sensible deliverable d5.4 energy market interaction of ... · sensible – deliverable d5.4 energy...

TRANSCRIPT

Sensible – DELIVERABLE

D5.4 Energy market interaction of business models

This project has received funding from the European Union's Horizon 2020 research and

innovation programme under Grant Agreement No. 645963.

Deliverable number: D5.4

Due date: 31.12.2017

Nature1: R

Dissemination Level1: PU

Work Package: 5

Lead Beneficiary: Empower

Contributing Beneficiaries: EDP, INDRA, INESC, USE

Editor(s): Olli Kilkki, Empower

Reviewer(s): André Leonide, Siemens

1 Nature: R = Report, P = Prototype, D = Demonstrator, O = Other

Dissemination level PU = Public PP = Restricted to other programme participants (including the Commission Services) RE = Restricted to a group specified by the consortium (including the Commission Services) CO = Confidential, only for members of the consortium (including the Commission Services) Restraint UE = Classified with the classification level "Restraint UE" according to Commission Deci-sion 2001/844 and amendments Confidential UE = Classified with the mention of the classification level "Confidential UE" according to Commission Decision 2001/844 and amendments Secret UE = Classified with the mention of the classification level "Secret UE" according to Commis-sion Decision 2001/844 and amendments

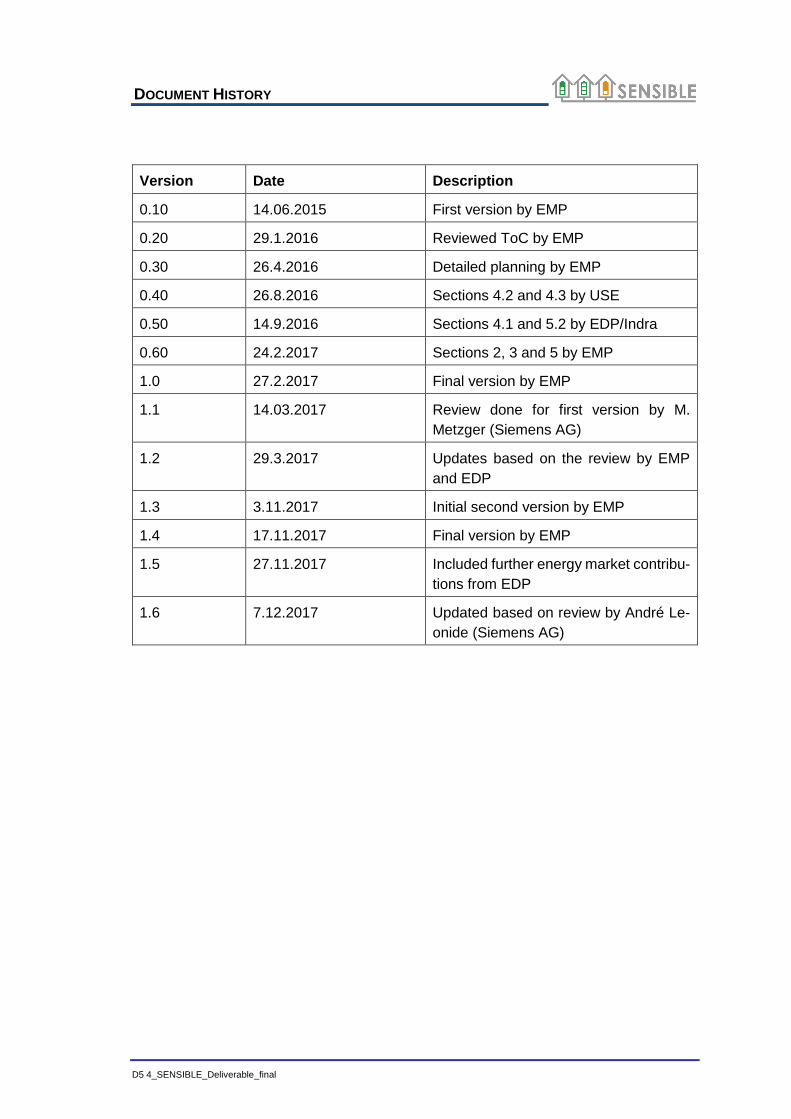

DOCUMENT HISTORY

D5 4_SENSIBLE_Deliverable_final

Version Date Description

0.10 14.06.2015 First version by EMP

0.20 29.1.2016 Reviewed ToC by EMP

0.30 26.4.2016 Detailed planning by EMP

0.40 26.8.2016 Sections 4.2 and 4.3 by USE

0.50 14.9.2016 Sections 4.1 and 5.2 by EDP/Indra

0.60 24.2.2017 Sections 2, 3 and 5 by EMP

1.0 27.2.2017 Final version by EMP

1.1 14.03.2017 Review done for first version by M.

Metzger (Siemens AG)

1.2 29.3.2017 Updates based on the review by EMP

and EDP

1.3 3.11.2017 Initial second version by EMP

1.4 17.11.2017 Final version by EMP

1.5 27.11.2017 Included further energy market contribu-

tions from EDP

1.6 7.12.2017 Updated based on review by André Le-

onide (Siemens AG)

