industry. »Germany has always made sure that key industries stayed in the country – even as costs rose,« AGCO chief Richenhagen says approvingly.

India has high hopes for manufacturing

Things look different in India, which has not experienced much industrialization since it became independent. That’s no surprise, because the country originally hoped to develop

China International Marine Container (CIMC), an industrial company with 63,000 employees on six continents, manufactures tank containers, tank trucks, and pressure vessels for production plants at its Nantong location on the east coast of China. Quality is more important than quantity for CIMC, which complies with the strictest international standards. The Chinese government increasingly sees manufacturing highquality products as the way to keep pace with international competition. The previous Chinese formula for success – manufacturing simple products on a large scale, or merely assembling products – is now considered outdated.

»

13Industry Journal | 01 | 2013 | Markets

and manufacturing has caused all process steps to merge into one unit, instead of being performed sequentially. This ranges from design to production planning, engineering, and manufacturing to services. The result is greater efficiency, shorter times to market, and increased flexibility.

Wage costs less important

This technological convergence is increasing productivity so much that factors like wage or transport costs become less important in comparison. This also makes production in Western economies competitive again. And new technologies are offering emerging markets the opportunity to manufacture effi ciently and flexibly from the outset, putting them on an equal footing with their global competi tion. However, economic opportunities also involve some risk: Companies that don’t join this

ing domestic demand and the effort of multinational companies to find alternatives to China as a place to do business could help India achieve its objective.

This paradigm shift knows no national boundaries. Severe, radical changes to industry are a key issue in almost every country. »It doesn’t matter whether a national economy wants to keep its industry competitive or bring it back into the coun try – this turnaround offers an opportunity for all companies,« says Siegfried Russwurm, CEO of the Industry Sector at Siemens.

In the final analysis, companies like his first unleashed the current rediscovery of industry with their technological developments. A clear trend toward connecting powerful industrial software and ultramodern hardware has taken shape in industry over a period of just a few years. Digitization of product development

There is more expertise embedded in a ton of computers than in a ton of metal ore.«

»

Ricardo Hausmann, Professor of the Practice of Economic Development at Harvard University

directly from an agrarian society into a service economy.

But the Indian government has now understood that the service sector alone cannot help the country make broad economic progress and it won’t offer enough wellpaid jobs. That led to the development of the National Manufacturing Policy (NMP), a plan for industrial growth.

National Investment and Manufacturing Zones will be created all over India. They will have modern infrastructure and be subject to less stringent regulations while being required to meet strict environmental standards. The goal is for automation to increase productivity and improve quality, in small and mediumsized companies as well as large enterprises. NMP is projected to increase the manufacturing industry’s share of GDP from its current level of 16 percent to 25 percent by 2025. That’s an ambitious goal, but grow

»

Industry Journal | 01 | 2013 | Markets14

The governments of emerging countries are also pinning their hopes on producing highquality products. That’s the right thing to do, says Ricardo Hausmann, Director of the Center for International Development and Professor of the Practice of Economic Development at Harvard University. He says that this increases value creation and allows greater scope for differentiation by national economies.

What is the advantage for emerging countries of producing high-quality products compared with inexpensive mass produc-tion?

As products become more complex, the possibilities of variation grow exponentially. There are many more varieties of chairs than of cocoa beans, and there are many more possible varieties of airplanes than of chairs. As your products involve

more knowledge, there is more scope for differentiation.

What should emerging countries pay special attention to in indus-try’s new orientation?

When we observe how countries develop, we tend to see that the new industries that succeed tend to be relatively close to the previously existing ones. It is easier to move from small jet aircraft to larger planes than it is to get there if you start with soybeans.

Does value creation grow as products get more complex?

We have determined that this correlation does in fact exist. More complex products are more valuable and more complex economies create more value. There is more expertise embedded in a ton of computers than in a ton of metal ore, and the

price per ton reflects that. There are no rich countries that export primarily coffee, and no poor countries that export primarily medical imaging equipment.

How does a strong industry that produces increasingly complex products affect a country’s service sector?

Among other things, manufacturing requires accounting and auditing services, design, marketing, legal advice, investment banking, advertising, wholesale and retail distribution, and postsale services. It is all part of the same value network – it is not a different economy. A country with a strong manufacturing sector will have a complex service sector that an economy without manufacturing will not have. The distinction between services and manufacturing is collapsing as the value network is divided and globalized.

The »virtual machine« at INDEX, a lathe manufacturer in Southern Germany, is a digital twin of the real machine. Using it can reduce runup times by more than 80 percent and increase production by almost ten percent during ongoing operation. This is one reason why INDEX is a successful manufacturer in highwage Germany.

15Industry Journal | 01 | 2013 | Markets

When developing and manufacturing vehicles, glass, paper, machines, or pharmaceuticals, using industrial IT and industry software and ultramodern hardware to digitize and interlink all production steps can increase productivity so much that factors like wage and transportation costs become less important.

hightech revolution in time could soon miss out.

VDMA, the German Engineering Federation, estimates that IT and automation currently account for 30 percent of the manufacturing costs involved in machine building. The market for industrial software in the strict sense will grow by some 70 percent to €28 billion from 2012 to 2018, according to experts. That doesn’t count the world market for industrial software in areas such as logistics, security, and energy management, which total another €100 billion or more.

New forms of manufacturing are also changing job descriptions – and pay levels. Industry is increasingly seeking qualified employees who also know how to use software to control complex processes. Industrial workers no longer wear overalls while manufacturing highquality products, and the tools of their trade are now tablet computers.

Crisis-resistant sector

National economies and companies that successfully adjust to this transformation will gain an obvious international competitive edge. For example, the manufacturing industry is far more resistant to economic bubbles than the service sector. »The barrier to entry is higher than for Internet companies,« explains Thomas Menze, senior consultant at the ARC Advisory Group, a technology research firm. He says that someone who wants to create a Web startup doesn’t need much more than a desk, a computer, a phone, and an idea. »But someone who wants to build an industrial enterprise will have to buy machines and ensure that the location is connected to global logistics flows,« says Menze. That costs a lot of money and protects against investing in business models that can’t be rationally justified.

Industry also creates a large number of wellpaid jobs. One industrial job

Industry Journal | 01 | 2013 | Markets16

chains and a good environment for innovation.

