sap-ifrs-ii

TRANSCRIPT

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 1/49

Parallel Accounting in SAP ERP

Thomas Jordan / IMS FinancialsSeptember 2014

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 2/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 2

Agenda

• Reasons for Parallel Accounting

• Basics of Parallel Accounting

• Parallel Accounting in FI

• Parallel Accounting in FI-AA

• Parallel Accounting in MM

• Parallel Accounting in CO

• Some Experiences with Parallel Accounting

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 3/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 3

Reasons for Parallel Accounting

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 4/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 4

Reasons for Parallel Accounting

Basically multinational companies are facing the challenge that they want to have

internationally comparable figures and have to fulfill legal requirements coming from local

commercial or tax law.

That means:

• Group closing according to IFRS or US-GAAP

• Local closing according to local law

The need to fulfill the requirements of international reporting and local reporting at the

same time leads to the need for parallel accounting

In addition there are countries that require to have more then one accounting principle.

Or a company wants to get Income Tax Accounting and commercial accounting out of one

system

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 5/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 5

Parallel Accounting is the Challenge

Important Differences between IFRS & US-GAAP

Topic IFRS US-GAAP

Business Combinations IFRS 3 FAS 141, 142

Fixed assets IAS 16 ARB 43

Employee Benefits IAS 19 FAS 87, 88, 106, 112, 132Consolidated Financial Statements IAS 27, SIC 12 ARB 51, FAS 94, FIN 46

Associates IAS 28 APB 18, FAS 94

Impairment IAS 36 FAS 142, 144

Provisions IAS 37, IFRIC 1 FAS 5, 143, 146, FIN 14

Intangible Assets IAS 38 FAS 2, 86, 142, SOP 93-7, 98-1, 98-5

Financial Instruments IAS 39, IFRS 7 FAS 107, 115, 133

Investment Property IAS 40 FAS 13, 66, 67

Agriculture IAS 41 SOP 85-3

Source: zfbf Zeitschrift für betriebswi rtschaftliche Forschung / Schmalenbachs Business Review

Jahrgang 60 / Dezember 2008

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 6/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 6

Basics of Parallel Accounting

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 7/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 7

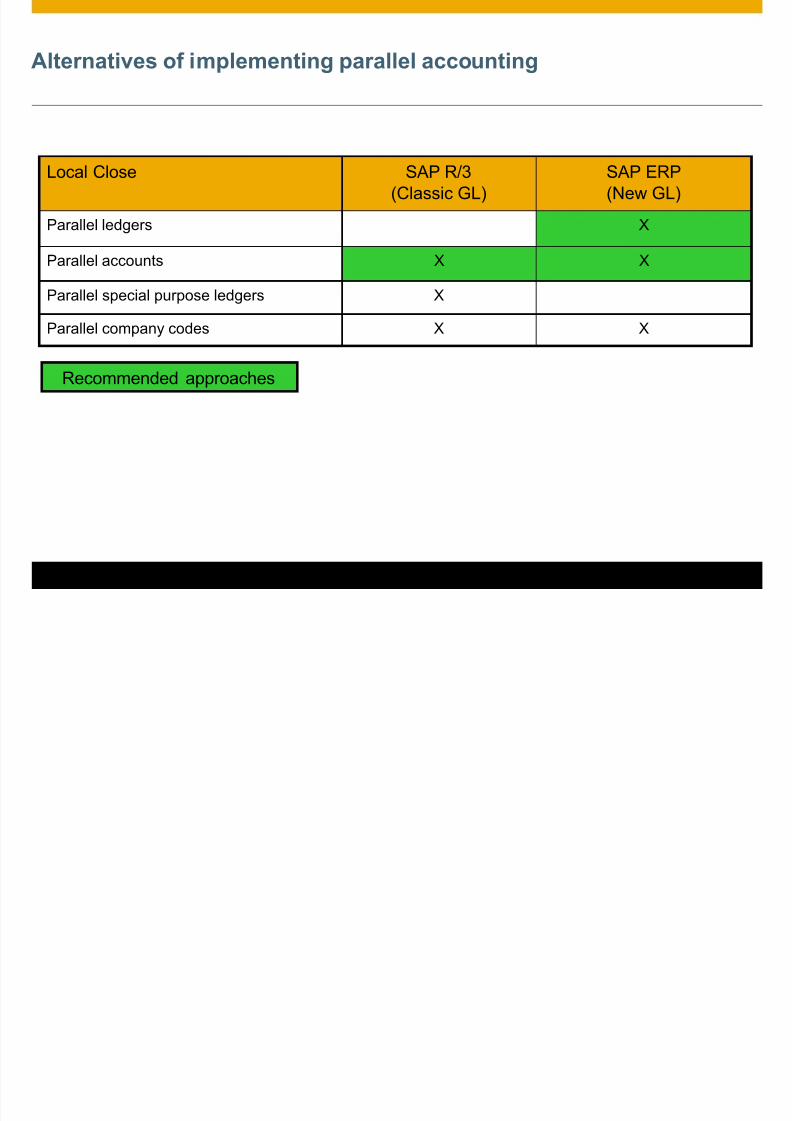

Alternatives of implementing parallel accounting

Local Close SAP R/3

(Classic GL)

