refi readi white paper

DESCRIPTION

This is by no mean an exhaustive list. Like 18 Strategies before it, Refi Readi © is intended to spark dialogue in your credit union and among your colleagues. We hope it spawns additional Suggestions that you will share with others, and with us. If you have an idea you’d like to share with all credit unions, drop us a line at [email protected]. Will rates go lower? Will housing prices fall further? Don’t know, I’ll wait and see.TRANSCRIPT

Prime Alliance Solutions, Inc.January 2009

Mortgage rates are the lowest they’ve been in almost 40 years. Can they go lower? Hard to say. As Yogi Berra once said, “Predictions are hard to make, especially when they are about the future.” Rates may, in fact, go lower. Even if they don’t, however, the time for many members to refinance is now, a fact of which they are frightfully aware as those of us in the mortgage business know full well. It’s also time for first-time homebuyers to consider their inaugural purchases. Low rates in concert with the lowest home prices in a decade should be music to their ears. It’s time for credit unions to spread the good word, seizing this opportunity while it lasts and building our reputations as the reliable, durable, sustainable local lenders we’ve always been.

Dan GreenExecutive Vice President, StrategyPrime Alliance

©2000-2009 Prime Alliance Solutions, Inc. All Rights Reserved.

1 2 3

4 5 6

Refi ReadiSix Survival Suggestions for the next Six Months

Refi Readi© 2Introduction 2

Part I: The Environment 3

Subvention Financing, Federal Reserve Style 3

The Mortgage/Mortgage Gap 4

Gone, Gone Away 5

Part II: Six Suggestions 6

Market, Advertise, Promote 6

Shuffle the Deck 7

Pricing 8

Product 11

FHA 13

From Traditional to Paperless to Electronic 15

Summary 16

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 1 of 16

Refi Readi© Six Survival Suggestions for the next Six Months

IntroductionMortgage rates are the lowest they’ve been in almost 40 years. Can they go lower? Hard to say. As Yogi Berra once said, “Predictions are hard to make, especially when they are about the future.” Rates may, in fact, go lower. Even if they don’t, though, the time for many members to refinance is now, a fact of which they are frightfully aware as those of us in the mortgage business know full well. It’s also time for first-time homebuyers to consider their inaugural purchases. Low rates in concert with the lowest home prices in a decade should be music to their ears. It’s time for credit unions to spread the good word, seizing this opportunity while it lasts and building our reputations as the reliable, durable, sustainable local lenders we’ve always been.

With the volume business credit unions are originating you might be wondering if we are thinking rationally, encouraging you to generate even more business. That’s the purpose of Refi Readi©. Your Prime Alliance Team developed the six suggestions you’ll find here to help you manage the current influx of business smartly while continuing to grow your market share.

Refi Readi© is in two parts. Part I, The Environment, discusses three factors driving today’s market. We hope the insights provided here will help you plan and execute in the coming months. Part II, Six Suggestions, is our latest thinking on mortgage lending management. They’ll help you through the next several months. Several suggestions, like Pricing and Paperless Lending, are viable in all market conditions. Implement them now; benefit for years. Following each suggestion is the Take Away: actions we suggest you take now to quickly become more efficient and cost-effective.

This is by no mean an exhaustive list. Like 18 Strategies before it, Refi Readi© is intended to spark dialogue in your credit union and among your colleagues. We hope it spawns additional Suggestions that you will share with others, and with us. If you have an idea you’d like to share with all credit unions, drop us a line at [email protected].

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 2 of 16

Part I: The Environment

Subvention Financing, Federal Reserve StyleAuto lenders are especially familiar with subvention financing: the pricing strategy auto companies use to incent buyers to purchase and finance certain models, usually those they need to move them most. Subvention, of a sort, has come to housing finance. The Federal Reserve’s monetary policy, specifically its announcement and subsequent actions to begin purchasing $500 billion in GSE mortgage-backed securities (MBS) and debt obligations of the GSEs is the root cause. On or about January 5, 2009, rates dropped to the 5% range for a 30 year fixed rate loan as a result.

Just as rates hit all time lows, applications are hitting all time highs. November was a slow month for mortgage lenders; December was altogether different; originations within Prime Alliance credit unions tripled month-over-month. January’s experience could wind up being 30% greater than December’s. The Mortgage Bankers Association does not expect that rates will increase throughout the year. Quite the contrary, their January Mortgage Finance Forecast calls for lower rates in the second and third quarters.

While this isn’t true subvention financing, it is the Federal Reserve’s way of stimulating the housing market. Five-hundred billion dollars is a lot of money. To put it in perspective, it equals almost 25% of all housing finance in 2008. What we can’t know is their total appetite. Is $500 billion the all-in amount? Keep in mind there are no constraints on the Fed’s ability to grow its balance sheet. Section 13(3) of the Federal Reserve Act provides the Fed with broad powers to lend to any individual, partnership or corporation under unusual and exigent circumstances. These are certainly unusual circumstances.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 3 of 16

Wait and See

Will rates go lower? Will housing prices fall further? Don’t know, I’ll wait and see.

