rio oil and gas expo conference diretor de abastecimento,2 paulo roberto costa

TRANSCRIPT

1

Pa

ulo

Ro

be

rto

Co

sta

Do

wn

str

eam

Dir

ecto

r

Pa

ulo

Ro

be

rto

Co

sta

Do

wn

str

eam

Dir

ecto

r

Petr

och

em

ical

an

d

Re

fin

ing

In

teg

rati

on

-

Petr

ob

ras P

an

ora

ma

Petr

och

em

ical

an

d

Re

fin

ing

In

teg

rati

on

-

Petr

ob

ras P

an

ora

ma

2

Ag

en

da

Ag

en

da

:: S

tra

teg

ic P

lan

- 2

02

0

:: R

efi

nin

g I

nv

es

tme

nts

:: P

etr

oc

he

mic

al

Ind

us

try

:: P

etr

oc

he

mic

al-

Re

fin

ing

In

teg

rati

on

:: P

etr

oc

he

mic

al

Inv

es

tme

nts

:: C

on

clu

sio

ns

:: S

tra

teg

ic P

lan

- 2

02

0

:: R

efi

nin

g I

nv

es

tme

nts

:: P

etr

oc

he

mic

al

Ind

us

try

:: P

etr

oc

he

mic

al-

Re

fin

ing

In

teg

rati

on

:: P

etr

oc

he

mic

al

Inv

es

tme

nts

:: C

on

clu

sio

ns

Na

tura

l G

as

Na

tura

l G

as

• G

as

Sale

s:

50 m

illi

on

s o

f m

³/d

ay

(b

razil

ian

pro

du

cti

on

an

d i

mp

ort

s)

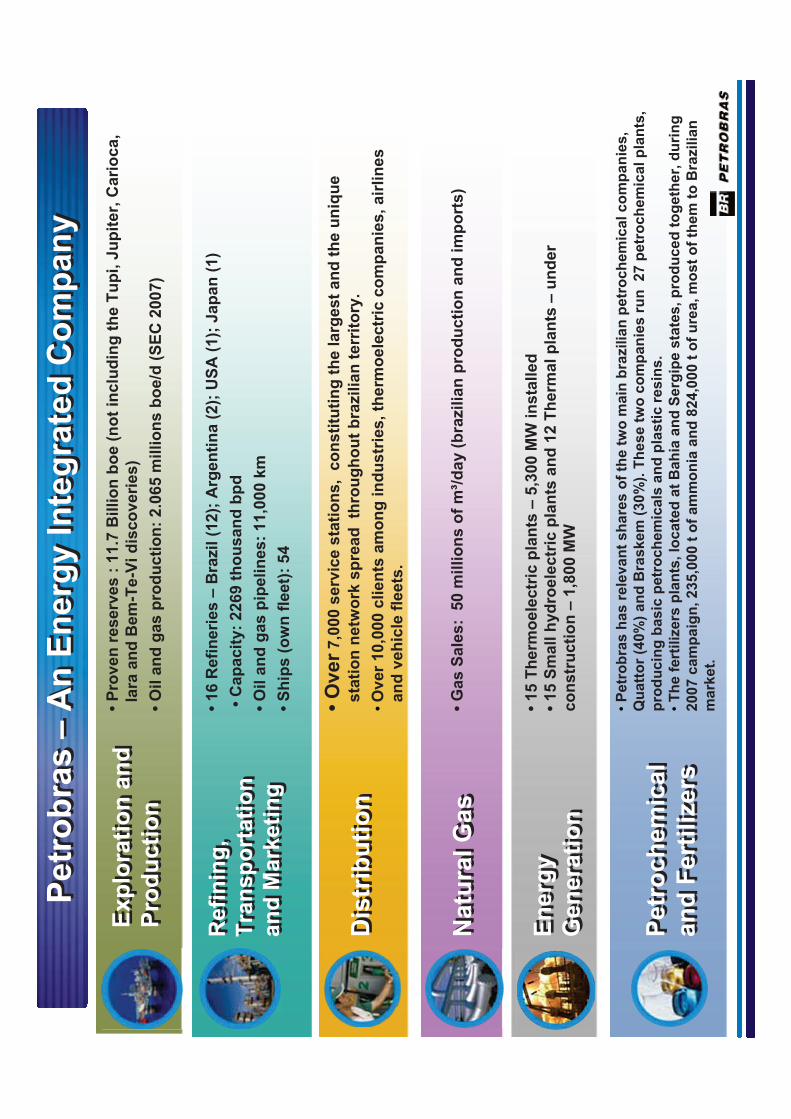

Exp

lora

tio

n a

nd

P

rod

ucti

on

Exp

lora

tio

n a

nd

P

rod

ucti

on

• P

rov

en

re

serv

es

: 1

1.7

Bil

lio

n b

oe

(n

ot

inc

lud

ing

th

e T

up

i, J

up

ite

r, C

ari

oc

a,

Iara

an

d B

em

-Te-V

i d

isco

veri

es)

• O

il a

nd

ga

s p

rod

uc

tio

n:

2.0

65

mil

lio

ns

bo

e/d

(S

EC

200

7)

Pe

tro

ch

em

ica

l a

nd

Fe

rtil

ize

rs

Pe

tro

ch

em

ica

l a

nd

Fe

rtil

ize

rs

•P

etr

ob

ras

ha

s r

ele

va

nt

sh

are

s o

f th

e t

wo

main

bra

zilia

n p

etr

oc

he

mic

al c

om

pa

nie

s,

Qu

att

or

(40%

) a

nd

Bra

sk

em

(3

0%

). T

he

se

tw

o c

om

pa

nie

s r

un

2

7 p

etr

oc

he

mic

al p

lan

ts,

pro

du

cin

g b

as

ic p

etr

oc

he

mic

als

an

d p

las

tic

re

sin

s.

•T

he

fert

iliz

ers

pla

nts

, lo

ca

ted

at

Ba

hia

an

d S

erg

ipe

sta

tes

, p

rod

uc

ed

to

ge

the

r, d

uri

ng

2

00

7 c

am

pa

ign

, 2

35,0

00

t o

f am

mo

nia

an

d 8

24

,00

0 t

of

ure

a, m

os

t o

f th

em

to

Bra

zilia

n

ma

rke

t.

• O

ver

7,0

00 s

erv

ice s

tati

on

s,

co

nsti

tuti

ng

th

e l

arg

est

an

d t

he u

niq

ue

sta

tio

n n

etw

ork

sp

rea

d th

rou

gh

ou

t b

razil

ian

te

rrit

ory

.

•O

ver

10,0

00 c

lie

nts

am

on

g i

nd

us

trie

s,

the

rmo

ele

ctr

ic c

om

pa

nie

s,

air

lin

es

an

d v

eh

icle

fle

ets

.

