reshaping ict, reshaping business - fujitsu.com without walls.pdf · auchan agrees with carrefour...

TRANSCRIPT

Retailing without walls: La trasformazione del punto vendita in un contesto di multicanalità

Reshaping ICT, Reshaping Business

Copyright 2013 FUJITSU

Maurizio Tomasso Head of Retail CEMEA&I, Fujitsu Technology Solutions

1

Un contesto in continuo cambiamento

Copyright 2013 FUJITSU

«Lidl abandonne le "hard discount" en France»

Le Monde AFP Oct. 2012

2

Un contesto in continuo cambiamento

Copyright 2013 FUJITSU

«Our hypermarkets are great, but we will need them less and less , as the future is multichannel»

Philip Clarke, DG Tesco, les Echos Aprile 2013

3

Un contesto in continuo cambiamento

Copyright 2013 FUJITSU

AUCHAN agrees with CARREFOUR on

hypermarket basics

Carrefour and Auchan agree they need to breathe life back

into hypermarkets. The comments came during a

conference organised by LSA.

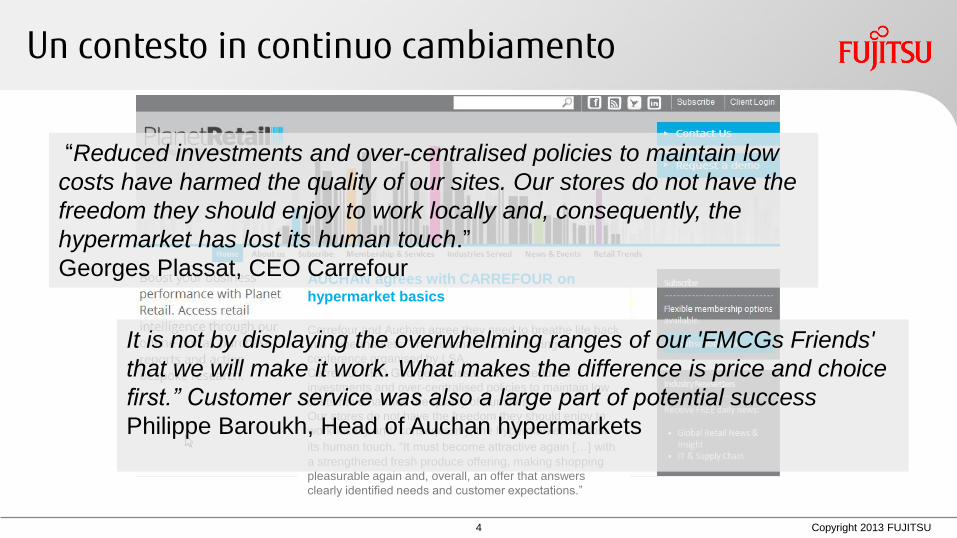

Carrefour CEO Georges Plassat noted: “Reduced

investments and over-centralised policies to maintain low

costs have harmed the quality of our sites.

Our stores do not have the freedom they should enjoy to

work locally and, consequently, the hypermarket has lost

its human touch. “It must become attractive again […] with

a strengthened fresh produce offering, making shopping

pleasurable again and, overall, an offer that answers

clearly identified needs and customer expectations.”

4

Un contesto in continuo cambiamento

Copyright 2013 FUJITSU

AUCHAN agrees with CARREFOUR on

hypermarket basics

Carrefour and Auchan agree they need to breathe life back

into hypermarkets. The comments came during a

conference organised by LSA.

Carrefour CEO Georges Plassat noted: “Reduced

investments and over-centralised policies to maintain low

costs have harmed the quality of our sites.

Our stores do not have the freedom they should enjoy to

work locally and, consequently, the hypermarket has lost

its human touch. “It must become attractive again […] with

a strengthened fresh produce offering, making shopping

pleasurable again and, overall, an offer that answers

clearly identified needs and customer expectations.”

“Reduced investments and over-centralised policies to maintain low

costs have harmed the quality of our sites. Our stores do not have the

freedom they should enjoy to work locally and, consequently, the

hypermarket has lost its human touch.”

Georges Plassat, CEO Carrefour

It is not by displaying the overwhelming ranges of our 'FMCGs Friends'

that we will make it work. What makes the difference is price and choice

first.” Customer service was also a large part of potential success

Philippe Baroukh, Head of Auchan hypermarkets

5

Un contesto in continuo cambiamento

«We would love to open Amazon retail stores”

Jeff Bezos, CEO Amazon, CNET Nov. 2012

Copyright 2013 FUJITSU

6

Il perimetro di indagine

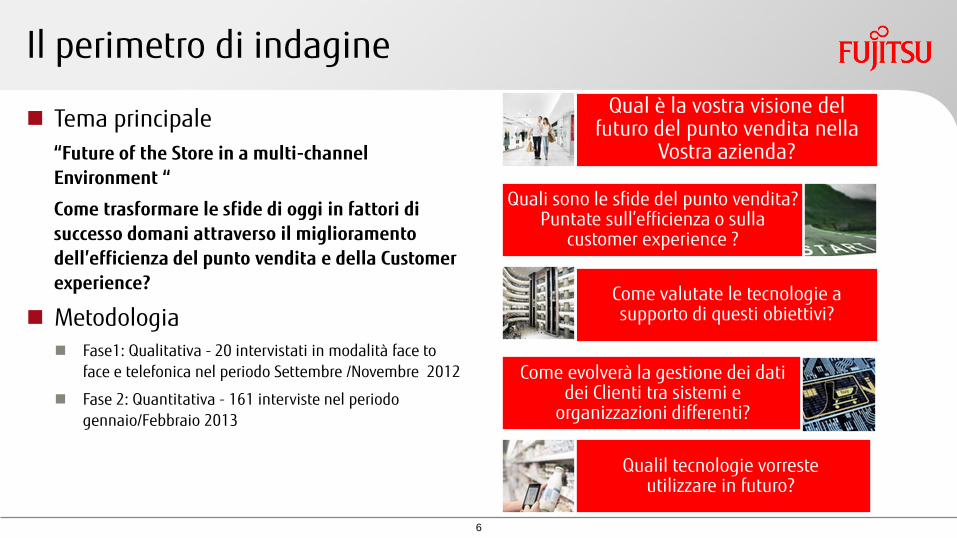

Tema principale

“Future of the Store in a multi-channel Environment “

Come trasformare le sfide di oggi in fattori di successo domani attraverso il miglioramento dell’efficienza del punto vendita e della Customer experience?