TABLE OF CONTENT

C O N F I D E N T I A L until public release by the SENSIBLE project consortium

D5 4_SENSIBLE_Deliverable_final

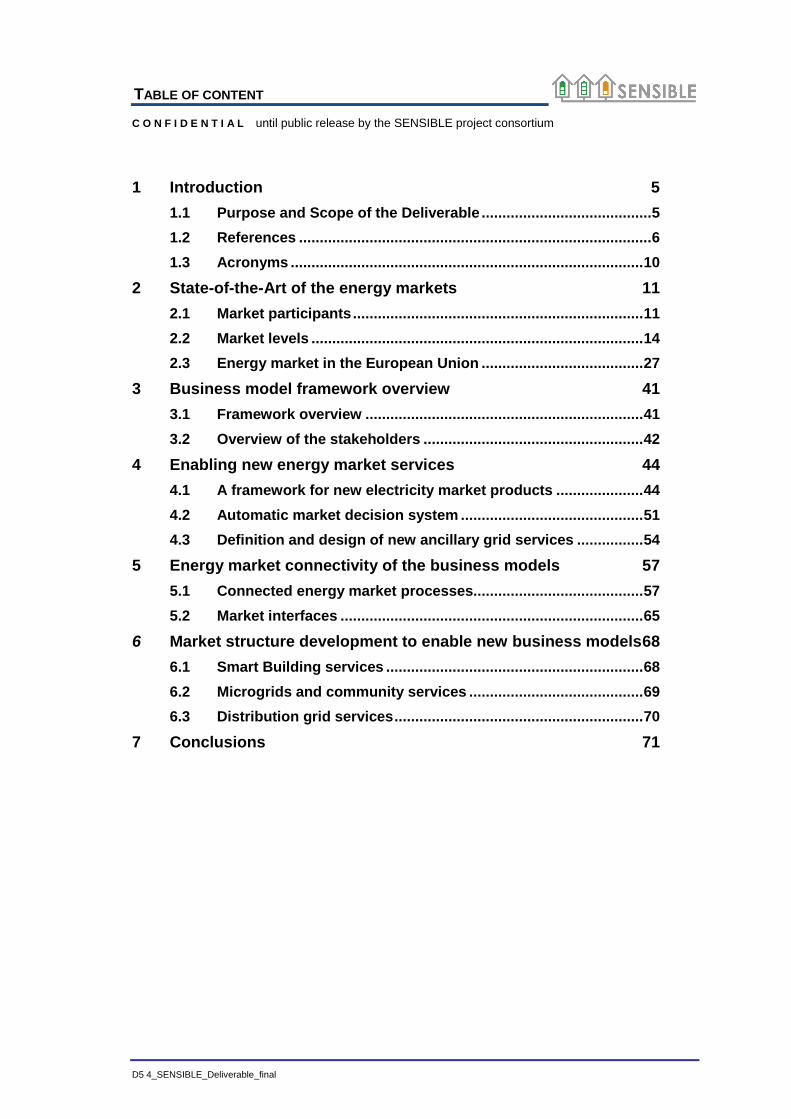

1 Introduction 5

1.1 Purpose and Scope of the Deliverable ......................................... 5

1.2 References ..................................................................................... 6

1.3 Acronyms ..................................................................................... 10

2 State-of-the-Art of the energy markets 11

2.1 Market participants ...................................................................... 11

2.2 Market levels ................................................................................ 14

2.3 Energy market in the European Union ....................................... 27

3 Business model framework overview 41

3.1 Framework overview ................................................................... 41

3.2 Overview of the stakeholders ..................................................... 42

4 Enabling new energy market services 44

4.1 A framework for new electricity market products ..................... 44

4.2 Automatic market decision system ............................................ 51

4.3 Definition and design of new ancillary grid services ................ 54

5 Energy market connectivity of the business models 57

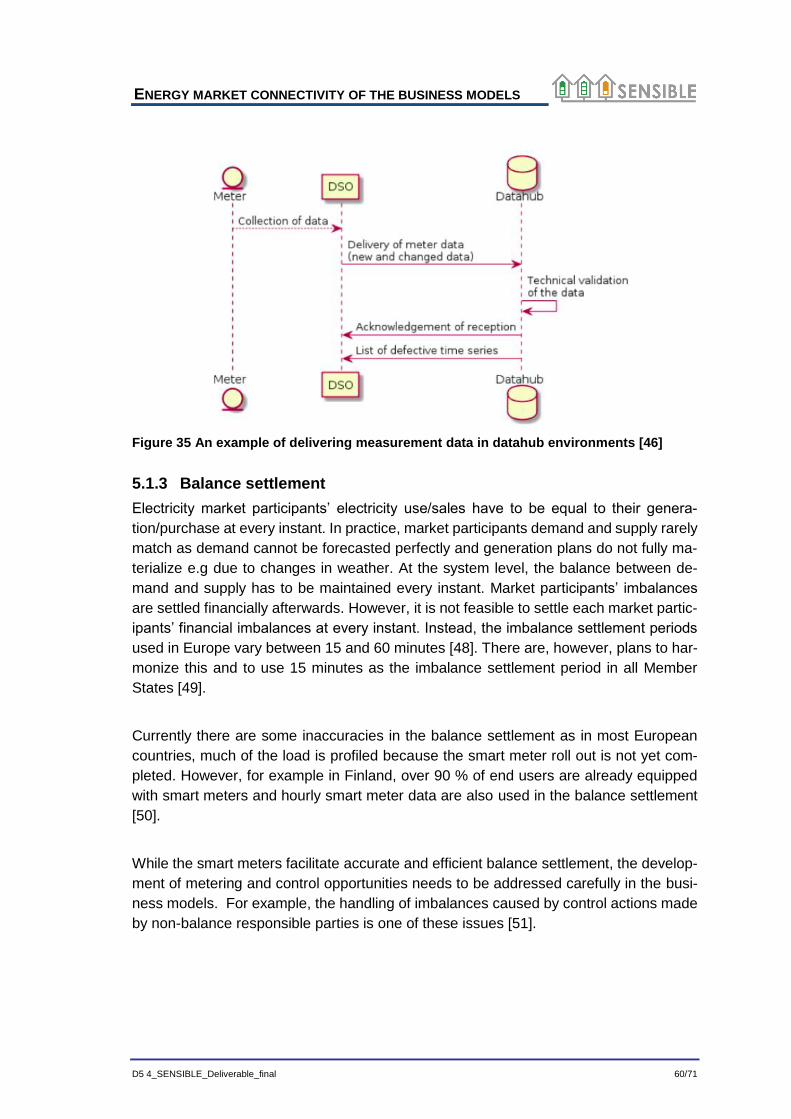

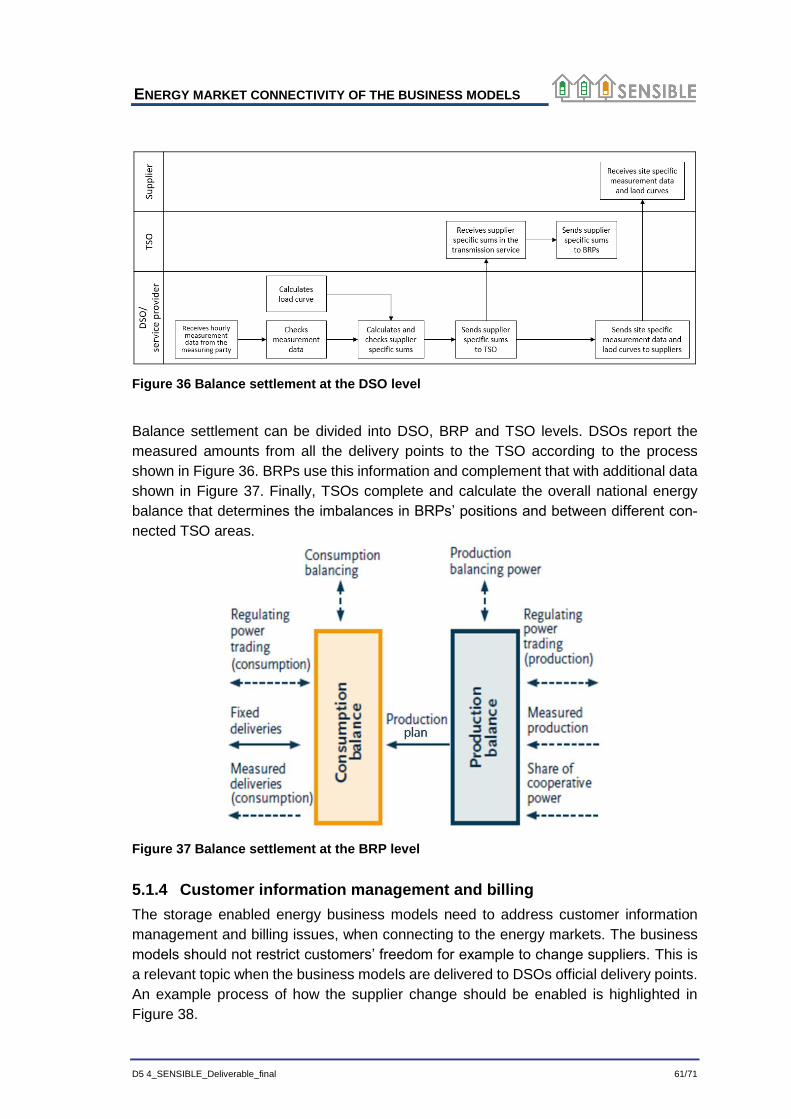

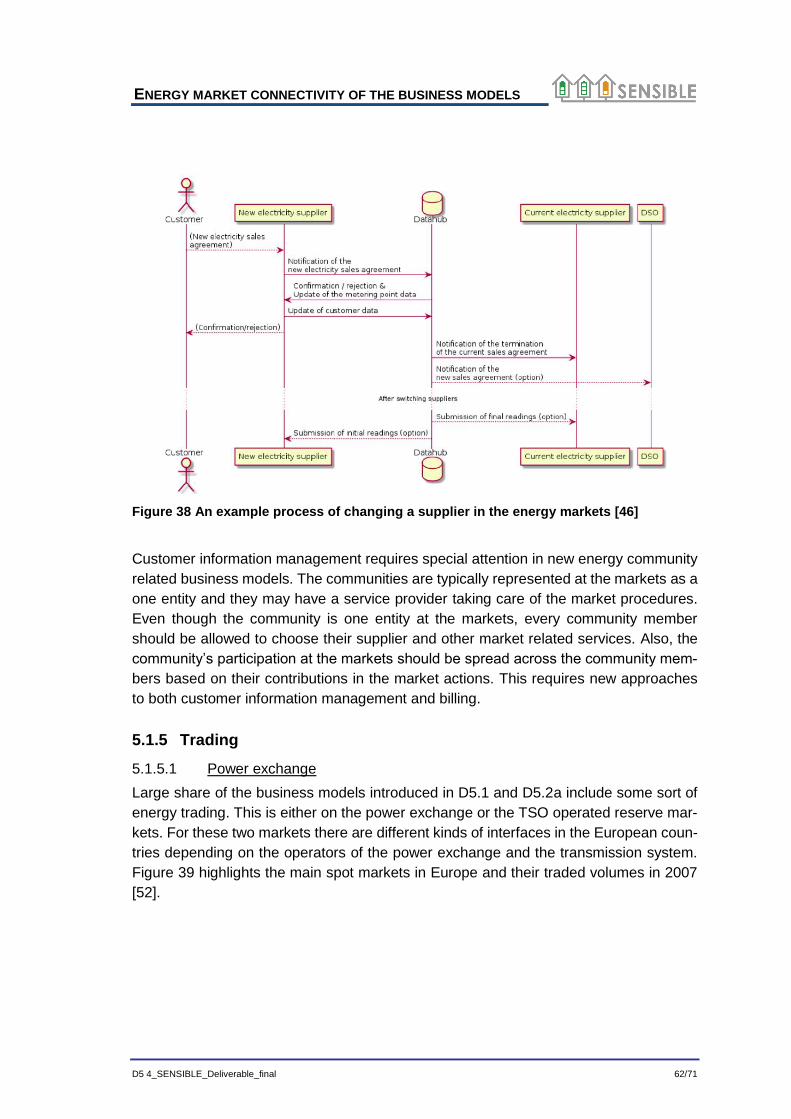

5.1 Connected energy market processes......................................... 57

5.2 Market interfaces ......................................................................... 65

6 Market structure development to enable new business models 68

6.1 Smart Building services .............................................................. 68

6.2 Microgrids and community services .......................................... 69

6.3 Distribution grid services ............................................................ 70

7 Conclusions 71

EXECUTIVE SUMMARY

D5 4_SENSIBLE_Deliverable_final 4/71

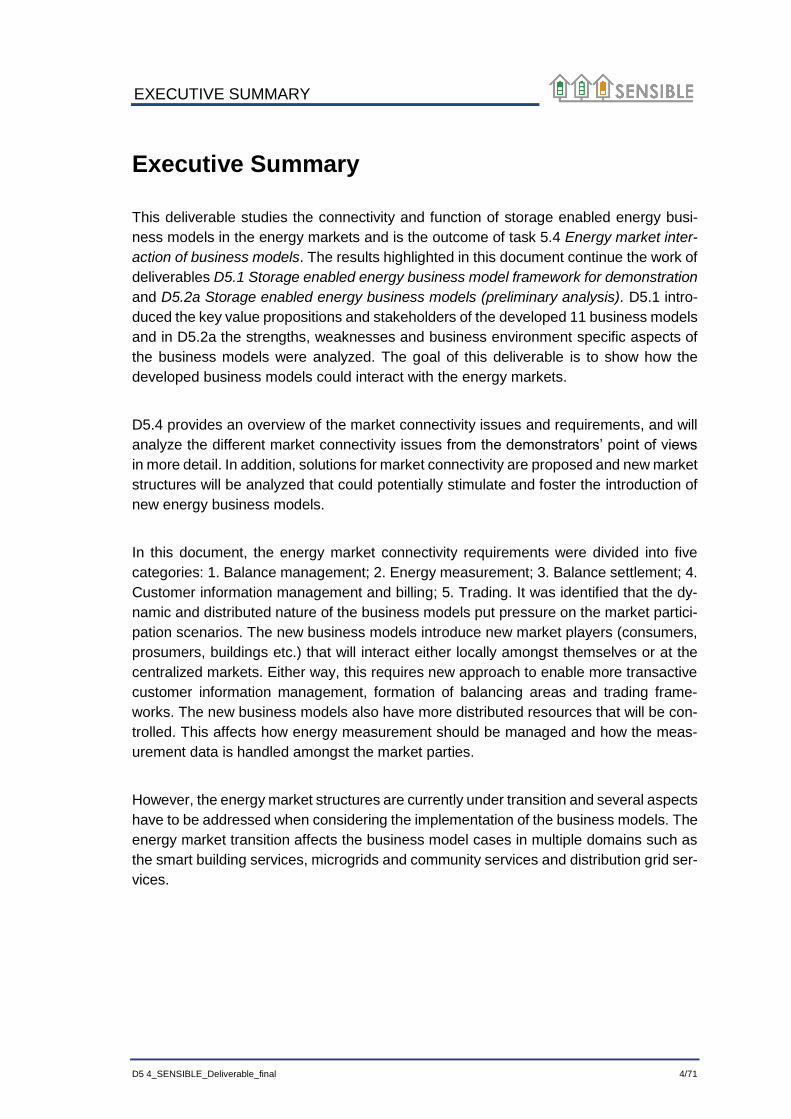

Executive Summary

This deliverable studies the connectivity and function of storage enabled energy busi-

ness models in the energy markets and is the outcome of task 5.4 Energy market inter-

action of business models. The results highlighted in this document continue the work of

deliverables D5.1 Storage enabled energy business model framework for demonstration

and D5.2a Storage enabled energy business models (preliminary analysis). D5.1 intro-

duced the key value propositions and stakeholders of the developed 11 business models

and in D5.2a the strengths, weaknesses and business environment specific aspects of

the business models were analyzed. The goal of this deliverable is to show how the

developed business models could interact with the energy markets.

D5.4 provides an overview of the market connectivity issues and requirements, and will

analyze the different market connectivity issues from the demonstrators’ point of views

in more detail. In addition, solutions for market connectivity are proposed and new market

structures will be analyzed that could potentially stimulate and foster the introduction of

new energy business models.

In this document, the energy market connectivity requirements were divided into five

categories: 1. Balance management; 2. Energy measurement; 3. Balance settlement; 4.

Customer information management and billing; 5. Trading. It was identified that the dy-

namic and distributed nature of the business models put pressure on the market partici-

pation scenarios. The new business models introduce new market players (consumers,

prosumers, buildings etc.) that will interact either locally amongst themselves or at the

centralized markets. Either way, this requires new approach to enable more transactive

customer information management, formation of balancing areas and trading frame-

works. The new business models also have more distributed resources that will be con-

trolled. This affects how energy measurement should be managed and how the meas-

urement data is handled amongst the market parties.

However, the energy market structures are currently under transition and several aspects

have to be addressed when considering the implementation of the business models. The

energy market transition affects the business model cases in multiple domains such as

the smart building services, microgrids and community services and distribution grid ser-

vices.

INTRODUCTION

D5 4_SENSIBLE_Deliverable_final 5/71

1 Introduction

1.1 Purpose and Scope of the Deliverable

This deliverable is the outcome of the task 5.4 Energy market interaction of business

models. In this document, an analysis is provided on how the business models devel-

oped in D5.1 and D5.2a can be connected to the different levels of the energy markets.

The document has been divided into five main sections. In Chapter 2, the State-of-the-

Art solutions and processes of the energy markets have been described. Chapter 3 gives

an overview of the business models that have been defined earlier in WP5. The main

stakeholders and value propositions are identified, in order to understand who needs to

interact with the energy markets and how. Based on the business models, chapter 4

describes a framework for new ancillary services. In Chapter 5 the energy market con-

nectivity requirements of the business models will be evaluated. Finally, in Chapter 6,

energy market structure developments to enable new business models are analyzed.

The D5.4 considers the energy market interaction of the business models. The purpose

is to identify all the relevant requirements for the energy market interaction of the busi-

ness models. In addition, the business models and demonstrators, and how they meet

the requirements of the energy market interaction, are evaluated.

INTRODUCTION

D5 4_SENSIBLE_Deliverable_final 6/71

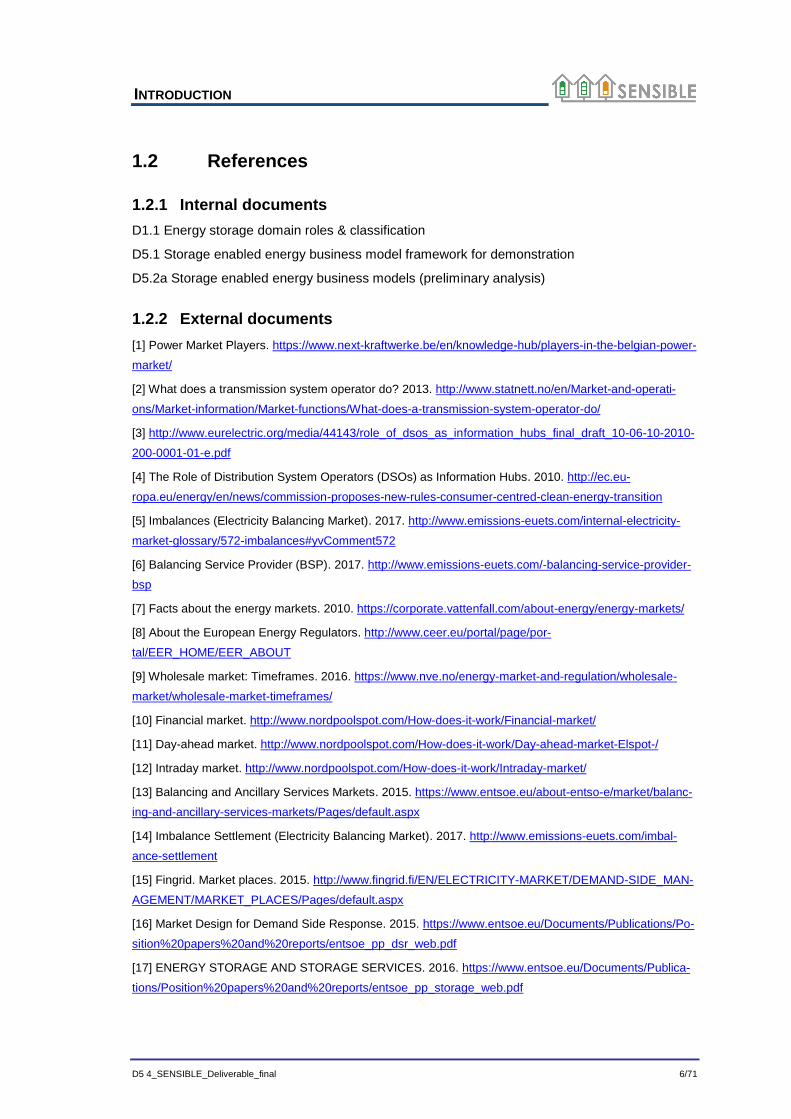

1.2 References

1.2.1 Internal documents

D1.1 Energy storage domain roles & classification

D5.1 Storage enabled energy business model framework for demonstration

D5.2a Storage enabled energy business models (preliminary analysis)

1.2.2 External documents

[1] Power Market Players. https://www.next-kraftwerke.be/en/knowledge-hub/players-in-the-belgian-power-

market/

[2] What does a transmission system operator do? 2013. http://www.statnett.no/en/Market-and-operati-

ons/Market-information/Market-functions/What-does-a-transmission-system-operator-do/

[3] http://www.eurelectric.org/media/44143/role_of_dsos_as_information_hubs_final_draft_10-06-10-2010-

200-0001-01-e.pdf

[4] The Role of Distribution System Operators (DSOs) as Information Hubs. 2010. http://ec.eu-

ropa.eu/energy/en/news/commission-proposes-new-rules-consumer-centred-clean-energy-transition

[5] Imbalances (Electricity Balancing Market). 2017. http://www.emissions-euets.com/internal-electricity-

market-glossary/572-imbalances#yvComment572

[6] Balancing Service Provider (BSP). 2017. http://www.emissions-euets.com/-balancing-service-provider-

bsp

[7] Facts about the energy markets. 2010. https://corporate.vattenfall.com/about-energy/energy-markets/

[8] About the European Energy Regulators. http://www.ceer.eu/portal/page/por-

tal/EER_HOME/EER_ABOUT

[9] Wholesale market: Timeframes. 2016. https://www.nve.no/energy-market-and-regulation/wholesale-

market/wholesale-market-timeframes/

[10] Financial market. http://www.nordpoolspot.com/How-does-it-work/Financial-market/

[11] Day-ahead market. http://www.nordpoolspot.com/How-does-it-work/Day-ahead-market-Elspot-/

[12] Intraday market. http://www.nordpoolspot.com/How-does-it-work/Intraday-market/

[13] Balancing and Ancillary Services Markets. 2015. https://www.entsoe.eu/about-entso-e/market/balanc-

ing-and-ancillary-services-markets/Pages/default.aspx

[14] Imbalance Settlement (Electricity Balancing Market). 2017. http://www.emissions-euets.com/imbal-

ance-settlement

[15] Fingrid. Market places. 2015. http://www.fingrid.fi/EN/ELECTRICITY-MARKET/DEMAND-SIDE_MAN-

AGEMENT/MARKET_PLACES/Pages/default.aspx

[16] Market Design for Demand Side Response. 2015. https://www.entsoe.eu/Documents/Publications/Po-

sition%20papers%20and%20reports/entsoe_pp_dsr_web.pdf

[17] ENERGY STORAGE AND STORAGE SERVICES. 2016. https://www.entsoe.eu/Documents/Publica-

tions/Position%20papers%20and%20reports/entsoe_pp_storage_web.pdf

INTRODUCTION

D5 4_SENSIBLE_Deliverable_final 7/71

[18] Energy storage. 2017. https://ec.europa.eu/energy/en/topics/technology-and-innovation/energy-stor-

age

[19] Eyer, J. & Garth C. (2010) Energy Storage for Electricity Grid: Benefits and Market Potential Assess-

ment Guide - A Study for the DOE Energy Storage Systems Program [Online] Albuquerque, N.M.: Sandia

National Laboratories. Available from: http://www.sandia.gov/ess/publications/SAND2010-0815.pdf

[20] Rastler D. (2010) Electricity Energy Storage Technology Options - A White Paper Primer on Applica-

tions, Costs, and Benefits [Online]. Palo Alto, CA: EPRI – Electric Power Research Institute. Available

from: http://www.epri.com/abstracts/Pages/ProductAbstract.aspx?ProductId=000000000001020676

[21] PRICES AND COSTS OF EU ENERGY. 2016. https://ec.europa.eu/energy/sites/ener/files/docu-

ments/report_ecofys2016.pdf

[22] EU:n sähkön vähittäismarkkinat. 2015.

http://188.117.57.25/sites/default/files/erikoistyo_raininkonayttoversio.pdf

[23] Electricity prices for industrial consumers, second half 2015. 2016. http://ec.europa.eu/eurostat/statis-

tics-explained/index.php/File:Electricity_prices_for_industrial_consumers,_sec-

ond_half_2015_(%C2%B9)_(EUR_per_kWh)_YB16.png

[24] Iberian Electricity Market. http://www.mibel.com/index.php?lang=en

[25] The Iberian Energy Derivatives Exchange. http://www.omip.pt/

[26] The Iberian Energy Derivatives Exchange. http://www.omie.es/en/inicio

[27] Intraday market in MIBEL. http://www.omie.es/en/home/markets-and-products/electricity-market/our-

electricity-markets/daily-and-intradaily

[28] Redes Energéticas Nacionais. http://www.ren.pt/

[29] Red Eléctrica de España. http://ree.es/en

[30] Interruptibility Service. http://www.mercado.ren.pt/EN/Electr/ActivitiesServices/Interruptibil-

ity/Pages/default.aspx

[31] Interruptibility Service. http://www.ree.es/en/activities/operation-of-the-electricity-system/interruptibil-

ity-service

[32] C. M. Gouveia, Carlos L.; Lopes, João A. P.; Varajão, Diogo; Araújo, Rui E. (2013, 12 December

2013) Microgrid Service Restoration - The Role of Plugged-In Electric Vehicles. IEEE Industrial Electronics

Magazine. 26-41.

