review of literature -...

TRANSCRIPT

80

CHAPTER 3

Review of Literature

3.1 Introduction

After conducting a study of various provisions in tax laws and decisions of

Courts and Tribunals , the researcher conducted exhaustive review of

literature available in the area of indirect taxes and in particular tax planning .

The researcher reviewed following.

Constitution of India with an objective to study the powers to levy and

collect taxes and other measures.

Basic provisions of Central Excise, Customs and Service Tax,

including Acts, Rules and Regulations and notifications issued

thereunder, especially to understand various benefits and exemptions

available to manufacturer and service providers, which contribute to

cost reduction.

Cenvat Credit Rules play an important role in the case of exemptions

under Central Excise and Service Tax. Any exemption under Central

Excise and Service Tax has to be read alongwith Cenvat credit

provisions as it will have direct effect on Cenvat credit.

81

Foreign Trade Policy, which provides various measures for export

promotions and facilities to exporters. Availing benefit of the same is

an important measure for cost reduction.

Legal Metrology Act, as it applies to packaged commodities. For

Valuation of goods under MRP provisions , review of Legal

Metrology Act was essential

Special Economic Zone (SEZ) is treated as island within India and

SEZ developers and Units get many tax concessions in Direct as well

as Indirect Taxes and therefore it helps the unit in reduction in cost by

way of tax concessions and also administratively.

Various decisions of Court and Tribunals in the area of indirect taxes

deciding many aspects of tax planning, valuation, manufacture,

classification etc.

Generally Accepted Cost Accounting Principles and Cost Accounting

Standards provide guidelines regarding accounting and determination

of cost and cost elements.

Cost Accounting Records Rules and Cost Audit Rules have direct

linkage with central excise and service tax. Usefulness of cost audit

mechanism in the area of indirect taxes is well recognized. The cost

audit mechanism provides great support in the area of tax

management.

Review of Committee and Task Force reports on Tax Reforms gives

an idea on the developments in the taxation provision and tax reforms.

82

Research articles.

Report of the Comptroller and Auditor General of India for the year

ended March 2012, on Indirect Taxes contains useful information as to

how tax planning and tax management has failed and resulted in heavy

penalties.

PhD Thesis.

Website of Central Board of Excise &Customs (CBE&C), Ministry of

Commerce, SEZ gives broad idea about various provisions,

amendments etc.

Review of the above is presented in this chapter of Review of Literature.

3.2 CONSTITUTION OF INDIA.1

Constitution of India, which came into effect on 26th January, 1950, is the

supreme of all laws in India and Government actions are subordinate to the

constitution. Power to levy and collect tax is derived from constitution. Any

Act, Rule, Regulation, Notification, Circular cannot be issued overriding the

scope and powers granted in Constitution, otherwise it will be ultra virus the

constitution.

Powers to levy and collect tax is derived from constitution. Statutory

provisions cannot override constitutional provisions and therefore the

researcher felt it necessary to review Constitution with an objective to

understand the powers of Central Government, State Governments and Local

Bodies to make rules, functioning of three organs namely Legislative Organ,

83

Administrative Organ and Judicial Organ, the mode of passing Act,

Ordinance, Notification and its effective date.

The structure of Government is federal in nature. In the basic scheme of

taxation, Article 246 of Seventh Schedule to Constitution indicates bifurcation

of powers to make laws between Union of India and State Governments.

Parliament has exclusive powers to make laws in respect of matters given in

List No. I, called as Union List. State Government’s powers are given in List

II, called as State List and List III, which is called as Concurrent List contains

entries where both Union as well as State Government can exercise powers.

All the three taxes Central Excise, Customs duty and Service Tax are in the

list I and Central Government has exclusive powers to make rules and changes

in these three taxes.

3.3 CENTRAL EXCISE

3.3.1. Central Excise Act 1944.2

Central Excise Act, 1944 is the basic Act, containing basic provisions related

to charging of excise duty, valuation of excisable goods, powers of officers,

penalties, adjudication and appeals, settlement of cases, advanced ruling etc.

The Central Excise Act, 1944, in the present form contains 40 sections. The

Act was known as Central Excises and Salt 1944. The word ‘salt’ was

dropped in 1996.

84

3.3.2. Central Excise Rules, 20022.

Sec 37 of the Central Excise Act, 1944, grants power to Government to frame

rules to carry into effect the purposes of Central Excise Act. Sec.38 of the Act

provides that rules should be made by issue of notification and should be

placed before Parliament for 30 days when Parliament is in session. The

Central Excise Rules do prescribe certain procedures and Returns. For

Contravention of any rules and procedures, stringent penalties have been

prescribed under Central Excise and therefore review of Rules was considered

important for the purpose of tax management.

3.3.3. Central Excise Valuation Rules, 20002

Sec. 4 of the Central Excise Act, 1944 contains the basic provisions related to

determination of value of the excisable goods for the purpose of charging

excise duty. However, in certain cases, value cannot be fixed under Sec 4 of

the Act. Where the value cannot be determined u/s 4 of the Central Excise

Act, Valuation Rules have been prescribed u/s 4(1) (b) of the Central Excise

Act 1944.

The Valuation Rules contain following areas where tax planning is possible

Claiming deduction of freight and insurance from the assessable value

and thereby reduce the excise duty liability as per Rule 5 of the

Valuation Rules.

Concept of additional consideration as envisaged in Rule 6 of the

Valuation Rules.

Determination of correct Cost of Production according to CAS4 as

prescribed in Rule 8 of the Valuation Rules.

Related party transactions in Rule 9 and 10 of the Valuation Rules.

Valuation of the goods in the case of Job Work, as per Rule 10A of the

Valuation Rules.

85

3.3.4. Cenvat Credit Rules, 20042.

Cenvat Credit Rules, 2004 are common for Central Excise and Service Tax.

These rules are framed with the basic objective of minimizing the cascading

effect of duties and service tax. These rules make provision for availing VAT

credit of excise duty paid on inputs and capital goods and service tax on input

services. The credit is interchangeable and can be utilized for making payment

of excise duty on manufactured goods and service tax on taxable output

services.

While reviewing various Exemption Notifications under Central Excise and

Service Tax and Cenvat provisions that every exemption under central excise

and service tax has to be studied alongwith its impact on Cenvat credit.

Cenvat Credit on inputs and input services is not available if final product or

output service is exempt from excise duty or service tax. Where the

manufacturer is manufacturing both dutiable goods and exempted goods or

service provider is providing taxable services and exempted services, there

may be common inputs and input services used for manufacturing dutiable

goods and exempted goods or taxable and exempted services. In such cases,

following four options have been provided under Rule 6 of the Cenvat Credit

Rules.

i) Rule 6(2) of CCR: - Maintain separate inventory and accounts of

receipt and use of inputs and input services used for exempted goods,

exempted services.

ii) Rule 6(3) (i) of CCR: - Pay amount equal to 6% of exempted goods /

exempted services.

86

iii) Rule 6(3)(ii) of CCR :- Pay an amount equal to proportionate Cenvat

credit attributable to exempted final product / exempted output service

as provided in Rule 6(3A).

iv) Rule 6(3) (iii) of CCR: - Maintain separate accounts for inputs and

pay amount as determined under rule 6(3A) in respect of input

services.

The option has to be exercised in respect of all exempted goods manufactured

and all exempted output services provided. As per explanation I to Rule 6(3)

of the Cenvat Credit Rules, the option once exercised shall not be changed in

remaining part of financial year. Therefore exercising correct option is an

important measure of tax planning.

The another important area for tax planning is removal of inputs and capital

goods as such. In case of removal of capital goods after use, paying correct

amount is also an important area for tax management.

Highlights of Cenvat Credit Scheme

Intents to avoid cascading effect of Excise Duty and Service Tax.

Credit of duty paid on inputs, input services and capital goods

available to manufacturer of excisable goods and provider of taxable

output services.

No credit of service in Jammu and Kashmir.

Inputs, moulds, dies, jigs and fixtures can be sent to Job Worker.

Removal of used capital goods as scrap or second hand capital goods

on payment of appropriate amount.

