revenue regulation 16-2008 as amended by revenue...

TRANSCRIPT

Revenue Regulation 16-2008 as amended by

Revenue Regulation 2-2010

1. Individuals:

i. Resident Citizen

ii. Non-resident Citizens

iii. Resident Alien

iv. Taxable estates and trusts

1. Corporation:

i. Domestic Corporation

ii. Resident foreign corporation

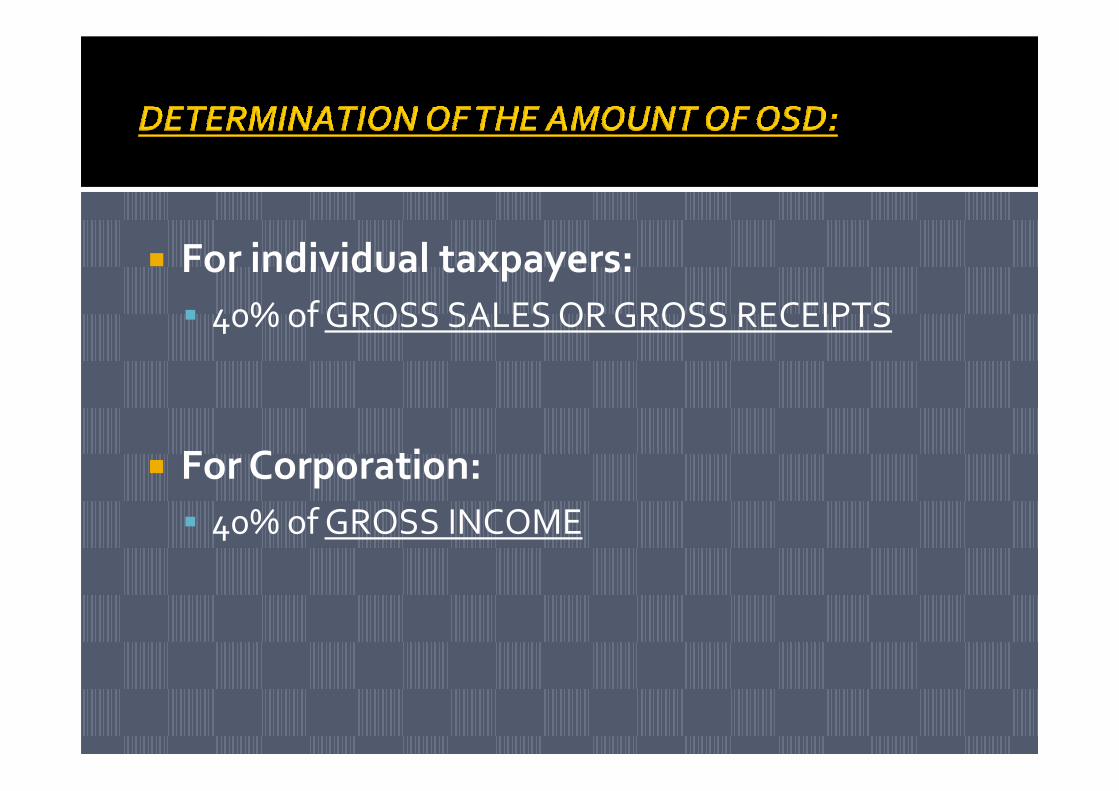

� For individual taxpayers:

� 40% of GROSS SALES OR GROSS RECEIPTS

� For Corporation:

� 40% of GROSS INCOME

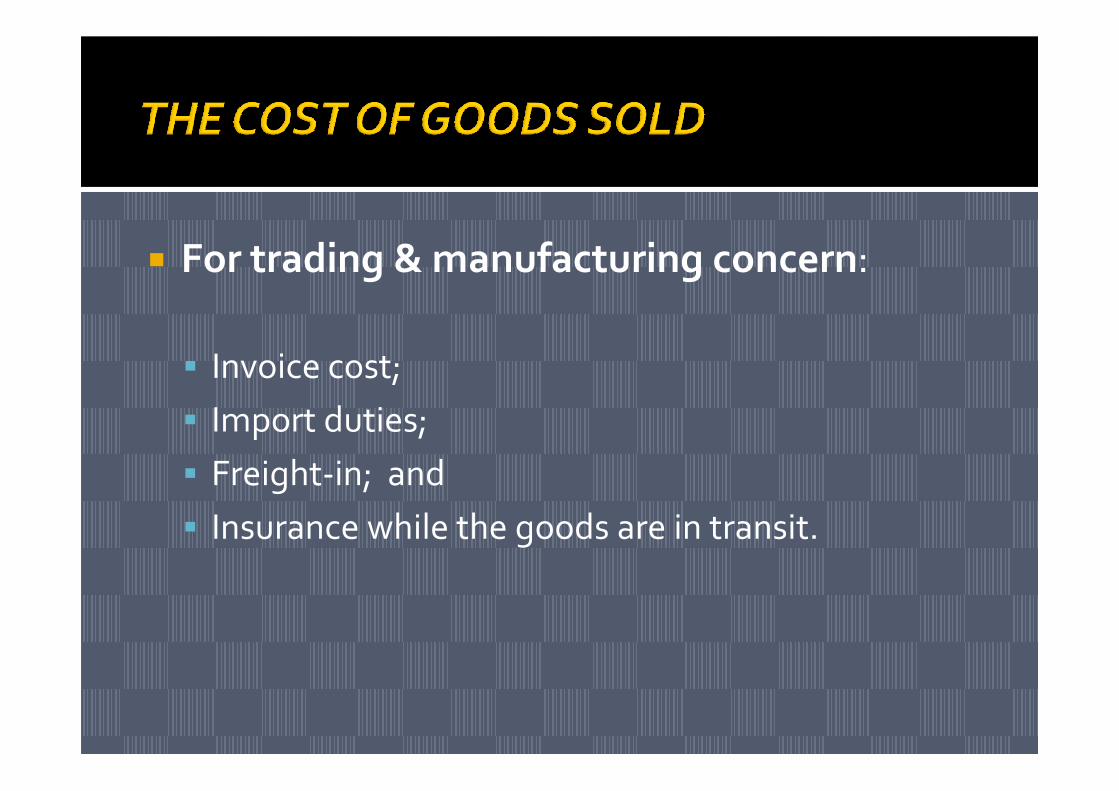

� For trading & manufacturing concern:

� Invoice cost;

� Import duties;

� Freight-in; and

� Insurance while the goods are in transit.

� For manufacturing concern:

� Raw materials used;

� Direct labor;

� Manufacturing overhead;

� Freight cost;

� Insurance; and

� Other costs.

