select 2017 the criminalisation of compliance

TRANSCRIPT

4 October 2017

Select 2017 The criminalisation of compliance

Claire Lipworth, Rupert Shiers and Hannah Piper

Introduction

Hogan Lovells | 3

• 1991 - 'Organizational Guidelines'

– Credited an organisation for having an already-existing compliance program.

– Began to convert companies from 'passive bystanders who hoped their employees would behave well to active advocates for ethical conduct on the job'.

– Raised status of the compliance officer.

• 2000s - Enron, WorldCom and Sarbanes-Oxley

– Compliance transformed into a mainstream corporate concern.

• 2010s - Prosecutors have become 'super regulators'

– Expanding the prosecutorial scope of law enforcement and interweaving compliance matters with criminal matters.

Compliance - the US story

| 4 Hogan Lovells

• 3 primary routes to corporate criminal liability:

– Specific corporate offences

– Identification doctrine

– Failure to prevent

• Deferred Prosecution Agreements

Models of corporate criminal liability in the UK

| 5 Hogan Lovells

– Failure to prevent bribery

– Failure to prevent facilitation of tax evasion

– Anti-Money Laundering

– Failure to prevent economic crime

– Failure to prevent human rights abuses

Topics

Failure to prevent bribery

Hogan Lovells | 7

• Bribery Act 2010 in force since July 2011.

• Section 7 - failure on the part of a commercial organisation to prevent bribery committed by an associated person, with the intention of benefiting that organisation.

• Organisation will have complete defence if can show 'adequate' procedures designed to prevent bribery were in place.

• Ministry of Justice: http://www.justice.gov.uk/downloads/legislation/bribery-act-2010-guidance.pdf

• SFO/CPS: https://www.sfo.gov.uk/publications/guidance-policy-and-protocols/bribery-act-guidance/

• FCA's 'Financial Crime Guide for Firms' (Chapter 6): https://www.handbook.fca.org.uk/handbook/document/fc/FC1_FCA_20160703.pdf

• BBA Guidance: https://www.bba.org.uk/policy/financial-crime/anti-bribery-and-corruption/anti-bribery-and-corruption-guidance/

• Wolfsberg Group Guidance: http://www.wolfsberg-principles.com/pdf/home/Wolfsberg-Group-ABC-Guidance-June-2017.pdf

Bribery Act – Quick recap

Hogan Lovells | 8

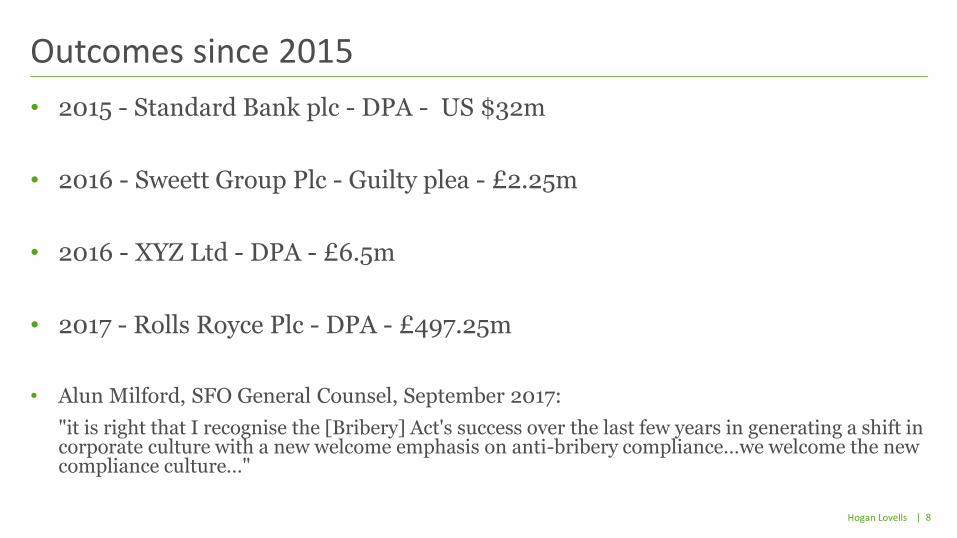

• 2015 - Standard Bank plc - DPA - US $32m

• 2016 - Sweett Group Plc - Guilty plea - £2.25m

• 2016 - XYZ Ltd - DPA - £6.5m

• 2017 - Rolls Royce Plc - DPA - £497.25m

• Alun Milford, SFO General Counsel, September 2017:

