revenue & business activity q1 2014 - … · t1 q4 q2 residential 2,145 4,440 2,436 3,542 ......

TRANSCRIPT

29 APRIL 2014

REVENUE & BUSINESS ACTIVITY Q1 2014Q1 2014

PAGE 2

DISCLAIMER

The information contained in this document has not been independently verified. No representation, warranty orundertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy,completeness or correctness of the information or opinions contained herein. None of the Company, itsshareholders, its advisors or representatives nor any other person shall have any liability whatsoever for any lossarising from any use of this document or its contents or otherwise arising in connection with this document.

This document does not constitute an offer to sell or an invitation or solicitation of an offer to subscribe for orpurchase any securities, and this shall not form the basis for or be used for any such offer or invitation or othercontract or engagement in any jurisdiction.

The information, assumptions and estimates that were used to determine these objectives are subject tomodification due to economic, financial and competitive uncertainties. Furthermore, it is possible that some of therisks described in chapter 4 in the Document de Référence, filed with the AMF under number D.14-0304 on 8 April2014, could have an impact on the company’s ability to achieve these objectives. Accordingly, the Company cannotgive any assurance as to whether it will achieve the objectives described, and makes no commitment or undertakingto update or otherwise revise this information.

No assurance is given as to the fairness, accuracy, completeness or correctness of the information or opinionscontained in this document.

1HIGHLIGHTS

29 APRIL 2014

KEY MESSAGES Q1 2014

� Q1 2014 Business activity:

�New home reservations in France up 5% in volume, +8% yoy in value

�Commercial order intake not significant over Q1, annual €100 million target confirmed

�Group backlog at the end of March over €3.3 billion equal to backlog at year-end 2013 (18 months’revenue from development activities)

� Q1 2014 consolidated revenue in line with Group expectations at €505 million

� Full-year 2014 Outlook and Guidance confirmed

� External growth: Oralia acquisition announced in December 2013 and finalised on 1 April 2014; PERL acquisition announced on 17 March, expected to finalise by the end of 1st half 2014 if approved by French Competition Authority

� Private placement of a €171million bond issue in two tranches of 6 and 7 years, at fixed coupons of 3.25% and 3.52% respectively, announced in a separate release today*

PAGE 4*Not for publication, distribution or release, directly or indirectly, in or into the USA, Australia, Canada or Japan

2Q1 2014 BUSINESS ACTIVITY

29 APRIL 2014

HOUSING SECTOR IN FRANCE: REGULATORY UPDATE

PAGE 6

MARKET SEGMENT

MAIN MEASURES

Landlords and investors

Caps on rents in areas with limited supply (28 metropolitan areas); maximum equal to the median reference rent for the home (by category and district), set by prefectural order (on the basis of data provided by a market monitoring centre) +20% at most for each new rental or new tenant

Gradual implementation of an optional Universal Rent Guarantee (financed by the public authorities)

Regulation of relations between landlords and tenants (limitation on required supporting documents, reduction of tenant’s notice to one month in areas characterised by limited supply, standard forms for leases and schedules of condition, etc.)

ALUR Act voted February 2014

Validated by the Constitutional Council, 20 March 2014

200 decrees pending

Real estate services to individuals

Limitation of letting expenses payable by the tenant (50% maximum, limits per sq.m)

Regulation of managing agents’ fees (limitation by decree of special expenses, all other services deemed as relating to day-to-day administration and included in the annual fee package), obligation to open a separate bank account for each condominium property with more than 15 units

All segments

Modernisation of urban development law: more systematic coordination of local urban planning schemes between municipalities (with 25% veto right granted to municipalities representing at least 20% of the affected population), clarification of the hierarchy of standards in urban planning documents, greater control of urban planning for commercial uses, local and regional ecological transitions, etc.

