section 2 a little more about accounting rules and choice of business entity module 2.a

TRANSCRIPT

Section 2 Section 2 A little more about accounting rules andA little more about accounting rules and

Choice of Business EntityChoice of Business Entity

Module 2.a. Module 2.a.

What is GAAPWhat is GAAP

Generally accepted accounting principlesGenerally accepted accounting principles

Set of standards that is generally accepted Set of standards that is generally accepted and universally practicedand universally practiced

How to report economic eventsHow to report economic events

Who makes the rulesWho makes the rules

Securities and Exchange CommissionSecurities and Exchange Commission

Financial Accounting Standards BoardFinancial Accounting Standards Board

American Institute of Certified Public American Institute of Certified Public AccountantsAccountants

International Standards CommitteeInternational Standards Committee

FASBFASB

Financial Accounting Standards BoardFinancial Accounting Standards Board

7 members7 members

Five year termsFive year terms

www.fasb.orgwww.fasb.org

The Big Five Becomes The Big Five Becomes the Final Four*the Final Four*

Deloitte & Deloitte & ToucheTouche (Tohmatsu) (6.13 (Tohmatsu) (6.13 billion)billion)Ernst & Young Ernst & Young (4.49)(4.49)KPMGKPMG (3.17) (3.17)PricewaterhouseCoopersPricewaterhouseCoopers (8.06) (8.06)Arthur Andersen Arthur Andersen (4.30)(4.30)

*Fiscal 2001 core business revenues*Fiscal 2001 core business revenues

The Conceptual FrameworkThe Conceptual Framework

Aids accountants in their task of interpreting and Aids accountants in their task of interpreting and communicatingcommunicating

Serves as foundation for specific rulesServes as foundation for specific rules

AssumptionsAssumptions– Economic entityEconomic entity– Cost principleCost principle– Going concernGoing concern– Monetary unitMonetary unit– Time periodTime period

Objectives of financial Objectives of financial reportingreporting

Primary – To Provide economic information to Primary – To Provide economic information to permit users of the information to make informed permit users of the information to make informed decisionsdecisions

Secondary –Secondary –– Reflect prospective cash receipts to investors and Reflect prospective cash receipts to investors and

creditorscreditors– Reflect prospective cash flows to the enterpriseReflect prospective cash flows to the enterprise– Reflect the enterprise’s resources and claims to its Reflect the enterprise’s resources and claims to its

resourcesresources

What makes accounting What makes accounting information usefulinformation useful

The Qualitative CharacteristicsThe Qualitative Characteristics– UnderstandabilityUnderstandability– RelevanceRelevance– ReliabilityReliability

VerifiabilityVerifiability

Representational faithfulnessRepresentational faithfulness

NeutralityNeutrality

– Comparability and ConsistencyComparability and Consistency– MaterialityMateriality– ConservatismConservatism