Dis

trib

uti

on

Dis

trib

uti

on

Re

fin

ing

,T

ran

sp

ort

ati

on

a

nd

Ma

rke

tin

g

Re

fin

ing

,T

ran

sp

ort

ati

on

a

nd

Ma

rke

tin

g

• 1

6 R

efi

ne

ries –

Bra

zil

(1

2);

Arg

en

tin

a (

2);

US

A (

1);

Jap

an

(1

)

• C

ap

acit

y:

2269 t

ho

usan

d b

pd

• O

il a

nd

gas p

ipeli

nes:

11,0

00 k

m

• S

hip

s (

ow

n f

leet)

: 5

4

En

erg

yG

en

era

tio

n

En

erg

yG

en

era

tio

n

• 15 T

herm

oele

ctr

ic p

lan

ts –

5,3

00 M

W i

nsta

lled

• 1

5 S

ma

ll h

yd

roe

lec

tric

pla

nts

an

d 1

2 T

he

rma

l p

lan

ts –

un

de

r c

on

str

uc

tio

n –

1,8

00

MW

Petr

ob

ras –

An

En

erg

y I

nte

gra

ted

Co

mp

an

yP

etr

ob

ras –

An

En

erg

y I

nte

gra

ted

Co

mp

an

y

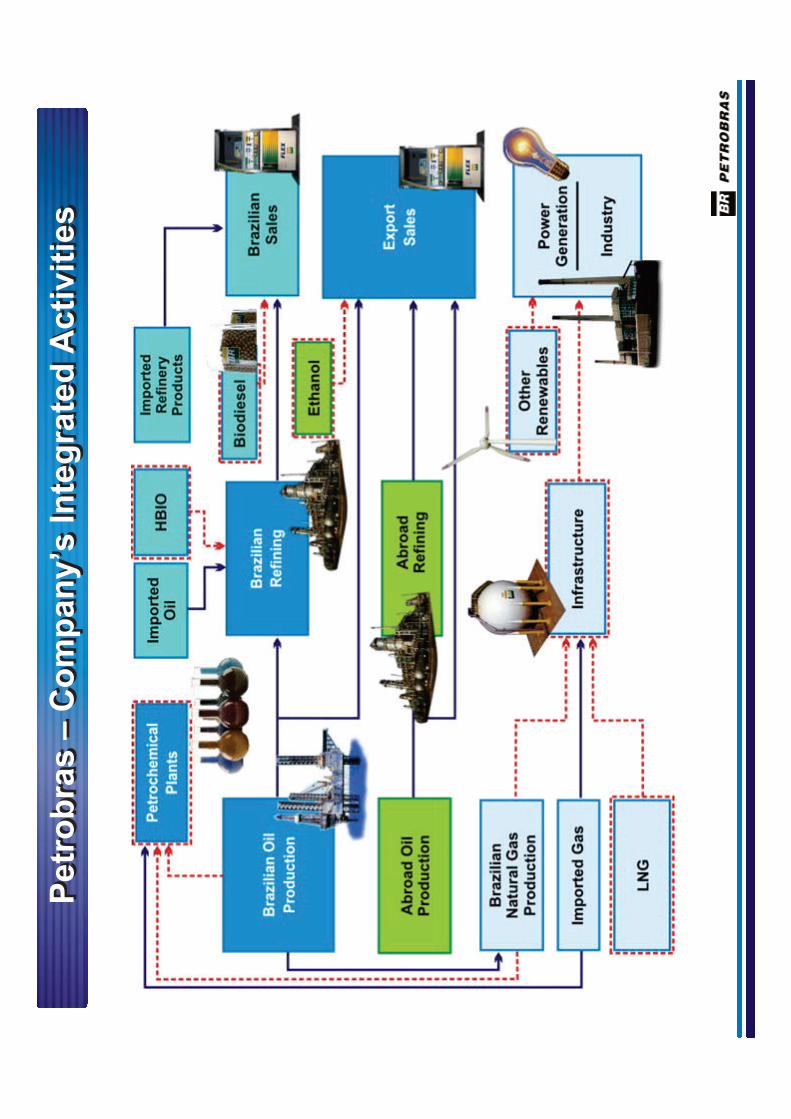

Petr

ob

ras –

Co

mp

an

y’s

In

teg

rate

d A

cti

vit

ies

Petr

ob

ras –

Co

mp

an

y’s

In

teg

rate

d A

cti

vit

ies

5

Str

ate

gic

Pla

n -

20

20

Str

ate

gic

Pla

n -

20

20

CorporateStrategy

Co

rpo

rate

Str

ate

gy

Bu

sin

es

s S

eg

me

nt

Str

ate

gy

- 2

02

0

Investm

en

t P

lan

by B

usin

ess S

eg

men

tIn

vestm

en

t P

lan

by B

usin

ess S

eg

men

t

PE

TR

OB

RA

S

26,1

1,1

4,2

3%

13

%

84

%

DO

WN

ST

RE

AM

2008-1

2 P

eri

od

US

$ 3

1,4

bi

2008-1

2 P

