semester end project 2011- satakshi arora

TRANSCRIPT

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 1/40

ACKNOWLEDGEMENT

I would like to convey my extreme gratitude towards all the people who supported

and guided me during the project. Especially, I’m grateful to Mr. Ramesh

Tahiliani, Mr. Alok Wadhwa, Mrs Sunita, Mrs Usha & immensely Mrs Nandita

Abraham for providing the initial guidance for the project, for routing my interests

in the research and, for believing in me and giving me the confidence that I can

succeed despite of the difficulties I faced the time I was working on this project.

In spite of my best effort, there may be some possibilities of errors in my

project. I shall acknowledge with gratitude any error if pointed out in the

project. Any suggestions for improvement in this project will be welcomed.

Satakshi Arora

MA-FMG – Semester 1

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 2/40

TABLE OF CONTENTS

1. Introduction

1.1 Organization and Product

1.2 History

2. Strategic Plan and Focus

2.1 Mission Statement

2.2 Goals and Objectives

2.3 Core Competencies

3. Situational Analysis

3.1 SWOT Analysis

3.2 Industry Analysis

3.3 Competitor Analysis

3.4 Customer Analysis

3.5 Environment Analysis

4. Market-Product Focus

4.1 Marketing and Product Objectives

4.2 Target Market

4.3 Brand Identity and Consumer Insights

4.4 Positioning and Perceptual Mapping

5. Marketing Program Strategy and Tactics

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 3/40

5.1 Product Line

5.2 Promotion

5.3 Place

5.4 Pricing

6. Financial Data and Projections

6.1 Overview

6.2 Operating Expense

6.3 Gross Profit Per unit Sold

7. Implementation Plan

7.1 Gantt Chart

8. Evaluation and Control

8.1 Quality Control

8.2 Risk Analysis

References

Appendices

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 4/40

Executive Summary

The purpose of this study was to probe and observe into the unorganized retailmarket sector in India, focusing on small-medium scale enterprises dealing in

Bridal Couture, and designing a strategy to expand them and furthermore heading

them towards more organized scenario. This was done by observing the internal

organizational structure of a company known as Khera Saree Sansar, taken as an

example in Delhi and studying the factors like showroom location, merchandise,

visual merchandise, supply chain management etc. and recommending a marketing

strategy for them. Then a consumer behavior survey was done in the locations that

are usually most shopped at for wedding trousseau i.e. rajouri garden, karol bagh,

south extension I, to identify the drivers that affect the buying behavior of a

wedding customer. Based on Primary Data, Market Study and Past Researches on

Indian Wedding industry, a Brand identity is created and promotional statrgies are

given. Also, as per the company’s interest to open a new showroom in a different

location in Delhi, a study of possibilities and locations is also done.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 5/40

CHAPTER – 1: INTRODUCTION

1.1 ORGANIZATION AND PRODUCT

Khera Saree Sansar is a 52 year old small-medium scale enterprise (SME)

established by Mr. Baldev Raj Arora in 1959 in the city of Agra and further

developed by his sons Mr. Deepak Khera and Mr. Sudhir Khera in Delhi. The

enterprise deals in different types of bridal wear like sarees, lehengas and suits. The

designs are executed and produced in-house. They have three showrooms in

Chandni Chowk (Delhi).

This family shares a common passion for fabrics, embroideries and bridal wear, buthave a very different qualification background. Mr. Baldev Raj came to India in

1948 while the division of India and Pakistan. He was 14 when he stated the

business of bridal wear in partnership with his uncle and studied side by side. He’s

a graduate in bachelors of arts.

Mr. Deepak Khera has done a Masters in commerce and has an extensive

knowledge and experience of 40 years about business management.

Mr. Sudhir Khera is a graduate in commerce and has a high level of interest and passion in fashion designing and has an experience of over 30 years.

Khera sarees deals in retail as well as wholesale of bridal wear. They use more of

traditional and ethnic work and embroideries for the merchandise like zardozi,

dabka, zari, crystal, silk bandhej and pitta etc. The fabric used is basically pure and

semi pure like georgette, silk, crepe, chiffon, semi georgette, semi crepe etc. Its

price range is from Rs.1000 – Rs. 200,000. The fabric used is sourced grey and is

dyed according to the trends and designs.

There is a very traditional way of organizing and arranging the merchandise in the

showrooms. The display is weak due to space limitation and weak location. The

merchandise is just classified by the price range in the inventory and the display.

The workforce is of 32 people including salesperson, embroiderers, helpers and

accountant.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 6/40

Job description of members :

Members Job Description

Baldev Raj Arora Management and HR

Deepak Khera Inventory and ProductionSudhir Khera Designing and Marketing

Khera Sarees has 3 Showrooms:

Showroom Address Description

Showroom 1 : 571-572,

1st Floor, Katra Ashrafi,

Chandni Chowk,

Delhi-6

• Area : 80 sq. yards

•

Sections : 2• Office

• Showroom

• Merchandise : High Fashion customized wear

• Target Customer : Loyal and repetitive

Showroom 2 : 552-553,

Katra Ashrafi,

Chandni Chowk,

Delhi-6

• Area : 60 sq. yards (3 floors)

• Sections : 4

• Showroom

•

Office• Embroidery Workstation

( Adda)

• Merchandise : Wide price range and variety

(preferably less expensive)

• Target Customer : First Time and Regular

Showroom 3 : 421-422,

Ground Floor, Katra

Ashrafi,

Chandni Chowk,

Delhi-6

• Area : 60 sq. yards

• Sections : 1

• Showroom

•

Merchandise : High Fashion• Target Customer : First Time and High

Budget

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 7/40

The Overview

The Showroom

The Merchandise

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 8/40

1.2 HISTORY

Khera Saree Sansar was rooted and established in Agra as a family owned business

in 1959. Mr. Baldev raj started it as a proprietor and earned a goodwill in the city.

He built the foundation that grew to 3 showrooms in Agra. By the Beginning of 1999, he and his sons decided to expand the enterprise in Delhi.

