report no. erbaijan financial ccountability...

TRANSCRIPT

Report No. 2699.5-AZ

erbaijan Financial ccountability Assessment

September 30, 2003

Operations Policy and Services Uni t Europe and Central Asia Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

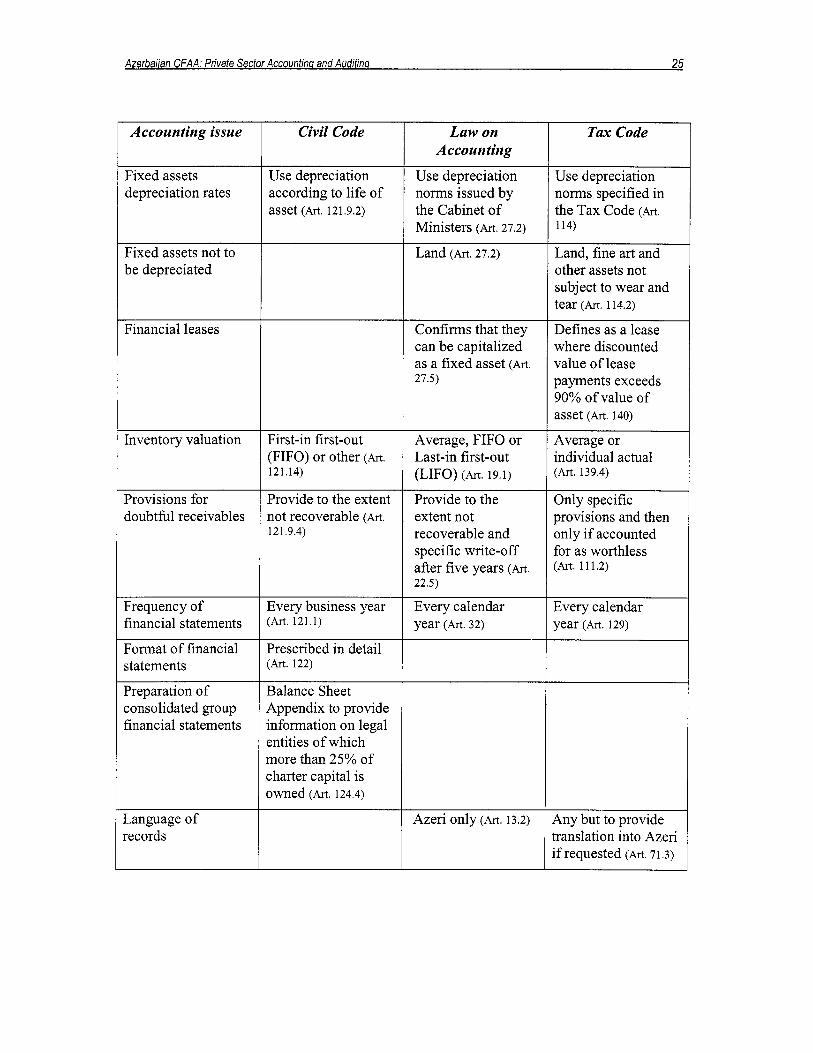

osur

e A

utho

rized

BO BSL CAS CFAA COA CPAR CPPR EBRD EU-TACIS

FIAS FSTA FY GFS GFMIS IAS IASB IASC IBTA2 IDA IFAC JMF INTOSAI I-PRSP ISA MOF MTES MTEF NBA OECD PRGF SAI

SPA TlMS TSA

SAC-I1

CURRENCY EOUIVALENTS (Exchange Rate Effective October 2002)

Currency Unit = Manat (AZM) US$ 1 = 4,885 Manat

FISCAL YEAR January 1 to December 3 1

ABBREVIATIONS AND ACRONYMS

Budget Organization Budget Systems Law Country Assistance Strategy Country Financial Accountability Assessment Chamber of Accounts Country Procurement Assessment Report Country Portfolio Performance Review European Bank for Reconstruction and Development European Union - Technical Assistance for Commonwealth of Independent States Foreign Investment Advisory Service Financial Sector Technical Assistance credit Fiscal Year Government Finance Statistics Government Financial Management Information Systems International Accounting Standards International Accounting Standards Board International Accounting Standards Committee Bank-financed Second Institution-Building Technical Assistance credit International Development Association International Federation of Accountants International Monetary Fund International Organization of Supreme Audit Institutions Interim Poverty Reduction Strategy Paper International Standards on Auditing Ministry of Finance Medium-Term Public Expenditure Strategy Medium-Term Expenditure Framework National Bank of Azerbaijan Organization for Economic Co-operation and Development Poverty Reduction and Growth Facility Supreme Audit Institution Second Structural Adjustment Credit State Procurement Agency Treasury Information Management System Treasury Single Account

Regional Vice-president: Shigeo Katsu, ECAVP

Sector Director: Alain Colliou, ECSPS Sector Manager: John Hegarty, ECSPS

Country Director: Donna Dowsett-Coirolo, ECCU3

Task Team Leader: Roberto Tarallo, LCOAA

Azerbaijan: Countw Financial Accounfabilitv Assessment i

TABLE OF CONTENTS

TABLE OF CONTENTS ............................................................................................................... i

PREFACE ..................................................................................................................................... i1

EXECUTIVE SUMMARY .......................................................................................................... V

SUMMARY OF ONGOING FINANCIAL MANAGEMENT INITIATIVES AND CFAA RECOMMENDATIONS .............................................................................................................. X

1 . COUNTRY AND ECONOMIC BACKGROUND ................................................................ 1

2 . PUBLIC SECTOR BUDGETING .......................................................................................... 3

3 . PUBLIC SECTOR ACCOUNTING. INTERNAL CONTROLS AND REPORTING ...... 8 Ministries and Budget Organizations. including the Ministry o f Finance (MOF) ...................... 8 Extra-budgetary Operations and Funds. Including the Oil Fund ............................................... 13 State-owned Enterprises ............................................................................................................ 15

4 . PUBLIC SECTOR AUDITING ............................................................................................ 17

6 . LOCAL GOVERNMENT INSTITUTIONS’ FINANCIAL MANAGEMENT ................ 23

7 . PRIVATE SECTOR ACCOUNTING AND AUDITING ................................................... 24 Enterprise Sector ....................................................................................................................... 24 Banking Sector .......................................................................................................................... 30 Corporate Governance and Financial Accountability ............................................................... 34

8 . FIDUCIARY CONSIDERATIONS IN RESPECT OF BANK-FINANCED PROJECTS

Reliance on Public Sector Financial Management Framework ................................................. 36 Project Financial Management .......................................................... : ....................................... 36 Considerations o f Corruption .................................................................................................... 38

9 . NEXT STEPS .......................................................................................................................... 40

ATTACHMENT 1: CFAA TEAM ............................................................................................. 41

ATTACHMENT 2: MAP OF AZERBAIJAN .......................................................................... 42

Azerbaijan: Counfrv Financial Accountability Assessment 11

PREFACE

This report was prepared after World Bank missions to Azerbaijan in 2002 and 2003 by a Task Team comprised o f Roberto Tarallo, Task Team Leader and Ranjan Ganguli, Financial Management Consultant. A counterpart team, comprising members o f Government, the Chamber o f Accounts and the State Procurement Agency, having been specifically formed for the purpose o f discussion o f both the C F A A as we l l as the CPAR, was engaged throughout the process o f formulation o f this CFAA. In M a y 2003, the Cabinet approved the recommendations contained in this CFAA.

The report i s based o n the results o f interviews and discussions with various public and private institutions as we l l as an analysis o f various data gathered during the missions including copies o f various legislation, instructions and reports. Government and private sector counterparts lent their fill and proactive support to the C F A A missions and engaged with the Bank’s team in a comprehensive dialogue. The Bank i s gratehl for this cooperation.

Objective of Country Financial Accountability Assessment

There i s considerable empirical evidence o f a strong causal relationship from better govemance to better development outcomes’. A country’s financial accountability and procurement frameworks are significant elements o f that aspect o f govemance relating to the capacity o f Government to manage resources and implement sound policy.

A C F A A i s a diagnostic instruments designed to facilitate a common understanding by the borrower, Bank and their development partners o f the borrower’s public and private sector financial accountability framework. In tum this enables the development o f plans to address any issues identified as well as o f appropriate capacity-building programs.

CFAAs also support the Bank in the exercise o f its fiduciary responsibilities by identifying the strengths and weaknesses o f a country’s financial accountability arrangements and the risks that these may pose to the use o f Bank funds. CFAAs are not audits; they are not intended to and do not provide assurance on the specific uses to which Bank funds have been or may be applied.

