retail intelligence utumn 2011 - fastighetsnytt

TRANSCRIPT

Retail Intelligence – Autumn 2011

The Retail Market in Sweden 2011

Sweden emerged from the global economic downturn fast, although the rate of economic growth is now slowing.

While still superior to most of Western Europe, Sweden‘s retail sales growth rate is lower now than in recent years.

Since 2009, retail transaction volumes have grown strongly, with prime retail property generating the greatest demand.

2 The Retail Market in Sweden • Autumn 2011

DefinitionsShopping centre A shopping centre is defined as a central location where shops, restaurants as well as service companies

and leisure operators are grouped together to serve a local or wider population. The building/s is/are created and managed as a single entity and the entity is managed by a single authority whose responsibility is to control the commercial mix, its implementation and adaption.

Retail warehouse Single level retail store selling non-food goods with at least 1,000 m² gross floorspace, occupying a warehouse, purpose-build or industrial-type building with substantial car-parking facilities.

Prime rent Represents the top open market net rent that could be expected for a notional prime position shop situated in the prime retail location in a market.

Prime yield Prime Yield represents the best (i.e. lowest) “rack-rented” yield estimated to be achievable for a shopping centre or retail warehousing.

Cross-border Cross-border describes investment flows from or into a country.

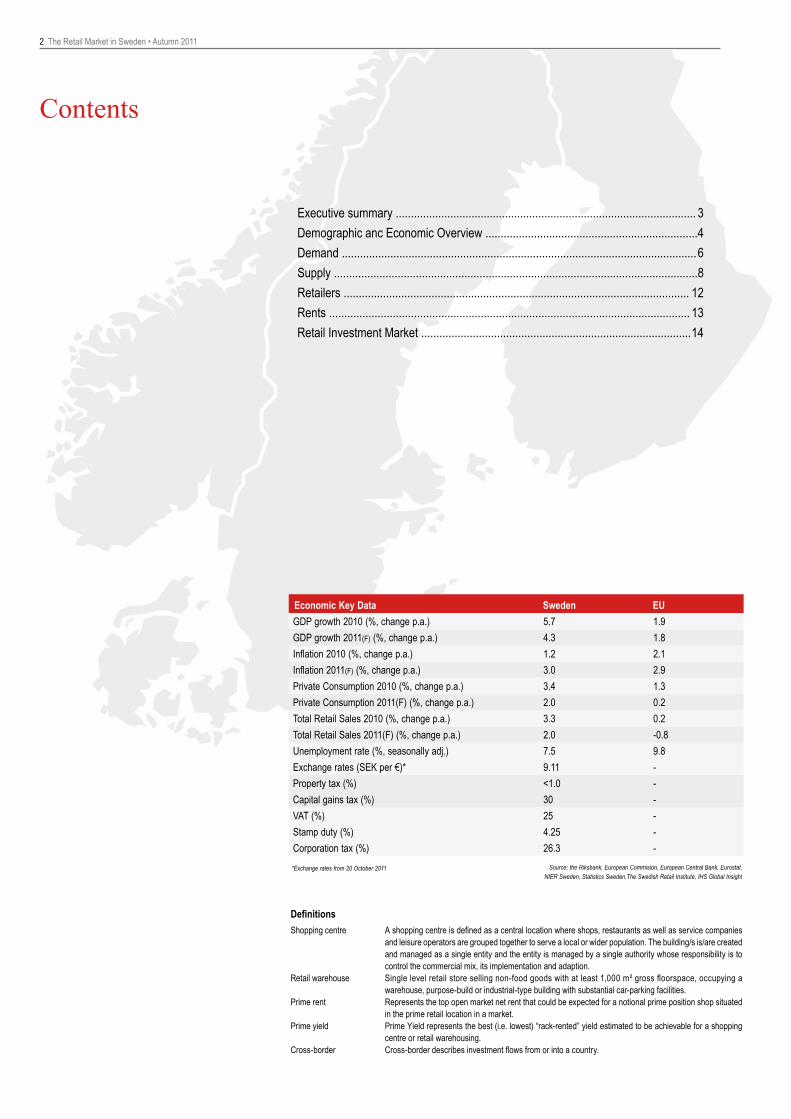

Executive summary ................................................................................................... 3 Demographic anc Economic Overview ...................................................................... 4 Demand ..................................................................................................................... 6 Supply ........................................................................................................................ 8 Retailers .................................................................................................................. 12 Rents ....................................................................................................................... 13 Retail Investment Market ......................................................................................... 14

Contents

*Exchange rates from 20 October 2011

Economic Key Data Sweden EUGDP growth 2010 (%, change p.a.) 5.7 1.9GDP growth 2011(F) (%, change p.a.) 4.3 1.8Inflation 2010 (%, change p.a.) 1.2 2.1Inflation 2011(F) (%, change p.a.) 3.0 2.9Private Consumption 2010 (%, change p.a.) 3.4 1.3Private Consumption 2011(F) (%, change p.a.) 2.0 0.2Total Retail Sales 2010 (%, change p.a.) 3.3 0.2Total Retail Sales 2011(F) (%, change p.a.) 2.0 -0.8Unemployment rate (%, seasonally adj.) 7.5 9.8Exchange rates (SEK per €)* 9.11 -Property tax (%) <1.0 -Capital gains tax (%) 30 -VAT (%) 25 -Stamp duty (%) 4.25 -Corporation tax (%) 26.3 -

Source: the Riksbank, European Commision, European Central Bank, Eurostat, NIER Sweden, Statistics Sweden,The Swedish Retail Institute, IHS Global Insight

The Retail Market in Sweden • Autumn 2011 3

Sweden emerged from the global economic downturn fast although the rate of growth is now slowing. Retail sales in Sweden have seen consistent growth for well over a decade, although in 2011, they are likely to record their lowest growth rate since 1996 for reasons including falling consumer confidence, the spill over effects of the debt crisis in several European countries and a general economic slow down in developed countries. Nevertheless retail sales growth will still be better than most West European countries. Disposable income is forecast to increase at a reasonable rate over the next couple of years as the government retains an expansive economic policy. Even during the recession of 2008 and 2009, Swedes’ be-nefitted from growing disposable incomes due to lower taxes, lower loan costs and decreasing inflation.