"it is right that I recognise the [Bribery] Act's success over the last few years in generating a shift in corporate culture with a new welcome emphasis on anti-bribery compliance…we welcome the new compliance culture…"

Outcomes since 2015

Hogan Lovells | 9

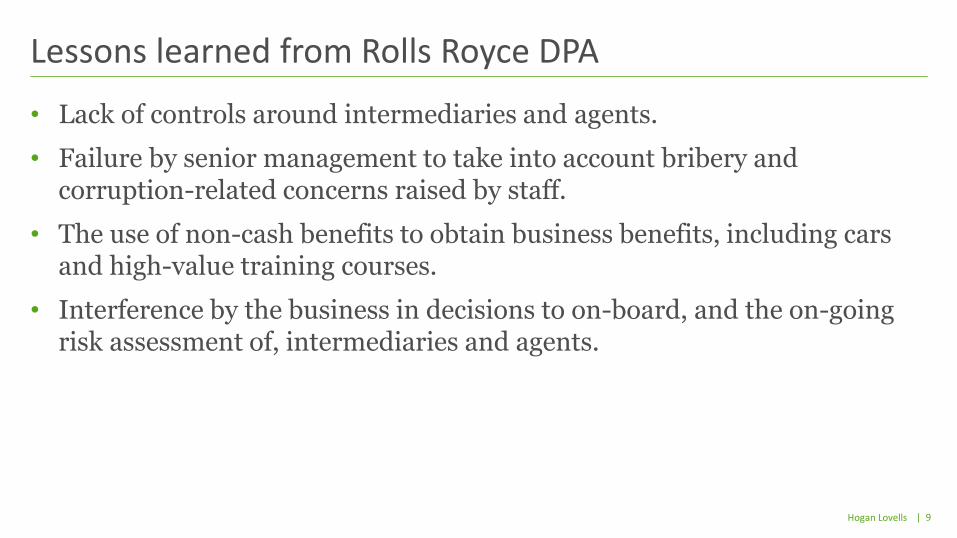

• Lack of controls around intermediaries and agents.

• Failure by senior management to take into account bribery and corruption-related concerns raised by staff.

• The use of non-cash benefits to obtain business benefits, including cars and high-value training courses.

• Interference by the business in decisions to on-board, and the on-going risk assessment of, intermediaries and agents.

Lessons learned from Rolls Royce DPA

Hogan Lovells | 10

• Issued March 2017.

• Compliance culture - Is senior and mid-level management setting a tone of compliance? Is the Board of Directors providing additional oversight of compliance? Is the company incentivising compliance by taking appropriate disciplinary actions against both employees engaging in misconduct and their managers?

• Compliance resources and expertise - Is the compliance department adequately staffed and funded? Do employees regularly receive guidance that is tailored to the specific risks faced by each business area?

• Policies and procedures - Have the company's compliance policies and procedures been effectively communicated to relevant employees and third parties? Does the company routinely reassess the effectiveness of its policies and procedures?

• Risk assessment - Does the company take appropriate steps to gather information or metrics to identify, analyse, and address risks?

• Internal audits and investigations - Is the company conducting regular internal audits that are appropriately scoped to identify areas of possible misconduct, particularly in high-risk areas? Is the company fully investigating reports of misconduct in a way that is appropriately scoped, independent, objective, and documented? Is the company appropriately responding to findings of investigations in a manner that targets root causes of misconduct?

• Third party management - Does the company conduct appropriate due diligence on vendors and other third parties that analyses those parties' own compliance structures?