Relationship o f the C F A A to the CAS, lending program and pol icy dialogue with the Government In light o f projected major increases in o i l revenues, the authorities have two basic objectives for pol icy reform in the next few years. The f i rs t i s to create a public sector that manages efficiently the country’s natural resource wealth and delivers on key social and economic services, critical to the reduction o f poverty. The second i s to remove impediments to growth and employment in the non-oil sectors.

Kaufmann, Kraay and Zoido-Lobath (1999). “Governance Matters”. World Bank Institute Policy Research Working Paper 2 196

Azerbaijan: Counfrv Financial Accounfabilitv Assessment iii

The Government’s Interim Poverty Reduction Strategy Paper (I-PRSP) o f M a y 2001 demonstrated i t s intention to improve the country’s economic management system with a view to enhancing i t s effectiveness, converting i t more fully to functional management, reducing the administrative structure, and raising the level o f professionalism and responsibility o f government employees. The IMF’s and Bank’s Joint Staff Assessment o f the I-PRSP expressed the view that corruption, particularly administrative corruption, had been a major constraint to Azerbaijan Republic’s economic growth and poverty alleviation and that the recent and ongoing initiatives offered an important opportunity to improve govemance in the Azerbaijan Republic.

One o f the main principles o f the Government’s Poverty Reduction Strategy i s to restructure the system o f public expenditure management with a view to improving the effectiveness o f the expenditures., As outlined in the I-PRSP and with respect to institutional reforms and improving the management o f the budget process, the Government plans to: include al l expenditures o f government agencies in the budget, including social funds, and execute payments through a treasury single account (TSA); establish an overall budget package and expenditure guidelines for Government agencies; set up an integrated process for the submission o f budget plans and reports; update the budget classification; introduce international accounting standards; introduce a more efficient system for reporting on budget execution; publish on a regular basis more extensive information on budget execution to ensure transparency o f budget revenues and expenditures.

The CAS o f November 29, 1999 (supporting Azerbaijan’s development agenda for the period FY00-02) identified the area in need o f the most urgent attention to be comprehensive public sector reform and improved governance. The main thrust o f the CAS was therefore assistance to the Government in implementing i t s public sector reform agenda to improve public sector management.

Consistent with the I-PRSP and the CAS, as wel l as the IMF’s three-year Poverty Reduction and Growth Facility (PRGF), the reform program supported by the Bank- financed Second Structural Adjustment Credit (SAC-11) currently under implementation seeks to: (i) improve transparency and accountability in public financial management, including the establishment o f the supreme audit institution; (ii) strengthen the tracking o f poverty-reducing public expenditures, and monitoring o f their impact on poverty; (iii) improve strategic priority setting and transparency o f medium-term public expenditure and investment programs; (iv) introduce transparency and financial discipline in the energy sector, including fiscalization o f quasi-fiscal activities: (v) reduce conflicts o f interest and corruption in the business environment, including enforcement of regulations, separation of regulatory and commercial functions, and tax and customs; (vi) improve transparency, financial discipline and competition in the banking sector; and (vii) improve the privatization process. Clearly, there are many issues addressed by a C F A A that are o f relevance to the Bank’s dialog and program with the Government. Thus SAC-I1 contains explicit references to the C F A A as well as to various issues that fal l within the scope o f th is diagnostic. The link to the SAC-I1 explains the timing o f CFAA: approval by the Government of Azerbaijan o f plans for the preparation o f the C F A A - including the establishment o f a

Azerbaijan: Countw Financial Accountability Assessment iv

counterpart team and approval o f the C F A A / CPAR Initiating Concept Memorandum (ICM) - was required prior to Board presentation o f SAC-11. SAC-I1 second tranche conditions include the provision o f evidence o f satisfactory implementation o f the action plans resulting from the C F A A and CPAR.

Discussions on preparation o f a new CAS for FY03-05, which wil l continue to focus on poverty reduction, has started and will refer to the reform measures identified by the C F A A and agreed-upon with the government and the donor community.

Finally, i t should be noted that a significant amount o f analysis o f assistance to develop Azerbaijan’s financial accountability framework has already been undertaken and is underway by various organizations, notably the IMF, FIAS, the Wor ld Bank, the USAID and the EU-TACIS. I t was not the intention that this C F A A should revisit these areas anew, nor was it to formulate separate recommendations. Rather, this CFAA summarizes these analyses and interventions whilst also identifying those areas not yet addressed.

Scope and terms o f reference of CFAA

The scope and terms o f reference o f the C F A A was articulated and agreed both intemally within the Bank and extemally with an Azerbaijan counterpart team in the C F A A / CPAR I C M dated February 19,2002.

Acknowledgements

The C F A A team wishes to acknowledge the extensive and grateful cooperation and assistance received from the staff o f the various institutions who contributed to the CFAA, including officials and staff o f the Government, state agencies and enterprises, private sector institutions, and bi-lateral and multilateral organizations. Grateful thanks go also to the Bank’s SAC-11, IBTA2 and FSTA task teams as well as the IMF’s Fiscal Affairs Department and FIAS for their considerable research on which a significant proportion o f this C F A A i s based. In addition: Akbar Noman, Azerbaijan Country Manager, and Farid Mamedov, Operations Officer, provided invaluable in-country assistance and information in carrying out the CFAA; Nigar Aliyeva, Team Assistant in the Bank’s Baku Office, provided support with logistical arrangements for the mission; John Hegarty, E C A Regional Financial Management Adviser, Ida Muhoho (ECSPS), Christian Petersen, Azerbaijan Country Economist, and peer reviewers, Mozammal Hoque (OCSFM) and Andrew Mackie (Consultant), offered invaluable comments and inputs; and Ana Cristina Hirata assisted with the editing and formatting o f the report.

Azerbaijan CFAA: Execufive Summarv V

EXECUTIVE SUMMARY

1. A s an independent nation for only ten years, Azerbaijan is s t i l l in political and economic transition. Azerbaijan shares al l the formidable problems o f the other countries o f the former Soviet Un ion in making the transition from a command to a market economy, but i t s considerable energy resources brighten its long-term prospects. The Constitution o f the Republic o f Azerbaijan, ratified by popular referendum six years ago in November 1995, contains a western system o f checks and balances aimed at securing separation o f powers among the legislative, executive and judiciary branches o f the government. Azerbaijan has begun making progress on economic reform, and old economic ties and structures are slowly being replaced. Important challenges need to be overcome if future growth prospects are to be realized and provide for rapid expansion o f employment and income opportunities as wel l as a decline in poverty: the non-oil sector remains constrained by slow progress with financial discipline and efficient management in public utilities that together generate a significant quasi-fiscal deficit; weaknesses in public sector governance, the judicial and financial systems, and slow progress in privatization o f large enterprises also deter non-oil investment; and delivery and quality o f infrastructure and social services have deteriorated, especially in the rural areas. Approximately 50% o f the population l ives below the poverty line. .. 11. In the area o f the country’s financial accountability framework, Azerbaijan has already received and continues to receive a considerable amount o f analysis, advice and assistance, particularly in the areas o f public financial management from the IMF, the World Bank, U S A I D and lately, the European Union. This C F A A summarizes the analysis performed to-date as well as any associated advice and development assistance and also identifies areas hitherto un-addressed and provides a framework to address issues arising.

