repeal, replace, repair, rinse and...

TRANSCRIPT

1

Repeal, Replace, Repair, Rinse and Repeat The ACA/AHCA Rollercoaster and What it Means

for New York State

May 9, 2017

2Agenda

The latest from Washington:

American Health Care Act (AHCA) Summary and Status

Comparison of the AHCA with the Senate Proposal (Cassidy-Collins)

Comparison of AHCA to ACA—and its impact on key healthcare stakeholders and sectors

What’s at stake in New York: the current status of the ACA in NYS

The future of the Medicaid program

The prospect of a “capped” program

The implications for New York and behavioral care

3Key elements of AHCA

Basic construct of legislation is essentially the same as original bill that was not brought to a vote in late March

Repeals Individual and employer mandates

Transforms Medicaid to per capita cap/block grant option

Eliminates enhanced funding for Medicaid expansion

Restructures tax credits for Marketplace/individual market coverage

Eliminates most ACA taxes

State waiver option to opt out of insurance premium rating protections and requirements relating to Essential Health Benefits

$141 billion in new funds between 2018-2026 to stabilize individual and small group market (high risk pools/reinsurance programs), support maternity and newborn care/mental health & SUD services and to help people with pre-existing conditions

Source: New York State of Health, York State Department of Health

4Key elements of AHCA

Latest amendments intended to gain support of Freedom Caucus

Federal Invisible Risk Sharing Program, provides virtual high risk pool that provides $15 billion over nine years to address high cost enrollees’ costs

State Waivers would allow states

To replace the Essential Health Benefits with a state-defined benefit package,

To waive the continuous enrollment penalty and

To use health status as a rating factor for up to 12 months for any enrollees who has a gap in coverage

Prohibits premium rating by gender and purportedly precludes allowing insurers to limit health insurers from rejecting applicants based on pre-existing condition—but would still allow insurers to charge higher premiums

Upton amendment provides additional $8 billion (2018-23) to subsidize coverage in states that waive the continuous enrollment penalty and allow premiums to be set based on health status

Source: New York State of Health,

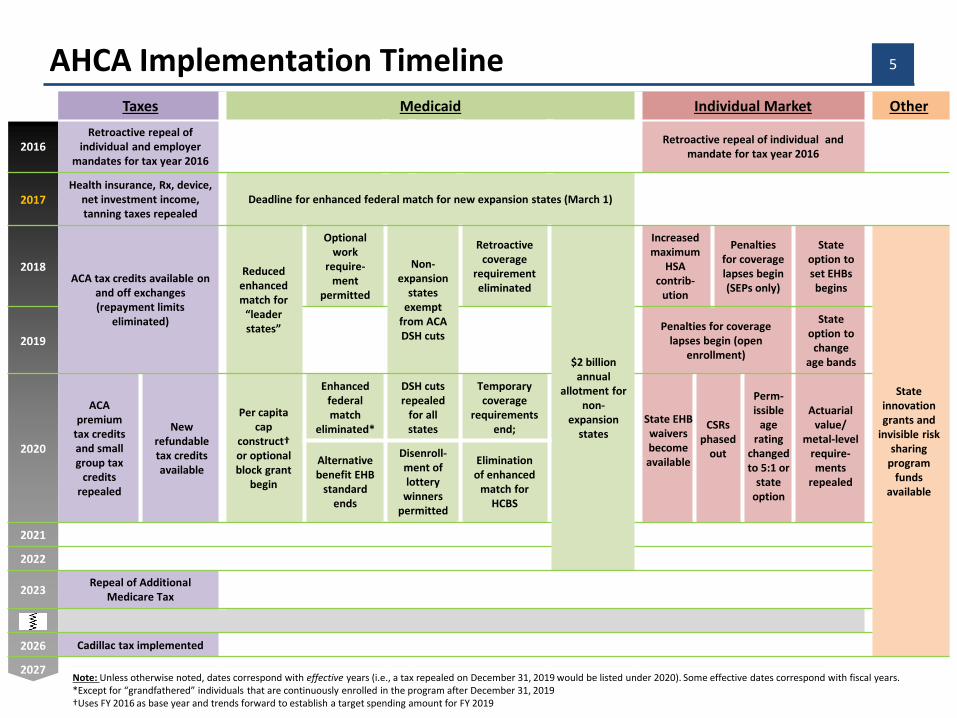

5AHCA Implementation TimelineTaxes Medicaid Individual Market Other

2016Retroactive repeal of

individual and employer mandates for tax year 2016

Retroactive repeal of individual and mandate for tax year 2016

2017Health insurance, Rx, device,

net investment income, tanning taxes repealed

Deadline for enhanced federal match for new expansion states (March 1)

2018ACA tax credits available on

and off exchanges (repayment limits

eliminated)

Reducedenhanced match for

“leader states”

Optional work

require-ment

permitted

Non-expansion

states exempt

from ACA DSH cuts

Retroactive coverage

requirement eliminated

$2 billion annual

allotment for non-

expansion states

Increased maximum

HSA contrib-

ution

Penalties for coverage lapses begin (SEPs only)

State option to set EHBs begins

State innovation grants and

invisible risk sharing

program funds

available

2019Penalties for coverage

lapses begin (open enrollment)

State option to

change age bands

2020

ACA premium

tax credits and small group tax

credits repealed

New refundable tax credits available

Per capita cap

construct† or optional block grant

begin

Enhanced federal match

eliminated*

DSH cuts repealed

for all states

Temporary coverage

requirements end;

Alternative benefit EHB

standard ends

Disenroll-ment of lottery

winners permitted

Elimination of enhanced

match for HCBS

2021

2022

2023Repeal of Additional

Medicare Tax

2026 Cadillac tax implemented

2027Note: Unless otherwise noted, dates correspond with effective years (i.e., a tax repealed on December 31, 2019 would be listed under 2020). Some effective dates correspond with fiscal years.*Except for “grandfathered” individuals that are continuously enrolled in the program after December 31, 2019†Uses FY 2016 as base year and trends forward to establish a target spending amount for FY 2019

CSRs phased

out

Actuarial value/

metal-level require-ments

repealed

Perm-issible

age rating

changed to 5:1 or

state option

State EHB waivers become available

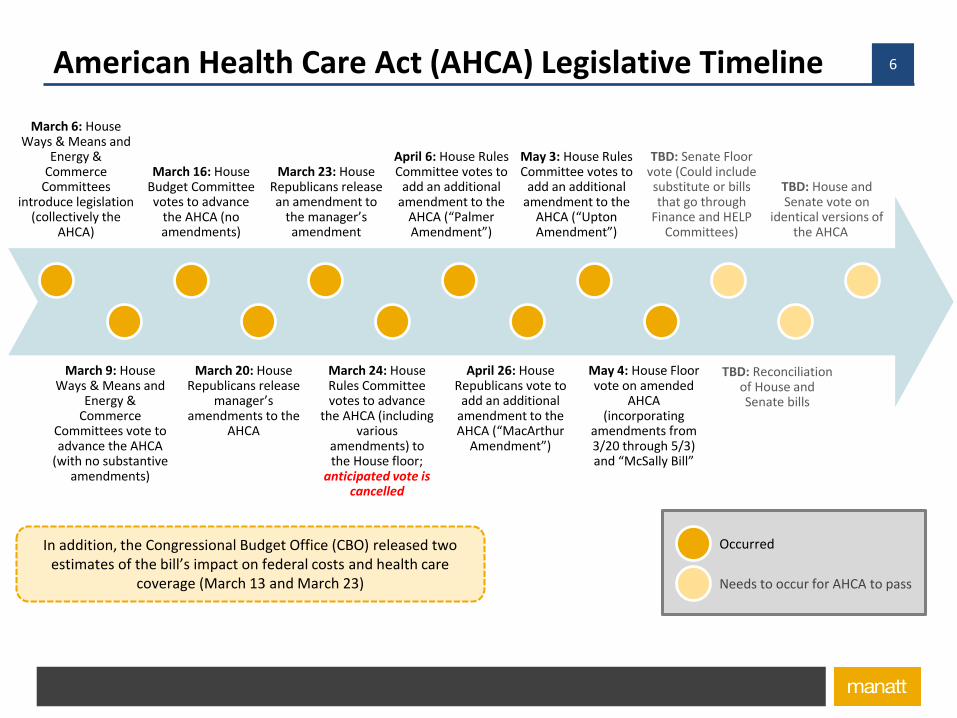

6American Health Care Act (AHCA) Legislative Timeline

In addition, the Congressional Budget Office (CBO) released two estimates of the bill’s impact on federal costs and health care

coverage (March 13 and March 23)

Occurred

Needs to occur for AHCA to pass

March 6: House Ways & Means and

Energy & Commerce

Committees introduce legislation

(collectively the AHCA)

March 9: House Ways & Means and

Energy & Commerce

Committees vote to advance the AHCA

(with no substantive amendments)

March 16: House Budget Committee votes to advance

the AHCA (no amendments)

March 20: House Republicans release

manager’s amendments to the

AHCA

March 23: House Republicans release an amendment to

the manager’s amendment

March 24: House Rules Committee votes to advance

the AHCA (including various

amendments) to the House floor;

anticipated vote is cancelled

May 4: House Floor vote on amended

AHCA (incorporating

amendments from 3/20 through 5/3) and “McSally Bill”

TBD: Senate Floor vote (Could includesubstitute or bills that go through

Finance and HELP Committees)

TBD: Reconciliation of House and Senate bills

TBD: House and Senate vote on

identical versions of the AHCA

April 6: House Rules Committee votes to

add an additional amendment to the

AHCA (“Palmer Amendment”)

April 26: House Republicans vote to

add an additionalamendment to the AHCA (“MacArthur

Amendment”)

May 3: House Rules Committee votes to

add an additional amendment to the

AHCA (“Upton Amendment”)

