ribner, kluft & berg, p.c. - decision - 05/20/97 in the...

TRANSCRIPT

RIBNER, KLUFT & BERG, P.C. - DECISION - 05/20/97

In the Matter of RIBNER, KLUFT & BERG, P.C.TAT (E) 93-958 (GC) - DECISIONTAT (E) 93-959 (GC), TAT (E) 93-960 (GC)

NEW YORK CITY TAX APPEALS TRIBUNALAPPEALS DIVISION

GENERAL CORPORATION TAX - ALTHOUGH PETITIONER'S SHAREHOLDERS HAD CEASEDPRACTICING LAW TOGETHER, PETITIONER'S CORPORATE EXISTENCE W AS RETAINED TO FULFILLA RELATED BUSINESS PURPOSE; THE RECEIPT AND DIVISION OF REVENUES FROM REFERRAL OFITS CLIENT BASE AND ITS W ORK IN PROGRESS. ALSO, PETITIONER DID NOT ESTABLISH THAT ITHAD A REGULAR PLACE OF BUSINESS OUTSIDE THE CITY DURING THE TAX YEARS. LASTLY, THEDEPARTMENT CORRECTLY INCLUDED AMOUNTS PAID TO THE ESTATE OF ONE OF THESHAREHOLDERS IN THE ALTERNATIVE TAX BASE AS SALARY AND OTHER COMPENSATION PAIDTO A CORPORATION'S STOCKHOLDERS OW NING IN EXCESS OF FIVE PERCENT OF ITS ISSUEDCAPITAL STOCK.MAY 20, 1997

By letter dated November 21, 1996, the Tribunal offered1

Petitioner the opportunity to request that the oral argument berescheduled; Petitioner did not respond to such letter.

New York City Tax Appeals Tribunal-----------------------------------x

:In the Matter of :

: DECISIONRIBNER, KLUFT & BERGER, P.C. :

: TAT (E) 93-958 (GC): TAT (E) 93-959 (GC)

Petitioner. : TAT (E) 93-960 (GC)::

-----------------------------------x

Ribner, Kluft & Berger, P.C. ("Petitioner") filed an Exception

to that part of an Administrative Law Judge ("ALJ") Determination,

dated June 21, 1995, which sustained a general corporation tax

("GCT") deficiency asserted by the New York City Department of

Finance (the "Department") for the fiscal years ended July 31, 1986

and July 31, 1987 and the short period ended December 31, 1987

(collectively, the "Tax Years").

Petitioner appeared by Michael Strauss, C.P.A. of Strauss &

Comas, P.C. The Commissioner of Finance of the City of New York

("Commissioner" or "Respondent") appeared by David M. Steiner,

Esq., Assistant Corporation Counsel, Law Department of the City of

New York. Both parties filed briefs and Petitioner's request for

oral argument was granted. However, no oral argument took place

because Petitioner's representative did not appear at the scheduled

date and time.1

A hearing was held before Conferee Melissa S. Siegel of the

Department's former Hearings Bureau. Pursuant to the provisions of

In this decision, the ALJ's findings of fact have, for the2

most part, been adopted. Where necessary, such findings have beenamplified and/or paraphrased. Petitioner did not take specificexception to any of the ALJ's enumerated findings of fact but didtake exception to certain of her conclusions of law dependent onsuch facts. To the extent that it could be argued that Petitionerintended to object to a finding of fact, Petitioner did not referto, nor can we find, any document or testimony in the record whichsupported such change. Any finding of fact that we expresslyrejected has been so noted.

-2-

sections 168 through 172 of the City Charter as amended by act of

the New York State ("State") Legislature on June 28, 1992, Ch. 808,

Laws 1992, section 140, this case, which was pending before the

Hearings Bureau on October 1, 1992, was transferred to the Tax

Appeals Tribunal for determination. Administrative Law Judge

Marlene F. Schwartz was assigned the case and issued the

Determination based on her review of the record and the briefs

filed by the parties.

Petitioner is a State corporation, which was formed in 1976 to

practice law as a Professional Service Corporation under Article 15

of the State Business Corporation Law ("BCL"). Its shareholders2

were Paul Ribner, Jerome Kluft and Lawrence Berger, each of whom

was an attorney and each of whom held one third of Petitioner's

outstanding shares.

Petitioner's law practice consisted primarily of obtaining

reductions in New York City ("City") real estate tax assessments

(i.e., Certiorari Law) and, to a significantly lesser extent,

obtaining real property tax exemptions for certain clients.

Petitioner represented its clients, who owned real property located

in the City, before the City Tax Commission, in proceedings for

reviews of tentative real estate tax assessments, and before the

State Supreme Court (in counties in the City) in proceedings to

obtain judicial review of decisions of the City Tax Commission

under Article 7 of the Real Property Tax Law ("Article 7

Proceedings"). In ll Article 7 Proceedings, the City was

Based on our review of the record, we have revised the3

amounts stated by the ALJ to be the "cash assets" per the balancesheets.

-3-

represented by attorneys from the City's Law Department.

In the fall of 1983, Messrs. Ribner, Kluft and Berger decided

to cease actively practicing law together. Petitioner's office

lease at 210 East 86th Street in Manhattan terminated on December

31, 1983 and the office was closed. Petitioner did not own or lease

any real property after December 31, 1983.

Petitioner was not formally dissolved. It did not file a

certificate of dissolution with the New York State Department of

State.

Petitioner filed a Federal Form 1120S, U.S. Income Tax Return

for an S Corporation; State Form CT-3S, Corporation Information

Report; and City Form NYC-4S, GCT Return (collectively, the

"Returns") for each of the Tax Years. Petitioner paid the minimum

GCT of $125 for each of the Tax Years. On the Returns, Petitioner

designated its business as "legal services." The balance sheets

thereon showed cash assets ranging from $37,000 to $9,000 and

unspecified "other assets" of $10,904. None of the Returns was3

designated a "final return."

When Petitioner's shareholders ceased practicing law together,

Messrs. Ribner and Kluft began a real estate investment venture at

an office located at 157 East 86th Street in Manhattan. Mr. Berger

formed his own firm, Lawrence J. Berger, P.C. ("Berger, P.C."), in

November of 1983, through which he practiced Certiorari Law at an

office located at 270 Madison Avenue in Manhattan.

