redevelopment agency of the city of fremont (fremont

TRANSCRIPT

Thi

s P

reli

min

ary

Off

icia

l Sta

tem

ent a

nd th

e in

form

atio

n co

ntai

ned

here

in a

re s

ubje

ct to

com

plet

ion

and

amen

dmen

t. U

nder

no

circ

umst

ance

s sh

all t

his

Pre

lim

inar

y O

ffic

ial S

tate

men

t con

stit

ute

an o

ffer

to s

ell o

r th

e so

lici

tati

on o

f an

y of

fer

to b

uy, n

or s

hall

ther

e be

any

sal

e of

thes

e se

curi

ties

by

any

pers

on, i

n an

y ju

risd

icti

on in

whi

ch s

uch

offe

r, s

olic

itat

ion

or s

ale

wou

ld b

e un

law

ful p

rior

to th

e re

gist

rati

on o

r qu

alif

icat

ion

unde

r th

e se

curi

ties

law

s of

suc

h ju

risd

icti

on.

PRELIMINARY OFFICIAL STATEMENT DATED JUNE , 2011NEW ISSUE - Book-Entry ONLY DRAFT OF MAY 31, 2011 RATING:

Moody’s: “A2”Standard & Poor's: “A+”

(See “MISCELLANEOUS — Ratings” herein)

In the opinion of Quint & Thimmig LLP, San Francisco, California, Bond Counsel, subject to compliance by the Agency with certaincovenants, under present law, interest on the Bonds is excludable from gross income of the owners thereof for federal income tax purposes and isnot included as an item of tax preference in computing the federal alternative minimum tax for individuals and corporations, but such interest is takeninto account in computing an adjustment used in determining the federal alternative minimum tax for certain corporations. In addition, in the opinionof Bond Counsel, interest on the Bonds is exempt from personal income taxation imposed by the State of California. See “LEGAL MATTERS-TaxMatters” herein.

$134,720,000*REDEVELOPMENT AGENCY OF THE CITY OF FREMONT

(FREMONT MERGED REDEVELOPMENT PROJECT)TAX ALLOCATION BONDS, 2011 SERIES A

Dated: Date of Delivery Due: September 1, as shown on the inside cover

The Redevelopment Agency of the City of Fremont (the “Agency”) will issue its “Redevelopment Agency of the City of Fremont (FremontMerged Redevelopment Project) Tax Allocation Bonds, 2011 Series A” (the “Bonds”) under an Indenture of Trust dated as of June 1, 2011 (the“Indenture”) by and between the Agency and Union Bank, N.A., as trustee. The Bonds are special obligations of the Agency payable from and securedby Tax Revenues (as defined herein). The proceeds of the Bonds will be used by the Agency to finance redevelopment activities, in particular theacquisition of land for, and the design and construction of, the Irvington BART station, fund a reserve fund for the Bonds and finance costs of issuanceof the Bonds, all as described herein. The Bonds will be sold by the Agency to the Fremont Public Financing Authority (the “Authority”) andimmediately resold by the Authority to the Underwriters named below.

Interest on the Bonds is payable semiannually on March 1 and September 1 of each year, commencing March 1, 2012. Principal is payableon September 1 as shown on the inside cover. The Bonds will be issued as fully registered Bonds and will initially be subject to a book-entry system(as described herein) of registration and transfer. Under the book-entry system, the Bonds, when delivered, will be registered in the name of Cede& Co., as nominee of The Depository Trust Company, New York, New York (“DTC”). DTC will act as securities depository of the Bonds. Thebeneficial ownership interests of individual purchasers of the Bonds will be recorded through the records of a DTC Participant (a securities broker,bank, trust company, clearing corporation or certain other types of organization) in amounts equal to $5,000 or an integral multiple thereof. Individualpurchasers will not receive securities certificates representing their beneficial ownership interests in the Bonds purchased. The Bonds are subjectto optional and mandatory redemption as described herein.

THE BONDS AND ANY PARITY DEBT (AS DEFINED HEREIN) OF THE AGENCY ARE PAYABLE SOLELY FROM THETAX REVENUES (AS DEFINED HEREIN) ALLOCATED AND PAID TO THE AGENCY. THE BONDS ARE NOT A DEBT OF THECITY OF FREMONT, THE STATE OF CALIFORNIA OR ANY OF ITS POLITICAL SUBDIVISIONS, AND NEITHER THE CITY OFFREMONT, THE STATE OF CALIFORNIA, NOR ANY OF ITS POLITICAL SUBDIVISIONS IS LIABLE THEREFOR. THE AGENCYHAS NO TAXING POWER.

The following firm, serving as financial advisor, has structured this issue.

MATURITY SCHEDULE ON THE INSIDE COVER

The Bonds are being purchased by Goldman, Sachs & Co. and Morgan Stanley & Co. Incorporated as Underwriters. The Bonds will beoffered when, as and if issued and accepted by the Underwriters, subject to approval as to legality by Quint & Thimmig LLP, San Francisco,California, Bond and Disclosure Counsel and to certain other conditions. Certain matters will be passed upon for the Agency by its Special Counsel,Goldfarb & Lipman LLP, Oakland, California. Fulbright & Jaworski L.L.P., Los Angeles, California, is serving as Underwriters’ Counsel. It isanticipated that the Bonds, in book-entry form, will be available for delivery through The Depository Trust Company Book-Entry System in New York,New York on or about June 30, 2011.

THIS COVER PAGE CONTAINS CERTAIN INFORMATION FOR QUICK REFERENCE ONLY. IT IS NOT A SUMMARY OF THISISSUE. INVESTORS MUST READ THE ENTIRE OFFICIAL STATEMENT TO OBTAIN INFORMATION ESSENTIAL TO THE MAKINGOF AN INFORMED INVESTMENT DECISION.

Goldman, Sachs & Co. Morgan Stanley

Dated: June __, 2011____________________*Preliminary; subject to change

MATURITY SCHEDULE*(Base CUSIP No. ___________**)

Maturity Date(September 1)

PrincipalAmount

InterestRate Yield

CUSIP Suffix*

Maturity Date(September 1)

PrincipalAmount

InterestRate Yield

CUSIP Suffix*

2012 20252013 20262014 20272015 20282016 20292017 20302018 20312019 20322020 20332021 20342022 20352023 20362024

**CUSIP is a registered trademark of the American Bankers Association. CUSIP data on the cover hereof is provided by CUSIP Global Services,managed by Standard & Poor’s Financial Services LLC on behalf of The American Bankers Association. This data is not intended to create adatabase and does not serve in any way as a substitute for the CUSIP Services. The Agency, the Financial Advisor and the Underwriters are notresponsible for the selection or correctness of the CUSIP numbers set forth herein.____________________*Preliminary; subject to change.

No dealer, broker, salesperson or other person has been authorized by the Redevelopment Agency of theCity of Fremont (the “Agency”) to give any information or to make any representations other than those containedherein and, if given or made, such other information or representation must not be relied upon as having beenauthorized by the Agency. This Official Statement does not constitute an offer to sell or the solicitation of any offerto buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such personto make such an offer, solicitation or sale.

This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Statementscontained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or notexpressly so described herein, are intended solely as such and are not to be construed as a representation of facts.

The information set forth herein has been obtained from either the books and records of the Agency or fromsources which are believed to be reliable. The information and expression of opinions herein are subject to changewithout notice and neither delivery of this Official Statement nor any sale made hereunder shall, under anycircumstances, create any implication that there has been no change in the affairs of the Agency since the datehereof. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and maynot be reproduced or used, in whole or in part, for any other purpose.

THE PRICES AND OTHER TERMS OF THE OFFERING AND SALE OF THE BONDS MAY BECHANGED FROM TIME TO TIME BY THE UNDERWRITERS AFTER SUCH BONDS ARE RELEASEDFOR SALE AND SUCH BONDS MAY BE OFFERED AND SOLD AT PRICES OTHER THAN THE INITIALOFFERING PRICES, INCLUDING SALES TO DEALERS WHO MAY SELL SUCH BONDS INTOINVESTMENT ACCOUNTS. IN CONNECTION WITH THE OFFERING OF BONDS, THEUNDERWRITERS MAY OVER-ALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE ORMAINTAIN THE MARKET PRICES FOR SUCH BONDS AT A LEVEL ABOVE THAT WHICH MIGHTPREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUEDAT ANY TIME.