7Rose Garden Celebration of AHCA Passage in the House

President Trump and Republican House Leadership Jubilant

Over Passage of AHCA

8Some other recent celebrations

Atlanta Falcon Owners Celebrate Commanding

Lead in Super Bowl

9Some other recent celebrations

“La La Land” Wins Best Picture at Academy Awards

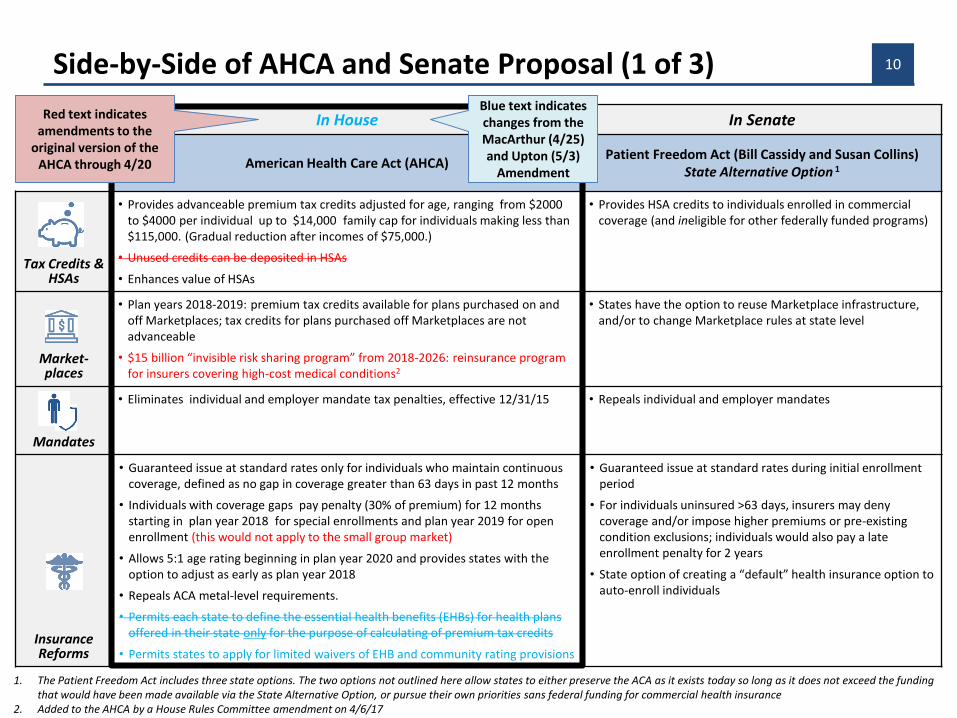

10Side-by-Side of AHCA and Senate Proposal (1 of 3)

In House In Senate

American Health Care Act (AHCA)Patient Freedom Act (Bill Cassidy and Susan Collins)

State Alternative Option 1

Tax Credits & HSAs

• Provides advanceable premium tax credits adjusted for age, ranging from $2000 to $4000 per individual up to $14,000 family cap for individuals making less than $115,000. (Gradual reduction after incomes of $75,000.)

• Unused credits can be deposited in HSAs

• Enhances value of HSAs

• Provides HSA credits to individuals enrolled in commercial coverage (and ineligible for other federally funded programs)

Market-places

• Plan years 2018-2019: premium tax credits available for plans purchased on and off Marketplaces; tax credits for plans purchased off Marketplaces are not advanceable

• $15 billion “invisible risk sharing program” from 2018-2026: reinsurance program for insurers covering high-cost medical conditions2

• States have the option to reuse Marketplace infrastructure,and/or to change Marketplace rules at state level

Mandates

• Eliminates individual and employer mandate tax penalties, effective 12/31/15 • Repeals individual and employer mandates

Insurance Reforms

• Guaranteed issue at standard rates only for individuals who maintain continuous coverage, defined as no gap in coverage greater than 63 days in past 12 months

• Individuals with coverage gaps pay penalty (30% of premium) for 12 months starting in plan year 2018 for special enrollments and plan year 2019 for open enrollment (this would not apply to the small group market)

• Allows 5:1 age rating beginning in plan year 2020 and provides states with the option to adjust as early as plan year 2018

• Repeals ACA metal-level requirements.

• Permits each state to define the essential health benefits (EHBs) for health plans offered in their state only for the purpose of calculating of premium tax credits

• Permits states to apply for limited waivers of EHB and community rating provisions

• Guaranteed issue at standard rates during initial enrollment period

• For individuals uninsured >63 days, insurers may deny coverage and/or impose higher premiums or pre-existing condition exclusions; individuals would also pay a late enrollment penalty for 2 years

• State option of creating a “default” health insurance option to auto-enroll individuals

1. The Patient Freedom Act includes three state options. The two options not outlined here allow states to either preserve the ACA as it exists today so long as it does not exceed the funding that would have been made available via the State Alternative Option, or pursue their own priorities sans federal funding for commercial health insurance

2. Added to the AHCA by a House Rules Committee amendment on 4/6/17

Red text indicates amendments to the

original version of the AHCA through 4/20

Blue text indicates changes from the MacArthur (4/25) and Upton (5/3)

Amendment

11Side-by-Side of AHCA and Senate Proposal (2 of 3)

1. The Patient Freedom Act includes three state options. The two options not outlined here allow states to either preserve the ACA as it exists today so long as it does not exceed the funding that would have been made available via the State Alternative Option, or pursue their own priorities sans federal funding for commercial health insurance

In House In Senate

American Health Care Act (AHCA)Patient Freedom Act (Bill Cassidy and Susan

Collins) State Alternative Option 1

FederalFunding to

States

• $100 billion in State Innovation Grants for CY 2018-2026 with distribution formula based on enrollment, insurer participation, claims, and poverty. States can use funds for broad range of purposes

• $15 billion in additional grants to support maternity and newborn care or mental health and substance abuse treatment from 2020 through 2026

• $8 billion for CY 2018-2023 to help individuals subject to increased premiums as a result of a MacArthur waiver permitting rating based on health status

• $2 billion per year in supplemental funds annually for non-expansion states available 2018-2022 to increase payments to Medicaid providers

Not addressed

Medicaid Expansion

• Maintains Medicaid expansion for states that have already expanded but eliminates enhanced federal funding effective CY 2020 for all but grandfathered enrollees (if they maintain continuous coverage after December 31, 2019)

• Terminates EHB requirement for expansion adult coverage

• Reduces mandatory coverage for children age 6-19 from 138% to 100% of FPL

• Sunsets enhanced federal match for new expansions effective March 1, 2017

• States that do not adopt Medicaid expansion would receive a heightened federal subsidy for HSAs (repurposing the dollars that would have been received for expanding Medicaid, without the “matching” requirement)

Medicaid Financing

• Aggregate cap on state Medicaid spending starting in FY 2020

• Per capita caps on spending across five categories are trended forward by either medical CPI (aged, blind and disabled, children, expansion adults, and other non-elderly/non-disabled/non-expansion adults) or by medical CPI plus one percentage point (elderly and blind/disabled groups)

• Uses FY 2016 as base year to establish a target spending amount for FY 2019; DSH payments excluded under cap; UPL payments included under cap; treatment of waiver payments unclear

• State option of block grants for children and non-disabled adults trended forward by CPI-U

No changes from ACA (other than to re-purpose Medicaid expansion dollars if selected by state as

outlined above)

DSH

• ACA DSH cuts repealed beginning in FY 2020

• Non-expansion states exempt from cuts beginning in FY 2018Not addressed

12Side-by-Side of AHCA and Senate Proposal (3 of 3)

1. The Patient Freedom Act includes three state options. The two options not outlined here allow states to either preserve the ACA as it exists today so long as it does not exceed the funding that would have been made available via the State Alternative Option, or pursue their own priorities sans federal funding for commercial health insurance1. The Patient Freedom Act includes three state options. The two options not outlined here allow states to either preserve the ACA as it exists today so long as it does not exceed the funding that would have been made available via the State Alternative Option, or pursue their own priorities sans federal funding for commercial health insurance

In House In Senate

American Health Care Act (AHCA)Patient Freedom Act (Bill Cassidy and Susan Collins)

State Alternative Option 1

RevenueRaising Taxes

• Eliminates most revenue raisers in 2017

• Repeals Additional Medicare Tax in 2023

• Cadillac tax delayed until CY 2026

• Keeps revenue-generating taxes to finance tax credits

Medicare

Not addressed Not addressed

Delivery System Reform

Not addressed Not addressed

Abortion Coverage

• Prohibits using tax credits to purchase plans that cover abortion

• Prohibits for one year any Medicaid, CHIP, Maternal and Child Health Services Block Grant and Social Services Block Grant funding for Planned Parenthood