These are the three most dangerous words in economics. The longer consumers ‘wait and see’ the longer economic hardship lasts. Will rates go lower? It’s possible. Think about this, though: the Fed said it would purchase $500 billion in GSE debt and MBS, in a mortgage finance market that experts now say could top $2.5 trillion. Where’s the other $2 trillion going to come from? Which investors will be willing to make long-term investments at these rates, other than the Fed? This is one of the reasons we believe the first six months of the year may generate the greatest activity.

What about housing prices? In some markets prices have further to fall. It may indeed by wise to ‘wait and see’ in areas of the country that experienced rampant appreciation. Conversely, it may be time to buy in those areas where home prices increased more gradually.

Wait and See? For those members who still have equity in their homes and have maintained their credit ratings, there’s no time like the present to refinance. Time to spread the word. Time to get the economy moving.

The Mortgage/Mortgage Gap1

Credit unions reliably provided mortgage financing annually for 2% of all those who took out a mortgage from 1996 through 2006. For an entire decade, our market share didn’t waver. That all changed in 2007, as the first act of the sub-prime opera took shape. Members, the general public, Realtors®, mortgage brokers and others realized credit unions continued to lend as those around them failed. By the end of the year we’d grown our market share by 70 basis points. During the fourth quarter the industry had managed a 3.60% share. While the numbers aren’t in for 2008 it is reasonable to assume market share grew yet again to the 4.00% to 4.25% range.

Assuming 2008’s prediction is accurate, credit unions doubled share from 2006 to 2008, a trend we need to sustain. The fact is, as well as we’re doing, more members continue to obtain their mortgages from lenders other than credit unions. This Mortgage Gap takes a little explaining.

We know, for instance, that there are over 92 million credit union members in the country out of a population of 305 million, which equals 40 million and 132 million households, respectively. One-third, therefore, of all households are credit union members. Using 2008 origination data, we estimate there were approximately 8.5 million mortgage loans granted last year; credit unions granted, as a high estimate, about 360,000 of them, or 4.24% of the total. We estimate, however, that credit union members took out more than 630,000 mortgage loans last year. While we financed between $75 and $85 billion, another $130 billion went to other lenders. This is the Mortgage Gap; the void we have left to fill between now and 2016 on our quest to 10% annual market share.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 4 of 16

1 Data used in this section is from a variety of sources, including CUNA & Affiliates Monthly Credit Union Estimates for November 2008 and its U.S. Credit Union Profile of the same month. Other sources include the U.S. Census, the Federal Reserve Bank of St. Louis and the Mortgage Bankers Association of America.

Can CU Balance Sheets Hold It All?

If the pundits’ estimates of $2.5 trillion in mortgage originations this year are correct, can credit union balance sheets hold our growing share? Consider this: at 4% share credit unions will originate $100 billion! Our industry has been selling 27% of mortgage production over the past several years, which means we’d place $73 billion in additional mortgage loans in portfolio during 2009.

Our portfolios are filling up, too. By September 30, 2008, our industry’s loan to share ratio had risen to 83.9%, close to an historic high. Likewise, long-term assets to total assets increased to 32.2%. First mortgages account for more than ⅓ of total loans, and the proportion is increasing.

Against the increases in mortgage loans, share growth is expected to top 10% this year, while auto loans as a percent of loans will decrease again, providing some much needed breathing room. Make more room in the portfolio by selling more, especially the low-rate, long-term fixed rate loans you’re originating now, as their duration is likely to lengthen as members stay in their homes longer and have little incentive to refinance.

The CU Housing RoundTable is working on its latest paper, Challenging the Financial Model, which explores mortgage liquidity alternatives and proposes solutions for the new environment. Look for it early second quarter 2009.

Gone, Gone Away

Where did the competition go? According to the Implode-O-Meter, found on The Mortgage Lender2 website, 3193 mortgage lenders have ‘imploded’ since 2006, gone completely out of business or much diminished from their pre-sub-prime crisis days. This number represents more than one-third of industry’s pre-2006 capacity, or about $1 trillion in peak years that must now be manufactured elsewhere. This is why credit unions may feel more ‘slammed’ now than during past times of heavy refinancing. There simply are not as many lenders making loans.

Viewed differently, all borrowers, members included, have 30% fewer options when seeking a mortgage loan. What better news could there possibly be for credit unions? Members are returning to their credit unions for their housing finance needs. Our industry’s increase in market share tells us this. Non-members, too, are looking to credit unions. Both are coming to us not because we are the last lenders standing but because they know us as the safe, trustworthy, reliable lenders that provide affordable, sustainable mortgage loans.

This is not a new trend, and, frankly, as far as trends go, it’s getting old. Prime Alliance starting talking about it in early 2007 as the market began to unravel. Consumers, it appears, have gone from following a trend to adopting the way they perceive credit unions as a mindset. We are all they perceive us to be and more: we’re also local, which is another way in which consumers are beginning to choose the financial institution they do business with. The nameless, faceless disappearing mortgage broker with their seemingly low rates and magic mortgage loans are out. Local lenders with community roots are the preferred choice.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 5 of 16

2 http://ml-implode.com/index.html#lists

3 Several on the list remain very much in business, such as Freddie and Fannie, both of which remain active market participants and are playing a vital role in today’s mortgage lending market.

‘Internal’ Competition is Down, Too

Last Spring Prime Alliance made the statement Auto Lending is Showing its Age in several presentations it made around the country, including during its own Symposium in May 2008.