»German industrial companies took the crisis of the mid1990s as an incentive to focus strictly on innovative technologies with comprehensive investments in research and development,« says Lichtblau. There was no question of dismantling the industrial base on a large scale, he said, adding that the country could look back on almost two hundred years of industrial history. The result of such deep roots: Between onequarter and onefifth of the German GDP – the values vary according to the source and the calculation method – is earned by the manufacturing industry. That is far above the international average.

U.S. profits from natural gas

The United States is currently in a particularly comfortable situation where reindustrialization is concerned. Huge deposits of domestic shale gas are soon likely to make the country mostly independent of the world market (see box on page 19). Abundant supplies have already affected the price of natural gas. It is about twothirds lower in the U.S. than in Germany, for example – which has massive effects on production costs.

Boston Consulting Group assumes that by 2015 manufacturing by U.S. industry could be 15 percent less expensive than in Germany or France and as much as 21 percent less expensive than in Japan. China would be only about seven percent less expensive by then, which hardly tips the balance compared with the other costs that are relevant to manufacturing. Factors influencing those costs – which in turn influence the reshoring plans of U.S. companies – include shorter transport distances, fewer customs formalities, greater protection against counterfeiting, and better quality assurance.

almost always has multiple jobs at suppliers’ or service providers’ businesses depending on it. The manufacturing industry is closely linked with other economic sectors, making it an engine for the entire economy. This also distributes prosperity more evenly. And wages and salaries in industry also ultimately prime the pumps of the domestic market. »This makes industry a guarantor of growth and stability,« says ARC consultant Menze.

»The manufacturing industry is the germ cell in a long value chain with enormous potential for employment,« confirms Gordon Riske, an American who is CEO of Kion Group, headquartered in Wiesbaden, Germany. Kion has 20,000 employees and operates internationally, manufacturing forklifts, warehouse technology, and industrial trucks.

The value chain starts with supplier companies, which are now closely involved in research and development, says Riske. »And it extends to the services related to our products that we provide to our customers.« He adds that modern IT connects these flows of products and data.

A good image in Germany

Riske praises the fact that manufacturing companies are highly esteemed in Germany. Karl Lichtblau, managing director of IW Consult, a subsidiary of the Cologne Institute for Economic Research, agrees: »Germany has a strong industry, which in turn profits from unusually advantageous background conditions in the country.«

Lichtblau and his colleagues studied the quality of 45 countries as business locations from the viewpoint of industry (see table on page 19). Germany was rated No. 5, scoring for wellestablished infrastructure, legal security, a high level of education, and stable supplies of energy and raw materials. Other factors were functional labor relations and value

»

Three questions for …

… Helmuth Ludwig, CEO North America at Siemens Industry

How important is the industrial renaissance for the United States?

Potentially very important. There is a broad based conversation going on in the U.S. about the future of manufacturing. Structural economic shifts have made manufacturing investment in the U.S. more attrac tive for companies in traditional manufacturing geographies and in emerging U.S. manufacturing »hubs.« An important example is the oil and gas industry and its investments in unconventional gas recovery.

What does this mean for manufacturers?

This is a moment of choice for many manufacturers. They are holding unprecedented levels of cash while looking at aging manufacturing infrastructure. While the catalyst for investment may be lower energy costs in the U.S. and growing manufacturing costs overseas, companies want to be cer tain that their investments will position them for longterm leadership. This is where we can help.

How can Siemens Industry help in this context?

As a technological pioneer, our vision is rooted in our customers’ future success. An example is our ongoing investment in the integration of industrial software with our product portfolio. As such, our products, solutions, and services help companies take better products to market and get them there faster.

17Industry Journal | 01 | 2013 | Markets

facturing one series of its computers in the U.S. again. Harold Sirkin of Boston Consulting expects the U.S. economy to grow by some US$20 billion to US$55 billion per year based solely on homecomings like this.

Countries like China will lose jobs as a result. China currently earns more than onethird of its GDP from manufacturing, primarily making relatively simple goods or assembling products that were developed in other countries.

China will have to find a way to cope with rising wages at home and reindustrialization in the West. »Think of the textile industry. It moved from Europe to China because wages were lower there – and now most of it has left that country again because production was no longer profitable,« says Thomas Döbler, a partner at Deloitte and coauthor of The Future of Manufacturing, a report for the World Economic Forum.

But China foresaw this trend and has taken precautions. Back in 2011, the Chinese government announced in its fiveyear plan that it would focus on manufacturing highquality products using ultramodern automation technology at a worldclass level. For example, Foxconn, a computer maker, recently announced that it would be using more robots for production.

The experts at Deloitte say that the Chinese economy is currently very interested in developing higher quality, more complex manufac turing and products to stimulate value creation. »Simple reproductions like those they previously made won’t get them any farther,« says Döbler.

Some American states, especially in the South and Southwest, could soon become some of the least expensive production sites in any industrialized country for that reason. Another reason: After years of seeing industry dismantled, American trade unions are ready to compromise and are calling for only modest wage growth.

As many as three million new jobs could be created in the United States in the coming years. Tapping the new sources of energy would directly and indirectly increase economic growth by two to three percent.

Costs rising in China

Falling costs at home isn’t the only reason U.S. companies are finding that it pays to bring production for the domestic market back from lowwage countries like China. Manufacturing is also getting more expensive there – in particular, due to rising pay levels. »Since 2001, wages and salaries in China have risen 15 to 20 percent – per year,« reports Harold L. Sirkin, a senior partner at Boston Consulting. The firm also assumes wage costs will continue to increase by about 18 percent annually in the coming years.

The list of American companies that are returning from other countries is already getting longer. For example, the sports equipment maker WhamO has shifted parts of its Frisbee manufacturing operation back to the U.S. Watts Water Technologies, a manufacturer of pipes and valves, is moving out of Asia and expanding in the state of New Hampshire.

Even the computer giant Apple has announced that in 2013 it plans to invest US$100 million in manu

Reindustrialization could create as many as three million jobs in the United States over the next few years. U.S. industry has added 500,000 jobs since early 2010.