Not addressed

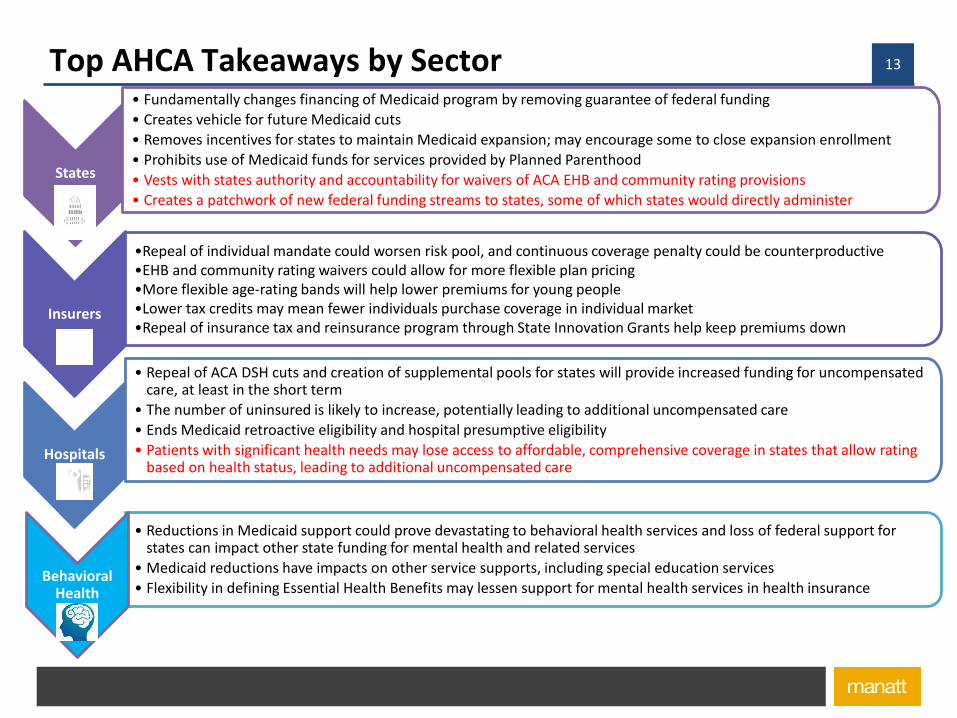

13Top AHCA Takeaways by Sector

States

• Fundamentally changes financing of Medicaid program by removing guarantee of federal funding

• Creates vehicle for future Medicaid cuts

• Removes incentives for states to maintain Medicaid expansion; may encourage some to close expansion enrollment

• Prohibits use of Medicaid funds for services provided by Planned Parenthood

• Vests with states authority and accountability for waivers of ACA EHB and community rating provisions

• Creates a patchwork of new federal funding streams to states, some of which states would directly administer

Insurers

•Repeal of individual mandate could worsen risk pool, and continuous coverage penalty could be counterproductive•EHB and community rating waivers could allow for more flexible plan pricing •More flexible age-rating bands will help lower premiums for young people•Lower tax credits may mean fewer individuals purchase coverage in individual market•Repeal of insurance tax and reinsurance program through State Innovation Grants help keep premiums down

Hospitals

• Repeal of ACA DSH cuts and creation of supplemental pools for states will provide increased funding for uncompensated care, at least in the short term

• The number of uninsured is likely to increase, potentially leading to additional uncompensated care

• Ends Medicaid retroactive eligibility and hospital presumptive eligibility

• Patients with significant health needs may lose access to affordable, comprehensive coverage in states that allow rating based on health status, leading to additional uncompensated care

• Reductions in Medicaid support could prove devastating to behavioral health services and loss of federal support for states can impact other state funding for mental health and related services

• Medicaid reductions have impacts on other service supports, including special education services

• Flexibility in defining Essential Health Benefits may lessen support for mental health services in health insuranceBehavioral

Health

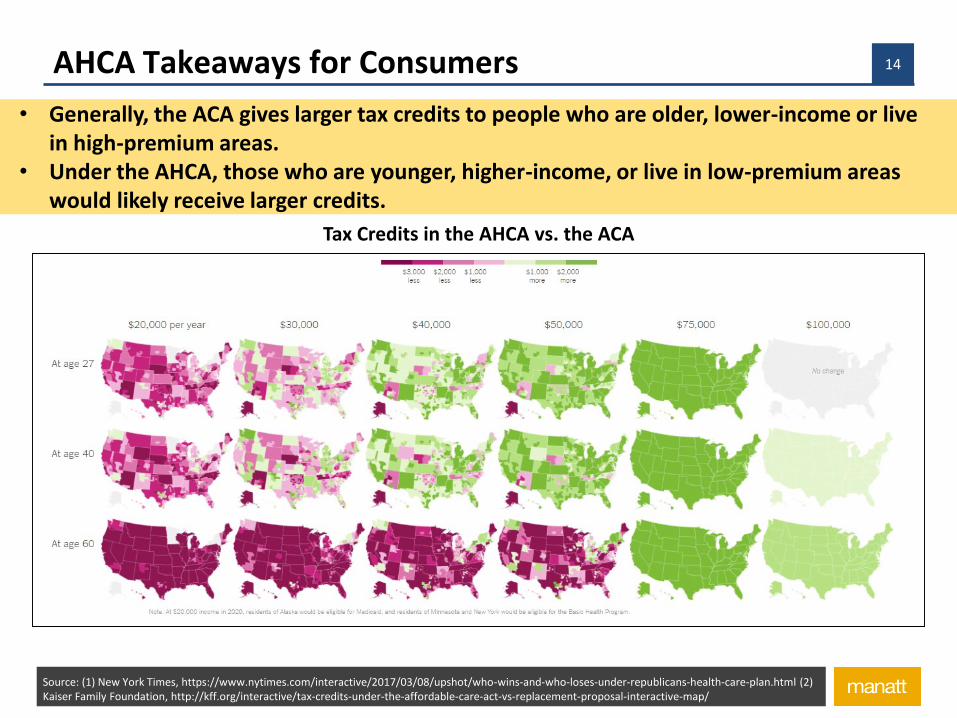

14AHCA Takeaways for Consumers

• Generally, the ACA gives larger tax credits to people who are older, lower-income or live in high-premium areas.

• Under the AHCA, those who are younger, higher-income, or live in low-premium areas would likely receive larger credits.

Tax Credits in the AHCA vs. the ACA

Source: (1) New York Times, https://www.nytimes.com/interactive/2017/03/08/upshot/who-wins-and-who-loses-under-republicans-health-care-plan.html (2) Kaiser Family Foundation, http://kff.org/interactive/tax-credits-under-the-affordable-care-act-vs-replacement-proposal-interactive-map/

15The elephant in the room

16Trump Administrative Actions Could Dismantle Much of ACA

Administration can issue new regulations and executive orders and establish new policies within statutory guidelines at any time

o Can suspend any rule that has not taken effect, 60 days for major rules

o Can reshape many policies by waivers/demonstrations: Some state Medicaid programs are run completely under waiver authority

o Some of the policies included in “replace” proposals could be achieved by administrative action (e.g., changes to essential health benefits)

Cost Sharing Reduction litigation: pending case can doom subsidy payments that make coverage on the exchange affordable

Both the bully pulpit, as well as formal issuance of Executive Orders, can result in dismantling the ACA

Trump’s use of administrative actions (directives that guide executive action and set requirements for stakeholders but do not require congressional approval, such as

regulations, waivers and enforcement policies) could significantly alter federal policy.

17Day One

First Executive Order instructs the HHS Secretary to “exercise all authority and discretion available to them to waive, defer, grant exemptions from, or delay” parts of the law that would place a fiscal burden on states, individuals or healthcare providers.”

18Current Post-ACA/Pre-AHCA Coverage in the United States

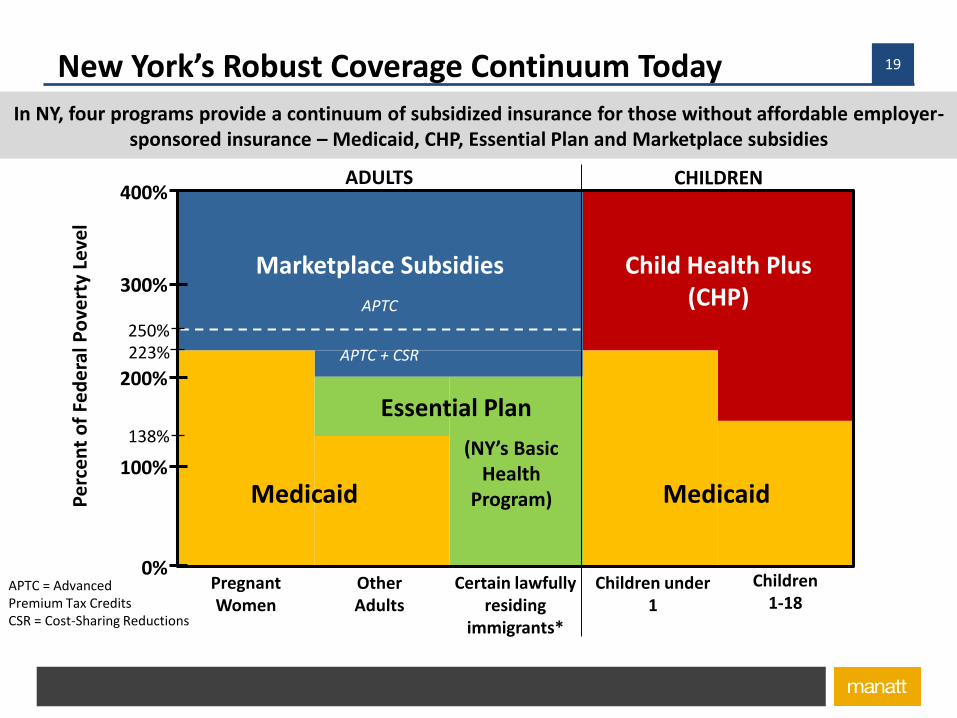

19New York’s Robust Coverage Continuum Today

*Per a 2001 NY Appeals Court decision (Aliessa v. Novello), legal immigrants in the federal 5-year ban and some categories of PRUCOL are

APTC = AdvancedPremium Tax CreditsCSR = Cost-Sharing Reductions

200%

400%

0%

100%

300%

Pregnant Women

Other Adults

Essential Plan

(NY’s Basic Health

Program)Medicaid Medicaid

Marketplace Subsidies Child Health Plus (CHP)

APTC + CSR

APTC

Certain lawfully residing

immigrants*

Children under 1

Children 1-18

Pe

rce

nt

of

Fed

era

l Po

vert

y Le

vel

223%

138%

250%

In NY, four programs provide a continuum of subsidized insurance for those without affordable employer-sponsored insurance – Medicaid, CHP, Essential Plan and Marketplace subsidies

ADULTS CHILDREN

20New York State of Health Performance

The New York State of Health has played an important role in expanding coverage for New Yorkers

The Exchange enrolled 3.6 million people in last enrollment period

2.4 million of that 3.6 million—two-thirds of the total—enrolled in Medicaid, which accounts for a substantial share of the total of 6.2 million enrolled in Medicaid

665,000 enrolled in the Essential Plan, made possible by the Basic Health Program provisions in the ACA

300,000 children enrolled in CHP through the exchange

242,000 enrolled in Qualified Health Plans for individual coverage, often viewed as the centerpiece of the ACA

Outside of the Exchange, roughly half of New Yorkers have employer-supplied coverage, twenty percent have Medicare

The combination of these efforts reduced uninsured rate in New York during the ACA’s tenure from around 10.7 percent to around 7 percent

Source: New York State of Health,

21Essential Plan

New York has leveraged the Basic Health Program to provide affordable coverage with significant State savings

New York is one of two states utilizing the ACA Basic Health Program option, creating the “Essential Plan”

The Essential Plan covers over 665,000 New Yorkers (as of January 2017) who are:

Individuals with incomes between 138% and 200% FPL who are ineligible for Medicaid/CHIP and do not have access to affordable employer-sponsored coverage

Individuals with incomes below 138% FPL who are ineligible for Medicaid due to immigration status (commonly know as Aliessa population)

Federal government provides the State with 95% of the premium tax credits and cost-sharing reductions that would have been available for coverage through the New York State of Health

Implementing the Basic Health Program has resulted in significant State savings due to decreases in State-only Medicaid expenditures for the Aliessa population.

