self-insurer jan 2016

DESCRIPTION

ÂTRANSCRIPT

OF BEING YOUR TRUSTEDPARTNER IN INSURANCE

Ensuring your success for 25 years with customized, forward-thinking brokerage, claims solutions and insurance services that are carefully planned, overseen by our dedicated support team and backed by years of experience. MIDLANDS is your total insurance solution.

WORKERS’ COMPENSATION | PUBLIC ENTITY | CATASTROPHIC CLAIMS MANAGEMENT | THIRD PARTY ADMINISTRATION | EXCESS WORKERS’ COMPENSATION | AUDITS | COMMUTATION | UTILIZATION & REVIEW

800.800.4007 midlandsmgt.com [email protected]

OF BEING YOUR TRUSTEDPARTNER IN INSURANCE

Ensuring your success for 25 years with customized, forward-thinking brokerage, claims solutions and insurance services that are carefully planned, overseen by our dedicated support team and backed by years of experience. MIDLANDS is your total insurance solution.

WORKERS’ COMPENSATION | PUBLIC ENTITY | CATASTROPHIC CLAIMS MANAGEMENT | THIRD PARTY ADMINISTRATION | EXCESS WORKERS’ COMPENSATION | AUDITS | COMMUTATION | UTILIZATION & REVIEW

800.800.4007 midlandsmgt.com [email protected]

January 2016 | The Self-Insurer 3

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

www.sipconline.net

4

January 2016 Volume 87

Bruce Shutan

AWinding Road

Self-Insuranceto

22

Tim Callender

Fiduciary Liability

the& Solution

GAP

12 INside the Beltway SIIA Moves Needle on Enterprise Risk Captive Legislation, Congress Moves Forward

14 OUTside the Beltway SIIA Members Continue to Clarify Stop-Loss with Texas Regulator

16 Captives Facing Legislative, Regulatory and Financial Obstacles in 2016

30 PPACA, HIPAA and Federal Health Benefit Mandates EEOC’s Proposed Rules for Wellness Programs Under the Genetic Information Nondiscrimination Act (GINA)

36 RRGs Report Financially Stable Results Through Third Quarter 2015

40 SIIA Endeavors A New Year, A New Chairman

The Self-Insurer (ISSN 10913815) is published monthly by Self-Insurers’ Publishing Corp. (SIPC)

Postmaster : Send address changes to The Self-Insurer P.O. Box 1237 Simpsonville, SC 29681

Editorial StaffPUBLISHING DIRECTORErica Massey

SENIOR EDITORGretchen Grote

CONTRIBUTING EDITORMike Ferguson

DIRECTOR OF OPERATIONSJustin Miller

DIRECTOR OF ADVERTISINGShane Byars

EDITORIAL ADVISORSBruce ShutanKarrie Hyatt

Editorial and Advertising Offi ceP.O. 1237, Simpsonville, SC 29681(888) 394-5688

2016 Self-Insurers’ Publishing Corp. Offi cers

James A. Kinder, CEO/Chairman

Erica M. Massey, President

Lynne Bolduc, Esq. Secretary

January 2016 | The Self-Insurer 5

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

A WINDING ROAD | FEATURE

95 and sharing the same benefits adviser, these two small and midsize employers charted the same course to save on employee health care costs. After years of fully insured plans, they briefly transitioned to a medical stop-loss captive program before embracing self-insurance for the long haul – despite being told their groups were too small to pursue that route.

Along the way, there was a sense about hedging their bets. A famous quote by actor Wesley Snipes in “Passenger 57” was invoked to describe the crossroads faced by NorthBay, which runs group retreats and other school-funded programs for sixth graders as well as other elementary and middle school students.

“You ever play roulette?” Mark Gerhard, the organization’s finance manager, remembers the film’s protagonist asking a European tourist, whose response was: “On occasion.” Snipes’s character then says, “ ‘Well, let me give you a little piece of advice: Always bet on black.’ So we thought it was better to bet on ourselves.”

A similar strategy unfolded at St. John Properties, faced down a 19% premium increase by United Healthcare. “We just thought that was ridiculous,”

recalls Teri Mallonee, the company’s VP of operations. In 2009, the company was paying about $9,000 per employee per year, which would have climbed to $12,000 if the fully insured plans were renewed.

While NorthBay was performing well in a traditional fully insured environment, Gerhard says “they were coming back with 10% increases every

year, even though they were making $200,000 in profit. So that was a little bit hard to take year after year.”

A Captive Transition The next stop for NorthBay

and St. John Properties was to join a heterogeneous medical stop-loss captive featuring at its height about 35 like-minded employers from various industries. It was the first benefit captive created in the Mid-Atlantic region, offering an “opportunity to take a peek under the hood and see what’s really driving their health care costs,” says Gary C. Becker, CEO of the Becker Benefit Group, Inc., a boutique benefit consulting firm.

He created the captive in 2010 from his own client base, then banded together with several brokers in 2013 to deepen its risk pool. Requirements included having to meet a certain risk profile and be willing to sponsor a wellness initiative. Each captive member also was expected to pay all claims within its self-funded retention and buy stop-loss insurance, including both specific and aggregate claim protection. In addition, they would post collateral to the group captive, but retain unused claim reserves.

“All these groups that I put into the captive were fully insured,” he explains, noting how each of these employers had arrived at a point in time where “they weren’t just going to sit back and just take it on the chin every year.”

St. John Properties was one of the first groups to join the captive in 2010, while North Bay came on board the following year. Before long,

they both determined that it made more sense to be self-funded on a standalone basis. The two companies were among the captive’s healthier groups and concerned about what Becker calls “a blending effect” that involves mixing the risks of disparate employee populations. Ultimately, they lost money and decided not to want to wait long enough to share in

any surplus down the road in the form of dividends. NorthBay exited the captive in 2012, after just eight months, while St. John Properties left in 2013, after three years.

Mallonee initially considered moving from a fully insured

arrangement to self-insurance, but was advised that their group was too small and it was a risky proposition. So instead, the captive became a bridge to self-insurance, but the journey wasn’t without troubled water.

“We were getting nailed,” Mallonee explains. “Every time we put up the collateral, they were calling the collateral at the end of the year, so basically it was really costing us more.” Collateral calls were made three years in a row, with multi-million dollar transplants involving other captive members cited as a major driver of the increase. Thus, it was time to move on.

“Once they learned about all these wonderful opportunities to manage risk, they felt that it was in their own best interest to do it and have many stop-loss carriers bidding for their business,” Becker says of his clients that sought yet another change in strategy.

In transitioning from a captive to stand-alone self-insurance, Becker says employers may prefer to shop for the best deal on stop-loss on their own and re-evaluate the pricing at a

6 The Self-Insurer | www.sipconline.net

SUBROGATION RIGHTS | FEATURE

later date, whereas all members of the captive lock in longer-term pricing with a single stop-loss carrier.

Although Becker’s clients were eager to cut bait from the captive as confidence in their risk-management strategies grew, he’s still a big believer in the potential of these arrangements.

“It’s absolutely the right place for employers to go into and stay into for a long time,” he says. “Every employer has a different level of risk tolerance and need to make a decision that they believe is in their own best interest... The whole idea of a captive is you’re going to have your good years and bad years.”

A Matter of Life or Death

At a time when many employers balked at forcing employees into wellness initiatives for fear of discrimination claims or undermined morale, St. John Properties decided to make twice-annual biometric screenings mandatory.

“I think people get too concerned or worried about the employees’ responses and then you take these little baby-steps,” Mallonee observes. “It’s like tearing off a Band-Aid. Just do it. Just tell them it’s part of being on the insurance.”