The first showroom was inaugurated in April 1999 at Chandni Chowk (Delhi). The

second showroom was opened 5 years later, after the establishment and success of

the fist showroom at the same place. By the end of 2005, Agra showrooms were

shut down because of the losses and mismanagement and the business was

completely moved to Delhi. In 2009, the third showroom was opened comprising

of high fashion merchandise.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 9/40

CHAPTER – 2: STRATEGIC PLAN AND

FOCUS

2.1 MISSION

Lucrativeness, business growth and financial security of the enterprise with a

strong essence of customer satisfaction and loyalty.

2.2 GOALS AND OBJECTIVES

Khera Saree Sansar is recently planning to open two new showrooms but are

uncertain of the area and places to choose which can turn out to be maximum

profitable according to their budgets. Therefore, following are the primary goals

that the enterprise is looking forward to:

• To study the major markets comprising of bridal wear showrooms in Delhi

• To analyze the cost and potential of profitability to the chosen location to

open the showroom

2.3 CORE COMPETENCIES

• Innovative Self designed and wide range of Merchandise

• Traditional work and embroideries from all over India

• Use of pure and authentic raw materials like fabrics (Eg. silk) and crystal

elements (Eg. Swarovski)

• After sales service for expensive merchandise (Eg. Stone and crystal

polishing)

• Good public relations

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 10/40

• Strong management with more than 50 years of experience

CHAPTER – 3 : SITUATIONAL ANALISIS

3.1 SWOT ANALYSIS

• STRENGTHS

- Because of the enterprise being 60 yrs old, the amount of experience

is really high.

- Innovative in-house designed merchandise makes the collections

trendy and different.

- The Enterprise has a very Skilled workforce with artisans from

different parts of India.

- Deals in B2B as well as B2C.

• WEAKNESSES

- Due to the conventional background of the enterprise, it is not open toinvest in promotional marketing strategies.

- The merchandise is delicate and weary and there is lack of proper

attention to inventory management.

- Limited capital for promotion.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 11/40

• OPPORTUNITIES

- There is a high increase in demand of Designer Bridal wear i.e.

increasing by 20-25% every year.

- A high scope in international market as NRIs demand increases for

Indian wedding apparel.

• THREATS

- Competitors like Chhabra 555, Frontier and CTC Emporio started

their business at the same time as Khera Saree Sansar but have already

established themselves in organized retail sector.

- Lack of awareness amongst Delhi customer.

3.2 INDUSTRY ANALYSIS

Indian Culture has been endowed by people with self-indulgent lifestyle since ages.A Wedding in India is marked with a grand celebration. With the innumeroustraditional ceremonies embellished with lavishness. The onset of the wedding

season in India, signals the season of splurging. The Bridal couture industry is veryhuge, especially in the capital region. People from northern India prefer to shopfrom Delhi for the wedding merchandise. Wedding apparel costs are predicted to

be up by 20-25 percent every year. As per the estimates, over 2,000 plannedweddings take place everyday across India.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 12/40

Retailing in India is predominantly unorganized. According to a survey by ATKearney, an overwhelming proportion of the Rs. 400,000 crore retail market isUNORGANISED. In fact, only a Rs. 20,000 crore segment of the market isorganized. We are known as a nation of shopkeepers with over 12 million,thehighest outlet density in the world in the world with an estimated turnover of $ 200

billion. However a disturbing point here is that as much as 96 per cent of them aresmaller than 500 square feet in area. This means that India per capita retailingspace is about 2 square feet (compared to 16 square feet in the United States).India's per capita retailing space is thus the lowest in the world. Another point tonote is that only 8 % of our population is engaged in Retail whereas the globalaverage is around 10-12%.Traditional retailing has established in India for somecenturies. It is a low cost structure, mostly owner-operated, has negligible realestate and labour costs and little or no taxes to pay. Consumer familiarity that runsfrom generation to generation is one big advantage for the traditional retailing

sector. The major advantage for the smaller players is the size, complexity anddiversity of our Indian Markets.

Although organized retail has taken hold in India -- with large, "modern trade"stores offering a more sophisticated shopping experience, better selection,competitive prices, and formalized return and exchange policies -- the unorganizedsector isn't going away any time soon. At present, unorganized outlets represent97% of Indian retail, and according to a 2008 report by the Indian Council for Research on International Economic Relations, the sector is expected to grow at anannual rate of 20-25%, reachingUS$496 billion in 2011.

Ethnic wear is ruling the charts in bridal wear as the festive season draws upon inIndia. The market is abuzz with the latest designs, styles and trends to woo thefashion-conscious Indian female. Shopping sees an upward trend in the festiveseason and apparel manufacturers are very much geared to welcome the femaleshopper.

Women’s ethnic wear is generally restricted to the wardrobes, showing its presenceonly on certain occasions like festivals and marriages. Women’s ethnic wear has astrong presence in the market and is drifting from an unorganized retail to anorganized one. But still the majority in ethnic wear category is still largelyunorganized. Women’s wear owns a huge share of 57% in the apparel retail out of which ethnic wear has a meager share of approximately 7%-9%, of which, largelyit is the unorganized sector that has the grip on the market. The unorganized

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 13/40

segment comprises tailors and embroiderers who have inherited the art of stitchingimmaculate sherwanis and achkans and embroideries like zari, zardozi, chikan,

pitta and dabka etc from their forefathers and are located in the ancient markets of Chandni Chowk of Delhi and Bada Bazar of Kolkata. However, with the changingtastes of the Indian female, women’s ethnic wear is witnessing a comeback. Now,the working professional who likes to dress immaculately while at work, needs to

be dressed to kill even at family functions and traditional celebrations. Apparelmanufacturers have of course noted the change in trend and are working towardscarving a niche for their respective brand.

The festival and wedding dates are marked well in advance in the calendars of alldesigners, manufacturers and retailers catering to this segment. The festive andwedding season in India is the time when the demand for ethnic wear for men is atits highest. 90% of Indian men opt for ethnic wear during involved. Pure silk

ensembles are expensive but a similar effect can be created in the polyester and poly blend fabrics too to make it price effective and suit all pockets. Traditionally,the embroideries were done by skilled artisans specializing in the art but to make itmore cost effective and turn around the product in quicker lead times theembellishment is now also done on the machines.