State saved $1 billion in its first year alone, and projects savings of $804 million in SFY 16-17.

Source: New York State of Health, York State Department of Health

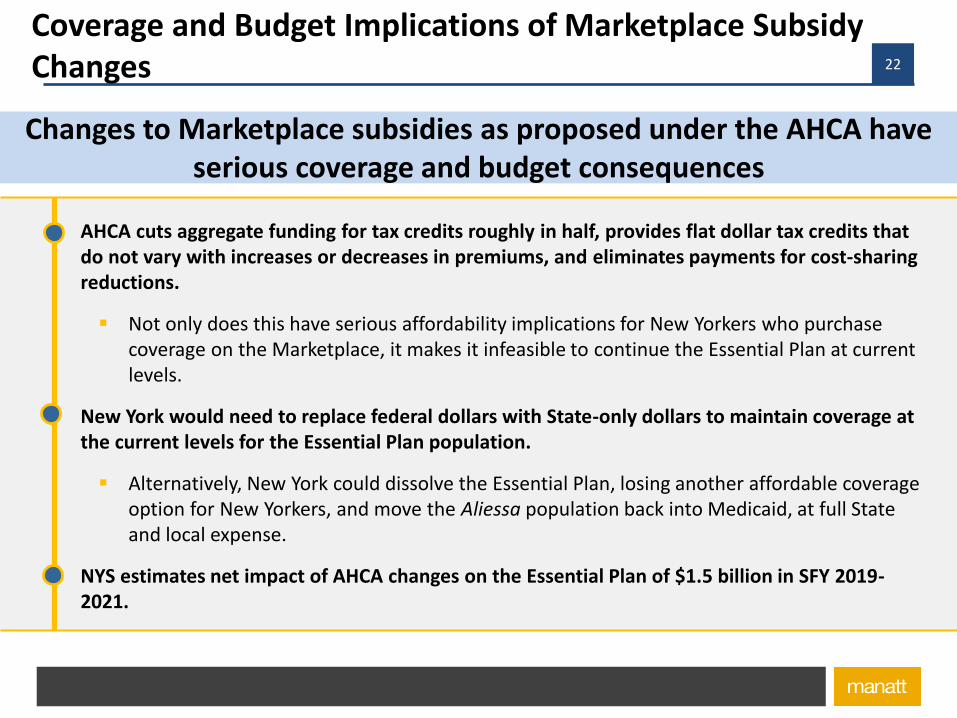

22

Changes to Marketplace subsidies as proposed under the AHCA have serious coverage and budget consequences

AHCA cuts aggregate funding for tax credits roughly in half, provides flat dollar tax credits that do not vary with increases or decreases in premiums, and eliminates payments for cost-sharing reductions.

Not only does this have serious affordability implications for New Yorkers who purchase coverage on the Marketplace, it makes it infeasible to continue the Essential Plan at current levels.

New York would need to replace federal dollars with State-only dollars to maintain coverage at the current levels for the Essential Plan population.

Alternatively, New York could dissolve the Essential Plan, losing another affordable coverage option for New Yorkers, and move the Aliessa population back into Medicaid, at full State and local expense.

NYS estimates net impact of AHCA changes on the Essential Plan of $1.5 billion in SFY 2019-2021.

Coverage and Budget Implications of Marketplace Subsidy Changes

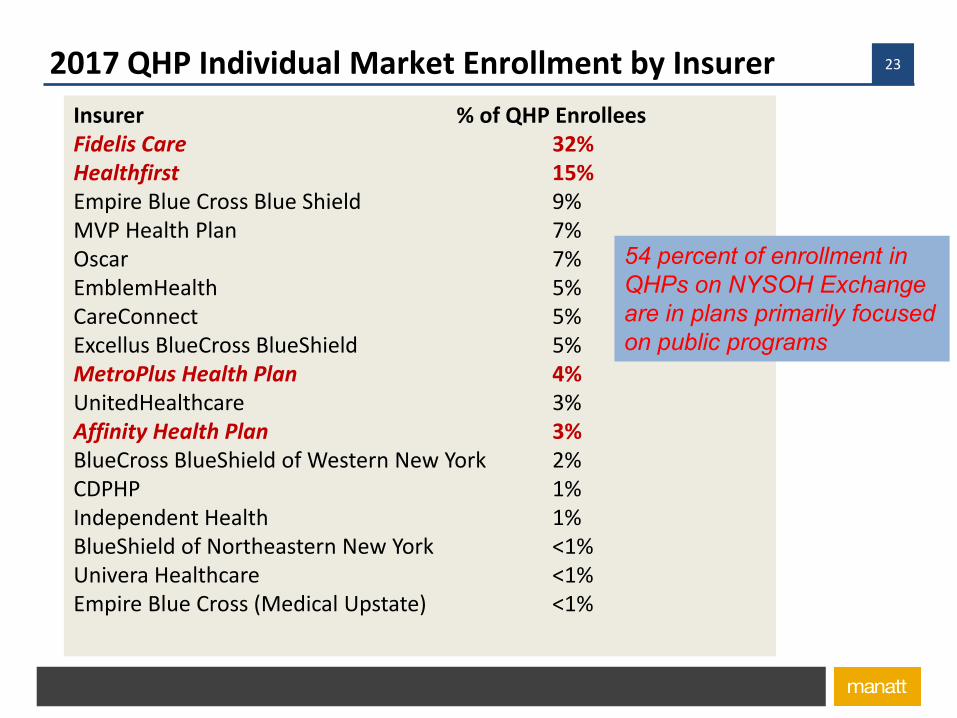

232017 QHP Individual Market Enrollment by Insurer

Insurer % of QHP Enrollees Fidelis Care 32% Healthfirst 15% Empire Blue Cross Blue Shield 9% MVP Health Plan 7% Oscar 7% EmblemHealth 5% CareConnect 5% Excellus BlueCross BlueShield 5% MetroPlus Health Plan 4% UnitedHealthcare 3% Affinity Health Plan 3% BlueCross BlueShield of Western New York 2% CDPHP 1% Independent Health 1% BlueShield of Northeastern New York <1% Univera Healthcare <1% Empire Blue Cross (Medical Upstate) <1%

54 percent of enrollment in

QHPs on NYSOH Exchange

are in plans primarily focused

on public programs

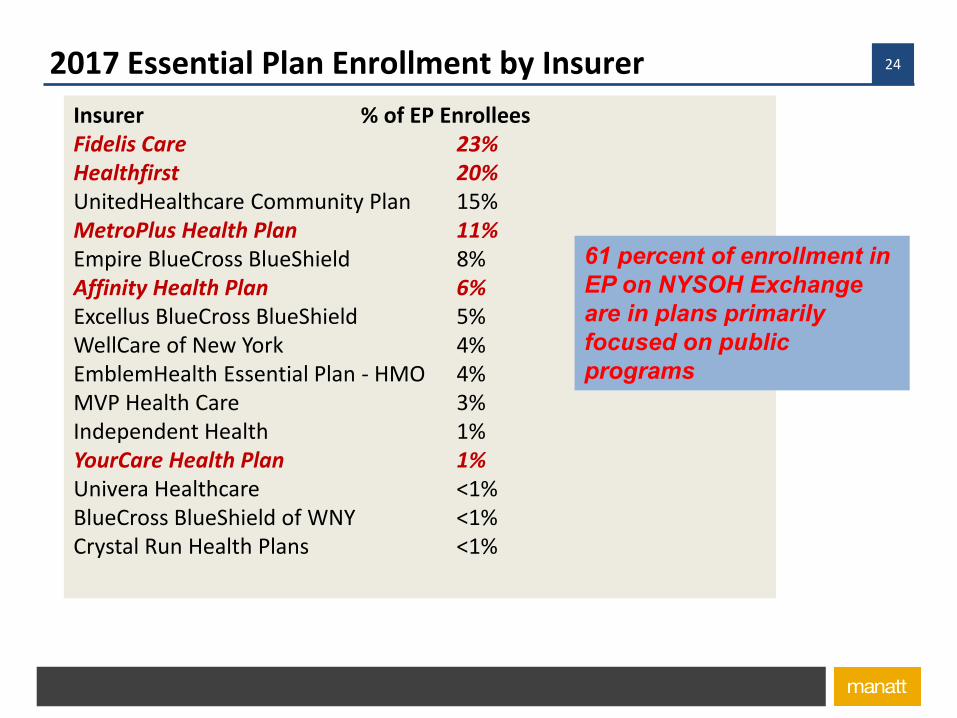

242017 Essential Plan Enrollment by Insurer

Insurer % of EP Enrollees Fidelis Care 23% Healthfirst 20% UnitedHealthcare Community Plan 15% MetroPlus Health Plan 11% Empire BlueCross BlueShield 8% Affinity Health Plan 6% Excellus BlueCross BlueShield 5% WellCare of New York 4% EmblemHealth Essential Plan - HMO 4% MVP Health Care 3% Independent Health 1% YourCare Health Plan 1% Univera Healthcare <1% BlueCross BlueShield of WNY <1% Crystal Run Health Plans <1%