THE BONDS HAVE NOT BEEN REGISTERED WITH THE SECURITIES AND EXCHANGECOMMISSION UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON THEEXEMPTION CONTAINED IN SECTION 3(A)(2) OF SUCH ACT, AND HAVE NOT BEEN QUALIFIEDUNDER THE TRUST INDENTURE ACT OF 1939, AS AMENDED, IN RELIANCE UPON AN EXEMPTIONCONTAINED IN SUCH ACT.

REDEVELOPMENT AGENCY OF THE CITY OF FREMONTAND CITY COUNCIL MEMBERS

Robert Wasserman, Chairperson and MayorSuzanne Lee Chan, Vice Chairperson and Vice MayorAnu Natarajan, Agency Member and Council MemberBill Harrison, Agency Member and Council Member

Dominic D. Dutra, Agency Member and Council Member

REDEVELOPMENT AGENCY AND CITY STAFF

Fred Diaz, Executive Director and City ManagerMark Danaj, Assistant Executive Director and Assistant City Manager

Harriet Commons, Finance Director and TreasurerElisa Tierney, Housing and Redevelopment Agency Director

Harvey E. Levine, Agency Counsel and City Attorney

SPECIAL SERVICES

Financial Advisor

KNN Public FinanceA Division of Zions First National Bank

Oakland, California

Bond and Disclosure Counsel

Quint & Thimmig LLPSan Francisco, California

Trustee

Union Bank, N.A.San Francisco, California

Agency Special Counsel

Goldfarb & Lipman LLPOakland, California

Fiscal Consultant

Seifel Consulting Inc.San Francisco, California

Underwriters’ Counsel

Fulbright & Jaworski L.L.P.Los Angeles, California

TABLE OF CONTENTS

Page

INTRODUCTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1The City and the Agency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Authority for Issuance of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1Purpose of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Description of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Tax Allocation Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2Housing Set-Aside Revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3The Merged Project Area . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3Sources of Payment for the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Risk Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4Professionals Involved in the Offering . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Tax Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5Offering and Delivery of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Summaries of Documents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Continuing Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Forward-Looking Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6Other Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

THE BONDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Authority for Issuance of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Purpose of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8Estimated Sources and Uses of Funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Description of the Bonds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Form and Registration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11Debt Service Schedule . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12Redemption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

SECURITY FOR THE BONDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Allocation of Taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14Tax Revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15Annual Review of Tax Revenues; Compliance with Plan Limits; Defeasance Escrow Account

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Reserve Requirement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16Pass -Through Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Issuance of Parity Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Issuance of Subordinate Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Proposed Disestablishment of Redevelopment Agencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19Special Mandatory Redemption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Reduction in Taxable Value — Economic Factors, Property Damage and Appeals of Assessed

Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21Reduction in Inflationary Rate . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Levy and Collection . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22Seismic Factors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

PROPERTY TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23County Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23Assessed Valuation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23State-Assessed Utility Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Tax Levies, Collections and Delinquencies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24Teeter Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Article XIIIA of the California Constitution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25Litigation Involving Assessment Practices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Article XIIIB of the California Constitution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26Articles XIIIC and XIIID of the California Constitution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Proposition 87 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Property Tax Administrative Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Assembly Bill 1290 — Redevelopment Time Limits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 27Statement of Indebtedness . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28ERAF and SERAF Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28Proposition 22 - Further Limit on State Use and Shifts of Local Government Funds . . . . . . . 29Future Initiatives and Changes in Law . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

PROPERTY TAX COLLECTION AND DEBT SERVICE COVERAGE . . . . . . . . . . . . . . . . . . . . . . 30Historic Tax Increment Revenues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30Secured Tax Charges . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31Estimated Debt Service Coverage . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

THE AUTHORITY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

THE REDEVELOPMENT AGENCY OF THE CITY OF FREMONT . . . . . . . . . . . . . . . . . . . . . . . . 33Agency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Management and Administration . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Powers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33Financial Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34Outstanding Bonds of the Agency . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36State Controller’s Office . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

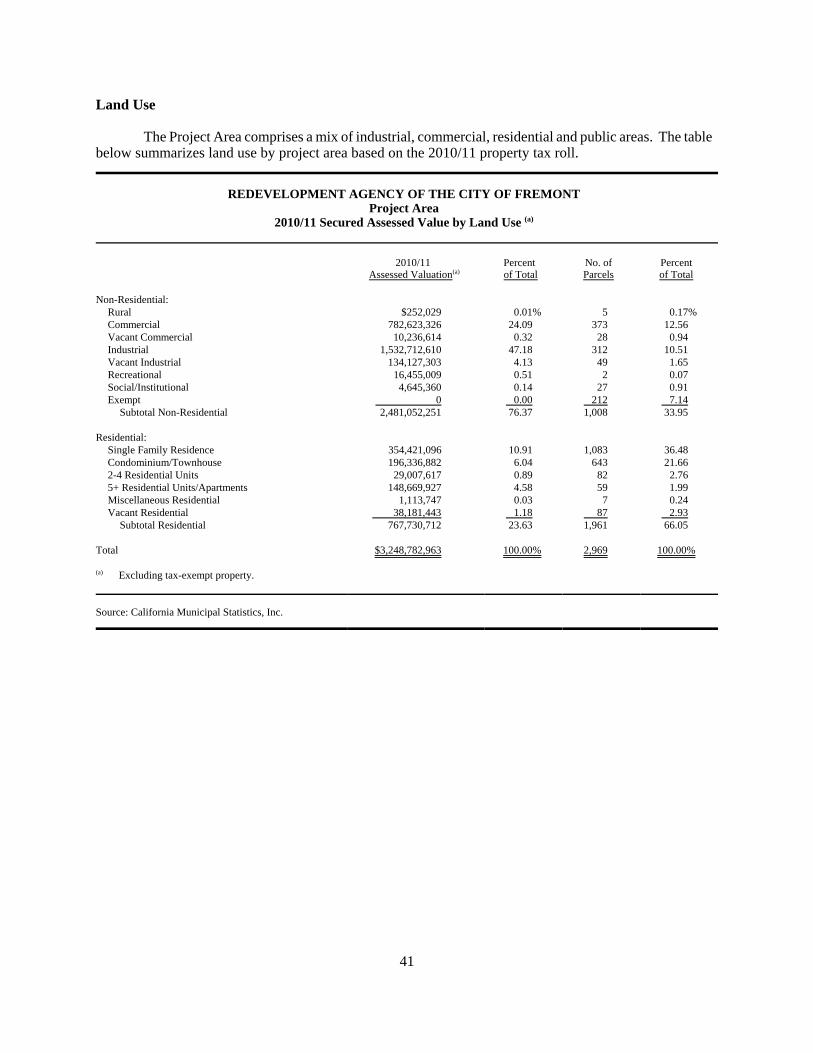

PROJECT AREA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36Redevelopment Plan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36Sub-Areas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37Plan Limits of Redevelopment Plans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39Pass -Through Agreements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Statutory Payments To Affected Taxing Entities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40Land Use . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41Largest Property Owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42Direct and Overlapping Bonded Debt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44Tax Matters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44No Litigation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46Legality for Investment in California . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46Legal Opinion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

MISCELLANEOUS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47Financial Advisor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47Continuing Disclosure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48Additional Information . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

APPENDIX A - AUDITED FINANCIAL STATEMENTS OF THE REDEVELOPMENT AGENCYOF THE CITY OF FREMONT FOR FISCAL YEAR ENDED JUNE 30, 2010 . A-1

APPENDIX B - CITY OF FREMONT GENERAL INFORMATION AND ECONOMICS . . . . . . B-1APPENDIX C - SUMMARY OF THE INDENTURE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . C-1APPENDIX D - FORM OF OPINION OF BOND COUNSEL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . D-1APPENDIX E - FORM OF CONTINUING DISCLOSURE CERTIFICATE . . . . . . . . . . . . . . . . . . . E-1APPENDIX F - FISCAL CONSULTANT’S REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1APPENDIX G - BOOK-ENTRY ONLY SYSTEM . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G-1

[BAY AREA MAP]

[RDA MAP]

OFFICIAL STATEMENT

$134,720,000*REDEVELOPMENT AGENCY OF THE CITY OF FREMONT

(FREMONT MERGED REDEVELOPMENT PROJECT)TAX ALLOCATION BONDS, 2011 SERIES A

INTRODUCTION

This introduction is not a summary of this official statement (the “Official Statement”). It is onlya brief description of and guide to, and is qualified by, more complete and detailed information containedin the entire Official Statement, including the cover page and appendices hereto, and the documentssummarized or described herein. A full review should be made of the entire Official Statement. The offeringof the Bonds to potential investors is made only by means of the entire Official Statement.