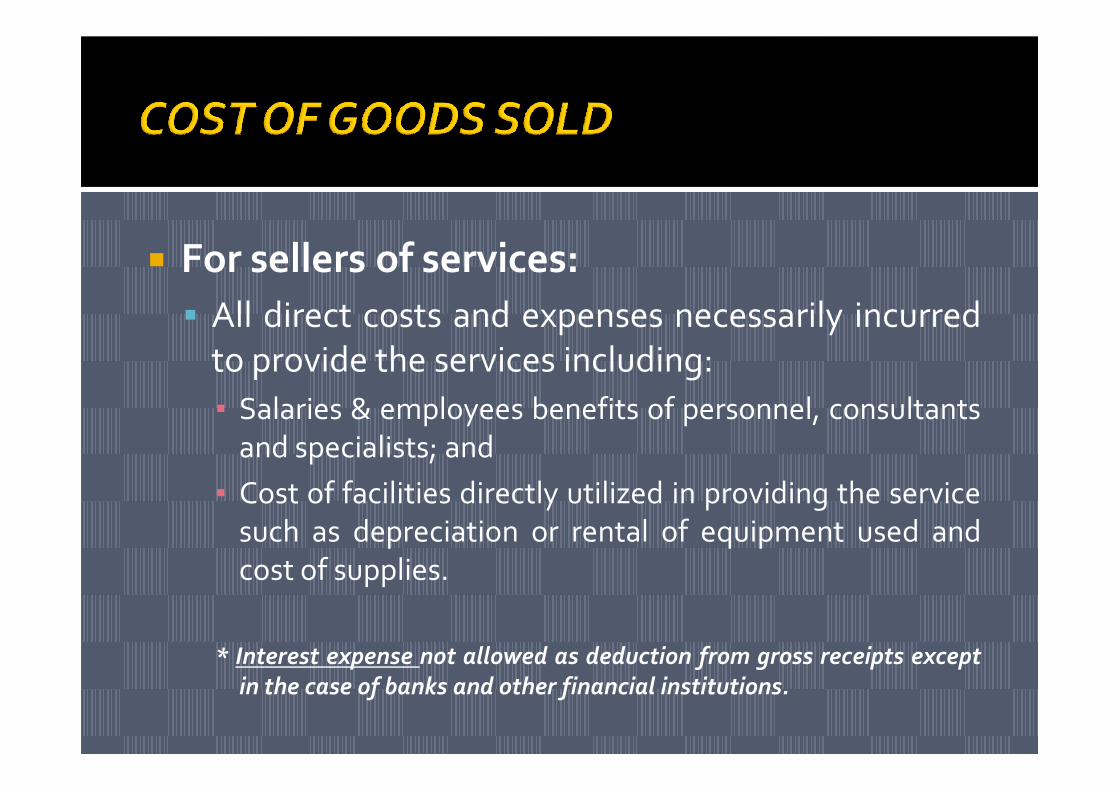

� For sellers of services:

� All direct costs and expenses necessarily incurred

to provide the services including:

▪ Salaries & employees benefits of personnel, consultants▪ Salaries & employees benefits of personnel, consultants

and specialists; and

▪ Cost of facilities directly utilized in providing the service

such as depreciation or rental of equipment used and

cost of supplies.

* Interest expense not allowed as deduction from gross receipts except

in the case of banks and other financial institutions.