[33] Z. Wang, J. Zhong, D. Chen, Y. Lu, and K. Men, "A Multi-Period Optimal Power Flow Model Including

Battery Energy Storage," presented at the IEEE Power & Energy Society General Meeting, Vancouver,

BC, 2013.

[34] P. Wang, D. H. Liang, J. Yi, P. F. Lyons, P. J. Davison, and P. C. Taylor, "Integrating Electrical Energy

Storage Into Coordinated Voltage Control Schemes for Distribution Networks," IEEE Transactions on

Smart Grid, vol. 5, pp. 1018-1032, 2014.

[35] The Future Role of DSOs, A CEER Public Consultation Paper; Council of European Energy Regula-

tors, December 2014

[36] State of the art and trends review of Smart metering in electricity grdis, Noelia Uribe-Pérez, Luis Her-

nández, David de la Vega and Itziar Angulo, 2016.

INTRODUCTION

D5 4_SENSIBLE_Deliverable_final 8/71

[37] MODERNIZING THE ELECTRIC GRID (Chapter 3 – QER Report: Energy Transmission, Storage, and

Distribution Infrastructure, April 2015)

[38] DOE/EPRI 2013 Electricity Storage Handbook in Collaboration with NRECA. 2013.

http://www.epri.com/Pages/Understanding-the-Cost-Effectiveness-of-Energy-Storage.aspx

[39] Energy Management Control to meet MTRs in PV plants, Víctor Andrés Díaz, José Ramón Gordillo,

Carlos Infante and Manuel Lagares (http://www.greenpower.es/en/communication/new-detail/Energy-

Management-Control-to-meet-MTRs-in-PV-plants/)

[40] California Independent System Operator - Integration of Renewable Resources. 2007.

http://www.caiso.com/1ca5/1ca5a7a026270.pdf

[41] Control for Renewable Energy and Smart Grids. 2011. http://ieeecss.org/sites/ieeecss.org/files/docu-

ments/IoCT-Part1-06RESG.pdf

[42] Flexibility and Aggregation Requirements for their interaction in the market. 2014. http://www.eurelec-

tric.org/media/115877/tf_bal-agr_report_final_je_as-2014-030-0026-01-e.pdf

[43] Regulatory Recommendations for the Deployment of Flexibility. 2015. http://ec.europa.eu/en-

ergy/sites/ener/files/documents/EG3%20Final%20-%20January%202015.pdf

[44] DOE/EPRI 2013 Electricity storage Handbook in collaboration with NRECA, Abbas A.Akhil, Geor-

gianne Huff, Aileen B. Currier, Benjamin C. Kaun, Dan M. Rastler, Stella Bingqing Chen, Andrew L. Cotter,

Dale T. Bradshaw, and William D. Gauntlett.

[45] The economics of battery energy storage, how multi-use, customer-sited batteries deliver the most

services and value to customers and the grid, 2015

[46] Study on future information exchange solutions in the electricity retail market. 2014. http://www.fin-

grid.fi/fi/asiakkaat/asiakasliitteet/Datahub/Datahub_final_en.pdf

[47] DR pooli, 2015. Kysynnän jousto - Suomeen soveltuvat käytännön ratkaisut ja vaikutukset

verkkoyhtiöille (DR pooli). https://tutcris.tut.fi/portal/files/4776899/kysynnan_jousto_loppuraportti.pdf)

[48] Statnett, Fingrid, Svenska Kraftnät, Energinet.dk, 2016a, Nordic project on finer time resolution – In-

formation to stakeholders. November 2016. http://www.fingrid.fi/fi/ajankohtaista/Ajankohtaista%20liit-

teet/Ajankohtaisten%20liitteet/2016/Finer%20time%20resolution_information%20to%20stakeholders_No-

vember%202016_Final.pdf

[49] European Commission, 2016c, Commission regulation establishing a guideline on electricity balanc-

ing, EB – Version 10.10.2016. https://ec.europa.eu/energy/sites/ener/files/documents/informal_service_le-

vel_ebgl_10-10-2016nov.pdf

[50] Energy Authority, 2016, National Report 2016 to the Agency for the Cooperation of Energy Regulators

and to the European Commission, Finland. http://www.ceer.eu/portal/page/por-

tal/EER_HOME/EER_PUBLICATIONS/NATIONAL_REPORTS/National_Report-

ing_2016/NR_En/C16_NR_Finland-EN.pdf

[51] SGTF-EG3, 2015, Regulatory recommendations for the deployment of flexibility, January 2015.

https://ec.europa.eu/energy/sites/ener/files/documents/EG3%20Final%20-%20January%202015.pdf

[52] https://ec.europa.eu/energy/sites/ener/files/documents/2008_eu_wholesale_energy_market_histori-

cal.pdf

INTRODUCTION

D5 4_SENSIBLE_Deliverable_final 9/71

[53] Guidelines Facilitating Access to and Participation in GME’s Electricity Market. 2016. http://www.mer-

catoelettrico.org/en/MenuBiblioteca/Documenti/20041011GuidaMe.pdf

[54] Energy market trading systems in G6 countries. http://www.cs.rug.nl/~andrea/publications/ener-

gyMarketG6.pdf

[55] TRADING DOCUMENTS. 2017. http://www.epexspot.com/en/extras/download-center/trading_docu-

ments

[56] API. http://www.nordpoolspot.com/TAS/api/

[57] STORAGE BUSINESS MODELS IN THE GB MARKET. 2014. http://www.poyry.com/sites/de-

fault/files/374_elexon_storagebusinessmodelsandgbmarket_v2_0.pdf

[58] MARKET AND POLICY BARRIERS TO ENERGY STORAGE DEPLOYMENT. 2013. http://www.san-

dia.gov/ess/publications/SAND2013-7606.pdf

[59] Transactive Energy. 2014. www.cpuc.ca.gov/NR/rdonlyres/F67634A7.../PPDTransactiveEn-

ergy_30Oct14.pdf

[60] Smart Grid Security. 2012. https://www.enisa.europa.eu/topics/critical-information-infrastructures-and-

services/smart-grids/smart-grids-and-smart-metering/ict-inderdependencies-of-the-smart-grid

[61] How renewables will change electricity markets in the next five years. Energy policy 48 (2012): 64-75.

Schleicher-Tappeser, Ruggero.

[62] Best practices on Renewable Energy Self-consumption, EC, http://eur-lex.europa.eu/legal-con-

tent/LV/TXT/?uri=CELEX%3A52015SC0141

[63] Designing fair and equitable market rules for demand response aggregation, 2015, Eurelectric

http://www.eurelectric.org/media/169872/0310_missing_links_paper_final_ml-2015-030-0155-01-e.pdf

[64] Overview of Current Microgrid Policies, Incentives and Barriers in the European Union, United States

and China. Ali, Amjad, et al, Sustainability 9.7 (2017): 1146.

[65] Development options for distribution tariff structures in Finland, Honkapuro, Samuli, et al., European

Energy Market (EEM), 2017 14th International Conference on the. IEEE, 2017.

[66] DSO – tariffs: Current issues in Finland, Energiavirasto / Energy authority (Finland)

http://www.nordicenergyregulators.org/wp-content/uploads/2017/02/DSO-tariffs-in-Finland.pdf

INTRODUCTION

D5 4_SENSIBLE_Deliverable_final 10/71

1.3 Acronyms

ACER Agency for the Cooperation of En-ergy Regulators

ID Intraday (Market)

AEP American Electric Power IPEX Italian Power Exchange

aFRR Automatic Frequency Restoration Reserve

IPP Independent Power Producer

AMI Advanced Metering Infrastructure ISO Independent System Operators

API Application Programming Interface LCT Low-Carbon Technologies

BRP Balance Responsible Party LSE Load-serving entity

BSP Balance Service Provider LV Low Voltage

C&I Commercial and Industrial mFRR Manual Frequency Restoration Reserve

CAES Compressed air energy storage MG Microgeneration

CCGT Combined Cycle Gas Turbine MTR Minimum Technical Requirements

CEER Council of European Energy Regu-lators

MV Medium Voltage

CES Community Energy Storage PGE Pacific Gas and Electric

CHP Combined Heat and Power POI Point of Interconnection

CSV Comma Separated Values PPA Power purchase agreement

DA Day Ahead (Market) PPC Power Plant Controller

DESS Distributed Energy Storage Systems PPS Plug and Play Storage System

DG Distributed Generation PUC Public Utility Commission

DR Demand Response PV Photovoltaics

DSM Demand Side Management RES Renewable Energy Sources

DSO Distribution System Operator RES Renewable Energy Resources

DSO Distributed Storage RR Replacement Reserve

EC European Commission RTO Regional Transmission Organizations

EES Electrical Energy Storage SCE Southern California Edison

EEX European Energy Exchange SDG&E San Diego Gas and Electric

EPRI Electric Power Research Institute SG Smart Grid

ESCO Energy Services Company SMUD Sacramento Municipal Utility District

EU European Union T&D Transmission & Distribution

FCR Frequency Containment Reserve TOU Time-of-Use

FCR-D Frequency Controlled Disturbance Reserve

TSO Transmission System Operator

FCR-N Frequency Controlled Normal Oper-ation Reserve

UC Use Case

FERC Federal Energy Regulatory Com-mission

UCSD University of California, San Diego

ICT Information and Communication Technologies

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 11/71

2 State-of-the-Art of the energy markets

In order to understand the energy market interaction of new storage enabled business

models, one has to be familiar with the market levels and participants. The markets can

be divided into wholesale and retail markets that have been described in sections 2.2.1

and 2.2.2. Both of the market levels have specific participants or stakeholders that are

active in the markets. These will be described in section 2.1 together with the partner

specific requirements and responsibilities.

2.1 Market participants

An overview of the different market participants and their roles/responsibilities has been

provided below in Table 1. The table introduces the main market participants that will

have an impact in the business models. The participants may be the owners of the busi-

ness models or they may influence them e.g. through regulation.

Table 1 Overview of the market participants

Market

Party

Role of the Party

(requirements/responsibilities)

TSO Transmission System Operator (TSO) is responsible for transmitting elec-

tricity generated in large power plants over long distances using high volt-

age lines [1]. TSOs are responsible for keeping the national power sys-

tems in balance, and thus responsible for the overall physical manage-

ment and control of the national power system. Technically this means

that the frequency is maintained at 50 Hz [2]. To maintain balance, TSOs

issue a reserve market where the required power can be exchanged. The

volume of power that TSOs trade in this manner is called regulating/bal-

ancing power [2]. The TSOs choose who will change their production or

consumption based on a price offer that the producers and consumers

have given for this. The producer or consumer who has given the lowest

price for the change that is required will be chosen [2]. Furthermore, TSOs

facilitate the power market by making it physically possible to transport

power from sellers to buyers. This is achieved by taking into account phys-

ical laws, which dictate for example that there must be balance between

the production and consumption of power at all times [2].

DSO Distribution System Operator (DSO) is responsible for distributing elec-

tricity to end customers typically at medium and low voltage levels [1].

Electricity distribution (and transmission) is considered to be a "natural

monopoly" activity, meaning that on this specific market segment one firm

can produce a desired output at a lower social cost than two or more firms

because of both high fixed costs and economies of scale [3]. This explains

why distribution tariffs are regulated by the national regulatory authorities

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 12/71

who also define approved level of profits that DSOs are allowed to make

[3]. Articles 15-20 of the 2003/54/EC Directive has set a requirement that

distribution of electricity has to be separated from other segments of the

electricity value chain i.e. generation and supply. DSOs have a key role

to play in enabling competitive retail markets in Europe since they facili-

tate supplier changes, renewables/DER integration in the grid, consum-

ers’ participation at the centralized markets and transparent/non-discrim-

inatory access to network and customer information [3]. DSOs are typi-

cally also responsible for metering services in their respective grid area.

DSOs measure the actual consumed and produced energy in the delivery

points and the data is afterwards used for billing and balance settlement

purposes.

BRP Balance Responsible Party (BRP) is a market participant or its chosen

representative responsible for its imbalances in the electricity market [4].

Electricity imbalance most commonly means deviations between genera-

tion, consumption and commercial transactions of a BRP within a given

imbalance settlement period [5]. More formally, imbalance is an energy

volume calculated for a BRP and representing the difference between the

allocated volume attributed to that BRP, and the final position of that BRP

and any imbalance adjustment applied to that BRP, within a given imbal-

ance settlement period [5]. Any imbalances after the closure of the intra-

day market should be balanced by TSOs within the regulating market

timeframe [5]. An Imbalance has a size and a direction, indicating the di-

rection of the settlement transaction between BRP and TSO, with nega-

tive indicating BRP's shortage, and positive indicating BRP’s surplus [5].