SAP ERP

(New GL)

Parallel ledgers X

Parallel accounts X X

Parallel special purpose ledgers X

Parallel company codes X X

Recommended approaches

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 8/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 8

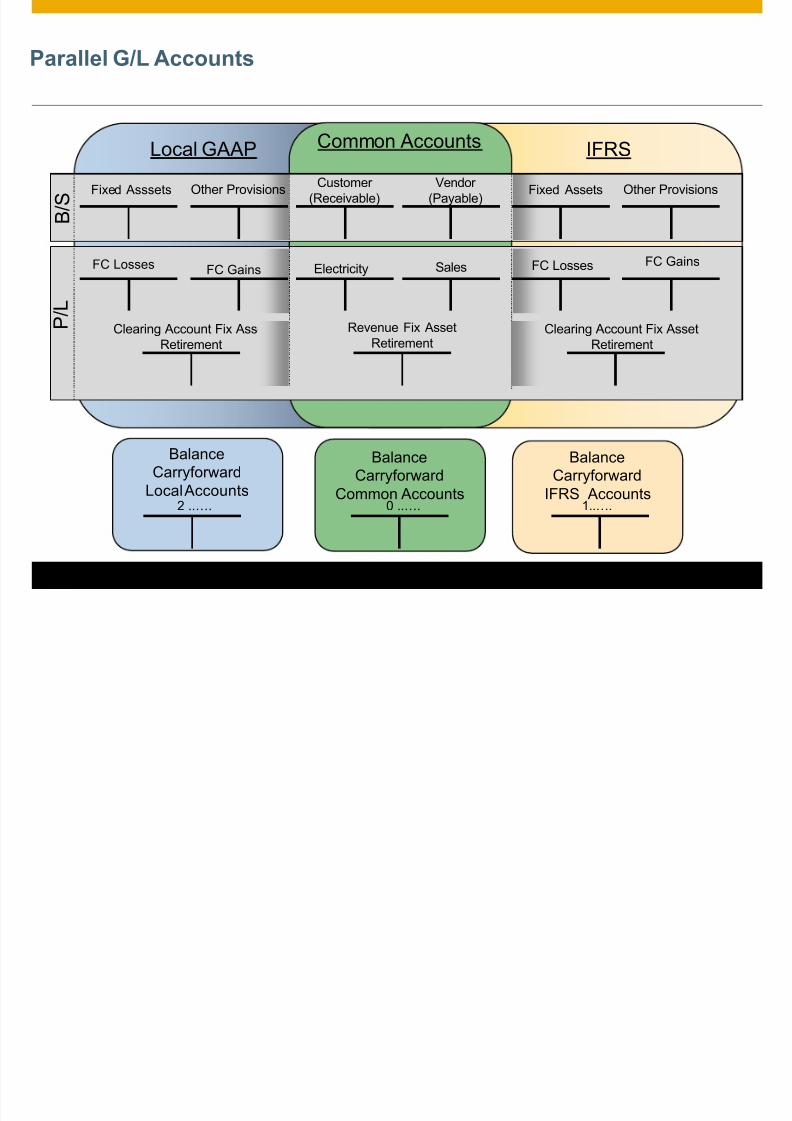

Parallel GL Accounts

Items with significant valuation differences are posted to different accounts. Each valuation

has its own set of “pure” accounts.

Common accounts are used where no material valuation differences occur.

It is advisable to have clearly discernable account number ranges or distinguishing digits or

letters to distinguish among sets of accounts.

Since each set must be in balance, extra care must be taken to ensure correct account

determination: establish an accounting guideline!

Common

Accounts

Pure IFRS

Accounts

PureLocal GAAP

Accounts

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 9/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 9

Parallel G/L Accounts

Options for creating charts of accounts

Prefix: Alphanumeric or

numeric

Account Number Suffix

A 0 xxxxxx Common accounts 0

B 1 xxxxxx IFRS accounts 1

C 2 xxxxxx Local accounts 2

IFRS Reporting

0 common accounts and

1 IFRS accounts

Local Reporting

0 common accounts and

2 local accounts

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 10/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 10

Parallel G/L Accounts

Local GAAP IFRSCommon Accounts

Fixed Asssets

FC Losses

Vendor

(Payable)

Customer

(Receivable)

B / S

P / L

FC GainsSalesElectricity

Revenue Fix Asset

RetirementClearing Account Fix Asset

Retirement

Clearing Account Fix Asset

Retirement

Other ProvisionsOther Provisions Fixed Assets

FC Losses

Balance

Carryforward

Local Accounts

Balance

Carryforward

Common Accounts

Balance

Carryforward

IFRS Accounts2 ..…. 0 ..…. 1..….