As a consequence of the 2009 recession, development of new retail accommodation has decreased. During the next few years, new shopping centre space will increase in Sweden’s 3 big city regions, with the Skåne region, which includes Malmö, seeing the highest rate of growth, not least due to the opening of Emporia shopping centre. Given that Sweden is a mature market for shopping centres, with amongst the highest amount of shopping centre space per capi-ta in Europe, the forecast rate of new shopping centre construction is considerably lower than less developed markets in Eastern Europe where existing shopping centre stock has historically been low.

The weaker economic and retail environment as well as the fact that the shopping centre market in Sweden is mature means that moving forward, more effort will be required for shopping centres to perform well. This means that retail property stock will need to evolve to reflect current lifestyles, socio-economic conditions and handle increased competition. This, in short, means creating more attractive shopping environments.

Sweden’s retailer mix has become increasingly international. New international fashion retailers in Sweden include, Hollister from the USA and Desigual from Spain. While the arrival of new retailers in Sweden has increased choice to the consumer, it has also increa-sed competition between retailers. For example, we have seen the effects of this increased competition in the electronic goods retail sector since the arrival of Germany’s Media Markt. Consumers have benefitted from lower prices and greater choice, while retailers have

battled to make money. During the Summer, OnOff was a high profile casualty in this sector and was forced to close its stores. With the recent arrival of Norwegian XXL Sport and the imminent opening of French Decathlon’s first store, it is likely that the sport & leisure sector will experience a similar evolution as the electronics goods sector.

In line with the ‘flight to quality’ trend by many retailers over recent years, retail rental growth shows a two tier structure, with prime retail units recording rental growth in excess of secondary units.

Similarly in the retail property investment market, it is prime property which is generating the greatest demand. Retail property investment transaction volumes have increased dramatically since the recession of 2009. Retail transaction investment volumes in H1 2011 were more than double the volumes recorded for the whole of 2009. In a European perspective, after the UK and Germany, Sweden recorded the most retail investment transactions in H1 2011. As confidence has returned to the retail investment market, so too have international purchasers. In H1 2011, 74% of the retail transaction volume was by international purchasers, up from 36% in H1 2010. The largest tran-saction, by far, in the first half of 2011 featured both an international vendor (Unibail Rodamco) and an international purchaser (Grosvenor Bouwinvest REIM) and was the sale of a portfolio of shopping centres in the Stockholm region, and an ICA Maxi in Helsingborg.

Since 2009, as transaction volumes have increased, we have seen prime retail yields harden, from 6.5% to 5.5% for prime external shopping centres and from 6.75% to 6.0% for prime retail warehouses. As economic uncertainty continues and interest rates increase, albeit gradually, we believe that prime retail yield compression will recede.

In summary, while the impressive retail sales growth we have seen in Sweden for many years is now slowing, performance is still likely to be better than most other West European countries. Given the increasing macro-economic and retail turnover head winds, compe-tition within the retail property market and amongst retailers will be intense. At the same time, prime retail property owners will benefit less from prime yields compression to realize increasing values, but instead, will primarily need to focus on superior asset management.

Executive Summary

4 The Retail Market in Sweden • Autumn 2011

Sweden – the largest country in the Nordic regionSweden sits at the heart of the Nordic region as well as being close to Germany, Poland and the Baltic countries. With a growing popu-lation of 9.4 million, Sweden is the largest of the Nordic countries. The majority of the population live in the southern part of the country where the country’s largest cities, Stockholm, Gothenburg and Malmö are situated. Urbanisation is occurring in Sweden, with population growth rates generally highest in the country’s larger urban areas and low or negative in rural areas.

GDP growthSweden has emerged strongly from the global economic downturn of 2008/09. GDP growth was 5.7% in 2010, far higher than the EU average of 1.8%. GDP growth in 2011 is also forecast to be relatively strong at around 4.3%, a rate which will surpass most other European countries. Reasons for the impressive growth have been increasing exports, household consumption and business investment, which have all been assisted by relatively low interest rates and the government’s expansive economic policies. These are being financed by strong public finances which have also meant that Sweden has been able to avoid implementing extensive economic austerity measures required in many Western countries.

The labour marketUnemployment in Sweden is decreasing. At the end of 2010 the unemployment rate was 8.4% but by the end of 2011 it is expected to have fallen to 7.5% and will remain at this level in 2012.

PoliticsSweden enjoys a politically stable climate and the change in govern-ment in 2006 from Social Democratic to Conservative rule, did not bring about economic instability. In the last general election in 2010 the Conservative government was re-elected.

Interest ratesDuring the recession of 2008 and 2009, the Riksbank (Swedish Central Bank) cut the official bank rate significantly to 0.25% in July 2009. However since September 2010, as the economy has impro-ved, the official bank rate has gradually been increased and in July 2011 stood at 2%. NIER forecast gradual increases in the official bank rate to 2% by the end of 2011 and 2.25% by the end of 2012.

Swedish Government Bond 10 year yieldsThe real Swedish Government Bond 10 year yield, approached 5% at the height of the financial crisis but is currently slightly negative and yields amongst the lowest in Europe. This yield reflects the market’s strong confidence about the relative economic health of Sweden.

InflationThe aim of Swedish monetary policy is to keep inflation growth at 2% per annum. In 2010, inflation (CPI) was 1.2% and the rate for 2011 is forecast to be 3%, reducing to 1.9% by the end of 2012. Current CPI at around 3% is due to higher home mortgage interest rates and the higher price of energy. However excluding energy, the direct effects of taxes and subsidies and the cost of interest, underlying inflation was low at only 0.8% in May according to the Swedish Statistics Agency. Reasons for this include the appreciation of the Swedish Kronor over the past year and a relatively weak labour market which limits pay increases.