Each party injecting to or taking from the grid needs to have a BRP [1].

Each access point has to be assigned to a balancing group (also balanc-

ing perimeter) of a BRP. The BRP is responsible for quarter-hourly (or

hourly) balance between total injections and total offtakes (measurements

at all assigned access points, trades on the power markets, cross-border

import/export and power exchanges with other BRPs) [1].

BSP Balance Service Provider (BSP) is a market participant providing balanc-

ing services to its connecting TSO [6]. This can be either balancing energy

and/or balancing capacity [4]. Each balancing energy bid from a BSP has

to be assigned to one or more BRP [6]. Settlements between TSOs and

BSPs are among tasks and functions that are fundamental to the core

objectives of ensuring operational security and integrating the balancing

market. These tasks include the calculation of activated volume of bal-

ancing energy and for invoicing purposes also price information about

each activation needs to be included [6].

Aggrega-

tor

An aggregator is a market participant who combines several decentral-

ized production and demand units in one portfolio. The aggregator can

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 13/71

then operate the portfolio in a coordinated manner and deliver the same

services as a large central power plant. This gives access to markets (re-

serve power and electricity markets) that cannot be entered by individual

units of the portfolio. This way the portfolio can be traded on the relevant

markets while furthermore system services can be offered to the TSO or

DSO supporting overall grid operation and integration of renewables. [1]

Producer Typically, producers refer to parties who generate electricity/energy in

large centralized power plants. This can be a nuclear, coal fired, natural

gas, offshore wind park, CHP etc. [1]. In addition to power generation,

producers can offer ancillary services to TSOs to help them maintain the

balance on the transmission grid. Most important ancillary services are

reserve products (frequency containment and restoration reserves), volt-

age regulation and black-start capability. [1]

Energy

supplier

Like it was written earlier, articles 15-20 of the 2003/54/EC Directive has

set a requirement that different electricity segments of the electricity value

chain i.e. generation, distribution and supply have to be separated from

each other [3]. This has led to the introduction of energy suppliers who

sell the electricity to the end-consumer [1]. Consumers can choose which

supplier they prefer (depending on the tariffs and services offered) [1].

Each supplier has to have a BRP to manage the energy balance of the

supplier.

Con-

sumer

An end-user (industrial, commercial or residential) that uses electricity to

drive industrial processes, household appliances, provide lighting or heat-

ing etc. [1]. Acquires electricity through a supplier. Access point to the grid

facilitated by the DSOs who measure and settle the use of electricity.

Prosumer Prosumers are consumers who also have their own production of electric-

ity. Prosumers can take electricity from the grid when their own production

is not sufficient or inject electricity into the grid when they are self-suffi-

cient. Likewise, prosumers can have storage resources and the use of

electricity can be managed for example by aggregators in relation to mar-

ket prices.

Power

exchange In Europe, there are more than twenty different energy exchanges. The

most liquid exchanges are the European Energy Exchange (EEX) and the

Nord Pool Spot / Nasdaq Omx Commodities [7]. The main markets within

an energy exchange are the spot market, for short-term trading, and the

forward market, where the physical delivery of, for example, electricity or

gas takes place at a future date [7]. The actors on the spot market are

producers, retailers and traders as well as large end users [7]. Power Ex-

changes are used for anonymous and transparent energy trading. A mul-

tilateral trading platform is set up, where market participants submit de-

mand or supply bids. The market operator will aggregate all the demand

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 14/71

bids and all supply bids and clear the market once every 15min (in Bel-

gium). The products offered on the power exchanges are standard prod-

ucts for which the demand is high enough to ensure liquidity and a good

price. [1]

Trader/

broker

Energy trader/broker is a company or a division of a supplier that assists

in procuring of electricity (or natural gas). Traders do not own or distribute

energy nor are they allowed to sell energy to customers. They are simply

participants that act on the markets and can influence market prices.

Regulator Since the transmission and distribution grid are operated as natural mo-

nopoly, there has to be an independent party, which checks the TSO and

DSO are not abusing their market power. They also keep an eye on pro-

ducers and consumers, to make sure (large) players do not try to influence

the prices. [1] The independent national regulators cooperate on Euro-

pean level through Agency for the Cooperation of Energy Regulators

(ACER) and the Council of European Energy Regulators (CEER). ACER’s

focus is on what is required in the legislation and CEER does everything

else in energy regulation [8].

2.2 Market levels

2.2.1 Wholesale markets

2.2.1.1 Traditional power markets

The wholesale electricity markets can be divided into four main categories. These cate-

gories enable the stakeholders to plan and manage their energy production and con-

sumption on both long and short term. The four main markets are: First, the financial

forward market; Second, the Day-Ahead Market; Third, the Intraday Market; Finally the

balancing markets. In addition to these four, the participants may also have bilateral con-

tracts with each other.

The financial forward market is regulated by the Financial Supervisory Authorities and

is placed under financial legislation. The financial market enables market participants to

secure their positions months or even several years ahead of the delivery day [9]. In the

Nord Pool for example, the contracts have a time horizon up to six years, covering daily,

weekly, monthly, quarterly and annual contracts [10]. There is no physical delivery for

financial power market contracts. Cash settlement takes place throughout trading and/or

the delivery period, starting at the due date of each contract, depending on whether the

product is a futures or a forward [10]. Technical conditions such as grid congestion and

access to capacity are not taken into consideration when entering financial contracts.

However, buyers and sellers can with the help of the financial (forward) power market

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 15/71

manage the risks associated to the physical market prices. [10] A well-functioning finan-

cial market and trade with power derivatives is important for market participants in the

physical power market because it allows them to off-set their positions and hedge future

income to adjust their risk profile. [9]

The Day-Ahead Market is the main arena for trading power. There, contracts are made

between seller and buyer for the delivery of power the following day, the price is set and

the trade is agreed. [11] The trading happens through a so-called implicit auction where

price and volume are calculated for every hour for the following day. This auction is based

on bids from both producers and consumers, and takes into account physical constraints

of cross-zonal capacity [9]. Consumers (typically suppliers) assess how much energy

they will need to meet demand the following day, and how much they are willing to pay

for this volume, hour by hour. The producers, on the other hand, assess how much power

they can deliver and at what price [11]. The bids are delivered through a trading system,

which feeds the information into a specialist computer system, which calculates the price.

Simply, the price is set where the curves for sell price and buy price meet. [11] By setting

price and volume for each bidding zone, the auction also determines the scheduled day-

ahead flows between bidding zones. The TSOs rely on the market clearing results when

planning next day’s operation of the grid. [9]

Figure 1 Formation of day-ahead electricity price

The system price is calculated based on the day-ahead market results and it represents

the unconstrained equilibrium price, i.e. by assuming there are no congestions in the

transmission grid. This price is used as reference for price setting in the financial market,

as well as for bilateral contracts and retail contracts in the market. The area specific

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 16/71

prices, i.e. the day-ahead price for each bidding zone take into account the restrictions

in the transmission grid. These capacities are given daily by the TSOs. [9]

The Intraday Market supplements the day-ahead market and helps secure the neces-

sary balance between supply and demand [12]. Market participants can trade until one

hour before the production hour in order to correct possible imbalances (such as if it

becomes colder or more windy than anticipated) [9]. The market opens once the day-

ahead market has closed, for example in Nord Pool three hours after the day-ahead

market closure [9]. Different to the day-ahead market, the intraday market has continu-

ous trading and trading takes place every day around the clock until one hour before

delivery [9,12]. Prices are set based on a first-come, first-served principle, where best

prices come first – highest buy price and lowest sell price [12]. The intraday market is

getting increasingly important as more intermittent wind and solar power, which is pre-

dictable only with uncertainty, is introduced to the markets [12]. In this sense, the market

plays a key role enabling larger shares of renewables in the grids.

The balancing (regulating) markets are operated by the TSOs who are responsible for

balancing the system [9]. According to ENTSO-E, balancing refers to the situation after

markets have closed (gate closure) in which a TSO acts to ensure that demand is equal

to supply, in and near real time [13]. Efficient balancing markets ensure the security of

supply at the least cost and decrease the need of back-up generation [13]. Within Eu-

rope, there is a will to harmonize the balancing markets in order to increase competition,

liquidity and efficiency [13]. Balancing also includes ancillary services, which refers to a

range of functions, which TSOs contract so that they can guarantee system operation.

These include [13]:

- black start capability (the ability to restart a grid following a blackout)

- frequency response (to maintain system frequency with automatic and very fast

responses. Includes Frequency Containment Reserve (FCR) and Automatic Fre-

quency Restoration Reserve (aFRR))

- fast disturbance reserve and strategic reserves (which can provide additional en-

ergy when needed. Includes Manual Frequency Restoration Reserve (mFRR)

and Replacement Reserve (RR))

- the provision of reactive power (provided only locally and not traded) and various

other services

The balancing markets can be accessed by both generators and demand response [13].

The ancillary services/markets defined above, can be divided into primary reserves

(FCR), secondary reserves (aFRR) and tertiary reserves (mFRR, RR) [9]. FCR and

aFRR are activated automatically while mFRR is activated manually. Furthermore, FCR

is the fastest, while mFRR is the slowest with a response deadline of 15 minutes. mFRR

is activated depending on need and with an hourly price resolution. Gate closure time for

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 17/71

bids in the balancing market is 45 minutes before time of production, but since mFRR

has a response time of 15 minutes, activation can happen within the production hour. [9]

An important aspect in the balancing markets is the imbalance settlement, which takes

place after the operational hour and is a TSO responsibility [9]. Imbalance settlement

means a financial settlement mechanism aiming at charging or paying Balance Respon-

sible Parties for their imbalances for each imbalance settlement period [14]. The general

principle of imbalance settlement is that all injections and all withdrawals should be cov-

ered by balancing responsibility and, depending on the state of the system, an imbalance

charge is imposed per imbalance settlement period on the BRPs that are not in balance

[14]. It typically aims at recovering the costs of balancing the system and include incen-

tives for the market to reduce imbalances while transferring the financial risk of imbal-

ances to BRPs [14]. This is especially important aspect also for storage enabled busi-

ness models and demand response. It is crucial to understand that all actions, made for

example by aggregators, affect the BRPs position and may cause it to be imbalance.

In addition to mentioned four marketplaces, power can also be exchanged through bi-

lateral contracts. A bilateral contract in the wholesale market is a market based contract

between a buyer and a seller with an agreed price, volume and time period [9]. Tradi-

tionally, power in the wholesale market was bought and sold through bilateral physical

contracts – both in short and long-term [9]. After the introduction of power exchange,

trading moved away from the physical bilateral contracts. However, there are still many

bilateral long-term contracts in the market, but most of these are financially settled [9].

For example in the Nordic countries, over 90 % of the physical power is traded through

Nord Pool and the Day-Ahead Market [9].

An overview of the described marketplaces and their relation to the delivery hour is de-

fined below in Figure 2.

Figure 2 Marketplaces for wholesale energy in relation to delivery hour

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 18/71

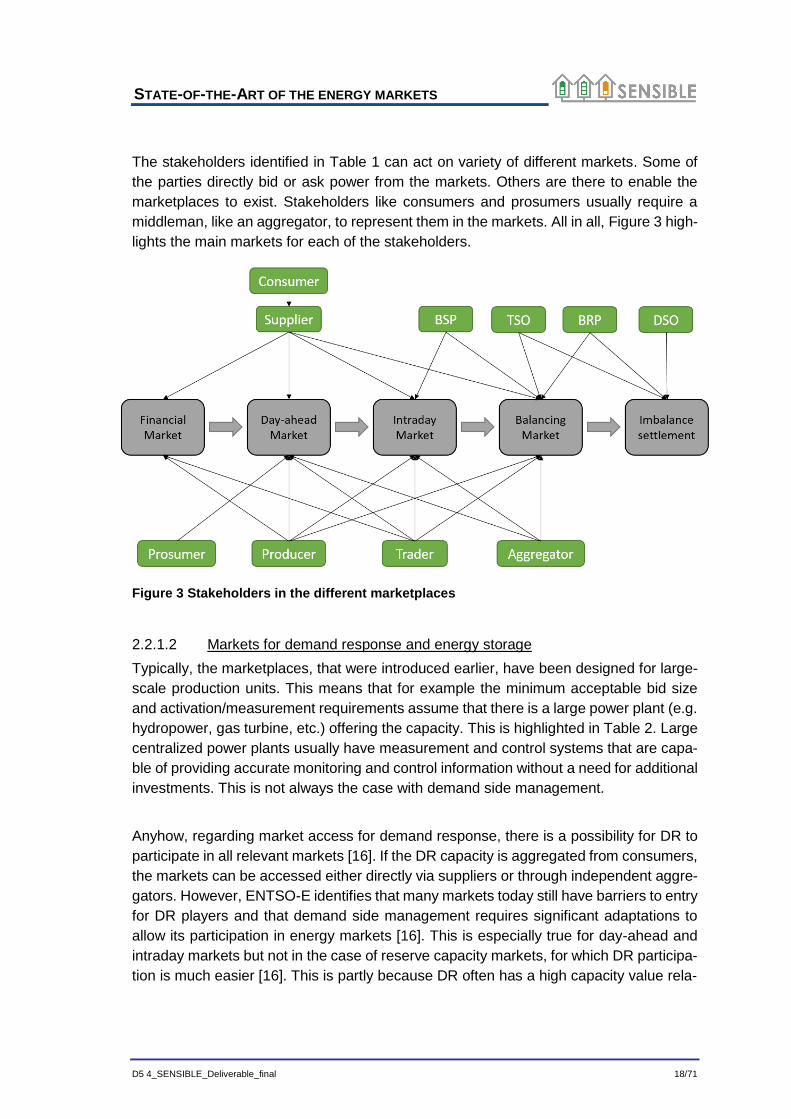

The stakeholders identified in Table 1 can act on variety of different markets. Some of

the parties directly bid or ask power from the markets. Others are there to enable the

marketplaces to exist. Stakeholders like consumers and prosumers usually require a

middleman, like an aggregator, to represent them in the markets. All in all, Figure 3 high-

lights the main markets for each of the stakeholders.