DOJ's 'Evaluation of Corporate Compliance Programs'

Failure to prevent facilitation of tax evasion

| 12 Hogan Lovells

• Criminal Finances Act - in force from 30 September 2017

• Two new criminal offences of 'failure to prevent facilitation of tax evasion'

• Modelled on the corporate offence under s7 2010 Bribery Act

• Can only be committed by companies

• Offences do not impose criminal liability on directors, but carry unlimited fines for companies

• Companies need to conduct specific risk assessments and implement new procedures - more than just tweaking their AML /ABC policies

Introduction

Hogan Lovells | 13

The offences

Failure to prevent facilitation of

UK tax evasion

Failure to prevent facilitation of foreign

tax evasion

Hogan Lovells | 14

'UK offence'

STAGE 1

Criminal evasion of any UK tax, by a taxpayer,

based anywhere

STAGE 2

Person associated with company,

acting in that capacity, criminally facilitates

this tax evasion

STAGE 3

Company guilty of offence if unable to show reasonable

prevention procedures in place

Hogan Lovells | 15

Person associated with

the company and acting in that capacity

Person performing

services for or on behalf of the

company

Employee

Agent

Contractor

Facilitator must be person 'associated with company'

Hogan Lovells | 16

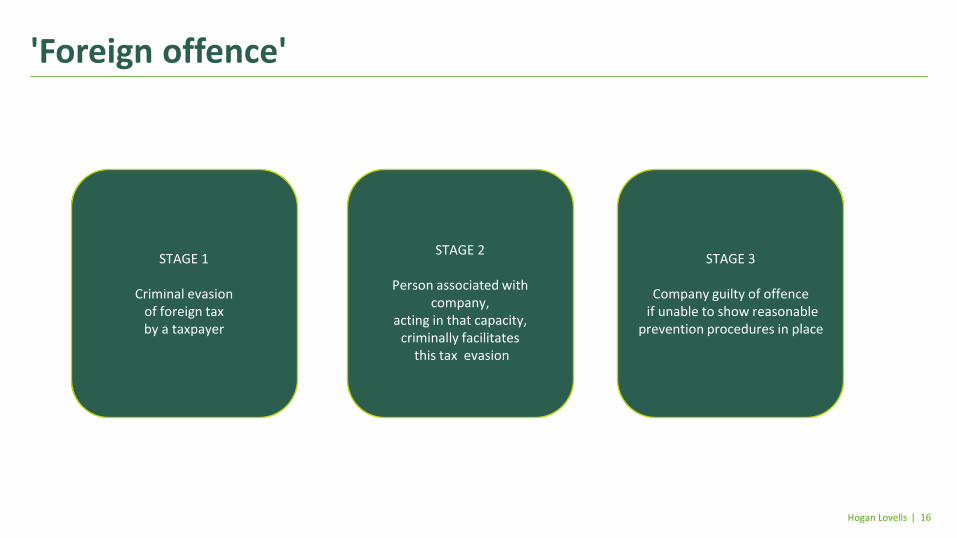

'Foreign offence'

STAGE 1

Criminal evasion of foreign tax by a taxpayer

STAGE 2

Person associated with company,

acting in that capacity, criminally facilitates

this tax evasion S

STAGE 3

Company guilty of offence if unable to show reasonable

prevention procedures in place

Hogan Lovells | 17

UK nexus is required for foreign offence

Company incorporated in the UK

Company has a permanent business presence in the UK

Some element of tax evasion facilitation takes place in UK

Hogan Lovells | 18

• Complete defence to both UK and foreign offence if company can show that when the tax evasion facilitation

offence was committed, it had reasonable prevention procedures in place designed to prevent 'associated persons'

from committing criminal tax evasion facilitation offences

• HMRC Guidance states prevention measures should be informed by the following six principles:

• Risk Assessment

• Proportionality

• Top level commitment

• Due diligence

• Communication (including training)

• Monitoring and review.

