russian steel market developments oecd steel committee5)_russian-steel_30nov2015.pdf ·...

TRANSCRIPT

Russian Steel Market DevelopmentsOECD Steel Committee

Focus on the domestic market prompting future capacity optimization

Russian Steel Organization Nikita Vorobyev, NLMK

Paris, France 30 November 2015

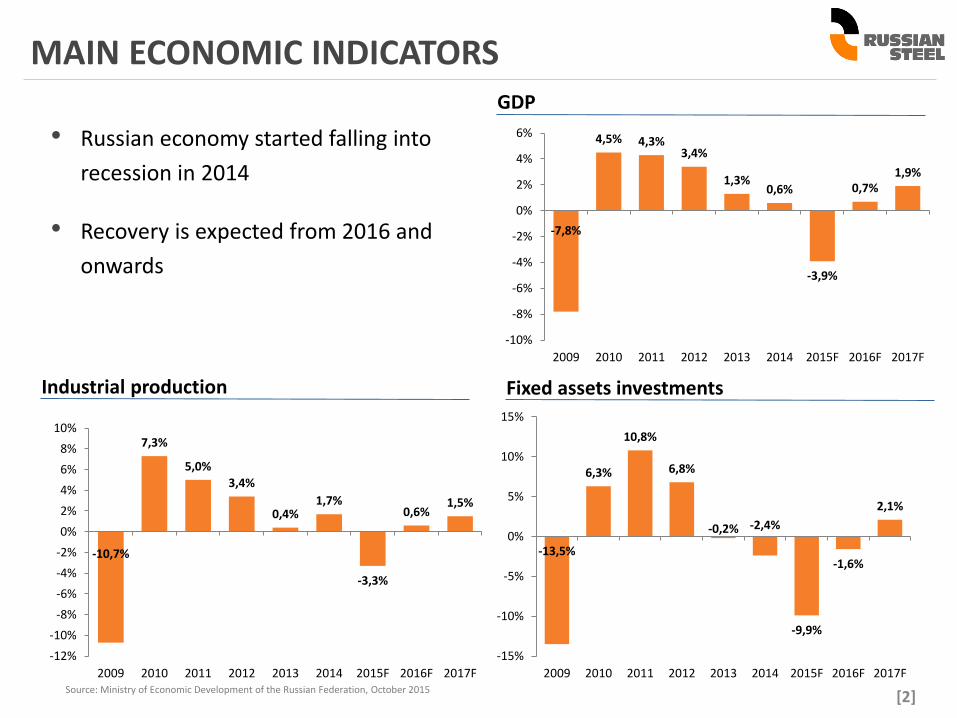

MAIN ECONOMIC INDICATORS

[2]Source: Ministry of Economic Development of the Russian Federation, October 2015