The women’s ethnic wear styles and silhouettes are predominantly a derivation andevolution of Mughal styles from Lucknow, Agra and Delhi. While Lehengas andSarees is an all-time favourite for all, various other options on offer are Sherwani,achkans, jodhpuris, dhoti kurta, other ethnic wear.

Price is no constraint. The more you pay the better you get. The entry-price pointfor a wedding ensemble is Rs 10000 – Rs 15000 to more than a lakh depending onthe requirements of the customer and the kind of detailing starts a year precedingthe launch of the season. The demand is on the up during the festive and weddingmonths of September to May. Thus, the product development activities need tocomplete at the latest by August every year.

For those crème de la crème clients, who are ready to shell out big money for both

style and service, high-end brands offer custom-made ethnic wear. This service isquite popular for bridegroom wedding shopping. A wide range of fabrics, trims,embellishment concepts, style ideas, silhouettes and fits are presented and a clientcan pick and drop as per his choice to arrive at the final style during the interactivesession with the designers and technicians. This kind of service is offered by alllegendary manufacturers like CTC Emporio, Chhabra 555, Frontier and MeenaBazaar and ace fashion designers like Tarun Tahiliani, Shantanu and Nikhil,

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 14/40

Suneet Varma etc.

3.3 COMPETITOR ANALYSIS

There are many traditional bridal wear businessmen who started their business withthe hub of the wedding market in Delhi i.e. Chandni Chowk and has expanded in a

rapid growth in recent past by engrossing their generations to the business and

educating their successive generations about more organized way of managing and

marketing the business. In fact, the head office and main showroom of some major

players like CTC Emporio, Chhabra 555 and Meena Bazaar is still situated in

Chandni Chowk itself.

COMPETITOR PROFILE

Chhabra 555 & CTC Emporio

• 50 year old family based business

• Turned to Organized retail by the time

• Adopted promotional and marketing strategies to establish and expand the

brand

• First to adopt franchising in the Bridal couture

• Entered B2B and Exports

Other key Competitors are Frontier, Meena Bazaar, Gyans, Charming etc.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 15/40

COMPANY MERCHANDISE STORES PRICE RANGE

Chhabra 555 Lehenga, Saree,Suits (Stitched &

Unstiched),

Blouses, EveningGowns, Sherwanis,Sharara

12 ~Rs.1000-6 lac

CTC Emporio 9 Rs.2000-10lac

Frontier Hand embroideredLehengas, Sarees,

Punjabi Suits,Ethnic wear and

Artificial Jewellery

3 (India)2(US and UK)

Rs. 2000-20 lac

Meena Bazaar Bridal wear, Indo-Western wear and

Shawls

13 Rs.1000-10lac

Gyans Lehenga, Saree,Suits, Evening

Gowns

2 Rs. 1500-5 lac

3.4 CUSTOMER ANALYSIS

the consumers have started spending more and more of their increasing disposableincomes. In the last few years’ Indian retail especially in the organized segment hasgone from strength to strength. Organized retailing has increased its share in theIndian retail market (estimated to be around $270 billion) from the three percent in2004 to 4.6 percent and is currently valued at $12.4 billion. According to the IndiaRetail Report 2007, at 2003-04 constant prices, the size of the organized retailmarket (projected to grow by over 45 percent per annum over the next three years)is expected to be in excess of $45 billion by the year 2010. This will make itscontribution to total retail sales about 15 percent.

Some of the key factors that are providing this thrust are as follows:

Booming service sector – bringing in a new consumer class with agreater exposure to overseas markets Rise in the disposable incomes of this class of consumers along withtheir aspirations

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 16/40

Over the last year salaries have increased by approximately 15-20 percent The growth of the Indian middle class from its current share of 22

percent to 32 percent of the total population by 2010

The minimum budget spend on a wedding varies from Rs 10 lakh ( Rs 1 million)

for medium size weddings to the upper middle class segment which go beyond Rs

50 lakh ( Rs 5 million). The change is visible in the middle class, who want the

flavour and ambience of elite weddings. Seeing the world around, they too are

spending and want the best available. It is a sort of chain reaction which percolates

down. With income levels going up, the middle class too wants to try and match

the royal weddings in everything, be it decor, ambience or cuisine is concerned, but

the apparel industry tops it too. With bollywood and fashion designers playing on

the wedding couture, the majority of Indian customer is heading towards being astrendy. With attraction created by Movies, Wedding exhibitions and Television

shows, people now are well informed of the trends in the wedding apparel.

Weddings were expensive enough for Indians before, but this is truly a hard burden

to expect a middle-class Indian to bear.