Prevention procedures

Anti - Money Laundering

Hogan Lovells | 20

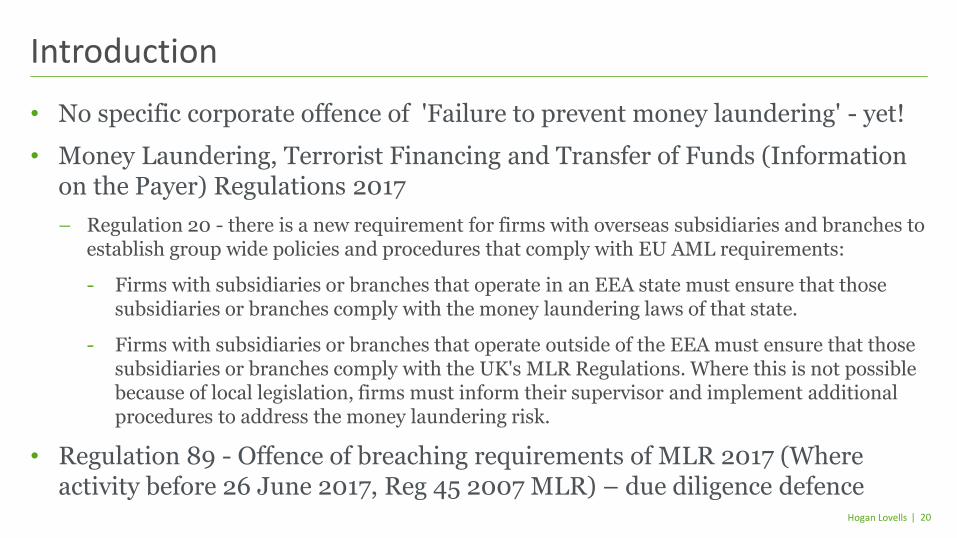

• No specific corporate offence of 'Failure to prevent money laundering' - yet!

• Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017

– Regulation 20 - there is a new requirement for firms with overseas subsidiaries and branches to establish group wide policies and procedures that comply with EU AML requirements:

- Firms with subsidiaries or branches that operate in an EEA state must ensure that those subsidiaries or branches comply with the money laundering laws of that state.

- Firms with subsidiaries or branches that operate outside of the EEA must ensure that those subsidiaries or branches comply with the UK's MLR Regulations. Where this is not possible because of local legislation, firms must inform their supervisor and implement additional procedures to address the money laundering risk.

• Regulation 89 - Offence of breaching requirements of MLR 2017 (Where activity before 26 June 2017, Reg 45 2007 MLR) – due diligence defence

Introduction

Hogan Lovells | 21

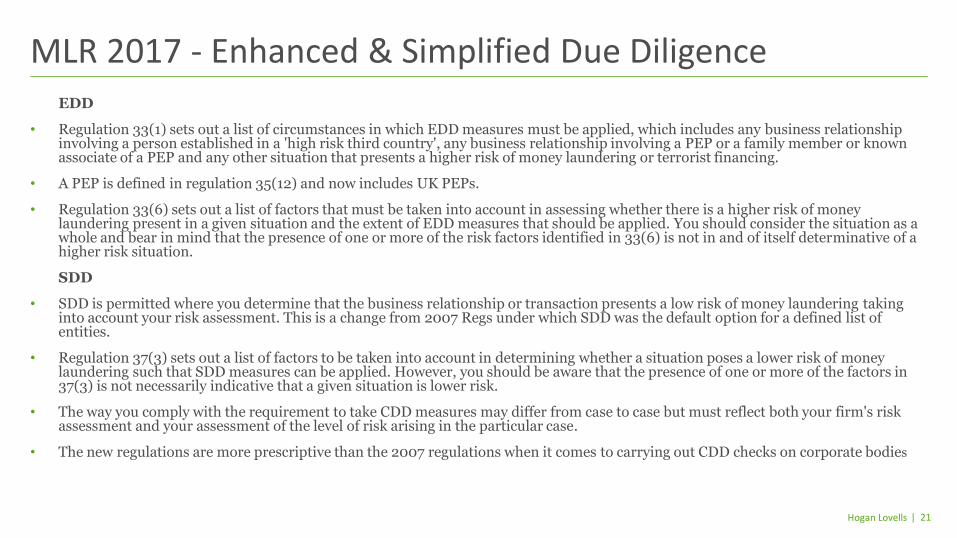

EDD

• Regulation 33(1) sets out a list of circumstances in which EDD measures must be applied, which includes any business relationship involving a person established in a 'high risk third country', any business relationship involving a PEP or a family member or known associate of a PEP and any other situation that presents a higher risk of money laundering or terrorist financing.

• A PEP is defined in regulation 35(12) and now includes UK PEPs.

• Regulation 33(6) sets out a list of factors that must be taken into account in assessing whether there is a higher risk of money laundering present in a given situation and the extent of EDD measures that should be applied. You should consider the situation as a whole and bear in mind that the presence of one or more of the risk factors identified in 33(6) is not in and of itself determinative of a higher risk situation.