Employees of St. John Properties are now reaping the rewards of this tough-love-in-the-workplace approach. They received up to $1,500 toward their health savings account, which led to a marked improvement in

St. John PropertiesUHC/PWC Trend

UHC/PWC PEPY

Self‐funded Collateral Call HSA Contr.Total Actual

CostsPEPY Savings

Number of Ee's

Number of Months

Annual SavingsCumulative Savings

2009 $8,937 96

2010 19.00% $10,635 $11,223 $588 $0 $11,810 ‐$1,175 94 6 ‐$55,245 ‐$55,245

2011 9.00% $11,592 $11,242 $769 $0 $12,011 ‐$419 89 11 ‐$34,168 ‐$89,4122012 8.50% $12,578 $12,029 $0 $0 $12,029 $549 94 12 $51,579 ‐$37,8342013 7.50% $13,521 $9,213 $0 $9,213 $4,307 82 12 $353,203 $315,3692014 6.50% $14,400 $8,123 $1,145 $9,269 $5,131 84 12 $430,996 $746,3652015 6.80% $15,379 $5,333 $637 $5,971 $9,408 87 10 $1,130,308 $1,876,6732016 6.50% $16,378

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

PWCActualUHC

‐$55,245‐$89,412 ‐$37,834

$315,369

$746,365

$1,876,673

‐$500,000

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

2010 2011 2012 2013 2014 2015

Cumulative Savings Since 2010

2010

2011

2012

2013

2014

2015

‐$55,245 ‐$34,168 $51,579

$353,203 $430,996

$1,130,308

‐$200,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

2010 2011 2012 2013 2014 2015

Annual Savings Since 2010

2010

2011

2012

2013

2014

2015

$8,937

$11,810 $12,011 $12,029

$9,213 $9,269

$5,971

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

Actual

UHC/PWC

St. John PropertiesUHC/PWC Trend

UHC/PWC PEPY

Self‐funded Collateral Call HSA Contr.Total Actual

CostsPEPY Savings

Number of Ee's

Number of Months

Annual SavingsCumulative Savings

2009 $8,937 96

2010 19.00% $10,635 $11,223 $588 $0 $11,810 ‐$1,175 94 6 ‐$55,245 ‐$55,245

2011 9.00% $11,592 $11,242 $769 $0 $12,011 ‐$419 89 11 ‐$34,168 ‐$89,4122012 8.50% $12,578 $12,029 $0 $0 $12,029 $549 94 12 $51,579 ‐$37,8342013 7.50% $13,521 $9,213 $0 $9,213 $4,307 82 12 $353,203 $315,3692014 6.50% $14,400 $8,123 $1,145 $9,269 $5,131 84 12 $430,996 $746,3652015 6.80% $15,379 $5,333 $637 $5,971 $9,408 87 10 $1,130,308 $1,876,6732016 6.50% $16,378

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

PWCActualUHC

‐$55,245‐$89,412 ‐$37,834

$315,369

$746,365

$1,876,673

‐$500,000

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

2010 2011 2012 2013 2014 2015

Cumulative Savings Since 2010

2010

2011

2012

2013

2014

2015

‐$55,245 ‐$34,168 $51,579

$353,203 $430,996

$1,130,308

‐$200,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

2010 2011 2012 2013 2014 2015

Annual Savings Since 2010

2010

2011

2012

2013

2014

2015

$8,937

$11,810 $12,011 $12,029

$9,213 $9,269

$5,971

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

Actual

UHC/PWC

St. John PropertiesUHC/PWC Trend

UHC/PWC PEPY

Self‐funded Collateral Call HSA Contr.Total Actual

CostsPEPY Savings

Number of Ee's

Number of Months

Annual SavingsCumulative Savings

2009 $8,937 96

2010 19.00% $10,635 $11,223 $588 $0 $11,810 ‐$1,175 94 6 ‐$55,245 ‐$55,245

2011 9.00% $11,592 $11,242 $769 $0 $12,011 ‐$419 89 11 ‐$34,168 ‐$89,4122012 8.50% $12,578 $12,029 $0 $0 $12,029 $549 94 12 $51,579 ‐$37,8342013 7.50% $13,521 $9,213 $0 $9,213 $4,307 82 12 $353,203 $315,3692014 6.50% $14,400 $8,123 $1,145 $9,269 $5,131 84 12 $430,996 $746,3652015 6.80% $15,379 $5,333 $637 $5,971 $9,408 87 10 $1,130,308 $1,876,6732016 6.50% $16,378

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

PWCActualUHC

‐$55,245‐$89,412 ‐$37,834

$315,369

$746,365

$1,876,673

‐$500,000

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

2010 2011 2012 2013 2014 2015

Cumulative Savings Since 2010

2010

2011

2012

2013

2014

2015

‐$55,245 ‐$34,168 $51,579

$353,203 $430,996

$1,130,308

‐$200,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

2010 2011 2012 2013 2014 2015

Annual Savings Since 2010

2010

2011

2012

2013

2014

2015

$8,937

$11,810 $12,011 $12,029

$9,213 $9,269

$5,971

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

Actual

UHC/PWC

St. John PropertiesUHC/PWC Trend

UHC/PWC PEPY

Self‐funded Collateral Call HSA Contr.Total Actual

CostsPEPY Savings

Number of Ee's

Number of Months

Annual SavingsCumulative Savings

2009 $8,937 96

2010 19.00% $10,635 $11,223 $588 $0 $11,810 ‐$1,175 94 6 ‐$55,245 ‐$55,245

2011 9.00% $11,592 $11,242 $769 $0 $12,011 ‐$419 89 11 ‐$34,168 ‐$89,4122012 8.50% $12,578 $12,029 $0 $0 $12,029 $549 94 12 $51,579 ‐$37,8342013 7.50% $13,521 $9,213 $0 $9,213 $4,307 82 12 $353,203 $315,3692014 6.50% $14,400 $8,123 $1,145 $9,269 $5,131 84 12 $430,996 $746,3652015 6.80% $15,379 $5,333 $637 $5,971 $9,408 87 10 $1,130,308 $1,876,6732016 6.50% $16,378

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

PWCActualUHC

‐$55,245‐$89,412 ‐$37,834

$315,369

$746,365

$1,876,673

‐$500,000

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

2010 2011 2012 2013 2014 2015

Cumulative Savings Since 2010

2010

2011

2012

2013

2014

2015

‐$55,245 ‐$34,168 $51,579

$353,203 $430,996

$1,130,308

‐$200,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

2010 2011 2012 2013 2014 2015

Annual Savings Since 2010

2010

2011

2012

2013

2014

2015

$8,937

$11,810 $12,011 $12,029

$9,213 $9,269

$5,971

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

Actual

UHC/PWC

St. John PropertiesUHC/PWC Trend

UHC/PWC PEPY

Self‐funded Collateral Call HSA Contr.Total Actual

CostsPEPY Savings

Number of Ee's

Number of Months

Annual SavingsCumulative Savings

2009 $8,937 96

2010 19.00% $10,635 $11,223 $588 $0 $11,810 ‐$1,175 94 6 ‐$55,245 ‐$55,245

2011 9.00% $11,592 $11,242 $769 $0 $12,011 ‐$419 89 11 ‐$34,168 ‐$89,4122012 8.50% $12,578 $12,029 $0 $0 $12,029 $549 94 12 $51,579 ‐$37,8342013 7.50% $13,521 $9,213 $0 $9,213 $4,307 82 12 $353,203 $315,3692014 6.50% $14,400 $8,123 $1,145 $9,269 $5,131 84 12 $430,996 $746,3652015 6.80% $15,379 $5,333 $637 $5,971 $9,408 87 10 $1,130,308 $1,876,6732016 6.50% $16,378

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

PWCActualUHC

‐$55,245‐$89,412 ‐$37,834

$315,369

$746,365

$1,876,673

‐$500,000

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

2010 2011 2012 2013 2014 2015

Cumulative Savings Since 2010

2010

2011

2012

2013

2014

2015

‐$55,245 ‐$34,168 $51,579

$353,203 $430,996

$1,130,308

‐$200,000

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

2010 2011 2012 2013 2014 2015

Annual Savings Since 2010

2010

2011

2012

2013

2014

2015

$8,937

$11,810 $12,011 $12,029

$9,213 $9,269

$5,971

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

2009 2010 2011 2012 2013 2014 2015

UHC/PWC PEPY Trend vs Self‐Funded PEPY

Actual

UHC/PWC

[St. John Properties by the Numbers]

January 2016 | The Self-Insurer 7

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

8 The Self-Insurer | www.sipconline.net

R e m e m b e R t h i s l o g o f o R

a l l t h i n g s s e l f - f u n d e d !

Benefit Indemnity Corporation is a far-reaching enterprise designed to help various stakeholders in and touched by the insurance industry to access the knowledge, skills and strategies to help them succeed amidst the changing world of insurance and health care reform.

• All group sizes from 10 to infinity• Electronic enrollment• Risk free analysis

• Self-funded exchange• Exchange-like selection capabilities• Wellness including biometrics

i f yo u c a n d R e a m i t, W e c a n b u i l d i t.

i f yo u c a n s e l l i t, W e c a n d e l i v e R i t.

i f yo u h av e p R o d u c t, W e a d d d i s t R i b u t i o n .

i f yo u n e e d i t. . . l e t u s k n o W.