• Russian economy started falling into

recession in 2014

• Recovery is expected from 2016 and

onwards

GDP

Industrial production Fixed assets investments

-7,8%

4,5% 4,3%3,4%

1,3%0,6%

-3,9%

0,7%1,9%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F

-10,7%

7,3%

5,0%

3,4%

0,4%1,7%

-3,3%

0,6%1,5%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F

-13,5%

6,3%

10,8%

6,8%

-0,2% -2,4%

-9,9%

-1,6%

2,1%

-15%

-10%

-5%

0%

5%

10%

15%

2009 2010 2011 2012 2013 2014 2015F 2016F 2017F

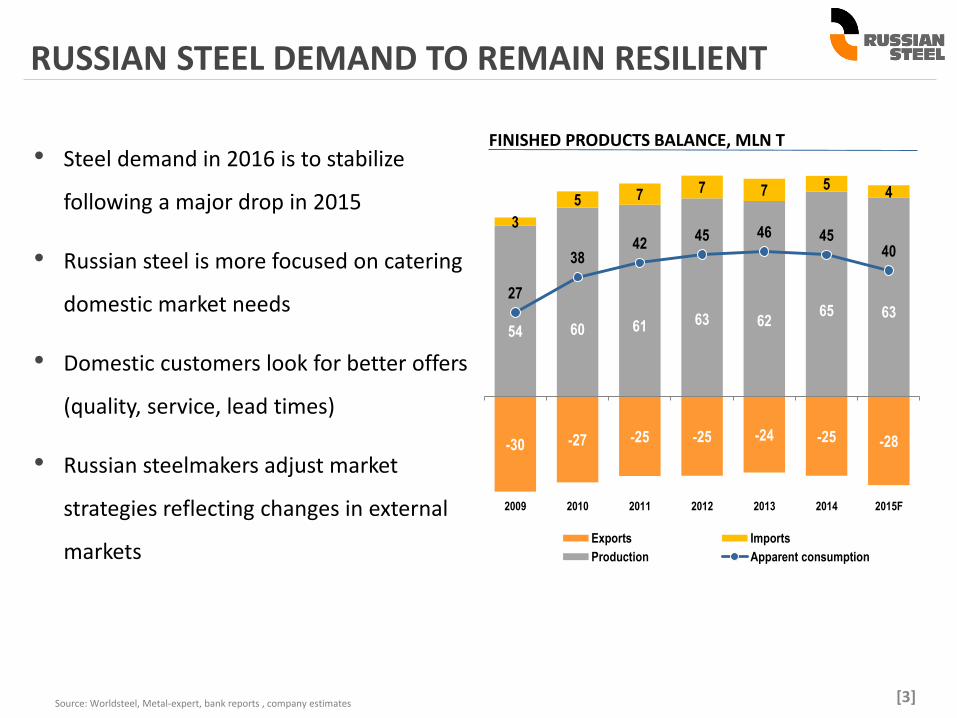

RUSSIAN STEEL DEMAND TO REMAIN RESILIENT

[3]Source: Worldsteel, Metal-expert, bank reports , company estimates

• Steel demand in 2016 is to stabilize

following a major drop in 2015

• Russian steel is more focused on catering

domestic market needs

• Domestic customers look for better offers

(quality, service, lead times)

• Russian steelmakers adjust market

strategies reflecting changes in external

markets

FINISHED PRODUCTS BALANCE, MLN T

54 60 61 63 6265 63

3

5 7 7 7 54

-30 -27 -25 -25 -24 -25 -28

27

3842

45 46 4540

2009 2010 2011 2012 2013 2014 2015F

Exports Imports

Production Apparent consumption

-

100

200

300

400

500

600

700

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

Nov

Dec

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015

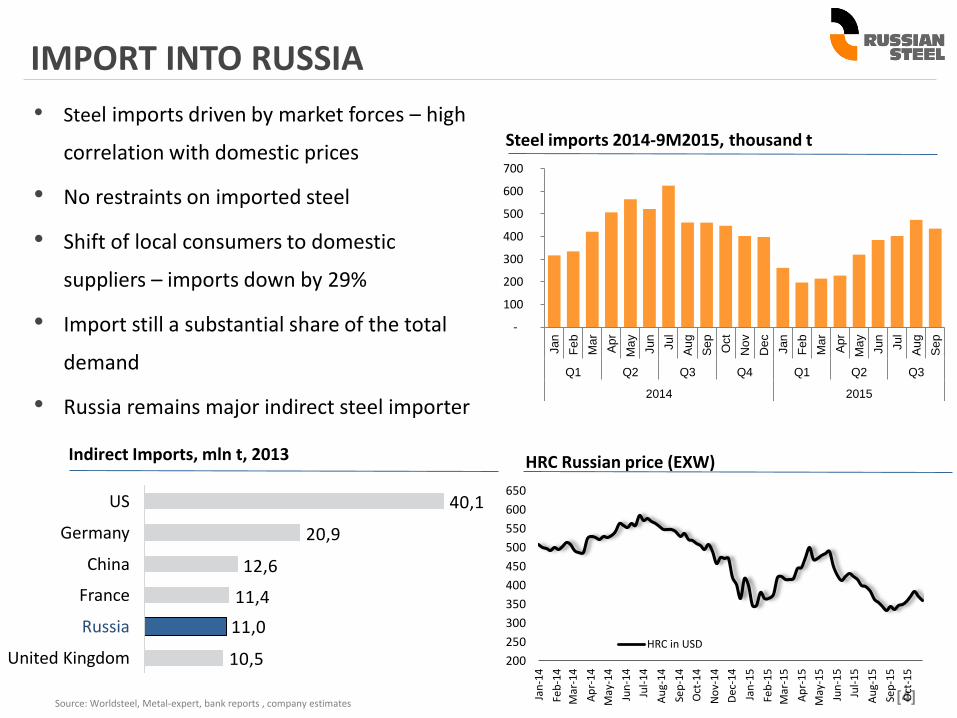

IMPORT INTO RUSSIA

[4]Source: Worldsteel, Metal-expert, bank reports , company estimates

• Steel imports driven by market forces – high

correlation with domestic prices

• No restraints on imported steel

• Shift of local consumers to domestic

suppliers – imports down by 29%

• Import still a substantial share of the total

demand

• Russia remains major indirect steel importer

Steel imports 2014-9M2015, thousand t

200

250

300

350

400

450

500

550

600

650

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

HRC in USD

HRC Russian price (EXW)

