samplepf

DESCRIPTION

Sample PF for us to explore!TRANSCRIPT

Elliott Gue, Editor Volume XXXVI, Number 1 • January 14, 2009

Legendary financier Baron Rothschild once advised investors to “buy when there’s blood in the streets, even if that blood is your own.”

Investors like Baron Rothschild and Warren Buffet became rich in-vesting in markets just like today’s. Panic- and cash-motivated selling has pushed many high-quality stocks to the lowest valuations seen in decades. For investors with more than a six- to 12-month investing horizon, the cur-rent market affords the best opportu-nities of the past two decades.

At right, we outline our strategy for weathering the current market turmoil and positioning our portfoli-os to benefit from the eventual recov-ery. In particular, we highlight three key sectors: health care, energy and consumer staples. Health care and consumer staples offer defensive growth potential—investors flock to these groups in unsettled markets.

Although out of favor in the short term, the energy patch will benefit from strong growth in energy de-mand from the developing world, coupled with continued supply con-straints.

We’re also repositioning our port-folios to reflect a core tenet of any ef-fective investing approach: diversifica-tion. Part of that mantra is a balance between growth- and income-orient-ed investments.

Roger Conrad has managed the PF Income Portfolio for more than 20 years, with stellar long-term re-sults. In the second article on p. 3, he outlines his approach to the current market environment. Roger will also be picking up coverage of several stocks formerly part of the Growth Portfolio. [230]

Marketwatch

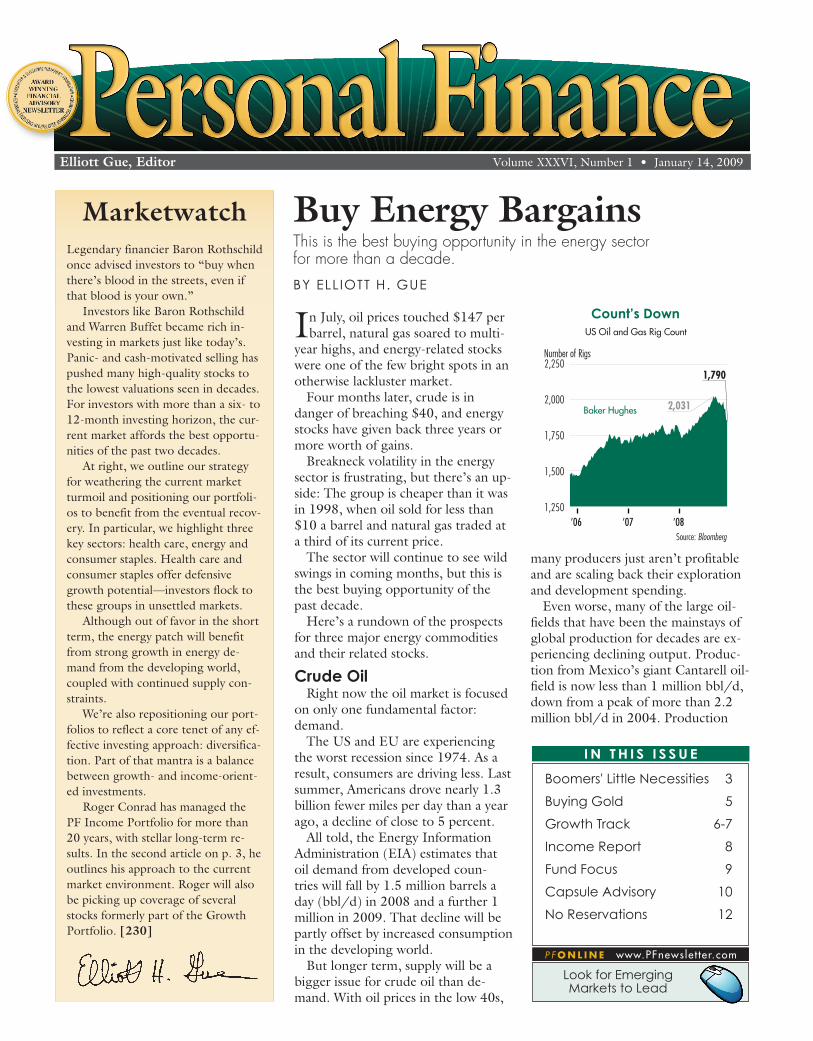

In July, oil prices touched $147 per barrel, natural gas soared to multi-

year highs, and energy-related stocks were one of the few bright spots in an otherwise lackluster market.

Four months later, crude is in danger of breaching $40, and energy stocks have given back three years or more worth of gains.

Breakneck volatility in the energy sector is frustrating, but there’s an up-side: The group is cheaper than it was in 1998, when oil sold for less than $10 a barrel and natural gas traded at a third of its current price.

The sector will continue to see wild swings in coming months, but this is the best buying opportunity of the past decade.

Here’s a rundown of the prospects for three major energy commodities and their related stocks.

Crude OilRight now the oil market is focused

on only one fundamental factor: demand.

The US and EU are experiencing the worst recession since 1974. As a result, consumers are driving less. Last summer, Americans drove nearly 1.3 billion fewer miles per day than a year ago, a decline of close to 5 percent.

All told, the Energy Information Administration (EIA) estimates that oil demand from developed coun-tries will fall by 1.5 million barrels a day (bbl/d) in 2008 and a further 1 million in 2009. That decline will be partly offset by increased consumption in the developing world.

But longer term, supply will be a bigger issue for crude oil than de-mand. With oil prices in the low 40s,

many producers just aren’t profitable and are scaling back their exploration and development spending.

Even worse, many of the large oil-fields that have been the mainstays of global production for decades are ex-periencing declining output. Produc-tion from Mexico’s giant Cantarell oil-field is now less than 1 million bbl/d, down from a peak of more than 2.2 million bbl/d in 2004. Production

Buy Energy Bargains This is the best buying opportunity in the energy sector for more than a decade. By Elliott H. GuE

Source: Bloomberg

Count’s Down

Number of Rigs2,250

2,000

1,750

1,500

1,250’06 ’07 ’08

2,031

1,790

US Oil and Gas Rig Count

Baker Hughes

Boomers' little Necessities 3

Buying Gold 5

Growth track 6-7

income Report 8

Fund Focus 9

Capsule Advisory 10

No Reservations 12

I N T H I S I S S U E

P F O N L I N E www.PFnewsle t ter.com

look for Emerging Markets to lead

is also falling faster than expected in Russia and the North Sea.

With production from older fields declining and new projects delayed if not cancelled, global oil output will fall rapidly. The longer oil remains be-low $70, the faster this decline will be.

As the global economy recovers in late 2009 and oil demand stabilizes, falling oil supplies will quickly balance the rising demand and crude will likely top $100 again in 2010.

To play crude oil, focus on two groups: the Super Oils and select ser-vices companies.

Most of the super majors have pristine balance sheets and huge cash positions; for example, ExxonMobil (NYSE: XOM) holds $38 billion in cash, while Chevron (NYSE: CVX) holds $11 billion. Given the still-shaky credit markets, investors are showing a preference for companies with solid financial positions.

In addition, the Super Oils have a long history of showing profitability even in low commodity price environ-ments. Chevron and Exxon remained profitable during the vicious bear mar-ket in energy prices in 1998, handing investors average annualized returns of 14 and 16 percent, respectively, in what was a bad decade for energy-related firms.

Our favorite Super Oil is longtime Income Portfolio denizen Chevron. The company’s production costs are less than $20 a barrel, and of all the majors Chevron has the best chance of showing real production growth

in coming years. The stock is also the cheapest it’s been since the late 1990s. Chevron is a buy.

Oil services companies such as Growth Portfolio holding Weather-ford International (NYSE: WFT) are more sensitive to commodity prices than the Supers. These companies perform vital functions related to oil and natural gas exploration and production; declines in drilling activity directly hit the bottom line.

But the oil business is becoming increasingly service-intensive. With giant, easy-to-produce onshore fields seeing flat or declining production, companies are targeting more com-plex deposits such as deepwater plays. These fields require advanced technol-ogies and techniques to be exploited efficiently.

Weatherford is a leader in services related to mature fields. To squeeze more oil out of these fields, producers are drilling complex horizontal wells and targeting smaller pockets of oil within existing fields.

Moreover, Weatherford has be-come a major player in the integrated project management (IPM) business. Under these deals, state-owned na-tional oil companies pay Weatherford a fee to manage specific oil develop-ment projects on their behalf. IPMs are typically long-term deals that offer Weatherford a steady, reliable source of revenue.