Call 443.275.7412 with any inquiry.

Rodger Bayne, President

303 West Allegheny Avenue • Towson, MD 21204Phone: 443-275-7400 • Fax: [email protected] • www.benefitindemnity.co

January 2016 | The Self-Insurer 9

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

SUBROGATION RIGHTS | FEATURE

biometric screening scores, as well

as free Fitbits in 2015. Also as part

of its health-conscious culture, St.

John Properties offers free vitamins

and toothbrushes, as well as physical

therapy sessions lasting 30 minutes

and an on-site gym.

Becker likened the notion of lower

monthly premiums for employees

with favorable biometric screening

results to a good-driver discount on

auto insurance, adding that it offers

employees “an incentive to start thinking

about taking their health more seriously.”

Beyond these incentives, which

have been well received, the company

occasionally is reminded that the

right health plan design could actually

save a life. For example, warning signs

surfaced for at least one employee

who was then able to make some

adjustments to reduce his high blood

pressure, such as losing 40 pounds.

There also was a light-hearted, weight-

loss contest during which employees

had to appear in a bikini. Another

employee wasn’t so lucky. He suffered

a stroke at a young age before

biometric screenings were required,

which Mallonee believes could have

prevented the unfortunate event.

Unlike St. John Properties,

NorthBay shied away from biometric

screening because of employee

pushback. It also wasn’t deemed all

that beneficial based on the group’s

current health status.

The results at St. John Properties

have been significant, with $1.5 million

saved over the past five and a half

NorthBayCarefirst & PWC Trend

PEPY Self‐funded Collateral CallTotal Self‐Funded

PEPY SavingsNumber of

Ee'sNumber of Months

Annual SavingsCumulative Savings

2010 $8,191

2011 9.00% $8,928 $6,364 $0 $6,364 $2,564 65 12 $166,667 $166,667

2012 8.50% $9,687 $5,617 $0 $5,617 $4,070 68 12 $276,785 $443,4522013 7.50% $10,414 $4,969 $0 $4,969 $5,445 69 12 $375,690 $819,1422014 6.50% $11,091 $6,519 $0 $6,519 $4,572 60 12 $274,305 $1,093,4462015 6.80% $11,845 $6,515 $0 $6,515 $5,330 65 10 $288,701 $1,382,1472016 6.50% $12,615

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

PEPY Spend Comparison

Carefirst & PWC Trend

Actual

$166,667

$443,452

$819,142

$1,093,446

$1,382,147

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

2011 2012 2013 2014 2015

Cumulative Savings

$166,667

$276,785

$375,690

$274,305$288,701

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2011 2012 2013 2014 2015

Annual Savings

$6,364 $5,617$4,969

$6,519 $6,515

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

Fully Insured Trend versus Actual PEPY

Actual

Carefirst & PWC Trend

[NorthBay by the Numbers]NorthBay

Carefirst & PWC Trend

PEPY Self‐funded Collateral CallTotal Self‐Funded

PEPY SavingsNumber of

Ee'sNumber of Months

Annual SavingsCumulative Savings

2010 $8,191

2011 9.00% $8,928 $6,364 $0 $6,364 $2,564 65 12 $166,667 $166,667

2012 8.50% $9,687 $5,617 $0 $5,617 $4,070 68 12 $276,785 $443,4522013 7.50% $10,414 $4,969 $0 $4,969 $5,445 69 12 $375,690 $819,1422014 6.50% $11,091 $6,519 $0 $6,519 $4,572 60 12 $274,305 $1,093,4462015 6.80% $11,845 $6,515 $0 $6,515 $5,330 65 10 $288,701 $1,382,1472016 6.50% $12,615

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

PEPY Spend Comparison

Carefirst & PWC Trend

Actual

$166,667

$443,452

$819,142

$1,093,446

$1,382,147

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

2011 2012 2013 2014 2015

Cumulative Savings

$166,667

$276,785

$375,690

$274,305$288,701

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2011 2012 2013 2014 2015

Annual Savings

$6,364 $5,617$4,969

$6,519 $6,515

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

Fully Insured Trend versus Actual PEPY

Actual

Carefirst & PWC Trend

NorthBayCarefirst & PWC Trend

PEPY Self‐funded Collateral CallTotal Self‐Funded

PEPY SavingsNumber of

Ee'sNumber of Months

Annual SavingsCumulative Savings

2010 $8,191

2011 9.00% $8,928 $6,364 $0 $6,364 $2,564 65 12 $166,667 $166,667

2012 8.50% $9,687 $5,617 $0 $5,617 $4,070 68 12 $276,785 $443,4522013 7.50% $10,414 $4,969 $0 $4,969 $5,445 69 12 $375,690 $819,1422014 6.50% $11,091 $6,519 $0 $6,519 $4,572 60 12 $274,305 $1,093,4462015 6.80% $11,845 $6,515 $0 $6,515 $5,330 65 10 $288,701 $1,382,1472016 6.50% $12,615

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

PEPY Spend Comparison

Carefirst & PWC Trend

Actual

$166,667

$443,452

$819,142

$1,093,446

$1,382,147

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

2011 2012 2013 2014 2015

Cumulative Savings

$166,667

$276,785

$375,690

$274,305$288,701

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2011 2012 2013 2014 2015

Annual Savings

$6,364 $5,617$4,969

$6,519 $6,515

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

Fully Insured Trend versus Actual PEPY

Actual

Carefirst & PWC Trend

NorthBayCarefirst & PWC Trend

PEPY Self‐funded Collateral CallTotal Self‐Funded

PEPY SavingsNumber of

Ee'sNumber of Months

Annual SavingsCumulative Savings

2010 $8,191

2011 9.00% $8,928 $6,364 $0 $6,364 $2,564 65 12 $166,667 $166,667

2012 8.50% $9,687 $5,617 $0 $5,617 $4,070 68 12 $276,785 $443,4522013 7.50% $10,414 $4,969 $0 $4,969 $5,445 69 12 $375,690 $819,1422014 6.50% $11,091 $6,519 $0 $6,519 $4,572 60 12 $274,305 $1,093,4462015 6.80% $11,845 $6,515 $0 $6,515 $5,330 65 10 $288,701 $1,382,1472016 6.50% $12,615

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

PEPY Spend Comparison

Carefirst & PWC Trend

Actual

$166,667

$443,452

$819,142

$1,093,446

$1,382,147

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

2011 2012 2013 2014 2015

Cumulative Savings

$166,667

$276,785

$375,690

$274,305$288,701

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2011 2012 2013 2014 2015

Annual Savings

$6,364 $5,617$4,969

$6,519 $6,515

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

Fully Insured Trend versus Actual PEPY

Actual

Carefirst & PWC Trend

NorthBayCarefirst & PWC Trend

PEPY Self‐funded Collateral CallTotal Self‐Funded

PEPY SavingsNumber of

Ee'sNumber of Months

Annual SavingsCumulative Savings

2010 $8,191

2011 9.00% $8,928 $6,364 $0 $6,364 $2,564 65 12 $166,667 $166,667

2012 8.50% $9,687 $5,617 $0 $5,617 $4,070 68 12 $276,785 $443,4522013 7.50% $10,414 $4,969 $0 $4,969 $5,445 69 12 $375,690 $819,1422014 6.50% $11,091 $6,519 $0 $6,519 $4,572 60 12 $274,305 $1,093,4462015 6.80% $11,845 $6,515 $0 $6,515 $5,330 65 10 $288,701 $1,382,1472016 6.50% $12,615

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

PEPY Spend Comparison

Carefirst & PWC Trend

Actual

$166,667

$443,452

$819,142

$1,093,446

$1,382,147

$0

$200,000

$400,000

$600,000

$800,000

$1,000,000

$1,200,000

$1,400,000

$1,600,000

2011 2012 2013 2014 2015

Cumulative Savings

$166,667

$276,785

$375,690

$274,305$288,701

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

2011 2012 2013 2014 2015

Annual Savings

$6,364 $5,617$4,969

$6,519 $6,515

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

2010 2011 2012 2013 2014 2015

Fully Insured Trend versus Actual PEPY

Actual

Carefirst & PWC Trend

10 The Self-Insurer | www.sipconline.net

years on a health plan that averages

about 95 employees.