10,5

11,0

11,4

12,6

20,9

40,1

France

US

Germany

China

United Kingdom

Russia

Indirect Imports, mln t, 2013

EXPORT CAPABILITIES DETERIORATE

Источник: Russian steel, Metal Bulletin

Export from Russia is set to decline

• Export price pressure (down by 50%

since 2014) due to stiff competition

from China and CIS

• Average costs of production inflated by

tariffs and doubled capital costs

• Industrial inflation boosted

• Demand in key importing regions

declined / shifted to Chinese imports

• Russian exports started to halt (e.g. pig

iron)

[5]

6,4 5,9 5,9 6,6 7,1 6,9

6,0

-

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

Q1 Q2 Q3 Q4 Q1 Q2 Q3

2014 2015

Steel exports 2014-2015, mln t

Steel exports structure, 2014-10M2015

57%

31%

12%

56%

32%

12%

Semis Flat products Long products

2014

10M2015

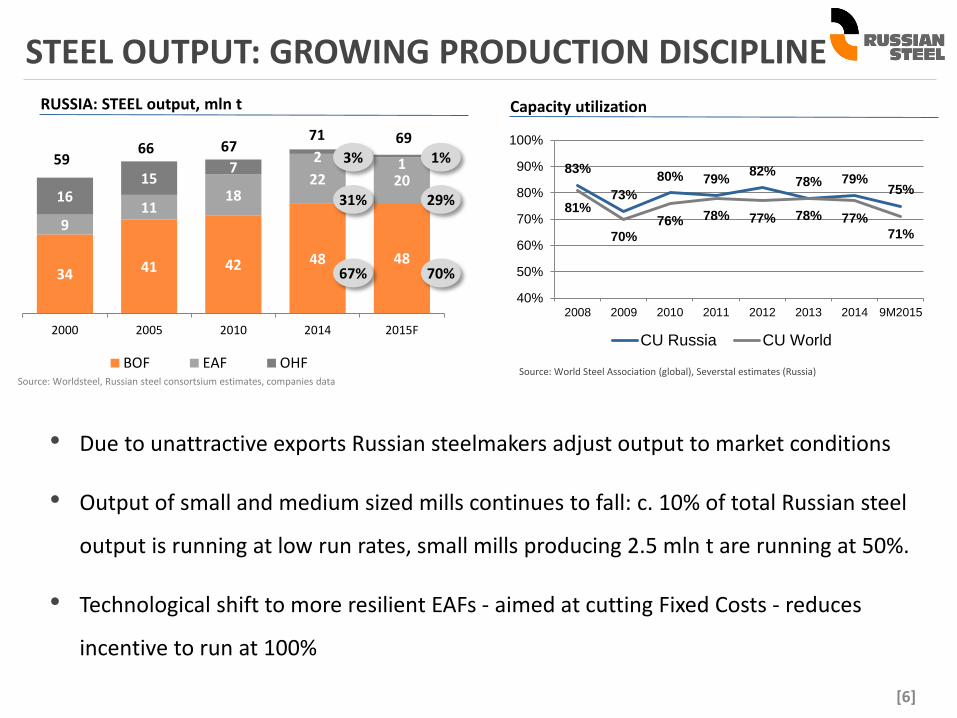

34 41 42 48 48

911

1822 20

1615

72 159

66 6771 69

2000 2005 2010 2014 2015F

BOF EAF OHF

STEEL OUTPUT: GROWING PRODUCTION DISCIPLINE

[6]

3%

31%

67%

Source: Worldsteel, Russian steel consortsium estimates, companies data

• Due to unattractive exports Russian steelmakers adjust output to market conditions

• Output of small and medium sized mills continues to fall: c. 10% of total Russian steel

output is running at low run rates, small mills producing 2.5 mln t are running at 50%.