Industry Journal | 01 | 2013 | Markets18

Promoting innovation

The Chinese government has pinpointed seven key industries ranging from biotechnology to machine and plant building for industries like aviation and telecommunications. Companies in those sectors will receive tax breaks for investments in research and technology and for using environmentally friendly manufacturing methods.

The densely populated regions along China’s coasts will be upgraded from »workshops« to hightech production centers. China plans to move more of its simple assembly work further inland to the western provinces – simultaneously developing more lowwage locations and promoting the economic development of remote areas. Many production facilities have already moved from more expensive locations like the Pearl River Delta to provinces where costs are lower.

In other words, lowwage manufacturing is on the move in China. And wages are already rising in smaller emerging countries. »The traveling circus must come to an end at some point. The last regions with low wages and acceptable background conditions have already been developed,« says Döbler.

The race for new lowwage locations can be a matter of indifference to companies that focus on highquality manufacturing and products. »A company that now invests in modern, efficient production technology can profitably manufacture products in industrialized countries and conserve resources over the next few decades,« says Siemens Industry CEO Russwurm. Now is the time to prepare for this trend.

Energy for the U.S. The United States has large deposits of shale gas in clay. Extracting it is more expensive and technically challenging than extracting conventional natural gas. The process, known as fracking (hydraulic fracturing), injects a mixture of water, chemicals, and sand into rock to release the gas.

The largest shale gas field in the U.S. is located directly south of the traditional industrial center in the Northeast. At least 30

petrochemical plants will be built there and in other economically underdeveloped regions over the next five years. Shell plans to spend US$2 billion to build a cracker in the old steelmaking region of Pennsylvania. The plant will break down natural gas into ethylene, which can then be used to make plastic products.

There are shale gas deposits in other countries, too. Gas companies are exploring for potential deposits in Poland and Scandinavia. But environmental concerns are thwarting plans to tap deposits in densely populated parts of Europe. Past experience indicates that yields are too low while the risks and costs are too great.

The best industrial locations in the world

Country 2010 rank 1995 rank Index value 2010*

U.S. 1 1 136

Sweden 2 4 132

Denmark 3 5 131

Switzerland 4 7 129

Germany 5 14 128

Australia 6 10 128

The Netherlands 7 2 127

Canada 8 3 127

Norway 9 8 126

Japan 10 12 126

Finland 11 13 122

Austria 12 15 122

Great Britain 13 6 121

Italy 14 9 120

New Zealand 15 11 118

* Average of all countries studied = 100Source: Cologne Institute for Economic Research, IW Consult

The Cologne Institute for Economic Research measured the quality of 45 countries as business locations from the viewpoint of industry. Analysts collected and weighted 58 indicators for their quality of labor relations, human capital, infrastructure, and inno vative strength and combined them in an index.

19Industry Journal | 01 | 2013 | Markets

Strengthening domestic industry is being pushed on many levels in the U.S. Industry

Journal spoke to Anthony Foxx, Mayor of Charlotte and head of the Task Force on

Advanced Manufacturing of the U.S. Conference of Mayors, about modernization

initiatives, the weak image of the industrial sector, and the competition among cities

and regions.

Manufacturing should come back to the U.S.«

»

Mayor Anthony Foxx as a guest speaker at Power2Charlotte, a municipal education initiative for more aware and more responsible energy consumption.

Industry Journal | 01 | 2013 | Markets20

Mayor Foxx, the United States is still the world‘s biggest industrial nation. However, about five mil-lion jobs were lost during the last decade. What has happened?

The United States has had several challenges with manufacturing, not the least of which is the relative lowcost manufacturing off United States shores. During the past 20 or 25 years, there was an exodus of U.S. companies that went overseas, having a huge impact on the American jobs front. But today there‘s an opportunity for us to reemerge as a manufacturing nation.

Because labor costs in Asia are rising?

Yes, in part. But also because locally we do everything to qualify workers for advanced manufacturing jobs. We try to improve their vocational skills so that they can take up positions beyond traditional areas of work. Education and vocational training are two main points in our endeavor to incentivize companies to come back to the U.S.

You are chairman of the new Task Force on Advanced Manu facturing of the U.S. Conference of Mayors. This team is supposed to promote modern industrial production. What are your plans?

We want to develop a bestpractice model – a kind of toolbox local politicians can use to mobilize resources that support their industries; activities such as partnerships of colleges and universities with the private sector, or infrastructure improvements from air and rail traffic all the way to the mechanics of moving goods around. Even though the latter are national tasks, we mayors want to press ahead with them.

How can a best practice model work? Mayors compete with each other, don’t they? So they’re prob-ably not really interested in having

their neighbor successfully foster investments.

That’s true. In a way, we’re competitors, the mayors, the cities, the Federal states. But it’s obvious that in certain regions particular industries grow faster than elsewhere. Concentration on highquality products is no uniform model, of course. Different regions have different strengths. For instance?

The Southeast, we here in Charlotte, is a growing location for energy companies. That’s why Siemens is based here. The company has considerably extended its plants and more than doubled the number of jobs. This could serve as a model for publicprivate cooperation with the aim of further developing this kind of industrial production. Other regions, on the other hand, are strong in car manufacturing or in information technology. North Carolina probably won’t pay as much attention to the automobile industry as Michigan. It comes down to each locality having a sense of where its strengths are.

How can such a division of labor work?

One of the big messages that is likely to come out of this is that we really have to move in clusters. There will be clusters in the Southeast, in the Midwest, and in the Northeast. Within these clusters there will be collaboration, among them competition. But with our work we’ll all contribute to pushing the sector as a whole. I see great opportunities in advanced manufacturing. What else is on your agenda when the task force will start work this year?

The basis is to number one orient our membership in what advanced manufacturing is because people will be coming into the room with

Anthony Foxx Since December 2009, the lawyer Anthony Foxx has been the mayor of Charlotte. Elected at the age of 38, the Democrat is the youngest mayor in the history of the metropolis. Earlier in his political career he held a council seat and specialized on traffic planning and business development. One of his main objectives is the reduction of unemployment. Since the beginning of his tenure it has gone down from eleven to nine percent.