“Their average spend went from

close to $11,000 per employee

per year back in 2009 before I got

involved to about $7,000 and change

this past year,” Becker marvels. “Their

spend per employee per year is going

down 30% to 40% when everybody

else’s rates or spend is going up...

They do a lot of things to enhance

the employee experience at their

company and it’s paying dividends.”

Indeed, premiums haven’t risen

in four years. “That’s huge,” Mallonee

exclaims, noting that the average per

employee per year cost is now down to

about $7,000. “We’ve been really, really,

really happy being self-insured,” she says.

Betting on Self-Insurance

When NorthBay entered the

captive market, the average age of its

65-employee group was about 28 or

29 and the workforce was healthy.

But when the numbers didn’t justify

sticking with this arrangement, the

company decided it could do better

with stand-alone self-insurance and

pocket any savings rather than hand it

over to the captive.

“The thought was we could

monitor ourselves better than we

could monitor other groups [in the

captive] that may have a lot more

employees and then worry about

them pushing health at their business,”

Gerhard explains.

He compares it to a six-sided die with ones on four of the sides, a two and three on the remaining sides. “If you roll a two, one year in six, you’re going to finish at par,” he explains. “And then maybe one year is bad and you’ve got some claims.”

As was the case with St. John Properties, NorthBay also was told that its size was inadequate for the actuaries if it switched to self-insurance and that the company should expect to pay a higher premium that would be commensurate with the risk level of a smaller group.

Still, he was confident that costs could be controlled on the front end through health and wellness programs that offered employees a financial incentive to stay healthy, as well as changing their mindset to reflect the importance of maintaining good health. This approach includes paying for free annual checkups for the workforce, whose average age is now about 32.

“Once we went into self-insurance, there was no turning back,” Gerhard notes. “We’ve been very happy.”

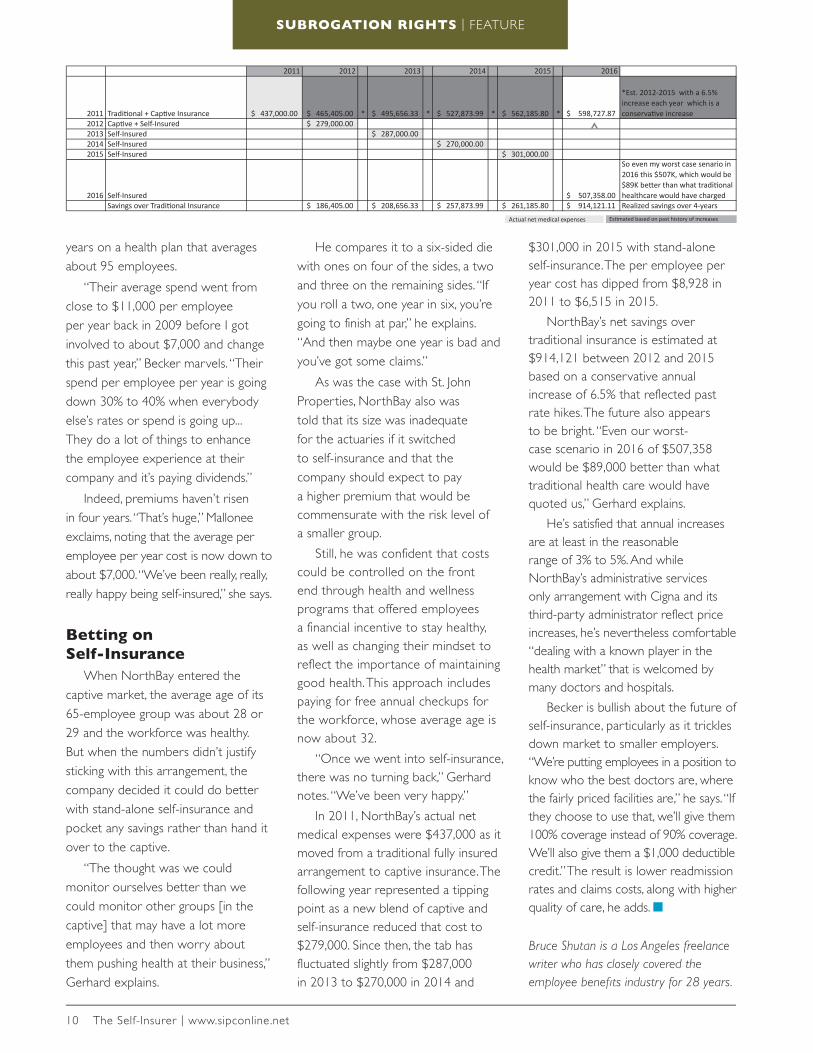

In 2011, NorthBay’s actual net medical expenses were $437,000 as it moved from a traditional fully insured arrangement to captive insurance. The following year represented a tipping point as a new blend of captive and self-insurance reduced that cost to $279,000. Since then, the tab has fluctuated slightly from $287,000 in 2013 to $270,000 in 2014 and

$301,000 in 2015 with stand-alone self-insurance. The per employee per year cost has dipped from $8,928 in 2011 to $6,515 in 2015.

NorthBay’s net savings over traditional insurance is estimated at $914,121 between 2012 and 2015 based on a conservative annual increase of 6.5% that reflected past rate hikes. The future also appears to be bright. “Even our worst-case scenario in 2016 of $507,358 would be $89,000 better than what traditional health care would have quoted us,” Gerhard explains.

He’s satisfied that annual increases are at least in the reasonable range of 3% to 5%. And while NorthBay’s administrative services only arrangement with Cigna and its third-party administrator reflect price increases, he’s nevertheless comfortable “dealing with a known player in the health market” that is welcomed by many doctors and hospitals.

Becker is bullish about the future of self-insurance, particularly as it trickles down market to smaller employers. “We’re putting employees in a position to know who the best doctors are, where the fairly priced facilities are,” he says. “If they choose to use that, we’ll give them 100% coverage instead of 90% coverage. We’ll also give them a $1,000 deductible credit.” The result is lower readmission rates and claims costs, along with higher quality of care, he adds. ■

Bruce Shutan is a Los Angeles freelance writer who has closely covered the employee benefi ts industry for 28 years.

2011 2012 2013 2014 2015 2016

2011 Tradi-onal + Cap-ve Insurance 437,000.00$ 465,405.00$ * 495,656.33$ * 527,873.99$ * 562,185.80$ * 598,727.87$

*Est. 2012-‐2015 with a 6.5% increase each year which is a conserva-ve increase

2012 Cap-ve + Self-‐Insured 279,000.00$ 2013 Self-‐Insured 287,000.00$ 2014 Self-‐Insured 270,000.00$ 2015 Self-‐Insured 301,000.00$

2016 Self-‐Insured 507,358.00$

So even my worst case senario in 2016 this $507K, which would be $89K beNer than what tradi-onal healthcare would have charged

Savings over Tradi-onal Insurance 186,405.00$ 208,656.33$ 257,873.99$ 261,185.80$ 914,121.11$ Realized savings over 4-‐years

Actual net medical expensesEs-mated based on past history of increases

2011 2012 2013 2014 2015 2016

2011 Tradi-onal + Cap-ve Insurance 437,000.00$ 465,405.00$ * 495,656.33$ * 527,873.99$ * 562,185.80$ * 598,727.87$

*Est. 2012-‐2015 with a 6.5% increase each year which is a conserva-ve increase

2012 Cap-ve + Self-‐Insured 279,000.00$ 2013 Self-‐Insured 287,000.00$ 2014 Self-‐Insured 270,000.00$ 2015 Self-‐Insured 301,000.00$

2016 Self-‐Insured 507,358.00$

So even my worst case senario in 2016 this $507K, which would be $89K beNer than what tradi-onal healthcare would have charged

Savings over Tradi-onal Insurance 186,405.00$ 208,656.33$ 257,873.99$ 261,185.80$ 914,121.11$ Realized savings over 4-‐years

Actual net medical expensesEs-mated based on past history of increases

2011 2012 2013 2014 2015 2016

2011 Tradi-onal + Cap-ve Insurance 437,000.00$ 465,405.00$ * 495,656.33$ * 527,873.99$ * 562,185.80$ * 598,727.87$

*Est. 2012-‐2015 with a 6.5% increase each year which is a conserva-ve increase

2012 Cap-ve + Self-‐Insured 279,000.00$ 2013 Self-‐Insured 287,000.00$ 2014 Self-‐Insured 270,000.00$ 2015 Self-‐Insured 301,000.00$

2016 Self-‐Insured 507,358.00$

So even my worst case senario in 2016 this $507K, which would be $89K beNer than what tradi-onal healthcare would have charged

Savings over Tradi-onal Insurance 186,405.00$ 208,656.33$ 257,873.99$ 261,185.80$ 914,121.11$ Realized savings over 4-‐years

Actual net medical expensesEs-mated based on past history of increases

SUBROGATION RIGHTS | FEATURE

January 2016 | The Self-Insurer 11

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

12 The Self-Insurer | www.sipconline.net

Many small to mid-size companies and the captive insurance industry are still assessing more restrictive

rules on small captives operating under IRS 831(b) status contained in hurried 2015 “tax extender” legislation passed by Congress just before the end of last year.