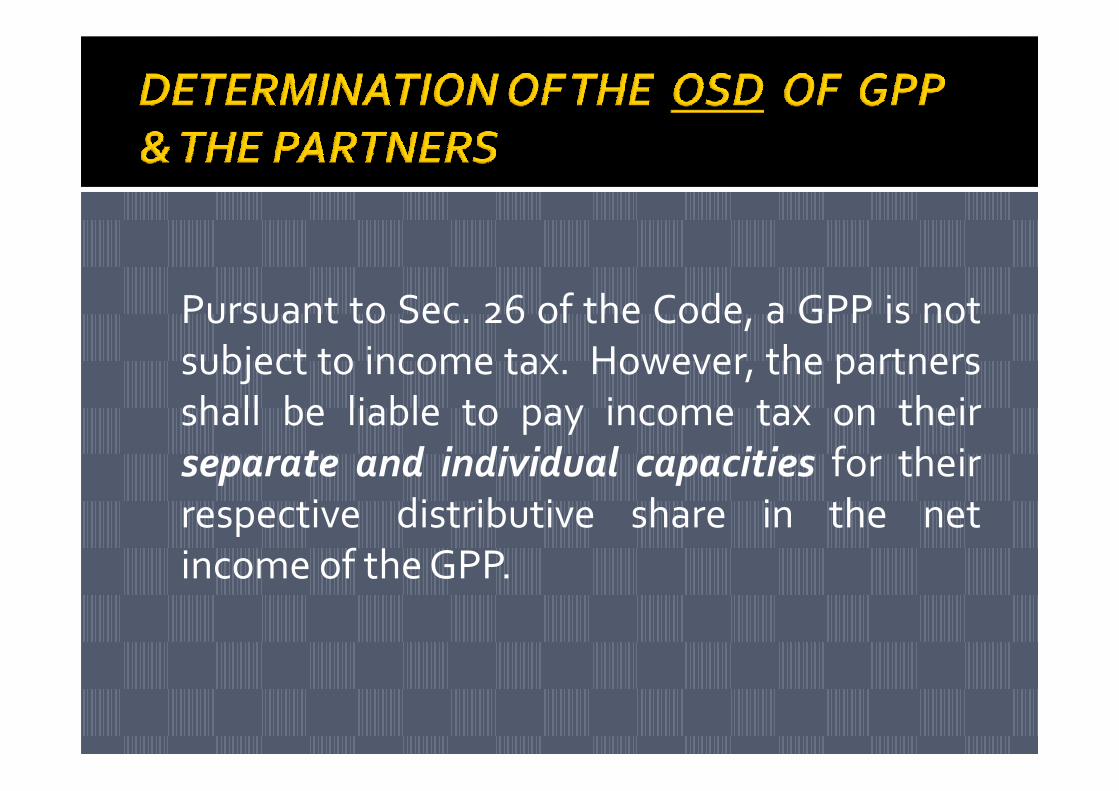

Pursuant to Sec. 26 of the Code, a GPP is not

subject to income tax. However, the partners

shall be liable to pay income tax on theirshall be liable to pay income tax on their

separate and individual capacities for their

respective distributive share in the net

income of the GPP.

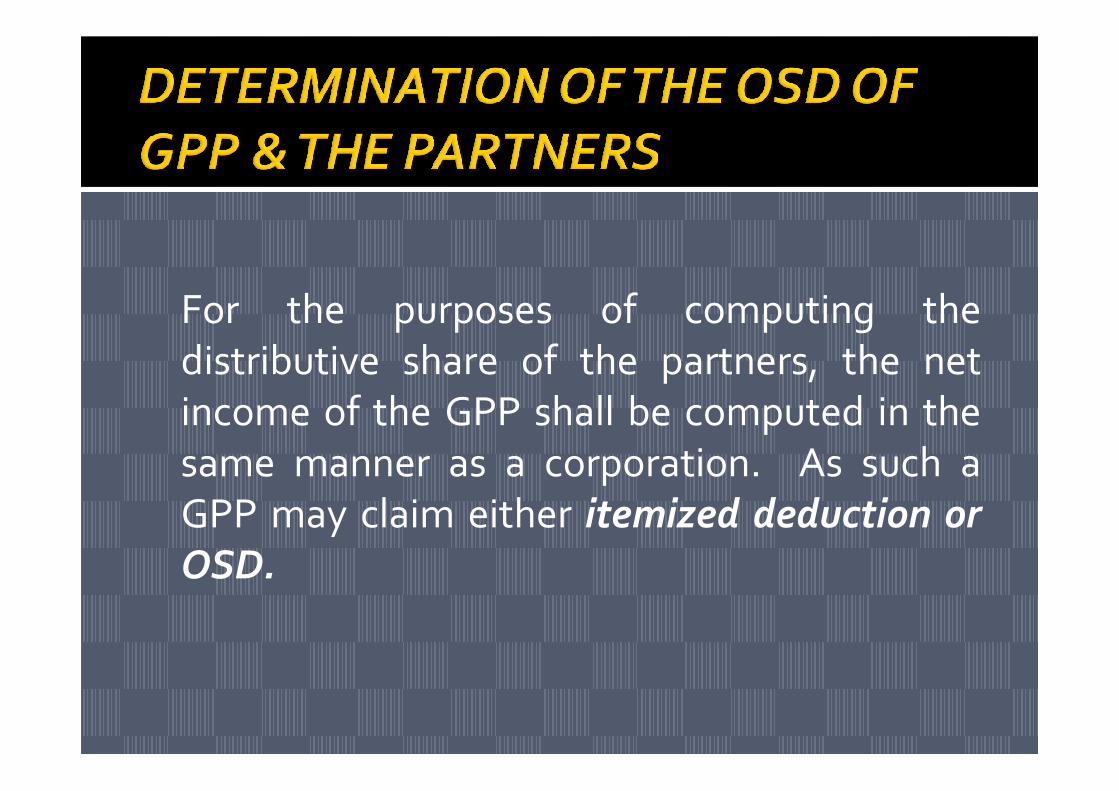

For the purposes of computing the

distributive share of the partners, the net

income of the GPP shall be computed in theincome of the GPP shall be computed in the