Weatherford will undoubtedly see a slowdown in its business as global oil

development projects are delayed due to weak commodity prices. But trad-ing at five times next year’s projected earnings, the stock has already priced that in. Buy Weatherford Internation-al under 17.50.

Natural GasIn the short term, natural gas looks

much better than oil. Natural gas demand is less sensitive

to economic growth than oil demand. Demand for gas as an electricity fuel has been climbing in recent years because gas is a more environmentally friendly fuel than coal. And as a rule of thumb, a 1 percent decline in US GDP will result in less than a 0.5 per-cent decline in electricity demand.

Cold weather drives demand for gas heating. This year temperatures have been below normal across much of the Northeast and Midwest. And forecasters are predicting it’s going to get colder. That’s good news on the demand side.

On the supply side, the focus remains growth in production from unconventional gas fields such as the Barnett Shale of Texas and Haynes-ville Shale in Louisiana. In the first half of this year, surging production from these fields threatened a gas glut in the US.

The graph “Count’s Down” shows the US active rig count, a measure of how many rigs are drilling for oil or gas in the US. The rig count has declined precipitously in recent weeks; producers are scaling back their drill-ing plans as a result of weak gas prices. Less drilling activity spells lower gas production.

Growth Portfolio denizen EOG Resources (NYSE: EOG) remains my top play on natural gas.

The company has a total of $1.9 bil-lion in debt and close to $900 million in cash; with a market cap of $20 bil-lion, EOG has a clean balance sheet. EOG doesn’t need to access the credit markets to fund its planned drilling

PERSONAL FINANCE (ISSN 0164-7768) is published semi-monthly. © 2009 by KCI Communications, Inc. Address editorial correspondence to KCI Communications, 7600A Leesburg Pike, West Building, Suite 300, Falls Church, VA 22043-2004. EDITOR: Elliott H. Gue; EXECUTIVE EDITOR: Gregg Early; MANAGING EDITOR: David Dittman; ASSOCIATE EDITORS: Roger S. Conrad, Yiannis G. Mostrous, Benjamin Shepherd; RESEARCH EDITOR: Peter Staas; DIRECTOR OF DESIGN AND PRODUCTION: Steve Kizer; CONTRIBUTING EDITORS: John Lumbard, Ron Faucheux, Adrian Day; CUSTOMER SER-VICE DIRECTOR: Andrea Prendergast; Product Manager: Heather Snead; MARKETING DIRECTOR: Doug Hill; PUBLISHER: Walter Pearce. SUBSCRIPTIONS: 24 issues, $97; in Canada, US$121; Interna-

tional US$199. POSTMASTER: Send address changes to: 7600A Leesburg Pike, West Building, Suite 300, Falls Church, VA 22043-2004. Send subscription-related correspondence to above address; enclose mailing label from a recent issue and a new address. For customer service, call 800-832-2330 or 703-394-4931. The information contained in Personal Finance has been carefully compiled from sources believed to be reliable, but its accuracy is not guaranteed. KCI Communications, Inc., its officers and owners, the editors of Personal Finance and their respective affiliates, or accounts managed by such persons, may from time to time have a position in investments referred to in this newsletter. Periodicals postage paid at Falls Church, Va., and addi-tional mailing offices. Printed in U.S.A. R136740115.

Recent Price to Price to Company (Exchange: Symbol) Price Sales Book WebsiteAvaya (NYSE: AV) $15.56 1.5 32.4 avaya.comHutchison Whampoa (OTC: HUWHY) 44.50 3.8 1.3 hutchison-whampoa.comInter-Tel (NSDQ: INTL) 29.95 2.0 3.9 inter-tel.comNEC Corp. (NSDQ: NIPNY) 7.84 0.5 2.1 nec.comQwest Communications (NYSE: Q) 4.25 0.5 N/A qwest.comVerizon Communications (NYSE: VZ) 37.77 1.5 3.0 verizon.comVodafone Group (NYSE: VOD) 26.19 3.2 0.7 vodafone.comFootnote here

Real Ringer-Dingers

PERSONAL FINANCE2 January 14, 2009

www.PFnewsle t ter.com 703-394-4931 January 14, 2009 3

activity. EOG has a strong emerging gas

prospect in Canada as well as signif-icant positions in major US fields. Although it will take time for pipe-line capacity in Canada to get up to speed, this unconventional gas play could rival the big US fields; EOG estimates that its reserves in the re-gion could top 6 trillion cubic feet. Buy EOG Resources under 100.

King CoalCoal isn’t a dying fuel. As the pie

chart “High Heat” shows, coal ac-counts for close to half the world’s electricity generation, 80 percent of China’s power and close to 70 percent of India’s.

Coal has a major advantage over other fossil fuels: It’s cheap and abundant. Even with gas prices at current depressed levels, coal still costs less than half as much.

Demand for coal is also more stable than demand for oil or natu-ral gas. Coal-fired electric plants are typically baseload generators; these plants run almost constantly regardless of demand conditions.

Coal prices have declined from their summertime highs of over their summertime highs of over their summertime highs of over their summertime highs of over their summertime highs of over their summertime highs of over their summertime highs of over their summertime highs of over their summertime highs of over $130 per short ton to around $70 today. But, in late 2007 coal traded under $60 per ton and in 2006 it was under $40. That’s a steady, long-term increase, even if it’s off its highs.

The best play is Peabody Energy (NYSE: BTU). Peabody’s main coal reserves are located in the western US in an area known as This is the largest and fastest-grow-ing source of coal in the US, and Peabody owns some of the lowest-cost mines there.

Buy new Growth Portfolio recommendation Peabody Energy under 32. [1340]

Elliott H. Gue is editor of Personal Finance and The Energy Strategist.

The health care sector has always been one of the most predicable

performers in a recession. That’s particularly true now, as an

aging population has become increas-ingly reliant on medicine to maintain longevity. As shown in the graph “Winning Health,” the S&P 500 Health Care Index has outperformed the broader S&P 500 by more than 10 percent.

But in a recession, even a depend-able sector requires a high degree of selectivity. Health care systems have been slaughtered this year as routine health maintenance practices such as annual physicals are put off and patients are less likely to go to the doctor for every sniffle.

Some of the biggest drugmakers have been hammered because their revenues are primarily generated by discretionary drugs such as erectile dysfunction treatments; others are under pressure from expiring periods of exclusivity on blockbuster medica-tions.

To succeed, focus on the companies that provide the products and services that, whether you’re rich or poor, you have to have when the time comes.

Stericycle (NSDQ: SRCL) operates in one of the most recession-proof corners of the health care market; medical waste.

Through its large network of collec-tion points and a fleet of trucks, Steri-cycle collects the medical waste gener-ated by 410,000 customers, ranging from individual doctors’ offices and hospitals to medical laboratories.

It also handles recalled prescription drug and medical device disposal. Medical waste processing is a highly regulated and dangerous industry that requires specialized procedures.

Suffice it to say, the barriers to entry are very high, giving Stericycle a competitive advantage that protects it from economic cycles; no matter what the economy is doing, medical waste

must be properly handled.Stericycle currently holds about 11

percent of the US market share and operates in the UK, Ireland, Canada, Mexico and Argentina, too. It also has licensed facilities in Japan, South Africa and Brazil, giving it a degree of insulation from US market condi-tions, though it is exposed to some degree of currency risk.

More than 95 percent of revenues are generated under long-term con-tracts with automatic renewals, most of which also include price increase pass-through provisions. Stericycle doesn’t have to wait for the next renewal period to pass along higher processing costs. And its customer base is well diversified

On a year-to-date basis through the third quarter of 2008, revenues have risen 18.9 percent, helping to push earnings per share (EPS) up 18.2 percent to $1.24.

Fourth quarter earnings should be steady to growing, with revenues getting a boost in the first half of the year. Given the company’s fleet of trucks, fuel costs burn up 7.6 percent of revenues. Falling fuel costs go straight to the bottom line.

With great prospects for even higher profits next year, Stericycle is a buy below 60.

The population in the developed world is growing and graying. That’s led to a higher incidence of heart

10%

0

-10

-20

-30

-40

-50J J JF M MA A S O N D

Winning HealthTotal Return

S&P 500 Health Care Index

S&P 500

Source: Bloomberg

2008

-26.24%

-36.57%

Boomers Little NecessitiesHealth care is a safe port in tough economic times. No matter how the markets or the economy may be performing, people always get sick.By BENjAMiN SHEpHERd

PERSONAL FINANCE4 January 14, 2009

disease and the need for long-term treatments such as pacemakers.