61 percent of enrollment in

EP on NYSOH Exchange

are in plans primarily

focused on public

programs

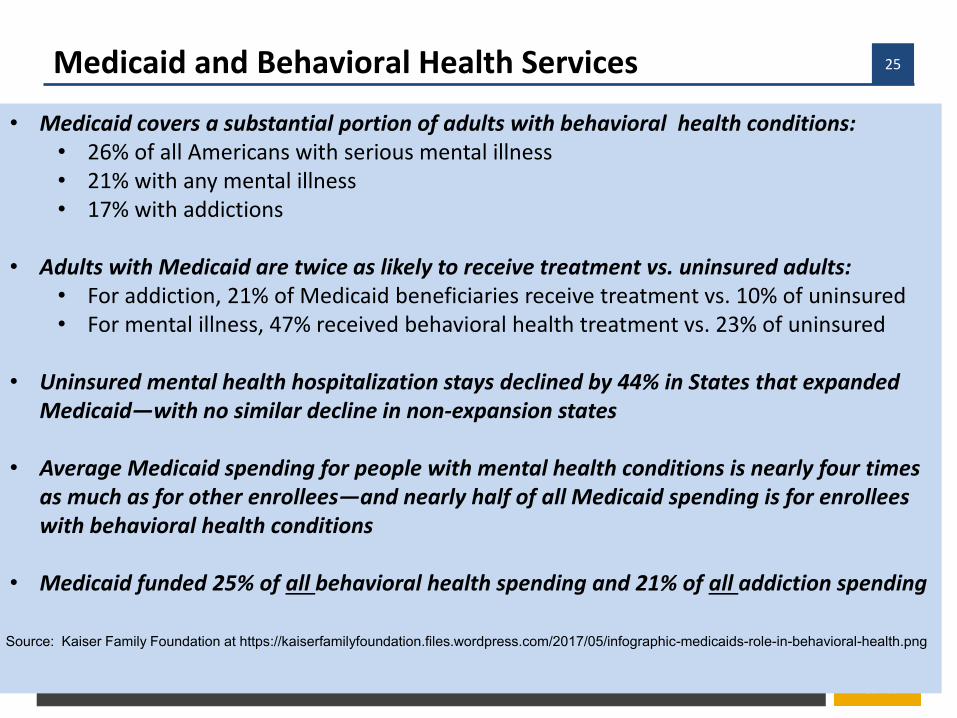

25Medicaid and Behavioral Health Services

• Medicaid covers a substantial portion of adults with behavioral health conditions:• 26% of all Americans with serious mental illness• 21% with any mental illness• 17% with addictions

• Adults with Medicaid are twice as likely to receive treatment vs. uninsured adults:• For addiction, 21% of Medicaid beneficiaries receive treatment vs. 10% of uninsured• For mental illness, 47% received behavioral health treatment vs. 23% of uninsured

• Uninsured mental health hospitalization stays declined by 44% in States that expanded Medicaid—with no similar decline in non-expansion states

• Average Medicaid spending for people with mental health conditions is nearly four times as much as for other enrollees—and nearly half of all Medicaid spending is for enrollees with behavioral health conditions

• Medicaid funded 25% of all behavioral health spending and 21% of all addiction spending

Source: Kaiser Family Foundation at https://kaiserfamilyfoundation.files.wordpress.com/2017/05/infographic-medicaids-role-in-behavioral-health.png

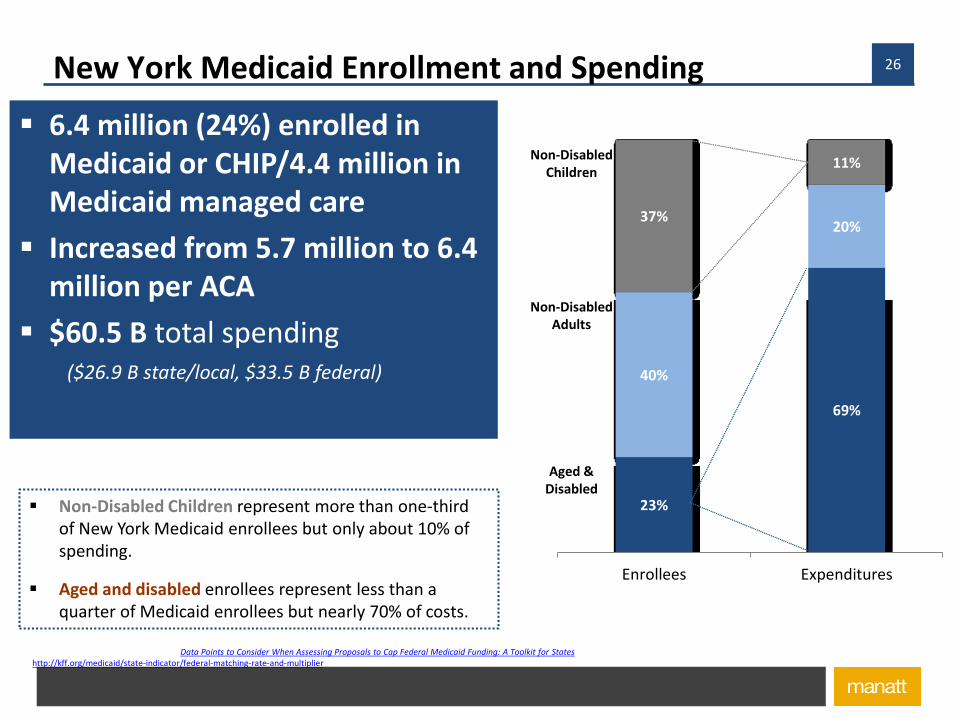

26New York Medicaid Enrollment and Spending

6.4 million (24%) enrolled in Medicaid or CHIP/4.4 million in Medicaid managed care

Increased from 5.7 million to 6.4 million per ACA

$60.5 B total spending ($26.9 B state/local, $33.5 B federal)

Sources: Robert Wood Johnson Foundation, “Data Points to Consider When Assessing Proposals to Cap Federal Medicaid Funding: A Toolkit for States”; Federal Medical Assistance Percentage (FMAP) FY17, http://kff.org/medicaid/state-indicator/federal-matching-rate-and-multiplier

Non-Disabled Children represent more than one-third of New York Medicaid enrollees but only about 10% of spending.

Aged and disabled enrollees represent less than a quarter of Medicaid enrollees but nearly 70% of costs.

23%

69%

40%

20%37%

11%

Enrollees Expenditures

Aged & Disabled

Non-Disabled Adults

Non-Disabled Children

27Medicaid’s Role in the New York Budget

Sources: Manatt analysis of National Association of State Budget Officers (NASBO) State Expenditure Report, 2016, available at https://higherlogicdownload.s3.amazonaws.com/NASBO/9d2d2db1-c943-4f1b-b750-0fca152d64c2/UploadedImages/SER%20Archive/State%20Expenditure%20Report%20(Fiscal%202014-2016)%20-%20S.pdf

Medicaid and Other Spending as aShare of State Funds in New York, SFY 2015

Sources of Federal Funds in New York’s State Budget, SFY 2015

Medicaid Public Assistance & Corrections

Elem. & Sec. Education Transportation

Higher Education All Other Expenditures

16.6%

24.3%

10.5%

4.3%

8.0%

36.2%

64.3%7.5%0.7%

5.9%

3.5%

18.1%

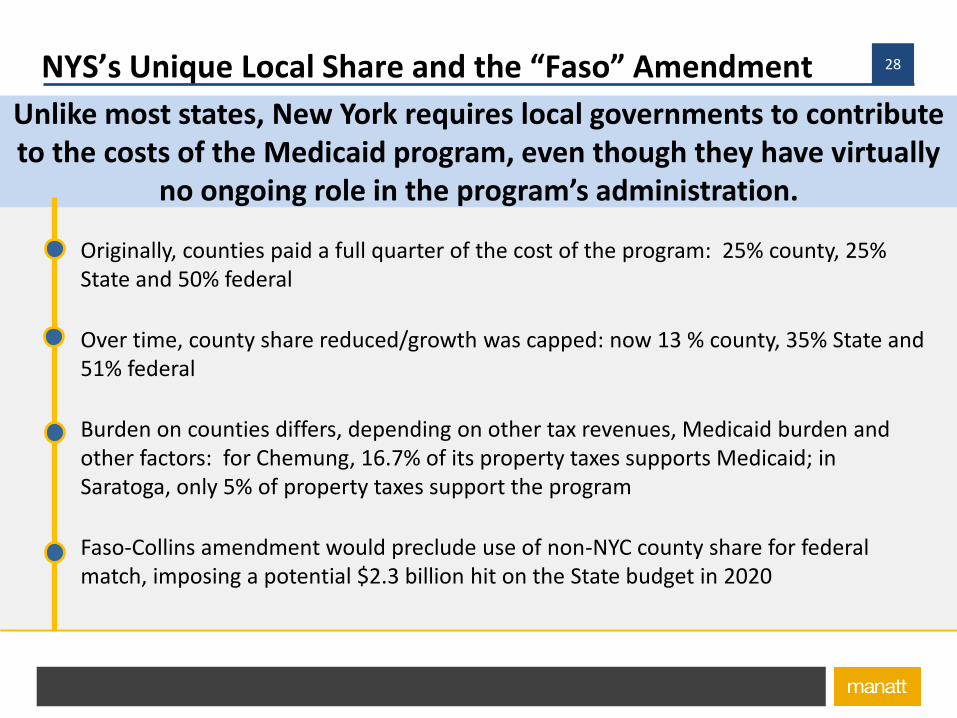

28NYS’s Unique Local Share and the “Faso” Amendment

Unlike most states, New York requires local governments to contribute to the costs of the Medicaid program, even though they have virtually

no ongoing role in the program’s administration.