Public sector budgeting

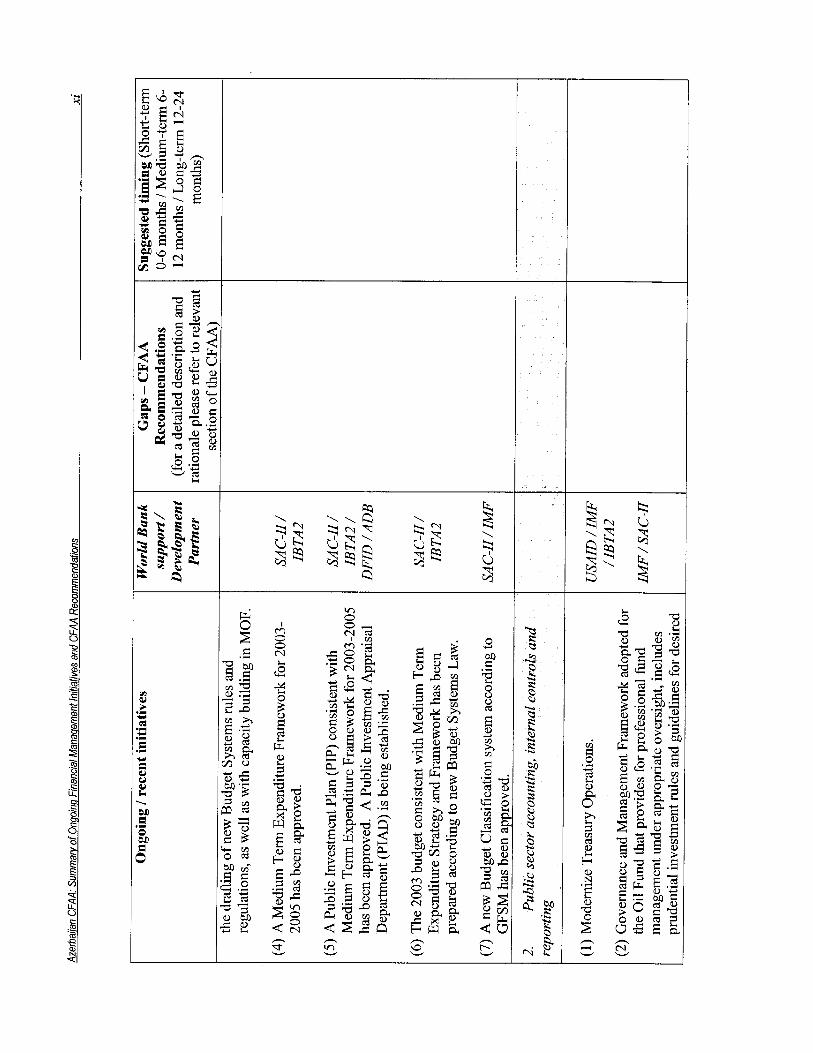

iii. There are many areas of weakness with the particular bottom-up approach adopted for budget formulation, including: poor economies o f scale; inflated budget demands with no link to output; the use o f norms o f expenditure; and the influence of the sectoral departments o f the Ministry o f Finance. However, and as promised in the I- PRSP, the government has started to improve the management o f the budget process, the most significant elements o f which include: the publication o f a Medium-Term Public Expenditure Strategy (MTES); the enactment o f a new Budget Systems Law (BSL); the development o f a Medium-Term Expenditure Framework (MTEF) for 2003-2005; and the development o f a Pubic Investment Program (PIP).

iv. Public sector budgeting has been and continues to be the subject o f considerable analysis and support, particularly from the IMF and the Bank, and the Bank continues to support reforms through the ongoing SAC-I1 and I B T A 2 operations.

Public sector accounting, internal controls and reporting

v. The Azerbaijan Government has engaged in extensive fiscal and monetary reform and has made notable improvements with respect to the establishment o f a Treasury, the

Azerbaijan CFAA: Executive Summarv V i

closure o f numerous bank accounts, the establishment o f a Treasury Single Account, and the centralization o f cash management functions. The Ministry o f Finance is thus able to produce more reliable and timely information on the government’s fiscal operations using a GFS-based classification. However, considerable scope remains for further improvement o f the Treasury systems and procedures; cash management and commitment controls need to be strengthened; and there is a need to generate more meaningful and timely reports. The Treasury has therefore embarked on the implementation o f a modem Treasury Information Management System (TIMS) to assist the government in achieving these and other improvements with the continued support o f the IMF and World Bank, particularly through SAC-I1 and IBTA2.

vi. Extra-budgetary operations o f ministries and Budget Organizations (BOs) pass through the Treasury and are subject to standard Treasury accounting, internal control and reporting requirements. After the enactment o f various laws, the specialized social h n d s - Social Protection, Disabled Person’s Fund and Employment Fund - are now merged; eleven o f 85 extra-budgetary funds are included directly in the 2002 Budget; al l other extra-budgetary funds wil l be included from 2003; and thus from 2003, only the Oil Fund and the Social Protection Fund will remain extra-budgetary. The Oil Fund in particular has been the subject o f considerable external analysis, particularly by the IMF and the Bank, and the government has been very responsive and transparent in devising its governance and financial management arrangements: the Supervisory Board comprises representatives o f government and civ i l society; i t i s audited annually; and unaudited financial information on the operations o f the Oil Fund i s published and reported widely.

Public sector external auditing

vii. The Supreme Audit Institution (SAI) o f the Azerbaijan Republic is the Chamber o f Accounts. Although this institution was foreseen in the Constitution, the relevant law establishing the Chamber o f Accounts was only passed in 1999 and the Chairman o f the Chamber o f Accounts only appointed in June 200 1. In view o f the fairly recent formation o f the Chamber o f Accounts as well as the comparatively limited experience o f key senior post-holders in matters o f auditing, there i s a considerable amount o f capacity- building to be done. The Bank i s actively supporting the strengthening o f the Chamber o f Accounts most notably with advice on the law and intemal regulations governing the Chamber o f Accounts, but also with technical assistance financed under IBTA2.

Public sector internal auditing

viii. In an attempt to reduce the negative impact o f the duplicative control and audit investigations performed, the President issued a decree in 1999 which abolished al l public sector intemal inspectiodcontrol departments with the exception o f the: M a i n Department o f Public Finance Control (MDPFC) in the MOF in respect o f public finances; the Ministry o f Taxes in respect o f matters within i t s jurisdiction; and the National Bank o f Azerbaijan (NBA) in respect o f its role as banking supervisor. Thus at present, no ministry, committee nor other central executive power bodies has a proper intemal audit function in the normal sense o f the term- being an appraisal activity established within an entity performing a service to the entity including, amongst other

Azerbaijan CFAA: fxecutive Summarv v i

things, examining, evaluating and monitoring the adequacy and effectiveness o f the accounting and internal control systems. N o r are there any plans to introduce internal audit in any of the ministries whilst at the same time addressing the earlier concerns of harassment, inefficiencies and corruption.

Legislative scrutiny of public sector jkancial management

ix. A Parliamentary Commission recently formed by the merger o f the two Parliamentary Permanent Commissions on Economic Policy and Budget Issues has the remit to scrutinize the public finances. Information provided to Parliament i s generally not considered comprehensive enough to generate a meaningful debate in the Parliament for informed decisions on the government’s budget proposals and execution. The information provided is highly aggregated and i s not based on full classification details. Partly in recognition o f the above, and as discussed elsewhere in this report, the government has embarked on a program o f reform, significant elements o f which includes a recently revised and enacted Budget Systems Law (BSL) as wel l as significant improvements in the MOF’s accounting and reporting systems, both o f which will go a long way towards remedying the above issues.

Local government institutions

x. Azerbaijan i s organized according to a two-tier administrative system (central government and sub-national governments comprising rayons, cities and municipalities, and one autonomous regioddistrict). Local executive power i s assigned to governors, who are appointed by the President. The Constitution defines the roles o f municipalities which, among others, impose taxes and approve their own budgets. A clear division of responsibilities between different levels o f government i s s t i l l emerging and Azerbaijan i s in the process o f establishing municipal governments.

Private sector

xi. The accounting framework o f the enterprise sector is fairly undeveloped and remains essentially unchanged from the time o f the Soviet Union in the form o f a fixed chart o f accounts, fixed bookkeeping methodologies and procedures, as we l l as fixed format accounting books and records. Accounting standards were directed towards the calculation and collection o f taxes as wel l as the compilation o f statistics rather than for the purposes o f managing and evaluating businesses. However, and since the collapse of the Soviet Union, the development o f different guidance and standards on accounting has created confusion because o f differences o f principle between the texts as wel l as omissions o f guidance on particular issues. This confusion, particularly given the close l i n k s between a company’s accounting and tax profit, is regarded a significant challenge to foreign companies wishing to invest in Azerbaijan and thus as an impediment to the growth o f foreign direct investment.

xi i . The Accounting Methodology Department established within the M O F has devised a program and action plan for the reform o f Azeri accounting standards however, whilst the program’s objectives are generally sound, program design and implementation could benefit from external assistance. The recently-initiated EU-TACIS project to assist in the introduction, development and application o f international financial reporting

Azerbaijan CFAA: Execufive Summarv Vii i

standards in the non-banking sector could help to fill this need by providing institutional support to the Ministry o f Finance in the planning, drafting and implementation o f new accounting standards in accordance wi th I A S as well as the development o f a comprehensive training program and support to selected enterprises to help them effectively adopt and implement the new standards.

x i i i . All jo int stock companies, and other legal entities exceeding prescribed thresholds are required to have an annual audit by an independent auditor or audit firm. The audit profession i s overseen by the Chamber o f Auditors which issues audit licenses, establishes auditing standards and monitors the performance o f auditors. There is scope to strengthen the private sector auditing framework by primarily adopting International Standards on Auditing and amending the legislative framework to eliminate conflicts o f interest inherent in the stated remit o f the Chamber o f Auditors.

xiv. The banking sector has been and continues to be the subject o f considerable analysis and the recipient o f considerable assistance from the development community, notably the IMF, the Bank and the EU-TACIS. There i s scope to strengthen further the banking sector by, primarily: coordinating the ongoing development o f banking accounting standards led by the NBA with the prospective development o f non-banking national accounting standards led by the MOF with a view to reconciling and eliminating differences between the core non-banking accounting standards; and establishing clear criteria by which auditors are deemed acceptable or otherwise to conduct the audits o f banks and banking institutions.