Figure 3 Stakeholders in the different marketplaces

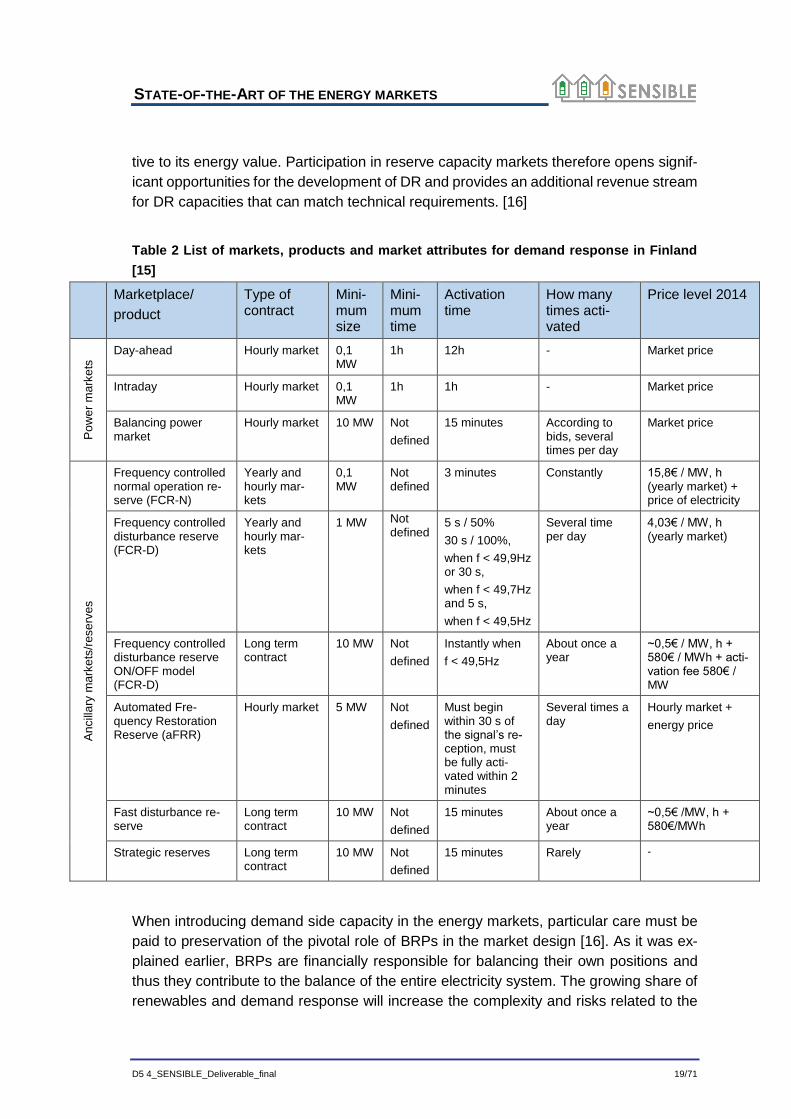

2.2.1.2 Markets for demand response and energy storage

Typically, the marketplaces, that were introduced earlier, have been designed for large-

scale production units. This means that for example the minimum acceptable bid size

and activation/measurement requirements assume that there is a large power plant (e.g.

hydropower, gas turbine, etc.) offering the capacity. This is highlighted in Table 2. Large

centralized power plants usually have measurement and control systems that are capa-

ble of providing accurate monitoring and control information without a need for additional

investments. This is not always the case with demand side management.

Anyhow, regarding market access for demand response, there is a possibility for DR to

participate in all relevant markets [16]. If the DR capacity is aggregated from consumers,

the markets can be accessed either directly via suppliers or through independent aggre-

gators. However, ENTSO-E identifies that many markets today still have barriers to entry

for DR players and that demand side management requires significant adaptations to

allow its participation in energy markets [16]. This is especially true for day-ahead and

intraday markets but not in the case of reserve capacity markets, for which DR participa-

tion is much easier [16]. This is partly because DR often has a high capacity value rela-

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 19/71

tive to its energy value. Participation in reserve capacity markets therefore opens signif-

icant opportunities for the development of DR and provides an additional revenue stream

for DR capacities that can match technical requirements. [16]

Table 2 List of markets, products and market attributes for demand response in Finland

[15]

Marketplace/

product

Type of contract

Mini-mum size

Mini-mum time

Activation time

How many times acti-vated

Price level 2014

Po

we

r m

ark

ets

Day-ahead Hourly market 0,1 MW

1h 12h - Market price

Intraday Hourly market 0,1 MW

1h 1h - Market price

Balancing power market

Hourly market 10 MW Not

defined

15 minutes According to bids, several times per day

Market price

An

cill

ary

ma

rke

ts/r

ese

rves

Frequency controlled normal operation re-serve (FCR-N)

Yearly and hourly mar-kets

0,1 MW

Not defined

3 minutes Constantly 15,8€ / MW, h (yearly market) + price of electricity

Frequency controlled disturbance reserve (FCR-D)

Yearly and hourly mar-kets

1 MW Not defined

5 s / 50%

30 s / 100%,

when f < 49,9Hz or 30 s,

when f < 49,7Hz and 5 s,

when f < 49,5Hz

Several time per day

4,03€ / MW, h (yearly market)

Frequency controlled disturbance reserve ON/OFF model (FCR-D)

Long term contract

10 MW Not

defined

Instantly when

f < 49,5Hz

About once a year

~0,5€ / MW, h + 580€ / MWh + acti-vation fee 580€ / MW

Automated Fre-quency Restoration Reserve (aFRR)

Hourly market 5 MW Not

defined

Must begin within 30 s of the signal’s re-ception, must be fully acti-vated within 2 minutes

Several times a day

Hourly market +

energy price

Fast disturbance re-serve

Long term contract

10 MW Not

defined

15 minutes About once a year

~0,5€ /MW, h + 580€/MWh

Strategic reserves Long term contract

10 MW Not

defined

15 minutes Rarely -

When introducing demand side capacity in the energy markets, particular care must be

paid to preservation of the pivotal role of BRPs in the market design [16]. As it was ex-

plained earlier, BRPs are financially responsible for balancing their own positions and

thus they contribute to the balance of the entire electricity system. The growing share of

renewables and demand response will increase the complexity and risks related to the

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 20/71

responsibilities of BRPs. Therefore, it is essential that BRPs are correctly informed about

the demand response actions so that they are able to fulfill their role and thereby avoid

counterbalancing and ensure proper forecasting. [16]

For storage resources, the participation on energy markets can be tricky because for

example European Commission and ENTSO-E see that storage is neither generation

nor demand [17,18]. Regarding energy market interaction, this will affect how storage is

handled in BRPs positions that consist of generation and demand portfolios, which have

to be matched. Eyer and Garth have identified below five categories for storage applica-

tions in the energy domain [19]. The issue of specifying storage as either generation or

demand will affect especially the category number two, ancillary services. For the other

four categories, there are no as significant barriers. Anyhow, their energy market inter-

action will also have to be taken into account since they affect billing and settlement.

Table 3 Five categories of electrical energy storage applications [19]

Another way to categorize storage participation/interaction in the energy markets is to divide it into groups from generation and system-level applications to T&D system applications and all the way to end-user applications. This is established in EPRI’s report, whose overview is defined in Table 4 [20].

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 21/71

Table 4 Definition of Energy Storage Applications [20]

Value Chain Application Description

Generation &

System-

Level Appli-

cations

T&D System

Applications

End-User

Applications

1 Wholesale Energy

Services

Utility-scale storage systems for bidding into en-

ergy, capacity and ancillary services markets

2 Renewables Inte-

gration

Utility-scale storage providing renewables time

shifting, load and ancillary services for grid inte-

gration

3 Stationary Storage

for T&D Support

Systems for T&D system support, improving T&D

system utilization factor, and T&D capital deferral

4 Transportable Stor-

age for T&D Sup-

port

Transportable storage systems for T&D system

support and T&D deferral at multiple sites as

needed

5 Distributed Energy

Storage Systems

Centrally managed modular systems providing in-

creased customer reliability, grid T&D support and

potentially ancillary services

6 ESCO Aggregated

Systems

Residential-customer-sited storage aggregated

and centrally managed to provide distribution sys-

tem benefits

7 C&I Power Quality

and Reliability

Systems to provide power quality and reliability to

commercial and industrial customers

8 C&I Energy Man-

agement

Systems to reduce TOU energy charges and de-

mand charges for C&I customers

9 Home Energy Man-

agement

Systems to shift retail load to reduce TOU energy

and demand charges

10 Home Backup Systems for backup power for home offices with

high reliability value

T&D=Transmission and Distribution; C&I=Commercial and Industrial; ESCO=Energy Services

Company; TOU=Time of Use

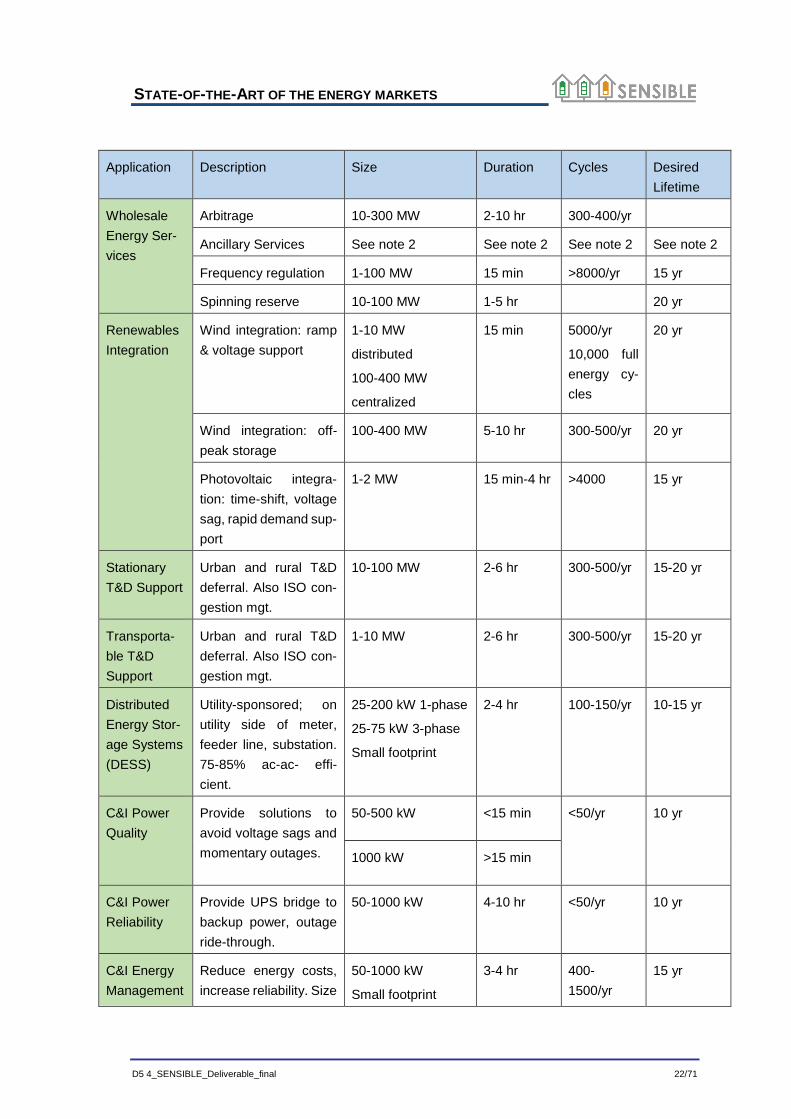

A key step in the EPRI’s report is the mapping between applications/benefits and the technical and energy storage performance requirements for each application [20]. This feature enables to see what kind of energy market interaction requirements there is for example in the wholesale energy market services. An overview of this study is shown in Table 5.

Table 5 General Energy Storage Application Requirements [20]

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 22/71

Application Description Size Duration Cycles Desired

Lifetime

Wholesale

Energy Ser-

vices

Arbitrage 10-300 MW 2-10 hr 300-400/yr

Ancillary Services See note 2 See note 2 See note 2 See note 2

Frequency regulation 1-100 MW 15 min >8000/yr 15 yr

Spinning reserve 10-100 MW 1-5 hr 20 yr

Renewables

Integration

Wind integration: ramp

& voltage support

1-10 MW

distributed

100-400 MW

centralized

15 min 5000/yr

10,000 full

energy cy-

cles

20 yr

Wind integration: off-

peak storage

100-400 MW 5-10 hr 300-500/yr 20 yr

Photovoltaic integra-

tion: time-shift, voltage

sag, rapid demand sup-

port

1-2 MW 15 min-4 hr >4000 15 yr

Stationary

T&D Support

Urban and rural T&D

deferral. Also ISO con-

gestion mgt.

10-100 MW 2-6 hr 300-500/yr 15-20 yr

Transporta-

ble T&D

Support

Urban and rural T&D

deferral. Also ISO con-

gestion mgt.

1-10 MW 2-6 hr 300-500/yr 15-20 yr

Distributed

Energy Stor-

age Systems

(DESS)

Utility-sponsored; on

utility side of meter,

feeder line, substation.

75-85% ac-ac- effi-

cient.

25-200 kW 1-phase

25-75 kW 3-phase

Small footprint

2-4 hr 100-150/yr 10-15 yr

C&I Power

Quality

Provide solutions to

avoid voltage sags and

momentary outages.

50-500 kW <15 min <50/yr 10 yr

1000 kW >15 min

C&I Power

Reliability

Provide UPS bridge to

backup power, outage

ride-through.

50-1000 kW 4-10 hr <50/yr 10 yr

C&I Energy

Management

Reduce energy costs,

increase reliability. Size

50-1000 kW

Small footprint

3-4 hr 400-

1500/yr

15 yr

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 23/71

varies by market seg-

ment.

1 MW 4-6 hr

Home En-

ergy Man-

agement

Efficiency, cost-sav-

ings

2-5 kW

Small footprint

2-4 hr 150-400/yr 10-15 yr

Home

Backup

Reliability 2-5 kW

Small footprint

2-4 hr 150-400/yr 10-15 yr

1. Size, duration, and cycle assumptions are based on EPRI’s generalized performance specifications

and requirements for each application, and are for the purpose of board comparison only. Data may

vary greatly based on specific situations, applications, site selection, business environment, etc.

2. Ancillary services encompass many market functions, such as black start capability and ramping ser-

vices, that have a wide range of characteristics and requirements.

2.2.2 Retail markets

2.2.2.1 Roles and responsibilities

After the liberalization of energy markets, the supply of electricity was separated from

generation and distribution. This has led to multiple stakeholders in the retail markets.

The main relevant stakeholders in the storage enabled business models are retailers,

DSOs, industrial/commercial clients and prosumers/consumers.

In the business models and on retail markets in general, retailers are responsible for

supply/sales of electricity to end customers. The retailers procure electricity from the

wholesale markets and supply that to the households or commercial/industrial custom-

ers. In addition to that, retailers may provide additional services like flexibility manage-

ment, like it is done in the Évora demonstrator.

Distribution System Operators are responsible for delivering the electricity to end cus-

tomers. An important responsibility for DSOs, regarding retail markets, is to measure the

actual consumption and production amounts in the delivery points. This information is

used for invoicing and balance settlement purposes. Likewise, in the integration of re-

newables, DSOs play a key role, since most of the capacity is connected to medium or

low voltage levels.