FC Gains

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 11/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 11

Parallel Ledgers

• International accounting principle for example IFRS is primary valuationrepresented by the leading ledger.

• Local GAAP books are maintained in an additional non-leading ledger

• Non-leading ledgers can use a different fiscal year variant. (For restrictions on

this, see SAP Note 844029).

• Same Accounts are used for all ledgers

Example:

0LLeading Ledger

(IFRS)

Z1

Non-LeadingLedger 1(LocalGAAP)

Z2

Non-LeadingLedger 2

(Tax)

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 12/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 12

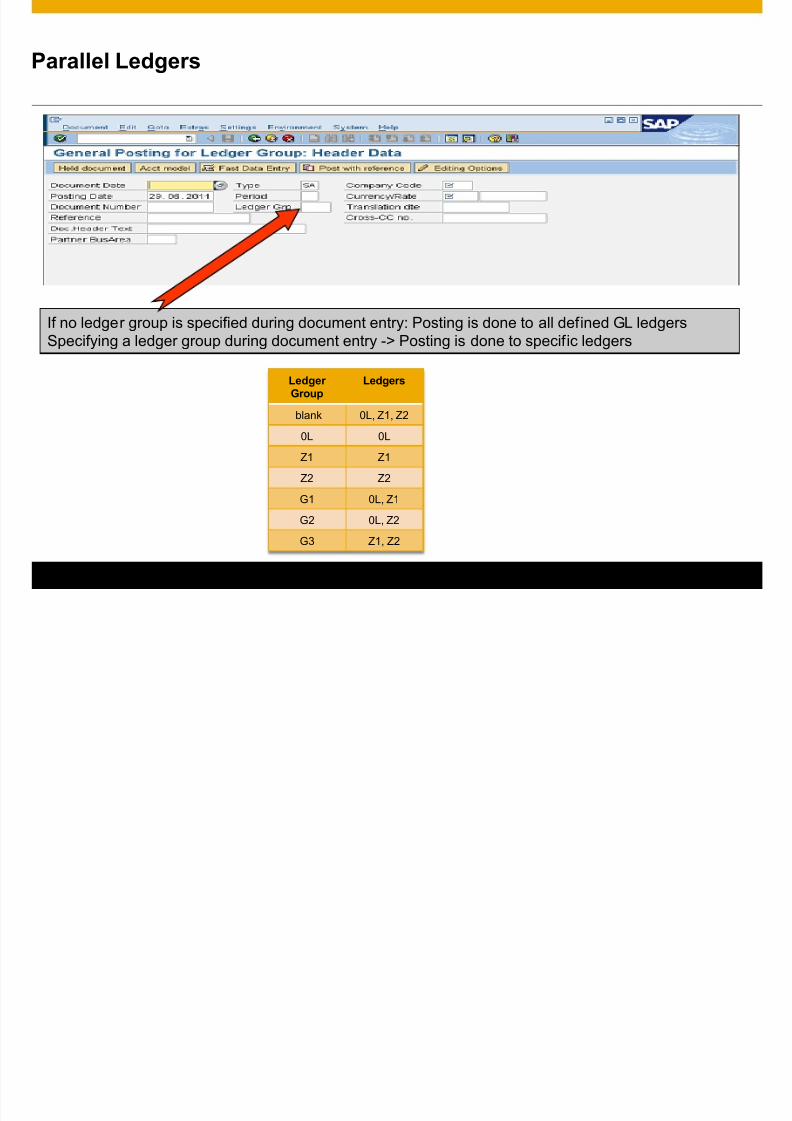

Parallel Ledgers

If no ledger group is specified during document entry: Posting is done to all defined GL ledgers

Specifying a ledger group during document entry -> Posting is done to specific ledgers

LedgerGroup

Ledgers

blank 0L, Z1, Z2

0L 0L

Z1 Z1

Z2 Z2

G1 0L, Z1

G2 0L, Z2

G3 Z1, Z2

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 13/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 13