• Technological shift to more resilient EAFs - aimed at cutting Fixed Costs - reduces

incentive to run at 100%

RUSSIA: STEEL output, mln t Capacity utilization

Source: World Steel Association (global), Severstal estimates (Russia)

1%

29%

70%

83%

73%

80% 79%82%

78% 79%75%

81%

70%

76% 78% 77% 78% 77%

71%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 9M2015

CU Russia CU World

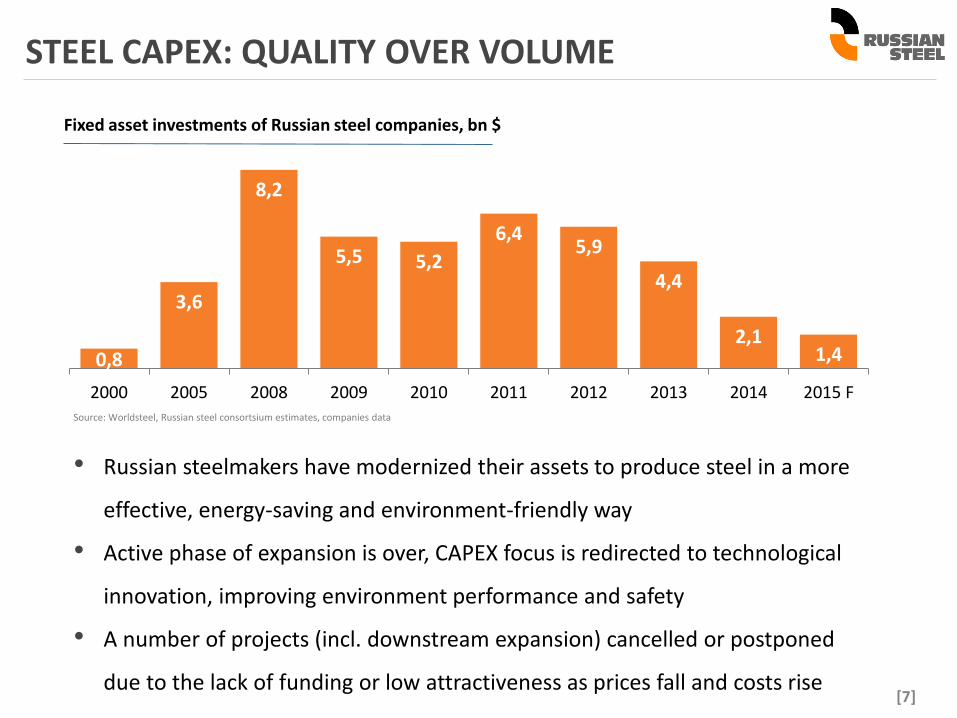

• Russian steelmakers have modernized their assets to produce steel in a more

effective, energy-saving and environment-friendly way

• Active phase of expansion is over, CAPEX focus is redirected to technological

innovation, improving environment performance and safety

• A number of projects (incl. downstream expansion) cancelled or postponed

due to the lack of funding or low attractiveness as prices fall and costs rise

STEEL CAPEX: QUALITY OVER VOLUME

[7]