As of 2002, about 3 million people worldwide had pacemakers implanted, with an average 600,000 installations annually. And for pacemakers to func-tion, they must have a power source.

Greatbatch (NYSE: GB) is one of the world’s largest manufacturers of implantable power sources as well as batteries for other medical equipment and commercial applications.

In the third quarter, 86.1 percent of revenues were generated by sales of implantable medical components, with 46.1 percent of that in cardiac rhythm management applications, i.e. pacemakers. The company also recently introduced a wireless sensing product line for commercial applica-tions, allowing remote monitoring of pressures, flows and temperature of fluid systems.

Growth has been strong; in the third quarter, medical sales were up 75 percent and commercial sales were up 58 percent over the same period last year. Operating margin improved to 14.2 percent.

Part of the margin improvement was due to a program of consolidating operations after the company closed several facilities in July and expanded its research and development opera-tions. Greatbatch is a buy up to 25.

Laboratory Corp of America (NYSE: LH) is a clinical laboratory company that offers comprehensive diagnostic testing services. It’s one of the largest lab services in the US, currently holding about 8 percent of market share in a $52 billion industry.

It’s one of the more recession-proof plays on health care because testing volume can only fall so much. People will always get sick, and lab tests have taken on a critical role in the diagnos-tic process.

LabCorp is also benefiting from the fact that no matter the economic con-ditions, Americans aren’t getting any younger. An average middle-aged pa-tient will have five lab tests performed per year; by the time she reaches 75 the number of tests increases to 13.

During the past five years, Lab-Corp’s revenues have been growing at an annual rate of about 8.5 percent, with EPS increasing 18.6 percent. That trend looks set to hold in 2009.

Year-to-date, revenue is up 10.6 per-cent to almost $3.4 billion with EPS growing 11.2 percent to $3.48.

Revenue streams are diversified, with patients accounting for 9 percent on a per-payer basis, with 19 percent gener-ated through government programs.

About 28 percent of revenue is gen-erated by companies contracted with LabCorp to perform routine drug screens, and the remainder comes from managed health care plans. That diversification helps to insulate the company from downturns in spending from specific payers.

With steady revenues and business prospects, Laboratory Corp of Ameri-ca is a buy under 67.

Although sales of some drugs may fall off a cliff in a recession, consumers can only cut back so much on pre-scription drug spending.

Medco Health Solutions (NYSE: MHS) is a pharmacy benefit manager, filling more 560 million prescriptions a year for health insurers, government agencies and corporations primarily through mail order. It’s also working to develop a presence in Germany, where it recently acquired a majority interest in Europa Apotheek Venlo.

Prescription drug sales slowed considerably in 2008 because cosmetic drug sales weaken in a recession. But 96 percent of drug costs in the US are generated by chronic disease treat-ment, which makes ceasing drug treat-ment extremely impractical.

The incoming Obama administra-tion could also prove a boon for the company. The President-elect em-phasized broadening the universe of insured Americans, encouraged further development of health care informa-tion technology and promoted the use of lower cost generic drugs during the campaign. It’s also anticipated that the new administration will make the

process of developing and marketing generic drugs much simpler.

Filling prescriptions for generic drugs is the core of the company’s profits because it realizes much higher margins on those sales. And beginning in 2009, more than $65 billion worth of branded drugs will lose patent pro-tection over the ensuing five years.

The primary risk associated with Cubist is that despite ongoing ef-forts to diversify, it’s totally reliant on revenues from a single drug, Cubicin. Primarily used to treat methicillin-re-sistant strepyloccocus aureus infections (MERSA), a drug-resistant staph in-fection that’s made the news in recent years, revenues generated by the drug are steady to growing.

The period of exclusivity on Cubicin patent on the active compound in the drug that doesn’t expire until 2016, version much more difficult.

To help offset that risk, Cubist has one drug currently in Phase II trials. loss during surgery; two others are about to begin clinical trials sometime next year.

It’s also closed a marketing deal with AstraZeneca for its antibiotic with AstraZeneca for its antibiotic with AstraZeneca for its antibiotic Merrem. While that deal is already generating revenue, it takes years for new drugs to complete trials and come to market.

But the company is on solid ground after turning to profitability last year, and its marketing deal will only add to the bottom line. Total revenues also shot up 41 percent to $112.4 million in the same period.

Cubist Pharmaceuticals is a buy up to 27 for those with a higher tolerance for risk. [1330]

Benjamin Shepherd is an associate editor of Personal Finance and editor of Louis Rukeyser’s Mutual Funds.

Recent Price to Price to Return on Company (Exchange: Symbol) Price* Book* Sales* Equity# SpecialityCubist Pharmaceuticals (NSDQ: CBST) $24.53 9.4 4.3 45.7% PharmaceuticalsGreatbatch (NYSE: GB) 23.64 1.6 1.0 3.9 Medical DevicesLaboratory Corp of America (NYSE: LH) 63.05 4.1 1.6 25.2 Diagnostic TestingMedco Health Solutions (NYSE: MHS) 41.64 3.5 0.4 16.6 Pharmacy BenefitsStericycle (NSDQ: SRCL) 54.14 6.7 4.5 19.8 Medical Waste Disposal*As of 12/08/08. #Trailing 12 months. Source: Bloomberg

Healthy Picks

www.PFnewsle t ter.com 703-394-4931 January 14, 2009 5

real value will come under scrutiny, allowing gold to break out. This, how-ever, is a couple years down the road.

Contrary to what gold bashers would like us to believe, gold has per-formed well this year. It’s moderately down in price since early January, but it performed solidly last month when it gained 13 percent—its best monthly performance since 1999. This perfor-mance took place while the US dollar was relatively strong and oil was weak.

That said, dollar weakness is a big posi-tive for gold. The dollar’s rally since the summer has contributed to gold’s weakness, as have the forced liquidations among hedge funds and other investors as they continued to liquidate their hugely leveraged posi-tions.

On the physical demand side, the dollar rally has also curbed appetites in some emerging markets. The weak-ening Indian rupee led to high gold prices in the local currency last month (a 32 percent year-over-year increase), so traditionally strong gold imports in India were down 30 percent in November.

This weakness came after strong de-mand from India in October, spurred by of strong jewelry sales during Diwali, the festival of lights and the Hindu version of Christmas.

Chinese demand, on the other hand, remains relatively strong as the renminbi’s weakness against the dollar remains subdued.

Bullion is the best way to own gold, though the popular alternative of an exchange traded fund (ETF) is a close

The best reason for being bullish on gold is gold itself. The yel-

low metal has never been refused as a means of payment, has no substitutes and carries no counterparty risk.

The demand for gold we’ve seen during the past three years has made it one of the world’s strongest curren-cies. And in today’s world of massive deficit spending and financial imbal-ances, expect demand for gold to increase and prices to move up from here.

Emerging Asian nations have been key demand catalysts. India has long been the big gold consumer, but China is also becoming a force as its middle class grows. Recent reports indicate that China is considering adding to its existing 600 tons of gold reserves—see the graph “It’s All Yel-low.” Analysts expect China to buy up to 4,000 tons in an effort to diver-sify its huge foreign exchange (FX) reserves.

Such a move would bring China’s gold holding to just 5 percent of FX reserves and would equal 1.4 times total annual mine production. Ac-cording to official data, China hasn’t purchased any gold since 2002.

Given the importance China’s reserves will play in easing the impact of the global recession, diversifying its paper currency holdings with gold is now a smart alternative.

Gold Stays AfloatThe scars of the current crisis will

stay with the global economy for a while, so gold prices will remain elevated for some time. Furthermore, declining production, low sales from official reserves and steady consumer and investor demand will ensure the trend continues for longer than many market observers expect.

And gold prices can reach unprec-edented levels once the rest of the world decides that the US monetary authorities have abused the dollar’s status as the reserve currency of the world. When this happens, the dollar’s

second. One of the most popular ETFs is SPDR Gold Trust (NYSE: GLD), and it’s a buy at current prices.

The Stock Gold stocks will catch up as long as

gold prices remain on the high side.Goldcorp (NYSE: GG) is our favor-

ite major gold company. The acqui-sition of Glamis Gold in late 2006

vaulted Goldcorp to the forefront of glob-al producers. The company now has growing production, low cash costs, solid earnings generating ability, large reserves, a strong balance sheet and one of the most respected man-agement teams in the industry.