Intermediate housingOfficial status for intermediate housing. Potential extension to home-ownership. Creation of a new long-term leasehold, the “BRILO”

20/02/2014Ordinance

All segments“Objectif 500.000” strategic working group and the “choc de simplification” (streamlining of bureaucratic procedures) promised by François Hollande, with the official aim of lowering the cost of new collective housing construction by 10%

Ongoing

RESIDENTIAL

PAGE 7

BUILDING PERMITS

Source : Commissariat Général au Développement Durable- N° 513 April 2014

NUMBER OF NEW HOME BUILDING PERMITS GRANTED IN FRAN CE(in thousand units, 12 months rolling)

RESIDENTIAL

2013 2014

400408420433

502496495535

March

-20%

FevJanDecDec 2012

Dec 2011

March

PAGE 8

NEW HOME RESERVATION MARKET (DEVELOPERS)

DEVELOPERS’ NEW HOME RESERVATIONS IN FRANCE(in units)

20,000

40,000

80,000

100,000

60,000

120,000

0

2012

89,000

2011

105,000

2010

115,000

200520042003 2006

127,000

2007

79,000

2008

106,000

2009

~-1%

20142013

88,000

Average 2003/2013: 107,000

Source: Commissariat Général au Développement Durable, chiffres & statistiques n°496 for 2013

Number of reservations

RESIDENTIAL

PAGE 9

MORTGAGE RATES

MORTGAGE RATES (all markets, excl. insurance, last month of the quarter, average)

2,98%

Q1 14

3,00%

2,08%

2,56%

Q4 13Q3 13

3,08%2,89%

Q2 13Q1 13

3,07%

Q4 12

2,00%

Q3 12Q2 12Q1 12Q4 11

3,93%

Q4 10

3,27%

Q4 09Q4 08

5,07%

Q4 07

4,42%

Q4 06

3,88%

Q4 05

3,36%

Q4 04Q4 03

4,30%

4,08%

* Observatoire Crédit Logement **French OAT 10-year rate reported by Bloomberg; the last quotation date of the quarter

mortgage rates*

French government 10 year bond (OAT**)

RESIDENTIAL

NEXITY RESIDENTIAL IN FRANCE*:Q1 2014 RESERVATIONS

VOLUME(in units)

VALUE(in €m, incl.VAT)

491

370326

+5%

Q1 2014

2,141

1,815

Q1 2013

2,030

1,660

Q1 2012

2,348

1,857

Subdivisions

New homes318

353

37 2829

Q1 2014

+8%

382

Q1 2013

355

327

Q1 2012

355

PAGE 10

+8%+9%

RESIDENTIAL

*Excluding International business.(Including International business, new homes reserva tions +5% in volume, +6% in value)

3,581

Q4Q3

2,099

Q2

2,781

Q1

1,660

Q4

3,052

Q3

2,506

Q2

2,776

Q1

1,857

Q4

3,414

Q3

2,685

Q2

2,992

Q1

2,333

Q4

4,042

Q3

2,542

Q2

3,069

Q1

2,201

Q4

2,998

Q3

2,016

Q2

3,225

Q1

2,569

Q1

1,815

2009 2010 2011 2012 2013

PAGE 11

RESIDENTIAL

2014

NEW HOME RESERVATIONS BY QUARTER

NUMBER OF NEW HOME RESERVATIONS(France, in units)

PAGE 12

571

10,989

2014

1,154

2013

11,734

3,044

4,440

2,436

4,566

3,542

4,393

2012

2,422

1,894

2011

1,427

11,182

2,1453,025

NEXITY RESIDENTIAL: NEW HOME COMMERCIAL LAUNCHES(France, excluding Iselection, in units)

Q3

T1

Q4

Q2

RESIDENTIAL

2,145

4,440

2,436

3,542

1,894

4,5664,393

2,422 3,044

1,427

3,025

Q1X2

PAGE 13

Q1 13

1,660

48129%

1046%

51831%

55734%

Q1 12

1,857

31117%

925%

1,01054%

1,815

Q1 14

49827%

1448%

62735%

54630%

44424%

-2%

+21%

+38%

+4%

NEXITY RESIDENTIAL: KEY CLIENT SEGMENTS PERFORMANCENEW HOME RESERVATIONS BREAKDOWN BY CUSTOMER TYPE(excl. International, in units)

First-time buyers

Individual investors

Other home buyers

Professional landlords

RESIDENTIAL

Total individuals net reservations: +15% (Q1 14 / Q1 13)