same manner as a corporation. As such a

GPP may claim either itemized deduction or

OSD.

The net income determined by either

claiming itemized deduction or OSD from

GPP’s gross income is the distributable netGPP’s gross income is the distributable net

income from which the share of each partner

is to be determined. Each partner shall report

as gross income his distributive share,

actually or constructively received, in the net

income of the partnership.

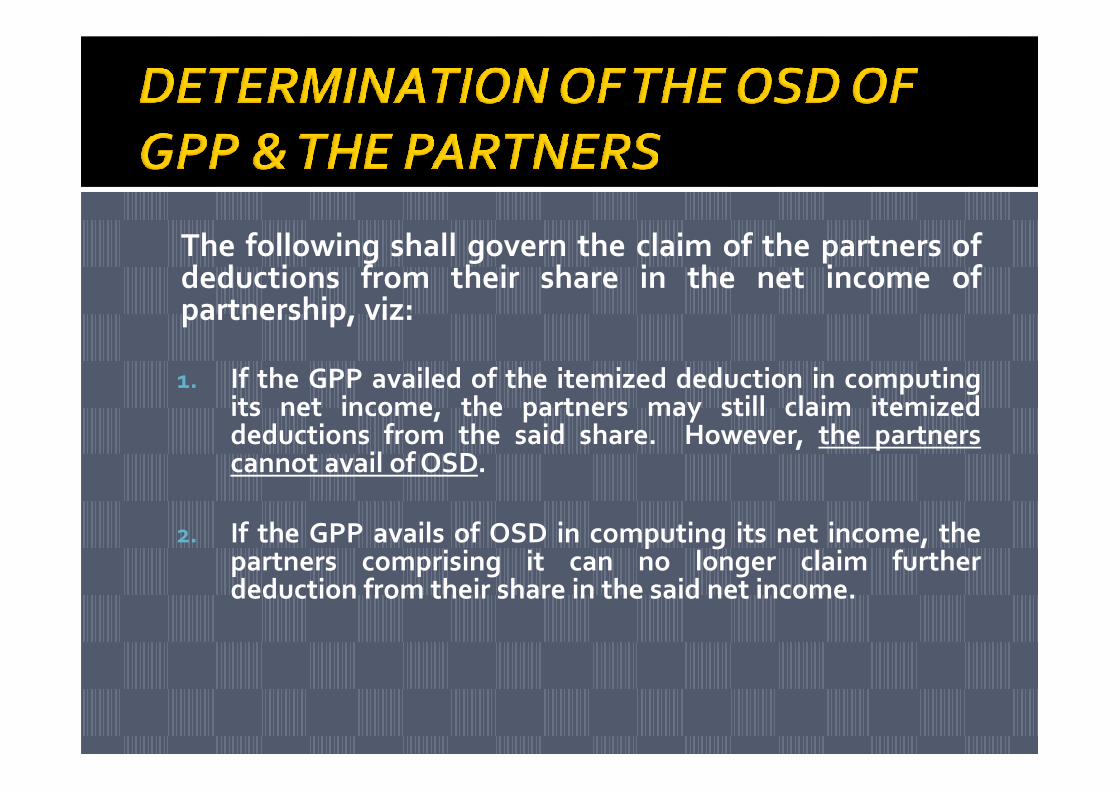

The following shall govern the claim of the partners ofdeductions from their share in the net income ofpartnership, viz:

1. If the GPP availed of the itemized deduction in computingits net income, the partners may still claim itemizedits net income, the partners may still claim itemizeddeductions from the said share. However, the partnerscannot avail of OSD.