It doesn’t hedge its gold production and pays dividends monthly. It’s gold

producers, as its main operaArgentina, Mexico and Australia.

The company’s costs should remain below $300 an ounce given to cost control. According to industry sourc-es, the company’s strong financial position allows it to profitif the price of gold is between $600 and $700 an ounce.

Goldcorp’s newest project is the Penasquito mine in Mexico; once completed it’s expected to produce 400,000 ounces a year.

The company boasts one of the best liquidity positions in the inin cash and working capital of $683 milrevolving es, the strong financial es, the compa-ny’s strong financial es, the company’s strong financial credit facility, which, as of Sept. 2008, was undrawn. Buy Goldcorp up to 35. [760]

Yiannis G. Mostrous is associate edi-tor of Personal Finance and editor of Silk Road Investor.

20 4

Source: World Gold Council

It’s All Yellow

Tons (x1,000) As of 09/31/086 108

USGermany

FranceItaly

SwitzerlandJapanChinaRussiaIndia

8,133.53,413.1

2,540.9

2,451.8

1,064.1765.2

600.0472.6

357.7

Official Gold Reserves

Buying GoldGold is a great hedge in any economic environment, and now is a great time to give it a place in your portfolio. By yiANNiS G. MoStRouS

PERSONAL FINANCE6 January 14, 2009

Investors have been hit with a steady diet of negative news in recent

weeks, including a weak start to the holiday shopping season, terror attacks in India and the worst jobs report in 34 years.

But despite the headwinds, the major US averages haven’t broken their November lows. Investors have become accustomed to the steady drumbeat of pessimism and are starting to expect and anticipate negative head-lines. This is an early sign of a bottom in the making.

There’s little doubt the economy will continue to deteriorate in coming months; I’m not looking for a recovery until the back half of 2009. However, the broader market’s decline of nearly 50 percent from its highs has already priced in a deal of that negative news.

One thing is certain: Volatility will remain the order of the day. The past three months have brought the most extreme volatility for the S&P 500 in the history of the index.

This is partly due to the cloudy eco-nomic outlook, partly to cash-motivat-ed selling by institutional traders. Insti-tutional traders strapped for cash to meet redemption requests and desper-ate to reduce their borrowings have been forced sellers of equities for months now.

My strategy for dealing with the current rollercoaster market is two-fold: focus on companies with reces-sion-resistant growth characteristics, and take advantage of depressed valua-tions in groups with solid long-term growth prospects.

Above all, however, stay diversified. Diversification doesn’t mean buying 10 stocks or funds in the same industry group that trade as a pack. Rather, in-vestors should consider buying a hand-ful of best-of-breed stocks across sever-al sectors.

New BloodMy favorite sectors right now are

health care, energy and consumer sta-ples. I favor healthcare for its defen-sive, recession-resistant growth char-acteristics. In the last issue, we added pharmaceutical giant Novartis and smaller drugmaker Baxter Interna-tional to the Growth Portfolio.

But pharmaceuticals companies are only one segment of the health care industry. As Benjamin Shepherd ex-plains on p. 3, the medical waste dis-posal business is an even more reces-sion-resistant business.

Thanks to strict government regu-lation and complex procedures for processing hazardous wastes, it isn’t easy for new competitors to enter this business. In addition, Stericycle oper-ates primarily under long-term con-tracts that allow it to pass through some of its rising costs to customers; this guarantees the company steady revenues.

A play on medical waste, new Growth Portfolio addition Stericy-cle is a buy up to 60.

Coal mining stocks remain among the most underappreciated stocks in the energy sector. But coal generates most of the world’s electricity, and coal prices have outperformed both oil and natural gas this year.

Thanks to strong growth in de-mand from emerging markets, coal’s expected to be the world’s fastest growing fossil fuel in coming years. Coal consumption has already grown at three times the pace of oil demand over the past five years.

Hedge funds were big holders of coal companies in the first half of the year; cash-motivated selling pressure has pushed the best companies in the sector to unheard of valuations. As noted on p. 3, we’re adding mining giant Peabody Energy to the Growth Portfolio as a play on the group.

Finally, as Yiannis Mostrous ex-plains on p. 5, gold and gold mining stocks are the ultimate hedge. In peri-ods of high inflation, gold—a store of value for thousands of years—has his-torically performed well.

The US and foreign governments are currently in the process of pump-ing trillions of dollars into the global economy in an effort to soften the blow of the financial crisis and global cussing unconventional monetary pol-icy tools such as buying bonds directly to bring down long-term interest rates. The government is basically at-tempting to inflate our way out of a depression.

Gold can also be a hedge against turmoil. In periods of severe financial unrest, investors tend to run for the security of gold.

The best-positioned gold miner is Goldcorp; we’re adding the stock to the Growth Portfolio as a buy under 35.

Portfolio News and MovesOil tanker giant Frontline declared

a 50 cent dividend for the quarter, far lower than the $3 it paid last quarter.

Earnings for tanker companies are highly dependent on tanker rates, the daily fee tanker companies charge to

Diversified and OpportunisticTo survive these uncertain times, we’re adding to our health care exposure and establishing a position in the ultimate hedge, gold.By Elliott H. GuE

Investors should focus their attention on my three top sectors: health care, energy and consumer staples. I’m adding stocks in two of these groups, medical waste specialist

Stericycle and coal mining giant Peabody Energy. Amid a volatile and uncertain market and economic environment, it’s time to boost your exposure to the ultimate hedge, gold.

We’re adding gold mining giant Goldcorp to the Portfolio.

Source: Bloomberg

Price

$60

50

40

30

20

10

Value Mine

J’08

F M A M J J A S O N DD

$51.06

Current

High

$27.03

Goldcorp

THEGROWTH TRACK

www.PFnewsle t ter.com 703-394-4931 January 14, 2009 7

ship oil. Tanker rates, in turn, fluctu-ate seasonally and in line with near-term ship supply and demand.

Tanker rates have been hit in recent weeks. One major reason for this is that OPEC countries are cutting oil output to stem the decline in oil pric-es. Falling OPEC supply means there’s less oil to be shipped on tank-ers; close to 90 percent of all oil mov-ing out of the Middle East is trans-ported by tanker.

There are some offsets to this headwind. Chief among those is that the credit crunch has made it tough for companies to finance the construc-tion of new ships, so ship supply is unlikely to expand as quickly as some analysts had projected.

Due to the cyclical and volatile na-ture of the tanker business, it’s not unusual to see dividends fluctuate from quarter to quarter. Given the muted reaction in the stock in the days after the cut, investors had clearly already priced in the move.

The tanker market has weakened but, unlike the dry bulk shipping business, rates haven’t collapsed. I see Frontline’s current lowered dividend highlighted in the article. I’m there-fore cutting Frontline to a hold.

BreitBurn Energy Partners and Linn Energy are publicly traded part-nerships (PTP) that focus on oil and natural gas production. Like most PTPs, both firms are set up to gener-ate strong, reliable cash flows so they can pay out sizeable yields.

Volatile commodity prices mean that the oil and gas production busi-ness doesn’t offer steady cash flows. To combat that problem, both Breit-Burn and Linn hedge their exposure to commodities.

That said, I prefer Linn Energy to Breitburn. Linn is close to 100 per-cent hedged on all its oil and gas pro-duction through the end of 2011. Whether oil trades at $60 or $160, it won’t really affect Linn’s cash flows.

Natural gas trades at different pric-es in different parts of the US, and those prices can be wildly divergent at times. Therefore, using the NYMEX contract based on prices at the Henry Hub in Louisiana may not represent a complete hedge for a producer like Linn—this is known as basis risk.

But Linn has actually taken on hedges to eliminate this risk. I don’t

see Linn raising its distributions until ever, Linn’s distribution is unlikely to be cut even if prices remain depressed for far longer.

Meanwhile, BreitBurn has left 20 percent of its 2009 oil and gas pro-duction unhedged. I recommend re-distributing the cash to Linn Ener-gy and our other recommended en-ergy plays.

Fellow PTP recommendation En-terprise Products Partners isn’t ento volumes transported, not commodity prices.

And Enterprise’s strong financial credit markets when needed to fund growth; the company recently took out a new loan and credit line totaling $593 million.

Enterprise Products Partners re-mains a solid buy under 27.[1170]

The following advice is suitable for investors who seek long-term capital appreciation.