Demographic and Economic Overview

GDP development in Europe

Source: Global Insight September 2011

-10

-8

-6

-4

-2

0

2

4

6Sweden

Russia

Poland

Germany

Finland

Czech Republic

Belgium

Netherlands

United Kingdom

France

Portugal

Italy

Hungary

Ireland

Spain

Romania

2009 2010 2011F 2012F%

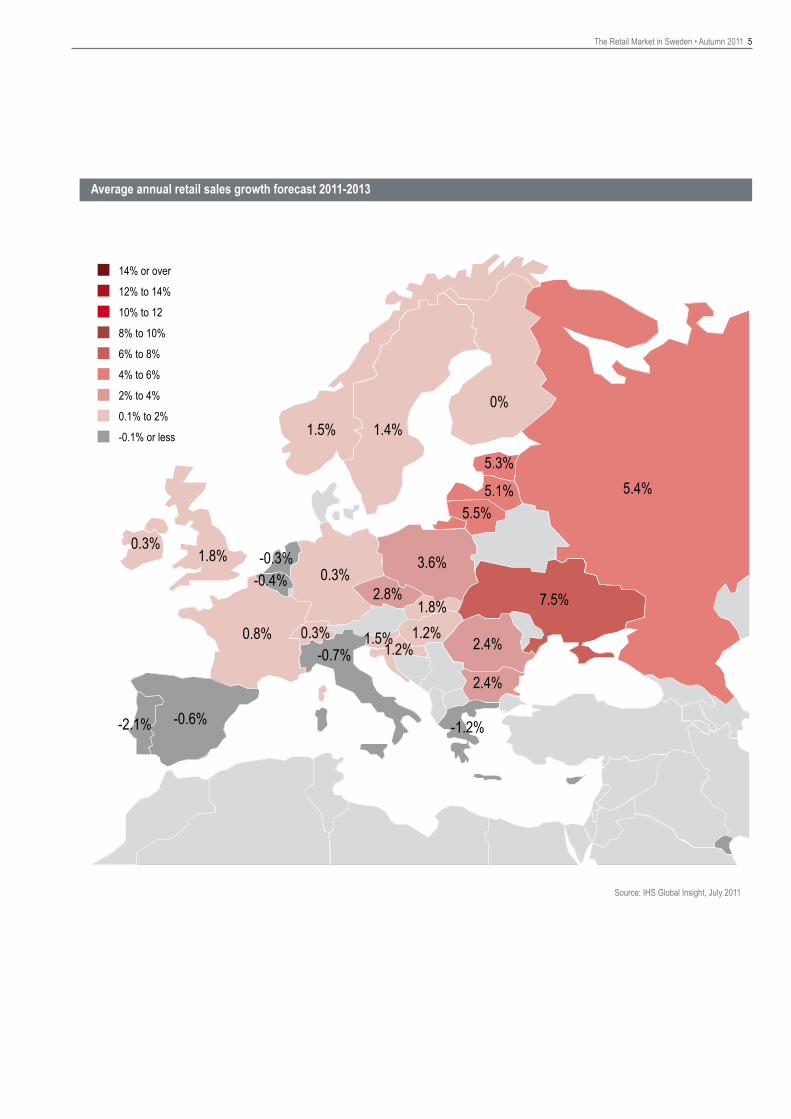

The Retail Market in Sweden • Autumn 2011 5

Source: IHS Global Insight, July 2011

Average annual retail sales growth forecast 2011-2013

14% or over

12% to 14%

10% to 12

8% to 10%

6% to 8%

4% to 6%

2% to 4%

0.1% to 2%

-0.1% or less

-2.1% -0.6%

0.8%

1.8%0.3%

1.5% 1.4%

0%

5.3%

5.1%5.5%

3.6%

1.8%2.8%

0.3%-0.7%

1.2%

7.5%

2.4%

2.4%

-1.2%

5.4%

0.3%-0.3%

-0.4%

1.5%1.2%

6 The Retail Market in Sweden • Autumn 2011

Population growthDuring the past twenty years Sweden’s population growth has increased by around 0.4% per annum. The last 5 years have witnessed an even higher average annual growth rate of around 0.7%. Immigration as well as a higher fertility and a lower mortality rate have contributed to the increase. Sweden’s largest urban areas are growing the fastest for these reasons, but also due to urbanisati-on. Sweden’s population is forecast to continue increasing and is expected to reach 10 million by 2021. The highest growth will be in the larger cities, as the following table shows:

In the period 2010 to 2020 the age structure of the population will not change significantly, but there is a trend that the 0-40 age group will gradually become a lower proportion of the whole population, while the 40+ age group will increase. For example in 2009, 49% of Sweden’s population were below 40 years old while 51% were over 40. By 2029, 47% of the population will be under 40 while 53% will be over 40 with the greatest increase being in the 80+ age group.Sweden’s age structure development is not unique and many Euro-pean countries are forecasting a similar trend. It will be important for retailers and retail property owners to recognise this trend and adapt their product and services to take advantage of it. Retailers will need to rise to the new wants generated by a retiring Baby Boomer popu-lation and a smaller, but very demanding, young adults (Generation Y) cohort and we explore this in greater detail in our Retail 2020 publication from 2010.

Increasing disposable income, private consumption and debtEven during the recession of 2008 and 2009, Swedes’ benefitted from growing disposable incomes due to lower taxes, lower loan costs and decreasing inflation. However increasing disposable incomes during this period, did not translate into as much growth in private consumption. This was due to the fact that the financial crisis made households more concerned about their economic future and they increased their savings rather than consumed more. The household savings ratio (savings as a proportion of disposable income) reached around 13% in 2009 – the highest for many years.

However, as economic conditions and households’ view on their economic future improved, the household savings ratio reduced to the current rate of just over 10% with private consumption regaining ground again.

Following the trend of previous years, disposable income is forecast to continue increasing at a stable pace, with an increase in real terms of 2.1% in 2011 and 2.6% in 2012, as economic growth continues and the government retains an expansive economic policy. It remains to be seen whether the continued volatility in the world’s financial markets will force a downward revision of these forecasts, but even if this is the case, it is likely that the figures for Sweden will still be seen as relatively strong compared to many other European countries, given the country’s current stronger economic fundamentals.

Over the past 10 years, private consumption in Sweden has gene-rally been above the European Union average, and was significantly above average in 2007, 2010 and 2011. Private consumption was recorded at -0.4% in 2009 and then grew by 3.4% in 2010.