After nearly a year of close consultation with Congress by SIIA and its allies in support of enterprise risk captives (ERC), the captive industry was surprised by bill language that largely set aside common-sense modifications proposed by SIIA, business organizations and regulators. The bill language affecting ERCs had never been circulated or seen publicly before being released just days before a scheduled vote, despite numerous conversations and meeting with policymakers and their staff.

SIIA’s discussions with Congress about ERCs were prompted last February by draft bill language introduced before the Senate Finance Committee intended to curtail possible abuses of the tax law for purposes of estate planning or capital accumulation beyond the scope of anticipated risks. For most of the year SIIA’s volunteer ERC Task Force, staff and lobbyists were engaged

SIIA Moves Needle on Enterprise Risk Captive Legislation, Congress Moves Forward

INSIDE the BeltwayWritten by Dave Kirby

in discussions with Congress that resulted in a succession of three documents suggesting bill language or modifications.

While these proposed modifications helped to educate policymakers and move the conversation forward, Congress nevertheless proposed further sweeping restrictions with what many believe will cause unintended consequences.

The new law provides an increase of allowable annual captive premium tax deductions from $1.2 million to $2.2 million but will provide major challenges to captive formation and operation in its limitations on familial ownership, new asset valuation reporting and other definitional changes.

Having been part of the process throughout and commenting on the outcome, Ryan Work, SIIA’s Senior Director of Government Relations, noted, “We have made progress and moved the needle substantially from where we began last February, particularly in overcoming some of the proposed ERC restrictions that were much more onerous. In addition, we were able to discuss and educate policymakers and their staff on captive issues that most of them had never encountered.” Work said that effort established an industry presence and legislators’ awareness that will continue to gain ground and pay dividends into the future.

January 2016 | The Self-Insurer 13

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

Upon learning of the tax extender bill threat last month, SIIA immediately mobilized the ERC Task Force (listed on the right) to begin pyramiding contacts to members of Congress from themselves, clients, colleagues, state captive associations and state insurance regulators.

“Our members responded with immediate response and firepower,” Work said. He guided the grassroots network from SIIA’s Washington DC office and provided daily updates, briefing documents and strategic planning.

Jeff Simpson, chair of the ERC Task Force, said,

I know that SIIA and its allies are being heard in Washington. I’m very impressed with how quickly SIIA hit the ground running and I’m very impressed with the greater industry in

aggressively dealing with the legislative threat in an organized and civil manner.

As an example of how support for ERCs has broadened, Simpson said he attended an on-line webinar on the tax extender bill by the American Bar Association that drew the largest attendance of any ABA event he had witnessed.

SIIA’s quick response in attempting pushback to the bill language was enabled by advance planning, in Simpson’s view. “We started the ERC group just over a year ago, before a significant government threat against small captives surfaced,” he said. “If we hadn’t created that structure to advocate for the industry, we couldn’t have responded in time to head off some of the worst legislative threats.” At one time, draft bill language would have prohibited ERCs from accessing reinsurance.

SIIA intends to continue this year its interface with Congress in support of ERCs and has already set meetings with key Members and staff to consider more flexible modifications to the rules. ■

Further information will be available from Ryan Work in SIIA’s Washington offi ce at [email protected] or (202) 595-0642.

Enterprise Risk Captive Task Force

MembersJarid Beck

Risk Management Associates

Bill BuechlerCrowe Horwath

Doug ButlerMIJS

John CapassoCaptive Planning Associates

Kevin DohertyNelson Mullins

Park EddyActive Captive Management

Rick EldridgeThe Intuitive Companies

Martin EveleighAtlas Captives

Sandra FentersCapterra Risk Solutions

Adam ForstotUSA Risk

Matt HolycrossThe Taft Companies

Matthew HowardMIJS

Jeremy HuishArtex

Keith LanglandsSynergy Captive Strategies

Jerry MessickElevate Captives

Josh MillerKeyState

Kevin MyersOxford

Michael O’MalleyStrategic Risk Solutions

Kerrie Riker-KellerThe Intuitive Companies

Mathew RobinsonWilmington Trust

Dana SheridanActive Captive Management

Jeff SimpsonGordon, Founaris & Mammarella, PA

Robert VogelProGroup

14 The Self-Insurer | www.sipconline.net

SIIA Members Continue to Clarify Stop-Loss with Texas Regulator

OUTSIDE the BeltwayWritten by Dave Kirby

TEXAS

SIIA members along with representatives of the Texas

Association of Life and Health Insurers (TALHI) and the Texas Association of Business (TAB) joined in a second recent consultation with the Texas Department of Insurance (TDI) as it ponders a draft rewrite of employee health insurance regulations targeted for adoption later this year.

The main point of discussion was stop-loss insurance for self-insured employee health plans. In contrast with the earlier public hearing that drew SIIA members’ participation, this was a lobbying event initiated by TALHI in partnership with SIIA.

“The best kind of lobbying is performed by local constituents of any government body,” said Adam Brackemyre, SIIA Director of State Government Relations, who was among the industry delegation that held meetings last month with TDI leadership and staff members of Governor Greg Abbott. “We very much appreciated TALHI’s leadership on this project.”

The SIIA contingent for the Austin meetings included Jay Ritchie of HCC Life and a SIIA Director ; Barry Koonce and Marc Marion of

American Fidelity Assurance Company;

Catherine Bresler of The Trustmark

Companies and Brackemyre. TDI

participants included Doug Danzeiser,

Deputy Commissioner, Life, Health

and Licensing.

As noted in a previous Self-Insurer

article, SIIA is concerned that some

employers would lose their health

plans and others would see stop-loss

premium increases if the early draft of

regulations were adopted. Particularly

troubling is a possible small business

minimum aggregate of $4,000 per

enrollee. SIIA members report that that

requirement is far too expensive for

small businesses and SIIA has consistently

urged the elimination of the minimum

products standards from the draft.

Deputy Commissioner Danzeiser

has stated that no new elements will

be added to the draft regulations but

that some revisions and reductions of

elements could be made. But the self-

insurance industry is unable to predict

when – or even if – the rewritten

regulations would be adopted.

One important issue raised by

the industry was the question of

whether stop-loss insurance would

be regulated as health insurance or

casualty insurance. “This is the classic

debate that we seem to encounter

in every state,” SIIA board member

Ritchie commented. “The point of

confusion for regulators appears to be

that stop-loss acts like liability insurance

but operates in the health world.

This was an informal meeting to help TDI understand how stop-loss insurance works to support the self-insured plans

of Texas employers, Brackemyre noted.

TDI has stated that the draft regulations are a work-in-progress that

could be shaped in part by meeting with the self-insurance industry, employers

and other interested parties.

January 2016 | The Self-Insurer 15

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

“While regulators mistakenly approach our product in the context of health insurance, we cannot operate as health insurance,” he said. SIIA has long made the distinction that stop-loss insurance pays no claims for health care to members of plans and so cannot be categorized as health insurance. Rather, it covers liabilities that plan sponsors experience in amounts above a predetermined level. A preponderance of federal and state courts have agreed with SIIA on this point and no court has ever defined stop-loss insurance as health insurance.

“To many, it appears that much of the Texas draft regulation is a solution looking for a problem,” Ritchie said. One member of the Texas industry group asked if TDI had evidence that supports the need for new regulations and none was offered in reply. ■

SIIA will continue to participate in the development of Texas regulations. Copies of the current draft and SIIA’s written comments are available from Adam Brackemyre in SIIA’s Washington DC offi ce, (202) 463-8161 or [email protected].