+15%

PAGE 14

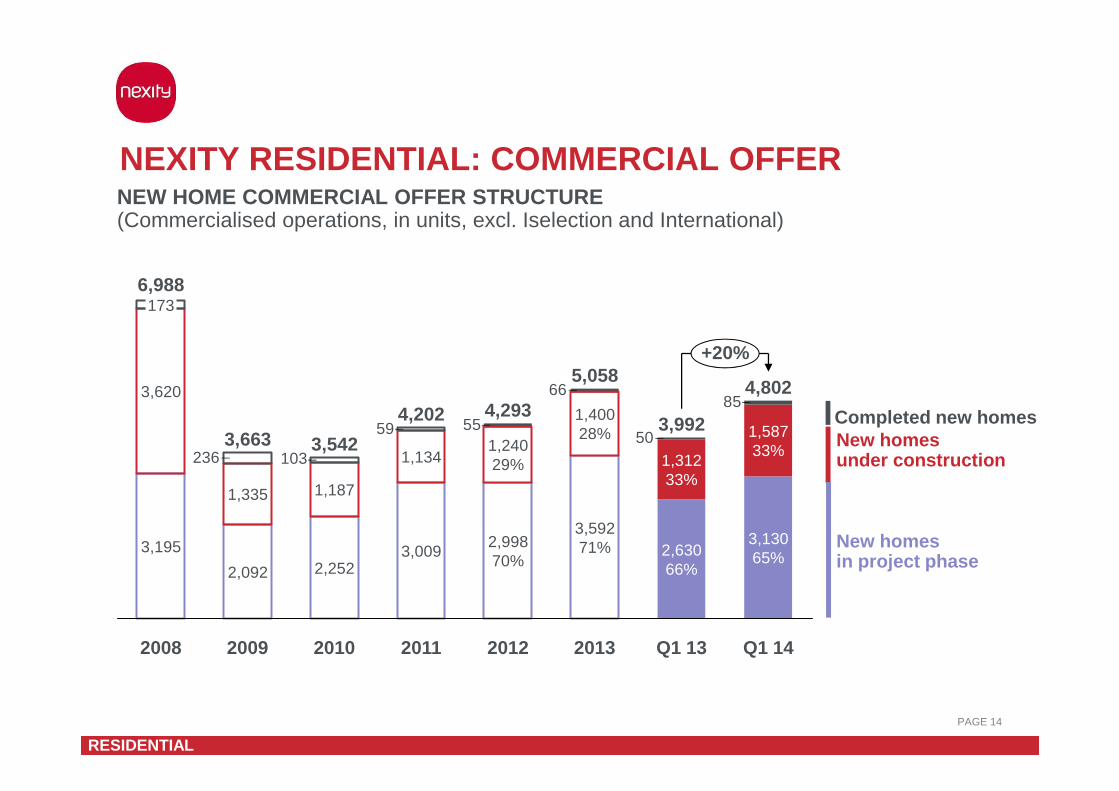

50

66

5559

103236

85

Q1 14

+20%

4,802

3,13065%

1,58733%

Q1 13

3,992

2,63066%

1,31233%

2013

5,058

3,59271%

1,40028%

2012

4,293

2,99870%

1,24029%

2011

4,202

3,009

1,134

2010

3,542

2,252

1,187

2009

3,663

2,092

1,335

2008

6,988

3,195

3,620

173

NEXITY RESIDENTIAL: COMMERCIAL OFFERNEW HOME COMMERCIAL OFFER STRUCTURE (Commercialised operations, in units, excl. Iselection and International)