eri

od

US

$ 1

12,4

bi

Pe

tro

qu

ímic

a

RT

C

Bio

co

mb

us

t ív

el

Su

pp

ly C

hallen

ges

Su

pp

ly C

hallen

ges

9

Re

fin

ing

Inv

es

tme

nts

Re

fin

ing

Inv

es

tme

nts

Cu

rre

nt

Re

fin

ing

In

fra

str

uc

ture

in

Bra

zil

Cu

rre

nt

Re

fin

ing

In

fra

str

uc

ture

in

Bra

zil

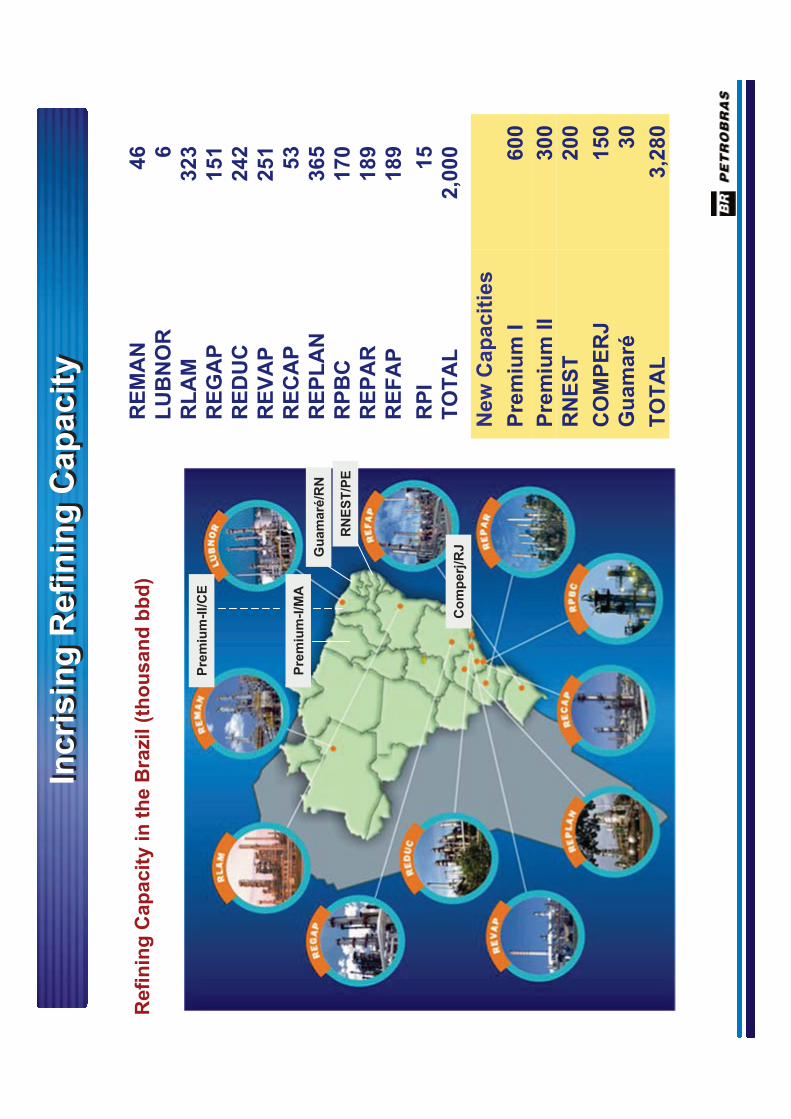

RE

MA

N46

LU

BN

OR

6

RL

AM

323

RE

GA

P151

RE

DU

C242

RE

VA

P251

RE

CA

P53

RE

PL

AN

365

RP

BC

170

RE

PA

R189

RE

FA

P

RP

I

189

15

TO

TA

L B

RA

ZIL

2,0

00

Re

fin

ing

Ca

pa

cit

y (T

ho

us

an

d b

arr

els

/da

y)

AR

GE

NT

INA

69

US

A

1

00

JA

PA

N100

TO

TA

L P

ET

RO

BR

AS

2,2

69

Refi

nin

g N

ew

Pro

jects

Refi

nin

g N

ew

Pro

jects

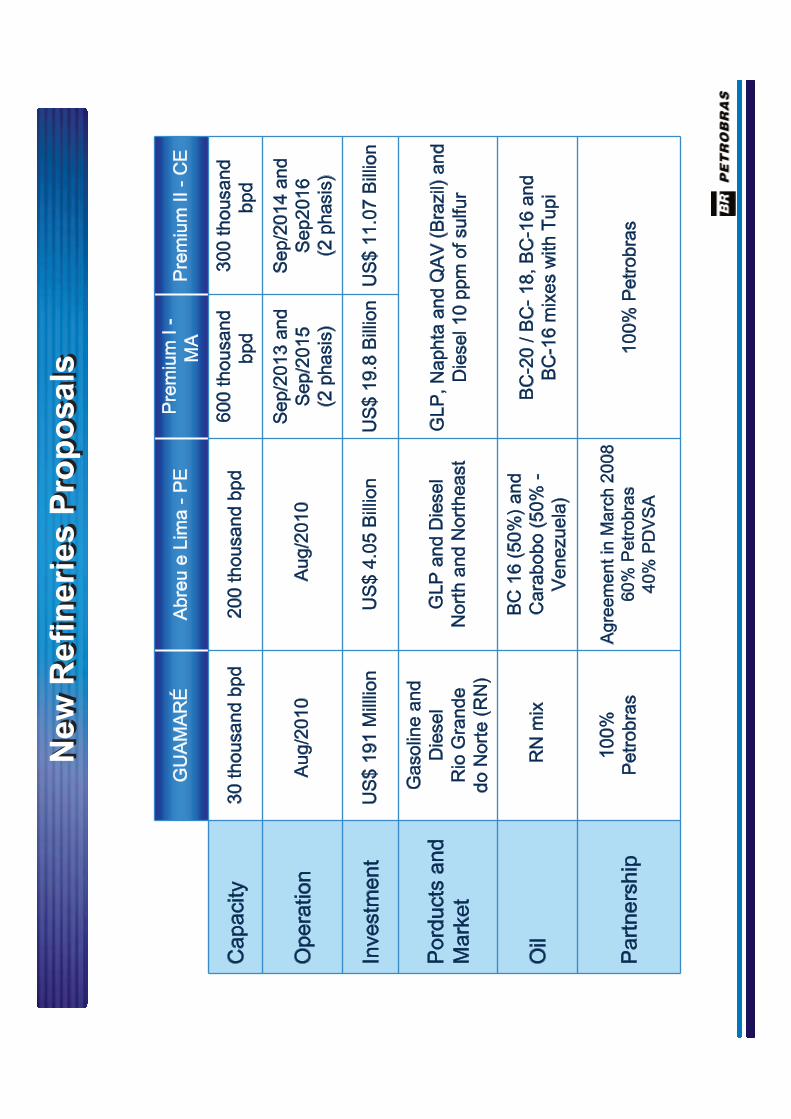

RN

ES

T(A

bre

u e

Lim

a)

Gu

am

aré

PR

EM

IUM

II

PR

EM

IUM

I

CO

MP

ER

J

New

Refi

neri

es P

rop

osals

New

Refi

neri

es P

rop

osals

RE

MA

N46

LU

BN

OR

6R

LA

M323

RE

GA

P151

RE

DU

C242

RE

VA

P251

RE

CA

P53

RE

PL

AN

365

RP

BC

170

RE

PA

R189

RE

FA

P

RP

I

189

15

TO

TA

L2,0

00

New

Cap

acit

ies

Pre

miu

m I

600

Pre

miu

m I

I300

RN

ES

T

CO

MP

ER

J

200

150

Gu

am

aré

TO

TA

L

30

3,2

80

Refi

nin

g C

ap

acit

y in

th

e B

razil (

tho

usan

d b

bd

)