Credit on motor vehicles available to specified output service

Credit on basis of specified documents.

87

Credit available instantly in case of input goods and input services.

Cenvat credit of capital goods in two stages, upto 50% in the year of

receipt and balance in any subsequent financial year.

Cenvat to manufacturer available only if there is a ‘manufacture’.

Cenvat Credit is available in respect of specified duties only such as

basic excise duty, service tax, education cess and higher education

cess, countervailing duty, special additional duty.

Cenvat Credit of special additional duty is not available to service

provider.

Utilization of Cenvat credit for payment of duty on final product as

well as service tax on output services. Cenvat Credit interchangeable.

Cenvat Credit is indefeasible.

One-to-one correlation between inputs and final product is not

required.

No input credit if final product / output service exempt from excise

duty/ service tax.

No cash refund, except in case of export or supply to SEZ.

Unutilized Cenvat Credit is transferable in case of transfer of location,

sale, and merger of the manufacturing unit.

Accounting entries not relevant for eligibility of Cenvat Credit.

88

3.3.5. Central Excise Tariff Act 1985.3

Excise duty is on excisable goods manufactured or produced in India. The

liability of payment of duty is on manufacturer of the goods. To determine

correct duty payable following two steps need to be followed.

1. Classify the goods correctly to find out rate of excise duty.

2. To determine assessable value of the goods, to which rate of duty is to

be applied for calculating amount of duty payable.

The Classification of goods, rate of duty and principles of classification are

given in the Central Excise Tariff, Schedules thereof. The Central Excise

Tariff Act, 1985 (CETA) classifies goods under 96 Chapters. A specific code

is assigned to each item. The classification forms basis for classifying the

goods under a particular chapter head / sub head to prescribe duty to be

charged on that particular product.

Central Excise Tariff Act, 1985 deals with the classification of goods and rate

of excise duty payable on it. Predominantly the classification of goods is

based on Harmonious System of Nomenclature and trade parlance i.e. a word

in statute should be construed in its popular sense and not in strict or technical

sense. Popular sense means that which people conversant with the subject

matter with which statute is dealing, would attribute to it. In CCE Vs Vicco

Laboratories-2005(179)ELT17(SC 3 member bench), Hon. Supreme Court

held that the burden of proof that a product is classifiable under a particular

tariff head is on the revenue and must be discharged by proving that it is so

understood by the consumers of product in common parlance.

89

Exemption Notifications are issued by the Central Government providing

concessions and exemptions from duty. The effective rate of duty is to be

found from the relevant notification issued under Central Excise Tariff.

3.3.6. Notifications3.

Under Sec.5A and 11C of the Central Excise Act, 1944 powers have been

granted to Government for granting partial or full exemptions from excise

duty. Central Excise Rules also provide for issue of notifications in respect of

various matters. The Rules and Notifications have full legislative backing and

are treated as part of the Act.

3.3.7. CBEC’s Excise Manual of Supplementary Instructions2.

The manual of supplementary instructions was issued by the Central Board of

Excise and Customs in 2005. Only general provisions and procedures

applicable to manufactured goods have been incorporated in this manual. The

manual is divided into 19 chapters and contain instruction related to following

Registration under Central Excise,(Chapter 2).

Assessments, Classification, valuation, provisional assessment,

manner of duty payment, account current, scrutiny (Chapter 3).

Invoice System (Chapter 4).

Cenvat Credit (Chapter 5).

Records and Returns under Central Excise (Chapter 6).

Export without payment of duty (Chapter 7)

Export under claim of rebate (Chapter 8)

Refund(Chapter 9)

Warehousing (Chapter 10).

Samples (Chapter 11).

90

Special Procedure for specified goods (Chapter 12).

Demand / Show Cause Notice, Adjudication, Interest, Penalty,

Confiscation, Seizure, Duty payment under protest. (Chapter 13).

Bonds and Letter of Undertaking (Chapter 14).

Excise Audit (Chapter 15).

Appeals (Chapter 16).

Search, Seizure, Arrest and Prosecution (Chapter 17).

Remission of duty, Return of duty paid goods to factory, Job Work

(Chapter 18).

Advance Ruling (Chapter 19).

3.3.8 Circulars issued by CBE & C4.

Central Board of Excise and Customs issues circulars and clarifications from

time to time. Trade Notices are issued by the Commissioners. Generally

circulars are issued to clarify the views of the Government in respect of

specific points under Act, Rules or Notifications or to give some information.

The circulars do not have any legal force and are not binding on assessee,

quasi judicial authorities and courts. If any circular or trade notice is beyond

the provisions of Act or Rules, they cannot be binding on Government also.

91

3.4 CUSTOMS.

3.4.1 Customs Act 1962, Rules and Regulations made thereunder5.

Customs Act 1962, contains basic provisions related to imports and exports

and customs duty. The Rules and Regulations framed thereunder contain

procedural aspects, valuation for the purpose of determination of customs

duty, person responsible for payment of duty, penalties, appeals etc. Like

Central Excise, Rules and Regulations are issued under Customs Act to carry

into effect the purposes of Customs Act, 1962. Notifications are issued

granting partial or full exemptions from Customs Duty.

3.4.2 Customs Tariff Act 19756.

Customs Tariff Act, 1975 deals with the classification of goods and rate of

customs duty payable on it. Predominantly the classification is based on

Harmonious System of Nomenclature and trade parlance. Exemption

Notifications are issued by the Central Government providing concessions and

exemptions from duty. The principles of classification of goods under Central

Excise and Customs are same.

3.4.3. Customs Manual-20115.

Customs Manual was released by Central Board of Excise and Customs on

27.01.2011. The manual gives an overview of Customs Law and Procedures.

Though it is useful guide to taxpayers and it does not substitute for the rules,

regulations, notifications, circulars and instructions.

92

3.5. SERVICE TAX7.

3.5.1. Finance Act, 1994

Sec 64 to Sec 99 of Finance Act 1994 , contain provisions related to Service

Tax. There is no separate Act for service Tax. Service Tax Rules and other

Rules are also issued under the powers granted under Finance Act 1994.

3.5.2 Rules relating to service tax.

Following are the important rules related to service tax.

Service Tax Rules,1994

Cenvat Credit Rules,2004

Point of Taxation Rules, 2011.

Service Tax (Determination of Value) Rules, 2006.

Service Tax (Advance Ruling) Rules, 2003.

Service Tax (Settlement of cases) Rules, 2012.

Place of provision of Service rules, 2012.

Service Tax (Registration of Special Category of Persons) Rules,

2005.

Service Tax (Publication of Names) Rules, 2008.

Service Tax (Provisional Attachment of Property) Rules, 2008.

Service Tax (Compounding of Offences) Rules, 2012.

Service Tax (Removal of Difficulty) Order, 2012.

93

3.5.3 Education Guide issued by Central Board of Excise and Customs.

This contains clarifications and explanations on various issues related to

service tax and provide useful information to tax payers.

3.6 Foreign Trade Policy8

Under powers of Sec 3 and Sec 5 of Foreign Trade (Development and

Regulation) Act, 1992, Ministry of Commerce issues policy for import and

export. Usually it is issued for five years but is amended from time to time.

The policy was earlier termed as EXIM policy. It was renamed as “Foreign

Trade Policy” for 2004 onwards.

Generally, policy announced by Ministry of Commerce is not followed by

customs and excise department unless there is corresponding excise or

customs notification.

The Foreign Trade Policy provides the overarching framework for catalyzing

India’s Exports. The Foreign Trade Policy for the year 2009-2014 was

announced on 27th August 2009.

The Foreign Trade Policy contains policy and procedures related to Special

Focus Incentives, Board of Trade- its composition and Terms of Reference,

General Provisions regarding imports and exports, Export Promotional

Measures, Deemed Exports, etc.

The Duty Exemption and Remission Schemes under Foreign Trade Policy

include following

94

Advance Authorization Scheme,

Duty Free Import Authorization (DFIA) Scheme,

Duty Entitlement Passbook (DEPB) Scheme,

Export Promotion Capital Goods (EPCG) Scheme,

Export Oriented Units (EOU), Electronics Hardware Technology Parks

(EHTPs), Software Technology Parks (STPs) and Bi-Technology Parks

(BTPs).