2. If the GPP avails of OSD in computing its net income, thepartners comprising it can no longer claim furtherdeduction from their share in the said net income.

3. Since one-layer of income tax is imposed on

the income of the GPP and the individual

partners where the law had placed the

statutory incidence of tax in the hands of thestatutory incidence of tax in the hands of the

latter, the type of deduction chosen by the

GPP must be the same type of deduction

that can be availed of by the partners.

� If the partner also derives other gross income

from trade, business or profession apart and

distinct from his share in the net income of

the GPP who opts for the OSD, the individual the GPP who opts for the OSD, the individual

partner may still claim OSD but not to include

his share from the net income of the GPP.

A taxpayer who elected to avail of the OSD:

� Shall signify in his/its return such intention,

otherwise he/it shall be considered as having

availed himself of the itemized deduction.availed himself of the itemized deduction.

� Once the election to avail of the OSD or

itemized deduction signified in the return, it

shall be irrevocable for the taxable year.

� The election to claim either OSD or the itemizeddeduction for the taxable year must be signifiedby checking the appropriate box in the incometax return filed for the first quarter of thetax return filed for the first quarter of thetaxable year.

� Once the election is made, the same type ofdeduction must be consistently applied for allthe succeeding quarterly returns and in thefinal income tax return for the taxable year.

� A taxpayer who fails to an income tax returnfor the first quarter of the taxable year, shallhave to claim itemized deductions for the restof the year.of the year.

� An individual taxpayer who is entitled to andclaimed OSD shall not be required to submitwith his tax return such financialstatements otherwise required under theCode.

End of presentation

Revenue Regulation 12-2011

These Regulations are hereby promulgated to

ensure that all owners or sub-lessors deal only

with BIR-registered taxpayers, to establish the

procedure for the submission of essentialprocedure for the submission of essential

information by the owners of commercial

establishments/buildings/spaces, and to impose

the appropriate sanctions to ensure observance

and compliance thereof.

� It shall be the primary responsibility of allowners or sub-lessors ofcommercial/buildings/spaces to ensure thatthe person intending to lease theirthe person intending to lease theircommercial space is a BIR- registeredtaxpayer.

* A BIR-registered taxpayer should have TIN, a BIRCertificate of Registration and duly registered receipts,sales or commercial invoice.

� Every 31st of January of the CY (for tenants asof Dec. 31st of the previous year) and 31st ofJuly of the CY (for tenants as of June 30th ofthe CY), all owners or sub-lessors who arethe CY), all owners or sub-lessors who areleasing or renting out such commercial spaceto any person doing business therein arehereby required to submit to the BIR RevenueDistrict Office (RDO) the followinginformation, under oath, in hard and softcopies:

� Building / space layout of the entire area being leased with proper unit/space address or reference;

� Certified True Copy of the Contract of Lease per � Certified True Copy of the Contract of Lease per tenant; and

� The lesee Information Statement shall be presented in the prescribed format, as follows: (Using excel format: printed copy & soft copy stored in a CD-R)

� Lessee Information Statement (for initial Filing):

Name of owner/Lessor_____________________________________ TIN: ____________________________Address:_________________________________________________________________________________

Tenant’s ProfileTenant’s ProfileAs of {June 30, _______} or { Dec. 31, ________}Location of Building/Space for commercial lease:________________________________________________

Location Name of Total Leased Monthly Start of Duration BIR-Registration Profile Flr/Unit # Tenant Area Rental Lease /Period of TIN No. Authority to POS/CRM

Print No. Permit No.*

* For taxpayers also using Point of Sale (POS) / Cash Register Machine (CRM) in dispensing receipts.