Source: Worldsteel, Russian steel consortsium estimates, companies data

0,8

3,6

8,2

5,5 5,2

6,45,9

4,4

2,11,4

2000 2005 2008 2009 2010 2011 2012 2013 2014 2015 F

Fixed asset investments of Russian steel companies, bn $

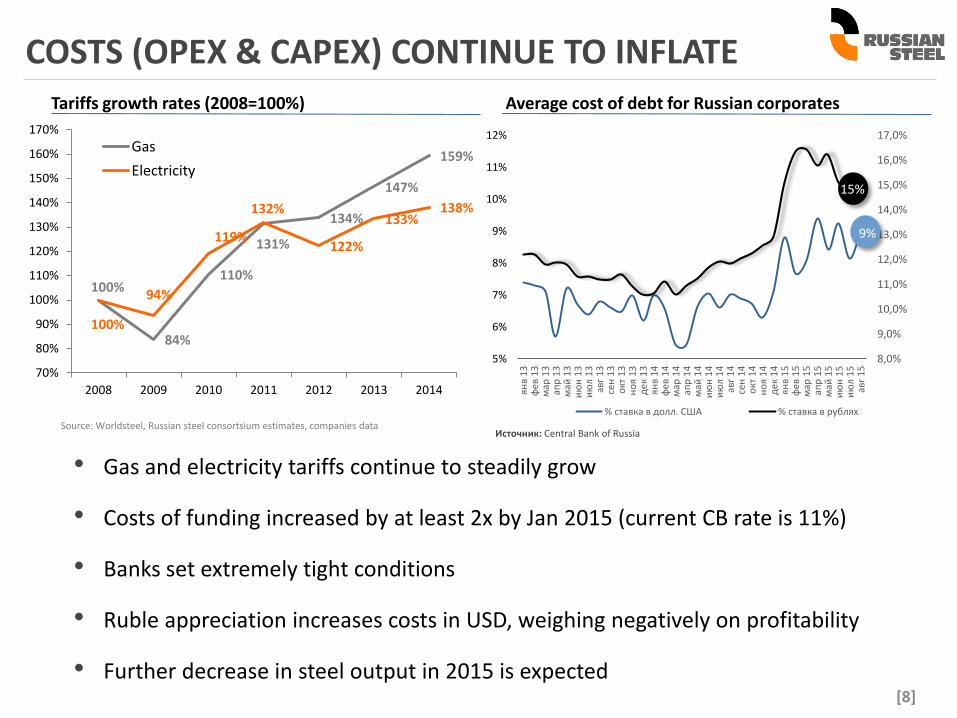

COSTS (OPEX & CAPEX) CONTINUE TO INFLATE

[8]

Source: Worldsteel, Russian steel consortsium estimates, companies data

• Gas and electricity tariffs continue to steadily grow

• Costs of funding increased by at least 2x by Jan 2015 (current CB rate is 11%)

• Banks set extremely tight conditions

• Ruble appreciation increases costs in USD, weighing negatively on profitability

• Further decrease in steel output in 2015 is expected

Average cost of debt for Russian corporates

100%

84%

110%

131%

134%

147%

159%

100%

94%

119%

132%

122%

133%138%

70%

80%

90%

100%

110%

120%

130%

140%

150%

160%

170%

2008 2009 2010 2011 2012 2013 2014

Gas

Electricity

Tariffs growth rates (2008=100%)