Metodologia Fase1: Qualitativa - 20 intervistati in modalità face to

face e telefonica nel periodo Settembre /Novembre 2012

Fase 2: Quantitativa - 161 interviste nel periodo gennaio/Febbraio 2013

Qual è la vostra visione del futuro del punto vendita nella

Vostra azienda?

Quali sono le sfide del punto vendita? Puntate sull’efficienza o sulla

customer experience ?

Come valutate le tecnologie a supporto di questi obiettivi?

Come evolverà la gestione dei dati dei Clienti tra sistemi e

organizzazioni differenti?

Qualil tecnologie vorreste utilizzare in futuro?

7

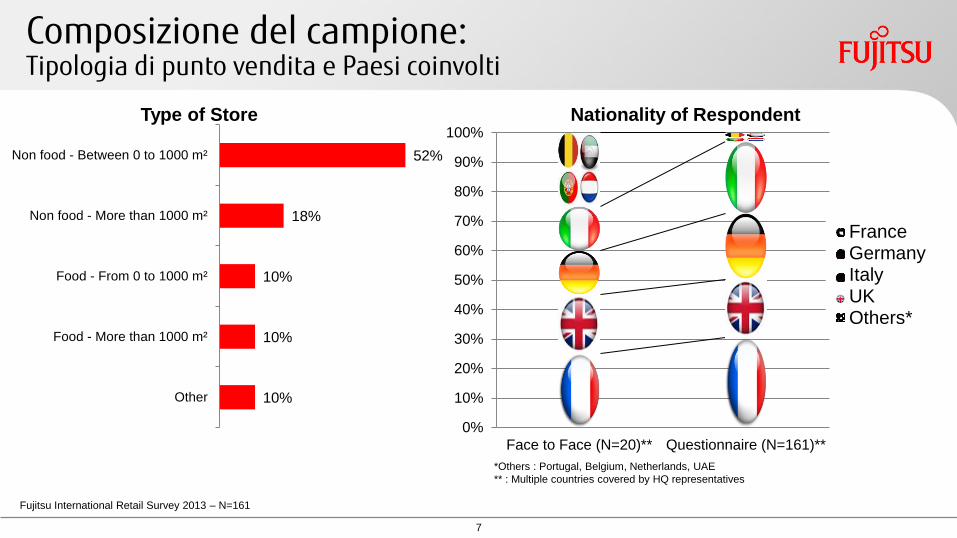

Composizione del campione: Tipologia di punto vendita e Paesi coinvolti

10%

10%

10%

18%

52%

Other

Food - More than 1000 m²

Food - From 0 to 1000 m²

Non food - More than 1000 m²

Non food - Between 0 to 1000 m²

Fujitsu International Retail Survey 2013 – N=161

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Face to Face (N=20)** Questionnaire (N=161)**