Using monthly auto and light truck sales data from the US Department of Commerce, we learn this trend began in November 2006, with negative growth in auto sales for the month, when compared with the same period one year prior. While there had been some earlier months with negative growth, the consistently negative growth trend began then. It continued through all of 2007 and 2008, with December of ’08 reporting a 35% decrease in sales when compared with the same month in 2007. This trend is now 26 months old, running three months longer than the previous record set beginning in April 1979.

How long will it continue? “The most optimistic predictions for 2009 call for people to buy about 13.5 million cars and trucks, down from more than 16 million in 2007. Pessimistic predictions range as low as 11 million,” according to Cleveland.com.

This doesn’t mean the credit union industry’s long relationship with auto lending is over. History shows us otherwise. Auto sales boomed after the recession of the late 1970s, then again after the recession of the early 1990s. Global Insight forecasts auto sales in 2010 could reach 15 million vehicles, with similar results for 2011.

What this means for credit unions is this: housing finance must become a core strategy. Housing will be one of the sectors to lead this economy out of recession. Mortgage lending is also a relationship strategy, especially when we focus on first-time homebuyers.

Part II: Six Suggestions

(1)Market, Advertise, Promote

What, are we nuts? How can anyone in their right mind suggest credit unions increase their marketing efforts with loan volumes at historic levels? Easy. As busy as we are, too many members still aren’t aware their credit union is the safest, most trustworthy, most reliable, most competitive mortgage lender they’ll encounter on their journey to purchase or refinance their home. The general public, though more aware than they were in 2006, still doesn’t recognize us as viable mortgage lenders, either.

Now is the time to tell them, for three reasons. First, consumers - - members and non-members alike - - are more receptive than ever to our message. While the phrase has grown trite - - credit union’s are the safe, trustworthy, reliable lenders that offer affordable, sustainable financing - - the values associated with these words are timeless. Oldest among the rules of advertising is this: your message hasn’t sunk in until your customers are tired of hearing it. It’s a good sign we’re tired of hearing it. We have a ways to go before the same can be said for our membership and for the general public.

Second, there are fewer options available to them. We discussed this in Part I. There are drastically fewer mortgage brokers, and rules for those that remain are much more stringent in most parts of the country. Fewer mortgage lenders are advertising as well; some that were familiar names just two years ago are now simply a part of history. Time to capitalize on this shift in the landscape. It’s not that all competitors are gone, that’s hardly the case. Competition is still difficult, though it is likely to be closer to home. Other local lenders, community banks and small mortgage companies, are vying for your members’ business. This is why our industry must market now to build lasting brand awareness. With so many consumers looking to refinance, we’ll have an opportunity to prove we’re the best solution, too.

Third, many consumers who haven’t yet refinanced could be financially advantaged by so doing. With all the news about tight credit and the credit freeze, some believe refinancing is not an option for them when, in fact, it is exactly the right thing for them to do. Call it advertising, marketing, promotion, or, in this case, more properly education, letting the general public know their local credit union can help them choose the best long-term financing solution for their situation builds long-term relationships as well as the credit union’s brand.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 6 of 16

Market, Advertise, Promote: The Take-Away

Not sure where to start? Don’t have time to create new marketing materials? No worries, visit www.mortgagestartshere.com, Prime Alliance’s ready-made mortgage marketing website, for all of your mortgage marketing needs. Another excellent resource on marketing from a strategic perspective is the CU Housing RoundTable’s Appoint a Housing Czar White Paper, available for download at www.cuhousingroundtable.com/publications.

(2)Shuffle the Deck

Notice something about auto lending volumes? Chances are they’re at some of the lowest levels you’ve experienced, a market dynamic that is unlikely to change for several years, driven by lack of consumer confidence and dismal trade-in values. Members will be driving their cars longer which means you’ll be financing fewer new and used car purchases. (See ‘Internal Competition is Down, Too’ sidebar, page 5.)

While that’s not the best news for credit unions since auto lending is a core business and competence, it does mean that consumer lending staff might be available to lend a hand in the mortgage department. This is easily done with Prime Alliance’s Retail Lending Center and Loan Fulfillment Center technologies. Our aim was to make it easier to process loans, part of our pledge to increase lending efficiencies and reduce costs. We did so by providing a task list for each mortgage that anyone even slightly familiar with lending can follow. Long learning curves are a thing of the past; most staff new to the mortgage department become productive in one or two days.

While hiring temporary workers is always an option, and one used extensively by mortgage lenders during peak periods, using the credit union’s existing staff makes more sense. They know your membership, they know your credit union, plus they bring skills that temporary employees don’t always have. There’s another benefit, too. According to a news story early this year, 9 out of 10 credit unions planned no lay-offs. With volumes at record highs, there’s no need since there’s enough loans in the mortgage department that everyone can make a contribution.

Prime Alliance Solutions, Inc., will publish a White Paper later this quarter on managing through the peaks and valleys inherent in housing finance. Using staff from across the credit union is one strategy, temporary employees is another it will discuss, among other innovative ideas for managing housing finance cycles.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 7 of 16

Shuffle the Deck: The Take-Away

Get your management team together to discuss - - and take action on - - utilizing credit union staff from other areas of the credit union. Keeping your service levels high in times of high volume builds your credit union’s brand as a lender that consistently delivers. It is also important from a cost standpoint. Missed locks and missing delivery commitments become very expensive very quickly.