SDD

• SDD is permitted where you determine that the business relationship or transaction presents a low risk of money laundering taking into account your risk assessment. This is a change from 2007 Regs under which SDD was the default option for a defined list of entities.

• Regulation 37(3) sets out a list of factors to be taken into account in determining whether a situation poses a lower risk of money laundering such that SDD measures can be applied. However, you should be aware that the presence of one or more of the factors in 37(3) is not necessarily indicative that a given situation is lower risk.

• The way you comply with the requirement to take CDD measures may differ from case to case but must reflect both your firm's risk assessment and your assessment of the level of risk arising in the particular case.

• The new regulations are more prescriptive than the 2007 regulations when it comes to carrying out CDD checks on corporate bodies

MLR 2017 - Enhanced & Simplified Due Diligence

Hogan Lovells | 22

• Updated JMLSG Guidance (June 2017)

• FCA's Guidance on PEPs (July 2017)

• Wolfsberg Group's Guidance on PEPs (May 2017)

• FCA's 'Financial Crime: a Guide for Firms' (updated 2016)

• Don't forget FCA Thematic Reviews

AML Guidance

Hogan Lovells | 23

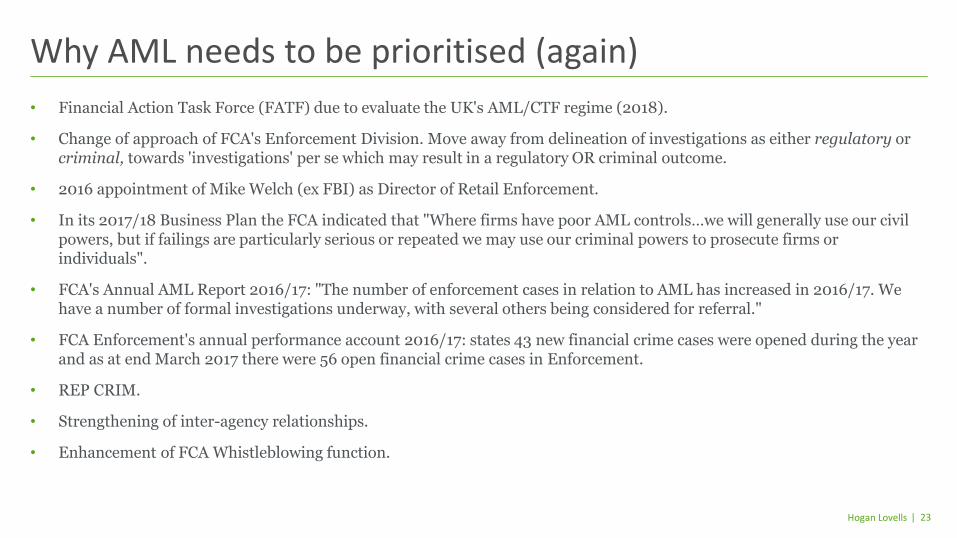

• Financial Action Task Force (FATF) due to evaluate the UK's AML/CTF regime (2018).

• Change of approach of FCA's Enforcement Division. Move away from delineation of investigations as either regulatory or criminal, towards 'investigations' per se which may result in a regulatory OR criminal outcome.

• 2016 appointment of Mike Welch (ex FBI) as Director of Retail Enforcement.

• In its 2017/18 Business Plan the FCA indicated that "Where firms have poor AML controls…we will generally use our civil powers, but if failings are particularly serious or repeated we may use our criminal powers to prosecute firms or individuals".

• FCA's Annual AML Report 2016/17: "The number of enforcement cases in relation to AML has increased in 2016/17. We have a number of formal investigations underway, with several others being considered for referral."

• FCA Enforcement's annual performance account 2016/17: states 43 new financial crime cases were opened during the year and as at end March 2017 there were 56 open financial crime cases in Enforcement.

• REP CRIM.

• Strengthening of inter-agency relationships.

• Enhancement of FCA Whistleblowing function.

Why AML needs to be prioritised (again)

Failure to prevent economic crime

| 25 Hogan Lovells

• Common law rule on corporate liability – identification doctrine.

– Where an offence has a mens rea element (and the route to criminal liability is not expressly set out) a company is only criminally liable for the acts of a person who was speaking or acting as the company's "directing mind and will", i.e. a member of the board of directors or a very senior manager.