Others*Italy

Germany

*Others : Portugal, Belgium, Netherlands, UAE

** : Multiple countries covered by HQ representatives

Type of Store Nationality of Respondent

Others*

Italy Germany

UK

France

8

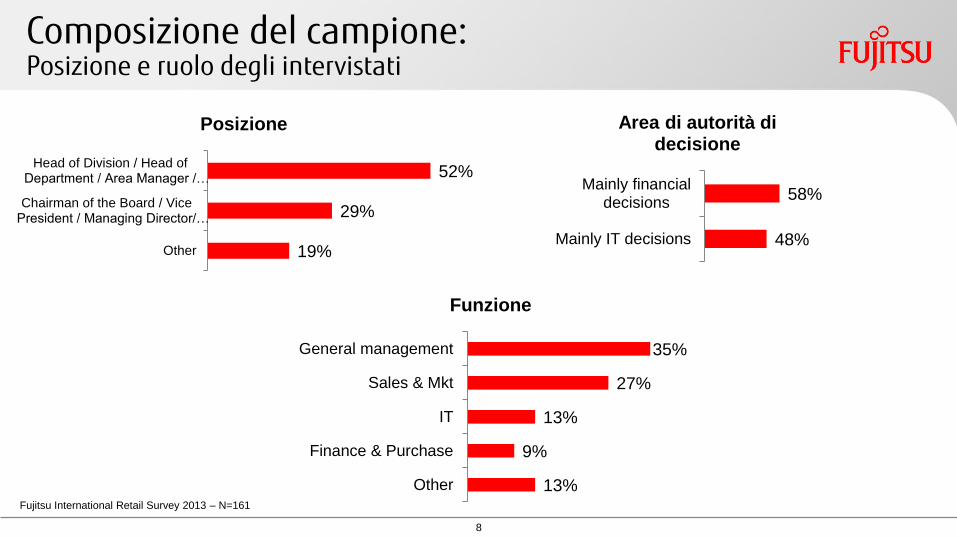

Composizione del campione: Posizione e ruolo degli intervistati

Fujitsu International Retail Survey 2013 – N=161

19%

29%

52%

Other

Chairman of the Board / VicePresident / Managing Director/…

Head of Division / Head ofDepartment / Area Manager /…

Posizione

48%

58%

Mainly IT decisions

Mainly financialdecisions

Area di autorità di decisione

13%

9%

13%

27%

35%

Other

Finance & Purchase

IT

Sales & Mkt

General management

Funzione

9

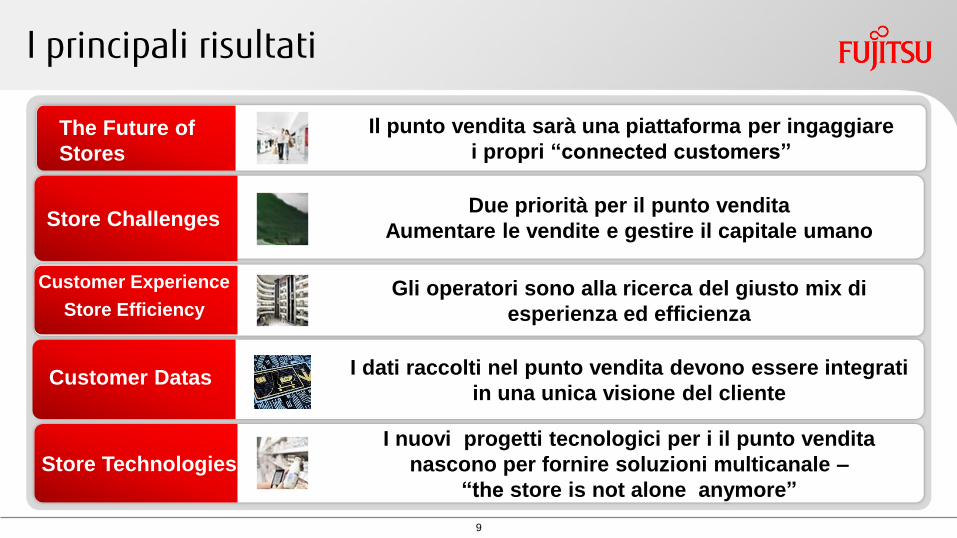

I principali risultati

Due priorità per il punto vendita

Aumentare le vendite e gestire il capitale umano Store Challenges

I dati raccolti nel punto vendita devono essere integrati

in una unica visione del cliente Customer Datas

Gli operatori sono alla ricerca del giusto mix di

esperienza ed efficienza

Customer Experience

Store Efficiency

I nuovi progetti tecnologici per i il punto vendita

nascono per fornire soluzioni multicanale –

“the store is not alone anymore”

Store Technologies

Il punto vendita sarà una piattaforma per ingaggiare

i propri “connected customers” Multi-Channel The Future of

Stores

10

Il punto vendita sarà una piattaforma per ingaggiare i propri «connected customers»

Copyright 2011 FUJITSU

“It's the 'central hub' of every activity” “Combining proximity and digital” “To make the web work better with the stores and the stores better with the web” “The store must be a customer experience, something pleasant where the products are highlighted"

11

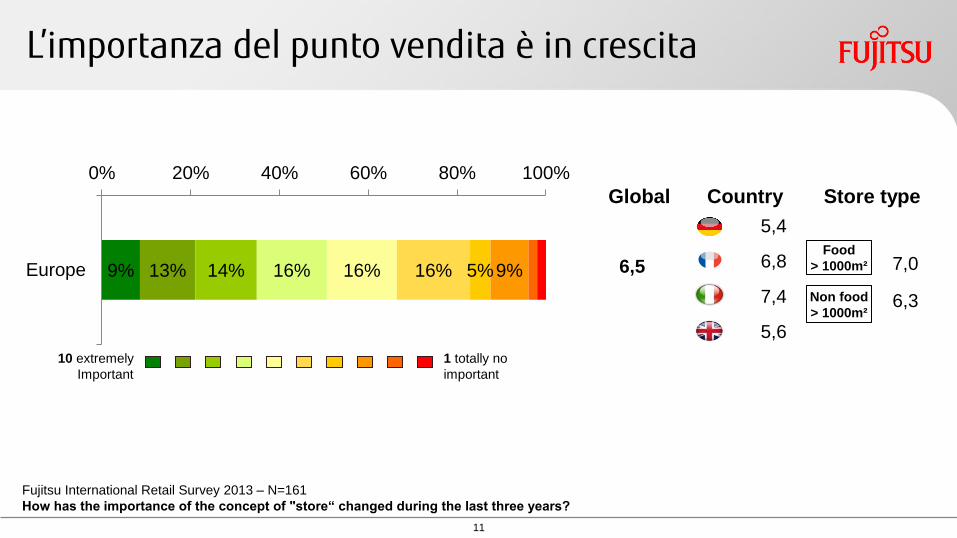

L’importanza del punto vendita è in crescita

10 extremely

Important

1 totally no

important

9% 13% 14% 16% 16% 16% 5% 9%

0% 20% 40% 60% 80% 100%

Europe 6,5

5,6

7,4

6,8

5,4

Country

Food

> 1000m²

Non food

> 1000m² 6,3

7,0

Store type Global

Fujitsu International Retail Survey 2013 – N=161

How has the importance of the concept of "store“ changed during the last three years?

12

Per l’ 86% il punti vendita è il luogo del servizio al cliente

58%

67%

76%

81%

86%

A pick-up point

A place of events,discovery andexperiences

Exposure to the brand

A shopping point

A place for service

Country Store type Food

> 1000m² Non food

> 1000m²

72% 94%

56% 91%

45% 88%

70% 46%

50% 76%

47%

75%

51%

69%

Fujitsu International Retail Survey 2013 – N=161

Thinking about the role “store”, to what extent do you agree or disagree regarding the following statements? The store is ...

13

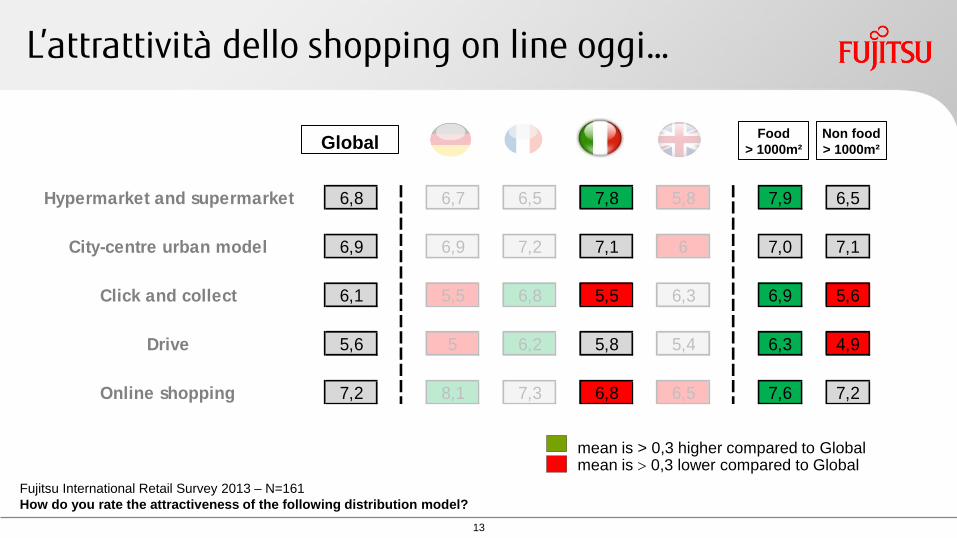

mean is > 0,3 higher compared to Global mean is 0,3 lower compared to Global

Global Food

> 1000m²

Non food

> 1000m²

Hypermarket and supermarket 6,8 6,7 6,5 7,8 5,8 7,9 6,5

City-centre urban model 6,9 6,9 7,2 7,1 6 7,0 7,1

Click and collect 6,1 5,5 6,8 5,5 6,3 6,9 5,6

Drive 5,6 5 6,2 5,8 5,4 6,3 4,9

Online shopping 7,2 8,1 7,3 6,8 6,5 7,6 7,2

L’attrattività dello shopping on line oggi…

Fujitsu International Retail Survey 2013 – N=161

How do you rate the attractiveness of the following distribution model?