Special Economic Zones.

Free Trade and Warehousing Zones.

Availing benefits of the various schemes under Foreign Trade Policy is an

important measure of tax planning and contributes to cost reduction activities

substantially.

95

3.7 Special Economic Zone Act

Special Economic Zone (SEZ), Act 2005 is an Act to provide for

establishment, development and management of the Special Economic Zones

for the promotion of Exports and for matters connected therewith or incidental

thereto. As spelt out is Sec 5 of the Special Economic Zone Act ,2005

following are the guiding factors in approving proposals to establish SEZ.

a) Generation of additional economic activity;

b) Promotion of exports of goods and services;

c) Promotion of investment from domestic and foreign sources;

d) Creation of employment opportunities;

e) Development of infrastructure facilities; and

f) Maintenance of sovereignty and integrity of India, the security of the

State and Friendly relations with foreign states.

Special Economic Zones offer well developed enclaves of industrial

infrastructure with plots, built up space, power, water supply, transport,

housing , social infrastructure etc. The Special Economic Zones are

specifically delineated areas wherein units may be set up for specified

purposes of manufacturing or trading or rendering services or for providing

warehousing facilities for export.

As per Sec 2(i) of the SEZ Act, the domestic tariff area (DTA) means the

whole of India including its territorial waters and continental shelf but not

including areas of the SEZ.

Sec 53 of the SEZ Act provides that SEZ shall be deemed to be a territory

outside the Customs territory of India. The legal implication is that the SEZs

are treated as foreign territory for the purposes of trade operations, duties and

96

tariffs . In other words goods and services going into the SEZ from DTA are

treated as exports and goods and services coming from SEZ are treated as

Imports. Therefore, domestic laws do not generally apply to the SEZs and the

units therein. Sec 51 of the SEZ Act provides that SEZ Act will have

overriding effect over other laws.

Vide Finance Act, 2002, changes were brought in the Customs Act, 1962 and

Central Excise Act,1944 in the context of the SEZs.

3.8 Review of Committee Reports.

3.8.1 A Task Force on Direct Taxes Reforms10.

Ministry of Finance and Company Affairs, with an objective to rationalize and

simplify Direct Taxes Laws and re-design procedures to bring them at par

with best international practices, so as to encourage voluntary compliance and

reduce compliance cost, vide Notification No. 153/191/2002-TPL dt.6th

November 2002, constituted a Task Force on Direct Taxes, under the

chairmanship of Dr. Vijay Kelkar.

The consultation paper of the Task Force on Direct Taxes was made available

on the website of the ministry of Finance & Company Affairs on 2nd

November 2002 inviting comments and suggestions of all concerned.

The Task Force submitted its final report to the ministry, recommending

various measures of simplification in tax provisions with respect to annual

information return, search and seizure, assessments, dispute resolutions, tax

administration, personal tax reforms, corporate tax reforms, taxation of capital

gains etc. The task force recommended more autonomy to CBDT.

97

It was expected that the recommendations of the task force will have

following impact.

1. Individual taxpayers of all categories and in every income group benefit

substantially from the package of recommendations. (Para 9.8)

2. Overall, the recommendations are revenue neutral at the existing level of

compliance. To the extent the new simplified and liberalized tax regime

will introduce compliance, the revenue gains are likely to be substantially

higher and it will enhance buoyancy by widening the personal and

corporate income tax bases.(Para 9.14)

3. The recommendations for eliminating the exemptions, the extensive use of

technology and privatization of non core activities of the tax

administration will result in sharp reduction in transaction cost. A 10 %

reduction in transaction cost for personal income tax would help taxpayers

to save an estimated Rs.4000/- Crores. Such reduction in transaction cost

is progressive.

The Task Force Recommendations were mainly on simplifications in tax

provisions and reducing the complications, resulted in helping taxpayers in

tax planning.

3.8.2 A Task Force on Indirect Taxes10.

Ministry of Finance and Company Affairs, with an objective to take advantage

of information technology and bring the indirect tax systems and procedures

at par with the best international practices , and thus , encourage compliance

and reduce compliance cost, vide Notification No. 201/65/2002-CX6 dt. 3rd

September 2002, constituted a Task Force on Indirect Taxes, under the

chairmanship of Dr. Vijay Kelkar.

98

On 25th October 2002, the Task Force presented the consultation paper to

the Government with a request that the same may be made available to the

public at large for discussion on the proposals contained therein.

The response was overwhelming; By and large the proposals contained in

the consultation paper were appreciated. However, there was also

constructive criticism to some proposals, particularly tax rates of some

items.

It was expected that with the proposed reforms, the reduction in the

transaction costs could be as much as 50%, the potential gains to the

economy would be Rs.4000-5000 Crores per annum.

The basic reforms recommended by the task force include following.

Customs Procedures and Trade Facilitation

1. Trust Based System (TBS); Universal Green Channel.

2. Liberal steps in Licensing of Customs House Agents. (CHA).

3. For improved Customs Administration, following measures were

recommended

Intelligence, investigations and audit sections of the customs house

may be strengthened.

Functioning of Special Valuation Branch should be reviewed to

provide time bound finalization of cases in practice. Further pre

deposit of duty should be dispensed with.

There should be sharing of merchant overtime fees for activities done

in customs area.

99

Export valuation rules should be framed for export promotion

schemes.

Customs should allow abandonment of warehoused goods.

Customs duty payment may be through cheques.

Expansion of scope of confiscation provisions to include non dutiable

goods as well as goods not covered under drawback scheme.

To accept Export Obligation Discharge Certificate issued by DGFT by

customs without delay.

Customs officers may be empowered to enforce IPR by a suitable

amendment to the Trade and Merchandise Marks Act and the

Copyright Act.

Central Excise

The recommendations aimed at comprehensively changing the essence of

central excise administration with the twin objective of tax payer facilitation

and encouraging compliance for increased revenue.

Following are the highlights of the recommendations made by the Task Force.

Manufacture

Levy of Central Excise should be progressively based upon value

addition to be applied only to the processing stage of manufactured

goods.

In order to prevent any misuse of the MRP provisions, it was

recommended that wherever MRP based levy is applied on an item,

the act of repacking, re-labelling and putting the item into unit

100

container for retail sale may be deemed to be amounting to

manufacture.

Valuation

Guidelines for determination of cost of production should be issued at

the earliest.

Value of the goods, when removed to sister units should be 105% of

cost of production.

The system of MRP based valuation may be expanded.

Cenvat

Abolish the distinction between capital goods and inputs and allow

credit on all inputs brought into factory except for those figuring in a

small negative list, such as office furniture, motor vehicles, MS, HSD

etc.

To allow full credit of the duty paid on capital goods immediately on

receipt, as in the case of inputs.

An explanation may be inserted in rule 16 of the Central Excise Rules,

to the effect that the amount paid on removal of returned goods can be

taken as Cenvat credit in the hands of the recipients.

A specific provision may be introduced to charge duty on the

dismantled capital goods when removed from the factory.

101

Cenvat Credit should not be allowed on deemed credit basis.

Rule 12 of the Cenvat Credit Rules, 2002 should be amended to

provide recovery of Cenvat credit erroneously refunded.

Cenvat inputs may be allowed to be stored outside the factory in an

identified place of storage subject to procedural safeguards for due

accountal of the inputs.

Export

Sealing of export consignments by Central Excise Officers should be

replaced by self sealing by the exporter, as a matter of right.

Improvement in the system of grant of rebate.

Manner of payment of duty

Fortnightly payment of duty may be replaced by monthly payment.

The date of payment of central excise duty may be prescribed as the

date of presentation of the cheque to the bank subject to its realization.

In the case of default in payment of duty, the provision of withdrawing

the facility of payment of duty in installments in case of defaults

should be revoked.

102

There should be automatic charge of interest and penalty in the event

duty is not paid on time.

In the event it is decided to retain the provision of withdrawing the

facility, the assessee should be allowed to pay duty during this period

through Cenvat credit.