While the outlook for both disposable income and private con-sumption is positive, it is also worth bearing in mind that Swedish households’ total debt as a percentage of disposable income is around 150%, a significant increase since 2000 when it was 100%. The current rate is also relatively high in a European perspective. The figure for Germany for example is 100%, and has remai-ned at approximately this level for the past decade. If Swedish households decide to discontinue the trend of increasing their debt as a percentage of disposable income, the effect upon consumpti-on will be negative.

County/Region

Population 2010

Population 2020

Average increase per

annum, 2010 - 2020

Stockholm 2,050,000 2,320,000 +1.3%Gothenburg 930,000 1,010,000 +0.8%Skåne, Malmö 1,230,000 1,360,000 +1.0%

Demand

Retail sales growth in EU 2005=100

100

110

90

120

130

140

150

Denm

ark

Hung

ary

Portu

gal

Italy

Latvi

aLit

huan

iaGe

rman

y Ne

therla

nds

Euro

zone

Irelan

dAu

stria

EU 27

Slov

akia

Belgi

umEs

tonia

Slov

enia

Swed

enUn

ited K

ingdo

mFr

ance

Finlan

dCz

ech R

epub

licNo

rway

Bulga

rian

Polan

dRo

mania

%

Source: HUI. Index, July 2011. 2005 = 100

The Retail Market in Sweden • Autumn 2011 7

Retail sales in Sweden

The relationship between retail turnover growth and disposable income growth in Sweden is shown on the graph below. Retail turnover growth increased significantly more than disposable income growth in the period 2002 to 2006 and this was due to the fact that people borrowed more. In 2008 and 2009 retail turnover growth was lower than disposable income growth as households were more worried about their future due to the financial crisis and saved more.

Retail sales in SwedenRetail sales per capita in Sweden are well above the European Union average and for the period 2011 to 2013, average retail sales in Sweden are forecast to outperform most other West European countries, which will continue a trend witnessed for many years.

Swedish retail sales have seen consistent growth over the past 14 years according to HUI (Swedish Retail Institute). During 2010, retail sales increased by 3.7% in current prices. Sales of non-daily goods increased by 5%, while sales of daily goods increased by 2.1%. In 2011, it is forecast that total retail sales, will increase by 1.5% of which non-daily goods will be 1.5% and daily goods will be 1.0%. This will be the weakest growth since 1996 and has been caused by falling consumer confidence due to the debt crisis in various European countries and weaker growth in the USA. In 2011, within the non-daily goods sector, sales in the home building & renovation supplies and clothes sectors are forecast to perform the best where-as electronic goods sales are forecast to perform worst. Positively, the base rate is forecast to increase at a slower pace than previously indicated by the Central Bank and the household savings rate is relatively high. This means there is the opportunity for households to spend more. A recovery in Europe next year is likely to have a posi-tive effect on Swedish retail sales during 2012, although the pace of economic growth in Europe is currently very uncertain.

Daily goods sales tend to be less volatile than non-daily goods sales but perform less well than non-daily goods during economic booms.

Consumer confidenceSwedish households were pessimistic in 2008 at the time of the financial crisis, but confidence quickly returned in 2009 and 2010 as economic conditions improved. Consumer confidence reached a peak in February 2011 according to NIER. However during recent months, consumer confidence has fallen to just below average. Nevertheless, consumer confidence in Sweden is still better than the EU and the USA.

Where do we shop?In a recent study by retail trade publication, ‘Market’, it was noted that generally, town centres and local suburban residential areas are taking a smaller share of retail sales while out of town retail and internet shopping are taking an increasing share of retail sales. For example, in 2006, 2.5% of Sweden’s total retail sales were from internet shopping while in 2009, it was 4.4%. According to HUI approximately 80% of future income and consumption will be in Sweden’s 10 largest regions and around 70% in the three largest.

Source: NIER, September 2011

Source: SCB

Consumer confidence in Sweden

Retail turnover growth vs. disposable income growth

Source: HUI & NIER

-10

-6

-2

2

6

10

Total retail salesNon daily goodsDaily goods

19921993199419951996199719981999200020012002200320042005200620072008200920102011F2012F

%

-40-30-20-10

0

10203040

2011

2010

2009

2008

2007

2006

2005

2004

2003

2002

2001

2000

1999

1998

1997

1996

1995

1994

1993

Consumer Confidence Index (CCI) Average 1993-2011 (M9)

-3

-1

1

3

5

7

9

11

Disposable income growth (%) Retail turnover growth (%)

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

%

8 The Retail Market in Sweden • Autumn 2011

Shopping Centres in SwedenSweden was one of the pioneering countries for shopping centres in Europe and has had enclosed centres similar in format to those today since the 1950’s. Shopping centres are in city centres, subur-ban areas and are increasingly out of town. The amount of shopping centre floor space per capita is above the European average due to less developed high street and retail warehouse provision.

Shopping Centre pipelineThe pace of new shopping centre development is slowing. In 2008, 2009 and 2010, the total area of newly constructed shopping centres or extensions was well in excess of 100,000 sq m each year. How-ever during 2011, we expect less will be completed. Completions in 2012 will also be less than in the latter years of the 2000s.

The most significant new shopping centre opening in 2010 was the 25,000 sq m Bromma Blocks Hangar 3 in the Bromma area of Stock-holm developed by KF Fastigheter. This centre also won Shopping Centre of the Year at Sweden’s Retail Awards. There were a number of significant extensions to existing shopping centres that opened in 2010, including 16,000 sq m at ‘design focussed’ Sollentuna Centrum (Steen & Ström) and 13,000 sq m at Åkersberga Centrum (Citycon), both in the Stockholm area. In June 2011, Sollentuna Centrum won the category for ‘Refurbishments & Expansions’ in the International Council of Shopping Centres (ICSC) Shopping Centre Awards. One of the most significant extensions outside Stockholm was 18,000 sq m at Hageby Centrum (Steen & Ström) on the outskirts of Norrköping.

2011 has been characterised by extensions to existing shopping cen-tres. The most significant are the 11,000 sq m extension to Diligentia’s regional shopping centre, Frölunda Torg in the Gothenburg region and the 18,000 sq m extension to Eurocommercial Properties’ Grand Sa-markand shopping centre on the outskirts of Växjö in south Sweden.