Fiduciary considerations in respect of Bank-financed projects

xv. In view o f the analysis presented in this CFAA, it i s clear that there i s a need for substantial strengthening in the areas o f budgeting, treasury management, financial reporting, internal auditing and external auditing. Most o f these needs have already been recognized and there are already plans and operations underway to address them (refer to immediately following summary matrix). At present however, there are sufficient concerns about the operation and integrity o f the country’s public sector financial management framework that i t would be inappropriate to place a blanket reliance on this framework for the purposes o f satisfying the Bank’s fiduciary financial management requirements. Reliance on any particular aspect o f the country’s financial management framework for the purposes o f satisfying the Bank’s financial management requirements would need to be established on a case-by-case basis by reference to the specific financial management arrangements o f the institutions involved. This i s not to say that the Bank’s current approach o f routinely “ring-fencing” Bank-financed projects and supporting the establishment o f so-called project implementation units i s appropriate, but rather in view of the ongoing and significant assistance being given to the government o f Azerbaijan in the strengthening o f its public sector financial management fi-amework, Bank teams should now be strongly encouraged to explore the possibilities o f relying o n parts o f that framework for the purposes o f satisfying the Bank’s fiduciary financial management requirements. The recent appointment by the Bank o f a Financial Management Analyst in i t s Baku office should help to address and coordinate this issue.

Azerbaijan CFAA: Executive Summaw ix

Next steps

xvi. A matrix summarizing ongoing financial management initiatives and CFAA recommendations immediately follows this executive summary. The CFAA i s intended to act as a unifying tool to bring the Government, the Bank and the donors around the table with a view to design a medium term reform program, prioritizing the actions to be taken, and assign funding and support responsibilities. In M a y 2003, the Cabinet approved the recommendations contained in this CFAA.

\

W

0 M

n -3

n C'I W

v,

Y

U

Y Y Y

n i W

Y

c

U

E .1 Y cd .I Y .I

c .I Y d Q) 0 Q) h \

.I 2

8 0 on

h

W N

I

M

n 3 W

Y

Azerbaiian CFAA: Countrv and Economic Backaround 1

1. COUNTRY AND ECONOMIC BACKGROUND

1. The Republic o f Azerbaijan i s located in the southeastern Caucasus region of western Asia. Azerbaijan was part o f the Russian Empire from the early 19th century to 191 8, brief ly an independent republic from 191 8 to 1920, and a part of the Soviet Union from 1922 to 1991. On August 30, 1991, i t declared its independence from the Soviet Union. Azerbaijan covers an area o f 33,440 square miles (86,600 sq. km), has a population o f approximately 7.8m and includes two administrative divisions with special status, the autonomous Republic of Nakhchivan, which i s separated from Azerbaijan proper by southern Armenia, and the autonomous district o f Nagomo-Karabakh (Qarabag). The capital and largest c i ty o f Azerbaijan i s Baku.

2. As an independent nation for only ten years, Azerbaijan i s s t i l l in political and economic transition. The Constitution of the Republic o f Azerbaijan (the “Constitution”), ratified by popular referendum six years ago in November 1995, contains a western system o f checks and balances aimed at securing separation o f powers among the legislative, executive and judiciary branches o f the government. The Constitution provides for a unicameral parliament (the National Assembly or Milli Majlis), a president, and a prime minister.

3. Fol lowing the break-up o f the Soviet Union and until the mid 1990s, Azerbaijan’s economy suffered a dramatic output collapse, with a cumulative real GDP drop o f about 60 percent, accompanied by hyperinflation, sharp currency depreciation and rapidly depleting foreign exchange reserves. These difficult ini t ial conditions largely reflected the collapse of the Soviet Union and related trade and transport l inks , sharp negative terms-of-trade shock as suppliers moved to market pricing, the mil i tary conflict over the Nagomo-Karabakh region, and large fiscal deficits financed by money creation.

4. Azerbaijan has only recently begun making progress on economic reform, and old economic ties and structures are slowly being replaced. Fol lowing President Aliyev’s succession to power in 1993 and the cease-fire in Nagorno-Karabakh in July 1994, the Government launched a comprehensive stabilization and structural reform program in 1995, supported by the IMF and IDA. Prospects for growth were further improved by the negotiation o f 19 production-sharing arrangements (PSAs) with foreign f i r m s that have thus far committed $60 bi l l ion to o i l field development and should generate the funds needed to spur future industrial development. During the past five years, Azerbaijan has made significant progress in securing macroeconomic stability, price and trade liberalization, as wel l as in land and small-scale enterprise privatization. Real GDP growth averaged 7.1 percent during 1996-2000.

5. Azerbaijan shares al l the formidable problems o f the other countries o f the former Soviet Union in making the transition from a command to a market economy, but i ts considerable energy resources brighten its long-term prospects. Important challenges need to be overcome if future growth prospects are to be realized and provide for rapid expansion o f employment and income opportunities as well as a decline in poverty: the non-oil sector remains constrained by slow progress with financial discipline and efficient management in public utilities that together generate a significant quasi-fiscal

Azerbaijan CFAA: Countrv and Economic Backuround 2

deficit; weaknesses in public sector governance, the judicial and financial systems, and slow progress in privatization o f large enterprises also deter non-oil investment; and delivery and quality o f infrastructure and social services have deteriorated, especially in the rural areas. Approximately 50% o f the population lives below the poverty line.

Azerbaijan CFAA: Public Sector Budsefins 3

2. PUBLIC SECTOR BUDGETING

Current situation

6. Budget formulation in Azerbaijan i s govemed primarily by the Budget Systems Law (BSL). I t begins with the issue o f budget circular in January o f the year preceding the relevant fiscal year, followed by a specification o f o f the state’s medium-term economic and social development pol icy in February, budget requests from municipalities for state subsidies by M a y 1, presentation o f the draft budget to the Cabinet o f Ministers by September 10, to the President by September 25, and presentation of the budget to parliament no later than October 15 with a view to approving and enacting the central budget by December20 and the local budgets by December 25. The budget circular for current, non-development budget assigns responsibilities and detailed timetable for budget submission by the l ine ministries and organizations and by the M O F offices at the district level. The budget for government expenditure i s prepared in four stages: (i) central operations, (ii) central administrative expenditure, (iii) central operations in the districts, and (iv) district administrative expenditure. In stages (i) and (ii), the headquarters o f line ministries and organizations prepare their own office budgets, collect the budget proposals o f budget organizations located at the center, consolidate these, and forward them to the concerned sectoral division o f the MOF for scrutiny. In stages (iii) and (iv), the budgets o f organizations at the district level are coordinated by the regional offices o f the MOF, which collect and apply initial scrutiny to the budget proposal o f the central institutions located in the district. These are then forwarded to the MOF sectoral departments for finalization.

7. which include:

There are various weaknesses with this approach o f bottom-up budget formulation

0 Poor economies o f scale. Current budget formulation process militates against efficient delivery o f services. This i s due to the fundamental structural weakness under which the decisions on financing requirement for the delivery o f a service i s irrationally distributed between central l ine ministries and the district offices o f the MOF. For example, the Ministry o f Health has hospitals al l over the country but the budgets o f the hospitals and medical establishments in the districts are neither influenced nor controlled by the Ministry o f Health even though the hospitals are under the administrative control o f and answerable to the Ministry o f Health on the quality o f the service rendered. Direct participation o f the MOF district office in budget formulation o f a l l agencies at the district level dilutes their ability to challenge the budget bids on any ground other than the simple check o f the norms applied and arithmetical accuracy. Thus the Ministry o f Health plays a very limited part in the preparation and i s only kept informed o f the budget proposals o f a hospital in the district.