14

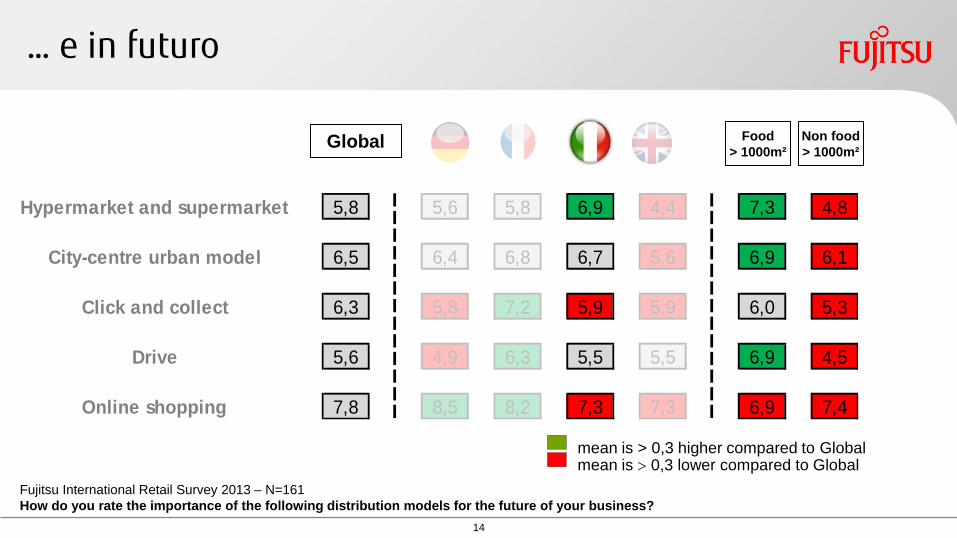

… e in futuro

mean is > 0,3 higher compared to Global mean is 0,3 lower compared to Global

Hypermarket and supermarket 5,8 5,6 5,8 6,9 4,4 7,3 4,8

City-centre urban model 6,5 6,4 6,8 6,7 5,6 6,9 6,1

Click and collect 6,3 5,8 7,2 5,9 5,9 6,0 5,3

Drive 5,6 4,9 6,3 5,5 5,5 6,9 4,5

Online shopping 7,8 8,5 8,2 7,3 7,3 6,9 7,4

Global Food

> 1000m²

Non food

> 1000m²

Fujitsu International Retail Survey 2013 – N=161

How do you rate the importance of the following distribution models for the future of your business?

15

Due priorità per il punto vendita Aumentare le vendite e gestire il capitale umano

Copyright 2013 FUJITSU

“The biggest challenge is improving sales while reducing costs” “Large volumes, lots of customers“ “The challenge is to optimise staffing

while keeping a significant level of

proximity to the customer"

16

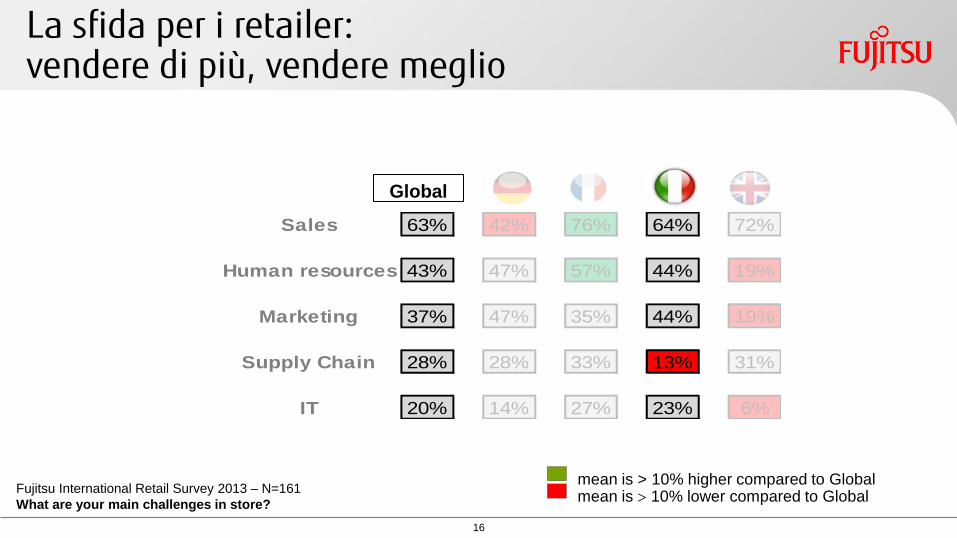

La sfida per i retailer: vendere di più, vendere meglio

mean is > 10% higher compared to Global mean is 10% lower compared to Global

Sales 63% 42% 76% 64% 72%

Human resources 43% 47% 57% 44% 19%

Marketing 37% 47% 35% 44% 19%

Supply Chain 28% 28% 33% 13% 31%

IT 20% 14% 27% 23% 6%

Global

Fujitsu International Retail Survey 2013 – N=161

What are your main challenges in store?

17

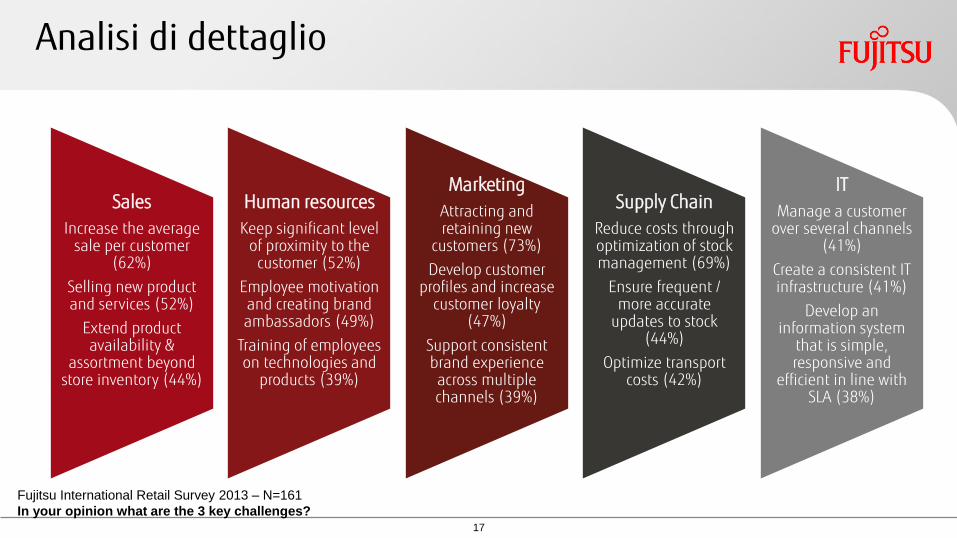

Sales

Increase the average sale per customer

(62%)