In the period 2011 to 2014, the shopping centre pipeline for Sweden’s 3 major cities is relatively low with a forecast increase of +4% for Stockholm and +11% for Gothenburg. In contrast, it is forecast that the Skåne region will have much higher growth at around +34%.This is mainly due to the opening of the Emporia shopping centre on the southern outskirts of Malmö which is currently being developed by Steen & Ström. Emporia will have over 200 shops and restaurants and is due to open in late 2012. Another significant project is Unibail Rodamco’s 25,000 sq m extension and total refurbishment of its regional shopping centre Täby Centrum, in north Stockholm. The ex-tension and refurbishment will be opened in phases between 2011 and 2015. The 90,000 sq m Mall of Scandinavia is a highly debated shop-ping centre being developed by Unibail Rodamco for Arenastaden (Eng: Arena Town) Solna in Stockholm. Its opening date has been delayed but latest information is that it is due to open in 2015.

Sweden has no national laws that regulate the development of shopping centres and retail parks. The Swedish municipalities have authority over such decisions, in contrast to Norway and Denmark, which are heavily regulated by national authorities. The total planned extension and new construction of retail accommoda-tion in Sweden up until the end of 2012 will not be exceptional in a European perspective. The highest level of new supply can mainly be seen in Eastern Europe including Russia, Turkey, Ukraine and Poland, where the existing stock and stock per capita has histori-cally been low. Sweden, which is a mature and stable market with amongst the highest shopping centre space per capita, will have a considerably lower stock increase.

Supply

Shopping centre stock & pipeline in Sweden

Source: Jones Lang LaSalle

Shopping centre stock & pipeline in Europe

Source: Jones Lang LaSalle

0 2000 4000 6000 8000 10000 12000 14000 16000 18000 20000UK

FranceItaly

GermanySpain

RussiaNetherlands

PolandTurkey

SwedenUkraine

PortugalCzech Republic

IrelandFinland

RomaniaHungarySlovakiaBelgiumGreece

LithuaniaBulgariaEstonia

Latvia Luxembourg Existing stock

Pipeline 2011-2012

Area ’000 sq m

0 200 400 600 800 1000 1200 1400 1600 1800 2000

Pipeline 2011-2014

Existing stockGothenburg

Skåne

Stockholm

+11%

+34%

+4%

Area ’000 sq m

The Retail Market in Sweden • Autumn 2011 9

Retail warehouse parks in SwedenRetail warehouse parks are a relatively new phenomenon in Sweden, but have expanded rapidly over recent years, both on greenfield sites or through the redevelopment of former warehouse / light industrial areas. The largest retail parks are Kungens Kurva and Barkarby in the Stockholm area.

The largest retail parks are often anchored by an IKEA store. IKEA has recently started a new concept where they open a shopping centre which adjoins their store. IKEA realises that its stores attract a large number of customers and there will be positive synergy effects if a shopping centre is developed next to it too. The recently opened IKEA store and adjoining two storey shopping centre in the Erikslund area of Västerås together total 80,000 sq m and is an example of this strategy.

Emporia, Malmö Grand Samarkand, Växjö

Sollentuna Centrum, Stockholm Bromma Blocks, Hangar 3, Stockholm

Source: Steen & Ström Source: Eurocommercial Properties

Source: Steen & Ström Photographer: Christer Carlsson

10 The Retail Market in Sweden • Autumn 2011

Other significant recent or ongoing new retail warehouse develop-ments are in the Boländerna area of Uppsala, Port 73 in Haninge, Stockholm and the expansion of Väla retail area near Helsingborg. Retail warehouse parks are continuing to expand, albeit at a slower rate than in the mid to late 2000s. Retail warehousing in the Stock-holm and Gothenburg regions is forecast to expand at a faster rate than in the Malmö region. This is partly because retail warehousing has developed rapidly over recent years in this region and also be-cause the rate of shopping centre development in the Malmö region is forecast to be greater than both Stockholm and Gothenburg.

Retail property ownersSwedish institutions and property companies dominate retail property ownership in Stockholm, Gothenburg and Malmö city centres. Vasakronan is the largest landlord and other significant owners include Hufvudstaden and AMF Fastigheter. Wallenstam is the largest retail landlord in Gothenburg city centre. The ownership of external shopping centres and retail warehouse parks is more varied, with a greater proportion of international owners. Large international retail property owners in Sweden include Unibail-Rodamco (France), Steen & Ström (France) and Eurocommercial Properties (Netherlands.)

Retail property will evolveIn order to retain and develop its value, retail property stock needs to evolve to reflect current lifestyles, socio-economic conditions and the increasing competition. These issues are explored in depth in our publication from September 2011 called, The New Retail Rulebook: 5 Key lessons from the Future.

The statistics outlined earlier show that both out of town retail as well as shopping centres will continue to grow in Sweden. In order to handle the increased competition and continue to be successful, shopping centres and retail parks will need to not only attract well known retailers, but will also need to differentiate themselves from the competition by providing some of the following: more leisure and entertainment, a more attractive shopping environment, unique retail tenants, better marketing and improved convenience. In order to be successful, local suburban shopping centres will need to focus on providing a more attractive, personal and time saving environment where the local population are able to efficiently shop, carry out errands and socialise. While every town centre has a unique atmos-phere, the success of town centre retail will need to be assisted by more convenient parking, public transport as well as further

improvement of the town centre environment to compete with the increasing number of out of town retail and shopping centres.

As online sales continue to grow and take an increasing share in retail sales, retailers will need to adapt their physical stores to become show rooms as well as traditional retail units. Social media will become increasingly important in order for retail areas to more successfully brand themselves and understand customers opinions and trends.

Designing shopping centres for successAs stated previously, successful shopping centres need to function well, have good parking facilities and a strong tenant mix. In the design of a shopping centre it is important to maximise pedestrian flow, by eliminating as much friction as possible and driving a large customer flow of the right quality throughout the centre.

A key aim in developing shopping centres is to create as many A locations as possible and minimise the number of B and C loca-tions. All shopping centres need anchors to create a good customer flow. Tenant clusters i.e. retailers within similar sectors can also be considered as anchors. A well-designed centre needs less anchors which means the shopping centre is able to generate a higher total rental income. A centre with destinations creates stronger competi-tion benefits but also higher rental income, with the parts together, creating a higher value than each part separately.