Mr. Kluft testified that Mr. Ribner died in April of 1985.4

On Petitioner's Form CT-3S for its fiscal year ended July 31, 1986,Petitioner indicated that Mr. Ribner was a stockholder until April13, 1986 and that the Estate was a stockholder beginning on April14, 1986. On its Form 1120S for that same fiscal year Petitioner'sordinary income (loss) from federal Form 1120S was allocated onethird each to Mr. Kluft and Mr. Berger. The remaining one thirdwas divided between Mr. Ribner and the Estate in proportion to theamount of time each was listed as a stockholder during that fiscalyear. During the following two tax years, one third ofPetitioner's ordinary income (loss) was allocated to the Estate.However, we agree with the ALJ that, as the inconsistency in thedate of Mr. Ribner's death is immaterial to the resolution of thiscase, it need not be decided.

We have added this statement to the findings of fact. The5

ALJ came to this same conclusion in her Determination at page 26and Petitioner has not disputed such conclusion.

-4-

Mr. Berger continued to own one third of Petitioner's shares.

These shares were never owned by Berger, P.C. Mr. Ribner became ill

in February, 1984 and died in April 1985 or 1986. On the Returns

for the Tax Years, Mr. Ribner's estate (the "Estate") was listed as

the owner of 33 and 1/3rd percent of Petitioner's shares beginning

in April, 1986. Petitioner did not comply with the statutory4

requirement of §1510 of the Business Corporation Law (the "BCL")

that it redeem the Estate's shares within six months after the

appointment of the Estate's legal representative.5

The address shown on the Returns for the fiscal year ended July

31, 1986 was 157 East 86th Street, the address of Messrs. Ribner and

Kluft's real estate investment venture. For the subsequent two tax

years, the address on the Returns was in care of Mr. Kluft at 500

East 88th Street in Manhattan.

City real estate tax assessments are made annually for each6

fiscal year beginning July 1st. The fiscal year beginning July 1,1983 is generally referred to as the "83-84 tax year." In theALJ's Determination, the term "Property Tax Year" refers to a Cityfiscal year for real estate tax assessment purposes; while the term"Tax Year" refers to Petitioner's year for purposes of filing itsReturns. In order to avoid confusion, we have adopted such termsand definitions for purposes of this Decision.

-5-

In December of 1983, when Petitioner closed its office, it had

an inventory of pending cases in which Petitions for Article 7

Proceedings ("Article 7 Petitions") had been filed either during

1983 for the Property Tax Year 83-84 or in a previous year for a

prior Property Tax Year. In general, certiorari attorneys are paid6

on a contingency fee basis; i.e., they receive a percentage of any

reduction they obtain in a real estate tax assessment ("Reduction").

Petitioner considered a case on which it was the attorney of record

to be its "property" since it had an interest in any fee that

resulted from an eventual Reduction.

Mr. Kluft testified that, when an attorney refers a client to

a certiorari attorney, it is customary for the certiorari attorney

who receives the referral to remit a portion of any fee ultimately

received (the "Referral Fee") to the attorney making the referral

(the "Referring Attorney"). In some cases, the certiorari attorney

receives the entire legal fee, retains his/her portion, and pays

over the Referral Fee to the Referring Attorney. In other cases,

the certiorari attorney remits the entire fee to the Referring

Attorney who keeps his/her Referral Fee and returns the balance to

the certiorari attorney. Since many property owners contest their

real property tax assessments annually, a referral is a valuable

source of business not only for the work in progress during a

particular Property Tax Year but also for the potential future work

it can engender.

We have omitted Finding of Fact No. 14 of the ALJ's7

Determination, as it is immaterial to our decision. Finding ofFact No. 14 read as follows:

Mr. Kluft testified that it was thepractice in the industry that ReferringAttorneys need not perform any servicesdirectly related to obtaining the Reduction toshare in the fee received by the ReferralAttorney. However, Mr. Kluft did not explainwhy this practice did not violate DR 2-107 ofthe Code of Professional Responsibility as ineffect at that time.

-6-

Mr. Kluft testified that Petitioner's work in progress had no

immediate value, since a fee is paid only upon the completion of a

case in which a Reduction is obtained. After Petitioner

discontinued the active practice of law, its inventory of cases had

to be referred elsewhere. Naturally, Petitioner wished to ensure

that it would eventually be compensated for work already performed

and for referring work in progress to another Certiorari Law firm.7

Petitioner wanted to have the ability to monitor the progress

of cases it referred to other firms to ensure that it received the

Referral Fees to which it was entitled when the cases were

completed. Petitioner also needed to track the precise source of

each Referral Fee, since the fees were not divided among

Petitioner's stockholders on a pro rata basis. Rather, the way

each Referral Fee was divided, depended upon which case generated

that fee.

Finding of Fact No. 16 of the ALJ's Determination has been8

modified to reflect the fact that the statements made about theReferral Agreement are based solely on the testimony ofPetitioner's witnesses.

-7-

The testimony indicates that Petitioner entered into an

agreement (the "Referral Agreement") with Berger, P.C. under which

Petitioner referred its cases to Berger, P.C. and Berger, P.C.

remitted the entire legal fee earned for each completed case to

Petitioner for deposit in a checking account maintained by

Petitioner specifically for this purpose. Petitioner then disbursed

each fee according to the Referral Agreement. According to the

testimony, the Referral Agreement was in writing and had been

executed by the parties involved, however, the Referral Agreement

is not in the record. The Department requested that Petitioner

produce a copy of the Referral Agreement for the record, but

Petitioner failed to do so. Mr. Berger testified that he was unable

to locate a copy of the executed Referral Agreement and that he had

been operating from an unsigned copy, but even this unsigned copy

was not entered into the record by Petitioner. 8

During the Tax Years, Berger, P.C. received total fees of

approximately $1,500,000 generated from the clients referred to it

by Petitioner. While Berger, P.C. issued bills to these clients in

its own name, pursuant to the Referral Agreement, Berger, P.C.

remitted the entire fee earned for each completed case to

Petitioner. Petitioner then disbursed the fee to the Estate, to Mr.

Kluft, and/or to Berger, P.C. (but not to Mr. Berger) by drawing

checks on Petitioner's checking account. Checks were written

virtually every month during the Tax Years, generally on several

different days during each month.

-8-

Petitioner included the full amount of the (approximately

$1,500,000) fees remitted by Berger, P.C. as income in Petitioner's

Returns for the Tax Years. Approximately $700,000 of this amount

was returned by Petitioner to Berger, P.C. for work actually done

by Berger, P.C. In turn, Berger, P.C. paid a salary to Mr. Berger.

Petitioner paid none of these fees directly to Mr. Berger.