• Failure to prevent bribery – section 7 Bribery Act 2010.

• Failure to prevent facilitation of tax evasion – sections 45 and 46 Criminal Finances Act 2017.

Why is reform necessary?

Failure to prevent economic crime

| 26 Hogan Lovells

• To assess whether there are problems with the identification doctrine and to consider the case for reform, in areas of economic crime other than bribery and tax evasion.

• CFE closed at the end of March 2017:

– Option 1 – Legislative amendment of the identification doctrine

– Option 2 – Creating a (strict) vicarious liability offence

– Option 3 – Creating a (strict) direct liability offence

– Option 4 – Creating an offence with failure to prevent as an element

– Option 5 – Regulatory reform on a sector by sector basis

Government call for evidence (January to March 2017)

Failure to prevent economic crime

| 27 Hogan Lovells

• MoJ favours Option 3 - new "failure to prevent" offences.

• Advantages:

– Readily applicable to offending by large and small organisations.

– Incentivises companies to concentrate on prevention of economic crime.

– May enhance the effectiveness of DPAs.

• Should the case be made out, the MoJ is likely to apply for offences of failure to prevent:

– Fraud.

– False accounting.

– Money laundering.

• Extension to human rights abuses too?

Looking to the future

Failure to prevent economic crime

Failure to prevent human rights abuses

| 29 Hogan Lovells

• Recommendation by the Joint Committee on Human Rights – report on Human Rights and Business published in April 2017.

• A duty on all companies to prevent human rights abuses.

– Including on parent companies to prevent abuses by subsidiaries.

– Potentially throughout supply chain to prevent abuses by (sub-)contractors.

– Both civil remedies and criminal sanctions.

• Modelled on section 7 of the Bribery Act 2010.

– Offence of failure to prevent human rights abuses.

– Defence of adequate procedures / effective human rights due diligence.

What is the proposal?

Failure to prevent human rights abuses

| 30 Hogan Lovells

• UN Guiding Principles On Business and Human Rights.

– Businesses must act with due diligence to avoid infringing on the rights of others and to address any negative impacts.

• UK track record of leading on human rights issues – e.g. first National Action Plan.

• But NAP criticised as being too modest and lacking a strategic vision.

• Difficulties with access to justice.

– Complex corporate structures.

– Jurisdictional issues with supply chains.

– Focus on "directing mind" of one individual – highly unlikely in many large companies.

Why is a new offence needed?

Failure to prevent human rights abuses

| 31 Hogan Lovells

• US

– Dodd-Frank Wall Street Reform and Consumer Protection Act 2010.

– California Transparency in Supply Chains Act 2010.

• France

– Corporate Duty of Vigilance Law 2017.

• Netherlands

– 2016 banking sector agreement on international responsible business conduct regarding human rights.

– Child Labour Due Diligence Act 2017.

Are there similar duties or offences in other jurisdictions?

Failure to prevent human rights abuses

| 32 Hogan Lovells

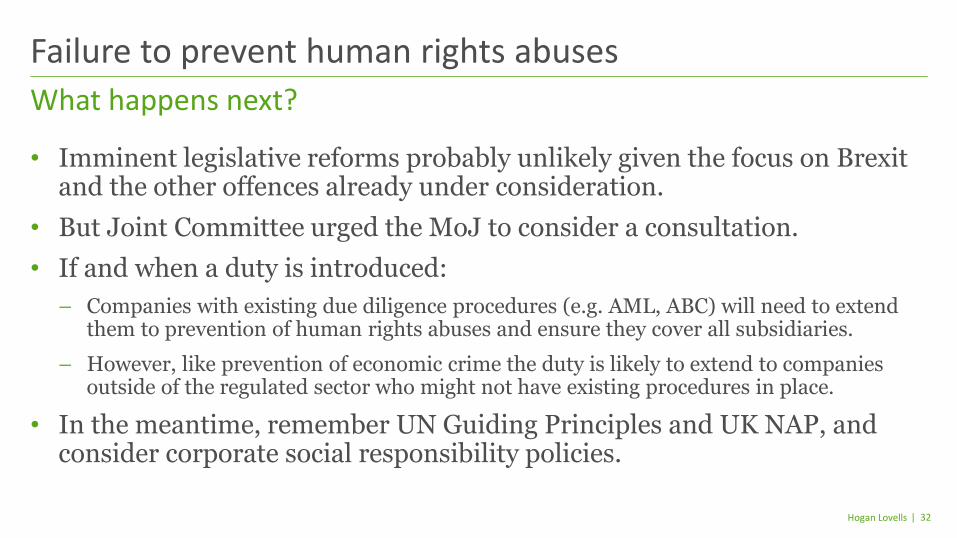

• Imminent legislative reforms probably unlikely given the focus on Brexit and the other offences already under consideration.