Selling new product and services (52%)

Extend product availability &

assortment beyond store inventory (44%)

Human resources

Keep significant level of proximity to the

customer (52%)

Employee motivation and creating brand ambassadors (49%)

Training of employees on technologies and

products (39%)

Marketing

Attracting and retaining new

customers (73%)

Develop customer profiles and increase

customer loyalty (47%)

Support consistent brand experience across multiple channels (39%)

Supply Chain

Reduce costs through optimization of stock management (69%)

Ensure frequent / more accurate

updates to stock (44%)

Optimize transport costs (42%)

IT

Manage a customer over several channels

(41%)

Create a consistent IT infrastructure (41%)

Develop an information system

that is simple, responsive and

efficient in line with SLA (38%)

Analisi di dettaglio

Fujitsu International Retail Survey 2013 – N=161

In your opinion what are the 3 key challenges?

18

La ricerca del giusto mix di esperienza ed efficienza

Copyright 2013 FUJITSU

“The real challenge is to work on productivity without harming the customer experience”

“We must find a balance between customer service and the cost of this service” “The real priority is to reintroduce proximity to the customers”

19

Efficienza operativa e customer experience le priorità per creare valore

Both store efficiency and customer experience 58% 56% 69% 49% 59%

Customer experience 18% 25% 8% 13% 25%

Store efficiency 17% 14% 14% 31% 13%

None of both 3% 3% 6% 0% 3%

Global

Fujitsu International Retail Survey 2013 – N=161

What are your current priorities for driving increased value from the store?

20

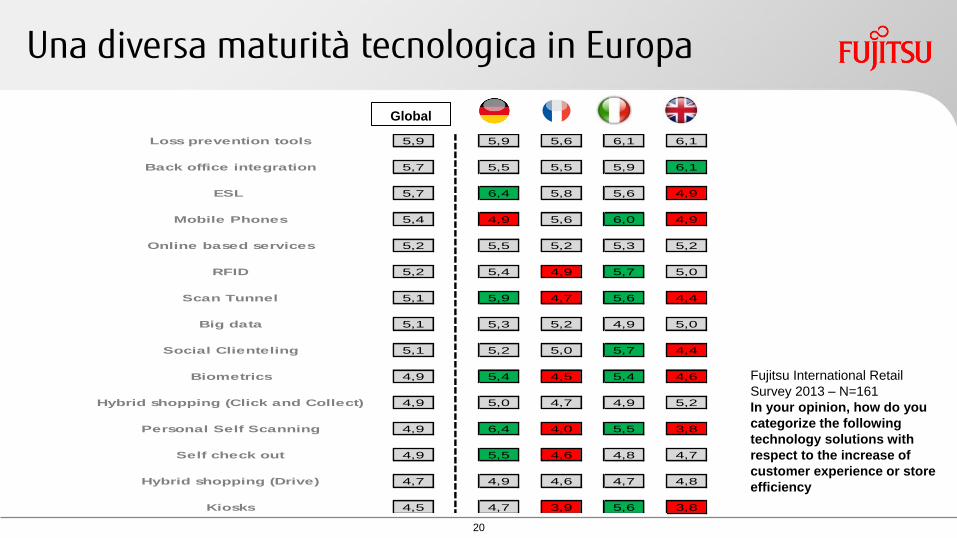

Una diversa maturità tecnologica in Europa

Global

Loss prevention tools 5,9 5,9 5,6 6,1 6,1

Back office integration 5,7 5,5 5,5 5,9 6,1

ESL 5,7 6,4 5,8 5,6 4,9

Mobile Phones 5,4 4,9 5,6 6,0 4,9

Online based services 5,2 5,5 5,2 5,3 5,2

RFID 5,2 5,4 4,9 5,7 5,0

Scan Tunnel 5,1 5,9 4,7 5,6 4,4

Big data 5,1 5,3 5,2 4,9 5,0

Social Clienteling 5,1 5,2 5,0 5,7 4,4

Biometrics 4,9 5,4 4,5 5,4 4,6

Hybrid shopping (Click and Collect) 4,9 5,0 4,7 4,9 5,2

Personal Self Scanning 4,9 6,4 4,0 5,5 3,8

Self check out 4,9 5,5 4,6 4,8 4,7

Hybrid shopping (Drive) 4,7 4,9 4,6 4,7 4,8

Kiosks 4,5 4,7 3,9 5,6 3,8

Fujitsu International Retail

Survey 2013 – N=161

In your opinion, how do you

categorize the following

technology solutions with

respect to the increase of

customer experience or store

efficiency

21

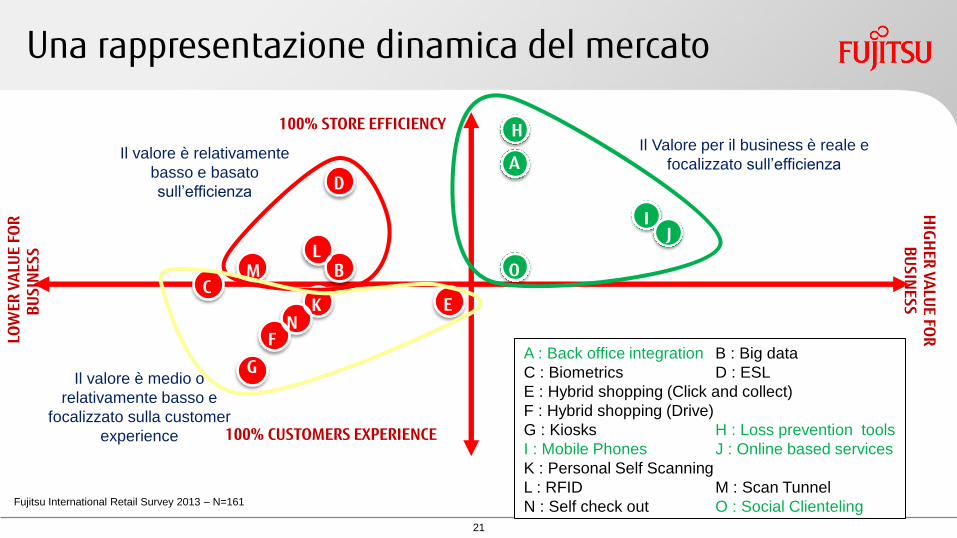

Una rappresentazione dinamica del mercato

100% CUSTOMERS EXPERIENCE

100% STORE EFFICIENCY

LO

WER

VA

LUE

FOR

B

USI

NES

S

A : Back office integration B : Big data

C : Biometrics D : ESL

E : Hybrid shopping (Click and collect)