Other important recommendations include the reforms in the Assessments,

Dispute Resolution, Filing of Returns, Voluntary filing of documents by tax

payers, Arrests, Tax clinics for small scale sector manufacturers.

Researchers Observations and Comments:-

The consultation paper was presented in October 2002. It has been observed

that during the last twelve years, the provisions under Central Excise Act,

Central Excise Rules and Cenvat Credit Rules have been amended to give

effect to almost all the recommendations made by the Task Force. Following

are the examples.

1. Section 2(f) of the Central Excise Act, 1944 has been amended to

include packing, repacking, labeling, relabeling, putting the item

into unit container for retail in the definition of “manufacture.”

2. Schedule III, to the Central Excise Act has been issued to provide

list of items where packing, repacking, labeling, relabeling, putting

the item into unit container for retail amounts to “manufacture.”

103

3. Notification No. 49 has been issued to provide for abatement in the

MRP to arrive at the assessable value of the items covered under

MRP Provisions.

4. Rule 16 of the Central Excise Rules, 2002 has been amended to

provide that the amount paid on removal of returned goods can be

taken as Cenvat credit in the hands of the recipients.

5. Cenvat Credit Rules have been amended to provide that Cenvat

Credit is not allowed on deemed credit basis.

6. Fortnightly payment of duty is replaced by monthly payment.

7. The date of payment of central excise duty is prescribed as the date

of presentation of the cheque to the bank subject to its realization.

In fact, e-payment is made mandatory where the duty liability is

more than Rs.10 Lacs annually.

8. Sec 11A of the Central Excise Act has been amended to provide

for automatic charge of interest and penalty in the event duty is not

paid on time.

The amendments made in the excise, in line with the recommendations of the

Task Force has removed many complications and made the compliance, tax

management and tax planning easier.

104

Service Tax

The task force recommended the following:

1. To the extent possible, Service Tax should be levied in a

comprehensive manner leaving out only few services by including

them in a negative list.

2. There should be complete integration of Cenvat credit and service tax

credit schemes.

3. Credit of central duties (on goods and services) should be utilized for

payment of service tax collected and appropriated by the Central

Government.

4. The rate of service tax should be suitable enhanced so as to achieve

parity with the Cenvat rate by 2006-07. However, there should be two

rates, one for service providers who avail credit and a lower rate for

those who do not.

5. Threshold limit of Rs.10 Lakhs for small service providers.

6. Separate enactment for service tax.

7. Service should be classified on the basis WTO classification, which

should be made a part of Service Tax legislation.

8. The task force also recommended measures of early settlement of

disputes.

105

9. It was also recommended that there should be a time bound review of

the automation needs of service tax administration and in like manner

as proposed for other indirect taxes steps should be taken to automate

the processes and allow online filing of returns and payment of service

tax.

Researchers Observations and Comments:-

The consultation paper was presented in October 2002. It has been observed

that during the last twelve years, the provisions related to Service Tax have

been amended to give effect to almost all the recommendations made by the

Task Force. Following are the examples.

1. Service Tax based on Negative List has been made effective from

01.07.2012.

2. “Service” has been defined in Sec 65(44) of the Finance Act, 1994.

3. Cenvat Credit Rules, 2004 made applicable to manufacturing and

service sector providing interchangeability of Cenvat Credit

Utilization.

4. Service Tax Rate and Cenvat Rate (Central Excise Duty rate) are at par

from 01.04.2011.

5. Threshold limit of Rs.10 Lakhs for small service providers.

The new law, (w.e.f. 01.07.2012) provides more area for tax planning.

106

Others

The Task Force also recommended various simplification measures in the area

of Export Promotion, SEZ and EOU schemes, Drawback Scheme, Automation

of indirect tax systems and procedures, improving indirect tax administration,

CBEC Administration, Revenue augmentation, Tax levies and rates, Central

Excise Duty Structure for Petroleum and Textile sector, Small Scale Sector

duty exemption, and VAT. As regards Central Excise Duty Exemptions, it

was recommended that the following factors must be taken into account while

considering the grant of a duty exemption.

Income elasticity of the product cost of compliance, international best

practices, and cannon of transparency.

Instead of duty exemption whether it is possible to extend the same

benefit through a budgetary mechanism.

If an exemption is issued, it should indicate the period of its validity

with a proviso that changed circumstances may warrant a mid-term

review.

On perusal of the recommendations made by the task force and the Central

Excise, Customs and Service Tax law in the present form, it can be seen that

most of the recommendations made by Task Force have been implemented

and the law has been amended suitably.

In the opinion of the researcher, the amended provisions do help in tax

management and tax planning in Indirect Tax areas. It has brought

simplification and clarity in the law and left very little scope for different

interpretation and confusion.

107

3.8.3 Advisory Group on Tax Policy and Tax Administration for Tenth

Plan10

The Planning Commission set up the Advisory Group in July 2000 under the

chairmanship of Shri Parthsarathi Shom to study tax policy and Tax

Administration issues and make appropriate recommendations at different

levels of government with the purpose of granting resources for the tenth Five

Year Plan.

Challenges before Advisory Group

The Advisory Group faced two challenges.

1. The parameters for the tenth plan were not finalized so far. The group

considered 15% growth target for its recommendations and suggestions.

2. While various aspects of tax structure have improved over time, many

deficiencies remained. Correction of such deficiencies would have

negative revenue impact in the short to medium term. The group took

option of analyzing such aspects and recommending corrective action

despite their potential negative impact. This implies that major

complimentary revenue yielding measures are needed to improve the

overall revenue productivity of the tax system, comprising both tax policy

and tax administration, and including all levels of government – Central,

State and Local.

108

Recommendations

Following major recommendations related to Indirect Taxes, were given by

the group.

Union Excise

1. It was recommended in the Interim Report that a two-rate structure of 16

percent together with a higher rate should be introduced. An increasing

number of items were to be converged to fall under the 16 percent rate to

minimize classification problems. This would be economically desirable

and administratively simple. The rates would have to be adjusted for

inclusion of services in the CENVAT. The 2001-02 Union Budget has

moved clearly towards a two-rate duty structure of 16 percent and 32

percent. However, the lingering lower rates of 4 percent and 8 percent

should now be merged with 16 percent in the next budget.

2. There is also a multiplicity of levies that include, apart from the excise

rate structure, additional excise duty (goods of special importance) in lieu

of sales tax on sugar, fabrics and tobacco; additional duty on motor

spirit (petrol and diesel); additional duty on textiles and textile articles

(fibers, yarn and fabric) under a subsidy scheme for "controlled cloth";

and cesses leviable under miscellaneous enactments. Separate accounts

are to be maintained for each of these levies, increasing administrative

and compliance costs. It is difficult to work out effective tax rates since

CENVAT credit is not given for all of them. It was recommended that

there should be a single levy under the Central Excise Act.

109

Base of Union Excises

The base of excise is manufacture. While many disputes have occurred over

the definition of manufacture, the effective twin test is: (a) a new article

should come into existence; and (b) it should be marketable. The current

definition—that does not include activities that may be deemed to be

manufacture such as labeling or printing a brand name—encourages

segregation of manufacturing activities to avoid tax. It was recommended in

the Interim Report that the definition of manufacture be widened to include

the chain of value addition by or on behalf of the manufacturer (undertaken

before marketing the product) to be charged to duty. The 2001-02 budget has

accepted this principle though only in the case of branded garments. This now

needs to be extended to other items like shoes, electrical gadgets etc.

Cenvat

It is recommended that both capital goods and other inputs "used in the

factory of the manufacturer" should be allowed CENVAT credit. Thus, capital

goods and other inputs should not be distinguished for purposes of input tax

credit.

Cenvat credit on capital goods should be immediately restored by giving the

credit in the year of purchase itself.

110

Exemptions

The Group observed that the excise base is eroded by exemptions, inter alia,

for: (a) small scale industry (SSI); (b) village industry marketed with KVIC

assistance; (c) specified goods supplied to various types of public institutions;

(d) goods produced without power; (e) cooperative society produced tea; (f)

goods produced in the North-East; (g) a number of food items including

bread, spices, coffee, khandsari sugar, cereals, edible oils and several

unbranded food items; (h) fertilizers; (i) unregistered branded garments,

clocks, watches upto Rs.500, electric bulbs upto Rs.20; (j) aircraft, ship and

boat; etc.