(3)Pricing

Warning: this is going to get technical, there’s no other way. Mortgage loan pricing may be our achilles heel, yet it is also the key to success for lending this year. Pricing is not as complex as it seems, once you understand the components and follow one simple rule: focus on the few variables you can control, especially those where the impact is greatest.

Before delving into the mechanics of pricing, there are a few items we ought to consider. First, rates are at historic lows, mainly because the Treasury is purchasing the GSE’s mortgage-backed securities (MBS). Everyone, borrowers and lenders alike holds the expectation that rates will rise as soon as government intervention ceases.

Second, everyone recognizes that, while rates are low, credit remains tight, which makes credit more expensive. We’re all familiar with loan level price adjustments (LLPA). We - - all lenders - - are subject to ever-increasing and increasingly complex secondary market pricing adjustments that simply didn’t exist 18 months ago.In that sense, though, the pricing field remains level. We all start with the same secondary market price; we’re all subject to the same adjustments. With Prime Alliance Solutions, your credit union, however, has an advantage over many other lenders. We’ve built the adjustments into our pricing engine, and as they change, we will continue to do so. As a result your members get the right loan rate at the time of origination. Your loan officers needn’t fumble with price sheets, scratch pads and calculators.

Third, mortgage loans made at today’s rates will have very long durations. Members with 30 and 15 year fixed rate loans in the 5% or under range will have very little incentive to refinance. It is even possible 15 year mortgage loans may have a longer life-span than 30s, simply because members who finance with 15 year loans most likely plan on staying in their home and paying it off. Placing any or too many 5% fixed rate loans in your portfolio places pressure on your balance sheet, especially as rates rise months or years in the future. Having a serious senior management discussion now about sell/hold practices in this rate environment will make for easier asset/liability management now and in the future.

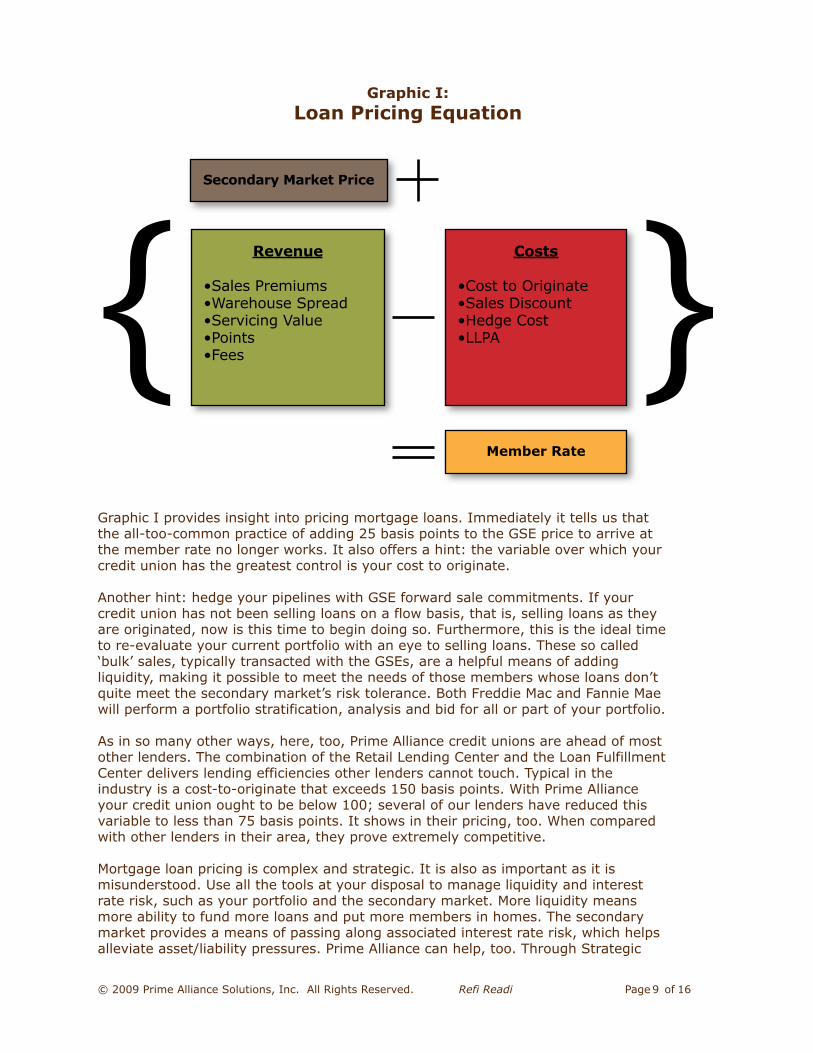

Back to pricing and the simple rule: manipulate the variables over which you have control. Take a look at Graphic I, the loan pricing equation, which shows each variable in the equation:

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 8 of 16

Graphic I:Loan Pricing Equation

Graphic I provides insight into pricing mortgage loans. Immediately it tells us that the all-too-common practice of adding 25 basis points to the GSE price to arrive at the member rate no longer works. It also offers a hint: the variable over which your credit union has the greatest control is your cost to originate.