F : Hybrid shopping (Drive)

G : Kiosks H : Loss prevention tools

I : Mobile Phones J : Online based services

K : Personal Self Scanning

L : RFID M : Scan Tunnel

N : Self check out O : Social Clienteling

C M

L

K N

F

D

B

E

G Il valore è medio o

relativamente basso e

focalizzato sulla customer

experience

Il valore è relativamente

basso e basato

sull’efficienza

A

O

H

I J

Il Valore per il business è reale e

focalizzato sull’efficienza

Fujitsu International Retail Survey 2013 – N=161

HIG

HER

VA

LUE FO

R

BU

SINESS

22

100% CUSTOMERS EXPERIENCE

100% STORE EFFICIENCY

LOW

ER V

ALU

E FO

R

BU

SIN

ESS

HIG

HER

VA

LUE FO

R

BU

SINESS

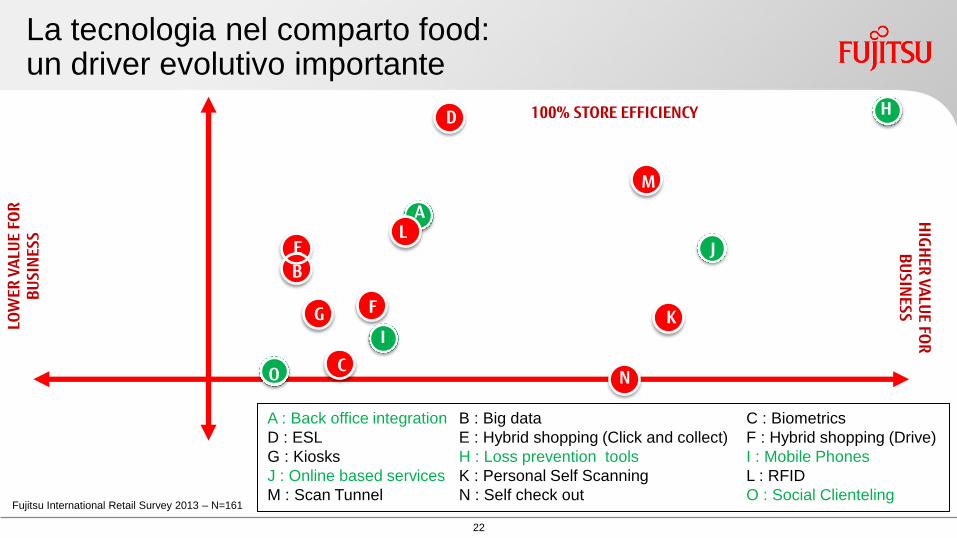

A : Back office integration B : Big data C : Biometrics

D : ESL E : Hybrid shopping (Click and collect) F : Hybrid shopping (Drive)

G : Kiosks H : Loss prevention tools I : Mobile Phones

J : Online based services K : Personal Self Scanning L : RFID

M : Scan Tunnel N : Self check out O : Social Clienteling

M

L

K

N

F

D

B

E

G

La tecnologia nel comparto food: un driver evolutivo importante

J

H

A

O

I

C

Fujitsu International Retail Survey 2013 – N=161

23

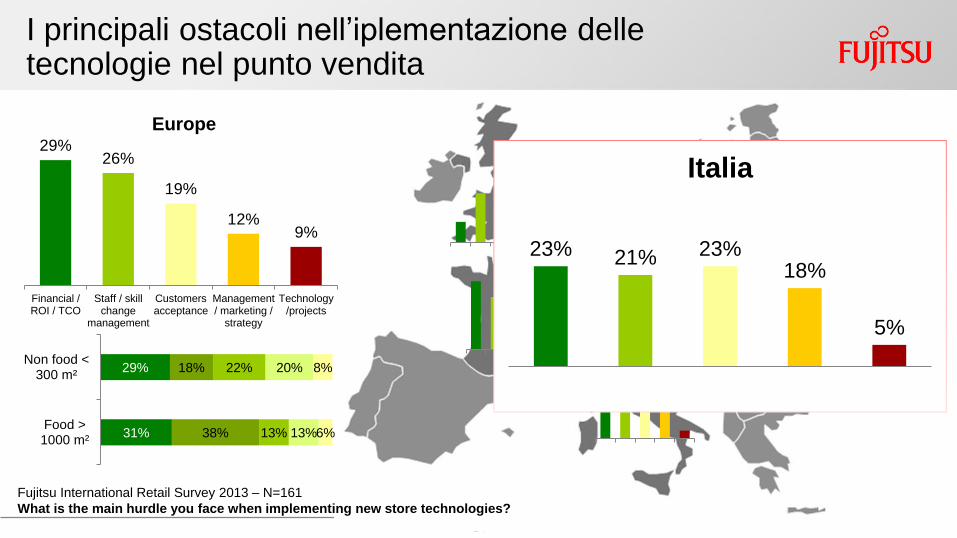

I principali ostacoli nell’iplementazione delle tecnologie nel punto vendita

Fujitsu International Retail Survey 2013 – N=161

What is the main hurdle you face when implementing new store technologies?

29% 26%

19%

12% 9%

Financial /ROI / TCO

Staff / skillchange

management

Customersacceptance

Management/ marketing /

strategy

Technology/projects

Europe

29%

31%

18%

38%

22%

13%

20%

13%

8%

6%

Non food <300 m²

Food >1000 m²

24

I principali ostacoli nell’iplementazione delle tecnologie nel punto vendita

Fujitsu International Retail Survey 2013 – N=161

What is the main hurdle you face when implementing new store technologies?

29% 26%

19%

12% 9%

Financial /ROI / TCO

Staff / skillchange

management

Customersacceptance

Management/ marketing /

strategy

Technology/projects

Europe

29%

31%

18%

38%

22%

13%

20%

13%

8%

6%

Non food <300 m²

Food >1000 m²

23% 21% 23% 18%

5%

Italia

25

I dati raccolti nel punto vendita devono essere integrati in una unica visione del cliente

Copyright 2013 FUJITSU

“You need more information and that's where the digital battle is being fought: information and comparing information.”