Further, the formulation of exemptions is extremely complex. Of the standard

publication of tariffs of 720 pages, 220 pages are devoted to exemptions.

There are 90 exemptions for textiles. For small scale industry, there are 5; for

exports, there are 20; for job work, there are 5, and so on. Each exemption has

many entries, conditions and lists, in turn, containing hundreds of items in

each list.

Credit is given on inputs manufactured in the North East even though no duty

is paid on such inputs. This is said to cause considerable leakage.

In the main notification which combines all exemptions for the different

chapters (3/2001CE), there are now 262 entries while in the previous year’s

notification (6/2000-CE), there were 259 entries. Thus, the list has expanded,

though marginally.

111

The Interim Report recommended that an intensive effort is necessary to

rationalize exemptions on the same subject through abolition and merger.

Conditions for exemptions must be minimized. When an item is covered

under the SSI exemption scheme, there should not be any separate exemption

except for some very valid reasons. SSI exemption should be extended to

textiles also by replacing the individual exemptions. Overall, there has been

no significant change in the area of exemptions.

SSI units receive concessional duty as well as full CENVAT credit. SSI units

below a turnover of Rs.3 Crores should pay a duty of 85-90 percent of the

normal rate if they opt for CENVAT credit. The 3 Crores turnover calculation

should not exclude exports and exempted goods produced by a SSI unit. SSI

units must maintain all records and give a declaration. Only really small units

with a turnover of Rs.15-20 lakhs should be exempted from

declaration/maintenance of records. The unutilised credit should lapse once

the Rs.1 Crores exemption limit is reached.

An important issue in expanding the base is the inclusion of services in the tax

net through comprehensive taxation of services. It is important to integrate

services as early as possible with the CENVAT to arrive at a full fledged VAT

at the Centre, perhaps as early as in the Budget of 2002-03, rather than to

continue with a separate structure of service taxation that cascades and causes

economic distortions. The Centre should also allow states to tax services so

that they can integrate services into their VAT base. A mechanism that would

make this feasible is elaborated below (see Section 7e).

112

Administration

While the VAT mechanism reduces tax induced economic distortions by

reducing cascading (of "tax on tax"), the aspect of input tax credit tends to

pose particular demands on administration. A substantially faster growth in

MODVAT credit vis-á-vis growth in gross revenue has caused concern

regarding potential misuse of MODVAT credit invoices. A field survey has

indicated that, besides procedural and technical offenses, other violations

included: (1) undervaluation of goods; (2) non-reversal of credit in respect of

returned rejected inputs; (3) misuse of facility of job work; and (4) availing of

credit on exempted final products; twice on the same invoice; without

payment of duty; by using fraud/fake documents. It appears that 10 percent of

revenue may be lost from these factors. There is also the perception that the

exempted SSI sector exacerbates the misuse of CENVAT credit invoices. As

the SSI sector has no interest in CENVAT credit invoices, the invoices

relating to their purchases have been misused by the non-exempted sector.

Thus rationalization of SSI exemptions from CENVAT should check evasion

over and above improving the excise structure.

The depot or other places of removal should be made into duty paying

agencies, with accounts-based checks and audits at regular intervals.

The fortnightly payment should be replaced by monthly payment to enhance

the liquidity of units and to reduce excessively stringent accounting needs.

Despite the move towards financial control, vestiges of physical restrictions

remain. When goods are returned by buyer to seller, in certain circumstances,

approval is necessary from the Chief Commissioner for re-entry of goods to

the factory. This is time consuming and unnecessarily exacerbates the need for

113

tax official—taxpayer contact. Reentry should be allowed on accounts based

self declaration or simple intimation to the Department.

Manufacturers may acquire spare parts for use or they may resell them. For

such trading activities, approval of the Department is needed which is

generally not given. Resale should be allowed on the basis of maintenance of

accounts and penalty imposed in case of misuse. On the whole, therefore,

excise administration should complete its movement towards financial control

from physical control based methods.

Researcher’s Observations

The recommendations made by the Advisory Group were very useful in

bringing simplicity in tax administration. The Government has accepted some

of the suggestions and accordingly changes were made in the following areas.

1. Concept of Deemed manufacture was introduced in the definition of

Manufacture u/s 2(f) of the Central Excise Act, 1944.

2. Rationalization in exemptions by merging the various exemption

notifications and issuing a mega notification No.12/2012-CE for

granting various exemptions.

3. The fortnightly payment replaced by monthly payment.(Rule 8 of

Central Excise Rules,2002)

4. Reentry of goods allowed on accounts based self declaration or simple

intimation to the Department.(Rule 16 of the Central Excise

Rules,2002).

5. Resale of goods allowed on the basis of maintenance of accounts.

However no changes were made in Cenvat Credit Provisions

114

Taxation of Services

1 An interim method that should enable states to tax services with

cooperation from the Centre and without the need for a Constitutional

amendment could be one where the Centre may levy the service tax on

them and authorize the states to administer/collect them. However, the

Centre and states must first arrive at a consensus on the list of services

that can be administered by the states.

2 The service tax collected by the states would have to first go to the

Consolidated Fund of India as per Article 266(2). After that, the

Centre would disburse an equivalent amount to the states. This interim

method has found favour with the Chief Ministers of states with whom

the Group discussed the matter.

3 The states should be given the powers to tax services whose

consumption is of an intrastate nature.

4 After the initial introduction, services could be incorporated into the

VAT.

5 The rate structure for the VAT on services should be identical to those

for goods to obviate distortions in producer and consumer decisions.

6 The state taxes like luxury and entertainment tax on restaurants, hotels

and other lodgings, professions tax, motor vehicles tax, goods and

passengers tax and electricity duty should be integrated with the state

level VAT.

115

7 Various public utility services that have scope for corporatization

should be brought within the state level VAT on services.

8 The VAT on services should be fully integrated with the VAT on

goods, both in its design and administration, with an appropriate

mechanism to set off service input tax against goods output tax and

vice versa. Therefore, a destination based, invoice credit method, dual

VAT—one at the central level and another at the level of states—

comprising both goods and services could be envisaged by the end of

the Tenth Plan.

9 The assignment of the powers to tax services to states must be viewed

as adequate compensation for revenue loss on account of abolition of

the central sales tax.

3.8.4 Task force on Direct Taxes10:

A Task Force on Direct Taxes was formed under the chairmanship of Dr.

Vijay Kelkar. The Task Force presented the consultation paper to the

Government on 2nd November 2002. The Task Force gave many

recommendations on Reform of Tax Administration, Search and Seizure,

Personal Income Tax, Corporate Tax Reforms, Taxation of capital gains.

The Task Force recommended the abolition of Wealth Tax. The Task Force

also recommended merger of tax on expenditure in hotels with service tax.

116

3.8.5 Tax Reforms Committee headed by Prof. Raja J. Chellaiah10:

The economic liberalization initiated in 1991 by the Government carried a

special focus on Tax Reform as it was felt that complexities in levy and

collection of tax could fetter economic activity. The Tax Reforms Committee

headed by Prof. Raja J. Chellaiah examined the Tax System and

Administration in the country. The Committee concluded that a simple,

credible and progressive system was necessary to improve Tax compliance.

The need for better relations between the Tax Collectors and Taxpayer was

also emphasized. The need to achieve both equity and efficiency in Taxation

was thought to be important.

3.9 Research papers presented in conferences or published in

Journals.