Another hint: hedge your pipelines with GSE forward sale commitments. If your credit union has not been selling loans on a flow basis, that is, selling loans as they are originated, now is this time to begin doing so. Furthermore, this is the ideal time to re-evaluate your current portfolio with an eye to selling loans. These so called ‘bulk’ sales, typically transacted with the GSEs, are a helpful means of adding liquidity, making it possible to meet the needs of those members whose loans don’t quite meet the secondary market’s risk tolerance. Both Freddie Mac and Fannie Mae will perform a portfolio stratification, analysis and bid for all or part of your portfolio.

As in so many other ways, here, too, Prime Alliance credit unions are ahead of most other lenders. The combination of the Retail Lending Center and the Loan Fulfillment Center delivers lending efficiencies other lenders cannot touch. Typical in the industry is a cost-to-originate that exceeds 150 basis points. With Prime Alliance your credit union ought to be below 100; several of our lenders have reduced this variable to less than 75 basis points. It shows in their pricing, too. When compared with other lenders in their area, they prove extremely competitive.

Mortgage loan pricing is complex and strategic. It is also as important as it is misunderstood. Use all the tools at your disposal to manage liquidity and interest rate risk, such as your portfolio and the secondary market. More liquidity means more ability to fund more loans and put more members in homes. The secondary market provides a means of passing along associated interest rate risk, which helps alleviate asset/liability pressures. Prime Alliance can help, too. Through Strategic

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 9 of 16

Secondary Market Price

Revenue

•Sales Premiums•Warehouse Spread•Servicing Value•Points•Fees

Costs

•Cost to Originate•Sales Discount•Hedge Cost•LLPA{ }

Member Rate

Mortgage Solutions we have helped many credit unions reform their pricing models so that members see them as more competitive. These credit unions also achieve better financial results once all the components of pricing are understood and properly managed.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 10 of 16

Pricing: The Take-Away

First things first. You need to know the value of each pricing variable for your credit union. The next step is understanding how other local lenders are pricing. You want to price competitively, yet not overly so. Your credit union offers other, differentiating benefits such as a simpler borrowing experience and quicker close times. You may even be offering the only paperless process in town or, if you’ve taken the step, the only electronic mortgage in your area. We all know competing on price is important, but it’s not a long-term strategy. Market your credit union’s other benefits as well.

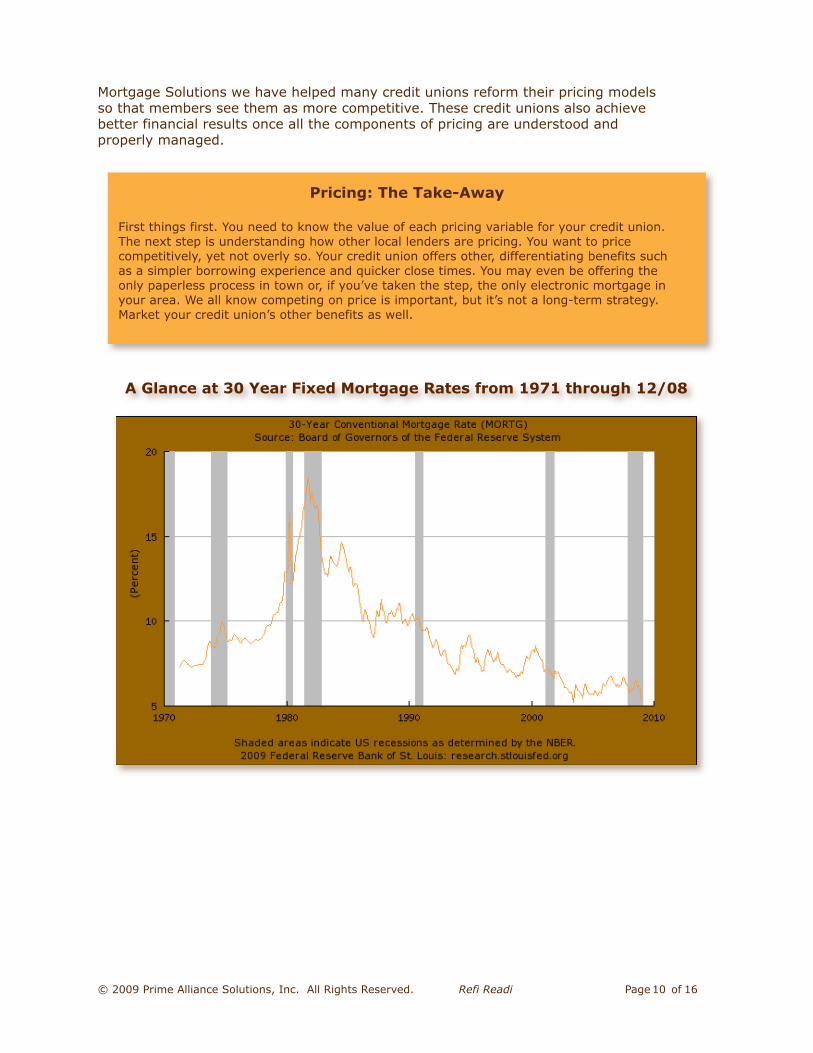

A Glance at 30 Year Fixed Mortgage Rates from 1971 through 12/08

(4)Product

We’re not sure about Justin Timberlake, but we do know that fixed-rate mortgage lending got its sexy back. Simple ARMs, too. Exotics are uncalled for in this market, the right and proper victims of their own unfortunate success. Members want financing they understand. Moreover, members want a mortgage they’re confident they can afford today, tomorrow, and possibly when the last payment is made 15 or 30 years from now.