26

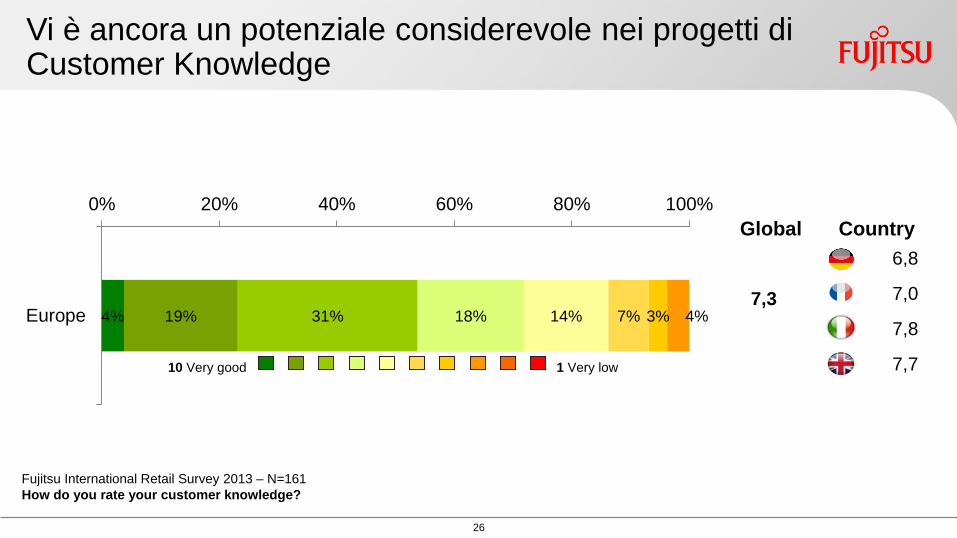

Vi è ancora un potenziale considerevole nei progetti di Customer Knowledge

1 Very low

4% 19% 31% 18% 14% 7% 3% 4%

0% 20% 40% 60% 80% 100%

Europe7,3

7,7

7,8

7,0

6,8

Country Global

10 Very good

Fujitsu International Retail Survey 2013 – N=161

How do you rate your customer knowledge?

27

I dati integrati nei sistemi CRM hanno fonti eterogenee: è necessario integrarle

Fujitsu International Retail Survey 2013 – N=161

Which of the following data types do you integrate in your CRM system as part of your business?

21% 17%

27%

14% 15%

Store data Multistoresdatas

Store andonline

channeldata

Store,online

channeland socialnetwork

data

None ofabove

Europe

28

I nuovi progetti tecnologici per i il punto vendita nascono per fornire soluzioni multicanale – “the store is not alone anymore”

Copyright 2013 FUJITSU

“Manage the increasing complexity of the customer relationship including with the increase of the social networks” “More and more integration between physical networks and the Internet"

29

Le tecnologie rivoluzioneranno il modo di acquistare nel punto vendita

83% 75% 92% 79% 78%

75% 67% 90% 64% 69%

71% 53% 90% 67% 63%

71% 50% 80% 77% 72%

70% 69% 65% 72% 75%

65% 67% 71% 59% 56%

61% 42% 71% 69% 53%

58% 53% 59% 51% 69%

Global

Retailers will transform into service providers,

moving beyond just selling merchandise

Multichannel interaction will be the norm

In-store shopping will become a more

enjoyable experience

Technology will be the key to allow the in-store

purchase to be revolutionised

Increase of in-store productivity will be a key

driver for growth

M-retailing will emerge to complement e-

commerce

The store will remain a majority source of

revenue

Store revenue as a percentage of retailer

revenue will continue to decline

Fujitsu International Retail Survey 2013 – N=161

Thinking ahead the next five years, do you agree/disagree with the following statements. How is your store

concept developing ...

30

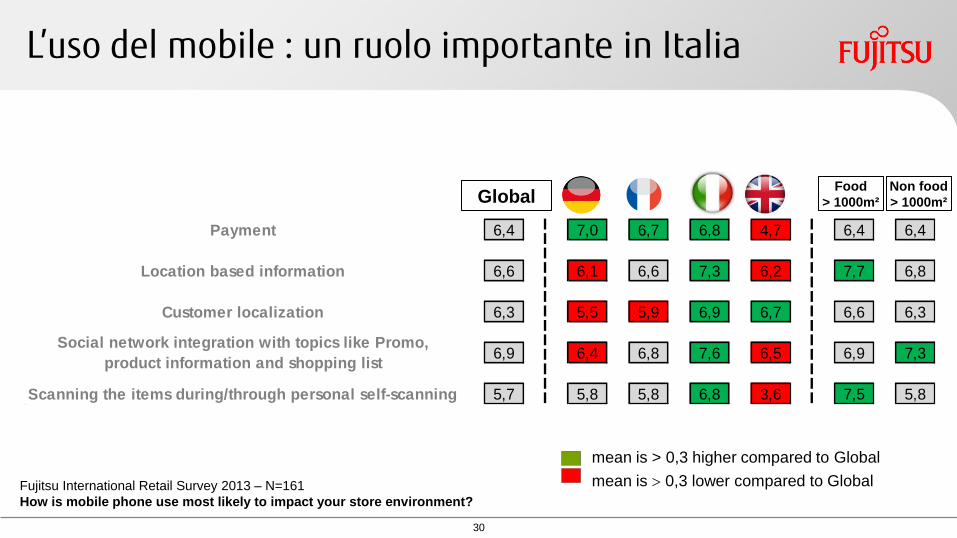

L’uso del mobile : un ruolo importante in Italia

mean is > 0,3 higher compared to Global

mean is 0,3 lower compared to Global

Payment 6,4 7,0 6,7 6,8 4,7 6,4 6,4

Location based information 6,6 6,1 6,6 7,3 6,2 7,7 6,8

Customer localization 6,3 5,5 5,9 6,9 6,7 6,6 6,3

6,9 6,4 6,8 7,6 6,5 6,9 7,3

Scanning the items during/through personal self-scanning 5,7 5,8 5,8 6,8 3,6 7,5 5,8

Social network integration with topics like Promo,

product information and shopping list

Global Food

> 1000m²

Non food

> 1000m²

Fujitsu International Retail Survey 2013 – N=161

How is mobile phone use most likely to impact your store environment?