3.9.1 Research Paper: Federalism in India: Political Economy and

Reform:

M. Govinda Rao and Nirvikar Singh had authored a paper in Conference on

“India: Ten Years of Economic Reform”, at the William Davidson Institute,

University of Michigan, September 2001. According to the study 1999-2000

the central indirect tax to GDP ratio is 6.23 percent. The Tax Reform

Committee of 1991 had also recommended minimizing exemptions and

concessions, simplification of laws and procedures, development of modern,

computerized information system and improvements in administration and

enforcement (Rao, 2000a). Work in the mid -1990s by Das - Gupta and

Mookherjee (198, Chapter 6) detailed the problems with Indian tax

administration both in terms of incentives for paying taxes and those

117

enforcing them. A reform that more directly affects India’s federal system lies

in Indirect taxes, which, as noted have not increased proportionately with

GDP in the last decade. As Rao (2000a) mentioned “The most important

challenge in restructuring the tax system in the country is to evolve a

coordinated consumption tax system.” This problem has been recognized for

some time, and is clearly in need of correction, as also recommended by the

Eleventh Finance Commission in its report.

3.9.2 Revenue Forecasting and Estimation – Techniques and

Applications

Mr. Graham Glendy, Mr. Gangadhar Shukla and Mr. Robino Sugana

presented paper in Duke University (U.S) on the subject “Revenue

Forecasting and Estimation- Techniques and Applications”.

The study material contains information on Principles of Taxation and Tax

Reforms, Revenue Forecasting, Revenue implications of Excise Tax, Trade

Tax, VAT and Income Tax.

In the said presentation they have defined Taxation as “Taxation is the transfer

of real economic resources from the private sector to the public sector to

finance public sector activities.”

Regarding Excise Tax, the presentation contains useful information about

Economic Incidence of Excise Tax, Effect on revenue when tax rate changes,

Effect on revenue when income increases.

118

3.9.3 Public Finance in Open Economics (Duke University (USA)

Mr. Gangadhar Shukla and Mr. Graham Glendy presented paper in Duke

University on “Public Finance in Open Economics”.

The paper contains information on Public Finance, Principles of Tax Reforms,

Economic Principles of Tax Revenue Tax incidence and Tax Burden,

Taxation of Income and Wealth, Indirect Taxation, Trade Taxes, Taxation of

State owned enterprises, Impact of Inflation, Tax Incentives.

On the Tax Incentives, the paper contains useful information about Cost

Effectiveness of Tax incentives, Impact of Tax incentives, Types of Tax

incentives and Tax Holidays, Tax Neutrality and Neutral Tax Structure.

As regards tax incentives, the resource persons observed that if a country or

region has poor infrastructure and public services, then the loss of tax

revenues from cost ineffective tax incentives can be expected to make this

situation worse by lowering the government revenues needed to improve these

infrastructure and public services. Investment tax incentives may well be self-

defeating.

The authors reproduced the following thoughts of Arnold C. Harberger, in

“Tax Neutrality in investment Incentives”, in Aaron and Boskin (eds).

Economics of Taxation, (1980)

The design of incentives requires a good deal of care. Three aspects of the

design of tax incentives are covered. The first aspect is the cost effectiveness

of a tax incentive. A basic question is whether the tax incentive costs more in

119

forgone tax revenues than the tax revenues gained from the incremental

induced activity? The second feature is the actual impact of the tax incentive

on the effective tax rate of the investor. Given tax incentives are structured in

a number of different ways, it is not always clear by how much the effective

tax rate on the investment income has been reduced. The third design feature

that is investigated here is whether a tax incentive is neutral. A neutral

investment tax incentive picks the next best investment that would otherwise

not have been undertaken. A non-neutral investment incentive may result in

investments with low rates of return of return being made financially feasible

and not some investments with higher rates of return. This arises because the

low-rate-of-return investments get relatively larger incentives than the high-

rate-of-return investments. The loss of output through non-neutrality is clearly

economically inefficient. Neutrality is achieved when an incentive does not

induce new investments with low rates of economic yield, while failing to

induce investments with higher rates of economic yield.

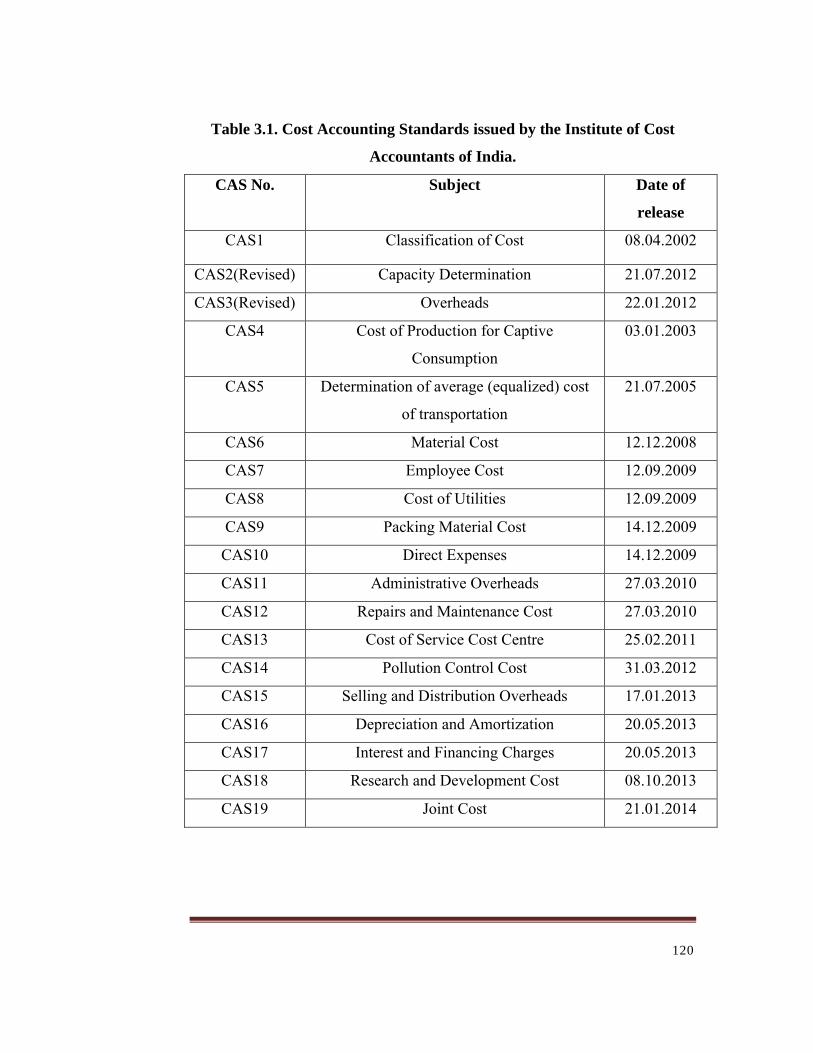

3.10. GACAP and Cost Accounting Standards issued by the Institute of

Cost Accountants of India.

The Institute of Cost Accountants of India is set up under an Act of Parliament

and is an apex body in the area of cost and management accountancy. The

Institute has issued Generally Accepted Cost Accounting Principles and

following 18 Cost Accounting Standards with the objective to bring

uniformity in Cost Accounting.

120

Table 3.1. Cost Accounting Standards issued by the Institute of Cost

Accountants of India.

CAS No. Subject Date of

release

CAS1 Classification of Cost 08.04.2002

CAS2(Revised) Capacity Determination 21.07.2012

CAS3(Revised) Overheads 22.01.2012

CAS4 Cost of Production for Captive

Consumption

03.01.2003

CAS5 Determination of average (equalized) cost

of transportation

21.07.2005

CAS6 Material Cost 12.12.2008

CAS7 Employee Cost 12.09.2009

CAS8 Cost of Utilities 12.09.2009

CAS9 Packing Material Cost 14.12.2009

CAS10 Direct Expenses 14.12.2009

CAS11 Administrative Overheads 27.03.2010

CAS12 Repairs and Maintenance Cost 27.03.2010

CAS13 Cost of Service Cost Centre 25.02.2011

CAS14 Pollution Control Cost 31.03.2012

CAS15 Selling and Distribution Overheads 17.01.2013

CAS16 Depreciation and Amortization 20.05.2013

CAS17 Interest and Financing Charges 20.05.2013

CAS18 Research and Development Cost 08.10.2013

CAS19 Joint Cost 21.01.2014

121

3.11 Cost Accounting Records Rules - 2011

In exercise of the powers conferred by clause (b) of sub-section (1) of section

642 read with clause (d) of sub-section (1) of section 209 of the Companies

Act, 1956 (1 of 1956), The Ministry of Corporate Affairs issued The

Companies (Cost Accounting Records) Rules, 2011 on 3rd Jane 2011.