New homesunder construction

Completed new homes

New homes in project phase

RESIDENTIAL

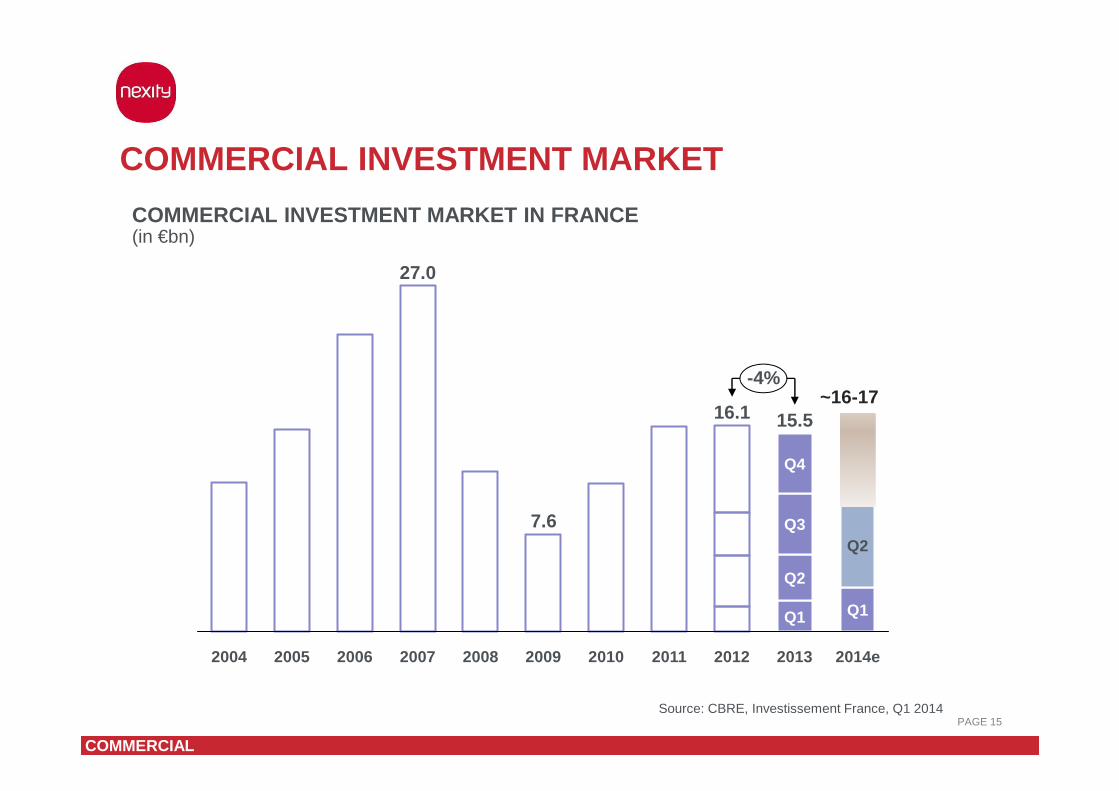

PAGE 15Source: CBRE, Investissement France, Q1 2014

COMMERCIAL INVESTMENT MARKET

COMMERCIAL INVESTMENT MARKET IN FRANCE(in €bn)

-4%

2014e

Q1

Q2

2013

15.5

Q1

Q2

Q3

Q4

2012

16.1

201120102009

7.6

20082007

27.0

200620052004

COMMERCIAL

~16-17

PAGE 16Source: CBRE, Bureaux Île-de-France Q1 2014

+16%

2.0

-25%

2014e

2.0

Q1 2014

0.5

2013

1.8

0.4

Q2

Q3

Q4

2012

2.4

1.9

2008

2.4

2007

2.7

2011

2.4

2010

2.1

2009

0.5

COMMERCIAL RENTAL MARKET

COMMERCIAL

TAKE-UP IN PARIS REGION (in millions of sq.m)

NEXITY COMMERCIAL: NEW ORDER INTAKE AND BACKLOG

PAGE 17

(in €m)

457486

31 March 14Additional works & other

adjustments

+24

2014 order intake

+2

Q1 2014 revenue

-55

31 Dec 13

-6%

COMMERCIAL

� Order intake in Q1 2014 not significant

� Confirmation of the 2014 objective: Order intake to r each €100m

31 Dec 13 31 March 14 1 April 14

PAGE 18

792

64481%

-1.7%

14919%

804

14819%

65581%

11.312.0

31 March 1431 Dec 13

NEXITY SERVICES: BUSINESS ACTIVITY - Q1 2014

REAL ESTATE SERVICES TO INDIVIDUALS(in thousands of units)