Name Date Recent Div. Total (Exchange: Symbol) Recomm. Price* Yield+ Return# Advice^AllianceBernstein Glob High Income Fund (NYSE: AWF) 05/31/06 $6.34 17.5% -32.6% SoldAMR Corp (NYSE: AMR) 11/12/08 9.62 NA 36.5 Buy @ 14AMR Corp 7.875% Mini (NYSE: AAR) 02/27/08 13.00 15.1 -34.9 SoldARC Energy (TSX: AET-U, OTC: AETUF) 03/23/05 13.11 10.7 27.8 HoldAreva (OTC: ARVCF, France: CEI) 11/12/08 485.00 2.2 7.8 Buy @ 550Baxter International (NYSE: BAX) 12/10/08 51.12 2.0 0.0 Buy @ 62Bayer (OTC: BAYZF) 09/10/03 53.10 4.0 170.2 Buy @ 62BlackRock Income Opportunity (NYSE: BNA)♣ 03/09/05 7.12 8.6 -14.7 SoldBreitBurn Energy Partners LP (NSDQ: BBEP) 06/13/07 6.20 32.9 -79.4 SELLBrookfield Asset Management (NYSE: BAM)♣ 06/08/05 14.87 3.5 -5.1 Buy @ 22Brookfield Infrastructure Partners LP (NYSE: BIP) 02/27/08 10.50 9.9 -42.0 SoldBunge (NYSE: BG)♣ 05/10/06 41.90 1.8 -29.7 Buy @ 51CBS Corp 6.75% Mini (NYSE: CPV) 05/14/08 11.57 14.6 -44.1 SoldCLP Holdings (HGK: 2, OTC: CLPHF) 08/13/08 6.92 4.7 -18.1 HoldDPL Inc. 7.875% Mini (NYSE: MJT) 09/10/08 18.50 10.6 -23.6 SoldEnterprise Products Partners (NYSE: EPD)♣ 12/13/06 20.78 9.8 -19.9 Buy @ 27EOG Resources (NYSE: EOG) 12/10/08 70.40 0.7 0.0 Buy @ 100First Banks 8.15% Pref A (NYSE: FBS A, CUSIP: 33610A209) 11/12/08 20.30 10.0 -1.5 SoldFred's (NSDQ: FRED) 09/24/08 10.58 0.7 -25.8 Buy @ 19Frontline (NYSE: FRO) 06/13/07 30.25 6.3 -8.8 HoldGeneral Dynamics (NYSE: GD) 11/12/08 54.25 2.6 -5.7 Buy @ 68Goldcorp (NYSE: GG) 12/24/08 24.53 0.6 NEW Buy @ 35Iowa Telecom (NYSE: IWA) 02/08/06 15.55 10.3 15.9 SoldLegacy Reserves (NSDQ: LGCY) 08/08/07 7.75 26.2 -59.9 SoldLinn Energy (NSDQ: LINE) 12/13/06 11.91 20.1 -51.9 Buy @ 18Monsanto (NYSE: MON) 11/12/08 81.73 1.2 4.0 Buy @ 97Nestle (OTC: NSRGY) 12/10/08 35.25 3.3 0.0 Buy @ 42Novartis (NYSE: NVS) 12/10/08 46.35 3.4 0.0 Buy @ 55Otelco (NSDQ: OTT) 01/26/05 9.25 18.3 -13.3 SoldPeabody Energy (NYSE: BTU) 12/24/08 21.76 0.9 NEW Buy @ 32Pittsburgh & West Virginia Railroad (NYSE: PW) 11/26/08 11.84 4.6 13.6 Buy @ 10Quality Systems (NSDQ: QSII) 11/26/08 35.27 3.3 16.2 Buy @ 41Qwest Communications 7.75% Mini (NYSE: PKH) 05/14/08 12.60 15.4 -40.5 SoldShaw Group (NYSE: SGR) 11/12/08 19.32 NA 37.1 Buy @ 20Stericycle (NSDQ: SRCL) 12/24/08 52.61 NA NEW Buy @ 60Templeton Emerging Markets (NYSE: TEI) 07/23/03 8.17 12.1 1.3 SoldTortoise Energy Infrastructure Corp (NYSE: TYG) 12/13/06 16.98 13.1 -44.0 HoldUnum Group 7.4% Mini (NYSE: PJR) 05/14/08 13.42 13.8 -42.0 SoldUS Cellular 7.5% Mini (NYSE: UZV) 05/14/08 14.20 13.2 -34.1 SoldVeolia Environnement (NYSE: VE, France: VIE)♣ 12/27/06 23.58 7.5 -64.5 Buy @ 42WD-40 Company (NSDQ: WDFC) 09/24/08 26.19 3.7 -24.7 Buy @ 41Weatherford International (NYSE: WFT) 12/10/08 10.34 NA 0.0 Buy @ 17.50Western Asset Emerging Markets (NYSE: EFL) 07/11/07 6.31 9.2 -48.8 SoldWindstream Corp (NYSE: WIN) 02/27/08 8.79 11.2 -22.3 SoldWP Carey Co (NYSE: WPC)♣ 03/14/07 21.50 9.0 -27.4 Hold

*Prices as of 12/09/08 close. +Estimated yields for the next 12 months can differ from actual dividends because of company policy. Estimated yields based on company filings because a full year's dividends have not yet been paid. #Since original recommendation. Returns can be volatile due to significant price and dividend moves. Returns for sold stocks are the returns on the date they were sold. ^Buy at or below prices given. ♣To order a free annual report, go to http://kci-com.ar.wilink.com or call 800-654-2582; reports are mailed on the next business day.

GROWTH PORTFOLIO

PERSONAL FINANCE8 January 14, 2009

percent increase in third quarter earn-ings per share, when were cracking.

Earning assets were increased 5.7 percent. And while non-performing loans rose 24 percent from last year, they remain only 0.24 percent of total loans. That compares to a peer group ment to the bank’s high standards, as is the fact that management never got involved in subprime loans.

Despite the deteriorating economy and the impact on real estate, Arrow’s return on assets, return on equity and book value all rose over the past year.

Looking ahead to 2009, Arrow has an opportunity to grow its business conservatively with acquisitions. And it continues to attract lending cus-tomers in search of a financial institu-tion that’s largely kept itself apart from the troubles now plaguing the industry.

Of course, this isn’t new territory for solid Arrow. Back in the early 1990s, we were able to ride its sucthe wake of the savings and loan collapse.

Now we’re again adding the stock to the Income Portfolio as a bet on the recovery of the financial system from the subprime collapse. Focusing on fundamentals has allowed the company to achieve new record totals for assets, deposits and loans out-standing in spite of historic trauma in the financial markets.

Note the dividend was increased 8.7 percent over the past year, a trend that’s set to continue this year. Buy Arrow Financial up to 28. [300]

It may be some years before a stron-ger, more conservative US financial

services industry emerges from the wreckage of recent months. Well-run local banks, however, healthy as ever.

This week, we’re adding back an old friend from that sector to the In-

come Portfolio, Arrow Financial. Even as global finance has become

more complex, Arrow’s northeastern New York operation has remained fo-cused on the tried and true formula of building deposits and customer rela-tionships. That paid off with an 11.9

Fabulous FinancialBy RoGER S. CoNRAd

The following investment advice is suitable for investors who seek a high level of current income while preserving wealth. Typically, these types of investors are retired or less than five years from

retirement.