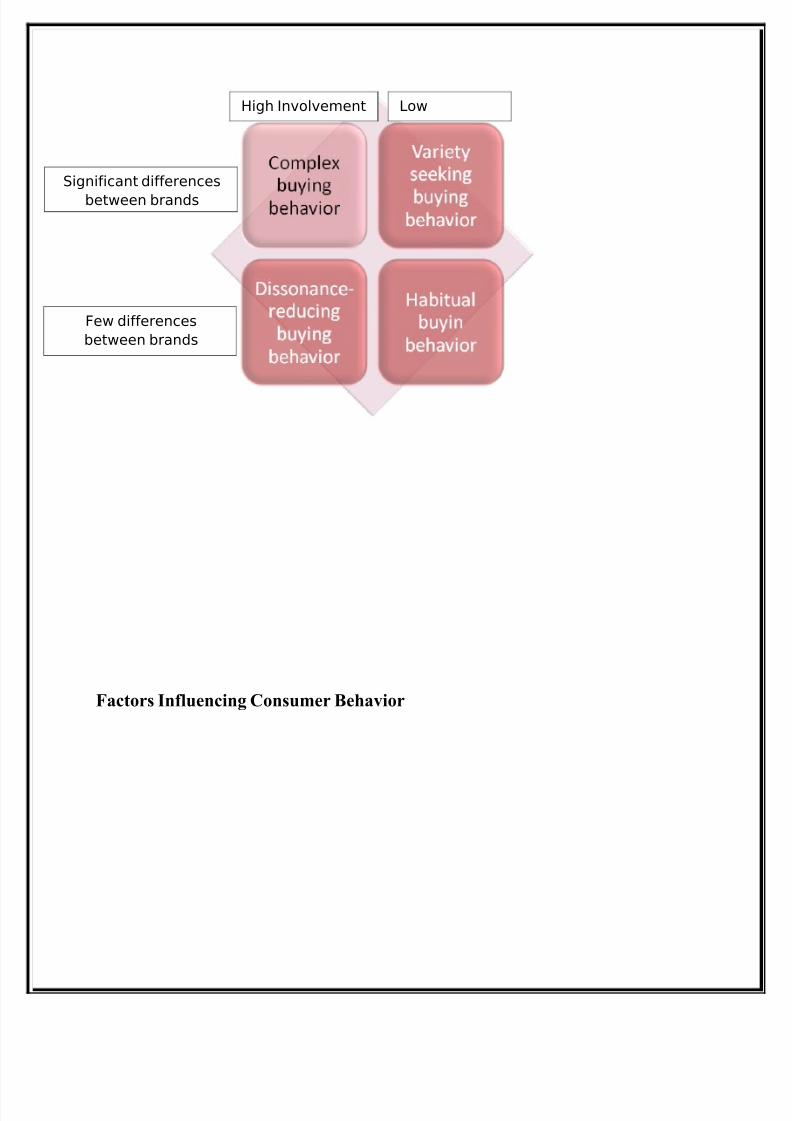

Types of Buying Behavior (Highlighted for Weddings)

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 17/40

Factors Influencing Consumer Behavior

LowHigh Involvement

Few differences

between brands

Significant differences

between brands

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 18/40

Majorly two types of customer are targeted:

Absolute is the customer who is inherently rich and belongs to elite class. For these

kind of customer, price is not a criteria, instead they look for experimentation with

innovation and new and unique designs.

Many brands especially

wedding apparel brands now

target specific subcultures

with marketing plan tailored

to their specific needs and

Buying

decisions areaffected by an

incredibly

complex

combination of

ABSOLUT

E

ASPIRATIO

NAL

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 19/40

Aspirational is the customer who has a new money and has grown rich recently.

These type of customers wants to flaunt the bling and display of being trendy and

rich. Eg. Young corporate professionals.

Primary Research and Data Analysis ( Appendix- A)

The research was done on the sample size of 200 and following are the findings:

• The brides-to-be plan and spend more than 2 months in bridal wear

shopping.

• Budget is high (~5-10 lac) and flexible.

• While selecting a store to shop for wedding trousseau, trends, designs variety

and price are the major criterias.

• Brand name doesn’t matter much if the designs are good.

• While shopping people don’t like to browse too many showrooms, as there is

a huge amount of time spent at one stop.

• The factors influencing the shopping behavior of a bride is more social but

doesn’t like someone else shopping for them.

•

The major source of medium for people to go to a showroom is by word of mouth (63%). This is the most reliable as per the explanation they give. The

second is Newspaper and magazines(22%).

• When asked if showroom location matters, majority of respondents said

“yes” (87%), specifically South Delhi (48%), Chandni Chowk(42%) and

Rajouri Garden(10%).

3.5 ENVIRONMENT ANALYSIS

India’s burgeoning middle class - now 300 million strong - are turning weddings

into showcases of their growing disposable incomes and newfound appetites for the

goodies of the global marketplace. The largesse has spawned an $11 billion

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 20/40

wedding industry, growing at 25 percent annually and beginning to rival the US

industry valued at $50 billion. The minimum budget for a wedding ceremony is

$34,000, say wedding planners, while the upper-middle and rich classes are known

to spend upward of $2 million. (The average American wedding costs $26,327.)

This doesn’t include cash and valuables given as part of a dowry.

If considered the fact that India’s middle class are those considered to be earning

“$4,545 to $23,000 a year”, weddings are priced comparably to an Ivy League

education in the US. To “help out” banks are offering specialized wedding loans (at

high rates). GE Money India has introduced an “auspicious” personal loan, a quick

and easy loan exclusively for weddings.

It might be a 'seasonal' industry, thriving only during the auspicious months of the

year but with an estimated worth of Rs 1,25,000 crore (Rs 1,250 billion) the Indian

wedding industry is getting bigger and fatter.

The Factors Leading to the Current Buying Behavior:

• High disposable incomes

• Large number of women are working

• High exposure to Trends and Fashion through movies and television

• Wedding seemed as a status symbol

• Modern Lifestyle and Preferences

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 21/40

CHAPTER – 4 : MARKET- PRODUCT FOCUS

4.1 MARKET AND PRODUCT OBJECTIVES

• To open the new showroom at the most profitable location for Bridal wear.

• To suggest a promotion plan.

4.2 TARGET MARKET

The market location for bridal wear showroom has to be in the center and prime

locations of city where there is the maximum footfall and shoppers for the same.

There are four major present locations in Delhi for bridal wear market – South

Delhi (South Ex & G.K), Chandni Chowk and Rajouri Garden. The Enterprise is

already established in Chandni Chowk, so the other two options are the ones to

choose from. With the budget given of Rs.5crores as total and the fact of entering a

new location market, we will take both the locations into the consideration andcompare them.