»

21Industry Journal | 01 | 2013 | Markets

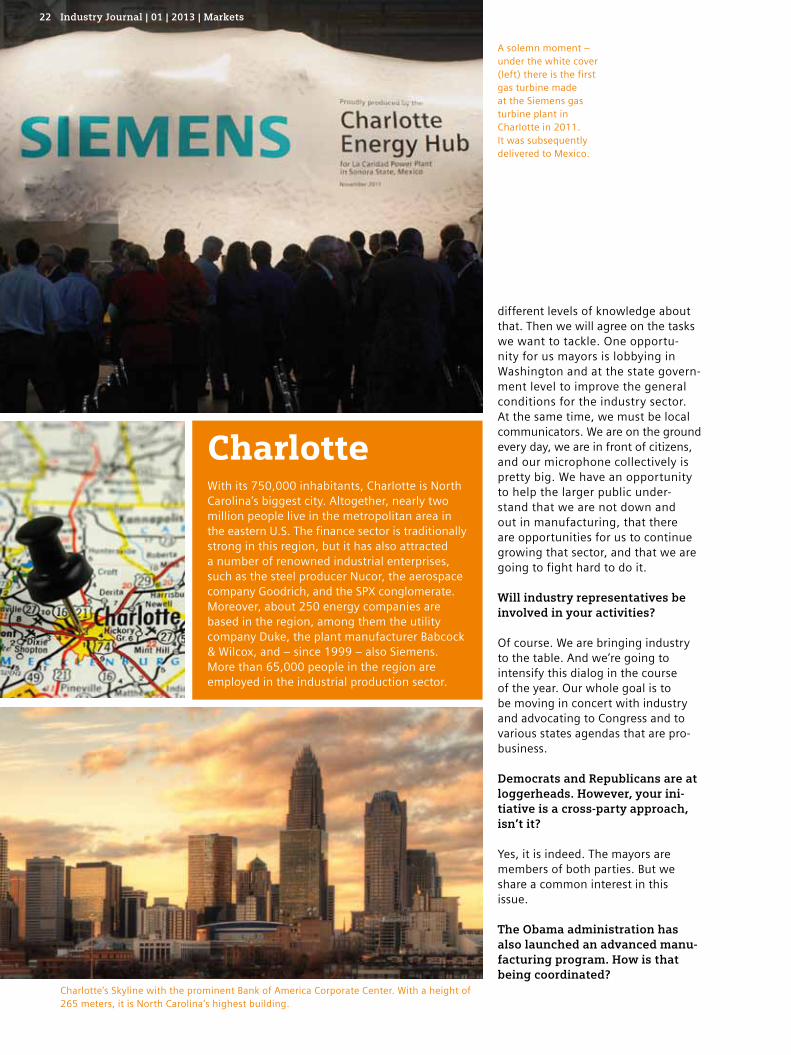

A solemn moment – under the white cover (left) there is the first gas turbine made at the Siemens gas turbine plant in Charlotte in 2011. It was subsequently delivered to Mexico.

Charlotte‘s Skyline with the prominent Bank of America Corporate Center. With a height of 265 meters, it is North Carolina’s highest building.

different levels of knowledge about that. Then we will agree on the tasks we want to tackle. One opportu nity for us mayors is lobbying in Washington and at the state government level to improve the general conditions for the industry sector. At the same time, we must be local communicators. We are on the ground every day, we are in front of citizens, and our microphone collectively is pretty big. We have an opportunity to help the larger public understand that we are not down and out in manufacturing, that there are oppor tunities for us to continue growing that sector, and that we are going to fight hard to do it.

Will industry representatives be involved in your activities?

Of course. We are bringing industry to the table. And we’re going to intensify this dialog in the course of the year. Our whole goal is to be moving in concert with industry and advocating to Congress and to various states agendas that are probusiness.

Democrats and Republicans are at loggerheads. However, your ini-tiative is a cross-party approach, isn’t it?

Yes, it is indeed. The mayors are members of both parties. But we share a common interest in this issue.

The Obama administration has also launched an advanced manu-facturing program. How is that being coordinated?

CharlotteWith its 750,000 inhabitants, Charlotte is North Carolina‘s biggest city. Altogether, nearly two million people live in the metropolitan area in the eastern U.S. The finance sector is traditionally strong in this region, but it has also attracted a number of renowned industrial enterprises, such as the steel producer Nucor, the aerospace company Goodrich, and the SPX conglomerate. Moreover, about 250 energy companies are based in the region, among them the utility company Duke, the plant manufacturer Babcock & Wilcox, and – since 1999 – also Siemens. More than 65,000 people in the region are employed in the industrial production sector.

Industry Journal | 01 | 2013 | Markets22

We have had some initial discussions with the administration about how to partner and help each other to advance this issue. Government representatives join our Task Force meetings. The American nation is making a big effort to develop industry further. We know this will take a lot of hard work and a lot of focus and a lot of talking to each other but we are ready to get going.

Many school graduates don’t even consider a career in manufacturing. Is the public image of the sector really that bad?

The image is even worse than the actual situation. You see thousands and thousands who may or may not have completed high school but who are working on jobs that are lowskill jobs but pay decent wages and allow that person to buy a house and take care of his or her family. Those folks haven’t gone away. And in advanced manufacturing, job requirements as well as wages are higher. And I do think it’s changing. Nothing focuses the mind like a doubledigit unemployment rate.

Do companies, small and medium-sized enterprises in particular, have to cooperate closer with high schools and colleges in order to find suitable graduates?

Absolutely. We have absolutely got to connect our young people to these promising career paths. This is going to require a different approach. When I came into the mayor’s office in 2009 we had the legal basis to create a Youth Work

force Development Board, but we hadn’t done it. I made sure we did it. And one of the most important tasks of the new board was a suitable conveyance of industry job opportunities. Once they see the opportunity, they can aspire to it, but if they never see it they won’t.

Which industrial sectors do you expect to benefit in particular from the regional and national initiatives?

Probably the carmaking and computer sectors. It’s not without reason that Apple has announced to return part of the Mac production back to the U.S. Another sector that is often not taken into account is the healthcare business, which is usually regarded as a service business. But many medical products are produced on an industrial scale. These are only a few examples. In Charlotte, I will consult my business community and we will see which sectors employ most people. And the question will be: how we can grow those sectors.

Why should globally active in-dustry giants be interested in strengthening the position of the U.S. as an industrial location at all?