Incri

sin

g R

efi

nin

g C

ap

acit

yIn

cri

sin

g R

efi

nin

g C

ap

acit

y

Pre

miu

m-I

/MA

Gu

am

aré

/RN

Co

mp

erj

/RJ

Pre

miu

m-I

I/C

E

RN

ES

T/P

E

14

Petr

och

em

ical

Ind

us

try

Petr

och

em

ical

Ind

us

try

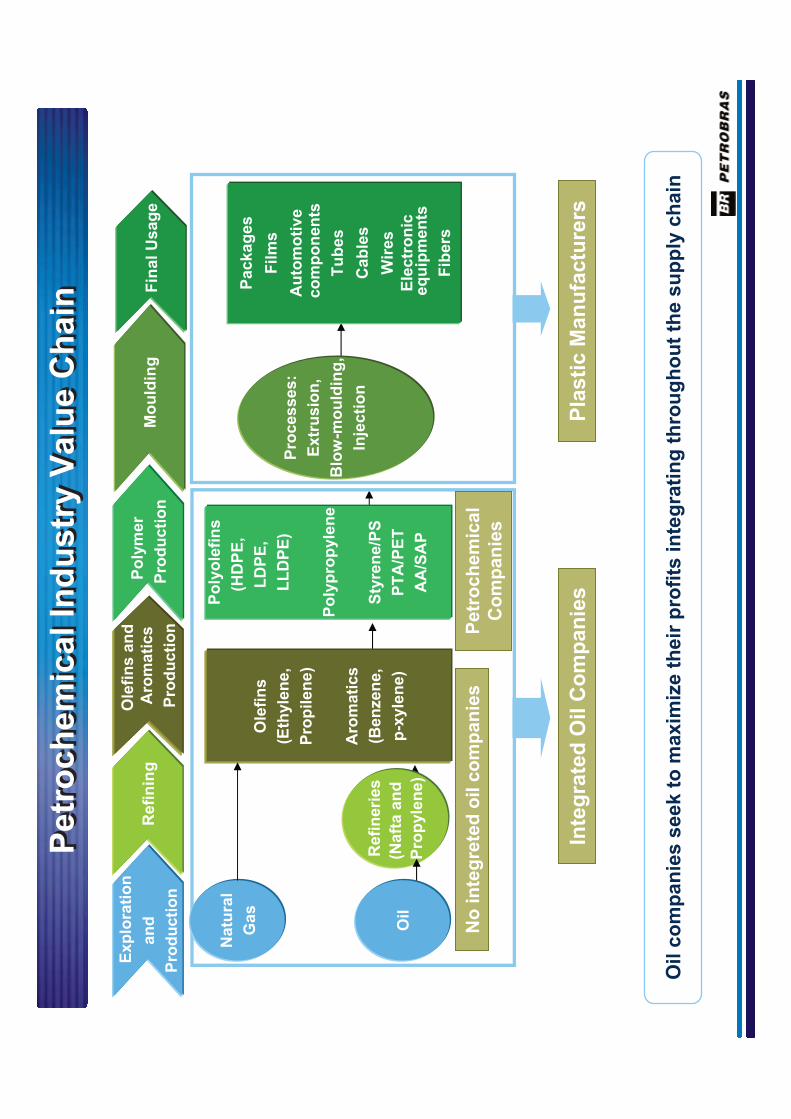

Oil c

om

pan

ies s

ee

k t

o m

axim

ize t

heir

pro

fits

in

teg

rati

ng

th

rou

gh

ou

t th

e s

up

ply

ch

ain

Refi

neri

es

(Naft

a a

nd

Pro

pyle

ne

)

Natu

ral

Ga

s

Oil

Ole

fin

s

(Eth

yle

ne

,

Pro

pil

en

e)

Aro

mati

cs

(Ben

zen

e,

p-x

yle

ne)

Po

lyo

lefi

ns

(HD

PE

,

LD

PE

,

LL

DP

E)

Po

lyp

rop

yle

ne

Sty

ren

e/P

S

PT

A/P

ET

AA

/SA

P

Pro

cesses:

Extr

usio

n,

Blo

w-m

ou

ldin

g,

Inje

cti

on

Packag

es

Fil

ms

Au

tom

oti

ve

co

mp

on

en

ts

Tu

bes

Cab

les

Wir

es

Ele

ctr

on

ice

qu

ipm

en

ts

Fib

ers

No

in

teg

rete

do

ilco

mp

an

ies

Pe

tro

ch

em

ica

lC

om

pan

ies

Inte

gra

ted

Oil

Co

mp

an

ies

Pla

sti

c M

an

ufa

ctu

rers

Refi

nin

gP

oly

me

r

Pro

du

cti

on

Ole

fin

sa

nd

Aro

mati

cs

Pro

du

cti

on

Fin

al

Usag

eM

ou

ldin

g

Ex

plo

rati

on

an

d

Pro

du

cti

on

Petr

och

em

ical

Ind

ustr

yV

alu

eC

hain

Petr

och

em

ical

Ind

ustr

yV

alu

eC

hain

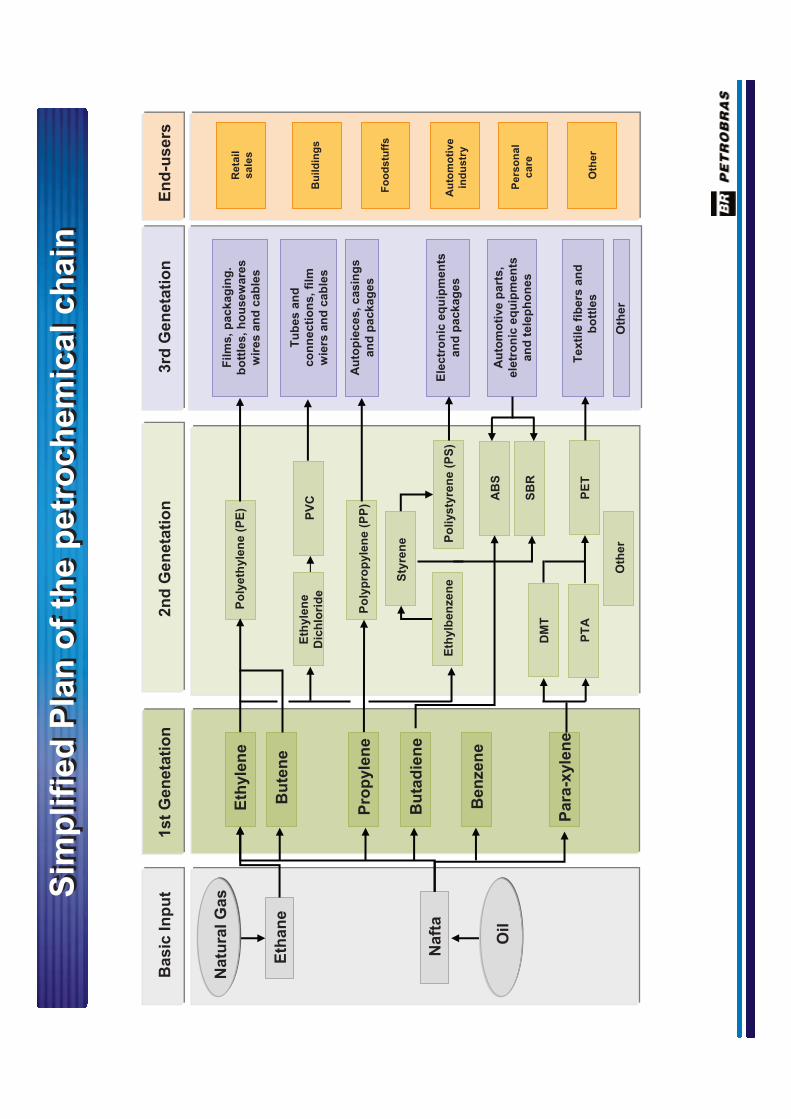

Sim

pli

fie

d P

lan

of

the

pe

tro

ch

em

ica

l c

ha

inS

imp

lifi

ed

Pla

n o

f th

e p

etr

oc

he

mic

al

ch

ain

Basic

In

pu

t

Eth

an

e

Naft

a

Na

tura

l G

as

Oil

1s

t G

en

eta

tio

n

Eth

yle

ne

Bu

ten

e

Pro

pyle

ne

Bu

tad

ien

e

Ben

zen

e

Para

-xyle

ne

2n

d G

en

eta

tio

n

Po

lye

thyle

ne

(P

E)

Po

lyp

rop

yle

ne

(P

P)

Sty

ren

e

AB

S

SB

R

PE

T

Oth

er

PT

A

DM

T

Eth

yle

ne

Dic

hlo

rid

eP

VC

Eth

ylb

en

zen

eP

oli

ys

tyre

ne

(P

S)