As per the said Rules, every company, including a foreign company as defined

under section 591 of the Act, which is engaged in the production, processing,

manufacturing, or mining activities and wherein, the aggregate value of net

worth as on the last date of the immediately preceding financial year exceeds

five Crores of rupees; or wherein the aggregate value of the turnover made by

the company from sale or supply of all products or activities during the

immediately preceding financial year exceeds twenty Crores of rupees; or

wherein the company’s equity or debt securities are listed or are in the process

of listing on any stock exchange, whether in India or outside India is required

to maintain cost records as per Generally Accepted Cost Accounting

Principles and Cost Accounting Standards issued by the Institute of Cost

Accountants of India .

These Rules do not apply to a company which is a body corporate governed

by any special Act;

The Rules define the manufacturing, processing, mining and production

activities as per the following.

122

“Manufacturing Activity” includes any act, process or method employed in

relation to -

(i) Transformation of raw materials, components, sub-assemblies, or parts

into semi-finished or finished products; or

(ii) Making, altering, repairing, fabricating, generating, composing,

ornamenting, furnishing, finishing, packing, re-packing, oiling,

washing, cleaning, breaking-up, demolishing, or otherwise treating or

adapting any product with a view to its use, sale, transport, delivery or

disposal; or

(iii) Constructing, reconstructing, reconditioning, servicing, refitting,

repairing, finishing or breaking up of any products. (k) “Mining

Activity” includes any act, process or method employed in relation to

the extraction of ores, minerals, oils, gases or other geological

materials from the earth’s crust, including sea bed or river bed.

“Mining Activity” includes any act, process or method employed in relation to

the extraction of ores, minerals, oils, gases or other geological materials from

the earth’s crust, including sea bed or river bed.

“Processing Activity” includes any act, process, procedure, function,

operation, technique, treatment or method employed in relation to-

(i) Altering the condition or properties of inputs for their use,

consumption, sale, transport, delivery or disposal; or

(ii) Accessioning, arranging, describing, or storing products; or

(iii) Developing, fixing, and washing exposed photographic or

cinematographic film or paper to produce either a negative image or a

positive image; or

123

(iv) Printing, publishing, finishing, perforation, trimming, cutting, or

packaging; or

(v) Pumping oil, gas, water, sewage or any other product; or

(vi) Transforming or transmitting, distributing power or electricity; or

(vii) Harboring, berthing, docking, elevating, lading, stripping, stuffing,

towing, handling, or warehousing products; or

(viii) Preserving or storing any product in cold storage; or

(ix) Constructing, reconstructing, reconditioning, repairing, servicing,

refitting, finishing or demolishing of buildings or structures; or

(x) Farming, feeding, rearing, treating, nursing, caring, and stocking of

living organisms; or

(xi) Telecasting, broadcasting, telecommunicating voice, text, picture,

information, data or knowledge through any mode or medium; or

(xii) Obtaining, compiling, recording, maintaining, transmitting, holding or

using the information or data or knowledge; or

(xiii) Executing instructions in memory to perform some transformation

and/or computation on the data in the computer's memory.

“Production Activity” includes any act, process, or method employed in

relation to -

(i) Transformation of tangible inputs (raw materials, semi-finished goods,

or sub-assemblies) and intangible inputs (ideas, information, know

how) into goods or services; or

(ii) Manufacturing or processing or mining or growing a product for use,

consumption, sale, transport, delivery or disposal; or

(iii) Creation of value or wealth by producing goods or services.

124

The rules provide for maintenance of productwise, unitwise cost records and

annually product groupwise compliance, to be submitted to Ministry of

Corporate Affairs.

“Product” means any tangible or intangible good, material, substance, article,

idea, know-how, method, information, object, service, etc. that is the result of

human, mechanical, industrial, chemical, or natural act, process, procedure,

function, operation, technique, or treatment and is intended for use,

consumption, sale, transport, store, delivery or disposal.

“Product Group” in relation to tangible products means a group of

homogenous and alike products, produced from same raw materials and by

using similar or same production process, having similar physical or chemical

characteristics and common unit of measurement, and having same or similar

usage or application; and in relation to intangible products means a group of

homogenous and alike products or services, produced by using similar or

same process or inputs, having similar characteristics and common unit of

measurement, and having same or similar usage or application.

Following Separate set of rules have been prescribed to the activities or

products.

(a) Cost Accounting Records (Pharmaceutical Industry) Rules, 2011

(b) Cost Accounting Records (Fertilizer Industry) Rules, 2011

(c) Cost Accounting Records (Sugar Industry) Rules, 2011

(d) Cost Accounting Records (Electricity Industry) Rules, 2011

(e) Cost Accounting Records (Petroleum Industry) Rules, 2011

(f) Cost Accounting Records (Telecommunication Industry) Rules, 2011

125

The product groups are based on the classification under Central Excise and

the base for quantitative information is excise records and excise Returns.

Therefore maintenance of cost records helps in tax management to a great

extent.

3.12 The Companies (Cost Audit Report) Rules, 2011.

In exercise of the powers conferred by clause (b) of sub-section (1) of section

642 read with sub-section (4) of section 233B, and sub-section (1) of section

227 of the Companies Act, 1956 (1 of 1956), and in supersession of the Cost

Audit Report Rules, 2001, the Central Government issued The Companies

(Cost Audit Report) Rules, 2011 on 3rd June 2011.

These rules apply to companies in respect of which an audit of the cost

records has been ordered by the Central Government under sub-section (1) of

section 233B of the Act. Accordingly The Ministry of Corporate Affairs have

issued following orders.

Cost Audit Report

The Companies Cost Audit Report Rules 2011, prescribes the Cost Auditor to

submit Cost Audit report alongwith his observations and suggestions and

Annexures to the Central Government in the prescribed form.

The Maintenance of Cost Accounting Records and Cost Audit have been

prescribed in respect of companies engaged in Manufacture; Production,

Processing, and Mining activities vide the Various Cost Accounting Records

Rules 2011 and Cost Audit Report Rules 2011. The activities covered under

Cost Accounting Records Rules and Cost Audit Report Rules are either

126

covered under Central Excise or Service Tax. The entire mechanism of Cost

Accounting Records and Cost Audit is based on the concept of Product

Groupwise reporting.

The product / activity groups have been classified under 267 groups.

Wherever a product is identified under first schedule to Central Excise Tariff

Act 1885, the same has been identified with reference to the 4 digit Chapter

Heading of the product. As per Notes to Annexure to the Compliance Report

under Cost Accounting Records Rules 2011, for produced / manufactured

product groups, the nomenclature as used in the Central Excise Act / Rules is

to be used and for service groups, the nomenclature as used in Finance Act /

service tax rules , as applicable to be used. Thus, the cost compliance is

closely linked with the Central Excise and Service Tax classification. Similar

is the case with Cost Audit.

As per Rule 22(3) of the Central Excise Rules, 2002, every assessee shall, on

demand, make available Cost Audit Reports to the officer empowered under

sub rule (1) or the audit party deputed by the commissioner. Cost Audit

Report is considered as one of the important tool for conducting the Central

Excise Audit , in particular EA 2000, as it provides quantitative and financial

details regarding production, clearance, capacity utilization, input output ratio,

related party transaction, valuation of captively consumed goods.

Due to change in format of information to be given in Schedule 6 to the

Annual Report, the quantitative details are not available in the Annual Report.

Therefore Cost Audit Report is the only authentic document which provides

quantitative as well as financial details regarding production, clearance, stock

etc.

127

The Annexures (Paras) to the Cost Audit Report help the assessee to ensure

tax compliance. It also helps in finding out revenue leakages.

The Annexures (Paras) to the Cost Audit Report contain following

information.

Annexure 1 :-

Annexure 1 contains the general information about the Company and Cost

Auditor.