Competition is the biggest source of savings for companies in many situations. The stronger and more competitive the U.S. manufacturing sector is, the better global companies will do. The U.S. will not win every future competition for employment, but a major world player is back in the game.

Nationalalliance for industryThe United States Conference of Mayors, founded in 1932, is a powerful crossparty advocacy body based in Washington, D.C. It represents cities with more than 30,000 inhabitants and currently has some 1,300 members.

In September 2012, the U.S. Conference of Mayors established a task force to support socalled advanced manufacturing from 2013 on – modern, capital intensive industrial production. Shortly after the reelection of the Obama administration, the chairman of the Task Force on Advanced Manufacturing, Anthony Foxx, met Secretary of Labor, Hilda Solis, and Trade Secretary in office, Rebecca Blank, to develop a mutual industrial policy strategy.

23Industry Journal | 01 | 2013 | Markets

Production for the people

Smaller than a milk crate: Bre Pettis, founder of MakerBot in the U.S., can easily lift the Replicator 2, one of the company’s 3D printers.

Industry Journal | 01 | 2013 | Markets24

The future is already here. At a small store with white walls and a cracked stone floor in New York’s trendy SoHo neighborhood, they’re busily at work – black devices about the size of scanners whose print heads whiz back and forth. These are replicators, and they print toy cars. Or apples. Or wrist bands. Not on paper, though: These are real threedimensional plastic objects.

The man some have dubbed the new Steve Jobs stands behind the counter. He’s wearing hipster glasses with black rims and a dark gray shirt over jeans. »Welcome to the revolution,« says Bre Pettis, founder of the MakerBot company and a new star on the horizon. He and one of his replicators were recently featured on the cover of Wired, a technology magazine. »This machine will change the world,« says the headline. Pettis explains why. In a few years every home will have a 3D printer, and we will be able to make objects just as easily as we print out text today.

What may have seemed like a crazy vision of the future just a few years ago is now becoming a reality. Tens of thousands of 3D printers are at work in homes and engineering firms, hobbyists’ workshops, and research laboratories. And that’s just the beginning. Terry Wohlers, an

industry expert from Fort Collins (Colorado, USA), predicts annual growth of about 30 percent and estimates that sales of additive manufacturing equipment will reach US$3.7 billion by 2015. Exciting times are ahead, according to Digital Trends, a tech nology magazine. That’s what’s known as hype.

Print your own spare parts

In technical terms, 3D printing is relatively simple. A material, usually plastic, is liquefied and successively laid down in very thin layers according to a digital model. That model can be downloaded – or you can design your own. This idea is captivating to consumers. If the temple of your glasses breaks, you can find the design on the Internet and print out your own replacement. Kids can make the toys they want. If you lose a button, just replicate a new one.

Can life really be that simple? »From the beginning we’ve faced the problem that people think of this as science fiction,« says Pettis. »That’s why we opened the store.« He opens the sliding door of a stall that looks like a photo booth. But instead of your picture, there is a 3D scan, and the result is printed out on a 3D printer. Your own personal minibust, which can be infinitely replicated.

The use of three-dimensional printers to manufacture

products was once limited to industry. As prices fall,

3D printers are now capturing the mass market. This

is the beginning of a major trend. It is also benefiting

manufacturing plants, which are increasingly using 3D,

also known as additive manufacturing.

»

25Industry Journal | 01 | 2013 | Markets

A huge number of printers are already available. Most manufacturers are small, owneroperated companies. Steve Wygant heads SeeMeCNC, a fiveperson company in Goshen (Indiana, USA). He made the move from routers to 3D printers in the fall of 2011 and sold more than 500 units within a year. Wygant found this to be »phenomenal.« He took a new model to the World Maker Faire in 2012 and had soon pocketed orders worth almost US$80,000.

Models from the Internet

The market leader MakerBot is in another league. Pettis’s company has sold more than 15,000 printers since it was founded in 2009. It received US$10 million in venture capital in August 2011, including from Amazon founder Jeff Bezos. That makes it possible to run the expensive store in SoHo as well as the »Thingiverse« Web site. The site offers thousands of digital designs for 3D printing – free of charge. The aim is to increase customer loyalty before the big boys like HP or Brother discover this area for themselves. »MakerBot is at the point where Apple was 30 years ago, when desktop publishing got popular,« says industry insider Chris Anderson, for many years the editorinchief of Wired (see interview on page 28).

The technology still leaves something to be desired, however. The printers are still very slow – it takes hours to finish a saucer. They can print only relatively small plastic parts in one color. If the resolution is too low, the surface of an object will be rough. That will change. But it’s still doubtful whether the application will ever offer quality as high as that of indus trial production, and it probably won’t be as convenient or inexpensive, either. The Gartner research firm predicts that 3D printing will not be ready for the mass market for more than five years.

»The public can access this manufacturing process here for the first time,« says Pettis.

The public can also thank Neil Gershenfeld, a professor at MIT, the Massachusetts Institute of Technology in the United States. He is a physicist who in 2001 began 3D production for scientific purposes at the Center for Bits and Atoms. But there was overwhelming demand from students, who simply wanted to make something, anything. Gershenfeld came up with the idea of the smallscale workshops known as FabLabs. Today there are some 100 FabLabs all over the world, from Takoradi, Ghana, to Jalalabad, Afghanistan.

Those early efforts have long since become the global phenomenon known as the maker movement, which is committed to the principles of open source. Instructions, designs, plans for 3D printers and all are distributed free of charge. An entire cosmos has been created in this way, including doityourselfers and professionals, the avantgarde and their imitators, and special online marketplaces. The industry also holds special gettogethers, the Maker Faires.

High-tech for all

The World Maker Faire in New York clearly shows how rapidly this trend is developing. Only two companies with 3D printers attended in 2010, and there was little interest. Almost 30 companies attended in 2012, and parents and children pushed their way into the 3D Printer Pavilion. Kids who grow up with smartphones and tablets think hightech crafts are cool. And they’re also increasingly affordable. If you want to put together your own printer, you can get a kit for less than US$600. A readymade Replicator 2 by MakerBot costs about US$2,200.

15,0003D printers since 2009.