3rd

Gen

eta

tio

n

Film

s,

packag

ing

. b

ott

les,

ho

usew

are

s

wir

es a

nd

cab

les

Tu

bes

an

d

co

nn

ecti

on

s,

film

w

iers

an

d c

ab

les

Au

top

ieces,

casin

gs

an

d p

ackag

es

Ele

ctr

on

ic e

qu

ipm

en

tsan

d p

ackag

es

Au

tom

oti

ve

pa

rts

, ele

tro

nic

eq

uip

men

ts

an

d t

ele

ph

on

es

Texti

le f

ibers

an

d

bo

ttle

s

Oth

er

En

d-u

sers

Reta

il

sa

les

Bu

ild

ing

s

Fo

od

stu

ffs

Au

tom

oti

ve

ind

ustr

y

Pers

on

al

ca

re

Oth

er

17

Petr

och

em

ical –

Re

fin

ing

Inte

gra

tio

n

Petr

och

em

ical –

Re

fin

ing

Inte

gra

tio

n

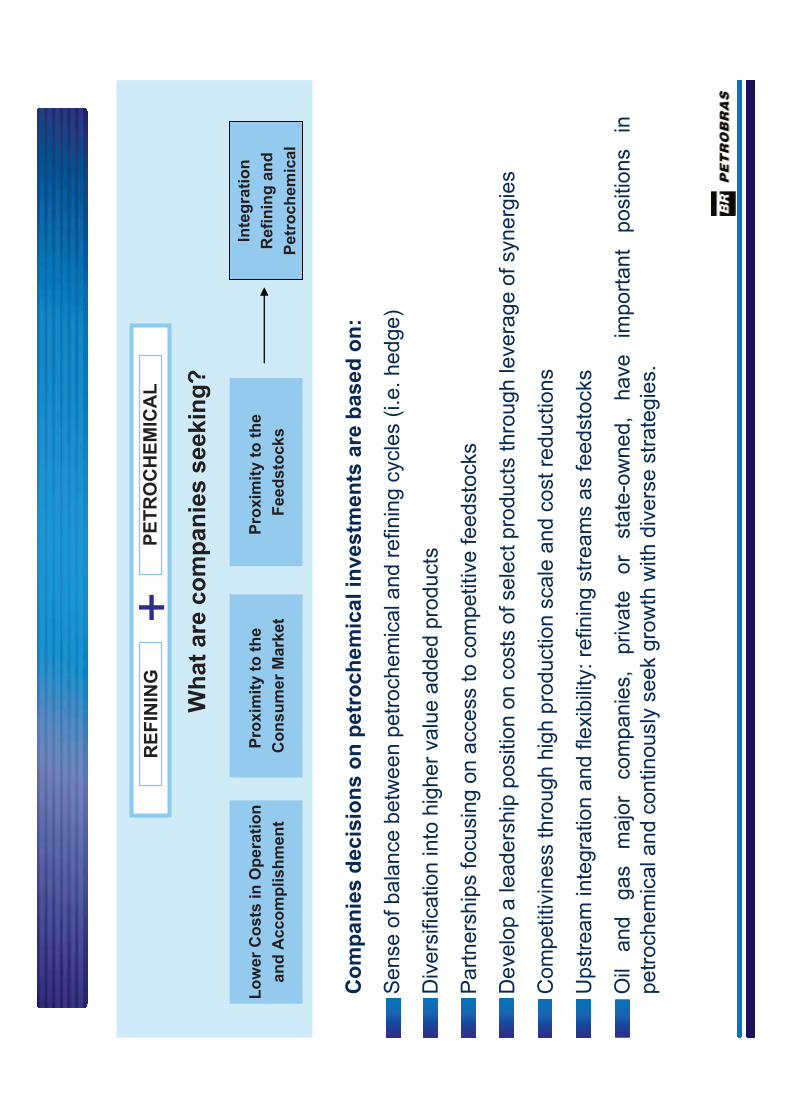

Wh

at

are

co

mp

an

ies s

eekin

g?

Lo

wer

Co

sts

in O

pe

rati

on

an

dA

cco

mp

lish

men

t

Pro

xim

ity

to t

he

Co

ns

um

er

Mark

et

Pro

xim

ity

to t

he

Feed

sto

cks

Inte

gra

tio

n

Re

fin

ing

an

d

Petr

och

em

ical

PE

TR

OC

HE

MIC

AL

RE

FIN

ING

+

Co

mp

an

ies

decis

ion

so

np

etr

och

em

ical

investm

en

tsare

based

on

:

Sense

of bala

nce b

etw

een p

etr

ochem

icala

nd

refin

ing

cycl

es

(i.e

. hedge)

Div

ers

ifica

tion

into

hig

her

valu

eadded

pro

duct

s

Part

ners

hip

sfo

cusin

gon

access

to c

om

petit

ive f

eedsto

cks

Develo

pa

leaders

hip

positi

on

on

costs

of sele

ctpro

ducts

thro

ugh

levera

ge

of synerg

ies

Com

petit

ivin

ess

thro

ugh

hig

hpro

duct

ion

scale

and c

ost

reductio

ns

Upstr

eam

inte

gra

tion

and

flexib

ility

: re

finin

g s

tream

sas f

eedsto

cks

Oil

and

gas

majo

r com

panie

s,

private

o

rsta

te-o

wned,

have

import

ant

positi

ons

inpetr

ochem

icala

nd c

ontin

ously

seek

gro

wth

with

div

ers

estr

ate

gie

s.