Large industrial or commercial companies are an important stakeholder in the retail

markets as they consume a significant part of the overall electricity. They can acquire

electricity either through retailers or they may be independent by procuring electricity

directly from the wholesale markets. Large companies or sites are also able to provide

substantial amounts of flexibility to the markets, like is the case in Nuremberg demon-

strator.

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 24/71

The European Commission identifies in their new winter package that consum-

ers/prosumers will play a key role in the future energy systems [4]. Consumers will not

only use electricity but they will introduce renewables in the distribution grids and thus

affect the retail market. The regulation and subsidies for renewables will have an impact

on consumer behaviour and the way in which new technology and services will be

launched.

2.2.2.2 Pricing and tariffs

Since the retail markets’ main task is to enable end customers to consume electricity, it

is natural that the corresponding pricing structures and tariffs are considered. The pricing

structures affect how people consume electricity, how energy efficiency and demand re-

sponse services are conceived and how attracting it is to develop new technology for the

energy markets.

The Figure 4 below highlights the three components of electricity retail price. End cus-

tomers price consist of energy, network and tax/levy components. Each of the compo-

nents can be divided into more detailed sub-components, which are also visible in Figure

4.

Figure 4 Components, sub-components and elements of consumer prices for energy [21]

Some of the cost components are easier to control and manage than others. Many de-

mand response services for example concentrate on transferring energy consumption

from expensive to cheap hours. Looking at the retail cost structure these actions only

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 25/71

address one of the three components, namely the energy part. Therefore, for the end

customer it is significantly more profitable if the storage enabled business models can

tackle also network and tax components by decreasing the overall intake from the grid.

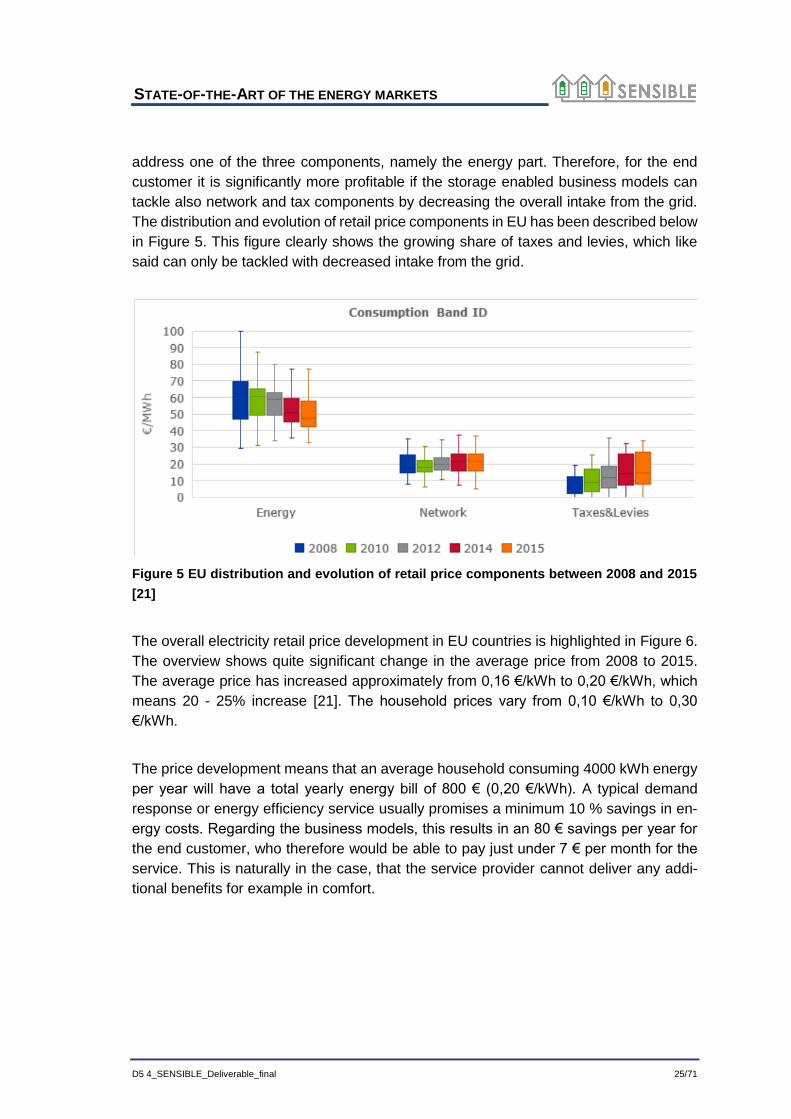

The distribution and evolution of retail price components in EU has been described below

in Figure 5. This figure clearly shows the growing share of taxes and levies, which like

said can only be tackled with decreased intake from the grid.

Figure 5 EU distribution and evolution of retail price components between 2008 and 2015

[21]

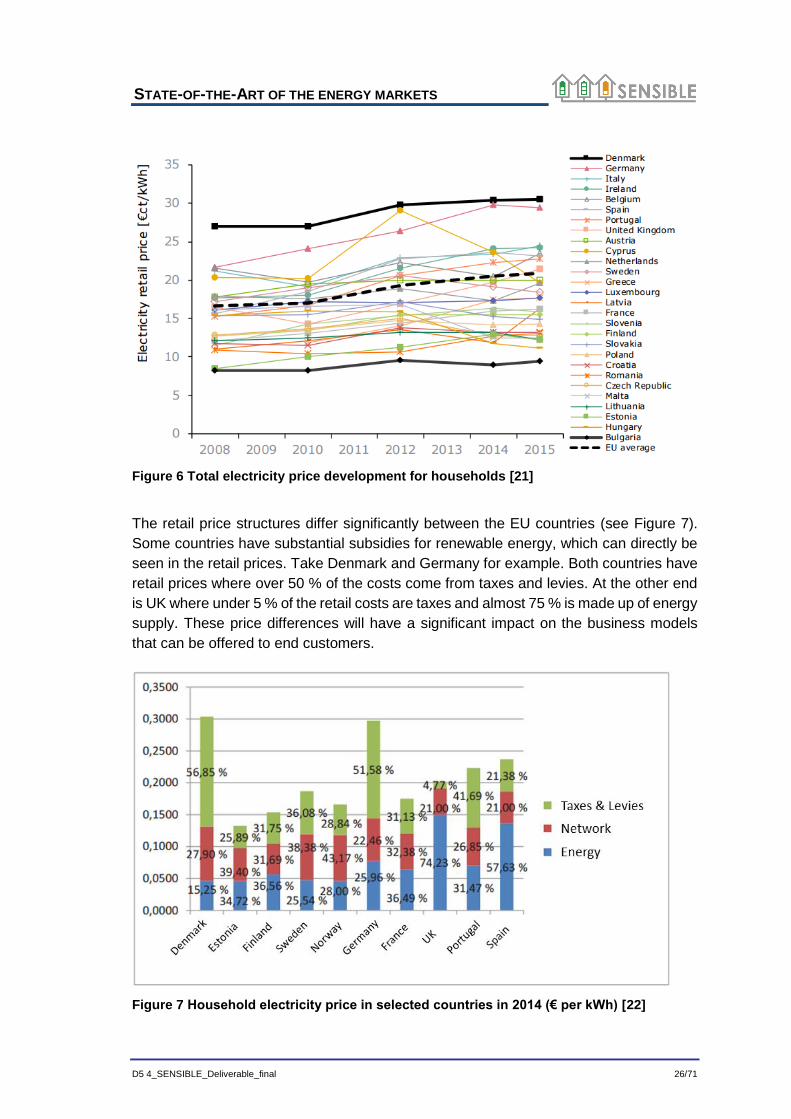

The overall electricity retail price development in EU countries is highlighted in Figure 6.

The overview shows quite significant change in the average price from 2008 to 2015.

The average price has increased approximately from 0,16 €/kWh to 0,20 €/kWh, which

means 20 - 25% increase [21]. The household prices vary from 0,10 €/kWh to 0,30

€/kWh.

The price development means that an average household consuming 4000 kWh energy

per year will have a total yearly energy bill of 800 € (0,20 €/kWh). A typical demand

response or energy efficiency service usually promises a minimum 10 % savings in en-

ergy costs. Regarding the business models, this results in an 80 € savings per year for

the end customer, who therefore would be able to pay just under 7 € per month for the

service. This is naturally in the case, that the service provider cannot deliver any addi-

tional benefits for example in comfort.

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 26/71

Figure 6 Total electricity price development for households [21]

The retail price structures differ significantly between the EU countries (see Figure 7).

Some countries have substantial subsidies for renewable energy, which can directly be

seen in the retail prices. Take Denmark and Germany for example. Both countries have

retail prices where over 50 % of the costs come from taxes and levies. At the other end

is UK where under 5 % of the retail costs are taxes and almost 75 % is made up of energy

supply. These price differences will have a significant impact on the business models

that can be offered to end customers.

Figure 7 Household electricity price in selected countries in 2014 (€ per kWh) [22]

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 27/71

In addition to household electricity prices, the storage enabled business models will have

to take into account separate prices for industrial consumers. Depending on the scope

of the business model and its key customer segments, it might be more relevant to con-

sider the prices shown in Figure 8. As with households, also the retail prices for industrial

customers have significant variance in the amount of taxes and levies [23]. Still, same

countries top the list in both household and industry energy costs. For industrial clients

in EU, the electricity prices vary roughly from 0,05 €/kWh to 0,15 €/kWh [23].

Figure 8 Electricity prices for industrial consumers, second half 2015 (EUR per kWh) [23]

2.3 Energy market in the European Union

This chapter aims to present key numbers about the electricity consumption and produc-

tion as well as electricity prices for the European Union countries. Then, a comparison

on wholesale electricity prices for the countries around Europe is performed and the his-

torical data of the last three years is depicted for each market. Furthermore, it is provided

some additional information on that markets.

2.3.1 Electricity consumption and generation in the European countries

Electricity consumption in European Union has been decreasing over the last years as it

is shown in Fehler! Verweisquelle konnte nicht gefunden werden., although a slight

increase in 2015 has been noticed. During the period from 2005 to 2014, the consump-

tion of electricity fell in the EU-28 by 6 %.

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 28/71

Figure 9 - Electricity consumption in European Union (28 countries) between 2006 and

2015. Source: Eurostat

Germany, France, United Kingdom, Italy and Spain are the countries with higher con-

sumption of electricity, although the consumption has decreased between 2006 and

2015 as well.

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 29/71

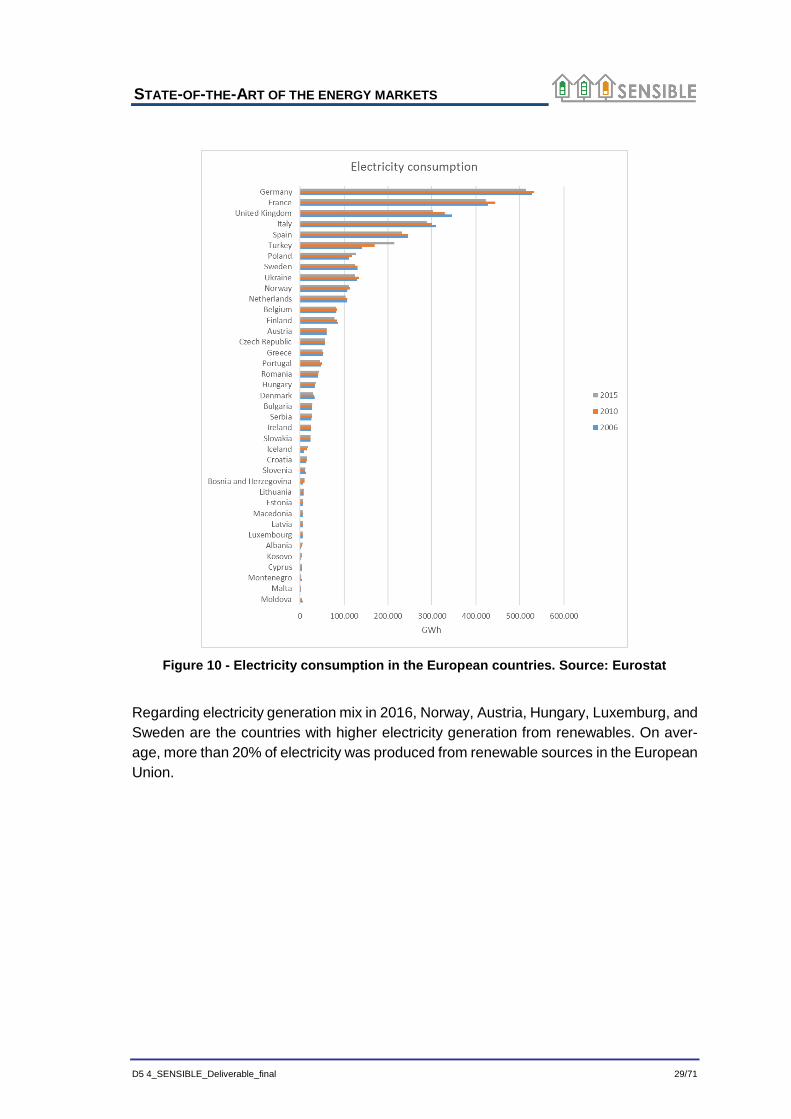

Figure 10 - Electricity consumption in the European countries. Source: Eurostat

Regarding electricity generation mix in 2016, Norway, Austria, Hungary, Luxemburg, and

Sweden are the countries with higher electricity generation from renewables. On aver-

age, more than 20% of electricity was produced from renewable sources in the European

Union.

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 30/71

Figure 11 - Breakdown of electricity production by source, 2016. Source: Eurostat.

During the second semester of 2016, the highest electricity price for households in the

European Union (28 counties) was recorded in Denmark (EUR 0.308 per kWh), followed

by Germany (EUR 0.298 per kWh) and Belgium (EUR 0.275 per kWh). On the hand,

Bulgaria (EUR 0.094 per kWh), Hungary (EUR 0.113 per kWh) and Lithuania (EUR 0.117

per kWh) were the countries with the cheapest electricity prices.

Figure 12 - Electricity prices for households in 2016 semester 2 (EUR kWh)

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 31/71

Figure 12 also demonstrate that the proportion of taxes varies widely among countries.

The lowest amount of taxes contributions is paid in Malta (4.8 %) where a low VAT rate

is applied to the basic price and no other taxes are charged to household consumers. In

opposition, in Denmark, the taxes and levies account for 67.8% of the total electricity

price paid by households.

On the other hand, if one considers the purchasing power standards (PPS)2, Portugal,

Germany, Romania and Spain are the countries where electricity presents the highest

impact on the available budget of consumers.