Market leader MakerBot

has sold more than

Industry Journal | 01 | 2013 | Markets26

Super-flexible manufacturing

What seems revolutionary for consumers is old hat to industry, which has been experimenting with additive manufacturing for 30 years now. It takes longer than conventional casting or stamping methods and is expensive for large batch sizes, but it allows extreme flexibility and customization.

The technology has already made its breakthrough in the area of prototype construction. Now, carried along by hype, it’s attempting to conquer the production floors. »This is a paradigm shift for manufacturing technology,« says Adrian Keppler, CEO of EOS GmbH in Krailling (Germany), a world leader in integrated emanufacturing solutions for industrial applications. Keppler is a specialist in laser sintering who since 1989 has been preaching the need for engineers to move away from conventional thinking, with design and construction still focused on established production methods. »We are casting off those bonds and in the future will be able to make innovative, functionally integrated parts,« Keppler promises.

More efficient structures are possible once CAD design joins the process. Those structures offer weight reductions of as much as 70 percent in lightweight construction. Professional applications are also able to handle materials that can’t be cast. In contrast to 3D printers for home use, industrial printers can work with weldable alloys like titanium and cobalt. Emanufacturing is everyday fare in aircraft manufacturing, medical technology, and mechanical engineering. MTU, EADS, Daimler, and BMW are all customers of EOS.

Funded by Obama

But Keppler says this is just the beginning: »At least half the major

»

The Replicator 2 by MakerBot (top) will fit on any desk. Highresolution 3D printers can make model cars or functional gearboxes (center left) or desk lamps with hinged bases (center right). The 3D Photobox by MakerBot (bottom) makes a threedimensional scan of the torso. Customers can then use the data to create busts of themselves.

27Industry Journal | 01 | 2013 | Markets

Companies don’t have to do every-thing themselves.«Interview with Chris Anderson, for many years the editor-in-chief of Wired magazine and a mover and shaker in the maker movement.

How revolutionary is production for the people?

3D printing and cloud manufacturing – access to factories over the Internet – is nothing new for the industrial world, but it is for individuals. It’s like with computers, which were at first used only professionally. It wasn’t technology that changed the world, but rather the democratization of technology.

Will this threaten the business model of industry?

Not on a large scale. However, many small manufacturers will be created that will produce things that large companies don’t want to or can’t make. The Internet wasn’t a threat to companies, either, but businesses and individuals profited from it equally, and the result was new business areas. The development of industrial production will advance the same way.

For example, for procuring spare parts?

That’s not a major business. How many spare parts do you actually buy? What’s much more interesting for established companies is the open innovation model – the idea of sharing inventions and continuing to develop them in communities.

How can companies profit from that?

Take a product and make the digital design available to your community. Let me mix it, improve its functions, and invent new accessories. You don’t have to do everything yourself if you allow your customers to contribute to value creation.

A car from a printerDrivAer offers a good example of how prototyping can be used by industry. The name may be a neologism, but this is a realistic model of a car. It was developed by Audi and BMW in collaboration with the Technical University of Munich (Germany), with the goal of performing accurate flow testing in wind tunnels.

The model, made of plaster and epoxy resin and just 1.20 meters long, was meticulously developed in the 3D laboratory based on real vehicles. More than 60 sensors measure air resistance. The simulation offers considerable advantages over the conventional Ahmed body. It is too far removed from reality, for example, because it doesn’t have a mirror or a fastback.

»

A feel for technology trends: Chris Anderson

Plaster is faster: The digital prototype is first generated at different levels of detail (top) and then printed as a real model made of plaster and epoxy resin for testing in wind tunnels (bottom).

Industry Journal | 01 | 2013 | Markets28

Perhaps the fears are as exaggerated as the hopes. »Glowing articles about 3D printers read like the stories in the 1950s that proclaimed that microwave ovens were the future of cooking,« says FabLab creator Neil Gershenfeld. Of course, today we know that »microwaves are convenient, but they don’t replace the rest of the kitchen.«

The future has begun

Whether they are critics or fans, experts agree that everything that has happened so far is just the beginning. Biotechnology companies are already testing whether it will someday be possible to print organs, using stem cells as the raw mate rial. At the University of Glasgow, chemistry professor Leroy Cronin is experimenting with a 3D printer that can mix different medications from a single set of active ingredients. And Gershenfeld is developing a 3D assembler for atom clusters that can be used to integrate sensors and circuits into a 3D product. The future has just begun.

industrial companies have additive manufacturing on their radar.« And EOS is not alone. Internationally listed companies, including the American printer manufacturers Stratasys and 3D Systems, are heavy hitters on the market. And U.S. President Barack Obama considers the technology to be so promising that his administration has invested US$30 million in a National Additive Manufacturing Innovation Institute.

The consumer and B2B sectors can inspire each other when developing additive manufacturing technologies. It’s likely they will also have to work together to solve a major problem: piracy. The open source community is willing to share free of charge. But companies can’t allow their designs to be copied for free over the long term. Many design plans are on the Internet, and 3D scanning can be used to copy almost every shape. Strategies for controlling digital rights, such as copy protection, are considered impracticable because the market is so fragmented.

At least half the major industrial companies have additive manufacturing on their radar.«

»

Adrian Keppler, CEO of EOS GmbH

Glossary

Additive manufacturing

A process in which products are produced by laying down materials in thin layers. Its opposite, subtractive manufacturing, involves first stamping out or casting products and then finishing them.

FabLab

Fabrication laboratory, or »fabulous laboratory.« A workshop for individuals and small companies equipped with 3D printers, laser cutters, and milling machines.

Rapid manufacturing

CADbased manufacturing of products using 3D printers; usually highquality, custom products suh as injection molds or prostheses.

Rapid prototyping

CADbased manufacturing of models using 3D printers, including models for conventional series production.

29Industry Journal | 01 | 2013 | Markets

The manufacturing imperativeAn essay by Dani Rodrik

Countries jeopardize their competitive edge as well as jobs and their political stabil-

ity when they neglect the importance of domestic production, says Harvard econo-

mist Dani Rodrik. He takes up the cudgels for manufacturing industries and warns

against an overestimation of the service sector.