MARKET LOCATION AND CUSTOMERS

• South Delhi (South Ex. & G.K) –

Area Cost (per sq ft): Rs. 6000-8000/6750-9000

Minimum Area Reqd: 540 Sq ft

Rental Cost: ~Rs. 130,000

Customer Base:

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 22/40

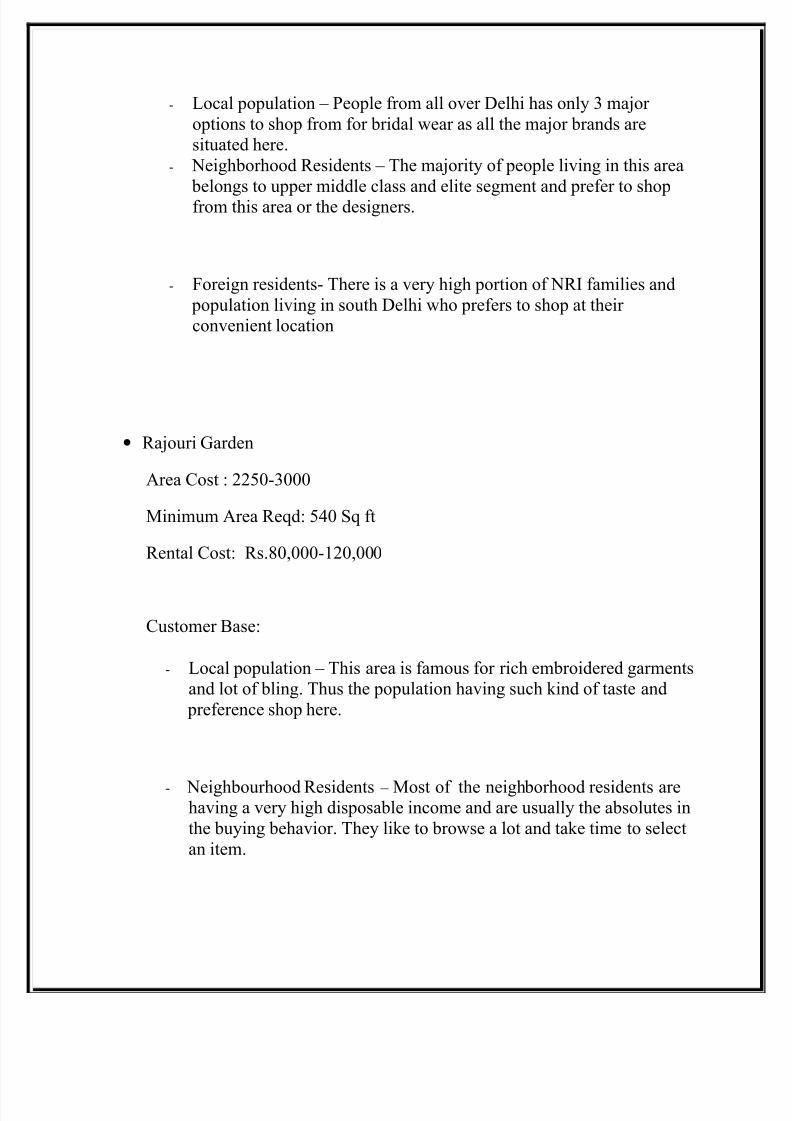

- Local population – People from all over Delhi has only 3 major options to shop from for bridal wear as all the major brands aresituated here.

- Neighborhood Residents – The majority of people living in this area belongs to upper middle class and elite segment and prefer to shopfrom this area or the designers.

- Foreign residents- There is a very high portion of NRI families and population living in south Delhi who prefers to shop at their convenient location

• Rajouri Garden

Area Cost : 2250-3000

Minimum Area Reqd: 540 Sq ft

Rental Cost: Rs.80,000-120,000

Customer Base:

- Local population – This area is famous for rich embroidered garmentsand lot of bling. Thus the population having such kind of taste and

preference shop here.

- Neighbourhood Residents – Most of the neighborhood residents arehaving a very high disposable income and are usually the absolutes inthe buying behavior. They like to browse a lot and take time to selectan item.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 23/40

SEGMENTATION

INCOME

Bridal wear of this enterprise targets the Upper class, upper middle class and

working professionals and youth. The reason being the kind of merchandise i.e.

very authentic and detailed workmanship, usage of pure and expensive materials

like silk fabrics and svarovski elements, and are self designed. Customers having

income above Rs. 8-10 lac per annum are expected to go to Kheras Saree Sansar.

DEMOGRAPHIC SEGMENTATION

AGE: 20-28 year of aged people are expected to shop.

PSYCHOGRAPHIC SEGMENTATION

The people who are aspirant and are willing to spend a good amount of money onthe wedding trousseau with customization and rich elements will be targeted.

4.3 POSITIONING AND PERCEPTUAL MAPPING

POSITIONING

Khera Sarees wants to position itself as a brand for the niche and wants to target

the upper class, upper middleclass families, working professionals and the youth.

BRAND IDENTITY PRISM

K H E R A

S A R E

E

S A N S

A R

PICTURE OF SENDER

PERSONALITY

TRADITION, CLASSIC,

INDIAN, ETHNIC, RICH,

CULTURE

“ENHANCE THE

BRIDE WITH

TRADITIONAL ROOTS

AND MODERN ART”