This suggestion is very simple, that’s precisely the point. Keeping your product offerings simple and concise does two things for your credit union. First, it is yet another brand differentiator.Use this traditional, straightforward product mix as a means of communicating your credit union’s lending values. Consumers have become remarkably disillusioned with the mortgage industry and the havoc it’s wreaked on the economy. While mortgage literacy remains at an all-time low, awareness of what got us into this mess is high. Consumers understand no-documentation, no-down payment, negative amortization loans are bad financing choices. Yet they also understand the more traditional mortgage products that worked well for decades work still. Offering them in a clear, easy to understand fashion is a winning marketing tactic.

Second, a simple product mix reduces your costs. Maintaining a healthy, hefty product menu is expensive from many perspectives. Each product must be priced daily, disclosed appropriately, underwritten specially, then serviced accurately throughout its life. Lenders are jettisoning everything they aren’t using, that consumers don’t want, that investors won’t buy and that they perceive are bad financing tools. While we haven’t put a savings figure on it, we expect a slimmed-down menu could save your credit union one to two hours per day at a minimum.

Like so many other aspects of fallout from the sub-prime apocalypse, this, too, plays into our industry’s hands. Credit unions are quite competent fixed and adjustable rate lenders, and this is just what our members want.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 11 of 16

A Farewell to ARMs?

Not at all. Adjustable Rate Mortgages, ARMs, good ARMs, were excellent financing alternatives for some members before the sub-prime boom, and remain good products after the bust. Educating members to differentiate between good ARMs and bad ARMs is the key to helping them make the financing choice that is right for them.

What’s a bad ARM? Any adjustable rate product that counts among its features any of the following:

• Negative amortization;• Prepayment penalties;• Artificially low start rates and

payments; and• Options such as skipping

payments, making partial payments, paying only some principal or some interest; or

• Any combination of these four features.

One last thought on features. Some good ARMs offer low initial rates / payments. That feature, in and of itself, does not make an otherwise good ARM a bad loan.

Conventional ARMs can be the right choice, especially if the member knows they will only be in their home for a short time. Help your members understand the difference.

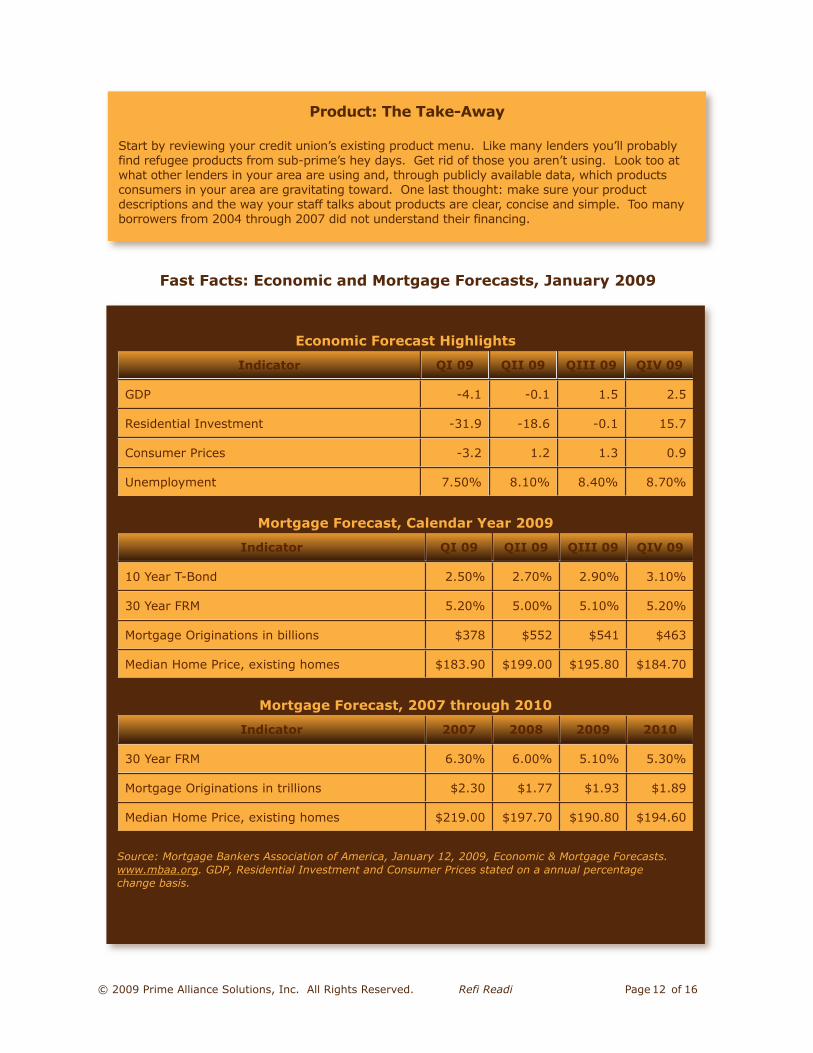

Fast Facts: Economic and Mortgage Forecasts, January 2009

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 12 of 16

Product: The Take-Away

Start by reviewing your credit union’s existing product menu. Like many lenders you’ll probably find refugee products from sub-prime’s hey days. Get rid of those you aren’t using. Look too at what other lenders in your area are using and, through publicly available data, which products consumers in your area are gravitating toward. One last thought: make sure your product descriptions and the way your staff talks about products are clear, concise and simple. Too many borrowers from 2004 through 2007 did not understand their financing.