This Official Statement, including the cover page and appendices hereto, is provided to furnishinformation regarding the Redevelopment Agency of the City of Fremont (the “Agency”) issuing its“Redevelopment Agency of the City of Fremont (Fremont Merged Redevelopment Project) Tax AllocationBonds, 2011 Series A” (the “Bonds”), in the aggregate principal amount of $134,720,000* to be sold to theFremont Public Financing Authority (the “Authority”) and immediately resold by the Authority to theUnderwriters named on the cover page. The Authority is a joint powers authority comprised of the City ofFremont (the “City”) and the Agency (see under “AUTHORITY” herein). Capitalized terms used in thisOfficial Statement and not defined elsewhere herein have the meanings given such terms in the Indenture.See “APPENDIX C—SUMMARY OF THE INDENTURE—Definitions.”

The City and the Agency

The City is a general law city encompassing approximately 90 square miles, located on the east sideof San Francisco Bay in the County of Alameda (the “County”), approximately 40 miles southeast of SanFrancisco and 15 miles northeast of San Jose, bordering on Santa Clara County (see “APPENDIX B —CITY OF FREMONT GENERAL INFORMATION AND ECONOMICS”). The Agency was activatedpursuant to law in 1976 by Ordinance 1121 of the City Council. The five members of the City Council alsoserve as the governing body of the Agency. See “THE REDEVELOPMENT AGENCY OF THE CITYOF FREMONT” herein. The fiscal year for the Agency, the City and for property tax is from July 1through June 30 of the next calender year (“fiscal year”).

Authority for Issuance of the Bonds

The Bonds will be issued by the Agency pursuant to the constitution and the laws of the State ofCalifornia (the “State”), including the State Community Redevelopment Law, constituting Part 1,Division 24 of the State Health and Safety Code (the “Law”), an Indenture of Trust, dated as of June 1, 2011(the “Indenture”) by and between the Agency and Union Bank, N. A., as trustee thereunder (the “Trustee”),and an authorizing resolution of the Agency adopted on June 7, 2011 (the “Resolution”).

1

Purpose of the Bonds

The proceeds of the Bonds will be used to finance the costs of acquisition of the land for, design andconstruction of, the new Irvington Bay Area Rapid Transit (“BART”) station (the “Project”), fund a ReserveFund held by the Trustee in the amount of the Reserve Requirement, as defined herein (“SECURITY FORTHE BONDS - Reserve Requirement”), and to pay costs of issuance of the Bonds. See “THE BONDS -Purpose of the Bonds; the Project” herein.

Description of the Bonds

The Bonds will be issued as fully-registered current interest bonds in denominations of $5,000principal amount each, or any integral multiple thereof, and will be registered initially in the name of Cede& Co., as nominee of The Depository Trust Company, New York, New York (“DTC”). DTC will act assecurities depository for the Bonds. See “THE BONDS — Form, Denomination and Payment and“APPENDIX G - BOOK-ENTRY ONLY SYSTEM”.

The Bonds will be dated the date of delivery thereof. Interest on the Bonds is payable semiannuallyeach March 1 and September 1, commencing March 1, 2012. Interest payable March 1, 2012 is from thedate of delivery of the Bonds. Principal of the Bonds is payable on September 1 in each year due, as setforth on the inside cover page hereof. The Bonds are subject to redemption as described herein. See “THEBONDS — Redemption” herein.

Tax Allocation Financing

The Law provides a means for a California city or county to designate a geographic area within itsboundaries as a “project area” and form a redevelopment agency, such as the Agency, to carry outredevelopment activities within or of benefit to that project area (a “redevelopment project”). In generalunder the Law, the purpose of redevelopment agency activity in a project area is to revitalize and enhancethe project area by providing necessary public improvements and facilities to the extent that the area willno longer constitute “blighted conditions” that are a serious physical, social or economic burden to thecommunity. The Law provides for the funding of a redevelopment agency and its activities from a portionof the general purpose ad valorem property taxes collected within the project area. The parameters (inaddition to those set forth under the Law and other applicable statutes) that limit the redevelopment activitiesin a project area and the financing thereof (the “plan limits”) are established in a specific “redevelopmentplan” for that project area adopted by the legislative body of the city or county that formed theredevelopment agency and designated the project area.

The taxable valuation of property in a project area last equalized prior to adoption of theredevelopment plan, or “base year” roll, is established and, except for any period during which the taxablevaluation drops below the base year level, taxing agencies otherwise entitled to receive an allocation of advalorem taxes on property within the project area thereafter receive the taxes produced by the levy of thethen current tax rate upon the base year roll only. Taxes collected upon any increase in taxable valuationover the base year roll (“tax increment”) are allocated to the redevelopment agency. Such tax incrementfunds the activities of the redevelopment agency and under the Law, subject to certain deductions requiredto pay County administrative fees and payments under contractual or statutory tax-sharing agreements, maybe pledged by the redevelopment agency to the payment of any indebtedness incurred in financing orrefinancing its activities. Redevelopment agencies themselves have no authority to levy property taxes andmust look specifically to the allocation of such tax increment.

2

Housing Set-Aside Revenues

With limited exceptions, the Law requires redevelopment agencies to set aside not less than twentypercent of all tax increment allocated and paid to the redevelopment agency into a “low and moderateincome housing fund” to be expended only for authorized low and moderate income housing purposes, asdefined by the Law (such funds of the Agency herein are the “Housing Set-Aside Revenues” and the lowand moderate income housing fund of the Agency herein is the “Housing Fund”). Amounts on deposit ina low and moderate income housing fund may also be applied to pay debt service on bonds, loans oradvances of the redevelopment agency, the proceeds of which are deposited into the low and moderateincome housing fund to provide financing for such low and moderate income housing purposes. Under theLaw, the twenty percent set-aside requirement is calculated on the basis of gross tax increment revenues,before deductions for county administrative fees, payments under tax sharing agreements or any otherpurpose.

Housing Set-Aside Revenues and balances generated from Housing Set-Aside Revenues on depositin the Housing Fund are not pledged, and are not available, for payment of debt of the Agency incurred forpurposes other than for “low and moderate income housing.” Under the Law, “low and moderate incomehousing” means housing available to persons and families of “low and moderate income,”defined ashouseholds with adjusted annual income not exceeding 120% of county median income for a similarly sizedhousehold, including “very low income,” defined as households with adjusted annual income not exceeding50% of county median income for a similarly sized household, at “affordable housing costs.” Under theLaw, “affordable housing costs” means that the sum of various elements of housing costs paid by ahousehold with a qualifying income does not exceed the applicable percentage of that household’s annualincome specified under Sections 50052.3 and 50053 of the California Health and Safety Code.

The Bonds are not secured by or payable from Housing Set-Aside Revenues.