Industry Journal | 01 | 2013 | Markets30

We may live in a postindustrial age, in which information technologies, biotech, and highvalue services have become drivers of economic growth. But countries ignore the health of their manufacturing industries at their peril.

Hightech services demand specialized skills and create few jobs, so their contribution to aggregate employment is bound to remain limited. Manufacturing, on the other hand, can absorb large numbers of workers with moderate skills, providing them with stable jobs and good benefits. For most countries, therefore, it remains a potent source of highwage employment.

Indeed, the manufacturing sector is also where the world’s middle classes take shape and grow. Without a vibrant manufacturing base, socie ties tend to divide between rich and poor – those who have access to steady, wellpaying jobs, and those whose jobs are less secure and whose lives are more precarious. Manufacturing may ultimately be central to the vigor of a nation’s democracy.

The United States has experienced steady deindustrialization in recent decades, partly due to global competition and partly due to technological changes. Since 1990, manufacturing’s share of employment has fallen by nearly five percentage points. This would not necessarily have been a bad thing if labor productivity (and earnings) were not substantially higher in manufacturing than in the rest of the economy – 75 percent higher, in fact.

The service industries that have ab sorbed the labor released from manu facturing are a mixed bag. At the high end, finance, insurance, and business services, taken together, have productivity levels that are similar to manufacturing. These industries have created some new jobs, but not many – and that was before the financial crisis erupted in 2008.

The bulk of new employment has come in personal and social services, which is where the economy’s least productive jobs are found.

This migrat ion of jobs down the productivity ladder has shaved 0.3 per centage points off U.S. produc tivity growth every year since 1990 – roughly onesixth of the actual gain over this period. The growing proportion of lowproductivity labor has also contributed to rising inequality in American society.

The loss of U.S. manufacturing jobs accelerated after 2000, with global competition the likely culprit. As Maggie McMillan of the Interna tional Food Policy Research Institute has shown, there is an uncanny negative correlation across individual manufacturing industries between employ ment changes in China and the U.S. Where China has expanded the most, the U.S. has lost the greatest number of jobs. In the few industries that contracted in China, the U.S. has gained employment.

In Britain, where the decline of manufacturing seems to have been pursued almost gleefully by Conservatives from Margaret Thatcher until David Cameron came to power, the numbers are even more sobering. Between 1990 and 2005, the sector’s share in total employment fell by more than seven percentage points. The reallocation of workers to less

productive service jobs has cost the British economy 0.5 points of productivity growth every year, a quarter of the total productivity gain over the period.

For developing countries, the manufacturing imperative is nothing less than vital. Typically, the productivity gap with the rest of the economy is much wider. When manufacturing takes off, it can generate millions of jobs for unskilled workers, often women, who previously were employed in traditional agriculture or petty services. Industrialization

The manufacturing sector is where the world’s middle classes take shape and grow.«

Dani Rodrik The 55yearold Professor of International Political Economy at Harvard University’s Kennedy School of Government is a leading scholar of globalization and economic development.

was the driving force of rapid growth in Southern Europe during the 1950s and 1960s, and in East and Southeast Asia since the 1960s.

India, which has recently experienced Chinese rates of growth, has bucked the trend by relying on software, call centers, and other business services. This has led some to think that India (and perhaps others) can take a different, serviceled path to growth.

But the weakness of manufacturing is a drag on India’s overall economic performance and threatens the sustainability of its growth. India’s highproductivity service industries employ workers who are at the very top end of the education distribution. Ultimately, the Indian economy will have to generate productive jobs for the lowskilled workers with which it is abundantly endowed. Much of that employment will need to come from manufacturing.

»

»

31Industry Journal | 01 | 2013 | Markets

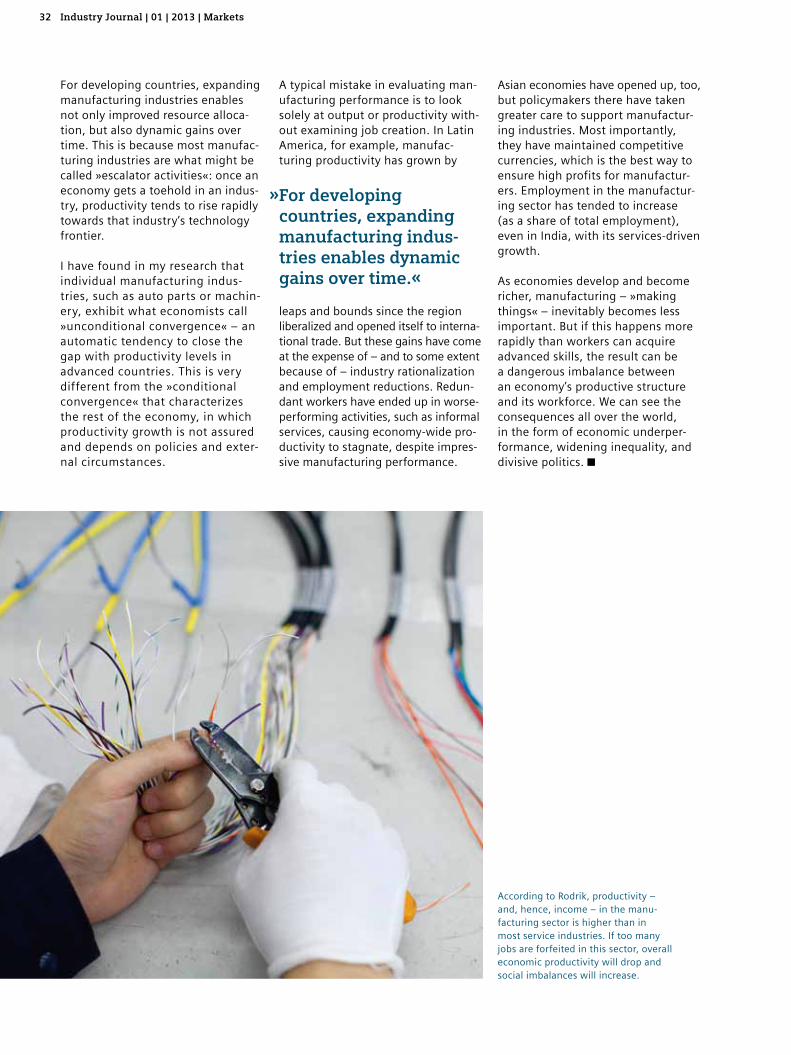

For developing countries, expanding manufacturing industries enables not only improved resource allocation, but also dynamic gains over time. This is because most manufacturing industries are what might be called »escalator activities«: once an economy gets a toehold in an industry, productivity tends to rise rapidly towards that industry’s technology frontier.