RELATIONSHIP

TO BE AN

EXCLUSIVE

MIRROR OF

EACH OTHER’S

PHYSIQUE

RICH

TRADITIONAL

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 24/40

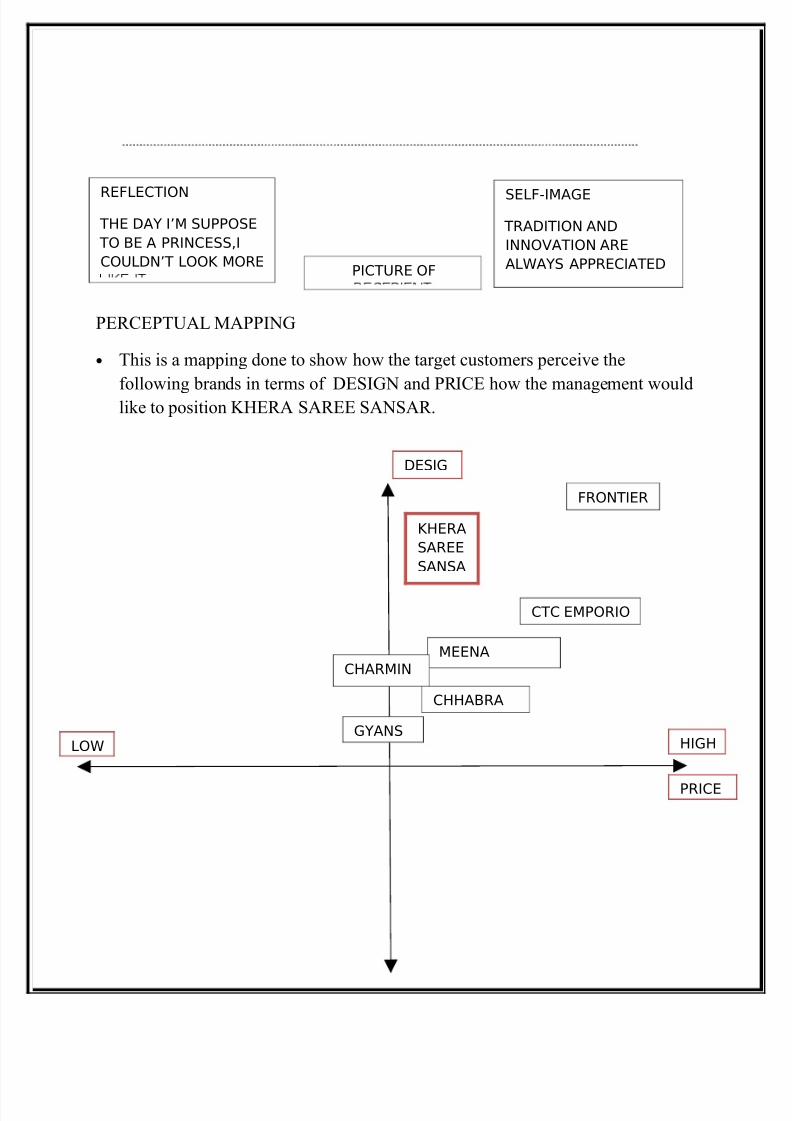

PERCEPTUAL MAPPING

• This is a mapping done to show how the target customers perceive the

following brands in terms of DESIGN and PRICE how the management wouldlike to position KHERA SAREE SANSAR.

PICTURE OF

SELF-IMAGE

TRADITION AND

INNOVATION ARE

ALWAYS APPRECIATED

REFLECTION

THE DAY I’M SUPPOSE

TO BE A PRINCESS,I

COULDN’T LOOK MORE

DESIG

PRICE

LOW HIGH

CTC EMPORIO

FRONTIER

CHHABRA

MEENA

GYANS

KHERA

SAREE

SANSA

CHARMIN

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 25/40

CHAPTER – 5 : MARKETING PROGRAM

AND STRATEGY

5.1 PRODUCT LINE

Self designed, ethnic and traditional bridal wear such as Lehengas, Sarees and Suits

with work and embroideries as zardozi, zari, dabka, pitta, crystal (using svarovski

elements)

BRANDING

The rich traditional work in modern ethnic designs.

The Logo in Edwardian Script ITC

Khera’s Saree SansarBrand Personality : TRADITION, CLASSIC, INDIAN, ETHNIC, RICH, CHIC

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 26/40

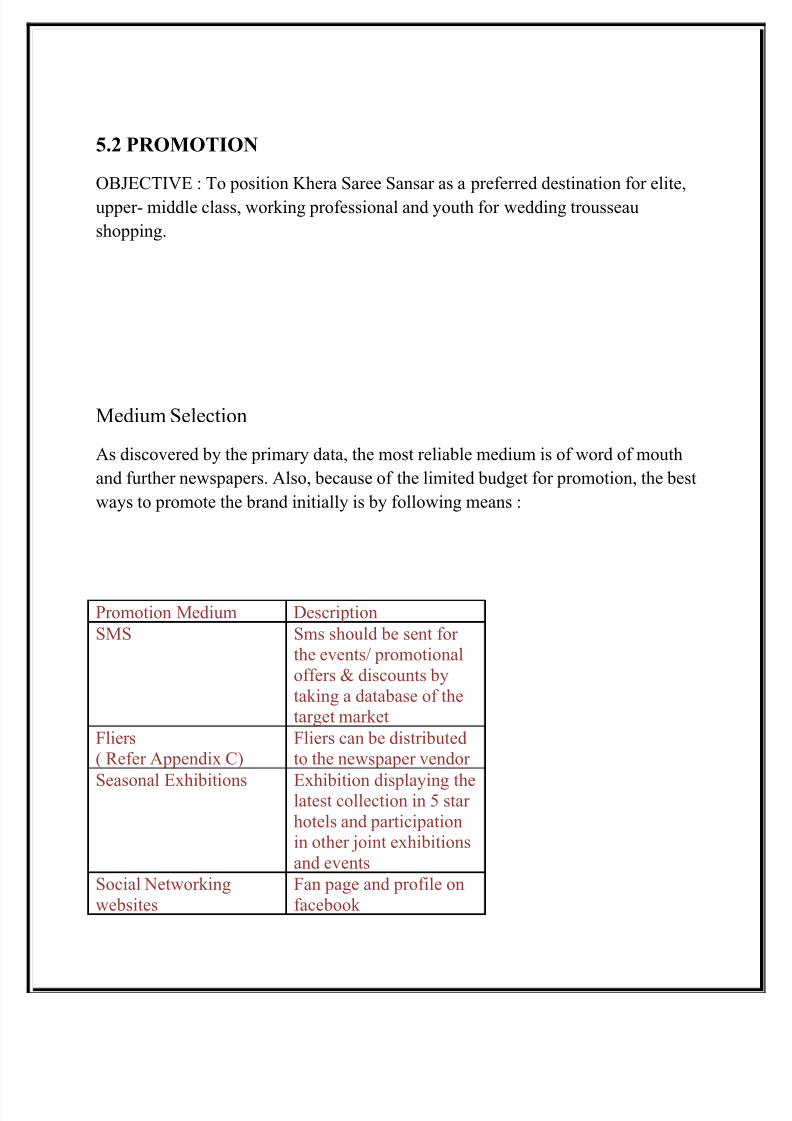

5.2 PROMOTION

OBJECTIVE : To position Khera Saree Sansar as a preferred destination for elite,

upper- middle class, working professional and youth for wedding trousseau

shopping.