16 The Self-Insurer | www.sipconline.net

Captives Facing Legislative, Regulatoryand Financial Obstacles in 2016

Written by Karrie Hyatt

2016 is looking to be an active year in the captive industry, with a continuing soft market, persistent scrutiny by the Internal Revenue Service (IRS) and the National Association of Insurance Commissioners (NAIC), captives will likely have a challenging year. In addition, there is still

a decision to be made by the Federal Housing Finance Agency (FHFA) whether

or not to exclude captives, as well as legislation that will bar the agency from

doing so. Congress has several legislative measures before them that could affect

captive formation and regulation.

In speaking with a number of captive professionals, from regulators to

attorneys to managers, the consensus is that conventional captives, pure captives

and long-standing captives, will likely be untouched by many of the issues likely to

come up in 2016. However, niche captives and small captives, will be bearing the

brunt of any inquiries or legislative changes. Small captives and group captives are

most likely to feel the effects of the soft market.

Another Year for a Soft MarketThe continuing soft market is one of the key issues captives will face in 2016.

In this soft market, well-capitalized traditional insurance companies are able to

January 2016 | The Self-Insurer 17

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

keep premiums low. When traditional insurers can offer low premiums, captive programs can lose their appeal.

According to Sandra A. Bigglestone, director of captive insurance, Vermont Department of Financial Regulation, “Captives will continue to contend with the soft market cycle and some captive programs may shrink as a result. The soft market may be a bigger problem for group captives as it may grow more difficult to keep membership engaged.”

“The continuing soft market is keeping premiums at historic low levels. Many of the admitted carriers are very well capitalized and can afford to compete on price,” said Christina Kindstedt, senior vice president, Willis Management (Vermont), Ltd. “Captives, with their capital requirements, will have a hard time competing on pricing alone with well-capitalized admitted carriers.”

While the continuing soft market is affecting all aspects of the insurance market, Robert H. Myers, Jr., partner with Morris, Manning & Martin, LLP believes that the captive industry will see growth but at a slow rate.

Kevin M. Doherty, director of the Tennessee Captive Insurance Association (TCIA) and partner with Nelson Mullins Riley & Scarborough LLP, agrees that the soft market does not warrant unnecessary concern. “No one has expected this soft market to last for so long. It doesn’t concern me that much. To me, people are forming captives for the right reasons – for the benefits of good financial management – not for the tax incentives. Captive growth is not being driven by a hard market.”

“Tennessee is about to license its 100th captive,” continued Doherty, “Which will happen before the end of [2015]. Add in the protected cells and incorporated cells and that number

is then pushing 300. All this growth in spite of the continued soft market.”

Inquiry Into Captives by Agencies and Associations

IRS In February 2015, the U.S. Internal

Revenue Service name captives to its “Dirty Dozen” list – an annual list issued by the department naming financial vehicles that are under scrutiny for illegal tax avoidance activity. The IRS singled out captives filing under the 831(b) designation, specifying that companies are using the designation to avoid taxation.

Captives will most likely once again be named to the “Dirty Dozen” list which could translate into more scrutiny of all captives. According to Bigglestone, “Increased scrutiny will be a certainty. I believe the “Dirty Dozen” list was a warning that should be heeded. Industry consultants should carefully consider the risks when generating business that is not for risk management and risk financing reasons.”

FHFA In 2014, the FHFA

proposed substantial rule changes governing membership in the Federal Home Loan Bank (FHLB) system which would effectively bar captive insurance companies from participating. The insurance industry responded to the recommended changes in force, with the agency receiving more than one thousand responses. During 2015, the FHFA did not taken any action and new captive members have been accepted into the FHLB system. However, the issue is still on the table and no decision has been made.

“Given the volume of responses to the FHFA in support of captive insurers being included,” said Bigglestone, “It’s likely that captive insurers will continue

to be allowed as members of the Federal Home Loan Banks. We support captives that want to be members of the FHLBs and hope they will continue to be allowed.”

It is not only the captive industry that is working to block the change, members of Congress have also taken an interest. In October, H.R. 3808 was introduced in Congress by Rep. Blaine Luetkemeyer (R-MO), Rep. Dennis Heck, (D-WA), Rep. Patrick McHenry (R-NC) and Rep. John Carney (D-DE). However, since its introduction there has been no actions taken in Congress.

Gary Osborne, president of USA Risk Group, Inc. said, “I think the captive industry will succeed in resisting this change... The industry support for this facility is strong and seems to meet the intent of the loan program.”

NAIC The NAIC will

likely continue to focus on captives. After nearly two years, the Financial Regulation Standards and Accreditation (F) Committee has agreed on a new Preamble Part A for the accreditation standards that will regulate a small niche of captive companies – those that reinsure life insurance products – as multi-state insurance companies.

While many captive professionals begrudgingly accept the change, Vermont’s Bigglestone sees it as an effort to increase transparency and understanding by state regulators. “As a result of initiatives already taken at the NAIC, life reinsurance captives are now subject to a set of rules to be applied consistently from state to state... . With defined standards... state regulators will achieve more uniformity, while maintaining some discretion for the assets allowed to support the excess level reserves under a state’s credit for reinsurance laws.”

18 The Self-Insurer | www.sipconline.net

Others, such as Osborne, see this as a step towards eliminating captives

from insuring these products. He said it’s likely that, “The reserving rules for life

insurance will be amended to eliminate the benefit from using captives. New York

and other states will attack this but change comes slow at the NAIC and there

are now many more captive friendly states than previously.”

“The NAIC attention to captives is unwelcome and unnecessary,” continued

Osborne. “Particularly their seeming desire to insist on “licensing” captive

managers could be problematic in reducing competition and adding cost and

administrative burden.”

At the most recent meeting of the F Committee, in November, the committee

began to consider additional changes to the Preamble Part A which would list risk

retention groups as multi-state insurance companies. This will certainly be an issue

to watch over the course of 2016.

On the recent efforts of the NAIC, Myers said, “Continuing to scrutinize the

captive industry, the NAIC will likely dig deeper into how captive regulation differs

from traditional insurance companies. They have experienced some success in

probing into the use of life, annuity and long-term care captives. This is leading the

NAIC towards seeking to regulate captives as traditional insurers in an effort to

achieve greater “harmony” in regulation.”

Election Year 2016In addition to bill H.R. 3808, there are several other pieces of legislation up

for consideration in Congress. In the spring of 2015, H.R. 1788 was introduced

into Congress to amend taxation law 831(b) to exclude many captive companies. This bill had been introduced in a previous Congress, but had languished. This bill is likely to see the same fate. However, if it does gain traction it could prove to be a very contentious bill with the captive industry.

Legislation to clarify the Nonadmitted and Reinsurance Reform Act (NRRA), passed as part of the larger financial reform bill Dodd-Frank in 2010, in regards to captives was introduced last July into the Senate. S.B. 1561 was introduced by Vermont’s Patrick Leahy and South Carolina’ Lindsey Graham. The bill, Captive Insurers Clarification Act, would amend NRRA to exclude captives under the definition of non-admitted insurer.

According to Doherty, “If NRRA is applied to captives then they will have to domicile in the state where their

January 2016 | The Self-Insurer 19

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

*#1 independent direct writer stop-loss carrier based on the 2013 year-end Sun Life Stop-Loss premium of $915.2M and our analysis of marketshare data from various third parties. Group stop-loss insurance policies are underwritten by Sun Life Assurance Company of Canada (Wellesley Hills, MA) in all states, except New York, under Policy Form Series 07-SL. In New York, group stop-loss insurance policies are underwritten by Sun Life and Health Insurance Company (U.S.) (Windsor, CT) under Policy Form Series 07-NYSL REV 7-12. Product offerings may not be available in all states and may vary depending on state laws and regulations. © 2015 Sun Life Assurance Company of Canada, Wellesley Hills, MA 02481. All rights reserved. Sun Life Financial and the globe symbol are registered trademarks of Sun Life Assurance Company of Canada.

PRODUCER USE ONLY.

BRAD-5073 SLPC 26354 01/15 (exp. 01/17)

Life’s brighter under the sun

TO A TRUE PARTNERIN STOP-LOSS.

HELP YOUR CLIENTS

The benefi ts of smart coverage, when it matters most. Sun Life is #1 in stop-loss for a reason:* our unparalleled expertise and innovative benefi ts and services help protect self-funded employers. Our new benchmarking tools arm you with customized data in an appealing, client-ready format. Coupled with our cost-containment products, you can tailor the perfect solution for each client. Put our expertise to work—call your Sun Life rep today.

sunlife.com/wakeup

20 The Self-Insurer | www.sipconline.net

Would you navigateuncharted waterswithout a compass?