• But Joint Committee urged the MoJ to consider a consultation.

• If and when a duty is introduced:

– Companies with existing due diligence procedures (e.g. AML, ABC) will need to extend them to prevention of human rights abuses and ensure they cover all subsidiaries.

– However, like prevention of economic crime the duty is likely to extend to companies outside of the regulated sector who might not have existing procedures in place.

• In the meantime, remember UN Guiding Principles and UK NAP, and consider corporate social responsibility policies.

What happens next?

Failure to prevent human rights abuses

Speakers

T

| 34

Financial Crime Investigations White Collar and Fraud

Areas of Focus

+44 20 7296 2982

Claire has 25 years' experience of financial crime cases and investigations. She advises corporates,

professional firms and individuals in relation to a variety of financial crime matters including money

laundering, bribery and corruption, tax evasion and fraud.

She joined Hogan Lovells in April 2017 from the Financial Conduct Authority where she was Chief

Criminal Counsel. While at the FCA she oversaw numerous investigations and prosecutions,

including Operation Tabernula, the largest and most complex insider dealing ring ever prosecuted

in the UK.

Before joining the FCA, Claire was a partner at Peters & Peters where she specialised in business

crime. Claire is recognised in Who's Who Legal 2017 as an expert in Business Crime Defence.

Partner, London

Claire Lipworth

Speaker

T

| 35

Tax Investigations Litigation Administrative and Public Law

Areas of Focus

+44 20 7296 2966

Partner, London

Rupert Shiers

Speaker

For more than fifteen years, Rupert has navigated complex HMRC discussions, tax litigation, and

tax-related internal investigations. He leads Hogan Lovells' contentious tax practice in the UK, and

across Europe.

Rupert has worked full-time in HMRC disputes since before it became a recognised legal discipline.

The main legal directories have recognised him as a leader in his field since the mid-2000s. He also

worked for many years with ex-HMRC officers and chartered tax advisers in a Big 4 environment

before returning to practice in an international law firm.

Clients in multiple sectors value Rupert's skills. He has particular experience in banking, insurance

and technology, but also in real estate, retail, media, manufacturing and investment funds.

T

| 36

Investigations Financial Crime Litigation

Areas of Focus

+44 20 7296 5493

For almost 10 years Hannah has been helping banks, financial institutions and corporates to resolve

their disputes. She has extensive experience of managing cross-border and domestic civil and

criminal investigations, and she brings and defends high value and complex High Court claims.

Hannah was a lead associate advising one of the banks involved in the international investigations

into the alleged manipulation of LIBOR, one of the most complex and high profile investigations

arising from the financial crisis.

Resolving disputes is all very well, but Hannah recognises that clients generally prefer to avoid them

altogether. She uses her experience to help clients identify potential regulatory and litigation risks

and take proactive steps to address them.

Senior Associate, London

Hannah Piper

Speaker

"Hogan Lovells" or the "firm" is an international legal practice that includes Hogan Lovells International LLP, Hogan Lovells US LLP and their affiliated businesses.

The word “partner” is used to describe a partner or member of Hogan Lovells International LLP, Hogan Lovells US LLP or

any of their affiliated entities or any employee or consultant with equivalent standing.. Certain individuals, who are designated as partners, but who are not members of Hogan Lovells International LLP, do not hold qualifications equivalent

to members.

For more information about Hogan Lovells, the partners and their qualifications, see www.hoganlovells.com.

Where case studies are included, results achieved do not guarantee similar outcomes for other clients. Attorney advertising. Images of people may feature current or former lawyers and employees at Hogan Lovells or models not

connected with the firm.

© Hogan Lovells 2017. All rights reserved

www.hoganlovells.com