8,0%

9,0%

10,0%

11,0%

12,0%

13,0%

14,0%

15,0%

16,0%

17,0%

5%

6%

7%

8%

9%

10%

11%

12%

янв

13

фев

13

мар

13

апр

13

май

13

ию

н 1

3и

юл

13

авг

13

сен

13

окт

13

но

я 1

3д

ек 1

3ян

в 1

4ф

ев 1

4м

ар 1

4ап

р 1

4м

ай 1

4и

юн

14

ию

л 1

4ав

г 1

4се

н 1

4о

кт 1

4н

оя

14

дек

14

янв

15

фев

15

мар

15

апр

15

май

15

ию

н 1

5и

юл

15

авг

15

% ставка в долл. США % ставка в рублях

Источник: Central Bank of Russia

15%

9%

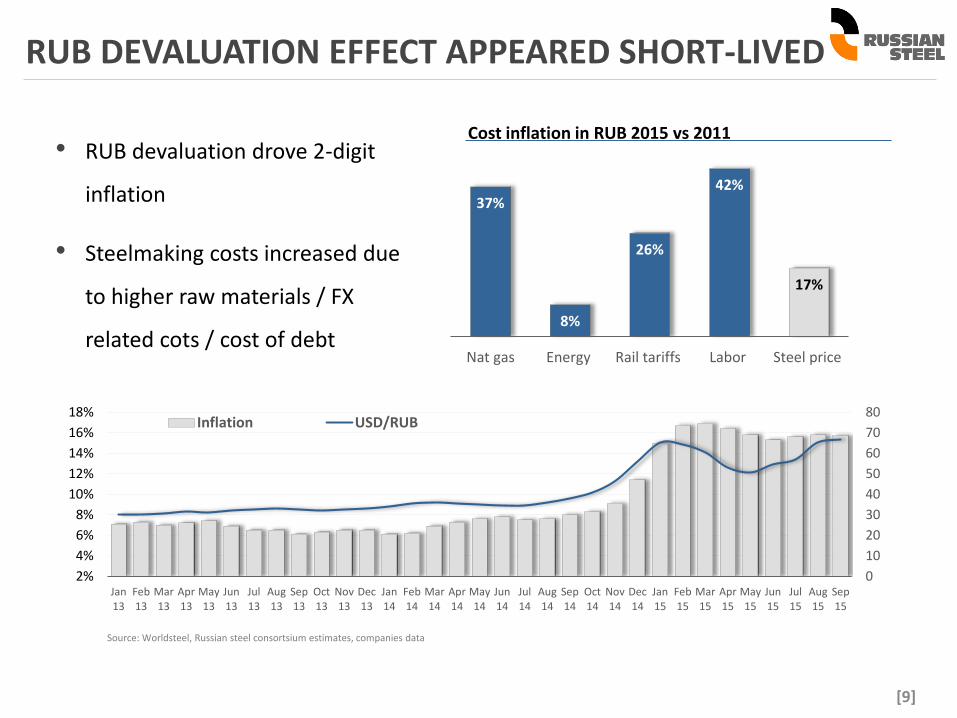

RUB DEVALUATION EFFECT APPEARED SHORT-LIVED

[9]

Source: Worldsteel, Russian steel consortsium estimates, companies data

• RUB devaluation drove 2-digit

inflation

• Steelmaking costs increased due

to higher raw materials / FX

related cots / cost of debt

0

10

20

30

40

50

60

70

80

2%

4%

6%

8%

10%

12%

14%

16%

18%

Jan13

Feb13

Mar13

Apr13

May13

Jun13

Jul13

Aug13

Sep13

Oct13

Nov13

Dec13

Jan14

Feb14

Mar14

Apr14

May14

Jun14

Jul14

Aug14

Sep14

Oct14

Nov14

Dec14

Jan15

Feb15

Mar15

Apr15

May15

Jun15

Jul15

Aug15

Sep15

Inflation USD/RUB

37%

8%

26%

42%

17%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Nat gas Energy Rail tariffs Labor Steel price

Cost inflation in RUB 2015 vs 2011

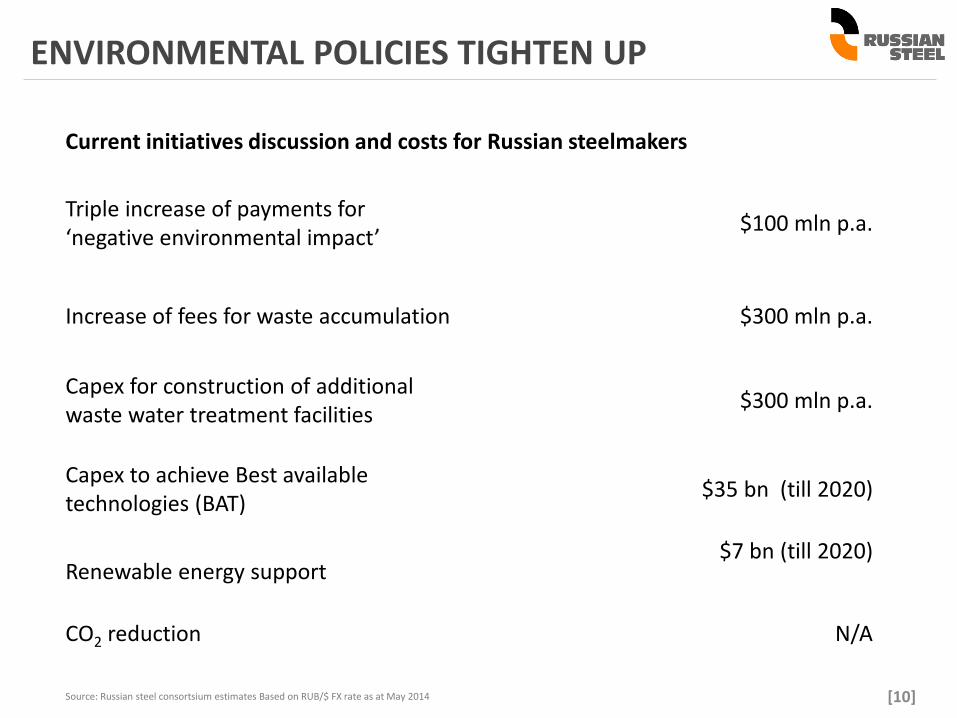

ENVIRONMENTAL POLICIES TIGHTEN UP

[10]Source: Russian steel consortsium estimates Based on RUB/$ FX rate as at May 2014

Current initiatives discussion and costs for Russian steelmakers

Triple increase of payments for ‘negative environmental impact’

$100 mln p.a.

Increase of fees for waste accumulation $300 mln p.a.