As a leader in Group Captives, Berkley Accident and Health can steer you in the right direction.

With EmCapSM, our innovative Group Captive solution, we can help guide midsize employers to greater stability, transparency, and control with their employee benefits.

With Berkley Accident and Health, protecting your self-funded plan can be smooth sailing.

Stop Loss | Group Captives | Managed Care | Specialty Accident

BAH AD-2014-0141 www.BerkleyAH.com

Insurance coverages are underwritten by Berkley Life and Health Insurance Company and/or StarNet Insurance Company, both member companies of W. R. Berkley Corporation and both rated A+ (Superior) by A. M. Best. Coverage and availability may vary by state.

©2015 Berkley Accident and Health, Hamilton Square, NJ 08690. All rights reserved.

January 2016 | The Self-Insurer 21

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

Do you aspireto be a published author? Do you have any stories or opinions on the self-insurance and alternative risk transfer industry that you would like to share with your peers?

We would like to invite you to share your insight and submit an article to The Self-Insurer! SIIA’s o� cial magazine is distributed in a digital and print format to reach over 10,000 readers around the world. The Self-Insurer has been delivering information to the self-insurance/alternative risk transfer community since 1984 to self-funded employers, TPAs, MGUs, reinsurers, stop-loss carriers, PBMs and other service providers.

Articles or guideline inquiries can be submitted to Editor Gretchen Grote at [email protected]

The Self-Insurer also has advertising opportunities available. Please contact Shane Byars at [email protected] for advertising information.

headquarters are. This is not really effective as far as we are concerned. There are only a handful of good domiciles so forming captives in other states may be a disadvantage to good captive regulation.”

Doherty, as part of TCIA, has been working with Vermont Captive Insurance Association and several other captive organizations to get this amendment enacted.

Whether any legislative action on these bills comes this year is a matter of wild speculation. As Myers said, “As it’s an election year, Congress’s main job will be making sure incumbents get reelected, so legislation that could affect the insurance industry is less likely to be passed.” ■

Karrie Hyatt is a freelance writer who has been involved in the captive industry for more than ten years. More information about her work can be found at: www.karriehyatt.com.

The problem getting it through Congress will be a matter of perception, continued Doherty.

NRRA was a completely separate bill that was tacked on to Dodd Frank and is now perceived as a law that was part of the larger financial reform bill. There is a lot of politics regarding

Dodd Frank, on both sides of the aisle.

22 The Self-Insurer | www.sipconline.net

As is the case in most American neighborhoods, a new neighbor might move in every few years.

Place yourself in this familiar scenario: A new neighbor has moved in

right across the street from your home. You spy through your front window and see kids, dogs, an assortment of nice furniture exiting the moving van and most importantly a really, really nice car parked in the driveway. Now you are interested. Protocol dictates that you immediately schedule a barbeque so that you might meet your new neighbor. If the stars align, you will somehow compel a conversation about that new, beautiful car parked in the driveway across the street.

Written by Tim Callender, Esq.

Fiduciary Liability

the& Solution

GAP

January 2016 | The Self-Insurer 23

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

Luckily for you, all goes according to plan. The kids play, the spouses compare vacation stories and the dogs romp through the green grass chasing butterflies. It really is a picturesque scene. You manage to force an awkward conversational segway and suddenly find yourself learning about “the car.” The gas mileage is unheard of, the safety features are top of the line, it vacuums itself, the wiper blades never need to be changed, it can parallel park for you, the paint simply does not show dirt, ever and its purchase price is insanely cheaper than any car you have ever owned. You do not understand how this can be – you figure there must be a catch – and then your neighbor mentions “The Downside.” “Well,” he says, “you do need to know that all maintenance for this car must be done by you. There are no mechanics or shops around that work on these cars, period. If you buy one, you better make sure you know what you’re doing. It’s a lot of responsibility. I hope you’re ready for that.” Sound familiar... ?

With Self-Funding Comes Great Responsibility

The advantages to self-funding are many and tend to revolve around two primary ingredients: customization and cost-savings. Custom processes tacked on to practices such as subrogation, claim negotiation, medical tourism, unique plan design and reference based pricing can all lead to cost-savings and significant financial performance for a health plan. As is routinely the case, though, all roses do come with thorns. In this case the “rose” of customization and cost-savings comes with the “thorn” of fiduciary responsibility. This thorn can be especially shocking for the self-funding rookie who has grown used to an insulated health insurance

experience where fiduciary liability concerns for the plan-sponsor are extremely limited and oftentimes nonexistent.

Like our neighbor’s new car and its maintenance needs, self-funding comes with a unique set of responsibilities that a plan-sponsor may not be equipped to handle. The fiduciary is solely responsible for the health plan’s administration, it will be expected to exercise discretion regarding claims decisions and the fiduciary is accountable for the handling of plan assets. Not to mention that ERISA §404 mandates that all of this must be done in the sole interests of plan participants and beneficiaries, commonly known as the “duty of undivided loyalty.” §404 further obligates that this undivided loyalty must be executed with the care, skill, prudence and diligence that a person acting in a similar capacity and familiar with such matters, would employ in a similar situation. Part of the problem, of course, is that a fiduciary that is new to the self-funding game may not be familiar with what a person acting in a similar capacity would do in a similar situation. The key phrase is “familiar with such matters,” and some fiduciaries are, in fact, not familiar with such matters.

The most daunting and serious of fiduciary liabilities comes when a plan administrator is faced with analyzing a final, internal appeal of a denied medical claim. The fiduciary absolutely must understand the claim and ultimately must decide how the plan’s governing plan document should be applied to that claim appeal – and of course ERISA §404(a)(1)(D) requires a plan fiduciary to strictly follow the terms of that plan document. It is fair to say that the vast majority of self-funded plan administrators lack the qualifications necessary to understand a medical claim let alone properly apply language from a complicated plan document to that same claim. Plan sponsors (and/or administrators) make widgets – they do not adjudicate health claims, nor should they have to handle such a task. Consider a final appeal of a health claim hinging on a medical necessity determination. Is it fair, or right, or even ethical to expect the widget maker to exercise fiduciary discretion based on medical expertise? Consider the final appeal of a health claim that hinges on the interpretation of a plan document’s uniquely worded and complicated “Illegal Acts Exclusion.” Is it reasonable to expect the plan administrator to play the role of lawyerly wordsmith while dealing with the stress of a contentious final claim appeal? Obviously not.

In addition, the unqualified plan administrator must not only juggle its duty to handle the responsibilities enumerated above, it must also sweat and worry about numerous penalties and consequences that may be realized, should the plan administrator fail to comply with any one of its vast array of fiduciary responsibilities.

The Thorny RealitiesERISA §409 tells us that a plan fiduciary is liable for losses caused to the

plan. Further, it mandates that a plan fiduciary can be held liable for equitable or remedial relief, as a court may find appropriate, should a breach of fiduciary duty occur, such as the wrong decision on the final appeal of a medical claim.

ERISA §502(a)(3) authorizes equitable relief for a breach of fiduciary duty. The United States Supreme Court has held that plan participants and beneficiaries are able to seek individual equitable relief under this section of the law.1 Recently, the Supreme Court has expanded the meaning of “equitable relief.”2 This recent holding broadened ERISA §502(a)(3) by specifically identifying possible, equitable remedies that could be levied against a fiduciary, including, reformation of the

FUDUCIARY LIABILITY | FEATURE

24 The Self-Insurer | www.sipconline.net

plan’s terms, estoppel and surcharge. Although traditional equitable remedies might not include “money damages,” this holding seems to suggest that the surcharge remedy would absolutely allow for a monetary payment, akin to money damages. This very well could lead to monetary payments by plan fiduciaries, for varieties of alleged fiduciary breach.

Further, ERISA allows for an award of attorney fees, to the prevailing party, in actions that involve the very scenarios we have discussed herein: a plan fiduciary denies a medical claim at the final level of appeal, yet the claim proves payable upon legal review and now interest and the participant’s attorney’s fees must be paid. As we all know, attorneys ain’t cheap.