Originally, counties paid a full quarter of the cost of the program: 25% county, 25% State and 50% federal

Over time, county share reduced/growth was capped: now 13 % county, 35% State and 51% federal

Burden on counties differs, depending on other tax revenues, Medicaid burden and other factors: for Chemung, 16.7% of its property taxes supports Medicaid; in Saratoga, only 5% of property taxes support the program

Faso-Collins amendment would preclude use of non-NYC county share for federal match, imposing a potential $2.3 billion hit on the State budget in 2020

Source: “

29Medicaid Expansion

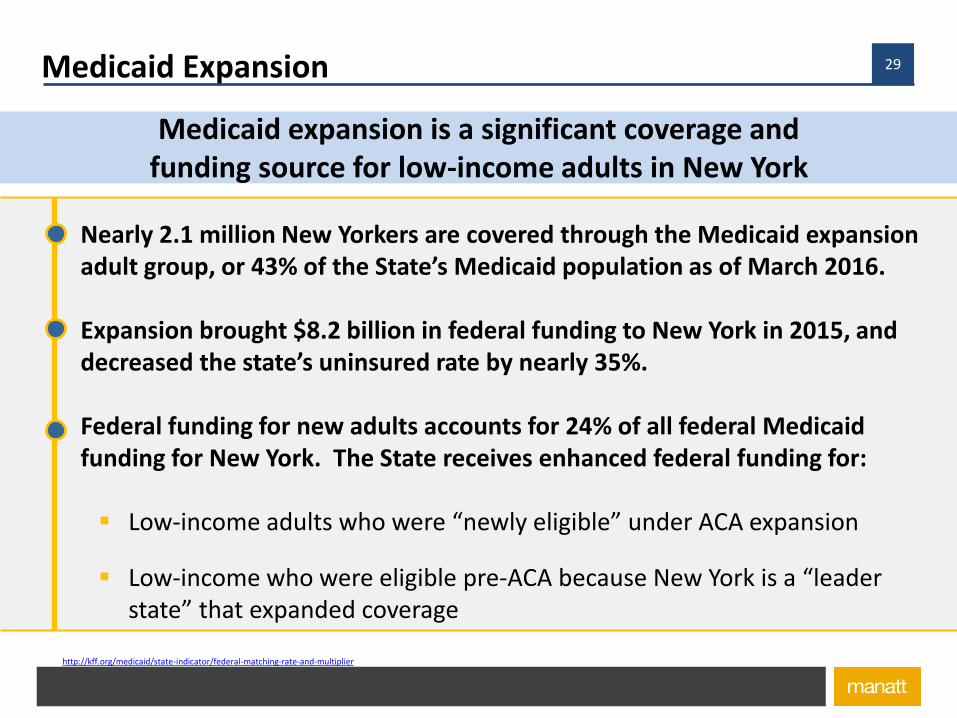

Medicaid expansion is a significant coverage and funding source for low-income adults in New York

Nearly 2.1 million New Yorkers are covered through the Medicaid expansion adult group, or 43% of the State’s Medicaid population as of March 2016.

Expansion brought $8.2 billion in federal funding to New York in 2015, and decreased the state’s uninsured rate by nearly 35%.

• Federal funding for new adults accounts for 24% of all federal Medicaid funding for New York. The State receives enhanced federal funding for:

Low-income adults who were “newly eligible” under ACA expansion

Low-income who were eligible pre-ACA because New York is a “leader state” that expanded coverage

Source: “Medicaid Capped Funding: Findings and Implications for New York,” prepared by Manatt Health for the Robert Wood Johnson Foundation State Network; Federal Medical Assistance Percentage (FMAP) FY17, http://kff.org/medicaid/state-indicator/federal-matching-rate-and-multiplier

30Enhanced Federal Match

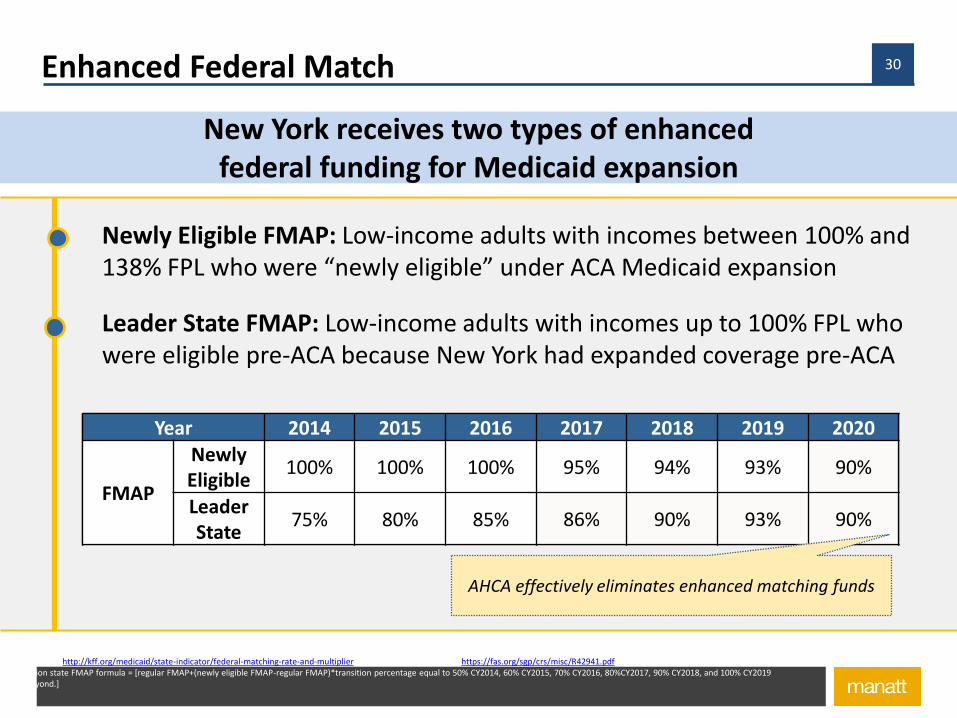

New York receives two types of enhanced federal funding for Medicaid expansion

Newly Eligible FMAP: Low-income adults with incomes between 100% and 138% FPL who were “newly eligible” under ACA Medicaid expansion

Leader State FMAP: Low-income adults with incomes up to 100% FPL who were eligible pre-ACA because New York had expanded coverage pre-ACA

Source: “Medicaid Capped Funding: Findings and Implications for New York,” prepared by Manatt Health for the Robert Wood Johnson Foundation State Network; Federal Medical Assistance Percentage (FMAP) FY17, http://kff.org/medicaid/state-indicator/federal-matching-rate-and-multiplier; Medicaid’s FMAP, FY2014, https://fas.org/sgp/crs/misc/R42941.pdfExpansion state FMAP formula = [regular FMAP+(newly eligible FMAP-regular FMAP)*transition percentage equal to 50% CY2014, 60% CY2015, 70% CY2016, 80%CY2017, 90% CY2018, and 100% CY2019 and beyond.]

Year 2014 2015 2016 2017 2018 2019 2020

FMAP

Newly Eligible

100% 100% 100% 95% 94% 93% 90%

Leader State

75% 80% 85% 86% 90% 93% 90%

AHCA effectively eliminates enhanced matching funds

31

Limiting Enhanced Funding to Grandfathered Individuals Will Have Significant Impact

AHCA eliminated enhanced funding for all except “grandfathered” individuals who remain continuously enrolled

Source: http://www.statenetwork.org/wp-content/uploads/2017/03/State-Network-Grandfathered-Medicaid-Enhanced-Match-March-2017.pdf

Based on states’ experiences with enrollment freezes, the number of beneficiaries for whom a state receives enhanced matching funds can be expected to dwindle rapidly.

14.3

7.2

4.93.8

3.02.1

1.1 0.7 0.5 0.4

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

Nu

mb

er o

f En

rolle

es (

mill

ion

s)

Year

Estimated Decrease Over Time in ContinuousEnrollment of Grandfathered Individuals

Total

New York

March 2016 March 2017 March 2018 March 2019 March 2020

By 2020, New York would receiveenhanced match for only 20% of its enrollees. NYS estimates net impact of $1.6 billion between

SFY 2017-2021.