The Merged Project Area

Through ordinances adopted by the City Council of the City (the “City Council”) on July 7, 1998, the Agency’s Niles redevelopment project, Centerville redevelopment project, Irvington redevelopmentproject and Industrial redevelopment project, each previously established under separate redevelopmentplans by the City Council under provisions of the Law, were fiscally merged while retaining formallyseparate project plans and project areas. Through an ordinance adopted by the City Council on March 16,2010, these separate plans and project areas were consolidated under a single “Consolidated Amended andRestated Redevelopment Plan for the Fremont Merged Redevelopment Project (Including Irvington, Niles,Centerville and Industrial Areas)” (the “Redevelopment Plan”) with a single, consolidated project area (the“Project Area”) containing all of the previously established project areas (these “sub-areas” are, respectively,the “Irvington, Niles, Centerville and Industrial Areas” herein). While the Redevelopment Plan addressesredevelopment activities throughout the Project Area, certain Redevelopment Plan limits remain determinedon the basis of the sub-areas. The Law permits the tax increment from the Project Area to be used to fundredevelopment activities within or of benefit to any or all of the original areas, that is, anywhere within theProject Area, including pledging such tax increment for payment of indebtedness, such as the Bonds, tofinance any such activities. See “PROJECT AREA” herein.

3

Sources of Payment for the Bonds

The Bonds are special obligations of the Agency payable only from Tax Revenues (a specific netportion, as defined herein, of the tax increment received by the Agency from the Project Area), the ReserveAccount and such other funds pledged therefore under the Indenture. Tax Revenues do not include HousingSet-Aside Revenues or balances generated from Housing Set-Aside Revenues held in the Housing Fund. Neither the faith and credit nor the taxing power of the Agency, the City or the State or any politicalsubdivision thereof, is pledged for the payment of the Bonds. See “SECURITY FOR THE BONDS”herein.

Risk Factors

Any future decrease in taxable valuation of the Project Area or in the applicable tax rates will reducethe tax increment allocated to the Agency from the Project Area, and correspondingly would reduce therevenues available to the Agency from which to pay debt service on any indebtedness the Agency has issuedsecured by a pledge of such revenues, including the Bonds. See “RISK FACTORS” herein.

In addition to the Bonds, the Agency may issue or incur other bonds, loans, advances orindebtedness payable from Tax Revenues on a parity with the Bonds (collectively, “Parity Debt”), subjectto meeting certain covenants related to additional indebtedness, to finance or refinance redevelopmentactivities for the Project Area by supplemental indenture to the Indenture (a “Supplemental Indenture”). See“SECURITY FOR THE BONDS - Issuance of Parity Debt” herein.

As part of the Governor’s 2011/12 Budget effort, legislation was introduced on behalf of theGovernor on March 16, 2011 (AB101 in the State Assembly and SB 77 in the State Senate; the “ProposedLegislation”) to, among other things, (a) prohibit new redevelopment agreements after the effective date ofthe Proposed Legislation, (b) disestablish redevelopment agencies as of July 1, 2011, (c) State-wide take$1.7 billion in what would have been redevelopment agency tax increment revenue for the State general fundin 2011/12, and (d) thereafter have what would have been tax increment revenue in excess of the amountrequired to pay existing debt and pass-through payment obligations of former redevelopment agencies flowto local taxing agencies as regular property tax revenue (and not have the character of being “tax incrementrevenue”). All debt service and other enforceable obligations of tax increment of a redevelopment agencythat were in existence prior to disestablishment would continue to be paid, in effect as a protected allocationof property tax revenue, according to a “Recognized Obligation Payment Schedule” from a “RedevelopmentProperty Tax Fund”, a repository for the former tax increment revenue as collected, administered by therespective County Auditor-Controller, for the remaining life of debt service and other enforceableobligations of tax increment.

The Proposed Legislation, effective after disestablishment, creates successor agencies (generally thecity or county who formed the disestablished redevelopment agency) under an “oversight board” empoweredand directed, subject to vote of the board, to, where possible, undo agreements the redevelopment agencyhad entered into, including to the extent of using tax increment revenue to pay damages to do so, for thepurpose of generally liquidating redevelopment agency non-housing assets and commitments other than topay existing bonds and other enforceable obligations, with the intent of maximizing revenue to the State andlocal taxing agencies.

If the Proposed Legislation became law, it is unknown whether any agreement of the Agency withthe City or BART in respect to the Project would be challenged by an oversight board created under theProposed Legislation, or what the outcome of such a challenge would be. As of the date of this OfficialStatement the Proposed Legislation failed by one vote to pass in the State Assembly, there have been no

4

subsequent attempts at passage and it has not been brought to a vote in the State Senate . On the other hand,without giving details or firm timing, the Governor’s 2011-12 Budget May Revision released on May 10,2011 indicated that disestablishing redevelopment agencies and flowing tax increment revenue through tolocal taxing agencies to the maximum extent possible remain goals of the Governor.

Since the introduction of the Proposed Legislation, additional legislation has variously beenproposed or introduced, that would, if enacted, modify how redevelopment projects and finance proceedgoing forward, but none appear to have a potential retroactive reach similar to the Proposed Legislation, nordo any appear to challenge existing tax allocation bonds.

It is unknown whether the Proposed Legislation or other legislative proposals to limit or prohibitredevelopment agency projects or obligations or curtail or take tax increment revenue ultimately will beenacted, or if enacted, will withstand court challenge. Any redevelopment agency disestablishmentlegislation would seem to at least have to be compatible with (a) Article XVI, Section 16 of the Stateconstitution establishing tax increment financing and requiring tax increment to be paid to redevelopmentagencies, (b) Article XIII, Section 25.5 of the State constitution prohibiting the transfer of tax increment tothe State, any agency of the State or any local jurisdiction and (c) State and federal constitutional provisionsprohibiting legislation impairing the obligation of contracts.

See “RISK FACTORS” herein.

IF LEGISLATION HAS BEEN INTRODUCED OR PROPOSED WHICH IF ENACTEDAND EFFECTIVE WOULD IMPOSE ADDITIONAL LIMITATIONS OR BURDENS ON THEAGENCY BY REASON OF THE ISSUANCE OF THE BONDS OR WHICH PURPORT TOPROHIBIT THE SALE OR ISSUANCE OF THE BONDS OR WHICH PURPORT TO PREVENTOR IMPAIR THE PLEDGE OF TAX REVENUES UNDER THE INDENTURE OR THERE IS NOTAN AGREEMENT AMONG BART, THE CITY AND THE AGENCY TO FUND AND BUILD THEPROJECT, THEN EITHER THE AGENCY OR THE UNDERWRITERS MAY ELECT NOT TOPROCEED WITH THE SALE OF THE BONDS IF SUCH OCCURS PRIOR TO THE SALE, ORWITH THE ISSUANCE AND DELIVERY OF THE BONDS IF SUCH OCCURS AFTER THESALE BUT PRIOR TO CLOSING.

Professionals Involved in the Offering

KNN Public Finance, A Division of Zions First National Bank, Oakland, California, is acting as theAgency's financial advisor (“Financial Advisor”) with respect to the Bonds. The proceedings of the Agencyin connection with the issuance of the Bonds are subject to the approval as to their legality of Quint &Thimmig LLP, San Francisco, California, bond and disclosure counsel to the Agency (“Bond Counsel”). Certain legal matters of the Agency will be passed upon for the Agency by Goldfarb & Lipman LLP,Oakland, California, special counsel to the Agency. The Financial Advisor, Bond Counsel and Trustee willreceive compensation from the Agency contingent upon the sale, issuance and delivery of the Bonds. Compensation by the Agency to Special Counsel to the Agency and to Seifel Consulting Inc., fiscalconsultant to the Agency, is not contingent upon the sale, issuance and delivery of the Bonds.

Tax Matters

In the opinion of Bond Counsel, subject to compliance by the Agency with certain covenants, underpresent law, interest on the Bonds is excludable from gross income of the owners thereof for federal incometax purposes and is not included as an item of tax preference in computing the federal alternative minimum

5

tax for individuals and corporations, but such interest is taken into account in computing an adjustment usedin determining the federal alternative minimum tax for certain corporations. In addition, in the opinion ofBond Counsel, interest on the Bonds is exempt from personal income taxation imposed by the State ofCalifornia. See “LEGAL MATTERS -Tax Matters” herein.