0 Inflated budget demands with no link to output. Budget users inflate their demand for funds as they are not bound to the discipline o f fkaming their budgets within a preset expenditure envelope. Thus the demand for funds typically exceeded availability o f funds by a factor o f three. N o systematic prioritization o f

Azerbaijan CFAA: Public Sector Budsefina 4

activities i s undertaken at any level, nor i s any attempt made to align expenditure proposals with the output expected. Since al l demands cannot be accommodated within the limited resource envelope, the MOF is compelled to make adhoc cuts and advise budget user to meet their shortfall f rom extra-budgetary sources.

0 The use o f norms o f expenditure. The budget is based mainly on approved norms o f expenditure items. Routine adherence to norms o f expenditure can lead to budget users selecting options that generate larger bids in preference to cheaper and more realistic options - such as bidding for larger number o f incidence of inpatients than outpatient altematives because the former would inflate the budget bid.

0 The influence o f the M O F as compared to l ine ministries. The crucial phase o f negotiating the budgets o f a l l budget users i s performed not in the budget department o f l ine ministries but rather in the sectoral departments o f the MOF. This undermines the accountability o f the l ine ministries.

Going forward

8. As promised in the I-PRSP, the government has started to improve the management o f the budget process. The practice o f adoption o f the budget prior to the beginning o f a new financial year will be continued. In addition, there are plans to: include in the budget al l expenditures o f government agencies, including social funds; establish an overall budget package and expenditure guidelines for govemment agencies; set up an integrated process for the submission o f budget plans and reports; update the budget classification; introduce intemational accounting standards; improve the system for making changes in tax rates, social contributions, customs duties, and other compulsory payments; introduce a more efficient system for reporting on budget execution; publish on a regular basis extensive information on budget execution to ensure transparency o f budget revenues and expenditures.

9. A Medium-Term Public Expenditure Strategy (MTES) published by the Government, outlines the priorities for consolidated public expenditures (i.e. including the Oil Fund) and the corresponding expenditure allocation path for the next three years (these years, leading up to the materialization o f substantial o i l revenues, are o f crucial importance). The Strategy stipulates implementation and governance arrangements for those consolidated public expenditures, as wel l as key institutional and pol icy reforms envisaged in the public expenditure area during this period. The rules and principles that would determine the magnitude o f expenditures out o f the Oil Fund during these three years are formulated, together with a timeframe for the fiscalization and eventual elimination o f utility subsidies. Within this strategic framework and on the basis o f ongoing PRSP work, the Government wil l formulate consistent medium-term expenditure programs for the social sectors and a three-year Public Investment Program (PIP) by end- September 2002.

10. The government developed the fol lowing medium-term consolidated budget, including Social Funds, Oil Fund, Privatization Fund and revenues and expenditures of budgetary organizations, for 2000-2005:

Azerbaijan CFAA: Public Sector Budaefina 5

Revenue

Expenditure

Economic classification

Personnel Emoluments Wages and salaries Employer's Contribution

Purchases o f goods and services Transfers t o households

Social Protection Fund Transfers to Households f r o m State Budget

budget project loans O i l Fund

Capital expenditure

All other items

Primary expenditure

Debt service interest principal

Functional classification

State operating functions General State Service Defence Courts, law enforcement, security

Social and welfare functions Education expenditure Health expenditure Social Protection and Social Security

State Budget Social Protection Fund

Culture, arts and religion Economic Services

Housing and Public Services Fuel and Energy Affairs Agriculture, Forestry and Fishing Industry and Construction

2000 2001

5739 5755

4955 5467

1090 1195 1084 1187

6 8 1150 1196 1563 1633 1341 1355 222 278 698 954 314 289 384 661

0 4 303 289

4804 5267

151 200 93 92 58 108

1118 1265 261 303 485 533 372 429

2731 2821 909 931 205 210

1514 1570 173 216

1341 1354 103 110

898 1177 93 82 0 -2

170 171 13 14

2002 2003 budget forecast

bn Manats

6455

7347

1524 1502

22 1430 1957 1515 442

1728 404 988 336 479

7118

229 115 114

1601 436 609 557

3377 1082 270

1896 381

1515 128

2076 95

1 248

18

7224

7845

1616 1603

13 1816 2135 1808 327

1530 324 5 64 642 591

7689

158 92 66

1864 551 683 630

3798 1216 301

2115 307

1808 166

1895 116

0 279

82

MEDIUM-TERM EXPENDITURE FRAMEWORK, 2000-2005 (CONSOLIDATED BUDGET)

Investment 517 791 1488 1130 1573 1638

2004 forecast

7655

8747

1849 1835

15 1961 2323 1983 340

1926 389

1021 515 511

8570

177 98 78

1920 571 746 603

4228 1339 390

2308 325

1983 192

2404 127

0 344 24

2005 forecast

857(

9408

2008 1992

1f 2183 248s 213C 353

2015 465

1022 525 515

921 1

198 114

84

2038 598 796 644

4635 1432 505

2490 354

2136 208

2562 139

0 395 28

Azerbaijan CFAA: Public Sector Buduetina 6

State Budget State Oil Fund Net foreign financed project loans

Transport and Communications Other economic affairs and services

Other Items Expenditure not included in major groups Employer contribution to SPF Extrabudgetary expenditure Privatization Fund expenditure (extrabudgetary)

2002 2003 2000 2001 budget forecast

bn Manats

2004 2005 forecast forecast

~ ~~

MEDIUM-TERM EXPENDITURE FRAMEWORK, 2000-2005 (CONSOLIDATED B U D G E T ) F l

Deficit 784 288 -892 -622 -1091 -8381

133 0

3 84 102

3 208 273

-277 202

10

126 4

661 118

3 205 280

-269 194

0

165 336 988 172 52

293 370

-327 250

0

425 142 564 223 64

288 61 1

-322 0 0

37 90 515 525

1021 1022 240 258 96 104

194 178 577 598

-383 -419 0 0

OI

0

1 1. With the support o f SAC-11, a new BSL has been approved by Parliament and has been enacted and became effective o n January 1, 2003. The B S L inter alia: (i) covers al l relations with state extra-budgetary funds, including the Oil Fund; (ii) provides for complete accounts o f extra-budgetary revenues, expenditures, and surplus balances as per economic and functional classification levels; (iii) ensures the full and transparent reporting to Parliament as well as to the media and public o f these accounts in the budget process; and (iv) stipulates that any resources drawn from the extra-budgetary funds, other than for meeting the State Oil Fund's o w n administrative expenses, shall be channeled through the State Treasury. The Law also establishes a firm link between local budgets and the central consolidated budget and prevents local self-governing bodies from borrowing outside the central budget. Separate comprehensive estimates o f extra- budgetary revenues and planned utilization wil l also be provided as wel l as revenue and expenditure estimates for investment projects.

12. and the 2004- 2007 MTEF and PIP for Cabinet approval before September 15,2003.

Consistent with the new BSL, the Government intends to prepare the 2004 budget

13. The Bank i s providing incentives and assistance in respect o f public sector budgeting through SAC-I1 and IBTA2. More specifically, second tranche conditionalities o f SAC-I1 which have now been met included the fol lowing measures to improve transparency and accountability in public financial management:

0 Cabinet approval o f Medium-Term Expenditure Framework for 2003-2005 ;

0 Cabinet approval o f Public Investment Program for 2003-2005 consistent with Medium-Term Expenditure Framework;

0 Cabinet approval o f 2003 budget consistent with Medium-Term Expenditure Strategy and Framework, and prepared according to key provisions o f new Budget Systems Law (calendar, comprehensiveness, documentation and

Azerbaijan CFAA: Public Secfor Buduefinu 7

disclosure), publication o f 2001 budget execution, and implementation o f 2002 budget according to new Budget L a w as applicable; and

0 Integration o f al l remaining state extra-budgetary resources into the state budget with the exception o f the Oil Fund.