Economic Forecast Highlights

Indicator QI 09 QII 09 QIII 09 QIV 09

GDP -4.1 -0.1 1.5 2.5

Residential Investment -31.9 -18.6 -0.1 15.7

Consumer Prices -3.2 1.2 1.3 0.9

Unemployment 7.50% 8.10% 8.40% 8.70%

Mortgage Forecast, Calendar Year 2009

Indicator QI 09 QII 09 QIII 09 QIV 09

10 Year T-Bond 2.50% 2.70% 2.90% 3.10%

30 Year FRM 5.20% 5.00% 5.10% 5.20%

Mortgage Originations in billions $378 $552 $541 $463

Median Home Price, existing homes $183.90 $199.00 $195.80 $184.70

Mortgage Forecast, 2007 through 2010

Indicator 2007 2008 2009 2010

30 Year FRM 6.30% 6.00% 5.10% 5.30%

Mortgage Originations in trillions $2.30 $1.77 $1.93 $1.89

Median Home Price, existing homes $219.00 $197.70 $190.80 $194.60

Source: Mortgage Bankers Association of America, January 12, 2009, Economic & Mortgage Forecasts. www.mbaa.org. GDP, Residential Investment and Consumer Prices stated on a annual percentage change basis.

(5)FHA

If it seems as though Prime Alliance sounds like a broken record on this topic, it’s because we predicted - - correctly - - that FHA lending would become a dominant product in a short period of time. We also believe this phenomenon is not short-lived.

There are five reasons FHA lending has become so popular:

1. Fixed rate loans at a decent rate. Earlier in Refi Readi© we discussed why rates are so low. If members are contemplating a purchase,especially a first home or a refinance, now is the time to make the move.

2. No Prepayment Penalties. Prepayment penalties went out of vogue many years ago, only to resurface as another, often surprise feature of many of the sub-prime loan products. There’s a misperception that FHA loans are hard for borrowers to understand. The truth is they are no more complicated, really, than a conventional loan, and there aren’t any ‘gotcha’s’ as there were with so many of the exotics that were popular during sub-prime’s hey days.

3. Simple Origination Process. While that didn’t used to be true, it is today. Using Prime Alliance, members can self-originate these loans just as they do conventional loans. They get the same on-line approval and their disclosures, too. For us, improving the member’s borrowing experience applies to all types of loans, not just conventional fixed rate and ARM products.

4. Low Down Payment. FHA may be the only loan available to borrowers who have as little as 3.5% down. As one colleague puts it, “97s are toast.” Another reason this is important is we can no longer count on Mortgage Insurance (MI) for our high loan -to-value (LTV) loans. Each passing month sees new metropolitan statistical areas (MSA) added to the distressed market list. Consequently, many areas of the country

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 13 of 16

Seizing the Opportunity

If market estimates for 2009 are correct, more than 12 million mortgage loans will be originated this year, up from approximately 8.5 million last year. Thirty percent of 12 million is 3.6 million loans, a significant number.

Just how big is the credit union industry’s opportunity in FHA lending? Starting with the overall market estimate and holding our share constant at 4%, we stand to grant 480,000 total mortgage loans during 2009. At 30% of the market, 144,000 of them should be FHA loans.

If we miss this opportunity, 144,000 members will finance elsewhere, leaving credit unions 336,000 loans to grant in the new year, or about the same number made during 2008. Taking a slightly different view, becoming active FHA lenders could be the difference between maintaining or growing the 4% market share credit unions have gained or backsliding to 3%. That’s simply because the market available to us, absent FHA loans, is almost exactly the same size as 2008’s market.

Credit unions can’t afford to let this chance slip by. FHA lending is not a passing fancy. This new market, with its return to more traditional lending standards, is here to stay. FHA was a staple of traditional lenders. It needs to become a staple for credit unions, too.

and practically all condos are limited to 90% LTV. As lenders that plan to concentrate on first-time homebuyers, buyers who have adequate income yet lack 20% down, we simply must offer FHA loans if we expect to make higher LTV loans. Under existing market conditions, this product is not only attractive, it’s the only way.

5. Easier Qualification. Loan level price adjustments (LLPAs) currently make it difficult for borrowers to qualify for conventional financing. While FHA loans, too, have their LLPAs, qualifying is easier. This is consistent with their history. FHA has its roots in affordability lending. This is one of the reasons first-time homebuyers flocked to FHA loans. If your the average age of most credit union members, maybe you financed your first home with a government loan. It may have made your first home purchase possible, and if you’re one of these people, it made your home sustainably affordable. Be the lender that offers your current members the same opportunity.