31

Riassumendo: in Italia abbiamo rilevato che…

L’importanza del punto vendita: l’85% definisce il pdv come

luogo del servizio, il 46% li considera un punto di semplice pick-up.

Il 49% dei dirigenti intervistati interviewed crede che il valore del

punto vendita potrebbe crescere attraverso un miglioramento

bilanciato di efficienza e customer experience.

Ancora oggi circa il 21% degli intervistati dispone di informazioni

che non utilizza.

Per il 77%, le tecnologie deiventeranno decisive nel ridisegno

delle abitudini di acquisto nel punto vendita.

I 3 principali progetti per il punto vendita per migliorare la store

efficiency e la Customer Experience: Social clienteling (54%),

Loss prevention tool (44%), Back office integration (44%)

L’importanza dei punti vendita è maggiore che in altri contesti europei

(7,4/10 rispetto alla media di 6,5/10)

32

Il punto di vista di Fujitsu

Copyright 2013 FUJITSU

33

Le risposte di Fujitsu alle sfide del Retail

Approccio “Lean” e di miglioramento continuo

Smart Sourcing e Retail as a Service per ridurre le OPEX

RBA : Sales & Mktg, Supply Chain e Loss Prevention insieme Store Challenges

Retail Business Analytics / SAP Hana / CRM Cloud Applications

Applicazione POS MultiChannel per ridurre i data silos

Offerta tecnologica per la Data Center efficiency

Customer Datas

Consulenza di processo

Portfolio End to End

Approccio basato su ROI per progetti tecnologici e funzionali

Customer Experience

Store Efficiency

Approaccio multicanale con COMO

Innovazione nel Self Service

Innovazione con investimenti in R&D

Store Technologies

Shaping tomorrow with you

Esperienza nel punti vendita da 30 anni Multi-Channel Future of Stores

34

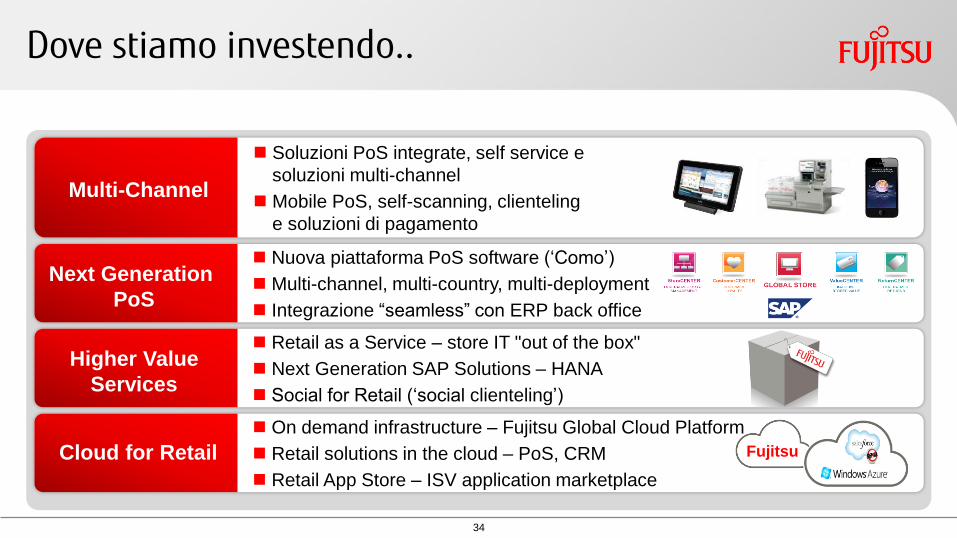

Dove stiamo investendo..

Soluzioni PoS integrate, self service e

soluzioni multi-channel

Mobile PoS, self-scanning, clienteling

e soluzioni di pagamento

Multi-Channel

Retail as a Service – store IT "out of the box"

Next Generation SAP Solutions – HANA

Social for Retail (‘social clienteling’)

Higher Value

Services

Nuova piattaforma PoS software (‘Como’)

Multi-channel, multi-country, multi-deployment

Integrazione “seamless” con ERP back office

Next Generation

PoS

On demand infrastructure – Fujitsu Global Cloud Platform

Retail solutions in the cloud – PoS, CRM

Retail App Store – ISV application marketplace

Cloud for Retail Fujitsu

35

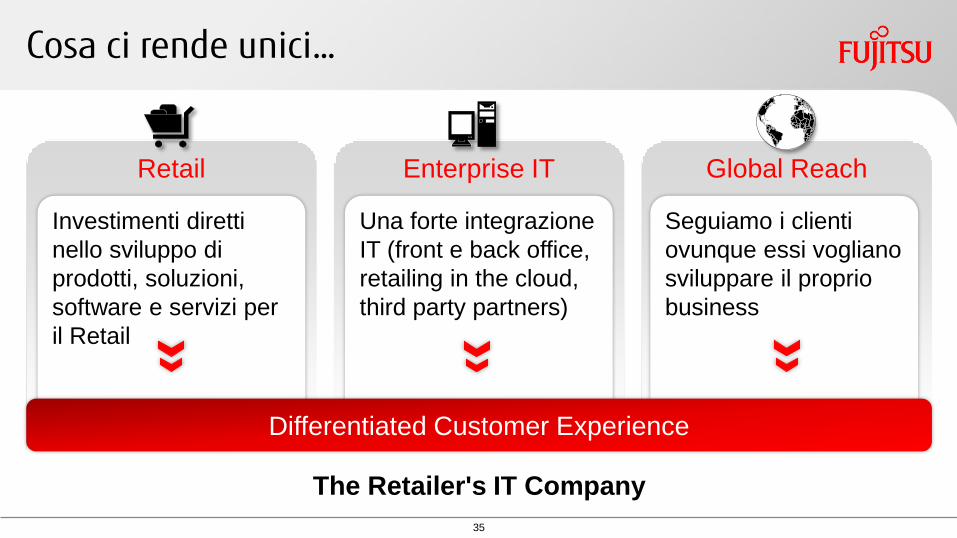

Cosa ci rende unici…

Retail

Investimenti diretti

nello sviluppo di

prodotti, soluzioni,

software e servizi per

il Retail

Enterprise IT Global Reach

Una forte integrazione

IT (front e back office,

retailing in the cloud,

third party partners)

Seguiamo i clienti

ovunque essi vogliano

sviluppare il proprio

business

Differentiated Customer Experience

The Retailer's IT Company

36

Il nostro più grande patrimonio: Lavorare con i retailer in tutto il mondo

37