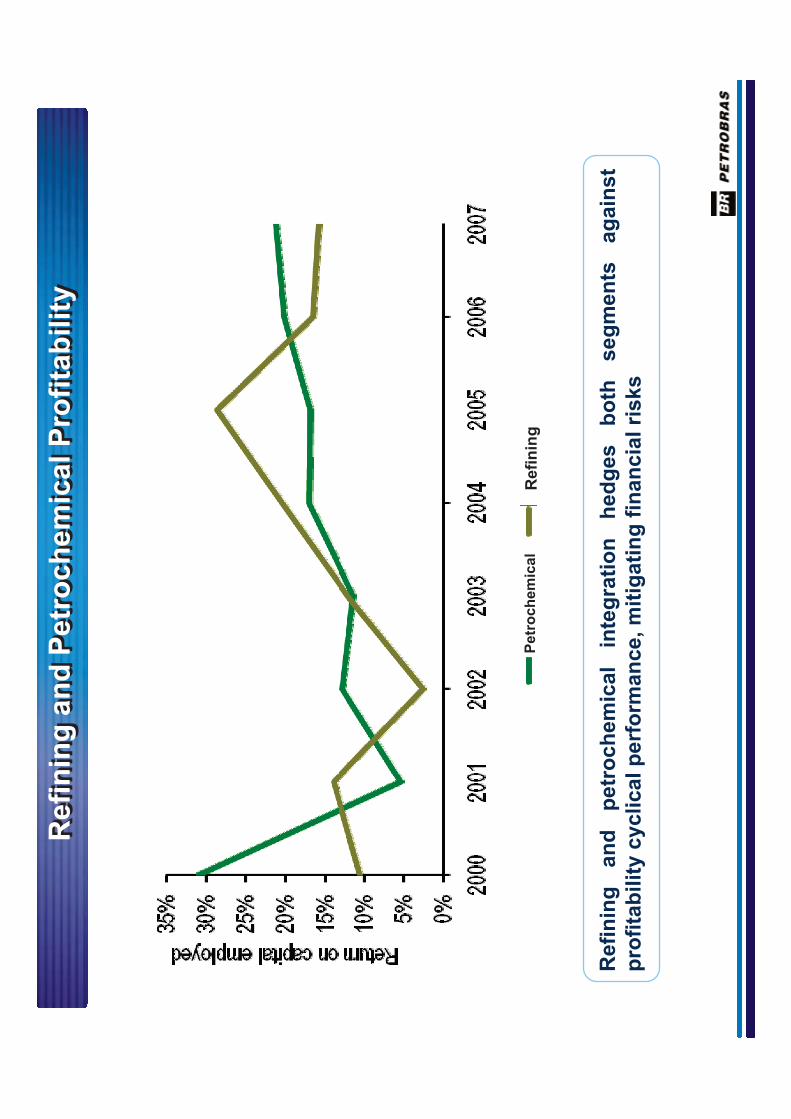

Refi

nin

g

an

d

petr

och

em

ical

inte

gra

tio

n

hed

ges

bo

th

seg

men

ts

ag

ain

st

pro

fita

bil

ity

cy

cli

ca

l p

erf

orm

an

ce

, m

itig

ati

ng

fin

an

cia

l ri

sk

s

Re

fin

ing

an

d P

etr

oc

he

mic

al P

rofi

tab

ilit

yR

efi

nin

g a

nd

Pe

tro

ch

em

ica

l P

rofi

tab

ilit

y

Pe

tro

ch

em

ica

lR

efi

nin

g

Op

ort

un

itie

s f

or

Petr

och

em

ical an

d R

efi

nin

g In

teg

rati

on

Op

ort

un

itie

s f

or

Petr

och

em

ical an

d R

efi

nin

g In

teg

rati

on

Pro

du

ct

Inte

gra

tio

n

!re

finery

str

eam

sa

s feedsto

ck

as feedsto

ck for

petr

ochem

ical p

lants

Ex

am

ple

:naphta

, pro

pyle

n, pro

pane, eth

ane a

nd r

efinery

gas

!petr

ochem

icalstr

eam

sa

s b

lendsto

ck

for

refinin

gopera

tions

Ex

am

ple

: p

yro

lysis

ga

so

line

Pro

du

ct

an

d E

ne

rgy

In

teg

rati

on

!p

rod

uctin

teg

ratio

nan

d p

ow

er

ge

ne

ratio

n

Ex

am

ple

: C

OM

PE

RJ, an in

tegra

ted s

olu

tion

Tech

no

log

y I

nte

gra

tio

n

Exam

ple

: a

uto

mation technolo

gy for

petr

ochem

ical com

panie

s

Inte

gra

tio

n f

or

Sch

ed

ule

d M

ain

ten

an

ce

!S

ynchro

niz

ation

of th

eschedule

d m

ain

tenance p

lans

in o

rder

to o

ptim

ize the

main

tenance e

ffort

s a

nd a

void

pro

duction g

aps

Exam

ple

: p

etr

ochem

ical re

finery

pla

nt

21

Petr

och

em

ical

Inv

es

tme

nts

Petr

och

em

ical

Inv

es

tme

nts

Expand

opera

tions

in

1st

and

2nd

genera

tion

pro

cesses,

incre

asin

g t

he

pro

du

ctio

n o

f p

etr

och

em

ica

ls,

wh

ile a

dd

ing

va

lue

to

the p

roducts

of

the G

roup’s

re

fin

erie

s b

y c

ap

turin

g s

yn

erg

ies

rela

ted to the p

roduction o

f oil,

gas, re

finin

g a

nd p

etr

ochem

icals

Develo

p n

ew

technolo

gie

s f

or

the c

hem

ical

industr

y b

ased o

n

the

technolo

gic

al

evolu

tion

of

petr

ochem

ical

fluid

cata

lytic

cra

ckin

g (

FC

C),

bio

de

gra

da

ble

po

lym

ers

an

d b

iop

oly

me

rs

Petr

och

em

ical S

eg

men

t S

trate

gie

s o

n S

trate

gic

Pla

n -

2020

Petr

och

em

ical S

eg

men

t S

trate

gie

s o

n S

trate

gic

Pla

n -

2020

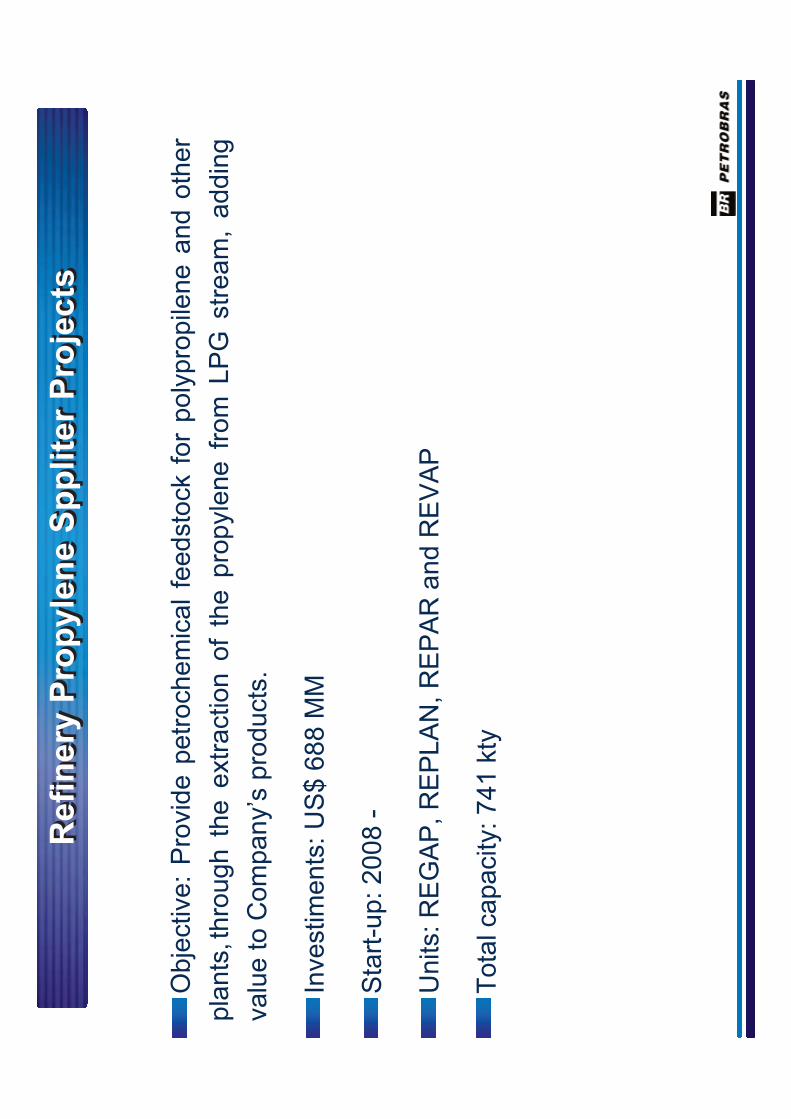

Refi

nery

Pro

pyle

ne S

pp

lite

r P

roje

cts

Refi

nery

Pro

pyle

ne S

pp

lite

r P

roje

cts

Obje

ctive:

Pro

vid

e p

etr

ochem

ical

feedsto

ck f

or

poly

pro

pile

ne a

nd o

ther

pla

nts

, thro

ugh t

he e

xtr

action o

f th

e p

ropyle

ne f

rom

LP

G s

tream

, addin

g

valu

e to C

om

pany’s

pro

ducts

.