Annexure 2 :-

The annexure contains information about cost accounting policy adopted by

the Company keeping in view the requirements of the Companies (Cost

Accounting Records) Rules, 2011, the Companies (Cost Audit Report) Rules,

2011, Cost Accounting Standards and its adequacy or otherwise to determine

correctly the cost of production/operation, cost of sales, sales realization and

margin of the product/activity groups under reference separately for each

product/activity group.

The information in this annexure is useful in complying with various

provisions of various Excise / Cenvat Rules such as

1. Treatment on non moving, obsolete goods in accounts:- Rule 3(5B) of the

Cenvat Credit Rules,2004, provides that if inputs or capital goods , before

being put to use , are written off fully or partly or any provision is made in

books of account to write off fully or partially , the manufacturer or

service provider is required to pay an “amount” equal to Cenvat credit

taken in respect of such inputs or capital goods . In case, the company has

128

a policy to write off / down the value of inputs periodically on account of

non moving nature of goods, the reversal of corresponding Cenvat credit

needs to be done.

2. Treatment of R & D Expenses :- as per rule 6 (1) of the Cenvat Credit

Rules, 2004, Cenvat Credit shall not be allowed on such quantity of input

used in relation to the manufacture of exempted goods or for provision of

exempted services. If company is engaged in any research activities,

which has not resulted in manufacture or clearance of excisable goods, and

if the company has availed Cenvat credit on inputs used in research

activities, it needs to be reversed.

3. Methodology for valuation of inter unit / intercompany and related party :-

In case of multi-locational companies, where the partly processed goods

are transferred to other units for further use in manufacture of goods, the

transfer price needs to be worked out as per Rule 8 of the Central Excise

Valuation Rules, 2000. CBE&C has clarified that the cost of production of

the captively consumed goods has to be determined as per Cost

Accounting Standard 4 (CAS4) issued by the Institute of Cost Accountants

of India.

4. Treatment of abnormal and non-recurring costs including classification of

other non-cost items:- the information about abnormal costs on account of

accident, theft etc is useful to verify whether the proportionate Cenvat

credit on the inputs and capital goods damaged / lost has been reversed or

remission of duty has been sought.

129

Annexure 3

The information in this annexure is to be submitted for a Company as a whole.

This Annexure contains following information.

Manufactured product group. The product group is linked with the

nomenclature as per Central Excise Tariff Act 1985

Service Groups – for Service group, nomenclature as per Finance Act /

Service Tax Rules is being used.

Product group wise details of Trading Activities.

Details of other Income

Net Sales (net of taxes and duties) to be specified and coverage of Cost

Audit to be mentioned

The Total Income shown in this annexure should match with the

income shown in the Profit & Loss A/c

The information in this annexure is useful in Tax Compliance in the

following manner –

1. Value reported in this Annexure may be compared with ER1 details.

This may not match with ER1 always because of different methods of

valuations adopted by the assessee, such as duty is paid on MRP, duty

paid under specific duty rate method etc. However, where the duty is

paid on the transaction value as per section 4 of the Central Excise Act

and where there are no stock transfers, the value shown in the said

annexure may be compared with the value shown in ER 1. The

analysis of difference in value shown in ER1 and value shown in this

annexure may help in finding out the mistakes, wrong accounting or

even removal of goods without payment of excise duty.

130

2. Amount shown in this Annexure in respect of service income should

match with the value of taxable services shown in ST3 Returns

submitted by the assessee. Analysis and reasons for difference may

help in finding nonpayment, short payment of service tax.

3. Details of trading activities are useful in verifying whether Cenvat

credit is availed on traded goods if the traded goods are similar to

inputs. Details of traded goods are also useful in verifying ratio used

for reversal of Cenvat credit under Rule 6(3) of the Cenvat Credit

Rules, 2004 since trading is considered as exempted service.

4. Details of other income may help in verifying the applicability of

excise duty, service tax on it.

Annexure 4

This annexure provides following Information, separately for each product

group

Capacity – installed, enhanced during the year, available through

leasing arrangement, loan licenses, third parties to be specified

Actual Production under each category to be given

Analysis of actual production and capacity vis-à-vis in house capacity

utilization can be made in Performance Appraisal Report

Details of stock purchased for trading from indigenous sources and

imports to be given separately.

Production as per excise records to be separately given and

observations on reconciliation to be made in the Audit Report.

131

The information in this annexure is useful in comparing –

1. The details of installed capacity with the information submitted to

Central Excise in ER7 Return. The details of addition /reduction in

installed capacity are useful in verifying the details of addition /

removal of capital goods and payment of excise duty / reversal of

Cenvat credit thereon under Rule 3(5) of the Cenvat Credit Rules

2004.

2. Actual production quantity with production quantity reported in

monthly Returns ER1. The Annexure provides the information in

respect of actual production and production as per excise records. The

reasons for difference in the production quantity as per production

reports and details submitted in ER1 Returns is useful in finding

removal of goods without payment of duty.

3. Details of stock purchased for trading may be useful in verifying

admissibility of Cenvat credit. Details of traded goods also help in

verifying ratio used for reversal of proportionate Cenvat credit under

Rule 6(3) of the Cenvat Credit Rules, 2004.

4. Details of captive consumption may be useful in ascertaining the duty

liability of the goods captively consumed if final product is exempt

from duty.

5. Details of quantity sold may be used in verifying details of quantity of

clearances as per Excise Returns ER1.

132

Annexure 5

Annexure 5 contains details of cost of production, cost of sales, profit / loss on

goods sold. This Annexure is to be submitted separately for each product /

activity group. Proforma and item of cost shown in the proforma can be

modified to meet the requirement of industry / product / activity group without

losing materiality factor. In case company follows Standard Costing System

element of cost to be reflected at actual after adjusting the variances therefore

the information contained in this annexure provides actual cost of production,

cost of sale, sales realization and profit / loss.

Usefulness in Central Excise Compliance

1. In case of goods captively consumed, Cost of Production can be

compared with the same given in CAS4 certificate by the assessee

from time to time. The cost of production reported at line item number

17 of the annexure may be useful in comparing the cost of production

submitted to the excise department. The information may be used to

find out differences on account of inclusion / non inclusion of various

overheads as prescribed in Cost Accounting Standard 4 issued by the

Institute of Cost Accountants of India. The information is useful in

finding out undervaluation of the goods captively consumed and

working of differential duty to be paid on it.

2. The comparison of cost details with the previous year may help in

understanding the changes in cost composition and analyzing the

reasons thereof.

133

Annexure 6

This Annexure contains operating ratio analysis in Tabular Format for each

product group separately. Ratio of operating expenses to cost of sales to be

worked out from following cost element.

1. Material cost

2. Utilities cost

3. Direct employees cost

4. Direct expenses

5. Consumable stores and Spares

6. Repairs and Maintenance cost

7. Depreciation /Amortization Cost

8. Packing Cost

9. Other Expenses

10. Stock Adjustment

11. Production Overheads

12. Administrative Overheads

13. Selling and Distribution Overheads

14. Interest and Financial Charges

The information in this annexure may be used for comparing value addition

and Cenvat / PLA payment ratio.

Annexure 7

The information in this Annexure is to be reported for company as a whole.

The annexure contains information about profit as per cost accounts, various

incomes and expenses not considered for costing and reconciliation of profit

134

as per cost accounts with profit before tax shown in the annual accounts of the

company.

As per generally accepted cost accounting principles (GACAP), income and

expenses that are abnormal in nature or purely financial in nature are not

considered as a part of cost accounts for computation of cost of production

and sales.

The details provided in this annexure may be useful in following:-

1. To ascertain applicability of excise duty / service tax on various other

income accounted in the books of account.

2. The information with respect to profit / loss on sale of capital goods may

be used in verifying applicability of Rule 3(5) of Cenvat Credit Rules,

2004.

Annexure 8

The information in this annexure contains statement of value addition and

distribution of earning for company as a whole. Value addition is to be

computed based on audited financial data and not based on cost data. The

information in this annexure is useful in comparing the ratio of payment of

excise duty from Cenvat credit and PLA payment.

Annexure 9