Capex for construction of additional waste water treatment facilities

$300 mln p.a.

Capex to achieve Best available technologies (BAT)

$35 bn (till 2020)

Renewable energy support$7 bn (till 2020)

CO2 reduction N/A

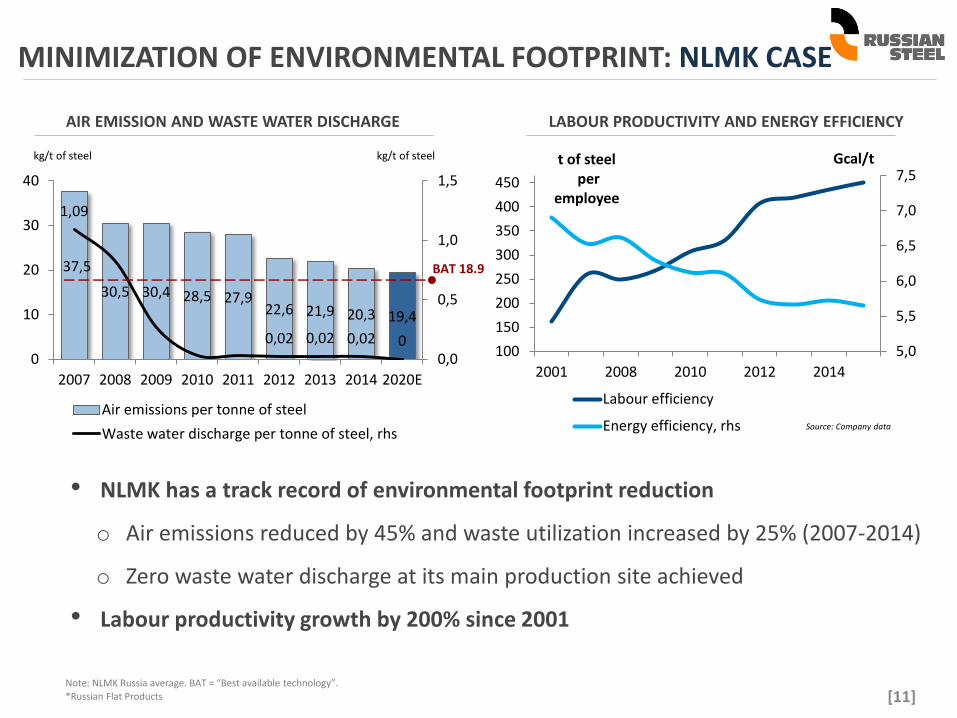

MINIMIZATION OF ENVIRONMENTAL FOOTPRINT: NLMK CASE

[11]

• NLMK has a track record of environmental footprint reduction

o Air emissions reduced by 45% and waste utilization increased by 25% (2007-2014)

o Zero waste water discharge at its main production site achieved

• Labour productivity growth by 200% since 2001

AIR EMISSION AND WASTE WATER DISCHARGE

37,5

30,5 30,4 28,5 27,922,6 21,9 20,3 19,4

1,09

0,02 0,02 0,02 00,0

0,5

1,0

1,5

0

10

20

30

40

2007 2008 2009 2010 2011 2012 2013 2014 2020E

Air emissions per tonne of steel

Waste water discharge per tonne of steel, rhs

Note: NLMK Russia average. BAT = “Best available technology”.

kg/t of steel kg/t of steel

BAT 18.9

*Russian Flat Products

LABOUR PRODUCTIVITY AND ENERGY EFFICIENCY

5,0

5,5

6,0

6,5

7,0

7,5

100

150

200

250

300

350

400

450

2001 2008 2010 2012 2014

Gcal/tt of steelper

employee

Labour efficiency

Energy efficiency, rhs Source: Company data

SUMMARY

[12]

779

• 2015 is challenging for the Russian economy, but stabilization is expected in 2016

• Contraction in machinery and construction sectors will negatively affect domestic

steel consumption

• Russian steel sector used super cycle profits to modernize production and improve

quality. Active phase of expansion is over. Next – shift towards efficiency

• Debt and fiscal pressure as well as unattractive exports lead to shutting down of

least effective capacities

• Ruble devaluation effect was short-lived and translated into cost inflation

• Steelmaking costs in Rub inflated, making the sector more vulnerable to FX swings

• Government policies tighten up, increasing administrative burden and private

expenses on regulation compliance

[13]

779

Thank You!