Predictions of FHA’s increasing importance have been consistent for at least six months. The number most bandied about is one-third of all borrowers will finance with this type of loan in 2009. To the extent these borrowers are members, most will have to use a lender other than their credit union. Our industry is behind the curve on this trend, and we’re losing market share because of it.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 14 of 16

A Brief History of FHA Lending

The Federal Housing Administration (FHA) was created in 1934 through the passage of the National Housing Act, one of the Government’s responses to the Great Depression and the resulting banking crisis of the early 1930s.

Prior to 1934 mortgage loans were short-term in nature, did not amortize and were callable. Consequently when the stock market collapsed in 1929, banks called many mortgage loans which resulted in a drastic rise in foreclosures.

FHA Lending was designed to prevent a similar crisis from happening again. Here we are, 78 years later, and Government Lending is once again coming to the rescue of many homeowners. It’s more than that, though. Federal Housing Administration Loans improved affordability then as today, proving everything old is new again.

FHA: The Take-Away

Do three things now. First, get educated, get partnered, get approved. Learn all you can about FHA lending (visit www.consultsms.com), find a partner that can jump start you into the business and start the approval process (www.fha.gov). Don’t delay, members want to rely on their credit union for loan products that will affordably and sustainably put them in their new home or keep them in their existing home. FHA Loans must be a staple on your menu, not simply as a daily or monthly special.

(6)From Traditional to Paperless to Electronic

Mortgage lending was, or is, depending on your point of reference, a paper-bound process. Prime Alliance’s Big, Hairy, Audacious Goal in 2000 was to take the entire process paperless, then electronic, within 10 years. We did it in eight.

First some definitions. Paperless lending, which is different from electronic lending, means handling the entire process, from origination through closing, without producing or handling a single piece of paper. Members, your loan officers, your branch and call center staffs, and others who originate for you all do so on-line. Assembling the mortgage file, including all service orders as well as documentation required from the member is also done using on-line and electronic fax technologies. Checking, verifying, underwriting, too, are all completed on-screen rather than in-file. When ready to close, closing documents are drawn on-line then emailed to the closing agent and the member, often times well ahead of the signing date. In a paperless mortgage, however, closing takes place using traditional paper mortgage documents because closing agents and recording authorities aren’t yet set-up for electronic mortgages.

Electronic mortgages are paperless mortgages that are closed electronically. Current technologies and laws have the member sign using a digital signature pad, with the help of a closing agent who is also a notary. With the simple click of a mouse and that one signature, the entire closing package is correctly signed. Final documents are then electronically distributed to all interested parties, including the recording authority. If the loan is destined for the secondary market, it is delivered electronically as well.

The benefits from paperless and electronic lending are obvious. Let’s consider paperless first. Imagine your mortgage department without files. Not on desks, not on file cabinets, not stacked on an underwriter’s desk, not nestled in a huge file room with a thousand others just like it. The savings from storage alone are significant, and lasting: space is expensive, as is paper, copies and couriers.

That’s not to mention gained efficiencies. The oft-heard call of the mortgage staff, “Who’s got the Smith file,” will be no more. All files are as close as the nearest internet-connected PC. Lenders that put two screens in front of every staffer watch productivity soar. One screen typically shows the loan’s ‘to do list’; the other the documentation or service order that requires verification. One of our credit unions has done the efficiency math. Mortgage staffers who work paperlessly gain as much as two hours’ productivity per day. Two hours per day. That equates to one .25 FTE.

Take the electronic mortgage step, assuming your local community is ready and efficiencies increase further. The real gain, though, is in the member experience. Think about the last time you personally signed for a mortgage. Loan documents typically run to more than 75 pages. Closed traditionally, the member must flip through each page, signing where appropriate, being very careful not to miss any spot that requires their John or Mary Hancock. This ancient ceremony usually takes about an hour and quite a few strokes of the pen. Closed electronically, just one signature is required; the entire closing takes less than five minutes. The best part from the member experience perspective - - other than the time

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 15 of 16

savings - - is that their copy of the closing package is handed to them on a USB drive. What once weighed three to five pounds and took up too much storage space now fits nicely in a pocket, briefcase or purse.

If your credit union is using Prime Alliance’s Loan Fulfillment Center you have all the technology you need to take the paperless / electronic step, save two things. We recommend two screens for every mortgage staffer. The small additional cost far outweighs the productivity gain. Second, you’ll need an e-fax system of some sort so loan documentation comes to your staff electronically. With these three things in place, and a cultural commitment to go paperless, your credit union will be on the cutting edge of mortgage lending.

SummaryWe hope you found Refi Readi© insightful and helpful. Prime Alliance believes the current low-rate, high volume environment could last for some time. And, while we know it is difficult to commit to new projects while business is brisk, none of these suggestions apply only to the refinance market. They work equally well in purchase-money markets, positioning your credit union as a highly competitive local lender that is on the cutting-edge of housing finance.

© 2009 Prime Alliance Solutions, Inc. All Rights Reserved. Refi Readi Page 16 of 16

From Traditional to Paperless to Electronic: The Take-Away

Not sure where to start? Talk with your Prime Alliance account executive today. We’ve helped a number of our credit unions make the leap, and we’ll be happy to point you in the right direction. Prime Alliance will be publishing a White Paper at the end of February 2009 on Paperless & Electronic Lending. It will contain additional information on the process of going paperless, the credit union and member experience as well as the productivity gains.

Refi ReadiSix Survival Suggestions for the next Six Months