Virtually the entire balance of Petitioner's fee income was

disbursed to the Estate and Mr. Kluft. Petitioner deducted all

these disbursements on its Returns as "referral and legal fees."

Since Petitioner's GCT Returns reflected no net income, Petitioner

paid the minimum GCT of $125 for each of the Tax Years.

Although Petitioner admits in its post-hearing brief that it

conducted bookkeeping activities in order to track the Referral Fees

paid by Berger, P.C., the record does not indicate who performed

this activity or where the activity was conducted.

Of the approximately $1,500,000 in fees generated from

Petitioner's clients during the Tax Years, about $400,000

represented fees for work begun by Petitioner with respect to the

Property Tax Year 83-84 and prior Property Tax Years. The remaining

amount of approximately $1,100,000 represented fees for work done

entirely by Berger, P.C., primarily with respect to Property Tax

years 84-85, 85-86, and 86-87.

-9-

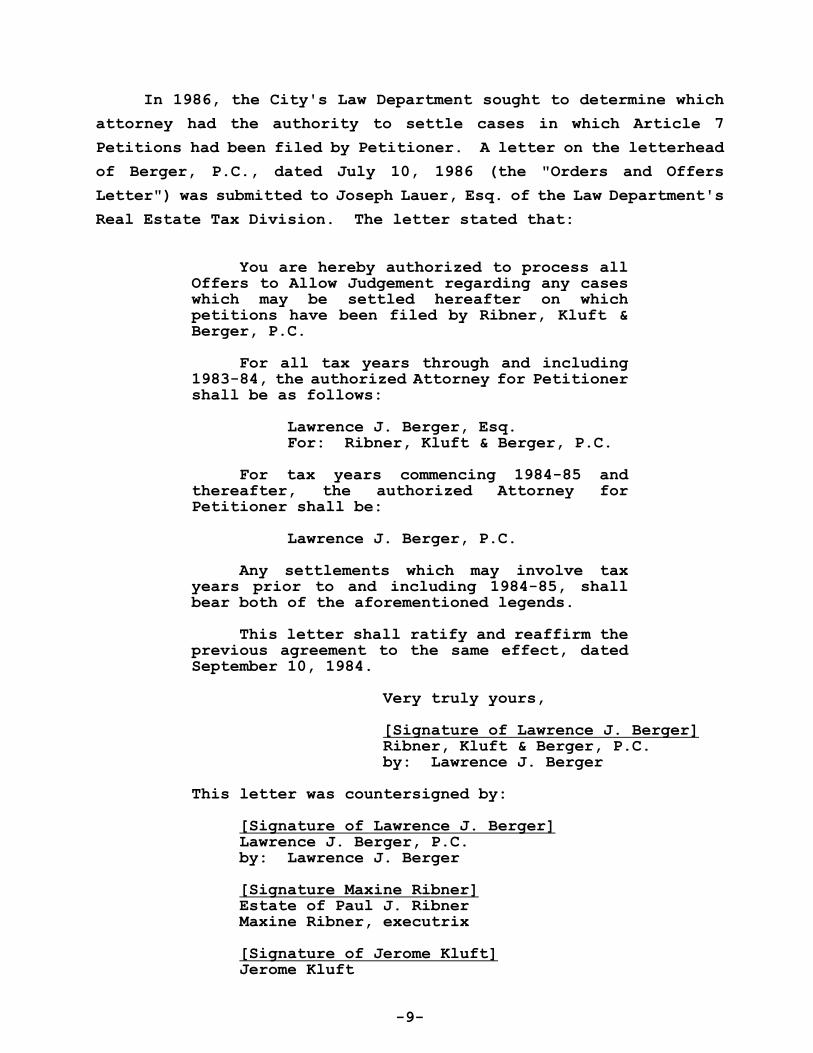

In 1986, the City's Law Department sought to determine which

attorney had the authority to settle cases in which Article 7

Petitions had been filed by Petitioner. A letter on the letterhead

of Berger, P.C., dated July 10, 1986 (the "Orders and Offers

Letter") was submitted to Joseph Lauer, Esq. of the Law Department's

Real Estate Tax Division. The letter stated that:

You are hereby authorized to process allOffers to Allow Judgement regarding any caseswhich may be settled hereafter on whichpetitions have been filed by Ribner, Kluft &Berger, P.C.

For all tax years through and including1983-84, the authorized Attorney for Petitionershall be as follows:

Lawrence J. Berger, Esq.For: Ribner, Kluft & Berger, P.C.

For tax years commencing 1984-85 andthereafter, the authorized Attorney forPetitioner shall be:

Lawrence J. Berger, P.C.

Any settlements which may involve taxyears prior to and including 1984-85, shallbear both of the aforementioned legends.

This letter shall ratify and reaffirm theprevious agreement to the same effect, datedSeptember 10, 1984.

Very truly yours,

[Signature of Lawrence J. Berger]Ribner, Kluft & Berger, P.C.by: Lawrence J. Berger

This letter was countersigned by:

[Signature of Lawrence J. Berger]Lawrence J. Berger, P.C.

by: Lawrence J. Berger

[Signature Maxine Ribner] Estate of Paul J. Ribner

Maxine Ribner, executrix

[Signature of Jerome Kluft]Jerome Kluft

Berger, P.C. filed Forms NYC-4S, GCT Returns, for its fiscal9

years ended January 31, 1986 and January 31, 1987 and the shortperiod ended December 31, 1987 (the "Berger Returns"). Berger,P.C. included the $700,000 returned to it by Petitioner in itsincome on the Berger Returns and paid GCT on the alternative taxbase of "income plus compensation paid to officers and more thanfive percent stockholders."

We have added this paragraph to the findings of fact. The10

ALJ included these two sentences in her Determination at page 15and Petitioner has not taken exception to such statement.

-10-

During the fiscal year ended July 31, 1987, Petitioner paid a

$300 Referral Fee to the firm of Katz, Weisberg. Katz, Weisberg was

never an officer or stockholder of Petitioner.9

Petitioner did not refer any of its tax exemption cases to

Berger, P.C. Any of those cases still in progress on December 31,

1983 were apparently completed by Mr. Ribner prior to his illness

or by Mr. Kluft sometime thereafter.

The record indicates that well after the time Petitioner claims

to have gone out of business, it was continuing to file Article 7

Petitions for its clients. The Orders and Offers Letter dated July

10, 1986, that was submitted to the City's Law Department,

specifically addressed, in part, pending cases for the Property Tax

Years 84-85 and thereafter, in which petitions had been filed by

Petitioner.10

There is no indication in the record that any work was done by

or on behalf of Petitioner at a place of business outside the City

during the Tax Years.