32

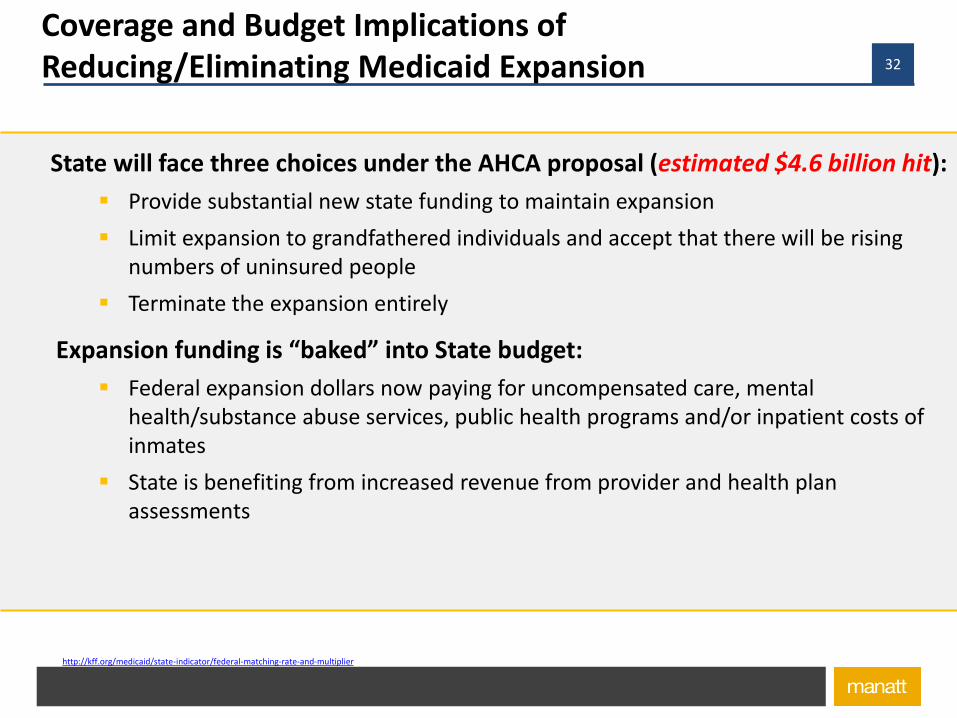

Coverage and Budget Implications of Reducing/Eliminating Medicaid Expansion

State will face three choices under the AHCA proposal (estimated $4.6 billion hit):

Provide substantial new state funding to maintain expansion

Limit expansion to grandfathered individuals and accept that there will be rising numbers of uninsured people

Terminate the expansion entirely

Expansion funding is “baked” into State budget:

Federal expansion dollars now paying for uncompensated care, mental health/substance abuse services, public health programs and/or inpatient costs of inmates

State is benefiting from increased revenue from provider and health plan assessments

Source: “Medicaid Capped Funding: Findings and Implications for New York,” prepared by Manatt Health for the Robert Wood Johnson Foundation State Network; Federal Medical Assistance Percentage (FMAP) FY17, http://kff.org/medicaid/state-indicator/federal-matching-rate-and-multiplier

33New York Medicaid Financing Structure Today

New York receives federal funding for all allowable program costs.

Federal dollars are guaranteed as match to state spending so long as state complies with federal Medicaid law, rules and the terms and conditions of any state waivers.

New York claims federal dollars for medical and administrative services, supplemental payments to providers (e.g. DSH, UPL) and other payments under waiver authority.

Federal Medicaid funding (nearly $33.5 billion in 2015) makes up nearly two-thirds (64%) of all federal funding in New York’s budget.

Source: “Medicaid Capped Funding: Findings and Implications for New York,” prepared by Manatt Health for the Robert Wood Johnson Foundation State Network; Federal Medical Assistance Percentage (FMAP) FY17, http://kff.org/medicaid/state-indicator/federal-matching-rate-and-multiplier

34Medicaid’s Financing Structure: Current v Proposed

Current Block Grants Per Capita Cap

Federal Funding Open ended Aggregate capPer enrollee cap

(by eligibility group)

RiskFederal government and state share

enrollment and spending riskStates bear risk of both higher

enrollment and health care costsStates bears spending risk of higher

health care costs

Annual TrendDetermined by health care costs in

the state and individual state spending decisions

National trend rate National trend rate

Ability to Accommodate Medical Advances or Public Health Crises

Federal payments automatically responsive

Federal payments not responsive Federal payments not responsive

Spending Outside of Cap

N/A Unknown/TBD Unknown/TBD

State FlexibilityState flexibility subject to federal

minimum standards; Section 1115 waivers provide additional flexibility

Increased flexibility, but some minimal standards and

accountability

Increased flexibility, but some minimal standards and

accountability

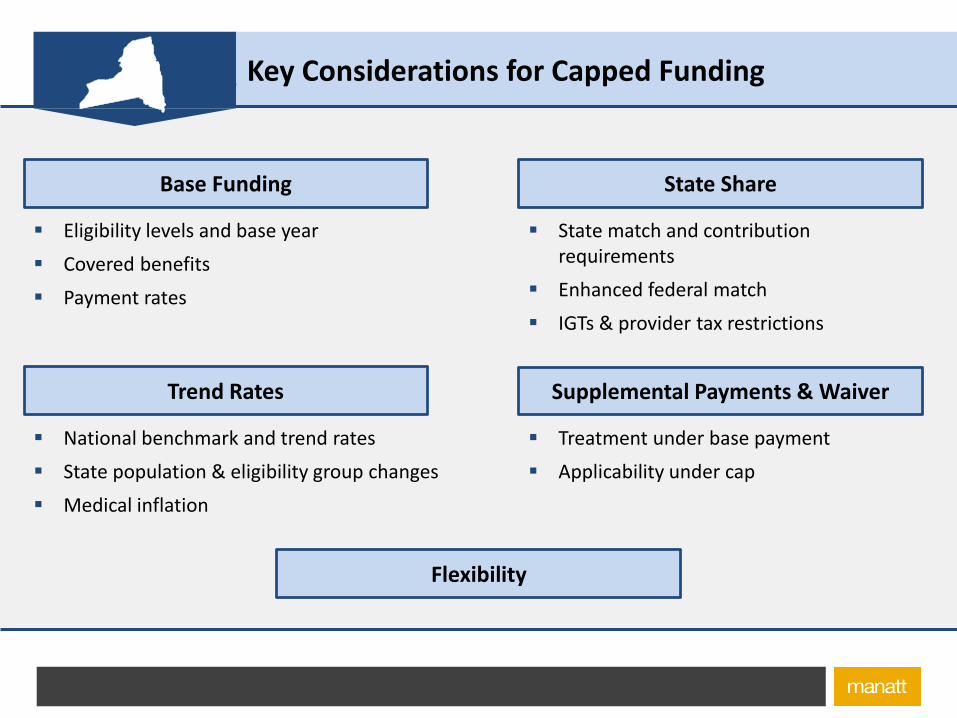

35Key Considerations for Capped Funding

Eligibility levels and base year

Covered benefits

Payment rates

Base Funding

National benchmark and trend rates

State population & eligibility group changes

Medical inflation

Trend Rates

State match and contribution requirements

Enhanced federal match

IGTs & provider tax restrictions

State Share

Supplemental Payments & Waiver

Flexibility

Treatment under base payment

Applicability under cap

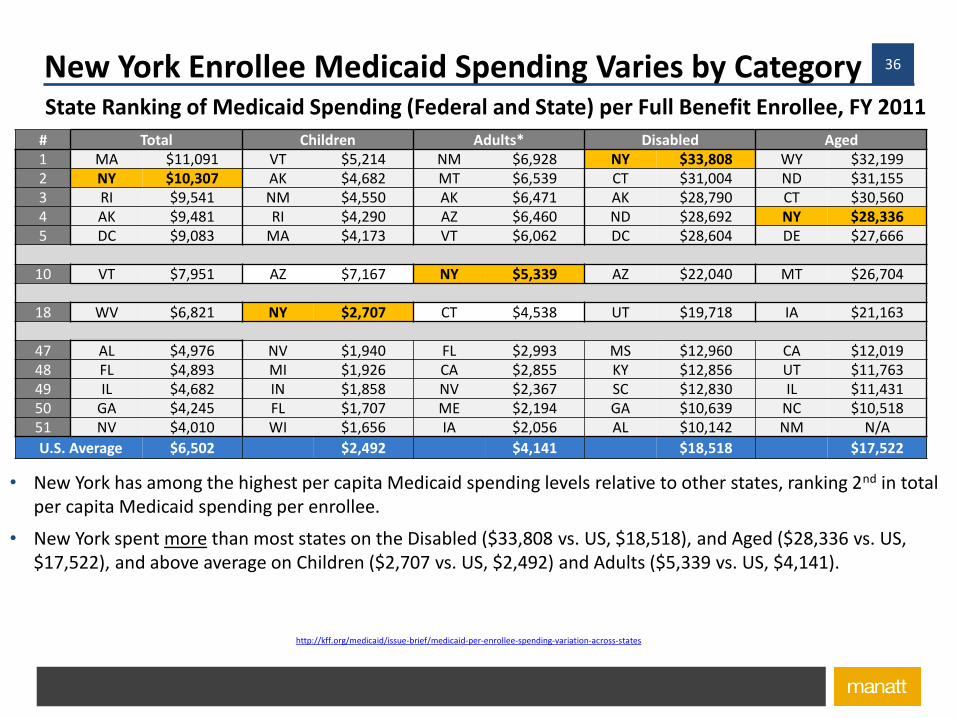

36New York Enrollee Medicaid Spending Varies by CategoryState Ranking of Medicaid Spending (Federal and State) per Full Benefit Enrollee, FY 2011

…

…

…

* Includes low-income parents and pregnant women. Source: Manatt analysis of Kaiser Family Foundation data. Available at: http://kff.org/medicaid/issue-brief/medicaid-per-enrollee-spending-variation-across-states. New Mexico’s spending per aged enrollee was not available.

# Total Children Adults* Disabled Aged1 MA $11,091 VT $5,214 NM $6,928 NY $33,808 WY $32,199 2 NY $10,307 AK $4,682 MT $6,539 CT $31,004 ND $31,155 3 RI $9,541 NM $4,550 AK $6,471 AK $28,790 CT $30,560 4 AK $9,481 RI $4,290 AZ $6,460 ND $28,692 NY $28,336 5 DC $9,083 MA $4,173 VT $6,062 DC $28,604 DE $27,666

10 VT $7,951 AZ $7,167 NY $5,339 AZ $22,040 MT $26,704

18 WV $6,821 NY $2,707 CT $4,538 UT $19,718 IA $21,163

47 AL $4,976 NV $1,940 FL $2,993 MS $12,960 CA $12,019 48 FL $4,893 MI $1,926 CA $2,855 KY $12,856 UT $11,763 49 IL $4,682 IN $1,858 NV $2,367 SC $12,830 IL $11,431 50 GA $4,245 FL $1,707 ME $2,194 GA $10,639 NC $10,518 51 NV $4,010 WI $1,656 IA $2,056 AL $10,142 NM N/A

U.S. Average $6,502 $2,492 $4,141 $18,518 $17,522

• New York has among the highest per capita Medicaid spending levels relative to other states, ranking 2nd in total per capita Medicaid spending per enrollee.