Rentalmanagement

Condominiummanagement

REAL ESTATE SERVICES TO COMPANIES(in millions of sq.m)

SERVICES AND DISTRIBUTION NETWORKS

*Oralia acquisition completed on 1 April 2014

79231

134 Oralia*

957

PAGE 19

Asnières120,000 sq.m

St-Priest146,800 sq.m

Marseille Docks Libres30,000 sq.m

Ermont Eaubonne21,400 sq.m

St-Ouen187,300 sq.m

Île-de-France

Lyon

Marseille

� ~615,100 sq.m in portfolio at the end of March 2014� Acquisition of a first plot of land in Montreuil, p art of a large scale development

programme (Acacias)

Montreuil

63,350 sq.m

URBAN REGENERATION: VILLES & PROJETS

URBAN REGENERATION

• Acquisition of a first plot of 14,000 sq.m for a large-scale mixed development project on the immediate outskirts of Paris

• Creation of a new city neighbourhood offering substantial social and functional diversity

• High environmental quality: passive buildings, optimised rainwater management

• Eventually a total floor space of: 104,500* sq.m including 81,200 sq.m of housing:

• 1,200 residential units;

• 13,000 sq.m of business and retail premises;• Public facilities: 1 school, 1 stadium, shared car parks

• Initial delivery date: end of 2017

Acacias, Montreuil (Seine-Saint-Denis, Paris Region)

PAGE 20

URBAN REGENERATION

URBAN REGENERATION: VILLES & PROJETS

* Including the 63,350 sq.m booked in the Nexity portfolio

3Q1 2014 REVENUE

29 APRIL 2014

Q1 2014 REVENUE

PAGE 22

341364

55114

107

1072

1

Other activities

+1

Q1 2013

-23

Services & Distribution Networks

-1

Commercial

-59

Residential

505

Q1 2014

587

-14.0 % *

Residential

Commercial

Services & Distribution Networks

(in €m)

* If co-development activities were not proportionately consolidated, the Group’s first quarter 2014 revenue would decrease by 15% vs Q1 2013. Please refer to page 4 of the English version of the press release.

-14.0%

BACKLOG

PAGE 23

556390

709 383457486

3,340

March 14

2,8832,869

3,355

Dec 13Dec 12

3,098

2,715

Dec 11

3,324

2,615

Dec 10

2,751

2,361

Dec 09

2,633

2,077

Commercial

Residential

(in €m, excl. VAT and incl. Iselection and International) 18 MONTHS’ DEVELOPMENT ACTIVITY

As a reminder, the Group’s backlog at the end of Marc h 2013 was €2.995 billion, the equivalent of 15 months of Nexity’s development act ivity

DIVIDEND

PAGE 24

2013 2014*

2.02.0

2012

2.0

2011 (Sept)

4.0

2011(May)

2.0

2010

1.6

2009

1.5

2008

2.0

2007

1.9

2006

1.6

2005

1.0

Exceptional

Paid:

Dividend of €2 per share to be proposed to the Shar eholders’ Meetingto be held on 20 May 2014

* Subject to the approval of the Shareholders’ Meeting

DIVIDEND PER SHARE(in € per share)

2014 OUTLOOK*

� Residential: level of activity at approximately 10,000 reservations, in line with 2013 in a new home market expected to remain stable in 2014, not to pick up before 2015

� Commercial: order intake to reach a low of around €100 million

� Consolidated revenue for 2014 expected to exceed €2.5 billion**

� Current operating profit target for 2014 of at least €170 million

� Confirmed proposal to distribute a dividend of €2 per share in respect of 2013. The Company is considering proposing to shareholders next year to renew the same dividend

PAGE 25

* Indicators measured using accounting methods comparable with 2013, without neutralising the share of revenue or profit earned by the Group in co-development activities. These targets take into account the consolidation of Oralia as of 1 April 2014, but do not include the impact of the potential acquisition of PERL, which remains subject to consent from the French CompetitionAuthority

** Reminder: 2013 consolidated revenue = €2.737 billion