Figure 13 - Electricity prices for household consumers, 2015s2 (PPP kWh)

2.3.2 Wholesale electricity markets in Europe

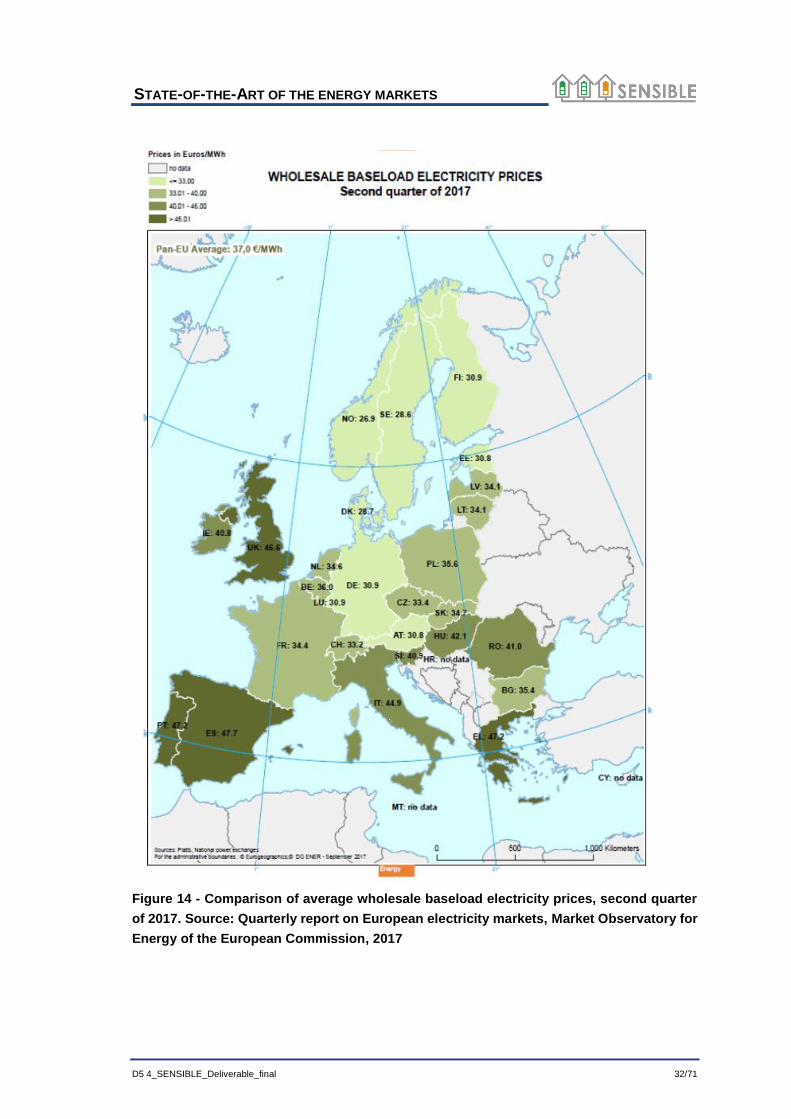

There are several wholesale electricity markets around Europe, exhibiting different rules

and prices. The map bellow depicts the price range of the wholesale baseload electricity

prices for the second quarter of 2017, where we can notice that the southern counties

such Portugal, Spain and Greece along with the UK are the ones where the wholesale

price is higher, ranging from 44,9 to 47.7€/MWh. In opposition the countries in the North

benefits from the lowest prices of the Nordpoolspot market.

2 PPS is an artificial common reference currency unit that eliminates price level differences between coun-

tries. One PPS thus buys the same given volume of goods/services in all countries (Eurostat definition).

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 32/71

Figure 14 - Comparison of average wholesale baseload electricity prices, second quarter

of 2017. Source: Quarterly report on European electricity markets, Market Observatory for

Energy of the European Commission, 2017

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 33/71

In the following sections, a more detail information about the electricity prices in the most

relevant European wholesale markets is presented as well as some details about its

functioning.

2.3.2.1 Central Western Europe (Austria, Belgium, France, Germany, the Nether-

lands, Switzerland)

One of the most important market in Europe is the EPEX SPOT3, which covers France,

Germany, Austria and Switzerland and it accounts for more than one third of the Euro-

pean power consumption.

EPEX SPOT is 100% owner of APX Group, operator of the spot power markets in the

Netherlands (APX Power NL), Belgium (Belpex) and in the United Kingdom (UKPX).

Figure 15 - Monthly traded volumes and prices in Central Western Europe. Source: Market

observatory for Energy of the European Commission

The CEW prices typically ranges between around 25 and 40 €/MWh, except during the

last months of 2016/ first month of 2017 mainly to weather conditions (colder tempera-

tures and low wind). Typically, the price goes down during summer and reach higher

values during the winter.

For the EPEX day-ahead market, a daily blind auction occurs once a day, 365 days a

year. There is a floor price of 500€/MWh and a cap price of 3000€/MWh. The publication

time is as soon as possible from 12.42 pm CET for all markets but Switzerland, where it

should be as soon as possible from 11.10 am CET. The order book opens 45 days in

3 http://www.epexspot.com/en/company-info/about_epex_spot

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 34/71

advance for France, Germany, Austria and Switzerland, 14 days for Netherlands, Bel-

gium and UK and closes one day before delivery at 12 pm CET (all markets but Switzer-

land, where it closes at 11 am.

Regarding the intraday market, it is divided into continuous and auction trading. The cap

and floor prices are the same as the intraday.

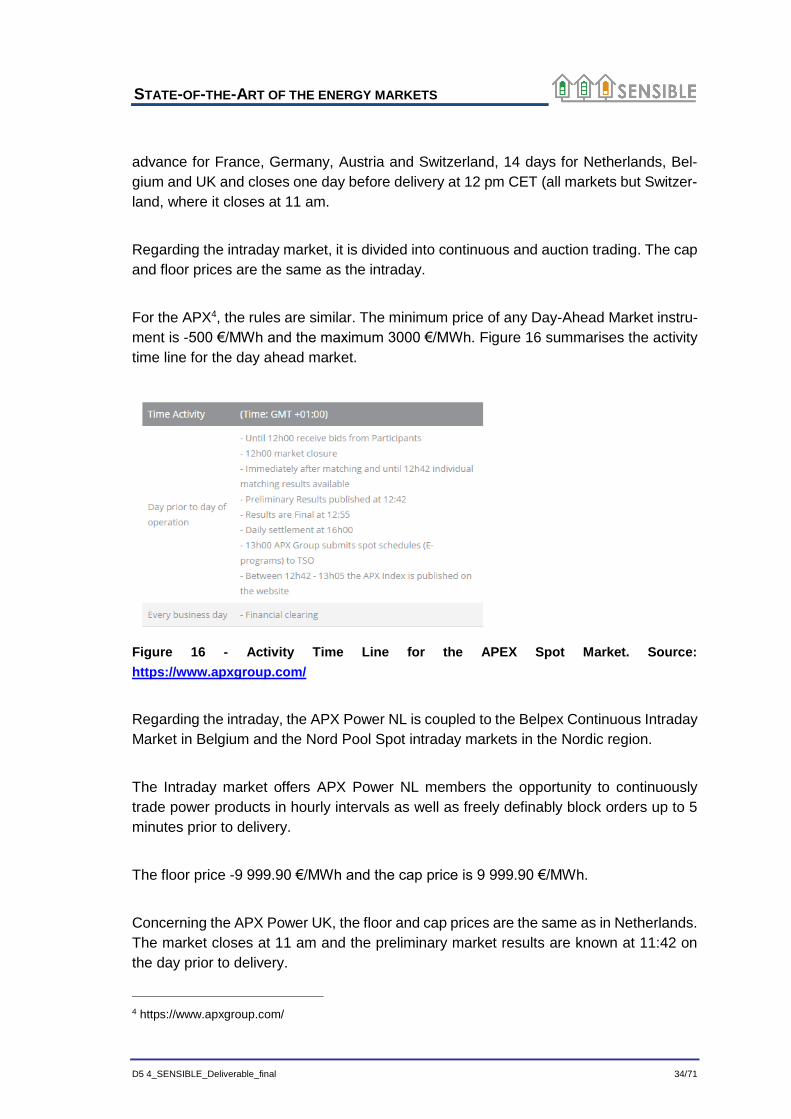

For the APX4, the rules are similar. The minimum price of any Day-Ahead Market instru-

ment is -500 €/MWh and the maximum 3000 €/MWh. Figure 16 summarises the activity

time line for the day ahead market.

Figure 16 - Activity Time Line for the APEX Spot Market. Source:

https://www.apxgroup.com/

Regarding the intraday, the APX Power NL is coupled to the Belpex Continuous Intraday

Market in Belgium and the Nord Pool Spot intraday markets in the Nordic region.

The Intraday market offers APX Power NL members the opportunity to continuously

trade power products in hourly intervals as well as freely definably block orders up to 5

minutes prior to delivery.

The floor price -9 999.90 €/MWh and the cap price is 9 999.90 €/MWh.

Concerning the APX Power UK, the floor and cap prices are the same as in Netherlands.

The market closes at 11 am and the preliminary market results are known at 11:42 on

the day prior to delivery.

4 https://www.apxgroup.com/

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 35/71

In addition, the market members at UK have also the opportunity to submit half hour bids

in a local Day-Ahead auction (double-sided blind auction) at 15:30 and the market results

are published 30 minutes later.

The physical power exchange for Belgium is the Belpex5 and the Day-Ahead market is

coupled with APX in the Netherlands and EPEX Spot in France and Germany. The order

books close at 12:00 and the results are published under normal circumstances no later

than 13:05. As for the other APX countries, the floor price is -500 €/MWh and the cap

price is 3000 €/MWh, whereas for the intraday the prices are between -9999.99 and

9999.99 €/MWh.

2.3.2.2 British Isles (UK, Ireland)

Figure 17 - Monthly electricity exchange traded volumes and average day-ahead wholesale

baseload prices in the UK and Ireland. Source: Market observatory for Energy of the Euro-

pean Commission

The monthly average price in the UK and Ireland ranges between around 35 and

70€/MWh over the last three years. More recently, in the autumn of 2016, the prices

increased rapidly but in the beginning of the 2017 the trend was reversed and currently

the prices continue to going down after the end of the heating season.

5 https://www.belpex.be/

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 36/71

As explained above, the UK market is operated by the APX power spot exchange, spe-

cifically by the APX Power UK. The floor and cap prices are the same as in the APEX

countries (-500€/MWh and 3000€/MWH, respectively). The market closes at 11 am and

the preliminary market results are known at 11:42 on the day prior to delivery.

The wholesale electricity market in Ireland and North Ireland is the Single Electricity Mar-

ket6 (SEM), which operates with dual currencies and in multiple jurisdictions, being the

first market of its kind in the world. In this case, the floor price was set at -100€/MWH

and cap price was set at 1000€/MWh.

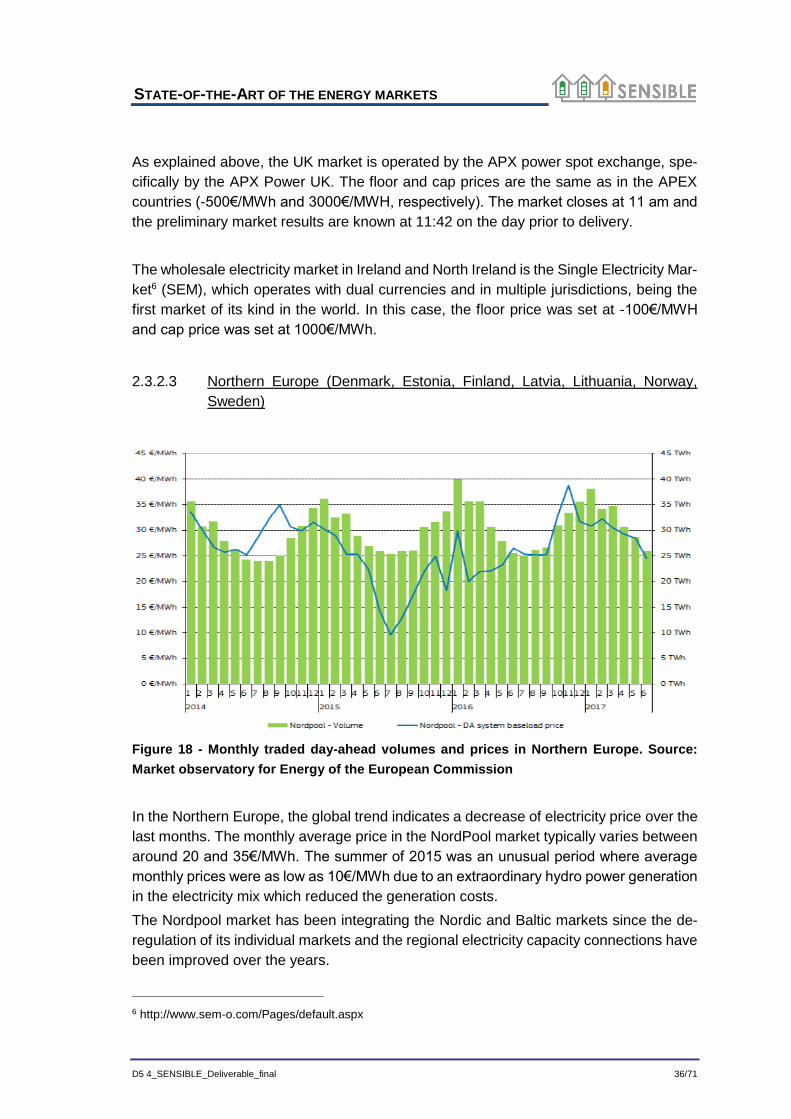

2.3.2.3 Northern Europe (Denmark, Estonia, Finland, Latvia, Lithuania, Norway,

Sweden)

Figure 18 - Monthly traded day-ahead volumes and prices in Northern Europe. Source:

Market observatory for Energy of the European Commission

In the Northern Europe, the global trend indicates a decrease of electricity price over the

last months. The monthly average price in the NordPool market typically varies between

around 20 and 35€/MWh. The summer of 2015 was an unusual period where average

monthly prices were as low as 10€/MWh due to an extraordinary hydro power generation

in the electricity mix which reduced the generation costs.

The Nordpool market has been integrating the Nordic and Baltic markets since the de-

regulation of its individual markets and the regional electricity capacity connections have

been improved over the years.