14. The recently approved Bank-financed Second Institution-Building Technical Assistance credit (IBTA2) wil l finance institution-building technical assistance to help the Government to set up a PIP and to build appraisal capacity for the investment program by setting up a Public Investment Appraisal Division (PIAD) in the Ministry o f Economic Development. The TA will assist

0 the Government to develop a Public Investment pol icy framework to reflect the needs o f he population and priorities o f the Government and consistent with the Government’s PRSP. Based on this pol icy framework the TA will help the Government develop an investment strategy to prioritize sectors and project classes including a negative l ist if warranted and set up the capital budgeting criteria and procedures consistent with the strategy. Based o n this strategy the TA will help the Government to identify a series o f projects and an implementation schedule spread over a number o f years;

0 the Government to develop policies and procedures for treating unsolicited projects and rules for their inclusion in the PIP. Sufficient flexibility would be built in the project l i s t and schedule, so that it can be reviewed in light o f developments in the country and elsewhere and modified as required;

0 to set up the methodology and the operating policies and procedures ( including environmental assessments) for appraising and approving projects that are proposed for the PIP;

0 the Government to search for, locate and recruit the appropriate technical and management human resource skills needed to staff the project appraisal fbnction so that the P I A D can be adequately staffed;

0 to educate and train the project appraisal staff so that they know the procedures to be followed and have the capability to fol low these;

0 in conducting demonstrative project appraisals to illustrate and educate by example, how the project appraisal process i s to be implemented;

0 in preparing a functional design o f the appraisal process to identify softwarehardware needs and assist in i t s procurement and installation.

Azerbaijan CFAA: Public Sector Accounfina, Internal Controls and Reportins 8

3. PUBLIC SECTOR ACCOUNTING, INTERNAL CONTROLS AND REPORTING

Ministries and Budget Organizations, including the Ministry of Finance (MOF)

15. In common with other countries o f the former Soviet Union, Azerbaijan had a system under which Ministries operated their own bank accounts and financial management systems and provided information to the Ministry o f Finance and other designated authorities under relevant statutory and other normative instruments. The M O F did not have a Treasury but rather the National Bank o f Azerbaijan (NBA), the country's central bank, managed the implementation o f the Budget and performed al l cash operations.

16. Fol lowing i t s independence in 1991, the Azerbaijan Government has been engaged in an extensive fiscal and monetary reform program aimed at, amongst other things, improved fiscal management and applying internationally accepted public sector accounting practices. Significant improvements have already been achieved in public sector resource management including: (i) the establishment o f a Treasury and entrusting it with the responsibility o f managing the execution o f the Budget - in addition to the Central Treasury in Baku, 85 Regional Treasury offices have been established throughout the country; (ii) the closure of numerous bank accounts of ministries and BOs and the establishment o f a Treasury Single Account at the NBA; (iii) centralizing the cash management functions o f the State Budget knded organizations in the Treasury.

17. The comparatively recent creation o f the Treasury (1997) enables the M O F to produce more reliable and timely in fomat ion on the government's fiscal operations using a GFS-based classification. The Treasury produces monthly, quarterly, and annual reports on a cash basis covering the budgetary and extra-budgetary fiscal activity o f the central government and local governments. In 1999 i t introduced reporting requirements for three extra-budgetary funds and for externally financed development projects so that reports on the fiscal activity of the general government can be produced. Reconciliation with budget appropriation and bank accounts appears effective and timely. However, the manual processing and recording of fiscal transactions i s cumbersome.

18. In recognition o f the problem o f accumulating payment arrears, commitment controls were introduced in 1999, and an inventory o f the stock o f payment arrears accumulated before 1999 was compiled. However, in cases o f under-budgeting for uti l i t ies, services are not shut o f f once the budget appropriation has been used and spending agencies accrue arrears without registering commitments. Another concern i s that many budget organizations, especially those providing health and education services, charge fees or otherwise collect and spend revenues that are outside the budget process. In principle, these transactions are now processed through the Treasury and included in Treasury reports. In practice, however, i t i s not known whether al l o f these transactions are processed by the Treasury. Finally, in 1998 and 1999 problems were encountered with the privatization process and other revenues outside the budget process. In order to meet the deficit target, other planned spending had to be reduced and budget arrears increased.

Some problems with Treasury reporting and expenditure control remain.

Azerbaijan CFAA: Public Sector Accountinu, lnfemal Controls and ReDortina 9

19. improvements:

The establishment o f the Single Treasury account has resulted in the following

0 a reduction o f idle balances and better cash management by putting all Government resources under control o f the Treasury;

0 better controls during budget execution. Treasury checks whether budgetary expenditures are in accordance with the approved budget, within the specified spending l imits and funds allocations, prior to approving an expenditure transaction; and

0 more comprehensive accounting and fiscal reporting, thereby contributing to better financial management.

20. However, considerable scope remains for mher improvement o f the Treasury systems and procedures. Cash management needs to be strengthened, commitment control has to be more rigorously implemented and there i s a need for significant improvement in the capacity to generate meaningful and timely reports. The Treasury has therefore embarked upon the implementation o f a modern Treasury Information Management System (TIMS) to assist the govemment in achieving these and other improvements.

21. include:

K e y pol icy actions that are currently being pursued by the MOF / Treasury

0 implementation o f a transaction based Treasury Information Management System (TIMS) embodying a new chart o f accounts conforming with the GFS methodology;

0 implementation o f effective Public Expenditure Control Regulations to manage the level and timing o f expenditures and the extent o f arrears, including: (a) Financial Control (i.e. the approval and authorization stages o f proposals to spend public moneys before a commitment is entered into); (b) Accounting Control (i.e. including the certification o f claims for payment before a payment i s made); and (c) Audit Control (Le. the ex post review o f expenditure undertaken);

0 improvements in Cash Management and Budget Execution including instituting effective forecasts o f monthly and weekly expenditure requirements and revenue collections; and

0 reduce reliance on physical movements o f cash in the Budget Revenue Collection and Execution processes by effecting general payments o f Government through electronic movements between bank account balances through the banking system rather than cash movements.

22. The IMF provided init ial technical assistance to the Treasury in the development o f a new budget classification structure, a chart o f accounts and the hnctional specifications for a fully functioning treasury system through an expert resident in Azerbaijan. The IMF also provided advice to the MOF/Treasury on issues o f Budget

Azerbaijan CFAA: Public Sector Accountinu, Internal Confrols and Reporting 10

Execution, Cash Management and Treasury Operations. Subsequently the U S AID, through a competitive bidding process, selected a systems integrator to select application software in accordance with the functional requirements devised with the assistance o f the IMF and to supervise its implementation, including testing. I t is anticipated that the USAID-financed assistance wil l include the fol lowing activities:

0 Review existing budget classifications and coding structures and develop and design a revised structure and chart o f accounts conforming with the IMF- GFS classification methodologies and suitable for both budget preparation and implementation.

0 Assist in the development o f the legal regulatory and operational framework and develop detailed guidelines, procedures, regulations, forms and operating manuals for budget execution processes required at a l l levels o f Treasury operations to implement the Treasury System and for payroll management.

0 Assist in the development o f methods to improve forecasting o f expenditure requirements and cash management.

0 Develop the fiscal reporting system o f Treasury and improve linkages between the Treasury fiscal reports and MOF analysis.

23. Second tranche conditionalities o f SAC-I1 include measures to improve strategic priori ty setting and transparency o f medium-term public expenditure and investment programs, including: the publishing o f quarterly financial and budget execution statements satisfactory to IDA, i.e., with expenditures (other than administrative expenses) in accordance with the Consolidated Budget, and financial flows in accordance with Governance and Management Framework.

Treasury Information Management System

24. The overall design o f the TIMS system wil l be based on the IMF recommendations for the Government Financial Management Information System (GFMIS). The core functional processes and information flows associated with the system are shown schematically below.

Azerbaijan CFAA: Public Secfor Accountina, lnternal Controls and Reporfina 7 7

Core Functional Processes and Information Flows - Treasury is responsible for making payments;

Flrcal Rep

.I

I

I\

f

1 R E A S U R Y

I

f n

0 r m

t I

n M

0

a n

c

e n

0

m

t

S Y

t

m

I

e

-

S

Paymenh through

SWIFT _ I i.

7

Online Transactmns & Balances

through SWFT

x -

r------7

I , I

v Commercbl

Banks (Regional Branches]

25. would be used by:

The Treasury Information Management System would be the core GFMIS and

0 the Central Treasury and the 85 Regional Treasury offices to perform comprehensive accounting functions and to undertake budget implementation and generate reports for use by respective offices;

0 the Cash Management Department to forecast and monitor cash flows and determine cash l imits for budget organizations;

0 the Central Treasury to access data o f a l l the treasury offices for quality assurance and other purposes and to carry out consolidation and generate reports for macro fiscal management purposes;

0 the Budget Department o f the MOF to obtain reports for instance on the status o f actual expenditures; and

0 the Chamber o f Accounts to access financial transaction data for auditing purposes.