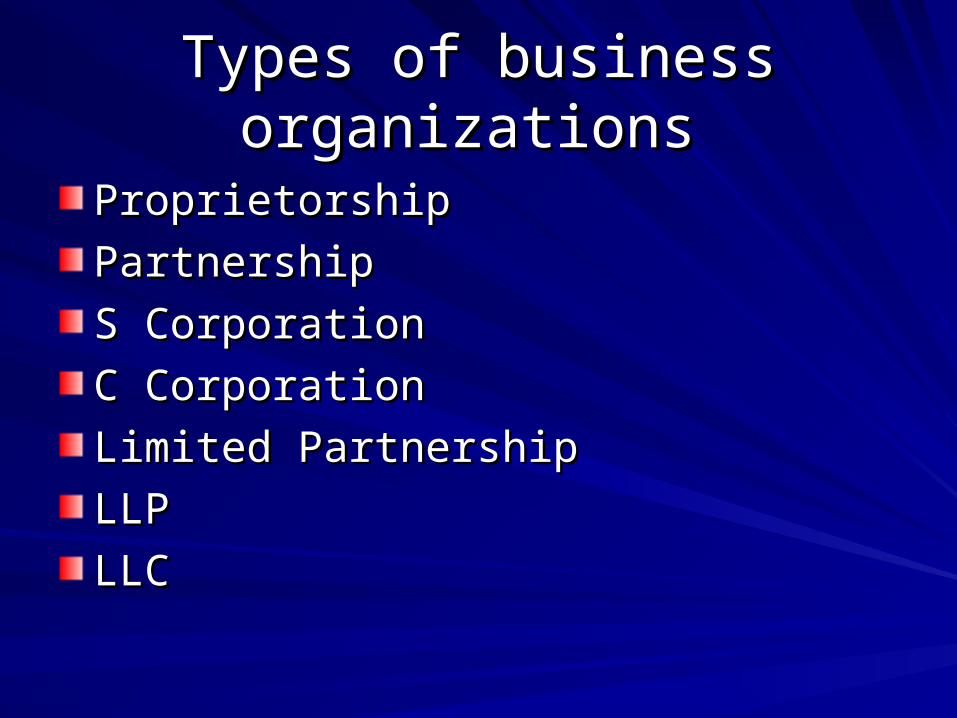

Types of business organizationsTypes of business organizations

ProprietorshipProprietorship

PartnershipPartnership

S CorporationS Corporation

C CorporationC Corporation

Limited PartnershipLimited Partnership

LLPLLP

LLCLLC

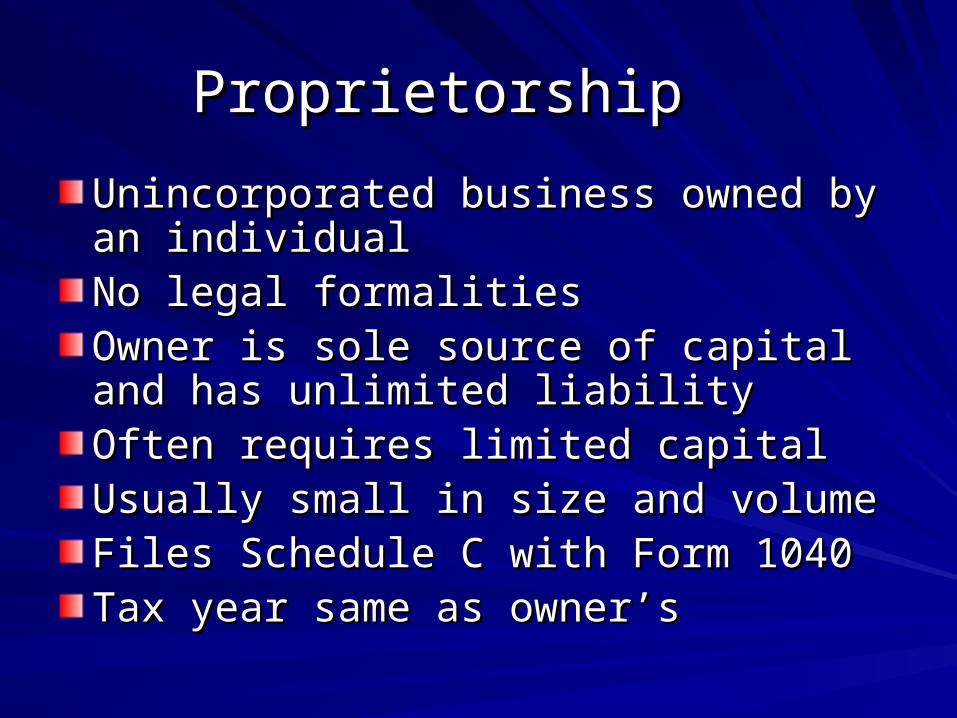

ProprietorshipProprietorship

Unincorporated business owned by an Unincorporated business owned by an individualindividualNo legal formalitiesNo legal formalitiesOwner is sole source of capital and has Owner is sole source of capital and has unlimited liabilityunlimited liabilityOften requires limited capitalOften requires limited capitalUsually small in size and volumeUsually small in size and volumeFiles Schedule C with Form 1040Files Schedule C with Form 1040Tax year same as owner’sTax year same as owner’s

PartnershipPartnership

Business is owned by 2 or more personsBusiness is owned by 2 or more personsPartnership agreement is highly Partnership agreement is highly recommendedrecommendedUnlimited liabilityUnlimited liabilityFiles Form 1065 with K-1 to partnersFiles Form 1065 with K-1 to partnersOwners report income in their tax year Owners report income in their tax year with or within which the entity’s tax year with or within which the entity’s tax year endsends