It is also important that shopping centre information and branding is visible. A strong, unique mix of international retailers, strong anchors and a generally dynamic centre will generate customer flow, new interesting tenants, high rents and leave competitors behind.It is also useful to consider the following shopping centre trends when designing / re-designing shopping centres with the aim of being up to date and successful:

From: To:

Single use Mixed useSingle purpose Multi purposeInside OutsideDemographic PsychographicsOne size fits all LifestyleFormulaic segmentation Hybrid colossusStandard case revenue Miscellaneous revenueStand alones Parasitic uses

The Retail Market in Sweden • Autumn 2011 11

Grand Samarkand, Växjö Source: Eurocommercial Properties

Internal view within a modern shopping centre

12 The Retail Market in Sweden • Autumn 2011

Chains dominateThe Swedish retail market is mature and is dominated by a rela-tively small number of large chains. This is especially true for the volume dependent retailers of clothing, furniture and food, where it is common for several different chains to have the same owner. The daily goods market is dominated by the major chains of ICA, Coop and Axfood.

Swedish H&M is Europe’s largest fashion chain with some 2,200 shops in 40 markets and IKEA the home furniture and furnishings retailer has some 320 stores in 35 countries. The success of IKEA and H&M illustrates that the Swedish retail market is mature and innovative and can compete well in the international market.

Retail Sector TrendsThe sport and leisure retail sector in Sweden is changing. With the recent arrival of XXL from Norway & Decathlon from France arriving in 2012, this market is becoming more competitive and both these retailers focus on low prices and a wide variety of stock. Existing Swedish sports chains like Stadium and Intersport are being forced to change their format in an attempt to compete successfully. Both Stadium & Intersport are opening shops in a larger format which will offer cheaper prices. Intersport has opened a new chain, Budget-sport, which is expected to establish 15 shops within 5 years. We expect the development of the sports and leisure retail sector to be similar to the way that home electronics sector has developed in Sweden over the last few years with new, strong and expansive entrants like German Media Markt creating intense competition, meagre profits and some casualties. For example in July 2011 home electronics chain OnOff with 67 stores in Sweden went bankrupt.

The retail market in Sweden is open to foreign operators and is largely unregulated. However foreign and private companies are prevented from selling alcoholic beverages due to the state mono-poly Systembolaget which sells these products. The pharmaceutical market was deregulated in 2009 and since then more pharmacies have opened and a number of new players, both domestic and in-ternational, like Alliance Boots and Celesio owned Doc Morris, have entered this market.

New international retailersSweden has traditionally been dominated by domestic brands, how-ever in recent years dynamic new brands have entered the market.

There have been a number of new international retailers opening shops in the Swedish market in 2010 and 2011 including the Spanish fashion retailer, Desigual which opened its first Swedish store in Spring 2010 and has opened several stores since then. US fashion chain Hollister opened its first Swedish store in Täby Centrum, Stockholm in Summer 2011 and this will be followed by a further store in Gallerian, Stockholm city centre during Autumn 2011. UK restaurant chain Wagamama, serving Japanese and Asian style food opened their first Swedish restaurant in Autumn 2010 in central Stockholm and are looking for more units in Sweden’s largest cities. There is also increasing interest from a number of new international luxury retail brands.

Retailers

Biblioteksgatan, Stockholm

The Retail Market in Sweden • Autumn 2011 13

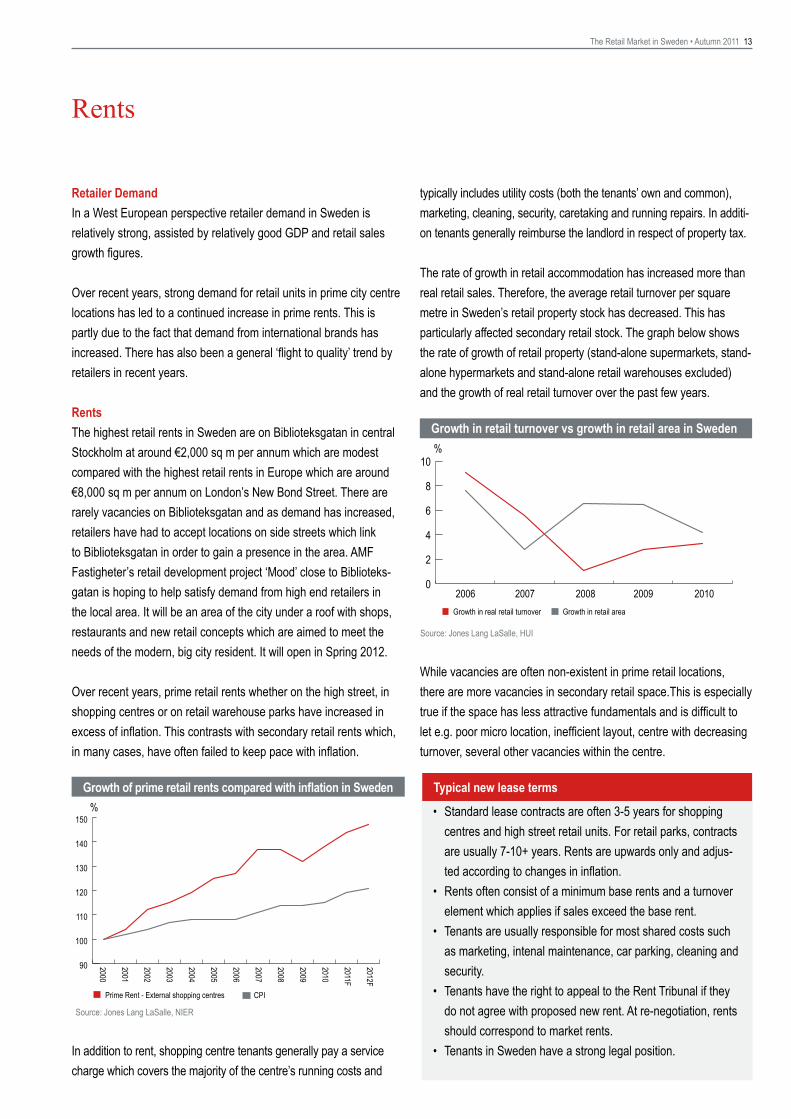

Rents

Retailer DemandIn a West European perspective retailer demand in Sweden is relatively strong, assisted by relatively good GDP and retail sales growth figures.