Offering and Delivery of the Bonds

The Bonds will be offered when, as and if issued by the Agency and received by the Underwriters,subject to approval as to their legality by Bond Counsel. It is anticipated that the Bonds, in book-entry form,will be available for delivery through DTC in New York, New York on or about June 30, 2011.

Summaries of Documents

Following in this Official Statement are descriptions of the Bonds, the Indenture, the Agency andthe City. The descriptions and summaries of documents herein do not purport to be comprehensive ordefinitive, and reference is made to each such document for the complete details of all terms and conditions. All statements herein are qualified in their entirety by reference to each such document and, with respect tocertain rights and remedies, to laws and principles of equity relating to or affecting creditors' rightsgenerally. Terms not defined herein shall have the meanings set forth in the Indenture. Definitions ofcertain terms used herein are set forth in APPENDIX C — “SUMMARY OF THE INDENTURE –Definitions”. Copies of the Indenture are available for inspection during business hours at the corporatetrust office of the Trustee in San Francisco, California. See APPENDIX C — “SUMMARY OF THEINDENTURE”.

Continuing Disclosure

The Agency has covenanted for the benefit of the holders and beneficial owners of the Bonds toannually provide certain financial information and operating data relating to the Agency (the “AnnualReport”) and to provide notices of the occurrence of certain enumerated events, if material. See“MISCELLANEOUS — Continuing Disclosure” herein and APPENDIX E — “Form of ContinuingDisclosure Certificate”.

Forward-Looking Statements

Certain statements included or incorporated by reference in this Official Statement, including inAPPENDIX F attached hereto, constitute “forward-looking statements.” Such statements are generallyidentifiable by the terminology used such as “plan,” “expect,” “estimate,” “budget” or other similar words. The achievement of certain results or other expectations contained in such forward-looking statementsinvolve known and unknown risks, uncertainties and other factors which may cause actual results,performance or achievements described to be materially different from any future results, performance orachievements expressed or implied by such forward-looking statements. Although such expectationsreflected in such forward-looking statements are believed to be reasonable, there can be no assurance thatsuch expectations will prove to be correct. The Agency is not obligated to issue any updates or revisionsto the forward-looking statements if or when the expectations, events, conditions or circumstances on whichsuch statements are based occur.

6

Other Information

This Official Statement speaks only as of its date, and the information contained herein is subjectto change.

Copies of documents referred to and information concerning the Bonds are available at the officesof the City of Fremont, Finance Department, 3300 Capitol Avenue, Building B, Fremont, CA 94538;telephone: (510) 494-4610. The City may impose a charge for copying, mailing and handling.

END OF INTRODUCTION

7

THE BONDS

Authority for Issuance of the Bonds

The Bonds will be issued pursuant to the constitution and the laws of the State, including the Law,the Indenture and the Resolution.

Purpose of the Bonds; the Project

A $120,000,000 portion of the net proceeds of the Bonds will be deposited in the Project Fund, heldby the Trustee and used to finance the Project; a portion of the net proceeds of the Bonds will be depositedin the Costs of Issuance Fund, held by the Trustee and used to finance costs of issuance of the Bonds; anda portion of the net proceeds will be deposited in the Reserve Account, held by the Trustee, in the amountof the Reserve Requirement (see “SECURITY FOR THE BONDS - Reserve Requirement” herein). Totalcosts to be funded, with contingency allowances, are estimated to be $124,350,000.

The Agency only expects to issue the Bonds if prior thereto an agreement is reached among BART,the City and the Agency to transfer ownership and control of the $120,000,000 to be on deposit in theProject Fund to BART in return for BART, with certain assistance from the City, to acquire, design andconstruct the Project, with no further involvement of the Agency (the “Project Agreement”). The ProjectAgreement will be presented to City Council for approval on June __, 2011 and to the BART board on June __, 2011. The Agency will not issue the Bonds without an executed Project Agreement.

The Project is part of an approximately 5.4 mile extension of the BART passenger rail system fromits present terminus in downtown Fremont to a new Warm Springs BART station at the south end of the City(the overall extension, including the Irvington and Warm Springs BART stations, is referred to as the “WarmSprings Extension” or “WSX”). The eventual BART plan is to extend this line further south, into SantaClara County to connect with other commuter rail lines and points therein, including the City of San Jose. The Project is to be located approximately half-way between the Fremont and Warm Springs BART stations.

The WSX was part of the original BART plan developed over 30 years ago. For at least the past20 years, BART and the City have included the Project in their respective planning for the WSX and theIrvington Area, and the southern portion of the City generally. A major (but not the only) purpose of theAgency’s consolidated Redevelopment Plan adopted in 2010 was to accommodate financing of the Projectwith tax allocation bonds. Since 2001, the City has held the responsibility for “identifying” and, ultimately,arranging for financing for the Project, basically as the City’s contribution to the overall WSX project. Inaddition, the Agency has provided some funding of early design and construction elements of the WSX overthe past three years. Construction of the WSX, starting with a portion under the City’s Central Park andLake Elizabeth, just south of downtown Fremont, was initiated by BART in 2009, and, between BART andthe Agency, most of the land for the Project and its parking lots has been purchased. The entire WSXproject, including the Project and the Warm Springs BART station, is expected to be completed and openfor operation in mid-2015. Completing construction of the stations prior to operating trains reduces stationconstruction difficulty and costs.

Only the Project is being funded through the Bonds. BART is funding the other parts of the WSXfrom other sources, and are not a responsibility or obligation of the Agency or the City to fund.

An aerial rendering of the proposed Project is on the following page.

8

9

[Irvington BART Station Picture]

10

Estimated Sources and Uses of Funds

The sources and uses of funds relating to the Bonds are as follows:

REDEVELOPMENT AGENCY OF THE CITY OF FREMONTEstimated Sources and Uses of Funds

Sources of FundsPar Amount of IssueNet Original Issue Discount

Total Sources

Uses of Funds Deposit to Project Fund Deposit to Reserve Account

Deposit to Costs of Issuance Fund(a)

Underwriters’ DiscountTotal Uses

(a) Includes printing costs, legal fees, financial advisor’s fees and other fees and expenses associated with the issuance of the Bonds.

Description of the Bonds

The Bonds will be dated the date of delivery thereof (the “Dated Date”), and will be issued in fullyregistered form in denominations of $5,000 each or any integral multiple thereof. Interest on the Bonds willbe payable on March 1 and September 1 of each year, commencing on September 1, 2011 (each an “InterestPayment Date”). Each Bond shall bear interest from the Interest Payment Date next preceding the date ofauthentication thereof unless (a) it is authenticated after the close of business on the fifteenth calendar dayof the month preceding each Interest Payment Date (each a “Record Date”) and on or before the followingInterest Payment Date, in which event it shall bear interest from the Interest Payment Date immediatelyfollowing such Record Date; or (b) a Bond is authenticated on or before August 15, 2011, in which eventit shall bear interest from the Dated Date; provided, however, that if, as of the date of authentication of anyBond, interest thereon is in default, such Bond shall bear interest from the Interest Payment Date to whichinterest has previously been paid or made available for payment thereon. Interest on any Bond which is notpunctually paid as duly provided for on any Interest Payment Date shall be payable to the person in whosename the ownership of such Bond is registered at the close of business on a Special Record Date to be fixedby the Trustee.

Subject to optional redemption as hereinafter discussed, the Bonds will mature on the dates and inthe principal amounts shown on the cover of this Official Statement.

Form and Registration

The Bonds will be issued in fully registered form and, when issued, will be registered in the nameof Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”). Individualpurchases of Bonds will be made in book-entry form only in the principal amount of $5,000 each or anyintegral multiples thereof. Beneficial owners of the Bonds will not receive bond certificates representingtheir interests in the Bonds purchased, but will receive a credit balance on the books of the nominees of suchpurchasers.