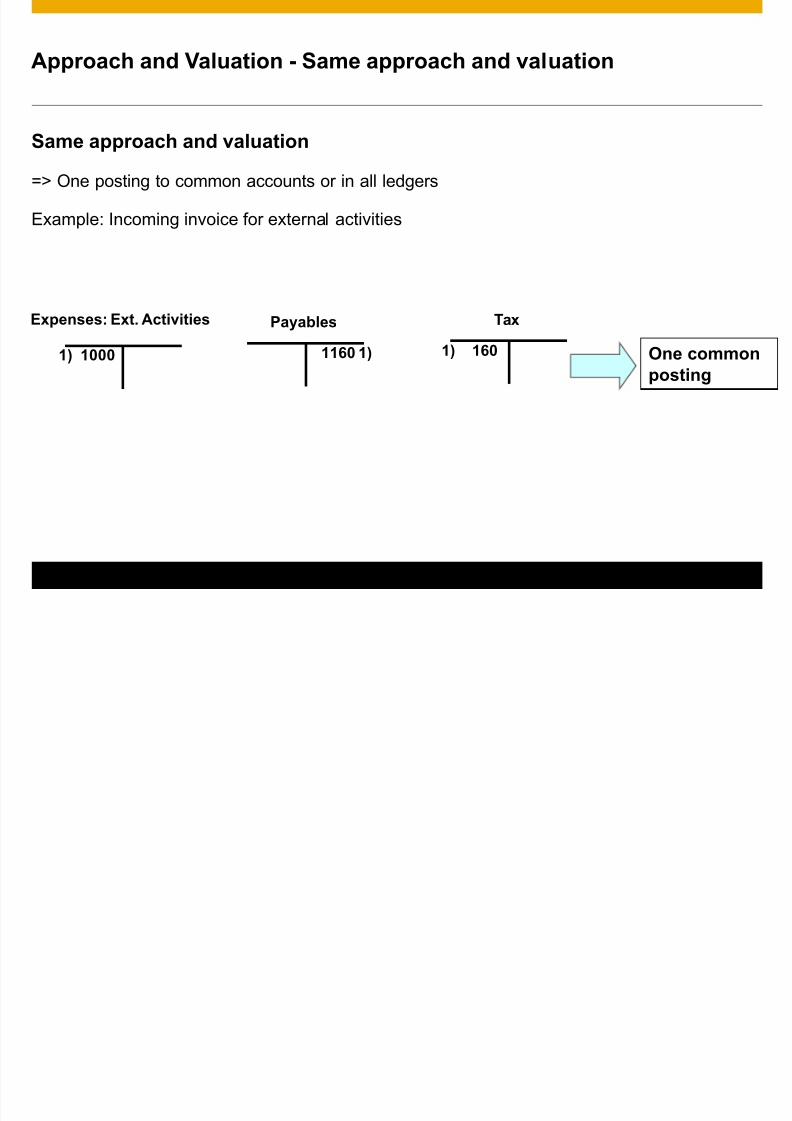

Approach and Valuation - Same approach and valuation

Same approach and valuation

=> One posting to common accounts or in all ledgers

Example: Incoming invoice for external activities

Expenses: Ext. Activities

1) 1000

Payables

1160 1)

Tax

1) 160 One common

posting

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 14/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 14

Approach and Valuation - Same approach different valuation

Expenses: PensionsLocal Valuation

2) 1000

Expenses: Pensions

IFRS

3) 500

Accruals

Local Valuation

1000 2)

Accruals

IFRS

500 3)

Two complete

postings,

separately for

each valuation

Same approach but different valuation

=> separate posting to local and IFRS accounts or ledgers

Example: Depreciation or reserves for pensions

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 15/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 15