Investim

ents

: U

S$ 6

88 M

M

Sta

rt-u

p:

2008 -

Un

its:

RE

GA

P,

RE

PL

AN

, R

EP

AR

an

d R

EV

AP

Tota

l capacity:

741 k

ty

Pe

tro

qu

ímic

a S

ua

pe

Location: S

uape/P

E;

Capacity: 640 k

ty P

TA

;

Tota

l investm

ent: U

S$ 6

32 m

illio

n;

Ra

w m

ate

ria

l: i

mp

ort

ed

p-x

yle

ne

un

til

20

12

an

d C

OM

PE

RJ f

rom

2013 o

nw

ard

s;

Sta

rt-u

p: 4th

Q 2

009.

Co

mp

an

hia

Tê

xti

l d

e P

ern

am

bu

co

- C

ITE

PE

Location: S

uape/P

E;

Capacity: 240 k

ty P

OY

;

Tota

l investm

ent: U

S$ 3

42 m

illio

n;

Raw

Mate

rial: i

mport

ed P

OY

until

2009 a

nd P

etr

oquím

ica S

aupe

fro

m 2

00

9 o

nw

ard

s;

Sta

rt-u

p: 2th

Q 2

008.Petr

och

em

ical

Pro

jects

Petr

och

em

ical

Pro

jects

CO

MP

ER

J’s

main

purp

ose i

s t

o i

ncre

ase t

he p

roduction o

f petr

ochem

icals

in

B

razil,

usin

g a

s f

ee

dsto

ck 1

50

th

ou

sa

nd

bp

d o

f d

om

estic h

ea

vy c

rud

e,

the

Ma

rlim

oil

from

Cam

pos B

asin

.

Are

a: 45 m

illio

n s

q. ft.

Location: Itabora

í -

RJ

Investm

ents

: U

S$ 8

.38 b

illio

n

Capacity:

•B

asic

Petr

ochem

icals

: 1,3

00 k

ty e

thene;

70

0 k

ty p

-xyle

ne

; 8

81

kty

pro

pyle

ne

; 608 k

ty b

enzene; 157 k

ty b

uta

die

ne;

•D

ow

nstr

eam

: 800 k

ty P

E;

850 k

ty P

P;

500 k

ty s

tyre

ne;

600 k

ty e

thyle

ne

gly

col; 5

00 k

ty P

TA

; 600 k

ty P

ET

;

Sta

rt-u

p: 2012

Technolo

gy:

Pe

tro

ch

em

ica

l F

CC

– d

ee

p flu

id c

ata

lytic c

rackin

g te

ch

no

log

y

•T

his

te

ch

no

log

y a

llow

th

e p

rod

uctio

n o

f h

ug

e a

mo

un

ts o

f o

lefin

s (

eth

en

e a

nd

p

rop

yle

ne

) a

nd

w

ill e

na

ble

tig

hte

r in

teg

ratio

n be

twe

en

re

fin

ing

a

nd

b

asic

petr

ochem

icals

pro

duction technolo

gie

s

CO

MP

ER

J –

Petr

och

em

ical

Co

mp

lex o

f R

io d

e J

an

eir

o

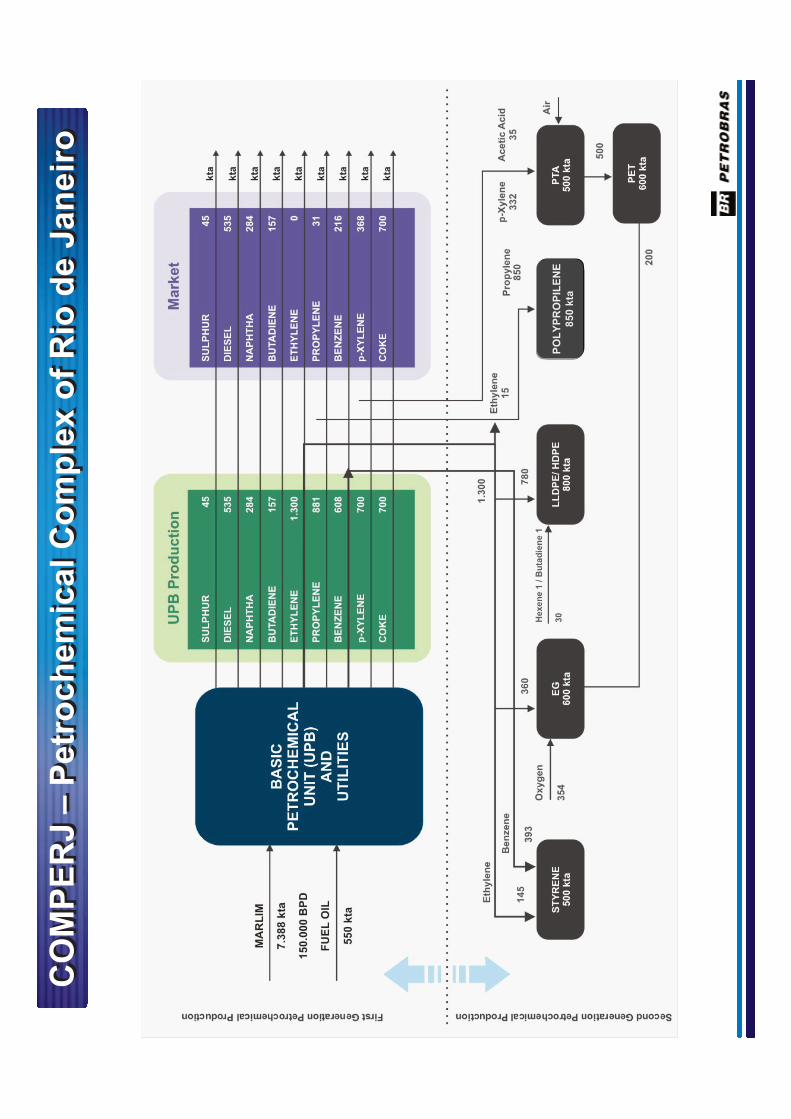

CO

MP

ER

J –

Petr

och

em

ical

Co

mp

lex o

f R

io d

e J

an

eir

o

CO

MP

ER

J –

Petr

och

em

ical C

om

ple

x o

f R

io d

e J

an

eir

o

CO

MP

ER

J –

Petr

och

em

ical C

om

ple

x o

f R

io d

e J

an

eir

o

PO

LY

PR

OP

ILE

NE

8

50

kta

CO

MP

ER

J L

ocati

on

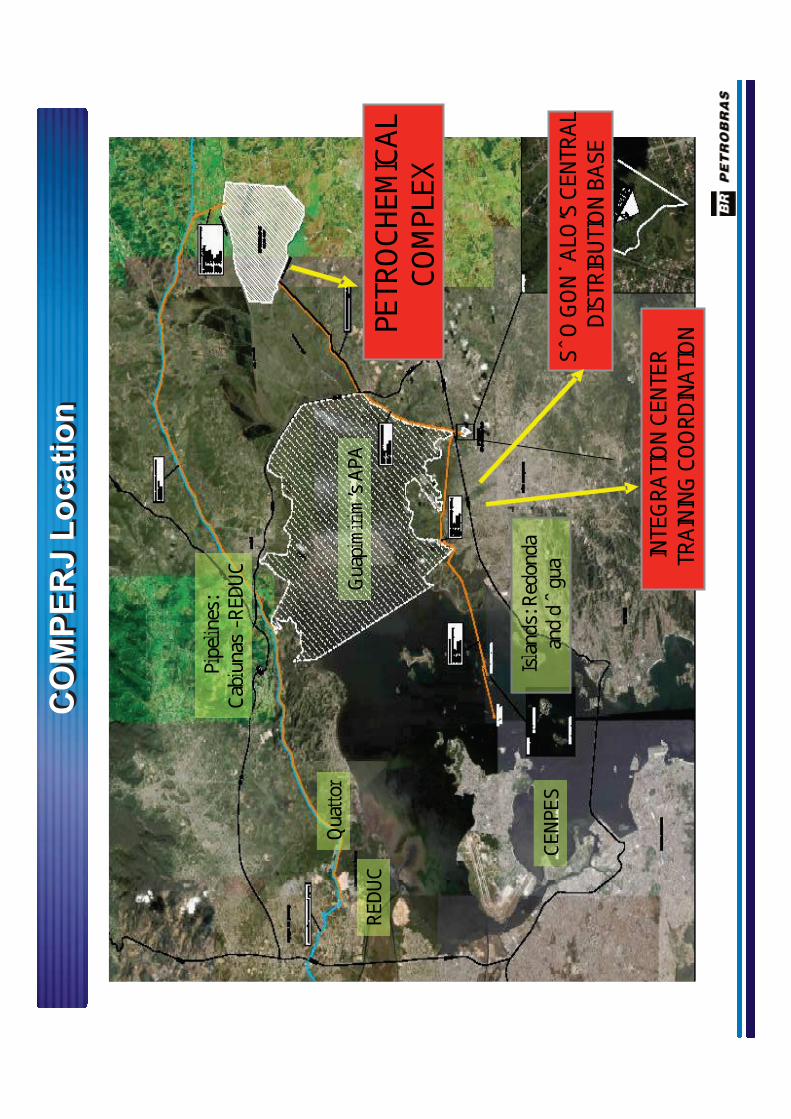

CO

MP

ER

J L

ocati

on

REDUCQuatt

orGuap

imirim’s AP

A

Islands: Re

donda

andd´Água

Pipelines:

Cabiunas-

REDUC

CENPES

PETROCHE

MICAL

COMPLEX

SÃO GONÇ

ALO’S CENT

RAL DISTR

IBUTION B

ASEINTEG

RATION CEN

TER TRAIN

ING COORD

INATION

CO

MP

ER

J P

rod

ucti

on

CO

MP

ER

J P

rod

ucti

on

Pro

du

cts

P

rod

uc

tio

n(k

ty)

Do

wn

str

ea

m

Po

lyp

rop

yle

ne

850

Po

lyeth

yle

ne

800

Sty

ren

e500

Eth

yle

ne

gly

co

l600

PT

A500

PE

T600

Pro

du

cts

Pro

du

cti

on

(kty

)

Ba

sic

s

Fu

els

Die

se

l535

Na

ph

tha

284

Co

ke

700

Petr

och

em

icals

Eth

yle

ne

1,3

00

Pro

pyle

ne

881

Be

nze

ne

608

Bu

tad

ien

e157

p-X

yle

ne

700

Su

lph

ur

45

CO

MP

ER

J M

ain

Fra

mew

ork

CO

MP

ER

J M

ain

Fra

mew

ork

FE

L 3

Conclu

sio

ns

De

z/0

8

Contr

act

ing o

f th

e I

nte

gra

tor

Oct

/07

End o

f th

e I

nte

gra

tion C

ente

r C

onst

ruct

ion

Oct

/08

FE

ED

Ela

bora

tion

Oct

/08

Acquis

itio

n o

f th

e M

ain

Access A

rea

De

c/0

8

Sta

rt o

f E

mbankm

ent

Mar/

08

*UP

B L

IF

eb/0

9

*Ma

in A

cce

ss R

oa

d L

IA

pr/

09

*345 k

V T

ransm

issio

n L

ine L

IJun/0

9

*Term

inal and P

ipelin

e L

IA

ug

/09

*Subm

arine E

mis

sary

LI

De

c/0

9

AN

P A

uth

orization

Oct

/09

Sta

rt o

f E

PC

s C

ontr

actin

gF

eb/0

9

Expecte

d S

tart

-up

Jun/1

2

Expecte

d F

ull

Opera

tion

Au

g/1

3

*LI – L

icenci

am

ento

de Inst

ala

ções

(Faci

litie

s Lic

ensi

ng)

CO

MP

ER

J S

ch

ed

ule

CO

MP

ER

J S

ch

ed

ule

Ste

pS

tep

2003

2003

2004

2004

2006

2006

2008

2008

2010

2010

2012

2012

2005

2005

2007

2007

2009

2009

2011

2011

2013

2013

Acco

mp

lish

men

t

Bu

sin

ess P

lan

nin

g

(FE

L 1

)

Co

ncep

tual E

ng

ineeri

ng

(F

EL

2)

Basic

En

gin

eeri

ng

(F

EL

3)

Co

nstr

. an

d A

ssem

bly

Un

its S

tart

-up

Co

nc

lud

ed

In p

rog

ress

To

be

sta

rted

UP

B C

on

dit

ion

ing

an

d S

tart

-up F

ull

Op

era

tio

n

31

Co

nc

lus

ion

sC

on

clu

sio

ns

Benefits

fo

r P

etr

obra

s,

addin

g

valu

e

to

the

supply

chain

, captu

ring

synerg

ies

rela

ted

to

both

segm

ents

and

follo

win

g

a

glo

bal

trend

of

upstr

eam

inte

gra

tion a

mong larg

e c

om

panie

s;

Te

ch

on

olo

gic

al ch

alle

ng

es w

ith

th

e u

se

of

he

avy c

rud

e o

ils fo

r petr

ochem

ical purp

oses, usin

g innovative

Pe

tro

ch

em

ica

l F

CC

te

ch

no

log

y,

de

ve

lop

ed

in

tern

ally

an

d a

do

pe

td a

t C

OM

PE

RJ,

inte

gra

tin

g r

efin

ing

opera

tions a

nd the p

roduction o

f basic

petr

ochem

icals

;

Str

en

gth

en

ing

o

f B

razili

an

P

etr

och

em

ica

l In

du

str

y,

pro

mo

tin

g

tra

inin

g,

technolo

gy d

evelo

pm

ent, e

mplo

ym

ent and incom

e for

the c

ountr

y.

Mo

tiv

ati

on

fo

r P

etr

oc

he

mic

al-

Re

fin

ing

In

teg

rati

on

Mo

tiv

ati

on

fo

r P

etr

oc

he

mic

al-

Re

fin

ing

In

teg

rati

on

33

ww

w.p

etr

ob

ras

.co

m.b

rw

ww

.pe

tro

bra

s.c

om

.br