Stocks and Preferreds (70%) Date Recent Div. Total Stock (Exchange: Symbol) Recomm. Price* Yield+ Return# Advice^Arrow Financial Corp (NSDQ: AROW) 12/24/08 $24.66 4.0% NEW Buy @ 28AES Corp 6.75% Pref C (NYSE: AES C, CUSIP: 00808N202)** 02/08/06 31.75 10.6 -9.3% Buy @ 50BellSouth 7.12% Mini (OTC: KTBB) 09/10/08 23.25 7.7 -2.2 Buy @ 25Canadian Apt Prop (TSX: CAR-U, OTC: CDPYF) 10/12/05 10.15 8.0 3.1 Buy @ 15Chevron (NYSE: CVX)♣ 03/28/90 75.56 3.3 752.8 Buy @ 80Comcast Corp 7% Pref B (NYSE: CCT, CUSIP: 20030N309)**♣ 04/11/07 19.80 8.8 -12.2 Buy @ 25Cons Energy $4.50 Pref B (NYSE: CMS B, CUSIP: 210518304)** 02/28/01 72.12 6.2 109.4 Buy @ 82Dominion Resources (NYSE: D)♣ 08/05/87 34.99 4.6 733.7 Buy @ 40Frontier Communications (NYSE: FTR) 05/25/05 8.32 11.4 -15.0 Buy @ 13Home Properties (NYSE: HME) 08/10/05 39.68 6.5 15.4 Buy @ 55Mid-America Apartment 8.3% Pref H (NYSE: MAA H, CUSIP: 59522J806)** 10/24/07 21.60 9.6 -7.2 Buy @ 25PIMCO Strategic Global Govt (NYSE: RCS)♣ 07/09/03 8.30 9.1 7.3 Buy @ 13Simon Prop 8 3/8% Pref J (NYSE: SPG J, CUSIP: 828806885)**♣ 10/22/03 48.00 8.7 17.1 SoldSouthern Co (NYSE: SO)♣ 07/09/97 36.56 4.6 378.6 Buy @ 38TEPPCO Partners (NYSE: TPP)♣ 06/12/02 18.95 14.5 -8.7 SoldUNITIL Corp (AMEX: UTL)♣ 07/25/07 20.43 6.9 -27.0 Buy @ 25Verizon Communications (NYSE: VZ)♣ 08/17/87 33.35 5.4 363.0 Buy @ 40Xcel Energy (NYSE: XEL) 09/24/08 18.01 5.2 -12.0 Buy @ 20Vermilion Energy (TSX: VET-U, OTC: VETMF) 04/14/04 18.07 9.4 91.2 Buy @ 30Yellow Pages Income Fund (TSX: YLO-U, OTC: YLWPF) 05/11/05 4.92 18.7 -40.2 Buy @ 10

Bonds (20%)Northeast Investors Trust (NTHEX, 800-225-6704) 12/24/03 3.90 16.4 -21.5 Buy @ 7Vanguard GNMA (VFIIX, 800-997-2798)♣ 04/14/93 10.48 4.7 154.1 Buy @ 10.50Vanguard Interm-Term Tax-Exempt (VWITX, 800-997-2798)♣ 07/17/91 12.34 4.2 141.3 Buy @ 14Vanguard Interm-Term INV-Grd (VFICX, 800-997-2798) 02/11/04 8.38 6.0 5.5 Buy @ 10

Cash (10%)

*Prices as of 12/09/08, close. +Estimated yields for the next 12 months can differ from actual divi-dends because of company policy. #Since original recommendation. Returns can be volatile due to signif-icant price and dividend moves. Returns for sold stocks are the returns on the date they were sold. ^Buy at or below prices given. **Call dates and prices for the preferreds are as follows: AES 03/17/08, $50.00; Comcast 05/15/11, $25.00; Cons En 03/17/08, $110.00; Mid-America 08/11/08, $25.00; and Simon Prop 10/15/27, $50.00. ♣To order a free annual report, go to http://kci-com.ar.wilink.com or call 800-654-2582; reports are mailed on the next business day.

INCOME PORTFOLIO

Flight of the ArrowArrow Financial

Source: Bloomberg

Price$30

28

26

24

22

20

18J

’08F M A M J J A S O N D

Current $24.90

THEINCOME REPORT

Investors should focus their attention on my three top sectors: health care, energy and consumer staples. I’m adding stocks in two of these groups, medical waste specialist

Stericycle and coal mining giant Peabody Energy. Amid a volatile and uncertain market and economic environment, it’s time to boost your exposure to the ultimate hedge, gold.

www.PFnewsle t ter.com 703-394-4931 January 14, 2009 9

ble as well as Kroger Company, Uni-lever and Colgate-Palmolive. The fund has held up well by owning companies that money, rain or shine.

On a year-to-date basis the fund is in the top 2 percent of the large blend category, outperforming its peer group by more than 7 percent and the S&P 500 by more than 11 percent. Those numbers illustrate the virtues of being a focused fund with an em-phasis on essential consumer goods rather than services—the former ac-count for about 17 percent of the portfolio—during tough times.

Manager Robert Lee also brings several years of experience to the table. He began his career at Fidelity as a research analyst, eventually taking the reins at Select Consumer Staples in June 2004. He had a rough first year—in 2005 the fund dropped to the middle of the category as the per-formance of consumer staples lagged—but he’s kept the fund in the top 5 percent ever since.

An expense ratio of 0.84 percent is reasonable for a focused fund, and this one features the added benefit of a 0.8 percent yield. Despite having a low beta of 0.7, meaning the fund

Consumer staples remains one of the best performing sectors in the

market today, and that trend is likely to hold. Made up of companies that offer goods and services consumers use every day regardless of economic conditions, revenues for the group have remained fairly steady despite a squeeze on margins earlier this year as commodity prices soared.

Wal-Mart Stores (NYSE: WMT) continues to attract penny-pinching consumers while other retailers strug-gle to get customers through the door. Brand equity and low prices have helped it stand out against com-petitors; customer traffic has risen, and seasonal is flying off the shelves. That’s led to improving sales.

Highly competitive pricing on store basics has also driven recent results; net sales for November rose 1.3 per-cent, with Wal-Mart store sales climb-ing 6.5 percent and Sam’s Club show-ing a 1.4 percent improvement. As at Nov. 30 overall net sales had improved 7.6 percent year to date.

Procter & Gamble, maker of house-hold products such as Folgers coffee and Head & Shoulders shampoo, has also been a solid performer in a tough market. Fiscal 2008 (ended Aug. 31) net global sales rose more than 8 per-cent as the company deepened its global penetration. Sales growth in its beauty and grooming segments was sluggish compared to past perfor-mance, but the household care seg-ment continued its typical robust growth. Net earnings per share grew by more than 16 percent, rising from $3.04 to $3.64.

It’s tough to go broke owning com-panies like that.

To harness that trend—and continu-ing our focus on consumer staples–we’re adding Fidelity Select Con-sumer Staples (FDFAX, 500-544-8544) to the Portfolio. Holdings in-clude Wal-Mart and Procter & Gam-

won’t whipsaw investors as badly as the broad market, it does have a heav-ily concentrated portfolio.

With more than 62 percent of assets in its top 10 positions, the market price can move drastically based on news about a single portfolio holding. Although big swings are extremely rare, it’s important to be aware of the potential and not to panic if one hap-pens. Buy Fidelity Select Consumer Staples.

Resource AllocationThe overall focus of the Fund Port-

folio is on achieving growth and in-come, but it’s easy enough to tailor your holdings to your specific needs.

Growth and income investors should simply maintain equal posi-tions in all of our holdings. Growth investors should skew toward our of assets to that category, 20 percent Special Situations holdings. Finally, those with lower risk tolerances should hold 45 percent of assets in our stock funds, 40 percent in bonds and 15 percent in Special Situations.

For the purpose of reporting re-turns, we’ll assume equal positions in all of our recommended funds. [630]

Eat, Drink and SpendBy BENjAMiN SHEpHERd

The following investment advice is suitable for investors who seek capital appreciation and current income.

Stocks Recent Date Total Annualized Return* (Symbol, Phone Number) Price* Recommˆ. Return+ 1-yr 3-yr 5-yr TypeFairholme (FAIRX, 866-202-2263) $21.32 12/10/08 0.0% -34.4% -4.3% 5.2% Large BlendMeridian Value (MVALX, 800-446-6662) 21.36 12/10/08 0.0 -35.0 -5.1 1.4 Mid-Cap BlendT. Rowe Price Small-Cap Value (PRSVX, 800-638-5660) 24.88 12/10/08 0.0 -32.6 -7.7 2.7 Small-Cap Value

BondsPrudent Global Income (PSAFX, 800-711-1848) 11.42 12/10/08 0.0 -4.8 5.7 3.4 World BondOsterweis Strategic Income (OSTIX, 800-700-3316) 9.72 12/10/08 0.0 -6.8 2.2 3.4 Multi-Sector Bond

Special SituationsFidelity Select Consumer Staples (FDFAX, 800-544-8544) 49.39 12/24/08 NEW -27.1 2.6 6.4 Large Blend

*As of 12/10/08. +Since original recommendation.