6 http://www.sem-o.com/Pages/default.aspx

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 37/71

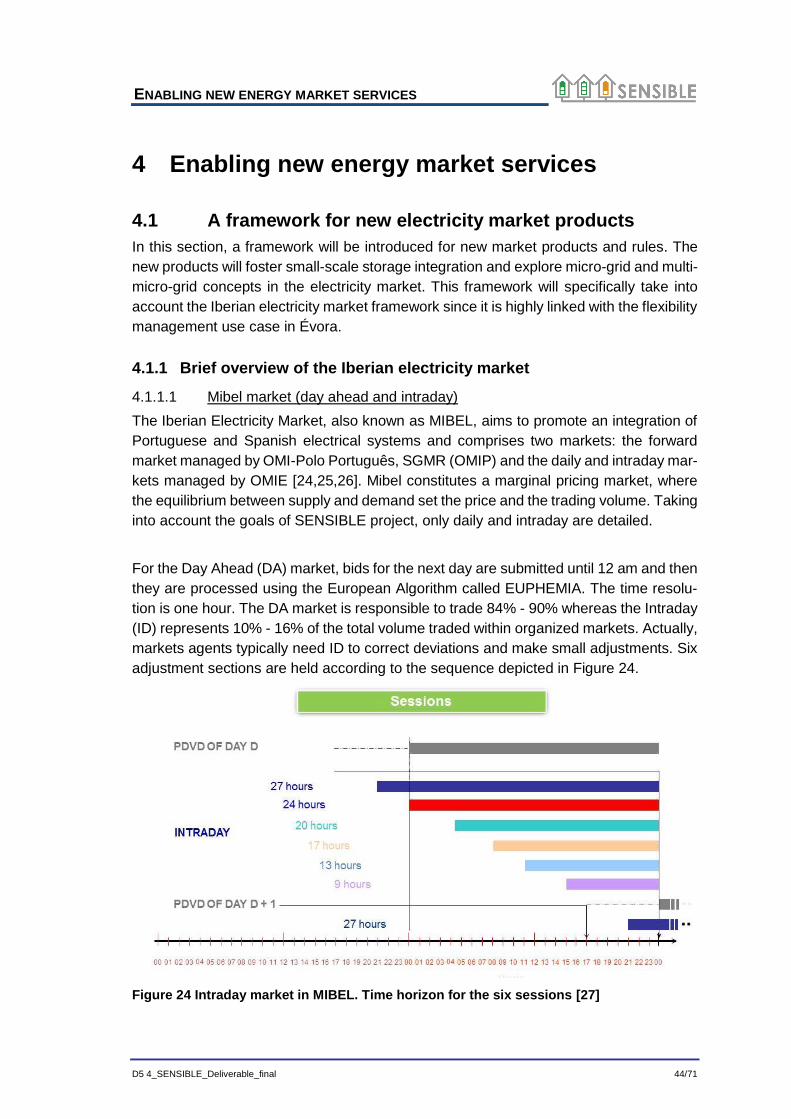

For the day ahead market, bids have to be submitted until 12:00 CET and the hourly

prices are typically announced at 12:42 CET. Regarding the intraday market, it embraces

not only the Nordic and Baltic countries, but also the UK and German markets.

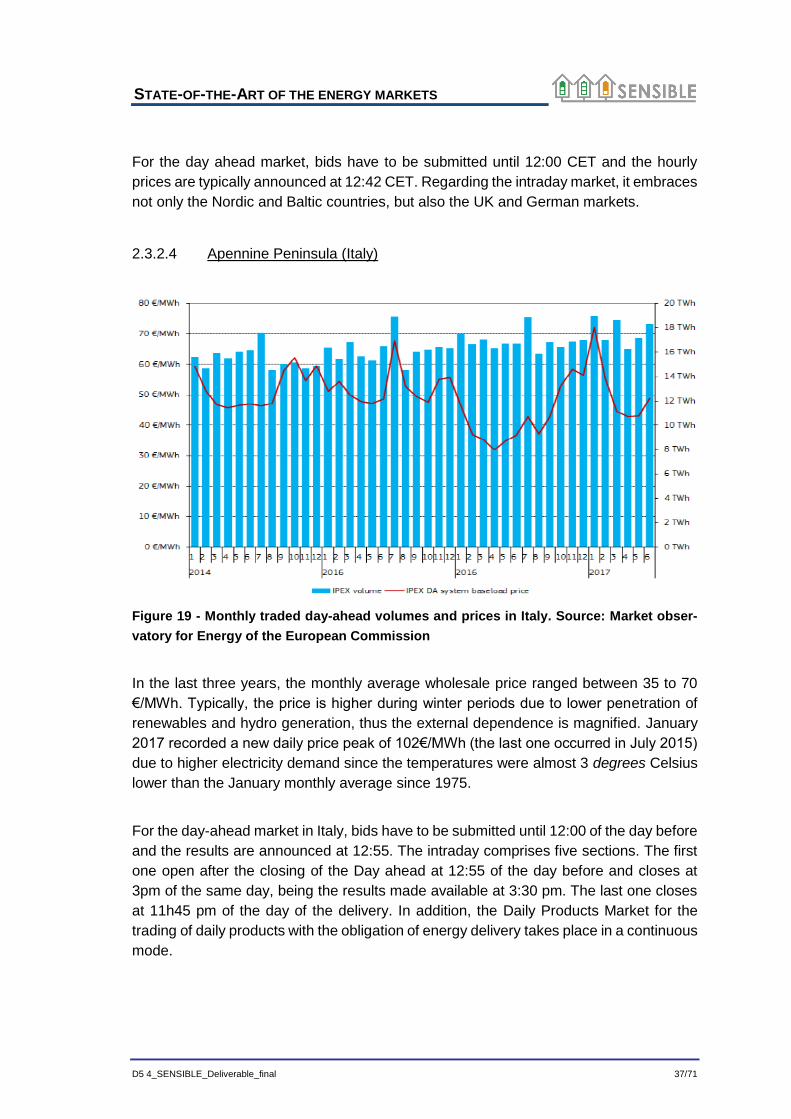

2.3.2.4 Apennine Peninsula (Italy)

Figure 19 - Monthly traded day-ahead volumes and prices in Italy. Source: Market obser-

vatory for Energy of the European Commission

In the last three years, the monthly average wholesale price ranged between 35 to 70

€/MWh. Typically, the price is higher during winter periods due to lower penetration of

renewables and hydro generation, thus the external dependence is magnified. January

2017 recorded a new daily price peak of 102€/MWh (the last one occurred in July 2015)

due to higher electricity demand since the temperatures were almost 3 degrees Celsius

lower than the January monthly average since 1975.

For the day-ahead market in Italy, bids have to be submitted until 12:00 of the day before

and the results are announced at 12:55. The intraday comprises five sections. The first

one open after the closing of the Day ahead at 12:55 of the day before and closes at

3pm of the same day, being the results made available at 3:30 pm. The last one closes

at 11h45 pm of the day of the delivery. In addition, the Daily Products Market for the

trading of daily products with the obligation of energy delivery takes place in a continuous

mode.

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 38/71

2.3.2.5 Iberian Peninsula (Spain and Portugal)

Figure 20 - Monthly electricity exchange traded volumes and average day-ahead prices in

the Iberian Peninsula. Source: Market observatory for Energy of the European Commis-

sion

Over the last three years, the monthly average wholesale electricity prices were usually

around between 40 and 60 €/MWh, with the exception of the two periods well stressed

in Figure 20 in 2014 and 2016, where the prices drop significantly. During the first months

of 2016, the prices started to shrink due to the rainy season which potentiated the hydro-

power generation. In addition, in the beginning of 2017 the prices rose above 60€/MWh

and reached the 75€/MWh due to higher domestic generation costs and less imports

from the CWE region.

OMIE7 manages the spot market on the Iberian Peninsula 365 days a year. Electricity

cannot be sold at negative values and the cap price is 180€/MWh, much lower than the

highest price allowed in the other European markets. OMIE encompasses the Day-

ahead and the intraday markets, although around 90% of energy is traded within the DA.

Bids have to be submitted until 12:00 for the day-ahead while the intraday market com-

prises six sessions closing at 18:45 (D-1), 21:45 (D-1), 01:45, 04:45, 08:45 and 12:45.

7 http://www.omie.es/en/inicio

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 39/71

2.3.2.6 Central Eastern Europe (Czech Republic, Hungary, Poland, Romania, Slo-

vakia, Slovenia)

Figure 21 - Monthly traded day-ahead volumes and prices in Central Eastern Europe.

Source: Market observatory for Energy of the European Commission

The monthly average baseload price in Central and Eastern Europe (CEE) over the last

three years is being quite stable, ranging mainly between 30 to 40€/MWh. The prices in

January 2017 were higher than usual due to higher pressure on the electric system be-

cause of lower temperatures (10 degrees Celsius lower compared to the normal long-

term average).

The day-ahead markets between the Czech Republic, Slovakia and Hungary are cou-pled since 2012, which improved the price stability in the region and the price conver-gence towards regional markets (it increased from 11% to 82% after market coupling in September 2012). In 2014, the Romanian DA started functioning in coupling mode as well.

The TGE (Polish power Exchanger) operates the market on Poland and the BSP Re-

gional Energy Exchange operates the wholesale market in Slovenia.

STATE-OF-THE-ART OF THE ENERGY MARKETS

D5 4_SENSIBLE_Deliverable_final 40/71

2.3.2.7 South Eastern Europe (Greece and Bulgaria)

Figure 22 - Monthly traded day-ahead volumes and prices in Greece and Bulgaria. Source:

Market observatory for Energy of the European Commission

Over the last months, the monthly day-ahead price in Greece was around 50€/MWh,

although in the first quarter of 2015 the prices rose up to about 60€/MWh and in the first

quarter of 2016 the prices shrunk to 40€/MWh. The weather conditions, similarly to the

other countries in Central Europe, were responsible for the higher prices in January

2017. The price in Bulgaria follow the same trend, however it is roughly 10€/MWh

cheaper.

The Hellenic Electricity Market Operator, LAGIE8, is the Day-Ahead Mandatory Pool in

which energy and ancillary services are simultaneously traded and are dispatched on

the available units. The price cap for the energy offers is €150/MWh. Regarding IBEX9,

the Independent Bulgarian Energy Exchange, it was established January 2014, as a

fully-owned subsidiary of the Bulgarian Energy Holding EAD.

8 http://www.lagie.gr/nc/en/home/

9 http://www.ibex.bg/en/

BUSINESS MODEL FRAMEWORK OVERVIEW

D5 4_SENSIBLE_Deliverable_final 41/71

3 Business model framework overview

3.1 Framework overview

In D5.1 Storage enabled energy business model framework for demonstration separate

business models were prepared for each project use case. The business models were

prepared based on the Business Model Canvas approach, which consist of nine key

components that are crucial in every business model. These components have been

described below in the Figure 23.

Figure 23 Business model framework template

The SENSIBLE project includes 11 use cases, which are distributed among the three

demonstrators. Therefore, also the business model framework includes 11 separate

business models which are analyzed based on their unique value propositions and re-

quirements. The main goal for the business model framework was to identify all the key

customer segments and stakeholders but also to define the key value propositions for

each demonstrator. Below in Table 6 are described the main scopes or value proposi-

tions of the business models. As it can be seen, balancing demand and supply is a sig-

nificant topic for majority of the use cases. This affects also how the business model

interaction with the energy markets is analyzed in this deliverable.

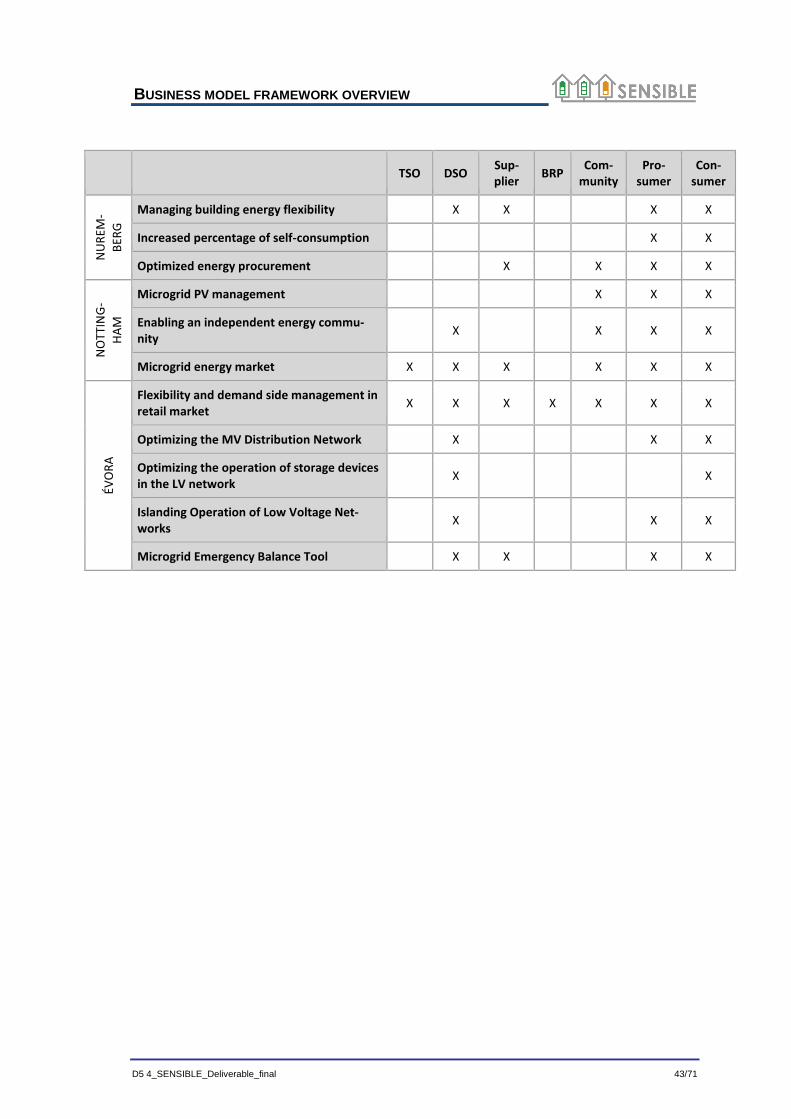

Table 6 Scopes of the SENSIBLE business models

BUSINESS MODEL FRAMEWORK OVERVIEW

D5 4_SENSIBLE_Deliverable_final 42/71

Balancing demand and supply

Grid manage-ment

Energy efficiency

NU

REM

BER

G Managing building energy flexibility X X

Increased percentage of self-con-sumption

X

Optimized energy procurement X X

NO

TTIN

G-

HA

M

Microgrid PV management X X

Enabling an independent energy community

X X

Microgrid energy market X

EVO

RA

Flexibility and demand side manage-ment in retail market

X X

Optimizing the MV Distribution Net-work

X

Optimizing the operation of storage devices in the LV network

X X

Islanding Operation of Low Voltage Networks

X X

Microgrid Emergency Balance Tool X X

3.2 Overview of the stakeholders

The key customer segments of the business models have been highlighted in Table 7.

The customer segments clearly show the scopes of the demonstrators but also how they