In addition to the above, plan fiduciaries involved in a fiduciary breach are likely to face a U.S. Department of Labor penalty, pursuant to ERISA

§502(l). By law, this civil penalty is set

at 20% of the applicable recovery

amount. ERISA 502(l) tells us that

“applicable recovery amount” means

“any amount which is recovered from a

fiduciary or other person with respect

to a breach or violation... pursuant to

any settlement agreement with the

Secretary, or ordered by a court to

be paid by such fiduciary or other

person to a plan or its participants and

beneficiaries in a judicial proceeding

instituted by the Secretary... .”

Most frightening in all of this is

the fact that a plan fiduciary may end

up being an individual, thus triggering

personal liability for fiduciary breaches,

pursuant to ERISA. Oftentimes

family-owned companies, closely-

held enterprises, or even large,

privately-held organizations will either

intentionally or inadvertently name

an owner, or a handful of high-level

individuals, as plan fiduciaries.

The risks to a plan fiduciary are numerous and the potential financial fallout is high. Here, then, is where our industry is faced with a unique and significant service gap regarding the transfer of fiduciary liability to a qualified entity. Multiply instances of this service gap by the growth of our industry and you can see the growing need that must be met.

The Fiduciary Service Gap and Industry Growth

Using a typical Request for Production as the benchmark indicator for rookie, self-funder concerns, it becomes readily apparent that every plan administrator (likely on the advice of its broker) is gravely concerned about fiduciary liability. In a survey orchestrated by The Phia Group, we learned that 88% of broker RFPs submitted to third-party administrators include a question

A R C H I T E C T SO F T H E F U T U R E

HCAA’s Executive Forum 2016

Look for more information: www.hcaa.org

FEBRUARY 9-11, 2016Caesars Palace 3570 Las Vegas Blvd., Las Vegas, NV 89109

WEDNESDAY OPENING KEYNOTE SPEAKER:SENATOR TOM DASCHLE

“An Insider’s View on President Obama’s Public Policy and Its Implications for the Election of 2016”

Senator Tom Daschle

FUDUCIARY LIABILITY | FEATURE

January 2016 | The Self-Insurer 25

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

CELEBRATING OF COST REDUCTION2020Y E A R S

1 9 9 5 - 2 0 1 5

2020

H.H.C. Group is a full-service health insurance consulting organization that alleviates the effects of rising healthcare costs for insurance payors by providing appropriate and

reasonable prices through innovative services and customized solutions.

YOUR ANSWER TO

HEALTHCARE SAVINGS

Visit www.hhcgroup.com for more information.

H.H.C. GROUP, PROUDLY CELEBRATING OUR 20TH YEAR DELIVERING COST CONTAINMENT SERVICES

438 North Frederick Avenue, Suite 200A

Gaithersburg, MD 20877

301.963.0762

CLAIMS EDITING

Reduce unnecessary

costs associated with

claims errors

COST CONTAINMENT

DONE RIGHT

CLAIMS NEGOTIATION & REPRICING

Secure reasonable, fair and

appropriate in and out-of-

network medical pricingnetwork medical pricing

CLAIMS AUDITING

Ensure your clients only

pay for the services

they receive

REFERENCE BASED PRICING

Receive services that can

deliver additional savings

over and above the

PPO discounts

26 The Self-Insurer | www.sipconline.net

2016Schedule of Events

April

march

may

Self-Insured Taft-Hartley Plan Executive ForumMay 18-19, 2016 | Chicago, IL

Taft-Hartley plans refer to the multi-employer pension plans collectively bargained by a union and a group of employers, usually in related industries. Taft-Hartley plans are governed by a trust, half of whose trustees are appointed by the employers and half by the union. This retirement plan model has enabled tens of thousands of small and medium-sized businesses to provide workers with the traditional defi ned benefi t pensions that used to be standard among larger employers, but have now vir tually disappeared in the non-unionized private sector.

Self-Insured Workers’ Compensation Executive ForumMay 24-26, 2016 | Scottsdale, AZ

SIIA’s Annual Self-Insured Workers’ Compensation Executive Forum is the country’s premier association sponsored conference dedicated to self-insured Workers’ Compensation employers and group funds. In addition to a strong educational program focusing on such topics as analytics, excess insurance, wellness initiatives and risk management strategies, this event will offer tremendous networking opportunities that are specifi cally designed to help you strengthen your business relationships within the self-insured/alternative risk transfer industry.

International Conference April 5-7, 2016 | San Jose, Costa Rica

SIIA’s International Conference provides a unique opportunity for attendees to learn how companies are utilizing self-insurance/alternative risk transfer strategies on a global basis. The conference will also highlight self-insurance/ART business opportunities in key international markets. Participation is expected from countries all over the world.

Self-Insured Health Plan Executive ForumMarch 21-23, 2016 | New Orleans, LA

The educational focus for this event will be to address the interests of plan sponsors, in addition to third party administrators and stop-loss entities. This forum delivers high quality educational content of interest to executives involved with the establishment, management and/or support of self-insured group health plans. In addition to the educational program, the event will feature multiple unique opportunities.

36th Annual National Educational Conference & Expo September 25-27, 2016 | Austin, TX

SIIA’s National Educational Conference & Expo is the world’s largest event dedicated exclusively to the self-insurance/alternative risk transfer industry. Registrants will enjoy a cutting-edge educational program combined with unique networking opportunities, and a world-class tradeshow of industry product and service providers guaranteed to provide exceptional value in three fastpaced, activity-packed days.

For more information visit › www.siia.org

sept

January 2016 | The Self-Insurer 27

© S

elf-

Insu

rers

’ Pub

lishi

ng C

orp.

All

righ

ts r

eser

ved.

focused on shifting fiduciary liability, whether in general, or for specific, final appeal functions. Like the Roadrunner fleeing from Wylie Coyote, the average TPA will run from this liability shift as quickly as its TPA legs will allow often losing business in the process. But, can any liability-conscious business person fault a TPA for answering “no” to this new and frightening RFP question? Absolutely not – the TPA’s hesitance is valid and understood.

As if it was not difficult enough for TPAs to field this fiduciary transfer question on 88% of the RFPs coming through the door, the rapid growth of self-funding is now necessitating even more RFPs, thus dramatically increasing the demand for this transfer of fiduciary liability. From the end of 2013 through the first six months of 2014, the number of lives covered by a self-funded health plan grew by approximately 4 million while the fully-insured platform saw a decline of approximately 5 million lives. It goes without saying that new self-insured lives equal new health plans which equal new plan-sponsors submitting RFPs, which RFPs, very likely, ask, “will you, pretty, pretty please, assume fiduciary liability for my health plan?” As noted above, this question will routinely be answered in the negative. A gap exists.

When a consumer becomes aware of a gap in service, the consumer will routinely shy away from those service providers unable to cure the gap. This results in lost business and another study performed by The Phia Group reveals that lost business is not good. In other fields, examples of a service gap leading to lost business can tend to seem ridiculous with so many solutions readily apparent to all involved. If a house painter refuses to include clean up in his painting services, the savvy home owner will choose a different house painter. A landscaper is not willing to include lawn fertilizing in her service offering – so the reasonably selective consumer will go with a different landscaping contractor. An auto mechanic does not offer a courtesy shuttle to drive his customers to/from his garage while he works on their cars – and the average consumer will look elsewhere for better service.

No business owner should allow business to walk away when the reason behind the customer’s departure is so easily fixed.

Fiduciary Service Gap Solutions and the Move ForwardThe plan administrator has a handful of options when considering the fiduciary

service gap.

Perhaps they flee. Some plan administrators are so frightened by the lack of fiduciary assistance that they simply pack up and return to the fully-insured world. In essence, these plan administrators – if also the plan-sponsors – choose to give up the rose to avoid the thorns.

Perhaps they go in-house. Should widget makers look to hire medical experts and legal wordsmiths, in-house, specifically to handle those complicated, final, internal appeals? This would most certainly assure that the widget-making plan administrator could meet its fiduciary responsibility when making complex appeals decisions. As nice as this might sound, it is completely unrealistic and an unfair expectation.

Perhaps they move forward, naked into the wilderness. Should plan administrators simply accept a “no” answer to the fiduciary RFP question and do nothing to prepare for their fiduciary demands? While clearly ill-advised, it seems that this tends to be happening more and more. Unfortunately, this option tends to result in a plan administrator being forced into the unappetizing position of

a final appeal reviewer, bringing the entire “C-suite” and a handful of attorneys into the room to sit and make a medical, or legal determination, on a complex final appeal. Not surprisingly, a few of these experiences over a plan year and you tend to see the typical plan administrator and/or plan-sponsor pack up and walk away from the self-funded platform.