Interest was computed to December 15, 1989.11

The Notice of Determination stated that the penalty was for12

late payment.

This Petition is stamped received June 12, 1990 by the13

Department's Adjustment and Review Section. However, the envelopein which the Petition was mailed is postmarked March 12, 1990 bythe United States Postal Service. This envelope is stampedreceived by the Department's Bureau of Tax Collection on March 14,1990. The file also contains additional photocopies of thisPetition which were stamped received by the Department's Office ofLegal Affairs on March 19, 1990. No explanation was provided forthe way in which the Petition was processed once it reached theDepartment. Based on the March 12, 1990 postmark on the envelope,the ALJ found that the Petition was timely filed under §11-680(2)of the New York City Administrative Code and the applicableregulations which are found at 19 RCNY §17-01(a)(2) and we adoptsuch conclusion for purposes of this Decision.

-11-

There is no information in the record regarding the amount of

time, if any, that Mr. Kluft performed work outside the City for

Petitioner during the Tax Years.

The Department issued a Notice of Determination, dated December

15, 1989, to Petitioner asserting the following GCT deficiency for

the fiscal year ended July 31, 1986:

Principal $12,005.67Interest 3,939.1211

Penalty 180.0912

Total $16,124.88

On March 12, 1990, Petitioner timely filed a Petition (which was

given the designation TAT (H) 93-959(GC)) for redetermination of the

deficiency for the fiscal year ended July 31, 1986.13

Interest was computed to April 30, 1990.14

This Petition was not offered into evidence by the Department15

although it was in the file provided to the Administrative LawJudge Division by the Hearings Bureau. Rather, the Departmentoffered into evidence and the Conferee accepted into evidence aPetition dated June 29, 1989 (which was given the designation TAT(H) 92-440 (GC)) which purports to be in response to a Notice ofDetermination issued to Petitioner dated April 3, 1984 (sic) in theamount of $26,048.32 for the fiscal year ended July 31, 1987. TheNotice of Determination dated April 3, 1984 (sic) is not in therecord. By letter dated April 7, 1995, the Department advisedJudge Schwartz that it had not located such a Notice. JudgeSchwartz stated in footnote 7 of her Determination, that, "...unless a written objection to the proposed dismissal is received bythe Tax Appeals Tribunal on or before July 21, 1995, the Petitiondated June 29, 1989 and designated TAT (H) 92-440(GC) will bedismissed as being premature (since it is not in response to aNotice of Determination) and duplicative of the Petition designatedTAT(H) 93-960(GC) which was filed in response to the subsequentlyissued Notice of Determination. Subsequently, a DismissalDetermination/Order dated August 23, 1995 was issued by JudgeSchwartz dismissing the Petition filed with respect to TAT(H) 92-440(GC).

-12-

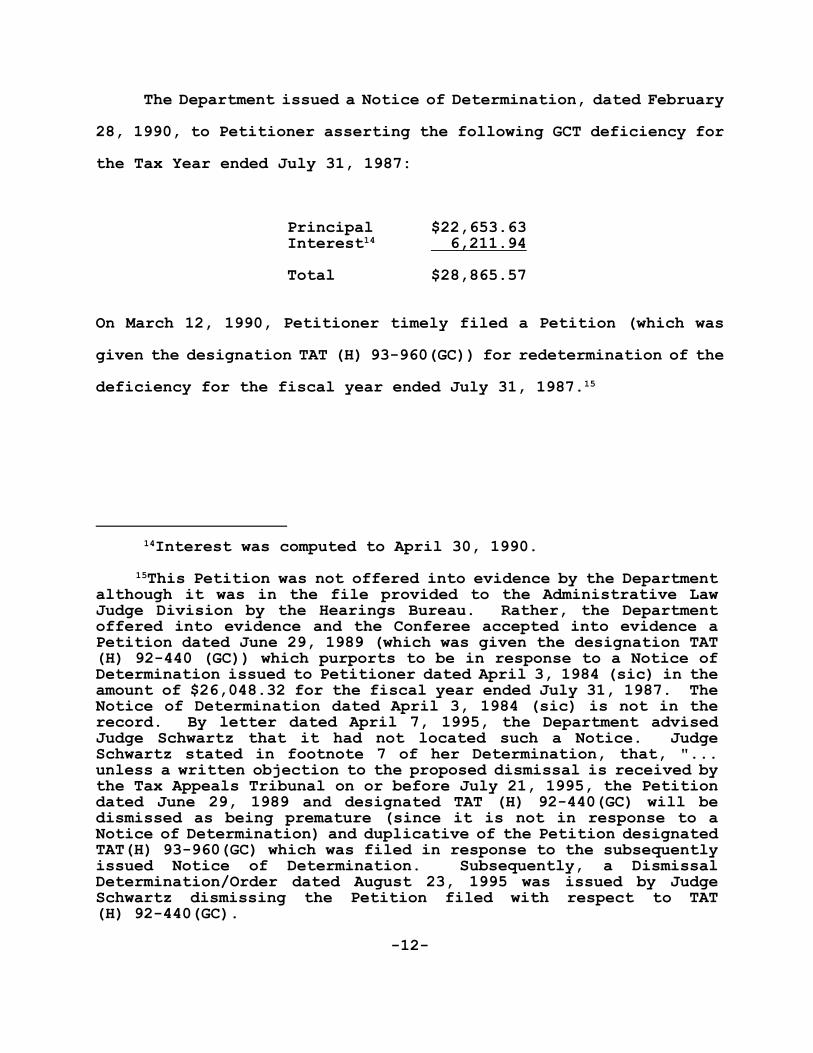

The Department issued a Notice of Determination, dated February

28, 1990, to Petitioner asserting the following GCT deficiency for

the Tax Year ended July 31, 1987:

Principal $22,653.63Interest 6,211.9414

Total $28,865.57

On March 12, 1990, Petitioner timely filed a Petition (which was

given the designation TAT (H) 93-960(GC)) for redetermination of the

deficiency for the fiscal year ended July 31, 1987.15

Interest Computed to September 6, 1989.16

Pursuant to the Notice of Determination, the Penalty was17

imposed for late payment.

This Petition was dated "9/5/89." This appears to be an18

error since the Petition responds to a Notice of Determinationdated September 6, 1989.