• New York spent more than most states on the Disabled ($33,808 vs. US, $18,518), and Aged ($28,336 vs. US, $17,522), and above average on Children ($2,707 vs. US, $2,492) and Adults ($5,339 vs. US, $4,141).

37

Sources: BLS data, available at, https://data.bls.gov/cgi-bin/surveymost?cu,; Kaiser Family Foundation Data, available at, http://kff.org/medicaid/issue-brief/medicaid-per-enrollee-spending-variation-across-states/, Rudowitz, R., Garfield, R., and Young, K., “Overview of Medicaid Per Capita Cap Proposals,” Kaiser Family Foundation, June 2016. Available at: http://kff.org/report-section/overview-of-medicaid-per-capita-cap-proposals-issue-brief/

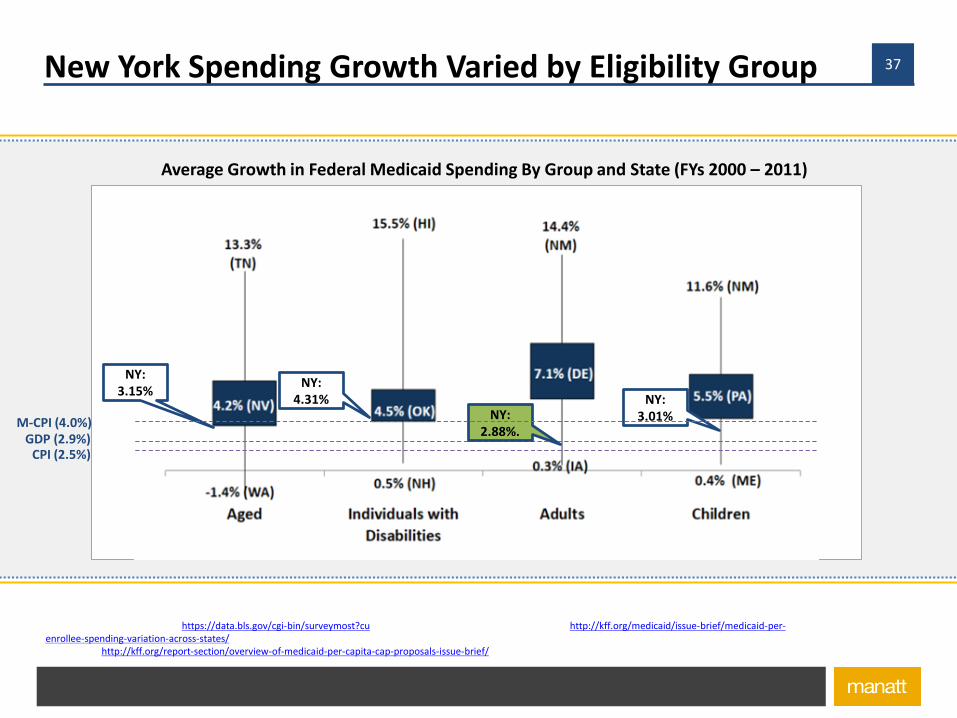

New York Spending Growth Varied by Eligibility Group

Average Growth in Federal Medicaid Spending By Group and State (FYs 2000 – 2011)

GDP (2.9%)CPI (2.5%)

NY:3.15%

NY:4.31%

NY:2.88%.

NY:3.01%M-CPI (4.0%)

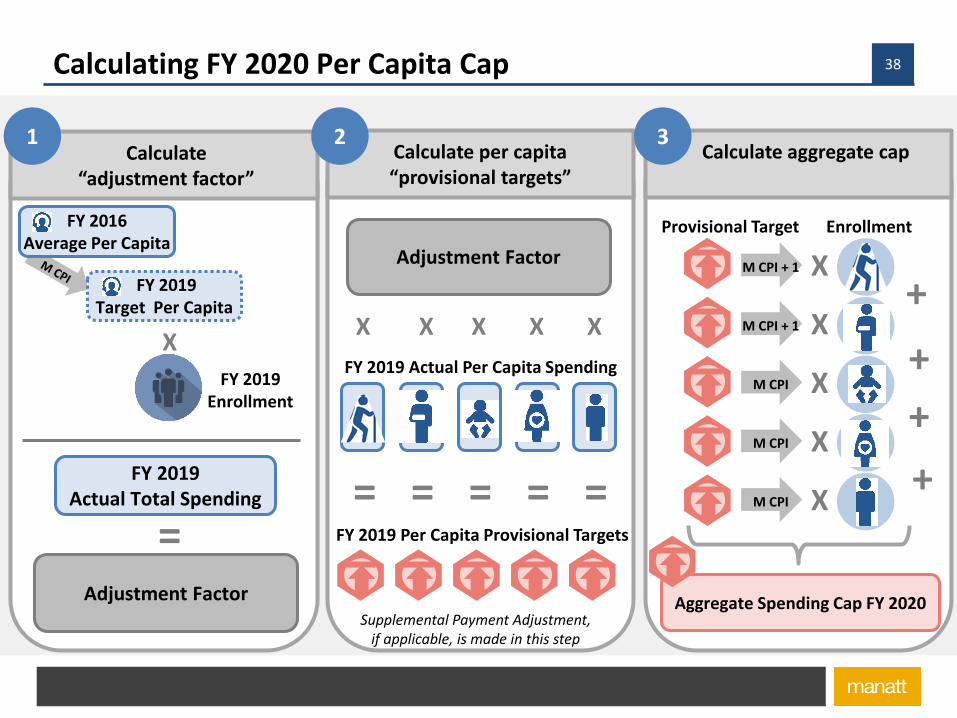

38Calculating FY 2020 Per Capita Cap

FY 2019 Enrollment

XX X X X X

FY 2019 Actual Per Capita Spending

= = = = =FY 2019 Per Capita Provisional Targets

Supplemental Payment Adjustment, if applicable, is made in this step

Enrollment

XM CPI + 1

Provisional Target

XM CPI

XM CPI + 1

XM CPI

XM CPI

1Calculate

“adjustment factor”

Calculate per capita “provisional targets”

Calculate aggregate cap2 3

FY 2019 Target Per Capita

FY 2019Actual Total Spending

=Adjustment Factor

Adjustment Factor

Aggregate Spending Cap FY 2020

+

+

+

+

FY 2016 Average Per Capita

39Why NYS is Uniquely Vulnerable to Medicaid Restructuring

New York has always been an outlier in Medicaid spending and any approach

to capping Medicaid spending is certain to take a greater toll on New York.

For behavioral health and other providers to persons with disabilities, our

outlier status is even more pronounced and the ability to cross-subsidize from

one beneficiary category to another places these services at special risk.

The medical inflation factor will not be sufficient to take into account unique

health care cost drivers in New York State.

Capped approaches fail to take into account new modalities of treatment,

new drugs, or new public health emergencies—and block grants would not

take into account economic downturns.

Converting an entitlement program to a capped program invites future, even

more drastic budget-cutting.

40Why NYS is Uniquely Resilient to Medicaid Restructuring

Since the mid-1980s, New York has embarked on a gradual implementation

of converting Medicaid to a managed care program, with capitated (or

“capped”) per enrollee expenditures.

Since 2011, New York has put in place a cap on its state share

expenditures—the “global” cap—which it has successfully lived within. In this

budget, New York has actually created a “sub-cap” on prescription drug

expenditures, which will be utilized to reduce growth in these expenditures.

NY has actually reduced the per capita expenditure growth in Medicaid below

the national average and could potentially do better under per capita caps.

NY operates already a number of waivers that could survive ACA repeal.

While the fiscal hit would be severe, New York has the resources and political

will to keep the safety net intact: case in point is the Essential Plan.

41Why NYS is Uniquely Resilient to other AHCA Changes

Since the 1990s, New York has its own insurance reforms in place that limit

age rating, preclude “medical underwriting,” ban use of pre-existing

conditions and require community rating.

New York’s exchange is not as dependent on the large national plans and

may be able to maintain coverage options through its reliance on plans that

are already committed to public

Even if changes to Essential Health Benefits are made, New York’ has a long

history of mandating coverages that will continue to require comprehensive

health insurance.

New York is unlikely to implement laws that discourage provision of

contraception or abortion services and will protect Planned Parenthood.

42Why Behavioral Health Services Can Survive

Even some of the Repeal/Replace advocates appreciate government’s

obligation to persons with disabilities—reflected in more robust trend.

Opioid epidemic underscored the universal nature of behavioral health

concerns and has resulted in strong “Red State” support for related services.

Science matters and growing scientific understanding of brain disease and

disorders will lead to greater recognition of importance of behavioral health.

Federal and state parity legislation, like New York’s Timothy’s Law, will

survive, regardless of what happens to Essential Health Benefits.

New York has a unique history in behavioral health reform and innovation and

a Constitutional imperative to provide aid and care to the needy.

And . . .

43Why Behavioral Health Services Can Survive

New York’s behavioral health advocacy community—

including providers, advocacy organizations, consumers,

family members, public officials—is up to the task.

44Are we prepared?

Need for concerted State planning and focus.

Need to engage constituencies to begin planning for

New York State response—beyond budget authority to

cut budget to reflect federal cuts.

Instead of repeal and replace, New York has to restore

and reinstate historic reputation for national leadership.

45Obligatory photo of my newly arrived first grandchild

46Questions and Discussion

Enjoy the conference.

Jim LytleManatt, Phelps & Phillips LLP 136 State StreetAlbany, NY 12203

(518) [email protected]