FUND PORTFOLIO

FUND FOCUS

Investors should focus their attention on my three top sectors: health care, energy and consum-er staples. I’m adding stocks in two of these groups, medical waste specialist Stericycle and coal mining giant Peabody Energy. Amid a volatile and uncertain market and economic environment, it’s time to boost your exposure to the ultimate hedge, gold. We’re adding gold mining giant Gold

PERSONAL FINANCE10 January 14, 2009

percent to a 12-year high. And China and Dubai haven’t been immune either; house prices in Shanghai, Shenzen and Guang-zhou have fallen, while home values in Dubai fell for the first time in October and some analysts expect further declines.

n In a move designed to support the hous-ing market and the general economy, the Federal Reserve plans to purchase Fannie Mae, Freddie Mac and Federal Home Loan Bank debt and mortgage-backed securities (MBS) backed by Fannie, Freddie Mac and Ginnie Mae. Purchases of up to $100 bil-lion in government sponsored entity direct obligations conducted by the Fed’s primary dealers through a series of competitive auctions began the first week of Decem-ber. Purchases of up to $500 billion in MBS will be conducted by asset managers selected via a competitive process, with purchases expected to begin before year’s end. The Fed aims to lower the enterprises’ funding costs and interest rates offered to homebuyers, MAKING IT EASIER FOR NEW BUYERS TO ENTER THE MAR-KET. After the Fed announced its efforts to increase liquidity in the mortgage market,

pany based on UNREALISTIC EXPECTA-TIONS FOR FUTURE GROWTH; as both unhappy insiders and interested observers have noted, Tribune’s businesses are mostly profitable, the major dailies among them. Zell—in his defense, not alone among investors—overestimated Tribune’s ability to maintain margins in what’s been a declining business. Although revenues continue to fall at many newspapers, most papers continue to make money, albeit not as much as they might be used to.

n In the wake of the domestic housing bubble, home prices have experienced a rare and protracted national decline, falling 21 percent since their 2006 peak. BUT THE US ISN’T THE ONLY COUN-TRY WHERE REAL ESTATE HAS GONE FROM BOOM TO BUST. Readers may be familiar with the problems afflicting the UK housing market, where prices have plunged 16 percent from last November as banks hoard credit and the economy slides into recession. Similar problems have wracked Denmark, where house prices have tumbled for the first three quarters of the year and foreclosures have jumped 17

n Privately held Extended Stay Hotels may be about to hand the keys over to the repo man. Owned by Lightstone Group and Arbor Realty Trust, the hotel chain caters primarily to business travelers on extended work assignments. But as the economic situation continues to deteriorate, COM-PANIES ARE KEEPING EMPLOYEES CLOSER TO HOME, and occupancy rates at the chain’s 684 hotels in the US and Canada have plunged. That’s left the com-pany in danger of defaulting on its debt within the next 60 days. But instead of filing for bankruptcy, which would expose more of its properties to possible seizure due to provisions of debt securitization deals, the company is likely to turn its properties o ver to bondholders. Extended Stay’s plight highlights problems not only with commercial real estate but also with securitized debt. With more than $300 billion of commercial mortgage-backed securities outstanding as of the end of last year, this could signal the next great wave of plunging asset prices.

n The Securities and Exchange Commis-sion has introduced new rules to improve transparency and accountability at the credit rating agencies, a business sul-lied by conflicts of interest and dubious reliability—failings driven home by raters’ formerly sanguine outlooks for even the riskiest mortgage-backed securities. THESE CHANGES PREvENT FIRMS FROM RATING ANY dEBT THEY HELPEd STRUCTURE ANd PROHIBIT ANALYSTS FROM ACCEPTING GIFTS in excess of $25 from issuers of debt they rate. Each rating agency will also be required to disclose publicly a sample of 10 percent of its ratings six months after their release; however, the regulator has also proposed rules that would force ratings firms to dis-close all ratings made after June 25, 2007 one year later. Although these moves are steps in the right direction, further reform is needed in an industry where debt issuers still pay for credit ratings.

n Tribune Company’s Chapter 11 filing set off frenzied coverage of the US newspa-per industry—kindling, it was. Sam Zell’s case is instructive, but not for the reasons pushed hard on TV. He leveraged the com-

The US consumer has finally hit the wall, and it’s evident that the world’s largest economy will rely on massive government expenditures to prevent an even deeper recession. Those efforts, focused on revitalizing the nation’s infrastructure, will benefit certain sectors and companies.

Asia, however, China in particular, is well positioned to show positive growth in 2009. Asian economies as a whole have the benefit of low interest rates, high savings rates, and low debt levels. The latter will be crucial during the first quarter of 2009, when bad economic news should peak. And Chinese authorities have announced significant spending plans designed to boost the domestic economy. Those efforts, too, will be concentrated on infrastructure repair and development.

The bottom line: The only places to find growth in 2009 will be the emerging market economies. Yiannis G. Mostrous, associate editor of PF and editor of Silk Road Investor, addresses these issues in the Dec. 10, 2008, Silk, available to PF subscribers at www.pfnewsletter.com as of Saturday, Dec 20. [170]

ADVISORYC A P S U L E

SMART GRID SMART INVESTING

P F O N L I N E www.PFnewsle t ter.com

www.PFnewsle t ter.com 703-394-4931 January 14, 2009 11

interest rates for fixed-rate mortgages took a dive—the decline for the week ending Dec. 3 was the largest since the week of Nov. 27, 1981.

n Since the advent of the housing and mortgage crises, certain pun-dits have savaged the Community Reinvestment Act (CRA), arguing that this piece of legislation, drafted over 30 years ago to encourage banks to service lower-income borrowers and areas, compelled or incentivized banks to engage in risky subprime lending. A seemingly pat argument, but one that’s ultimately flawed: The CRA doesn’t es-tablish minimum thresholds for loan volume nor does it reward banks for making unsound loans to low-income individuals. A recent study conducted by the Federal Reserve bears this out. Not only does long-term evidence indicate that CRA LOANS HAvE PERFORMEd IN LINE with those originated by banks’ broader lending programs, but CRA loans constituted only 6 percent of overall subprime volume (a small portion), and those loans have performed on par with non-CRA subprime loans.

n Shut up and blog: That’s what we’ve been telling the editors and researchers around here. During any given day there are plenty of insights, trivia and opinions being tossed back and forth in the editorial department. Instead of some of that go to waste, we’ve been encouraging everyone from the publisher to the editors to the researchers to post their kernels of insight at our blog, At These Levels (www.attheselevels.com). AT THESE LEvELS WILL KEEP YOU CONNECTEd to our take on fast-moving markets, bank bailout plans, recession, our favorite stocks and much more. What’s more, because it’s a blog you can write comments back to us and connect with other cyber-subscribers as well as us. And it’s free and a no-spam zone. We offer up real-time information and observations in an effort to keep you engaged with us, as well as us engaged with you. See you there. [1000] CA Word Cout Total [1400]

High-Impact HybridBayer (OTC: BAYZF) is a pharmaceuti-

cal/chemical conglomerate with three main divisions: HealthCare, CropScience (agrichemicals), and MaterialsScience (chemicals and polymers). It’s one of the so-called hybrid companies in the chemi-cal sector because of the increasing role the pharmaceutical business is playing in its profitability and earnings growth. Estimates peg Bayer’s 2008 pharmaceu-

tical sales at EUR11 billion and other health care sales at EUR4.5 billion. Al-most 60 percent of profits will be coming from the health care sector, up from less than 40 percent in 2005. Bayer has a strong pipeline, with few

patents expiring in the near term. One ex-ception is venerable multiple sclerosis drug Betaseron, Bayer’s trade name for interferon; recent Growth Portfolio addi-tion Novartis (NYSE: NVS) will start sell-ing its own version in early 2009. How-

ever, the impact on Bayer’s bottom line should be minimized by the royalty Bayer will receive from Novartis. The company’s CropScience division

(crop protection, pest control, seeds and plant biotechnology) remains the largest global agrochemical company with lead-ing positions in most core markets. Given that global agricultural needs are

becoming greater by the day, the busi-ness should continue to deliver steady growth next year, too. The company re-mains committed to research and devel-opment (R&D) and is steadily gaining ex-posure to the higher-growth seeds and ag-biotech market. Last year’s agreement to collaborate with Growth Portfolio hold-ing Monsanto (NYSE: MON) in agricul-tural technologies should boost the com-pany’s long-term growth prospects in the field. Bayer is also one of the world’s leading

manufacturers of polymers and high-quali-ty plastics. Apart from its polycarbonates and polyurethanes, the MaterialScience

division also offers coatings, adhesives, insulating materials and sealants. Principal customers are the automotive and con-struction industries, the electrical/electron-ics sector and manufacturers of packag-ing and medical equipment.This is the company’s most cyclical busi-

ness and should be the weakest in 2009 as the global economy slows. But Bayer’s turn toward pharma means the division now accounts for only 14 percent of earn-ings. The situation for the sector is directly opposite that for agrichemicals—namely lower prices and high stocks. That said, the division will benefit from

lower prices in oil and gas, as 25 per-cent of its costs as percentage to sales comes from raw materials. The company has been prolific in the

mergers-and-acquisitions arena; we ex-pect that to continue. The health care sec-tor should remain the company’s focus, but short-term economic uncertainty dic-tates that deals should be small to mid-size. [400]

S t o c k Update

Redirect the stress built up during this long bear and bask in the Florida sunshine as winter extends into its extra six weeks: Join new PF Editor Elliott Gue, longtime associate editor Roger Conrad and executive editor Gregg Early Feb. 4-7, 2009, for the Orlando Money Show.