-13-

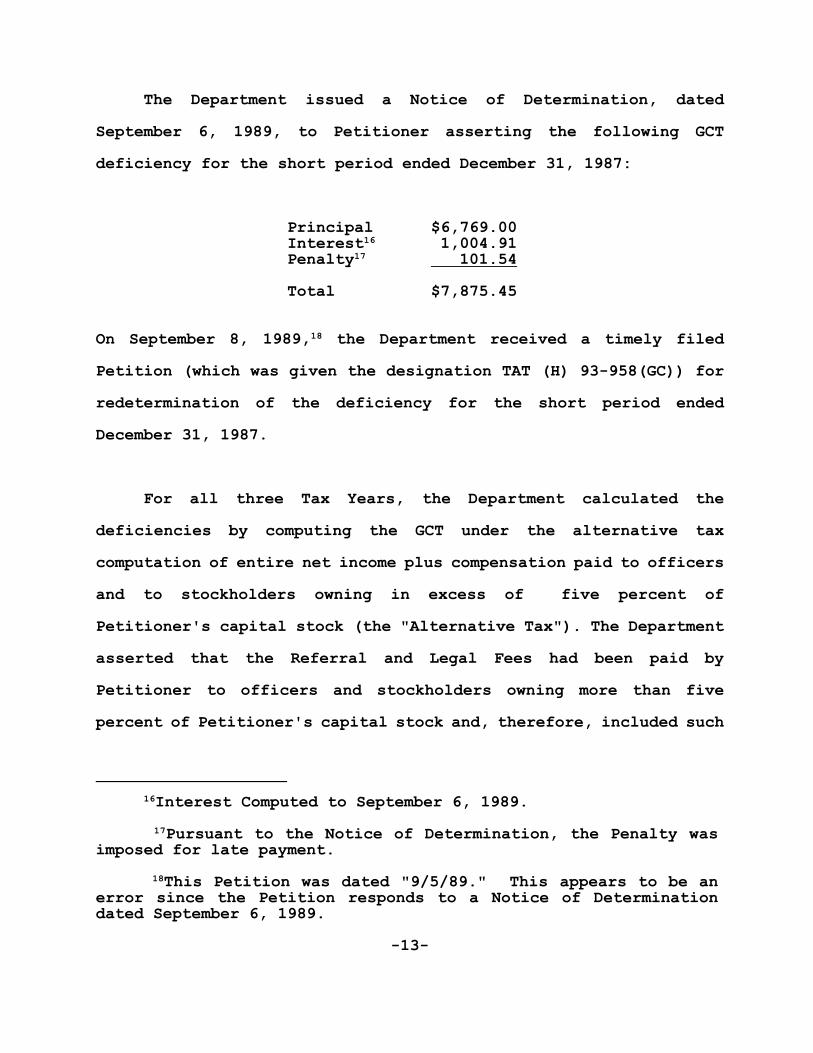

The Department issued a Notice of Determination, dated

September 6, 1989, to Petitioner asserting the following GCT

deficiency for the short period ended December 31, 1987:

Principal $6,769.00Interest 1,004.9116

Penalty 101.5417

Total $7,875.45

On September 8, 1989, the Department received a timely filed18

Petition (which was given the designation TAT (H) 93-958(GC)) for

redetermination of the deficiency for the short period ended

December 31, 1987.

For all three Tax Years, the Department calculated the

deficiencies by computing the GCT under the alternative tax

computation of entire net income plus compensation paid to officers

and to stockholders owning in excess of five percent of

Petitioner's capital stock (the "Alternative Tax"). The Department

asserted that the Referral and Legal Fees had been paid by

Petitioner to officers and stockholders owning more than five

percent of Petitioner's capital stock and, therefore, included such

We have modified the ALJ's Finding of Fact No. 33 to19

accurately reflect the record.

-14-

amounts in the computation of the Alternative Tax base. In its19

brief, however, the Department conceded that it should not have

treated payments made to Berger, P.C. as payments to an officer or

stockholder for purposes of computing the Alternative Tax base.

At the hearing, Petitioner asserted that it ceased doing

business in the City in December, 1983. Petitioner contended that

its activities in the City during the Tax Years were limited to

maintaining a bank account and certain bookkeeping records and that

these activities were insufficient to constitute "doing business"

within the meaning of §11-603.1 of the New York City Administrative

Code (the "Code"). Petitioner claimed that it merely acted as

nominee, for purposes of accounting for various fees due the

Estate, Jerome Kluft, and Berger, P.C. In the alternative,

Petitioner asserted that if it is deemed to have been doing

business during the Tax Years, such business was conducted from

Rockland County, New York and that it should be permitted to

apportion its income within and without the City based solely on

the amount of time actually spent within and without the City by

Mr. Kluft on its activities. Petitioner also asserted that, under

section 1507 of the BCL, only attorneys admitted to practice in the

State may own shares in Petitioner and vote on corporate matters.

Since the Estate was not an attorney admitted to practice in the

State, Petitioner argued that the Estate could not be an officer or

-15-

stockholder of Petitioner for purposes of the Alternative Tax.

Thus, Petitioner claimed that if it is subject to the GCT, payments

to the Estate should not be added back in computing the Alternative

Tax base.

In response, the Department asserted that Petitioner continued

to carry on business in the City during the Tax Years. The

Department contended that Petitioner may not allocate its business

income within and without the City because Petitioner failed to

prove the existence of any regular place of business outside the

City during the Tax Years. The Department also asserted that,

since the Estate owned the right to share in Petitioner's profits

and to participate in its dissolution or liquidation, the Estate

was a stockholder for purposes of computing the Alternative Tax

base.

In her Determination, the ALJ concluded that:

(1) Petitioner was doing business in a corporate capacity in

the City during the Tax Years, within the meaning of the GCT.