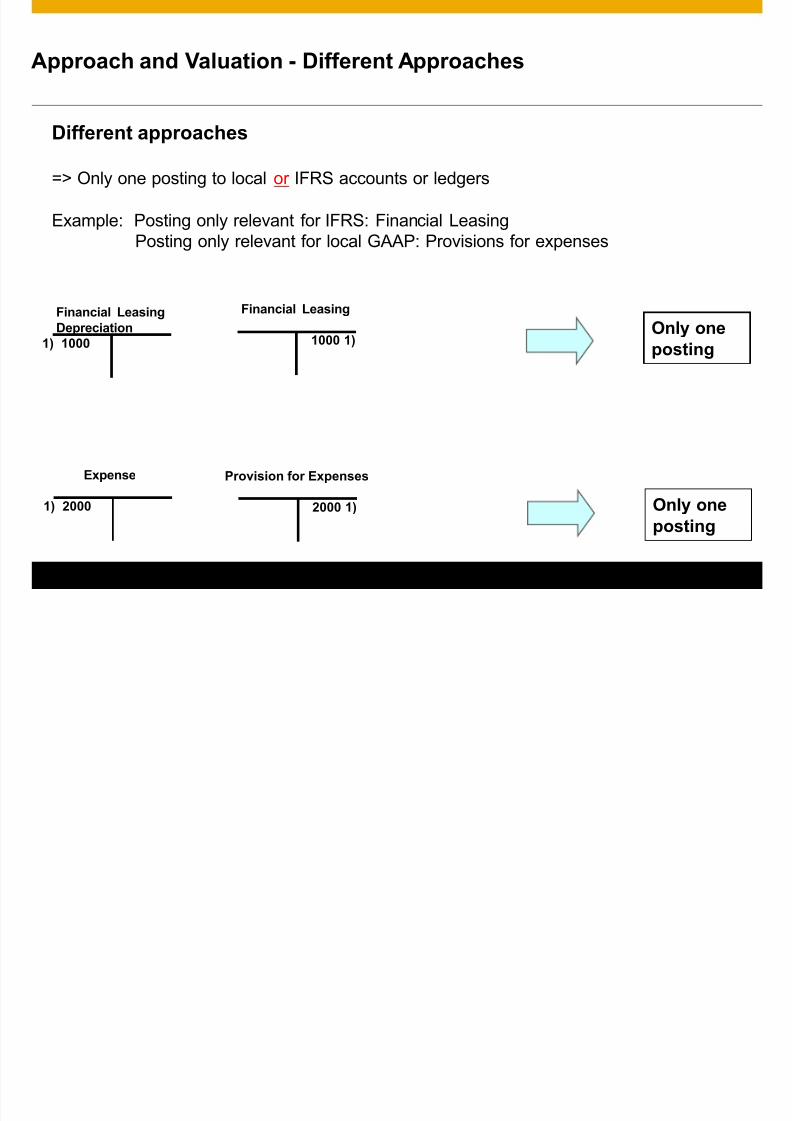

Approach and Valuation - Different Approaches

Financial Leasing

Depreciation

1) 1000

Financial Leasing

1000 1)Only one

posting

Expense

1) 2000

Provision for Expenses

2000 1) Only one

posting

Different approaches

=> Only one posting to local or IFRS accounts or ledgers

Example: Posting only relevant for IFRS: Financial Leasing

Posting only relevant for local GAAP: Provisions for expenses

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 16/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 16

Parallel Accounting in FI

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 17/49© 2014 SAP SE or an SAP affiliate company. All rights reserved. 17

Parallel Accounting in FI

Parallel accounting is required for example regarding the following topics:

Foreign currency valuation

Value adjustments

List of terms / Reclassifications

Provisions

…

Parallel valuation in FI is represented by valuation area. The valuation area has to be

assigned to an accounting principle.

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 18/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 18

Parallel Accounting in FI - Foreign Currency Valuation

Receivables, Payables, foreign currency balance sheet accounts may be valuated

differently on the basis of different accounting principles.

• Account approach

• A valuation area is assigned to certain target accounts that belong to the specific

accounting principle.

• The valuation report (Classic G/L -> SAPF100, New G/L -> FAGL_FC_Valuation)

has to be run for each valuation area.

• Ledger approach

• Determination of the ledger group using the assignment of the

valuation area to an accounting principle that is assigned to a target ledger group.

N:1 N:1

Valuation area ----> Accounting principle ----> Ledger group

• The valuation report (FAGL_FC_Valuation) has to be run for each valuation area.

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 19/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 19

Parallel Accounting in FI - Flat-Rate Individual Value Adjustment

• Receivables (where applicable, payables) can be valuated differently by number of

days overdue and risk classes in accordance with different accounting principles.

Transaction F107 has to be run for each valuation area.

• Account approach:

• Assignment of different accounts using valuation areas.

• Ledger approach:

• Assignment of ledger group using valuation areas

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 20/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 20

Parallel Accounting in FI - Sorting Open Items by Maturity

Receivables (where applicable, payables) can be portrayed by remaining term on

different balance sheet items in accordance with different accounting principles (transfer

posting).

Transaction FAGLF101 in New G/L has to be run for each valuation area.

In Classic G/L transaction F101 has to be run for each valuation area.

• Account approach:

• Assignment of different accounts using valuation areas.

• Ledger approach

• Assignment of ledger group using valuation areas

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 21/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 21

Parallel Accounting in FI-AA

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 22/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 22

Parallel Accounting in FI-AA - General -

The FI-AA application component portrays parallel accounting using depreciation areas.

• An accounting principle is represented by a depreciation area.

• Different depreciation parameters (such as depreciation method or useful life) are

defined for each depreciation area.

• The depreciation area settings specify whether

• No postings are made

• Asset balances and depreciation are posted

• Only asset balances are posted

• Only depreciation is posted

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 23/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 23

Parallel Accounting in “classic” FI-AA - Account Solution

Depreciation

Assets are depreciated using different depreciation rules in accordance with different

accounting principles.

• Customizing:

• One depreciation area is required for each accounting principle

• Separate accounts can be defined for the combination

- chart of depreciation

- chart of accounts

- account determination

- depreciation areas.

Account determination is assigned to the asset class.

For each accounting principle, the depreciation run posts documents to the accounts

defined.

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 24/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 24

Parallel Accounting in “classic” FI-AA - Ledger Solution

The FI-AA application component portrays parallel accounting using depreciation areas.

Ledger groups, representing different accounting principles, are assigned to the depreciation

areas. Consequently, postings are made to separate ledgers in FI.