11

Subject to the limitations described “APPENDIX G - BOOK-ENTRY ONLY SYSTEM”, Bondregistration may be transferred, and any Bond may be exchanged for Bonds of the same maturity of otherauthorized denominations and/or canceled at the office of the Trustee in the manner and with the effect setforth in the Indenture.

Debt Service Schedule

The following schedule sets forth the payments of the principal of and interest on the Bonds by bondyears ending September 1 (“Bond Years”). Tax Revenue received in each fiscal year fund the Bondpayments due on March 1 of that fiscal year and on September 1 of the following fiscal year.

Debt Service

The Bonds Bond Year

Ending September 1, Principal Interest Total Bond Year Total

20112012201320142015201620172018201920202021202220232024202520262027202820292030203120322033203420352036

TOTAL

Redemption

Special Mandatory Redemption. The Bonds shall be subject to redemption in whole, or in part, onMarch 1, 2014, if, by action of law or otherwise, the Agency, any successor to the Agency or any entity towhom Project Fund moneys are transferred, is prevented from expending any of the Bond proceeds tofinance the Project, from amounts on deposit in the Project Fund and from any other moneys applied forsuch purpose, at a redemption price equal to one hundred percent (100%) of the principal amount thereofplus interest accrued thereon to the date fixed for redemption, without premium.

12

Optional Redemption of the Bonds. The Bonds maturing on or before September 1, 2020 are notsubject to optional redemption prior to their maturities. Bonds maturing on or after September 1, 2021 aresubject to redemption, at the option of the Agency, on any date on or after September 1, 2020, as a wholeor in part, by such maturities as shall be determined by the Agency (and in lieu of such determination, prorata among maturities), and by lot within a maturity, from any available source of funds, at a price of 100%of the principal amount thereof, plus accrued interest to the date of redemption, without premium.

Sinking Account Redemption. Term Bonds maturing on September 1, 20__, shall be subject tomandatory redemption, in part by lot, and by lot within a maturity, from sinking account payments in thefollowing amounts and on the following dates, at a redemption price equal to the principal amount thereofto be redeemed, without premium, plus accrued interest thereon to the date fixed for redemption:

Redemption Date Principal Amount

The principal amount of each mandatory sinking fund payment of any maturity shall be reducedproportionately in integral multiples of $5,000 by the amount of any Bonds of that maturity optionallyredeemed prior to the sinking account mandatory redemption date.

Selection of Bonds for Redemption. Whenever provision is made in the Indenture for the redemptionof Bonds and less than all Bonds then currently outstanding are called for redemption, the Trustee will selectBonds for redemption from Bonds then currently outstanding and not previously called for redemption, atthe written direction of the Agency in such order for maturity as shall be designated by the Agency, and inthe absence of such direction, pro rata among maturities and by lot within a maturity. The Trustee willpromptly notify the Agency in writing of the Bonds so selected for redemption.

Partial Redemption. If only a portion of any Bond is called for redemption, then upon surrenderof such Bond the Agency will execute and the Trustee will authenticate and deliver to the Owner thereof,at the expense of the Agency, a new Bond or Bonds of the same interest rate and maturity of authorizeddenominations, in aggregate principal amount equal to the unredeemed portion of the Bond to be redeemed.

Notice of Redemption. While the Bonds are subject to the Book-Entry System, the Trustee shall berequired to give notice of redemption only to DTC, and the Trustee shall not be required to give any suchnotice of redemption to any other person or entity. DTC and the DTC Participants shall have soleresponsibility for providing any such notice of redemption to the beneficial owners of the Bonds to beredeemed. Any failure of DTC to notify any Direct Participant, or any failure of a DTC Participant to notifythe beneficial owner of any Bonds to be redeemed, of a notice of redemption or its content or effect will notaffect the validity of the notice of redemption, or alter the effect of redemption. The Trustee will mail thenotice of redemption of Bonds to be redeemed not less than 30 days nor more than 60 days prior to the datefixed for redemption, during any period in which the Bonds are not subject to the Book-Entry System toOwners of all Bonds as their respective names and addresses appear on the registration books of the Trustee,and during any period, to the Securities Depositories and to one or more Information Services. Notice ofthe redemption of Bonds will be given by the Trustee on behalf of the Agency. Failure of an Owner toreceive any such notice so mailed nor any defect therein will not affect the validity of the proceedings forthe redemption of such Bonds or the cessation of the accrued interest thereon. All Bonds redeemed pursuantto the redemption provisions of the Indenture will be canceled.

Effect of Redemption. From and after the date fixed for redemption, if funds available for thepayment of the redemption price of, and interest on, the Bonds so called for redemption have been deposited

13

with the Trustee, such Bonds so called shall cease to be entitled to any benefit under the Indenture other thanthe right to receive payment of the redemption price and accrued interest to the redemption date, and nointerest shall accrue thereon from and after the redemption date specified in such notice.

SECURITY FOR THE BONDS

Allocation of Taxes

As provided in the Redevelopment Plan and pursuant to Article 6 of Chapter 6 of the Law(commencing with Section 33670 of the California Health and Safety Code) and Section 16 of Article XVIof the California Constitution, taxes levied upon taxable property in the Project Area each year by or for thebenefit of the State, Agency, County and any district or other public corporation (herein collectively referredto as “taxing agencies”) for each fiscal year beginning after the effective date for allocation of tax increment,are divided as follows:

(a) To Taxing Agencies: That portion of the taxes which would be produced by the rate upon whichthe tax is levied each year by or for each of said taxing agencies upon the total sum of the assessedvalue of the taxable property in the Project Area as shown upon the assessment roll used inconnection with the taxation of such property by such taxing agency last equalized prior to theeffective dates of the ordinances approving the Redevelopment Plan, shall be allocated to, and whencollected shall be paid into the funds of the respective taxing agencies as taxes by or for said taxingagencies on all other property are paid (for the purpose of allocating taxes levied by or for anytaxing agency or agencies which did not include the territory in the Project Area on the effectivedate of the applicable ordinance but to which such territory is annexed or otherwise included aftersuch effective date, the assessment roll of the County last equalized on the effective date of saidordinance shall be used in determining the assessed valuation of the taxable property in the ProjectArea on said effective date) (the “Base Year Amount”);

(b) To the Agency: With the exceptions noted in paragraphs (c) and (d) below, that portion of saidlevied taxes each year in excess of the amounts provided for in (a) above, together with subventionsor other amounts reimbursed by the State in respect of property tax exemptions with respect to theProject Area, shall be allocated to, and when collected, paid into a special fund of the Agency to paythe principal of, and interest on, bonds, loans, moneys advanced to, or indebtedness (whetherfunded, refunded, assumed, or otherwise) incurred by the Agency to finance or refinance, in wholeor in part, the redevelopment of the Project Area, and to pay certain amounts to various taxingagencies pursuant to respective contractual or statutory tax sharing agreements between the Agencyand such taxing agencies (“Pass-Through Agreements”; see “Project Area — Pass-ThroughAgreements” herein);

(c) Exception For Voter-Approved Indebtedness: That portion of the taxes identified in paragraph(b) above that are attributable to a tax rate levied by a taxing agency for the purpose of producingrevenues in an amount sufficient to make annual repayments of principal of, and interest on, anybonded indebtedness for the acquisition or improvement of real property approved by the voters ofthe taxing agency on or after January 1, 1989, shall be allocated to, and when collected shall be paidinto, the fund of the taxing agency.

(d) Exception for Industrial Area: Pursuant to a provision of the Redevelopment Plan, that portionof taxes identified in paragraph (b) above attributable to annual increases in the assessed value of

14

property within the Industrial Area which are, or otherwise would be, calculated pursuant tosubdivision (f) of Section 110.1 of the California Revenue and Taxation Code (the provisionlimiting normal real property annual assessed value growth to a specified inflation factor notexceeding 2 percent) shall not be claimed as tax increment revenue, with the purpose and result thatsuch amount is allocated to the respective taxing agencies as tax revenue to them, similar to theamounts described in paragraph (a) above.