Although Petitioner claimed that it ceased doing business at the

end of 1983, the ALJ determined that the record did not support

such assertion. Petitioner did not liquidate and dissolve at the

end of 1983 but rather retained its corporate existence to fulfill

a related business purpose (the receipt and division of revenues

from referral of its client base and its work in progress) and even

-16-

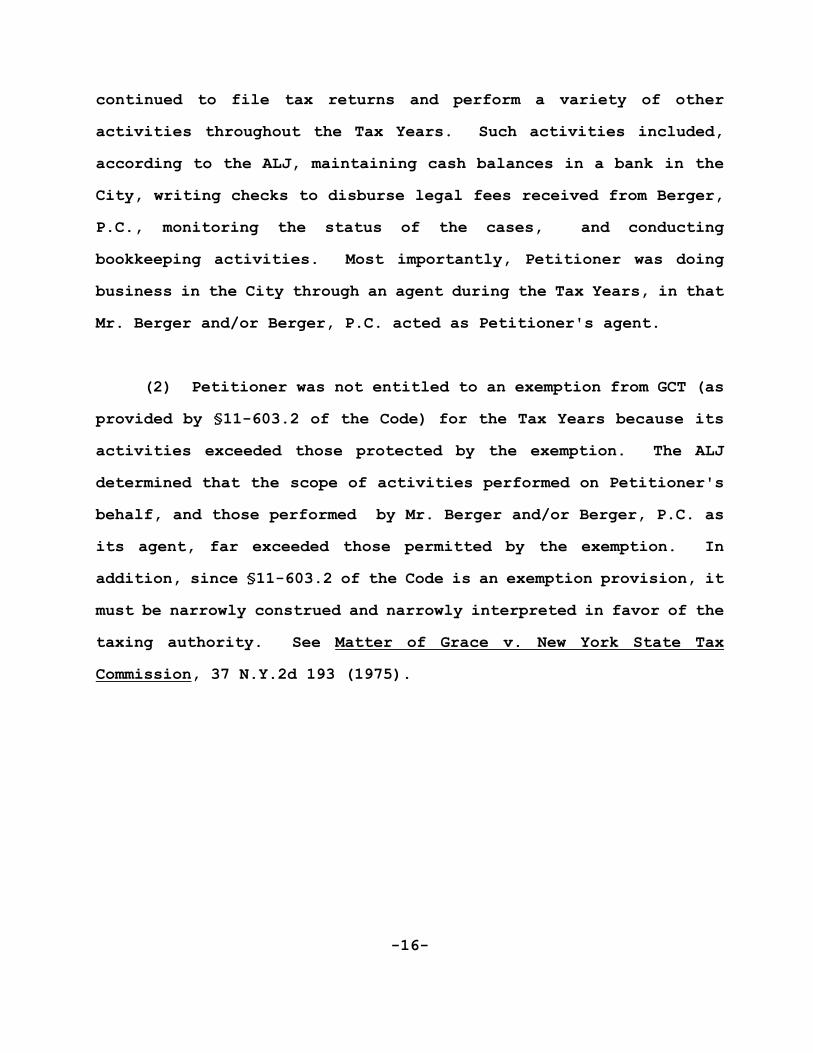

continued to file tax returns and perform a variety of other

activities throughout the Tax Years. Such activities included,

according to the ALJ, maintaining cash balances in a bank in the

City, writing checks to disburse legal fees received from Berger,

P.C., monitoring the status of the cases, and conducting

bookkeeping activities. Most importantly, Petitioner was doing

business in the City through an agent during the Tax Years, in that

Mr. Berger and/or Berger, P.C. acted as Petitioner's agent.

(2) Petitioner was not entitled to an exemption from GCT (as

provided by §11-603.2 of the Code) for the Tax Years because its

activities exceeded those protected by the exemption. The ALJ

determined that the scope of activities performed on Petitioner's

behalf, and those performed by Mr. Berger and/or Berger, P.C. as

its agent, far exceeded those permitted by the exemption. In

addition, since §11-603.2 of the Code is an exemption provision, it

must be narrowly construed and narrowly interpreted in favor of the

taxing authority. See Matter of Grace v. New York State Tax

Commission, 37 N.Y.2d 193 (1975).

-17-

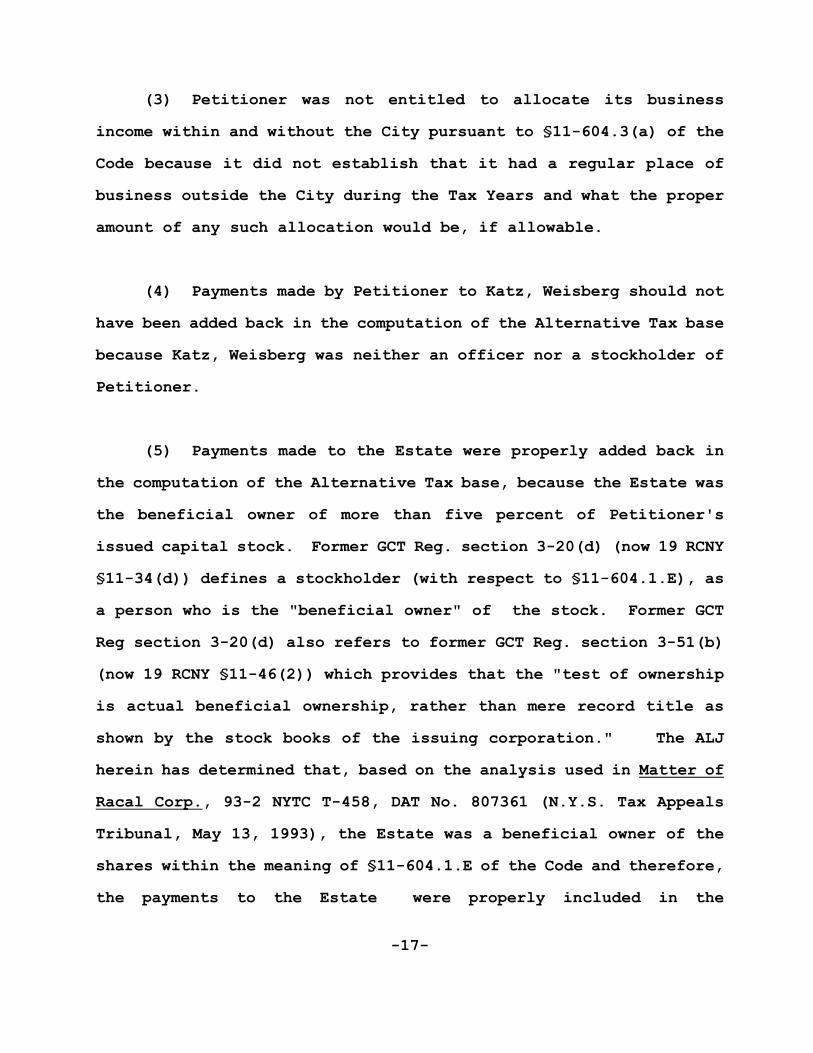

(3) Petitioner was not entitled to allocate its business

income within and without the City pursuant to §11-604.3(a) of the

Code because it did not establish that it had a regular place of

business outside the City during the Tax Years and what the proper

amount of any such allocation would be, if allowable.