26. In a fully automated accounting system, as it exists in most developed countries and several middle income countries, the basic accounting processes are automated and data captured only once as an accounting transaction progresses through the system. Such a system, introduced along with a modem budget classification system and an appropriate

Azerbaijan CFAA: Public Sector Accountina, Internal Controls and RePodinins 12

chart o f accounts, enables expenditures and revenues to be recorded at a very detailed level and related to specific programs and projects. Data recorded at this level can be directly used for program and project management. This data i s also easily amenable to cross classification in other ways as required for financial analyses. In the absence o f an automated accounting system data recording is not at as detailed a level and more important, cross classification o f data to other schema is very cumbersome and therefore seldom carried out. Further more the introduction o f an automated accounting system would ensure completeness o f data capture (that i s no transaction would be processed outside the system) and rigorous application o f a l l relevant financial controls to a l l transactions processed by the system. The information contained in the system data bases would provide the MOF and other core financial agencies a foundation for a comprehensive management information related to the country’s financial resources. The information contained in the data bases would be available to other core government agencies o n a as required / approved basis. In addition, the system would provide usefu l financial information to the ministries, spending units (in their respective areas) to enable them to better manage their work programs.

27. The TIMS system wil l encompass the functional requirements for the budget implementation and accounting processes and would cover the appropriation, commitment, funds allocation, and payment processes for both the investment and current budgets. Specifically the budget execution system would have a capability to:

Record init ial budgets and inform spending ministries about their initial budget appropriations as approved by the legislature, keep a record o f ini t ial budgets, revised budgets, and budget transfers, for a typical government ministry/ spending unit.

During the course o f a year distribute appropriation and commitment authorization in fomat ion to ministries/ spending units and to record commitments incurred by a ministry against the approved limits and the appropriation.

Keep a record o f the amounts o f funds allocations against the appropriations and any changes thereto.

Record expenditure against commitments / budget and funds allocations (e.g. due to purchase orders, or other payments). The system will have facilities to check availability o f appropriation, commitment and funds allocation prior to approving a payment.

Print or transmit electronic consolidated payment instructions to be acted upon by the banking system.

Record revenue and other receipts against appropriate account heads.

If required, print checks against payment instructions and or make arrangements for the electronic transfer o f payment information to an external paying entity (e.g. a Bank).

Azerbaijan CFAA: Public Sector Accountins, lnternal Controls and ReDorfins 13

0 Consolidate data from regional treasury offices, as necessary. The system will have good report writing facilitates and enable easy retrieval and reporting on data in the system data bases, in a variety o f formats. The system would be able to produce the commonly required accounting and management reports.

0 The system would have facilities to restrict access only to duly authorized staff.

28. The architecture proposed for the TIMS system by the Government under advice from the resident IMF advisor envisages a centralized system running at the central Treasury office in Baku. The 85 regional treasuries distributed through out the country would connect to this system in an online mode to process transactions. Such an architecture has the advantage that i t eliminates the need to synchronize system data bases that would be necessary in a distributed system and would reduce system maintenance costs and efforts since the application software would only be operating at the Central site. This strategy i s dependent upon a high speed and reliable telecommunications network; such a network will, according to the Ministry o f Communications, be established within the next two or three years, and indeed is already available for approximately 50% o f the 85 cities in which the regional treasuries operate.

29. The recently approved Bank-financed IBTA2 project will assist in the implementation o f TIMS by financing: technical assistance, computer equipment, software and training to assist the authorities to design, develop, test and implement processes, procedures and systems, related regulations and training programs for budget execution and treasury operations. The TIMS system wil l f i rst be implemented at a set o f pi lot sites and then replicated across the country. More technical details in respect o f financing to be provided by I B T A 2 may be found in the relevant project documentation.

Extra-budgetary Operations and Funds, Including the Oil Fund

30. are subject to standard Treasury accounting, internal control and reporting requirements.

Extra-budgetary operations o f ministries and BOs pass through the Treasury and

3 1. The Parliament adopted the Law "On the Social Protection Fund" o n November 15, 2001, which provided for the specialized social funds - Social Protection Fund, Disabled Person's Fund and Employment Fund - to be merged. Similarly, according to the Law on Budget 2002, eleven extra-budgetary funds (0.8 bln Manats) out o f 85 are to be included directly with the revenues and expenditure parts o f the Budget 2002. In 2003 the other extra-budgetary funds and operations o f budget agencies wil l be included to the state budget. At that point the O i l Fund and the Social Protection Fund will be the only remaining extra-budgetary funds. Bo th the Law on Budget 2002 and the L a w "On the Social Protection Fund" were made effective on January 1,2002.

32. The o i l windfall has been handled well to date, with the Government avoiding oil- fueled spending sprees, rapid external debt accumulation, or excessive real appreciation o f the exchange rate. To improve management o f natural resource revenues, the State Oil Fund was established by Presidential Decree on December 29, 1999. The Fund was set up as an extra-budgetary institution accountable to the President and became effective at the beginning o f 2001. Preparation o f the Oil Fund budget and the Government budget i s

Azerbaijan CFAA: Public Sector Accounfina, lnternal Controls and Reporting 14

done in tandem within overall macroeconomic and fiscal aggregates agreed with the IMF, and the consolidated budget presented to Parliament. Sources o f Oi l Fund revenues include bonuses and revenues from sale o f crude o i l and gas, and earnings from related activities. In i t ia l ly the Oil Fund’s assets amounted to US$270 mil l ion. These assets increased to US$499 and US$690 mi l l ion at end-2001 and end-2002 respectively.

33. The Oil Fund’s non-operational expenditures are: (i) strictly l imi ted to funding projects within the consolidated Government budget, which correspond to strategic priorities as outlined in the PRSP, MTEF, and PIP; (ii) channeled through the Treasury; (iii) consistent with the overall fiscal policy, which aims at continued macroeconomic stability and growing the national wealth, including the value o f human, physical and natural resources; (iv) subject to high standards with regard to accountability and transparency to ensure aggregate fiscal restraints and good governance essential for fiscal discipline and avoiding the danger o f hurriedly and ill-conceived expenditure projects; (v) not only to be based on the availability o f resources, but also to take into account institutional capacity to spend these efficiently today, as compared to saving them for future generations; (vi) subject to a proper assessment o f r isk and uncertainty, especially with regard to volatile o i l prices; and (vii) not to be made for investing in commercial activities where the private sector is typically more efficient. In this way, the O i l Fund will help to strengthen fiscal discipline by providing a measure o f insulation for i t s assets from political spending pressures. Adherence to the Oil Fund regulations and disclosure rules i s a structural performance criterion o f the ongoing IMF’s PRGF program.

34. Given the current low-income status o f Azerbaijan and the pressing need to reduce poverty, some o f the Oil Fund’s funds, consistent with sustainable development, wil l be allocated for additional expenditure for lifting bottlenecks that prevent growth and especially affect the poor. Direct poverty reducing measures are warranted to alleviate the plight o f the poorest, and among them the one million Internally Displaced Persons (IDPs) and refugees o f the Nagorno-Karabakh conflict. Thus, the f i rs t allocation by the O i l Fund was for housing projects for IDPs in the amount o f US$36 m i l l i on which was followed by a second allocation of US$40 million. Other alternatives for spending out o f the O i l Fund are investment in human capital and rehabilitation o f infrastructure, especially in rural areas.

35. A Supervisory Board for the O i l Fund was appointed in December 2001 and implements general oversight over the composition o f the Oil Fund’s assets and compliance to the expenditure rules. I t represents a structure o f a very formal nature, as ultimate supervision and decision-making prerogative rests only with the President. The first meeting o f the Supervisory Board was held in July 2002, was inaugurated by the President and elected the Prime Minister to the position o f Chairman. Members o f the Board are also appointed by the President and comprise ten members including key governmental officials (such as the prime minister, key economic ministers and advisers, and the Chairman o f the Board of the National Bank) as we l l as academia. Members o f the Supervisory Board meet at least once every quarter, but any member o f the Supervisory Board or the Executive Director can call for an ad-hoc meetings, when necessary. The preparation o f the Oil Fund’s budget and investment pol icy are carried out in consultation and coordination with the MOF and endorsed by the Supervisory Board prior to approval by the President. In November 2002, the Oil Fund’s 2003 budget was

Azerbaijan CFAA: Public Secfor Accountinq, lnfernal Controls and Reoodinq 15

discussed and endorsed. O i l Fund expenditures (other than administrative expenses) wil l be part o f the approved and published Consolidated Budget, MTEF and, for investment projects, o f the PIP, which al l wil l be submitted to the Parliament according to the new BSL.