• Customizing: The following depreciation areas need to be set up accordingly:

• Depreciation area 01 is assigned to leading ledger (leading valuation)

• Depreciation areas and derived depreciation areas (delta areas) assigned to Non-

leading ledgers (valuations)

Start date and end date of the fiscal year variant in the depreciation areas in Asset

Accounting need to correspond to the fiscal year variant of the leading ledger.

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 25/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 25

Parallel Accounting in “classic” FI-AA - Ledger Solution

LedgerGroup

Ledger

Posting of

Asset

B/S Value

Periodic

Depreciation

Depreciation area 01

(leading)

0L IFRS X X

Depreciation area 30 (non-

leading)

N1 US GAAP - X

Depreciation area 60

(delta area 30-01)

N1 US GAAP X (1) -

• The portrayal of parallel valuation requires the depreciation areas listed below.

Delta postings are used.

• The base value of the leading area is transferred to all ledgers, and a secondperiodic APC posting corrects the base value in the parallel ledger.

• The derived area (delta area) posts the difference between the leading area andthe non-leading area to the ledger assigned to the non-leading area.

• The following example assumes:The IFRS ledger is the leading ledger. US GAAP ledger is the non-leadingledger

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 26/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 26

Parallel Accounting in “classic” FI-AA - Ledger Solution

Different APC values reflecting different accounting principles have to be posted to the

ledgers (for example, freight costs need to be capitalized for US GAAP).

FI-AA

FI-GL

IFRS (Leading)

US GAAP

01 IFRS

30 US GAAP

60 30 - 01

…

Postings IFRS US

GAAP

Asset Acquisition 0L N1

Capitalization of Freight

Costs (ledger group-

specific document with

separate transaction type)

-- N1

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 27/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 27

Parallel Accounting in “classic” FI-AA - Ledger Solution

Integration with Controlling

Only Depreciation area 01 posts to Controlling

• This is the leading depreciation area

• It posts to the leading ledger

• It posts to Controlling

• Accounts are created as cost elements

• It uses the same accounts as depreciation areas 30 and 60

Ledger Group Ledger

Posting of

Asset

B/S Value

Periodic

Depreciation

Depreciation area 01(leading)

0L IFRS X X (CO)

Depreciation area 30 (non-

leading)

N1 US GAAP - X

Depreciation area 60

(delta area 30-01)

N1 US GAAP X -

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 28/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 28

Parallel Accounting in “new” FI-AA - Ledger Solution

The new FI-AA solution is available for ECC 6.17 EHP 7 through business function

FIN_AA_PARALLEL_VAL.

The new functionality will bring more flexibility for parallel valuation and more

transparency and simplicity.

See more information on SAP Service Portal:

http://service.sap.com/rkt-erp -> SAP Business Suite -> SAP-ERP -> SAP EHP 7 for

SAP ERP 6.0 -> FI: Financial and Management Accounting).

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 29/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 29

Benefits of the new solution:

• Flexibility concerning “Leading Valuation” • No more hard coupling of depreciation area 01

• Always separate documents per Ledger group (FI-AA)• Post the values correctly right from the beginning, using multiple parallel documents per

valuation

• Realtime postings per ledger group• Common understanding of posted document

• Posting to different periods possible (restriction: beginning/end of FY needs to be equal)

• Only one Depreciation Area per Valuation necessary• No further depreciation areas (Delta areas) necessary to portray a parallel Valuation

Parallel Accounting in “new” FI-AA - Ledger Solution

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 30/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 30

Parallel Accounting in “new” FI-AA - Ledger Solution

Assets activated in only some (but not all) accounting principles

In the new architecture: Only relevant ledger groups need to be represented on the asset by their

corresponding depreciation areas

All postings issued within from FIAA will only affect those ledger groups which

are relevant for the involved asset(s).

P&L postings for all other ledger groups have to be handled manually by the end user

Behavior during integrated acquisitions:

Due to the need to balance the technical clearing account, one document for each ledger group

assigned to the chart of depreciation has to be posted

If a ledger group is not represented on the asset by an area which posts APC online to GL, the

posting will be re-directed to “Account for non-operating expense“ (KTNAIB)

If no ledger group is represented on the asset by an area which posts APC online to GL, the system

issues an error can be changed into warning, then statistical areas in FI-AA will be updated

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 31/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 31

Parallel Accounting in “new” FI-AA - Ledger Solution

Assets activated in only some (but not all) accounting principles- New Logic -

In the new architecture (cont’): Behavior during integrated retirements:

For those ledger groups which are not represented on the asset by an area which posts APC online

to GL, the revenue will remain on the manually entered revenue account. The end user might need

to manually transfer this value to a different P&L account

If no ledger group is represented on the asset by an area which posts APC online to GL, the system

issues an error can be changed into warning, then statistical areas in FI-AA will be updated

Behavior during creation of assets:

Due to the P&L posting of acquisition costs during integrated acquisitions, the system has to checkthat no other depreciation area in this ledger group posts depreciation to GL. Otherwise, the

expense amounts in the P&L statement would be doubled over the useful life of the asset

If such a setup is found, the system issues an error. This can be changed into a warning, e.g. if the

asset is not used for integrated acquisitions

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 32/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 32

Parallel Accounting in Material Management

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 33/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 33

Parallel Accounting in Material Management

Externally purchased goods

Parallel accounting is possible in the Materials Management (MM) application component.