(4) Payments made by Petitioner to Katz, Weisberg should not

have been added back in the computation of the Alternative Tax base

because Katz, Weisberg was neither an officer nor a stockholder of

Petitioner.

(5) Payments made to the Estate were properly added back in

the computation of the Alternative Tax base, because the Estate was

the beneficial owner of more than five percent of Petitioner's

issued capital stock. Former GCT Reg. section 3-20(d) (now 19 RCNY

§11-34(d)) defines a stockholder (with respect to §11-604.1.E), as

a person who is the "beneficial owner" of the stock. Former GCT

Reg section 3-20(d) also refers to former GCT Reg. section 3-51(b)

(now 19 RCNY §11-46(2)) which provides that the "test of ownership

is actual beneficial ownership, rather than mere record title as

shown by the stock books of the issuing corporation." The ALJ

herein has determined that, based on the analysis used in Matter of

Racal Corp., 93-2 NYTC T-458, DAT No. 807361 (N.Y.S. Tax Appeals

Tribunal, May 13, 1993), the Estate was a beneficial owner of the

shares within the meaning of §11-604.1.E of the Code and therefore,

the payments to the Estate were properly included in the

In Matter of Racal Corp., 93-2 NYTC T-458, DAT No. 80736120

(N.Y.S. Tax Appeals Tribunal, May 13, 1993), the State Tax AppealsTribunal construed provisions of 20 NYCRR section 3-6.2 (a part ofthe State's Corporate Franchise Tax regulations). Such regulations(prior to their subsequent amendment) were virtually identical to19 RCNY section 11-46. Racal Corp. dealt with whether a secondtier subsidiary could be a "subsidiary" under 20 NYCRR section 3-6.2 for purposes of excluding interest on subsidiary capital. Inreaching its decision, the State Tax Appeals Tribunal addressed thequestion of what constituted "beneficial ownership" under thatregulation.

Although there are two penalties computed at the rate of one-21

half of one percent for each month which are applicable to the GCT(§11-676.1(b) and §11-676.1(c) of the Code), Respondent did nottake exception to the ALJ's conclusion. Therefore, the penaltyissue is not before us.

-18-

Alternative Tax base.20

(6) No penalties should be imposed in this matter because the

record did not indicate why they were imposed. Since there was no

penalty designated a "late payment" penalty and no penalty that was

computed at a rate that would generate an amount of one and one half

percent of the principal tax deficiency, the ALJ abated the

penalties asserted for the fiscal year ended July 31, 1986 and the

short period ended December 31, 1987.21

Petitioner has taken the following specific exceptions to the

conclusions of the ALJ:

(a) Petitioner denies doing business in the City during the

Tax Years. Petitioner contends that its substantial activity in

the City ceased in December of 1983 when it closed its office and

that as there was no corporate location in the City and no

-19-

corporate activity was performed within the City, there was no nexus

for GCT purposes. Moreover, Petitioner asserts that it is

exempt from GCT as any activity it did engage in, is protected

activity. In addition, Petitioner asserts that, pursuant to the

Referral Agreement, it retained an independent contractor, Berger,

P.C.: (1) to monitor its ongoing cases; (2) to report to

Petitioner on the progress being made on the cases; and (3) to pay

over funds received. Petitioner argues that the existence of a

professional relationship between client and attorney, as in this

case, cannot be extended to mean that nexus is created whenever an

attorney is retained.

(b) Petitioner claims the right to allocate its business

income within and without the City. On exception, Petitioner

contends that if it is deemed to be doing business in the City, it

should be permitted to allocate its business income within and

without the City. Petitioner states that the ALJ determined that

services were performed by Petitioner to generate the fee income.

Petitioner argues that such services as were performed by

Petitioner, were limited to the initial referral and subsequent

follow-up on any case and that such services could only be

performed by Mr. Kluft from his office in Rockland County.

Petitioner contends that, as Mr. Kluft performed these services

outside the City, "equity requires that the location of the

services constitutes a place of business outside the City" for

purposes of allocating Petitioner's income.

-20-

(c) Petitioner maintains that, if it was subject to the GCT

at all, payments made to the Estate were improperly added back in

computing the Alternative Tax base. Petitioner asserts that a

review of the powers possessed by the Estate leads to the

conclusion that these administrative powers do not rise to the

level of beneficial ownership. Petitioner contends that Racal

Corp. is distinguishable from the facts in this case since, in

Racal Corp., the taxpayers controlled every incident of ownership

over the second tier subsidiaries.

In response, the Commissioner contends that the Tribunal

should affirm the ALJ's Determination.

Respondent asserts that the ALJ was more than justified in

concluding that Mr. Berger and/or Berger, P.C. was Petitioner's

agent, rather than an independent contractor, and that Petitioner

was doing business through its agent. In addition, Respondent

contends, Petitioner itself engaged in numerous activities during

the Tax Years, never dissolved and continued its corporate

existence, filed tax returns reporting substantial sums of income

and indicated, in such returns, that it was in the business of

practicing law.

-21-

In addition, regarding Petitioner's contention that it should

be permitted to allocate its business income outside the City,

Respondent contends that the record is devoid of evidence of a

regular place of business outside the City and that Petitioner has

submitted no evidence as to what work was done outside the City.

Lastly, with respect to the inclusion of payments made to the

Estate in the Alternative Tax base, Respondent asserts that the

Estate was a "stockholder," (within the meaning of §11-604.1.E of

the Code), owning in excess of five percent of Petitioner's stock.

Respondent agrees with Petitioner: (1) that pursuant to §1507 of

the BCL, a professional services corporation, such as Petitioner,

may issue shares only to those authorized to practice the

profession, and; (2) that §1511 of the BCL prohibits the transfer

of shares by a shareholder in a professional service corporation to

anyone not authorized to practice the profession. However,

Respondent argues that §1511 of the BCL specifically allows

transfers of interest in a professional service corporation by

operation of law. Therefore, Respondent asserts, the Estate became

the beneficial owner of one third of Petitioner's shares upon the

transfer of such shares, and continued as such by reason of

Petitioner's failure to redeem the shares, within six months after

the appointment of an executor, pursuant to §1510 of the BCL.

Although 19 RCNY §11-03(b) was not promulgated until after22

the Tax Years, identical language was contained in InformationBulletin Number 2-A, section 3(a) that was issued in August, 1973.Since 19 RCNY §11-03(b) merely restates a long-standing Departmentpolicy, we agree with the ALJ that it is proper to give itretroactive effect. Varrington Corp. v. City of New YorkDepartment of Finance, 85 N.Y.2d 28 (1995).