Over recent years, strong demand for retail units in prime city centre locations has led to a continued increase in prime rents. This is partly due to the fact that demand from international brands has increased. There has also been a general ‘flight to quality’ trend by retailers in recent years.

RentsThe highest retail rents in Sweden are on Biblioteksgatan in central Stockholm at around €2,000 sq m per annum which are modest compared with the highest retail rents in Europe which are around €8,000 sq m per annum on London’s New Bond Street. There are rarely vacancies on Biblioteksgatan and as demand has increased, retailers have had to accept locations on side streets which link to Biblioteksgatan in order to gain a presence in the area. AMF Fastigheter’s retail development project ‘Mood’ close to Biblioteks-gatan is hoping to help satisfy demand from high end retailers in the local area. It will be an area of the city under a roof with shops, restaurants and new retail concepts which are aimed to meet the needs of the modern, big city resident. It will open in Spring 2012.

Over recent years, prime retail rents whether on the high street, in shopping centres or on retail warehouse parks have increased in excess of inflation. This contrasts with secondary retail rents which, in many cases, have often failed to keep pace with inflation.

In addition to rent, shopping centre tenants generally pay a service charge which covers the majority of the centre’s running costs and

typically includes utility costs (both the tenants’ own and common), marketing, cleaning, security, caretaking and running repairs. In additi-on tenants generally reimburse the landlord in respect of property tax.

The rate of growth in retail accommodation has increased more than real retail sales. Therefore, the average retail turnover per square metre in Sweden’s retail property stock has decreased. This has particularly affected secondary retail stock. The graph below shows the rate of growth of retail property (stand-alone supermarkets, stand-alone hypermarkets and stand-alone retail warehouses excluded) and the growth of real retail turnover over the past few years.

While vacancies are often non-existent in prime retail locations, there are more vacancies in secondary retail space.This is especially true if the space has less attractive fundamentals and is difficult to let e.g. poor micro location, inefficient layout, centre with decreasing turnover, several other vacancies within the centre.

• Standard lease contracts are often 3-5 years for shopping centres and high street retail units. For retail parks, contracts are usually 7-10+ years. Rents are upwards only and adjus-ted according to changes in inflation.

• Rents often consist of a minimum base rents and a turnover element which applies if sales exceed the base rent.

• Tenants are usually responsible for most shared costs such as marketing, intenal maintenance, car parking, cleaning and security.

• Tenants have the right to appeal to the Rent Tribunal if they do not agree with proposed new rent. At re-negotiation, rents should correspond to market rents.

• Tenants in Sweden have a strong legal position.

Typical new lease terms Growth of prime retail rents compared with inflation in Sweden

Source: Jones Lang LaSalle, NIER

90

100

110

120

130

140

150

Prime Rent - External shopping centres CPI

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011F

2012F

%

0

2

4

6

8

10

Growth in real retail turnover Growth in retail area

%

2006 2007 2008 2009 2010

Growth in retail turnover vs growth in retail area in Sweden

Source: Jones Lang LaSalle, HUI

14 The Retail Market in Sweden • Autumn 2011

Global

France / Holland

Denmark

UK

Sweden

Global

France/ Holland

Denmark

UK

Sweden

7%18%

28%

9%

38%

Increased volumesSince the recession of 2009 retail property investment transaction volumes have increased significantly as the graph below shows. The retail property transaction volume increased from around SEK 1.10 billion in the first half of 2009 to SEK 3.22 billion for the first half of 2010 and then SEK 8.537 billion for the first half of 2011.

Investor demand has been driven by strong GDP and consumption growth and the increased availability of debt finance (especially for prime stock) over the last couple of years. However, demand is weaker for secondary / tertiary retail property investments. Shopping centres accounted for around 79% of retail transactions in H1 2011 whilst retail warehouses accounted for 15%.

The largest retail property transaction in 2011 to date has been Unibail Rodamco’s sale of a portfolio of shopping centres mainly in the Stockholm area for SEK 2.4 billion to Grosvenor Bouwinvest REIM. The portfolio totalled 98,000 sq m and included Haninge Centrum, Bålsta Centrum, Väsby Centrum and an ICA Maxi in Helsingborg. Other large retail transactions included Boultbee’s sale of Punkt & Gallerian shopping centres with a combined area of 45,000 sq m in Västerås city centre to The Carlyle Group for SEK 850 million and Heron International’s sale of the shopping and entertainment centre, Heron City in the Kungens Kurva area of Stockholm. The sale price of this 46,000 sq m centre was SEK 825 million and NIAM was the purchaser.

Increase in foreign investor volumesIn H1 2011, 94% of retail property investment transactions involved either an international vendor or purchaser, which compares with 70% in 2010 and 30% in 2009. When comparing 2010 with H1 2011, the investment volume purchased by foreign investors has increa-sed significantly, from 36% to 74%. In 2009 the figure was 0%. The increase in volume by foreign investors has been driven by factors including Sweden’s relatively strong economic performance over the economic crisis and availability of high quality stock.

Unibail Rodamco was the largest vendor of retail property in H1 2011. Their recent property sales are in line with the company’s aim of focussing on owning only the largest shopping centres in the markets where they hold property.