36. In the init ial stage, the Oil Fund aims to build up i t s capital. Prudential asset management guidelines have been developed to ensure that the assets are managed in a professional way, and in an open and competitive tender internationally recognized f i r m s are hired to manage the assets. The intention o f the Oil Fund’s disbursement rules is to allow the Fund to make a contribution to current consumption and to domestic capital investment o n a sustainable basis. The adopted Regulations provide that the Oil Fund budget be prepared at the same level o f detail and classification as the state budget. Furthermore, the expenditure o f the Oil Fund will be consistent with the approved annual state budget and (except for i t s own administrative expenses) wil l be executed through the Treasury, subject to standard accounting, procurement and other rules. In line with i t s Regulations, the Oil Fund i s audited annually by an intemationally recognized auditor, and makes public both the audited financial statements as well as an annual report and budget. Unaudited quarterly financial information o n the revenues and assets o f the O i l Fund is released to the general public and mass media as well as on other occasions if deemed necessary. Finally, quarterly published budget execution reports include information o n Oil Fund expenditures.

State-owned Enterprises

37. As discussed earlier, the non-oil sector remains constrained by slow progress with financial discipline and efficient management in public utilities that together are estimated to generate a quasi-fiscal deficit which averaged approximately 14 percent o f GDP in the period 1998-2001. To support and enable the design and implementation o f the programs o f reform and privatization in the utility and o i l sectors, the Government is aware o f the need to have access to and provide prospective investors with appropriate financial and operational information. In this regard, the ongoing MOF-led reform o f A z e r i accounting standards (see discussion further on in this CFAA) i s a key tool of government.

38. The Government has also recently instructed SOCAR, Azerenergy, Azerigaz and A R W C to deliver and also share with the Government, NBA, IMF and World Bank: (i) monthly accounts receivable statements arranged by user groups; (ii) monthly statements o f non-technical losses; (iii) monthly statements of historic and projected cash flows; (iv) annual financial statements prepared in accordance with International Accounting Standards (IAS’) as well as an audit opinion thereon from a reputable intemationally- recognized auditor having performed the audit in accordance with International Standards on Auditing (ISA); and (iv) a plan to upgrade their financial management arrangements, including the design and implementation of appropriate accounting procedures and internal controls, to enable the production of reliable, relevant, accurate and timely

For the purposes o f this report, the term “IAS” encompasses the standards endorsed by the International Accounting Standards Board (IASB), including those designated “International Financial Reporting Standards” (IFRS)

Azerbaijan CFAA: Public Sector Accounfinu, lntemal Controls and Reportinu 16

financial and management accounting information. Additionally, the Government wil l begin a review o f the adequacy o f electricity, gas and water tariffs.

39. I t i s anticipated that, in the context of the prospective EU-TACIS project to assist in the introduction, development and application o f international financial reporting standards in the non-banking sector (see discussion later), support will be given to selected state-owned enterprises to help them effectively adopt and implement the new standards .

Azerbaijan CFAA: Public Sector Audifinu 17

4. PUBLIC SECTOR AUDITING

External auditing

40. The Constitution invests Parliament with the power to establish the Chamber of Accounts, the Supreme Audit Institution (SAI) o f the Azerbaijan Republic. The Internal Regulations (Charter) o f the Parliament confirms that the Chamber o f Accounts i s “a permanent budget control organ” reporting to Parliament and that the key senior positions o f the Chamber o f Accounts (the Chairman, the Deputy Chairman and seven Auditors) are to be elected to their positions by Parliament. After some confusion following the creation o f the Chamber o f Auditors in 1994 (see section below on private sector auditing), the L a w on the Chamber o f Accounts (1999) was passed establishing the Chamber o f Accounts

41. Fol lowing a review o f the Law on the Chamber o f Accounts by the IMF as wel l as a review o f the draft Internal Regulations o f the Chamber o f Accounts by the Bank, amendments to the Law on the Chamber o f Accounts have been enacted and Parliament has approved the Internal Regulations (Charter) of the Chamber o f Accounts. Together with the enactment o f the new Budget Systems Law, the Chamber o f Accounts is now invested with the necessary authority and r ights to enable it to audit and make public the results o f i t s audits o f a l l public sector bodies and organizations, including al l budgetary and extra-budgetary organizations and funds. I t was agreed that further revisions to the Law on the Chamber o f Accounts as well as the Internal Regulations (Charter) would be made in due course based upon practical experience o f their implementation.

42. The Chairman and the Deputy o f the Chamber o f Accounts were appointed by Parliament in June 2001 and five Auditors have since also been elected. Resources for the full staffing and proper functioning o f the Chamber were allocated in the 2002 budget. During 2002, and in conjunction with the Bank-financed Second Institution- Building Technical Assistance credit (BTA2), the Chamber intends to: (i) complete the appointment o f a l l seven Auditors; (ii) develop a revised organizational structure; (iii) formulate staff grades with appropriate j ob descriptions and recruitment criteria; (iv) equip the Chamber with appropriate numbers and types o f computers and software; and (v) prepare the Chamber’s 2003 work plan and present the related 2003 financial plan to Parliament. These matters are explicit pre-conditions for release o f the SAC-I1 second tranche.

43. In view o f the recent formation o f the Chamber o f Accounts as wel l as the comparatively limited experience o f i t s key senior post-holders in matters o f auditing, there i s a considerable amount o f capacity-building to be done. The objective o f the T A financed under B T A 2 is to advise the Chamber o f Accounts to maintain an appropriate legislative framework and develop an appropriate professional and institutional capacity in order that it may have a positive impact on the Azerbaijan public sector financial management. More specifically, the TA will:

0 Assist the Chamber o f Accounts to review, on an ongoing basis, the appropriateness of, and compliance with, the legal framework relating to the

Azerbaijan CFAA: Public Sector Audifina 18

Chamber o f Accounts, and provide advice on i t s internal organizational structure and human resource arrangements.

0 Provide the Chamber o f Accounts with the necessary working tools and practices including international Standards and Practices (INTOSAI), IT systems and office equipment, and procedures for developing the necessary work program and budgets.

Provide the Chamber o f Accounts with training, including formal training by Consultants in accounting and auditing, training provided by SAIs, INTOSAI, EUROSAI, Association o f Certified Chartered Accountants (ACCA).

0 Help the Government to arrange study tours and fellowships and support the qualification o f staff in professional accounting and auditing examinations such as those administered by the ACCA. The TA will also provide on-the j o b training to the staff o f the Chamber o f Accounts.

0 Provide advice and help to develop and implement an information strategy for the Chamber o f Accounts, including the manner by which the Chamber o f Accounts wil l communicate i t s objectives and results to the public.

0 Secure representation o f the Chamber o f Accounts in the appropriate international forum, including INTOSAI and its regional associations, EUROSAI and ASOSAI. I t wil l also help to organize and advise o n the participation o f the Chamber o f Accounts at appropriate international SA1 conferences, symposiums, seminars and working parties.

44. The Chamber o f Accounts i s planning to submit to Parliament reports on budget execution and other reports for the six-month period ending June 30, 2002. I t will take some time before the Chamber i s fully functioning, but it i s planning to audit at least one ministry and one state owned enterprise in the course o f 2002.

Internal auditing

45. Presidential Decree No. 462, On Compliance o f Rules in Controlling the Industry, Service and Finance-Credit Activities, o f June 17, 1996 sought to reduce the number o f dual, parallel and unwarranted inspections which were fe l t to be negatively impacting the development o f the market economy. However, i t was fel t that the measures introduced by the Decree did not go far enough and thus Presidential Decree No. 69, On Improvement o f Public Control System and Addressing the Art i f ic ial Obstacles in the Development o f Ownership, o f January 7, 1999 was also enacted. The latter decree abolished al l intemal inspectiodcontrol departments o f ministries, committees and other central executive power bodies, except for: the M a i n Department o f Public Finance Control (MDPFC) in the M O F in respect o f public finances; the Ministry o f Taxes in respect o f matters within i t s jurisdiction; and the National Bank o f Azerbaijan (NBA) in respect o f i t s role as banking supervisor. The Government took this action as part o f its strategy to reduce obstacles for private sector development; i t was felt that these departments unduly harassed the Budget Organizations (BOs) and companies under their jurisdiction leading to both widespread inefficiencies and corruption.

Azerbaijan CFAA: Public Sector Auditins 19