-22-

For the reasons set forth below, we affirm the ALJ's

Determination.

Section 11-603.1 of the Code imposes the GCT on the privilege

of "doing business ... in the city in a corporate or organized

capacity ...." The term "doing business" is expansively defined

under 19 RCNY §11-03(b)(1) to include "all activities that occupy

the time or labor of people for profit." This regulation further22

explains that "[r]egardless of the nature of its activities, every

corporation organized for profit and carrying out any of the

purposes of its organization is deemed to be doing business . . .

." [Emphasis added] According to 19 RCNY §11-03(b)(2), whether a

corporation is "doing business" is a factual determination. The

relevant factors to be considered include: (1) the nature,

continuity, frequency and regularity of the activities in the City;

(2) the purposes for which the corporation was organized; and (3)

the employment in the City of agents, officers and employees.

Although Petitioner contends that it ceased doing business at

the end of 1983, the record does not support such assertion.

Petitioner did not liquidate at the end of 1983, it did not file

final tax returns, and it did not file a certificate of dissolution

-23-

with the New York State Department of State. Instead, it retained

its corporate existence, and continued to file tax returns which

reflected substantial sums of income and indicated that Petitioner

was in the business of performing legal services. The record also

indicates that Petitioner was continuing to file Article 7

Petitions for its clients well after the time it claimed to have

gone out of business. As the ALJ noted, "it cannot be determined

from the record when, if ever, Petitioner ceased to exist in

corporate form." (Determination at 14)

The record supports the ALJ's finding that, although

Petitioner's shareholders had ceased practicing law together,

Petitioner's corporate existence was retained to fulfill a related

business purpose; the receipt and division of revenues from

referral of its client base and its work in progress.

Moreover, even accepting that the mere hiring of an attorney

is insufficient by itself to create nexus for GCT purposes, we

reject Petitioner's assertion that, under the facts herein,

Petitioner simply "retained an attorney" to protect its interest.

Based on the record before us, we conclude that Berger, P.C. was

retained by Petitioner to conduct Petitioner's business with

respect to the Article 7 Petitions which Petitioner had previously

filed and to handle its matters with the Law Department of the City

of New York. All legal fees generated pursuant to such arrangement

were transmitted to Petitioner, which then disbursed a portion to

-24-

Berger, P.C. That Mr. Berger and/or Berger, P.C. was acting as

Petitioner's agent is clearly established in the Offers and Orders

Letter and in the transmittal of the total fees received. A

taxpayer whose business is conducted through an agent is considered

to be doing business if the activities performed by the agent would

constitute doing business. De Amodio v. Commissioner, 299 F.2d 623

(3rd Cir. 1962); Lewenhaupt v. Commissioner, 20 T.C. 151 (1953),

affirmed 221 F.2d 227 (9th Cir. 1955).

Although Petitioner asserts that, pursuant to the Referral

Agreement, it retained an independent contractor and that the use

of independent contractors by a person or business does not under

15 U.S.C. 381(c), create taxability, we note that, as Respondent

argues, (1) the Referral Agreement was not submitted into evidence;

and (2) 15 U.S.C. 381(c) has no application to the facts before us.

The focus of such statute is on interstate commerce and, as

Respondent states, the "statute aims at preventing individual

states from impeding interstate commerce by imposing a net income

tax on a foreign person for no other reasons than that such foreign

person employs an independent contractor, who serves more than one

principal, to sell tangible personal property." (Respondent's

brief at 8)

Nor do we believe that Petitioner should be permitted to

allocate its business income within and without the City. Section

11-604.3(a) of the Code permits a taxpayer to allocate business

-25-

income within and without the City unless the taxpayer does not

"have a regular place of business outside the city other than a

statutory office." As the ALJ concluded, there is nothing in the

record regarding: (1) whether Petitioner had a regular place of

business outside the City during the Tax Years; and (2) what

activities, if any, Petitioner conducted or performed outside the

City. Therefore, Petitioner is not permitted to allocate its

business income within and without the City.

Lastly, we conclude that the Department correctly included

amounts paid to the Estate in the Alterative Tax base as salaries

and other compensation paid to a corporation's stockholders owning

in excess of five percent of its issued capital stock. Although §

1511 of the BCL prevents the sale or transfer of shares by one

shareholder in a professional services corporation to anyone who is

not authorized to practice the profession, such statute also

specifically provides that "[n]othing herein shall be construed to

prohibit the transfer of shares by operation of law or by court

decree." It is noted that §1510 of the BCL requires a professional

service corporation to redeem the shares of a deceased partner

within six months after the appointment of an executor. Although

the record is unclear as to whether Mr. Ribner died in 1985 or 1986,

it is clear that Petitioner did not redeem the shares before or

during the Tax Years. Petitioner now wishes to derive benefit from

that section of the BCL which supports its contention that the

Estate is not an appropriate shareholder, while completely ignoring

We have considered all remaining arguments raised by23

Petitioner, and find them unpersuasive.

-26-

the requirement in the preceding section that it was to redeem the

shares of Mr. Ribner within a specific period of time. Whether or

not Petitioner was properly constituted to conduct its practice

cannot be the focus of this inquiry. For purposes of its tax

liability, the payments to the Estate clearly constituted payments

to a shareholder.

The above conclusion stands because the ALJ correctly found

that Petitioner was the beneficial owner of the shares for purposes

of the GCT. As Respondent argues, "[t]he Estate became the

beneficial owner upon transfer of the shares. It continued as

beneficial owner due to Petitioner's failure to redeem the shares."

(Respondent's brief at 14) Moreover, there is evidence in the

record that the Estate did exercise control over Petitioner, i.e.,

it signed the 1986 Orders and Offers Letter along with Mr. Kluft

and Mr. Berger. Under these facts, we find that the Estate

possessed sufficient control over, and economic benefit from, the

corporation, to be the beneficial owner (as well as the titular

holder) of the shares. Therefore, the payments made by Petitioner

to the Estate were appropriately considered payments to a greater

than five percent shareholder and added back to the Alternative Tax

base.23

John Trubin retired from the Tribunal on April 30, 1997.24

-27-

Accordingly, the ALJ's Determination is sustained.24

Dated: May 20, 1997New York, New York

__________________________MARK FRIEDLANDERCommissioner and President

__________________________SUSAN GROSSMANCommissioner