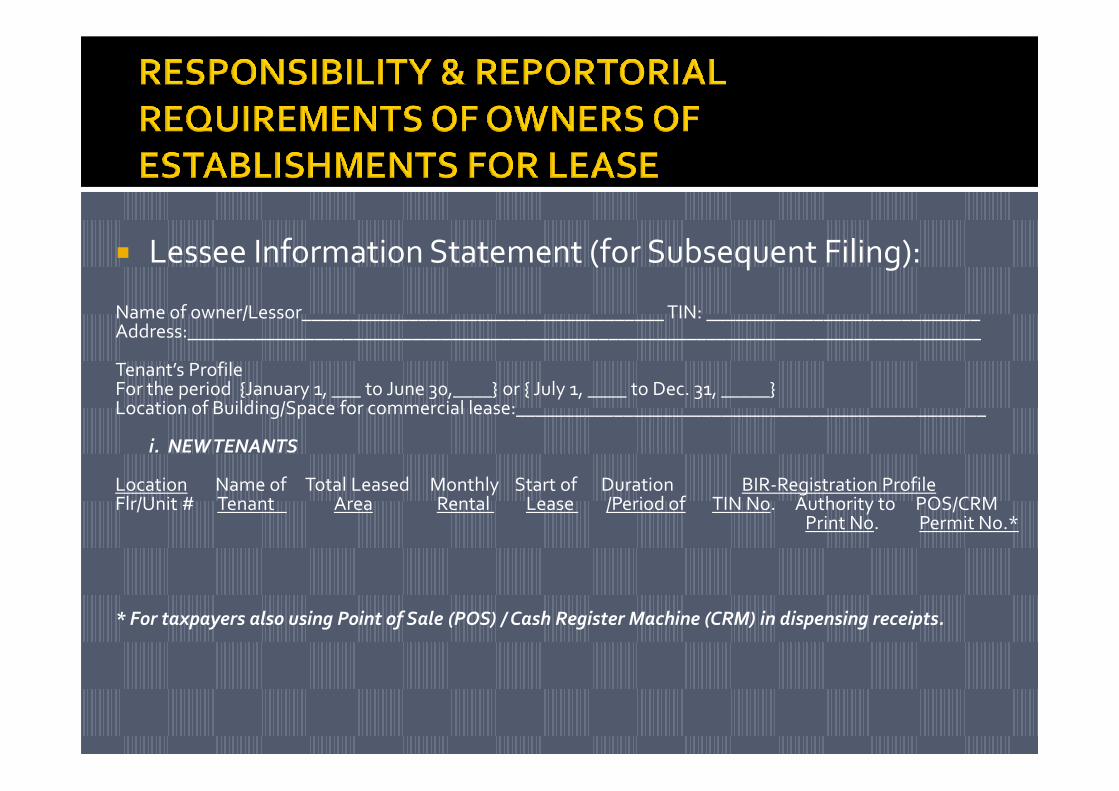

� Lessee Information Statement (for Subsequent Filing):

Name of owner/Lessor_____________________________________ TIN: ____________________________Address:_________________________________________________________________________________

Tenant’s ProfileFor the period {January 1, ___ to June 30,____} or { July 1, ____ to Dec. 31, _____}Location of Building/Space for commercial lease:________________________________________________For the period {January 1, ___ to June 30,____} or { July 1, ____ to Dec. 31, _____}Location of Building/Space for commercial lease:________________________________________________

i. NEW TENANTS

Location Name of Total Leased Monthly Start of Duration BIR-Registration Profile Flr/Unit # Tenant Area Rental Lease /Period of TIN No. Authority to POS/CRM

Print No. Permit No.*

* For taxpayers also using Point of Sale (POS) / Cash Register Machine (CRM) in dispensing receipts.