Medium Selection

As discovered by the primary data, the most reliable medium is of word of mouth

and further newspapers. Also, because of the limited budget for promotion, the best

ways to promote the brand initially is by following means :

Promotion Medium Description

SMS Sms should be sent for the events/ promotionaloffers & discounts bytaking a database of thetarget market

Fliers( Refer Appendix C)

Fliers can be distributedto the newspaper vendor

Seasonal Exhibitions Exhibition displaying thelatest collection in 5 star hotels and participationin other joint exhibitionsand events

Social Networkingwebsites

Fan page and profile onfacebook

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 27/40

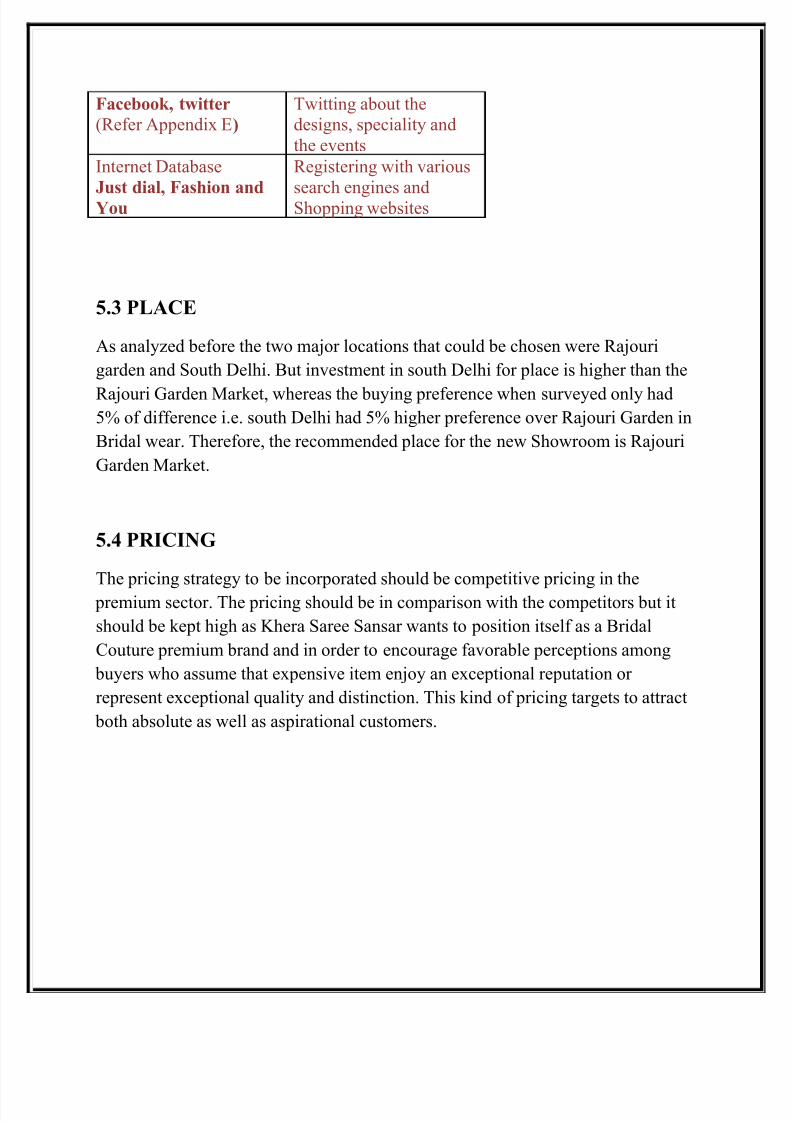

Facebook, twitter

(Refer Appendix E)

Twitting about thedesigns, speciality andthe events

Internet Database

Just dial, Fashion andYou

Registering with various

search engines andShopping websites

5.3 PLACE

As analyzed before the two major locations that could be chosen were Rajouri

garden and South Delhi. But investment in south Delhi for place is higher than the

Rajouri Garden Market, whereas the buying preference when surveyed only had5% of difference i.e. south Delhi had 5% higher preference over Rajouri Garden in

Bridal wear. Therefore, the recommended place for the new Showroom is Rajouri

Garden Market.

5.4 PRICING

The pricing strategy to be incorporated should be competitive pricing in the

premium sector. The pricing should be in comparison with the competitors but it

should be kept high as Khera Saree Sansar wants to position itself as a Bridal

Couture premium brand and in order to encourage favorable perceptions among

buyers who assume that expensive item enjoy an exceptional reputation or

represent exceptional quality and distinction. This kind of pricing targets to attract

both absolute as well as aspirational customers.

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 28/40

CHAPTER – 6 : FINANCIAL DATA AND

PROJECTIONS

Khera Saree Sansar’s present three showrooms in Chandni Chowk has the

following financial overview : (Appendix B)

Asset Turnover Ratio = 1.6

Gross Profit= Rs. 4,90,000

Current Ratio =1

6.1 PROJECTED SALES

For the new to-be opened showroom, the best suitable time would be initial

wedding season as per the Indian calendar i.e. around july. Following are the

overview of the projected sales for initial 6 months( a whole season)

Projected Sales Amount

1st Month Per day sales: Rs 200,000Per month Sales: Rs 200,000*30=Rs60,00,000

2nd Month Per day Sales: Rs 300,000

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 29/40

Per month sales: Rs 90,00,000

3rd Month Per day Sales: Rs 400,000Per month sales: Rs 120,00,000

4th-6th Month Per day sales: Rs 600,000

Per month sales: Rs 180,00,000Total sales: Rs 540,00,000

Being a family owned and conventional drivers of the business, they are not very

open to investing a high amount in promotion and prefers to continue with the

growth with majorly by word of mouth. Rest is done by filers, exhibitions and

social media(internet).