• Operational stock valuation in MM is done either based on standard price or on moving

average price.

• Parallel valuation is important on balance sheet date. On balance sheet date operational

valuation has to be “corrected”.

• Stocks have to be valuated based on a consumption sequence like FIFO valuation (first

in, first out), lowest value principle or LIFO valuation (last in, first out) according to the

accounting principle.

• This valuation is transferred from MM to FI

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 34/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 34

Parallel Accounting in Material Management

Externally purchased goods

Balance Sheet valuation is done by transaction MRN9.

For balance sheet valuation correction technique is used. Corrections are stored to

valuation correction accounts.

• Account Solution

• Customizing: Valuation correction Accounts have to be assigned to a account

modification

• Adequate account modification has to be selected for MRN9

• Ledger Solution

• Customizing: Ledger groups have to be assigned to accounting principle

Valuation correction Accounts have to be assigned to a account

modification

• For each Valuation Run the necessary accounting principle has to be selected

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 35/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 35

Parallel Accounting in Material Ledger (actual costing)

In case that Material Ledger is activated a periodic unit price is calculated using the value

flows for the period. (Operational stock valuation with standard price)

• Periodic actual costing run determines single and multilevel costs of all goods for each

period performs revaluation of stock, costs of goods sold and WIP at actual price

according to the leading accounting principle.

• Alternative valuation runs are used to perform revaluation of stock, costs of good sold

and WIP according to non-leading accounting principles using alternative activity rates

and / or alternative material prices.

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 36/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 36

Parallel Accounting in Material Ledger (actual costing)

For balance sheet valuation based on actual costs basically the non leading valuation is

done be alternative valuation run (AVR) .

• Account Solution

• Customizing: Valuation correction Accounts have to be assigned to a account

modification

• Classic AVR is used to do the necessary delta postings

• COGM AVR can also be used with adequate BADI (Full Postings)

• Ledger Solution

• Customizing: Ledger groups have to be assigned to accounting principle

For classic AVR Valuation correction Accounts have to be assigned to

a account modification

For COGM AVR only the ledger group has to be assigned to an

accounting principle

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 37/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 37

Parallel Accounting in Controlling

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 38/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 38

Parallel Accounting in Controlling

Necessity of parallel accounting in CO

• Basically data for controlling should be derived from international comparablenumbers within the group.

• Usually the internationally comparable numbers are represented by the leading

ledger.

• Therefore only the leading ledger should post to CO to have a consistent set of data

all over the group for accounting and management reporting purposes.

• But there are some countries that require actual costs based on their country specific

law.

• Brazil

• Russia

• Turkey• Also one industry specific regulation in USA is requiring actual costs

• FERC (Federal Energy Regulatory Commission)

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 39/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 39

Parallel Accounting in Controlling

Parallel Determination of Costs of Goods Manufactured

• For example Different depreciation values (according to two different accounting principles)

can be transferred into Cost Center Accounting.

• The depreciation costs can be included in the activity rates for the work performed and in

the costs of goods manufactured, both of which are calculated at period close.

• Ledger groups / accounts in FI-GL with inventory values calculated according to two

different valuation methods, can be updated. For example,

• CO Version 0 represents the leading valuation (IFRS) Actual costs are calculated

using the periodic costing run and update inventory values in the leading ledger in FI-

GL.

• Second CO Version represents the local valuation (GAAP), Actual costs are

calculated using an alternative valuation run and update inventory values in the local

ledger in FI-GL.

.

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 40/49

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 41/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 41

Some Experiences with parallel Accounting

E i

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 42/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 42

Experiences

IFRS implementation itself is not the big challenge but implementation of parallel accounting

1. Figure out how many accounting principles have to be implemented

• Local GAAP / IFRS

• Local GAAP / IFRS / Local Taxes

• …

Have in mind whether an additional accounting principle is expected to be implemented in near

future.

Find out which accounting principle should be the leading one.

In most of he cases it makes sense for internationally operating companies to choose the

international principle as the leading one because mainly the leading principle is directly postedto CO!