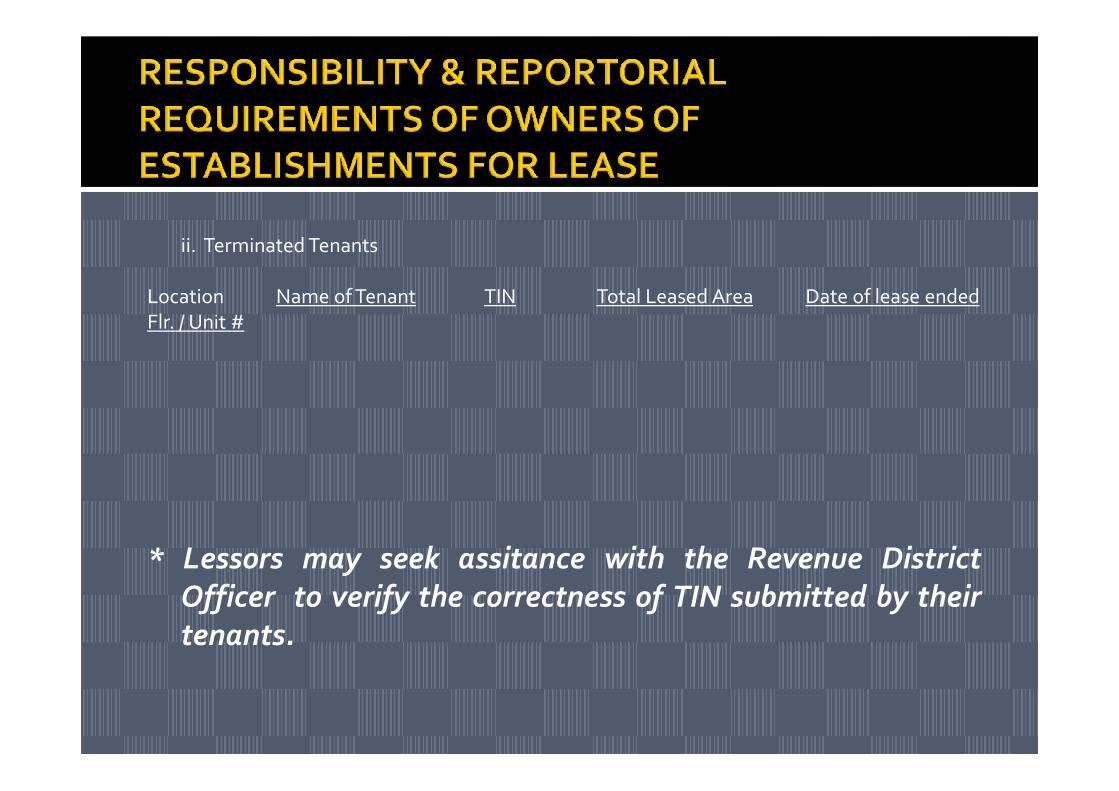

ii. Terminated Tenants

Location Name of Tenant TIN Total Leased Area Date of lease ended

Flr. / Unit #

* Lessors may seek assitance with the Revenue District

Officer to verify the correctness of TIN submitted by their

tenants.

� The first filing of tenants profile will cover tenants as of July 31, 2011. All owners/ sub- lessors are required to comply with these regulations by submitting the ff. Documents on or before September 1, 2011:

� Building / space layout of the entire area being leased with � Building / space layout of the entire area being leased with proper unit/space address or reference;

� Certified True Copy of the Contract of Lease per tenant; and

� The lesee Information Statement shall be presented in the prescribed format, as follows: (Using excel format: printed copy & soft copy stored in a CD-R)

Name of owner/Lessor_____________________________________ TIN: ____________________________

Address:_________________________________________________________________________________

Tenant’s ProfileAs of July 31, 2011Location of Building/Space for commercial

lease:______________________________________________lease:______________________________________________

Location Name of Total Leased Monthly Start of Duration BIR-Registration Profile Flr/Unit # Tenant Area Rental Lease /Period of TIN No. Authority to

POS/CRMPrint No.

Permit No.*

* For taxpayers also using Point of Sale (POS) / Cash Register Machine (CRM) in dispensing receipts.

END OF

PRESENTATIONPRESENTATION