6.2 OPERATING EXPENSE

Depriciation – 150

Packing Exp. – 5000

Postage – 800

Electricity – 25000

Accountancy Charges – 8000

Bank Charges – 4000

Conveyance – 20000

Membership fee – 1500

Diwali Exp. – 2500

Salaries – 95000

House tax – 4500

Misc. Exp. – 35000

Intt. – 90000

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 30/40

Insurance – 5500

Sales promotion – 9000

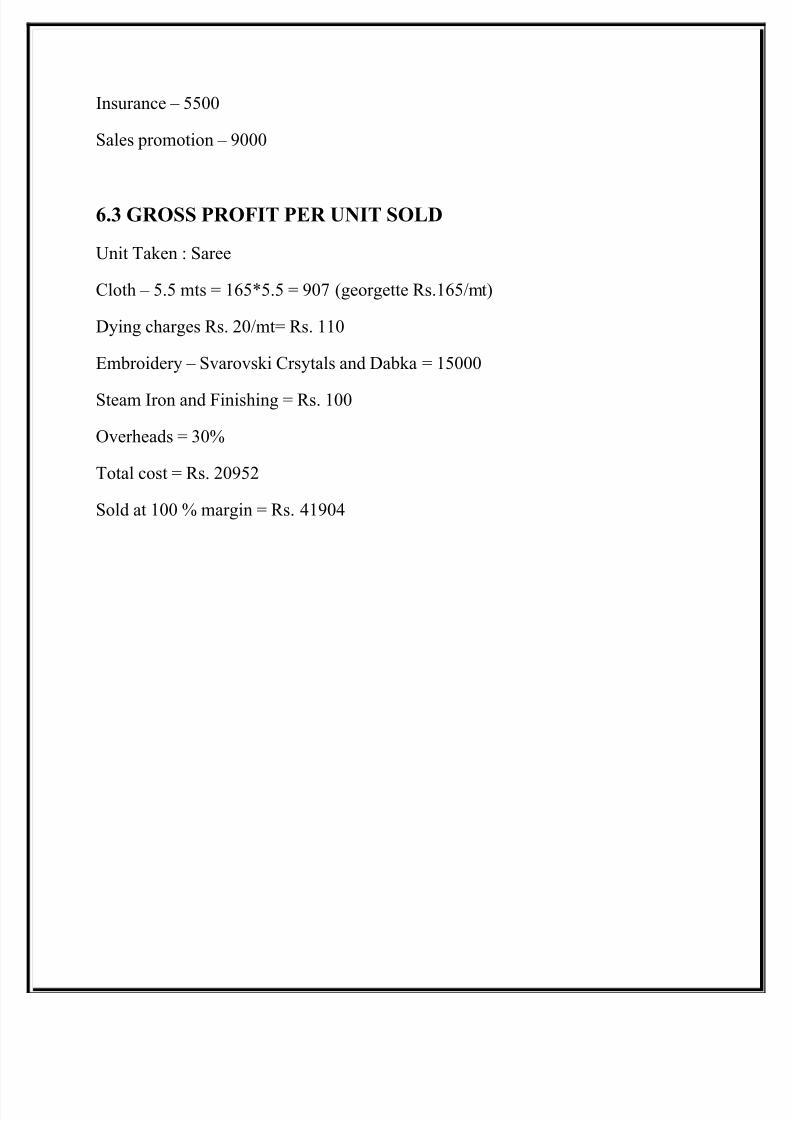

6.3 GROSS PROFIT PER UNIT SOLD

Unit Taken : Saree

Cloth – 5.5 mts = 165*5.5 = 907 (georgette Rs.165/mt)

Dying charges Rs. 20/mt= Rs. 110

Embroidery – Svarovski Crsytals and Dabka = 15000

Steam Iron and Finishing = Rs. 100

Overheads = 30%

Total cost = Rs. 20952

Sold at 100 % margin = Rs. 41904

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 31/40

CHAPTER – 7 : IMPLEMENTATION PLAN

GANTT CHART

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 32/40

CHAPTER – 8 : EVALUATION AND

CONTROL

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 33/40

8.1 QUALITY CONTROL:

• Customer feedback form: Customer feedback should be taken in terms of quality, design, experience and after sales service to know if the customer is

satisfied.

• Inventory and merchandise management control measure should be taken like

pest control etc. so that the delicate merchandise and fabric is not spoiled

8.2 RISK ANALYSIS:

• Other Independent entities having a similar identity

• Unable to recover the fixed cost by the end of two yrs

• Competition with renowned established Showroom who already have a large

market share and customer base

• Increase in the rent of the property where the showroom is suppose to be

situated

• Disagreement/ Dispute between the members

• Economic depression

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 34/40

REFERENCING

• Big fat Indian wedding just got more expensive,Yashpal Parmar . McClatchy- Tribune Business News. Washington: Sep 18, 2009.

• http://www.asianewsnet.net/home/

• http://proquest.umi.com/pqdweb?

did=2282155991&sid=1&Fmt=3&clientId=105187&RQT=309&VName=

PQD

• www.frontierbazaar.org

• www.ctcemporio.in

• The Hindu Aug 21, 2009 by Snehesh Alex Philip in New Delhi

• CMAI Apparel journal, October 07,2010

• Innovation in unorganized sectors by PA RV ATH I ME NO N ON JU NE

29 2008

• http://knowledge.wharton.upenn.edu/india/article.cfm?articleid=4348

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 35/40

APPENDICES

Appendix- A

Following questionnaire was made to survey a sample size of 200 in order to

identify the tastes and preferences, buying behavior and decision making of the

customer of the particular category.

Age :

Place :

Q1. How much in advance you started planning and shopping for your wedding?

Less than a month 2-3months more than 3 months

Q2. What are the criteria to select a Bridal outfit?

Design Variety Trend

Price Brand Name Quality

Q3. What is the Budget for Apparel for your wedding?

Less than 2 lacs 2-5 lacs More than 5 lacs

Q4. Is it flexible?

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 36/40

Yes No

Q5. How many showrooms you browse in one day?

1-5 5-10 more than 10

Q6. Is your buying decision influenced by anyone?

Yes No

Q7. How do you get aware of the present brands for bridal wear?

Newspaper & Magazines Television/ Radio

Word of mouth Other Media

Q8. Does the Location and convenience matters to you for Bridal trousseau

shopping?

Yes No

Q9. Where in Delhi you shop for the same?

South Delhi Karol Bagh

Rajouri Garden Designers

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 37/40

Appendix – B

Location of present Showrooms

Appendix – C

The Website

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 38/40

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 39/40

Appendix – D

The Balance Sheet 2009

8/3/2019 Semester End Project 2011- Satakshi Arora

http://slidepdf.com/reader/full/semester-end-project-2011-satakshi-arora 40/40

Profit and Loss A/C