The Agency is authorized to make pledges of the portion of taxes mentioned in paragraph (b) aboveas to specific advances, loans and indebtedness as appropriate in carrying out the Redevelopment Plan.

Tax Revenues

The Bonds are secured by and payable from an irrevocable pledge of, and charge and lien upon,“Tax Revenues”. Under the Indenture, “Tax Revenues” means all taxes pledged and annually allocatedwithin the Plan Limitations, following the date of issuance of the Bonds, and paid to the Agency with respectto the Merged Redevelopment Project pursuant to Article 6 of Chapter 6 (commencing with section 33670)of the Law and section 16 of Article XVI of the Constitution of the State, or pursuant to other applicableState laws, and as provided in the Merged Redevelopment Plan, and all payments, subventions andreimbursements, if any, to the Agency specifically attributable to ad valorem taxes lost by reason of taxexemptions and tax rate limitations, excluding all other amounts of such taxes (if any): (a) which are requiredto be deposited into the Low and Moderate Income Housing Fund of the Agency in any Fiscal Year pursuantto section 33334.3 of the Law, (b) which constitute supplemental subventions payable by the State to theAgency under and pursuant to Chapter 1.5 of Part 1 of Division 4 of Title 2 (commencing with section16110) of the California Government Code, (c) which constitute amounts required to be paid by the Agencyto taxing agencies under tax sharing agreements to pass through a portion of tax increment (“Pass-ThroughAgreements”), except and to the extent such amounts so payable are payable on a basis subordinate to thepayment of the 2011A Bonds and any Parity Debt, (d) which constitute amounts payable by the Agencyunder sections 33607.5 or 33607.7 of the Law for payments to affected taxing entities, except and to theextent such amounts so payable are payable on a basis subordinate to the payment of the 2011A Bonds andany Parity Debt, and (e) which constitute amounts payable by the Agency under section 33676 of the Lawfor payments to affected taxing entities. See also “PROPERTY TAX COLLECTION AND DEBTSERVICE COVERAGE” and “Pass -Through Agreements” and “Project Area” herein and“APPENDIX F - FISCAL CONSULTANT’S REPORT” for further discussion, and history andprojections of Tax Revenues and their allocation for various Agency purposes.

The Agency has no power to levy and collect property taxes, and any property tax limitation,legislative measure, voter initiative or provisions of additional sources of income to taxing agencies havingthe effect of reducing the property tax rate, could reduce the amount of Tax Revenues that would otherwisebe available to pay the principal of, and interest on, the Bonds. Likewise, changes in the methodology bywhich property is assessed or broadened property tax exemptions could have a similar effect. See “RISKFACTORS” and “LIMITATIONS ON TAX REVENUES AND POSSIBLE SPENDINGLIMITATIONS” herein.

THE BONDS ARE NOT A DEBT OF THE CITY, THE STATE OR ANY OF ITSPOLITICAL SUBDIVISIONS, AND NEITHER THE CITY NOR THE STATE NOR ANY OF ITSPOLITICAL SUBDIVISIONS (OTHER THAN THE AGENCY) IS LIABLE THEREON. THEAGENCY HAS NO TAXING POWER. THE BONDS ARE PAYABLE EXCLUSIVELY FROM THETAX REVENUES AND OTHER FUNDS AS PROVIDED IN THE INDENTURE. THE BONDS ANDANY PARITY DEBT OF THE AGENCY ARE PAYABLE SOLELY FROM TAX REVENUES

15

ALLOCATED TO THE AGENCY FROM THE PROJECT AREA EXCEPT AS OTHERWISEPROVIDED IN THE INDENTURE.

Annual Review of Tax Revenues; Compliance with Plan Limits; Defeasance Escrow Account

The Indenture requires that the Agency annually cause to be prepared a report which sets forth theestimated annual and cumulative total amount of tax increment revenues remaining available to be receivedby the Agency under the Redevelopment Plan’s plan limits (the “Remaining Limit Amount”), the estimatedCurrent Year Obligations (as defined below), and the estimated Future Obligations (as defined below). Ifthe Remaining Limit Amount is equal to or less than 110% of the Future Obligations, then, in each fiscalyear, the Agency shall cause to be deposited in a Trustee-held account (the “Defeasance Escrow Account”),for investment in Defeasance Obligations (see APPENDIX C — “SUMMARY OF THE INDENTURE”),that portion of tax increment revenues, if any, allocated to the Agency in excess of the Current YearObligations to the extent necessary, to enable repayment when due of all Future Obligations within theRemaining Limit Amount, taking into account (a) the Remaining Limit Amount, (b) all Future Obligations,and (c) the amounts already existing in the Defeasance Escrow Account. Amounts in the Defeasance EscrowAccount, including interest earned thereon, shall only be used to (a) prepay the Bonds and any Parity Debt,in such manner as the Agency shall determine, or (b) pay debt service on the Bonds and any Parity Debt.Amounts remaining in the Defeasance Escrow Account following payment in full or defeasance of the Bondsand all Parity Debt shall be transferred to the Agency for any lawful purpose under the Law.

“Current Year Obligations” means the amounts necessary to pay the debt service and other amountsdue in the applicable fiscal year for which the annual report is then being prepared with respect to the Bonds,applicable Pass-Through Agreements, deposits into the Housing Fund and other statutory obligations, anysubordinate debt and the Agency’s administrative costs.

“Future Obligations” means the estimated amounts necessary to pay the debt service and otheramounts due in all succeeding fiscal years (until the earlier of the final maturity date of the Bonds or theRemaining Limit Amount is estimated to be reached) with respect to the Bonds, applicable Pass -ThroughAgreements, deposits into the Housing Fund and other statutory obligations, any subordinate debt and theAgency’s administrative costs; provided that, in estimating the portion of the Future Obligations related tothe Bonds, the amount of remaining debt service will take into account the early prepayment or defeasanceof the Bonds estimated to occur using amounts deposited or to be deposited in the Defeasance EscrowAccount.

Reserve Requirement

Under the Indenture, there is a Reserve Account established for the Bonds and any Parity Debt. TheReserve Account is funded at the Reserve Requirement. “Reserve Requirement” means, as of any calculationdate, an amount, calculated by or on behalf of the Agency and certified to the Trustee in writing, equal tothe least of (a) Maximum Annual Debt Service on all Outstanding Bonds and any Parity Debt, (b) 125% ofaverage annual debt service on the Bonds and any Parity Debt, and (c) 10% of the then outstanding principalamount of the Bonds and any Parity Debt. The Reserve Requirement as of the date of delivery of the Bondsis $___________.

If the Trustee has actual knowledge that the amount on deposit in the Reserve Account at any timeis less than the Reserve Requirement, the Trustee will promptly notify the Agency of such fact. Promptlyupon receipt of any such notice, the Agency will transfer to the Trustee, Tax Revenues sufficient to maintainthe Reserve Requirement on deposit in the Reserve Account. If there shall then not be sufficient Tax

16

Revenues to transfer an amount sufficient to maintain the Reserve Requirement on deposit in the ReserveAccount, the Agency shall be obligated to continue making transfers as Tax Revenues become available inthe Special Fund until there is an amount sufficient to maintain the Reserve Requirement on deposit in theReserve Account. See APPENDIX C – “SUMMARY OF THE INDENTURE.”

Pass -Through Agreements

The Agency has entered into a Third Amended and Restated Fiscal Agreement Regarding FremontIndustrial Redevelopment Project Amended and Restated as of September 1, 2009 by and among the Agencyand the City of Fremont, the County of Alameda, the Alameda-Contra Costa County Transit District, theAlameda County Flood Control District, the Alameda County Library District, the Alameda CountyMosquito Abatement District, the Alameda County Resource Conservation District, the Alameda CountyWater District, the Bay Area Air Quality Management District, the Bay Area Rapid Transit District, the EastBay Regional Park District and the Washington Hospital District (the “County Agreement”), a tax sharingagreement under which specified amounts of tax increment revenue from the Industrial Area are to be passedthrough by the Agency to the aforesaid taxing entities. The County Agreement precludes the pledge of theaggregate amount of such pass-through tax increment revenue by the Agency for payment of any bonds orother indebtedness of the Agency unless and until the Agency obtains approval from the County. TheAgency has provided for and received the subordination of pass-through payments under the CountyAgreement to payment of the Bonds. No other existing Pass-Through Agreements with any other taxingentities subordinate the right to receive pass-through tax increment to the Agency for payment of the Bonds.