Retail Investment Market

Vendors H1 2011

Purchasers H1 2011

Change in retail property transaction volumes 2005-H1 2011 in Sweden

Holland

USA

Global

Finland

Sweden

Holland

USA

Global

Finland

Sweden13%

26%

5%

46%

10%

0

5

10

15

20

25Shopping centres

Retail Warehousing

Supermarkets

Billion SEK

2006 2005 2007 2008 2009 2010 H1 2011

Source: Jones Lang LaSalle

Source: Jones Lang LaSalle

Source: Jones Lang LaSalle

The Retail Market in Sweden • Autumn 2011 15

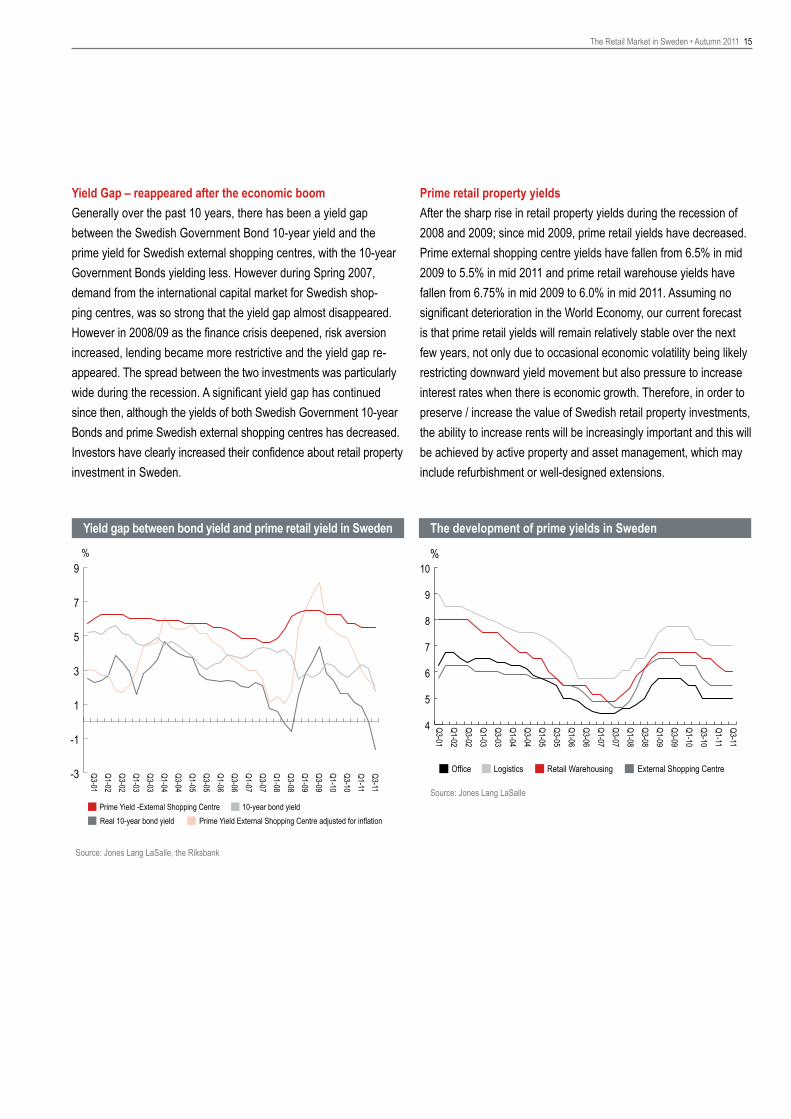

Yield Gap – reappeared after the economic boomGenerally over the past 10 years, there has been a yield gap between the Swedish Government Bond 10-year yield and the prime yield for Swedish external shopping centres, with the 10-year Government Bonds yielding less. However during Spring 2007, demand from the international capital market for Swedish shop-ping centres, was so strong that the yield gap almost disappeared. However in 2008/09 as the finance crisis deepened, risk aversion increased, lending became more restrictive and the yield gap re-appeared. The spread between the two investments was particularly wide during the recession. A significant yield gap has continued since then, although the yields of both Swedish Government 10-year Bonds and prime Swedish external shopping centres has decreased. Investors have clearly increased their confidence about retail property investment in Sweden.

Prime retail property yieldsAfter the sharp rise in retail property yields during the recession of 2008 and 2009; since mid 2009, prime retail yields have decreased. Prime external shopping centre yields have fallen from 6.5% in mid 2009 to 5.5% in mid 2011 and prime retail warehouse yields have fallen from 6.75% in mid 2009 to 6.0% in mid 2011. Assuming no significant deterioration in the World Economy, our current forecast is that prime retail yields will remain relatively stable over the next few years, not only due to occasional economic volatility being likely restricting downward yield movement but also pressure to increase interest rates when there is economic growth. Therefore, in order to preserve / increase the value of Swedish retail property investments, the ability to increase rents will be increasingly important and this will be achieved by active property and asset management, which may include refurbishment or well-designed extensions.

Yield gap between bond yield and prime retail yield in Sweden The development of prime yields in Sweden

Source: Jones Lang LaSalle, the Riksbank

4

5

6

7

8

9

10

Q3-11

Q1-11

Q3-10

Q1-10

Q3-09

Q1-09

Q3-08

Q1-08

Q3-07

Q1-07

Q3-06

Q1-06

Q3-05

Q1-05

Q3-04

Q1-04

Q3-03

Q1-03

Q3-02

Q1-02

Q3-01

%

Office Logistics Retail Warehousing External Shopping Centre

Source: Jones Lang LaSalle

-3

-1

1

3

5

7

Q3-11

Q1-11

Q3-10

Q1-10

Q3-09

Q1-09

Q3-08

Q1-08

Q3-07

Q1-07

Q3-06

Q1-06

Q3-05

Q1-05

Q3-04

Q1-04

Q3-03

Q1-03

Q3-02

Q1-02

Q3-01

Prime Yield -External Shopping Centre 10-year bond yield

Real 10-year bond yield Prime Yield External Shopping Centre adjusted for inflation

9%

© Copyright Jones Lang LaSalle 2011. This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

Contacts: Håkan PehrssonHead of Asset Management & RetailTel: +46 8 453 50 [email protected]

Antony PastiroffRetail Capital MarketsTel: +46 8 453 51 88 [email protected]

Fredrik TellefsenHead of Retail Development & LeasingTel: +46 8 453 51 [email protected]

Benjamin RushRetail Research Tel: +46 8 453 50 [email protected]

Jones Lang LaSalle offices: StockholmBox 1147SE-111 81 StockholmJakobsbergsgatan 22Tel: +46 8 453 50 00

GothenburgBox 1058SE-405 22 GöteborgLilla Bommen 6Tel: +46 31 708 53 00

www.joneslanglasalle.se