I have found in my research that individual manufacturing industries, such as auto parts or machinery, exhibit what economists call »unconditional convergence« – an automatic tendency to close the gap with productivity levels in advanced countries. This is very different from the »conditional convergence« that characterizes the rest of the economy, in which productivity growth is not assured and depends on policies and external circumstances.

A typical mistake in evaluating manufacturing performance is to look solely at output or productivity without examining job creation. In Latin America, for example, manufacturing productivity has grown by leaps and bounds since the region liberalized and opened itself to international trade. But these gains have come at the expense of – and to some extent because of – industry rationalization and employment reductions. Redundant workers have ended up in worseperforming activities, such as informal services, causing economywide productivity to stagnate, despite impressive manufacturing performance.

Asian economies have opened up, too, but policymakers there have taken greater care to support manufacturing industries. Most importantly, they have maintained competitive currencies, which is the best way to ensure high profits for manufacturers. Employment in the manufacturing sector has tended to increase (as a share of total employment), even in India, with its servicesdriven growth.

As economies develop and become richer, manufacturing – »making things« – inevitably becomes less important. But if this happens more rapidly than workers can acquire advanced skills, the result can be a dangerous imbalance between an economy’s productive structure and its workforce. We can see the consequences all over the world, in the form of economic underperformance, widening inequality, and divisive politics.

According to Rodrik, productivity – and, hence, income – in the manufacturing sector is higher than in most service industries. If too many jobs are forfeited in this sector, overall economic productivity will drop and social imbalances will increase.

For developing countries, expanding manufacturing indus-tries enables dynamic gains over time.«

»

Industry Journal | 01 | 2013 | Markets32

Production comes homeAn essay by David Bosshart

Goods are increasingly being produced where they are purchased, says futurist

David Bosshart, CEO of the renowned Gottlieb Duttweiler Institute. He describes

the many signs of the trend toward re-regionalization in an exclusive essay

for Industry Journal.

The Western world sometimes feels like it’s running on a hamster wheel. Technical progress is moving faster than ever before, but it never gets ahead. Economic output, still the most important measure of a society’s prosperity, is growing – if at all – rather anemically. All of the money spent on research, development, and restructuring ends up making it just barely possible to stay in business.

But the feeling of running in place immediately shifts if you look at something other than pure economic data. Numerical growth may have

come to an end, and measuring affluence in terms of monetary units may have reached its zenith: peak wealth. But that doesn’t apply to people’s feeling of wellbeing or to the state of society. New technologies will succeed on the market if they promise additional benefits, thereby promoting structural change.

One characteristic of the coming structural change that is currently taking shape is the reregionalization of production. For thousands of years, goods were produced where the consumers of those goods lived.

Now, after two centuries of migration of production sites, they are moving closer to the people who use what they make.

In the 19th century, production was attracted to places where raw materials were available (such as the Ruhr region in Germany), and in the 20th century it moved where it could find the right workers – who were either particularly inexpensive, as in China, or particularly qualified, as in California, Germany, or Switzerland. Now the circle is closing: »Production is coming home.«

»

33Industry Journal | 01 | 2013 | Markets

Several current trends are behind this reregionalization:

• Narrowing of the global cost gap: Differences in labor costs all over the world are decreasing. In China, still the world’s factory, labor costs are increasing massively and will continue to do so due both to higher wages and improved working conditions. The caravans of laborintensive industries like textiles – which have moved from southern Europe to southeast Asia to China – will no longer be able to find such attractive destinations. And the narrower the worldwide cost gap, the less incentive there is to move production to places where labor costs are lowest.

• Higher logistical costs and risks: Globalization in the 1990s benefited from a decade of cheap oil, but that won’t be coming back anytime soon. The switch to renewable energy sources may one day lead to an era of cheap electricity, but it will be less favorable for ship ping than for manufacturing. And the disastrous tsunami in Japan in 2011 has reminded us that upheaval and turmoil in one part of the world can immobilize process chains all over the globe.

• Lower barriers to market entry: Digitization and the communication revolution have drastically reduced the competitive edge of experts, specialists, and veterans in many industries. Anyone who can sell muesli, lights, or custom computers online is avoiding the barriers to entering traditional markets. Capital requirements for new entrants are plummeting, which simultaneously increases opportunities for peer production, the trend that favors production among equals – and also among those who are located physically nearby.

Gottlieb Duttweiler Institute (GDI) in Rüschlikon, Switzerland, is named after the founder of the Migros retail chain, who created it in 1962.

Re-regionalization of products is a characteristic of structural change.«

»

Industry Journal | 01 | 2013 | Markets34

• Longing for originality: Studies by Gottlieb Duttweiler Institute on the values of consumers in Germany and Switzerland have for some years shown an increased longing for originality that cannot be satisfied by industrial mass production. This marks a return to craftsmanship and local value creation. Even if this longing is often not reflected in a corresponding shift in consumer behavior, it does point to a trend for production. If slow living becomes the new luxury, there will soon be slow living for all. Luxury has always invited imitation from below: today’s luxury is tomorrow’s bulk commodity.

• Bursting of the abstraction bubble: The American economist Robert Reich coined the term »supercapitalism« in the 1990s, meaning that companies tend to act more like analysts of symbols than producers and to outsource everything related to physical production. A decade later, the financial markets became a symbol of such abstraction when they dealt in derivatives of derivatives of derivatives – until investors lost first their grip on reality and then their money. Since that time, value has increasingly been physically created instead of abstractly destroyed.

• More individual products and shorter production cycles: The era when the fashion houses launched their collections only twice a year has long passed. Many clothing chains offer new items every month, or even every day. The same applies to other industries. Large producers are also relying less on trade shows to set trends, which are instead being multiplied on the street and in social networks. This can make demand harder to predict, so the supply side has to be able to respond faster. Shorter delivery times and logistical paths will increasingly offer a competitive edge.