The Agency has also entered into certain tax sharing agreements under which lump sum paymentswill be made by the Agency, in return for which no future pass-through of tax increment will be made to thetaxing entity. Such lump sum payments are treated as expenditures for redevelopment projects by theAgency.

See APPENDIX C — “SUMMARY OF THE INDENTURE – Definitions” for a list of theexisting Pass-Through Agreements.

Under the Indenture, the Agency may enter into additional agreements for payments to affectedtaxing agencies, provided that such agreements subordinate the right of the taxing agency to paymentthereunder to the Agency for payment of the Bonds and any Parity Debt, as defined below.

Issuance of Parity Debt

In addition to the Bonds, the Agency may issue or incur Parity Debt to finance redevelopmentactivities within or for the benefit of the Redevelopment Project in such principal amount as shall bedetermined by the Agency. The Agency may issue and deliver any such Parity Debt, which shall be payableat a fixed interest rate or rates, subject only to the following specific conditions:

(a) The Agency shall be in compliance with all covenants set forth in the Indenture and all existingParity Debt Instruments;

(b) Tax Revenues for the then current fiscal year, based on the most recent assessed valuation ofproperty in the Redevelopment Project as evidenced in written documentation from an appropriateofficial of the County, plus, at the option of the Agency, the Additional Revenues, and assuming nogrowth in assessed valuations as of such date of computation, shall be at least equal to one hundred fifty percent (150%) of Maximum Annual Debt Service on all Bonds and any Parity Debt which will

17

be Outstanding following the issuance of such Parity Debt; provided, however, that Tax Revenuesshall be reduced to the amount by which Tax Revenues would be decreased if all pendingassessment appeals were to be determined in favor of the property owners in an amount equal to theaverage percent of reductions over an appropriate period of appeals history, as determined by anIndependent Redevelopment Consultant;

(c) The aggregate amount of the principal and sinking fund installments of and interest on allOutstanding Bonds, Parity Debt, Subordinate Debt and any Pass-Through Agreements notsubordinated to any Outstanding Bonds, Parity Debt, Subordinate Debt coming due and payablefollowing the issuance of such Parity Debt shall not exceed the maximum amount of tax incrementrevenues permitted under the Plan Limitations;

(d) The aggregate amount of the all Bonds, Parity Debt and Subordinate Debt to be outstandingfollowing the issuance of such Parity Debt shall not exceed the maximum amount of obligationspermitted under the Plan Limitations to be outstanding at any time;

(e) The Parity Debt shall be payable as to principal on September 1 in each year in which principalbecomes due, and shall be payable as to interest semiannually on March 1 and September 1, exceptthat the first installment of interest may be payable on either March 1 or September 1 and shall befor a period not longer than twelve (12) months;

(f) The Trustee or any successor shall act as trustee for such Parity Debt;

(g) The Parity Debt Instrument providing for the issuance of such Parity Debt may provide for theestablishment of separate funds and accounts or may make reference to and include any fund oraccount established under the Indenture; and

(h) The Parity Debt Instrument providing for the issuance of such Parity Debt shall provide for thedeposit of moneys in the Reserve Account if required to increase the balance of the Reserve Accountto at least equal to the Reserve Requirement upon the issuance of such Parity Debt.

Notwithstanding the foregoing, the Agency may issue or incur Refunding Debt in such principalamount as shall be determined by the Agency so long as certain conditions set forth in the Indenture are met.

Issuance of Subordinate Debt

From time to time the Agency may issue or incur Subordinate Debt in such principal amount as shallbe determined by the Agency; provided that (a) the Agency shall be in compliance with all of its covenantsset forth in the Indenture and any Parity Debt Instruments (or any non-compliance shall be cured inconnection with the issuance of the Subordinate Debt, (b) the issuance of such Subordinate Debt (after takinginto account the Bonds and all other obligations of the Agency payable from Tax Revenues, as well as allother bonded indebtedness of the Agency) shall not cause the Agency to exceed any applicable PlanLimitations, and (c) the Agency will at all times that the Bonds and any Parity Debt are Outstanding havesufficient capacity to receive Tax Revenues in an amount at least equal to the remaining Debt Service onthe Bonds and any Parity Debt as well as all fixed debt service or other obligations of the Agency (includingsuch Subordinate Debt) payable from Tax Revenues.

18

RISK FACTORS

Proposed Disestablishment of Redevelopment Agencies

Proposed Legislation

As part of the Governor’s 2011/12 Budget effort, the Proposed Legislation was introduced on behalfof the Governor on March 16, 2011 to, among other things, (a) prohibit new redevelopment agreements afterthe effective date of the Proposed Legislation, (b) disestablish redevelopment agencies as of July 1, 2011,(c) State-wide take $1.7 billion in what would have been redevelopment agency tax increment revenue forthe State general fund in 2011/12, and (d) thereafter have what would have been tax increment revenue inexcess of the amount required to pay existing debt and pass-through payment obligations of formerredevelopment agencies flow to local taxing agencies as regular property tax revenue (and not have thecharacter of being “tax increment revenue”). All debt service and other enforceable obligations of taxincrement of a redevelopment agency that were in existence prior to disestablishment would continue to bepaid, in effect as a protected allocation of property tax revenue, according to a “Recognized ObligationPayment Schedule” from a “Redevelopment Property Tax Fund”, a repository for the former tax incrementrevenue as collected, administered by the respective County Auditor-Controller, for the remaining life ofdebt service and other enforceable obligations of tax increment.

The Proposed Legislation, effective after disestablishment, creates successor agencies (generally thecity or county who formed the disestablished redevelopment agency) under an “oversight board” empoweredand directed, subject to vote of the board, to, where possible, undo agreements the redevelopment agencyhad entered into, including to the extent of using tax increment revenue to pay damages to do so, for thepurpose of generally liquidating redevelopment agency non-housing assets and commitments other than topay existing bonds and other enforceable obligations, with the intent of maximizing revenue to the State andlocal taxing agencies.

Finally, the Proposed Legislation would lengthen the statute of limitations (a) for the commencementof an action to review a determination or finding by a redevelopment agency or its legislative body, from90 days to two years after the determination or finding, if such determination or finding is made afterJanuary 1, 2011, and (b) for any action that is brought on or after January 1, 2011, to determine the validityof bonds issued by the redevelopment agency, from 60 days to two years after the date of the triggeringevent. Although the Agency does not believe there is any defect in the proceedings for the issuance of theBonds that could give rise to a successful challenge and Bond Counsel is providing its opinion with respectto the Bonds as set forth in “APPENDIX E” to this Official Statement, there could be an increased risk ofa legal challenge because the Agency is issuing the Bonds after January 1, 2011, and any such challengecould affect the market price of the Bonds on the secondary market.

If the Proposed Legislation became law, it is unknown whether any agreement of the Agency withthe City or BART in respect to the Project would be challenged by an oversight board created under theProposed Legislation, or what the outcome of such a challenge would be. As of the date of this OfficialStatement the Proposed Legislation failed by one vote to pass in the State Assembly, there have been nosubsequent attempts at passage and it has not been brought to a vote in the State Senate . On the other hand,without giving details or firm timing, the Governor’s 2011-12 Budget May Revision released on May 10,2011 indicated that disestablishing redevelopment agencies and flowing tax increment revenue through tolocal taxing agencies to the maximum extent possible, presumably along the lines of the ProposedLegislation, remain goals of the Governor. While the Proposed Legislation was introduced as “urgency

19

legislation”, so requiring two-thirds legislative approval, if it or similar legislation were part of the 2011-12Budget Act, presumably it would require only the simple majority legislative adoption of the Budget Act.