Elliott will detail PF’s new direction and provide sig-nificant insight into his approach to stock selection and portfolio management. What’s required now amid these difficult times are clarity and focus, qualities Elliott has demonstrated in these pages and through The Energy Strategist for years.

Roger, a steady hand through many market events such as the one we’re dealing with now, will talk about his new service focused on exploiting the greatest spending boom in history, New World 3.0.

Gregg, a constant at PF for nearly two decades, will be there to address recent developments with the publica-tion. He’ll also discuss the Smart Grid, an endeavor he’s exploring as part of his role with New World 3.0.

Be sure to bring your questions. These guys love to talk markets and everything that impacts them.

To attend as a guest of PF, call 800-970-4355 [190]

ORLANDO

Money Market Liquidity Facility and the Money Market Investor Funding Facility, both of which were designed to provide liquidity to money mar-ket funds and enable them to meet redemption requests.

In late November, the central bank announced the creation of the Term Asset-Backed Securities Loan Facility, availability to consumers and busi-nesses by lending up to $200 billion by newly and recently originated con-sumer and small business loans.

And the ailing mortgage market is slated to receive similar assistance: The central bank has pledged up to purchase up to $100 billion of Fannie Mac’s (NYSE: FRE) debt as well as lower the enterprises’ funding costs and interest rates offered to home-buyers.

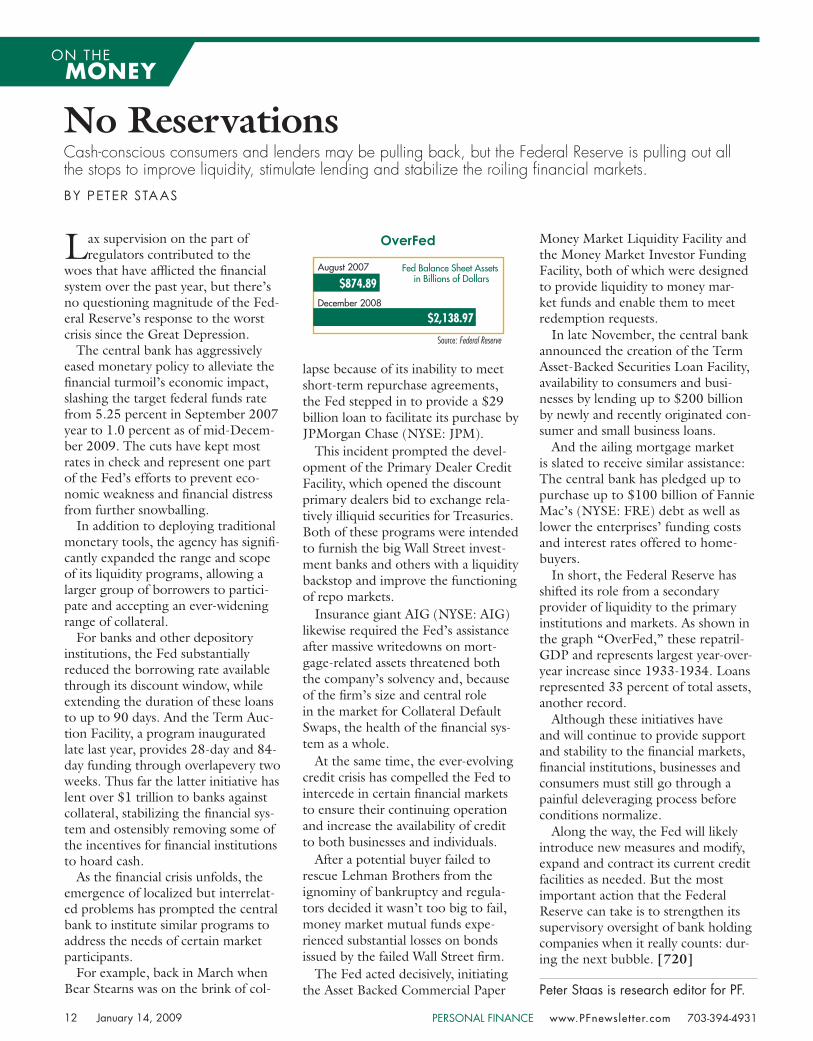

In short, the Federal Reserve has shifted its role from a secondary provider of liquidity to the primary institutions and markets. As shown in the graph “OverFed,” these repatril-GDP and represents largest year-over-year increase since 1933-1934. Loans represented 33 percent of total assets, another record.

Although these initiatives have and will continue to provide support and stability to the financial markets, financial institutions, businesses and consumers must still go through a painful deleveraging process before conditions normalize.

Along the way, the Fed will likely introduce new measures and modify, expand and contract its current credit facilities as needed. But the most important action that the Federal Reserve can take is to strengthen its supervisory oversight of bank holding companies when it really counts: dur-ing the next bubble. [720]

Peter Staas is research editor for PF.

lapse because of its inability to meet short-term repurchase agreements, the Fed stepped in to provide a $29 billion loan to facilitate its purchase by JPMorgan Chase (NYSE: JPM).

This incident prompted the devel-opment of the Primary Dealer Credit Facility, which opened the discount primary dealers bid to exchange rela-tively illiquid securities for Treasuries. Both of these programs were intended to furnish the big Wall Street invest-ment banks and others with a liquidity backstop and improve the functioning of repo markets.

Insurance giant AIG (NYSE: AIG) likewise required the Fed’s assistance after massive writedowns on mort-gage-related assets threatened both the company’s solvency and, because of the firm’s size and central role in the market for Collateral Default Swaps, the health of the financial sys-tem as a whole.

At the same time, the ever-evolving credit crisis has compelled the Fed to intercede in certain financial markets to ensure their continuing operation and increase the availability of credit to both businesses and individuals.

After a potential buyer failed to rescue Lehman Brothers from the ignominy of bankruptcy and regula-tors decided it wasn’t too big to fail, money market mutual funds expe-rienced substantial losses on bonds issued by the failed Wall Street firm.

The Fed acted decisively, initiating the Asset Backed Commercial Paper

Lax supervision on the part of regulators contributed to the

woes that have afflicted the financial system over the past year, but there’s no questioning magnitude of the Fed-eral Reserve’s response to the worst crisis since the Great Depression.

The central bank has aggressively eased monetary policy to alleviate the financial turmoil’s economic impact, slashing the target federal funds rate from 5.25 percent in September 2007 year to 1.0 percent as of mid-Decem-ber 2009. The cuts have kept most rates in check and represent one part of the Fed’s efforts to prevent eco-nomic weakness and financial distress from further snowballing.

In addition to deploying traditional monetary tools, the agency has signifi-cantly expanded the range and scope of its liquidity programs, allowing a larger group of borrowers to partici-pate and accepting an ever-widening range of collateral.

For banks and other depository institutions, the Fed substantially reduced the borrowing rate available through its discount window, while extending the duration of these loans to up to 90 days. And the Term Auc-tion Facility, a program inaugurated late last year, provides 28-day and 84-day funding through overlapevery two weeks. Thus far the latter initiative has lent over $1 trillion to banks against collateral, stabilizing the financial sys-tem and ostensibly removing some of the incentives for financial institutions to hoard cash.

As the financial crisis unfolds, the emergence of localized but interrelat-ed problems has prompted the central bank to institute similar programs to address the needs of certain market participants.

For example, back in March when Bear Stearns was on the brink of col-

No ReservationsCash-conscious consumers and lenders may be pulling back, but the Federal Reserve is pulling out all the stops to improve liquidity, stimulate lending and stabilize the roiling financial markets. By pEtER StAAS

ON THE MONEY

PERSONAL FINANCE www.PFnewsle t ter.com 703-394-493112 January 14, 2009

Source: Federal Reserve

OverFed

Fed Balance Sheet Assets in Billions of Dollars

August 2007

December 2008