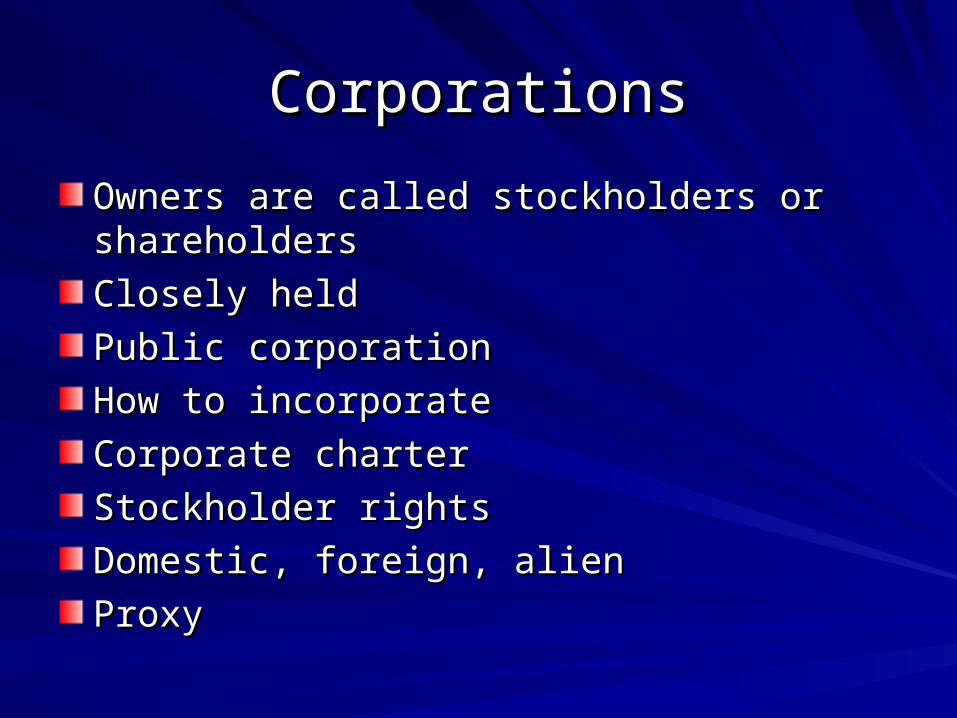

CorporationsCorporations

Owners are called stockholders or shareholdersOwners are called stockholders or shareholders

Closely heldClosely held

Public corporationPublic corporation

How to incorporateHow to incorporate

Corporate charterCorporate charter

Stockholder rightsStockholder rights

Domestic, foreign, alienDomestic, foreign, alien

ProxyProxy

Corporate structureCorporate structure

StockholdersStockholders

Board of DirectorsBoard of Directors

Corporate OfficersCorporate Officers

EmployeesEmployees

CorporationsCorporations

Limited liabilityLimited liability

Easy to raise capitalEasy to raise capital

Easy to transfer ownershipEasy to transfer ownership

Specialized managementSpecialized management

Continuity of lifeContinuity of life

No privacy if publicNo privacy if public

Government regulation if publicGovernment regulation if public

C corporationsC corporations

Organized under Subchapter C of IRCOrganized under Subchapter C of IRC

Files form 1120Files form 1120

Double taxationDouble taxation

Top corporate rate 35%Top corporate rate 35%

Can choose tax yearCan choose tax year

S CorporationsS Corporations

Only individuals, estates, and certain Only individuals, estates, and certain trusts can be ownerstrusts can be ownersMaximum shareholders 75Maximum shareholders 75Only one class of stock allowedOnly one class of stock allowedFiles Form 1120S with Schedule K to Files Form 1120S with Schedule K to shareholdersshareholdersTaxed as if partnershipTaxed as if partnershipUsually a calendar year TPUsually a calendar year TPLimited liabilityLimited liability

Limited Liability CompanyLimited Liability Company

Limited liability of corporation but taxed like Limited liability of corporation but taxed like a partnershipa partnership

Owners are called membersOwners are called members

Recognized by all statesRecognized by all states

Allows foreign investors, unlike the S CorpAllows foreign investors, unlike the S Corp

Some states require 2 owners (25%)Some states require 2 owners (25%)

One member LLC taxed as proprietorshipOne member LLC taxed as proprietorship

Disadvantage is that state statutes are not Disadvantage is that state statutes are not uniformuniform

Limited Liability PartnershipLimited Liability Partnership

Similar to LLC but designed for Similar to LLC but designed for professionals who normally do business professionals who normally do business as partners in a partnership.as partners in a partnership.

Personal liability protection for Partner but Personal liability protection for Partner but not joint liability.not joint liability.

Taxed as a partnershipTaxed as a partnership

All states have LLP statutesAll states have LLP statutes

Limited PartnershipLimited Partnership

At least one general partnerAt least one general partnerLimited partners cannot participate in Limited partners cannot participate in managementmanagementLimited partners’ liability limited to amount Limited partners’ liability limited to amount investedinvestedOnly general partners liable to creditorsOnly general partners liable to creditorsOften used for acquiring capital in a real Often used for acquiring capital in a real estate ventureestate venture

Choosing the right formChoosing the right form

Ease of creationEase of creation

Liability of ownersLiability of owners

Tax considerationsTax considerations

Need for capitalNeed for capital