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 43/49

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 44/49

E i

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 45/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 45

Topic Exposure

Draft

Standard

from

Comment

RevenueRecognition

Replacement IAS

11, IAS 18

Standardavailable

since May 28th

2014

2017 Most important joined project of IASB and FASB, will completely change theexisting world of revenue recognition.

SAP Components: FI, MM, SD, CRMSAP Comment letter

Leases Amendments

IAS17

2010/Q3Re-Exposure

Draft

expected inH2/2014

2017? The new standard will change the accounting on the lessee side significantly.It is also expected that leasing of real estate objects will change.

SAP Components: FI

Experiences

IFRS implementation itself is not the big challenge but implementation of parallel accounting

4. Have in mind: IFRS is still changing

Currently IASB and FASB are still working on “big” standards.

Both standards will be valid for IFRS and US-GAAP

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 46/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 46

Attention: Parallel Accounting within IFRS !

Reporting according to IFRS and local GAAP.

With the new IFRS regulations, e.g. revenue recognition (effective 2017) and the SEC

requirements to present 2 comparable pre-years, the situation will be as follows:

Similar requirements are expected for the new Leasing standard.

Year Leading RevRec Retrospective view Prospective view

2018 RevRec new (RevRec old comparable)

2017 RevRec new RevRec new RevRec old comparable

2016 RevRec old RevRec new comparable

2015 RevRec old (RevRec new comparable)

2014 RevRec old

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 47/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 47

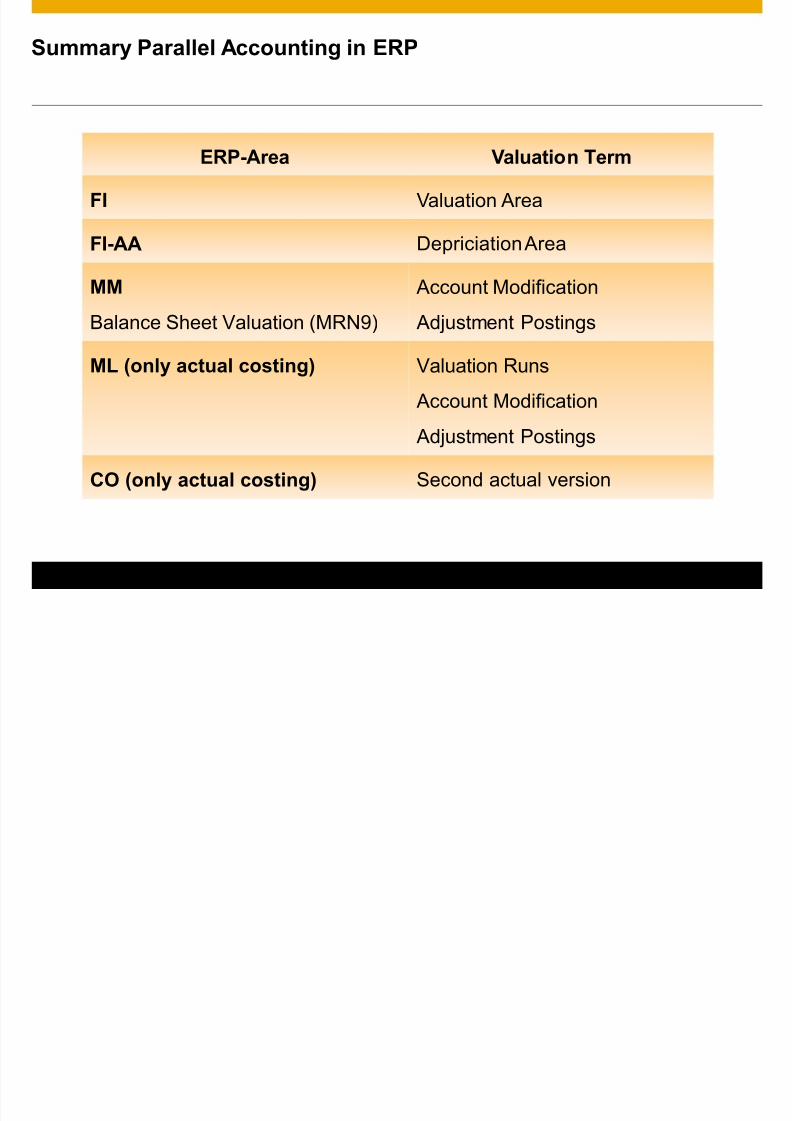

Summary Parallel Accounting in ERP

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 48/49

© 2014 SAP SE or an SAP affiliate company. All rights reserved. 48

Summary Parallel Accounting in ERP

ERP-Area Valuation Term

FI Valuation Area

FI-AA Depriciation Area

MM

Balance Sheet Valuation (MRN9)

Account Modification

Adjustment Postings

ML (only actual costing) Valuation Runs

Account Modification

Adjustment Postings

CO (only actual costing) Second actual version

8/10/2019 SAP-IFRS-II

http://slidepdf.com/reader/full/sap-ifrs-ii 49/49

Contact information:

Thomas Jordan

IMS Financials