september 7, 2015 mp: ₹99 time horizon 12 months target: … · its network of 1500...

TRANSCRIPT

Anand Rathi Research

Time Horizon – 12 Months

September 7, 2015

Jun-15 Mar-15 Dec-14 Sep-14

Promoters 75.0% 75.0% 75.0% 75.0%

FII 0.5% 1.5% 2.8% 3.2%

DII 0.3% 0.0% 0.0% 0.0%

Bodies Corporate 4.0% 3.6% 3.3% 3.2%

Others 20.3% 20.0% 18.9% 18.6%

Total 100% 100% 100% 100%

Source: Company, Anand Rathi Research, Bloomberg

V

A

L

U

E

P

I

C

k

(In ₹ Mn.) FY14 FY15 FY16E FY17E

Net Sales 4,704 5,439 6,391 7,620

EBITDA 26 168 304 495

EBITDA Margin 0.6% 3.1% 4.8% 6.5%

EPS (₹) (0.8) 0.5 1.1 2.5

EV/Sales 2.1 1.8 1.6 1.3

EV/EBITDA 383.6 59.9 33.1 20.3

P/E (x) (128.1) 198.3 87.4 39.9

Price Performance CY12 CY13 CY14 YTD

Absolute 54% -28% 76% 67%

Relative 26% -35% 45% 72%

Analyst: Narendra [email protected]

Relative stock performance (Sep’14=100)

CMP: ₹99

Target: ₹135

Shareholding Pattern (as on Jun’15)

Key Data

Bloomberg Code CAMLN IN

NSE Code KOKUYOCMLN

BSE Code 523207

Sector Cons. Discretionary

Industry Home & Office Prod.

Face Value (₹) 1.0

BV per share (₹) 21

Dividend Yield (%) 0.0%

52 Week L/H(₹) 50 / 127

Market Cap. (₹ mn.) 9,965

Kokuyo Camlin Limited (CAMLN)

65

100

135

170

205

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

CAMLN Nifty

2 Anand Rathi Research

Kokuyo Camlin Limited is over 80 years old company started in 1930s as Dandekar & Co. which got renamed as Camlin during 1941.Over the years, the Company has become synonymous with quality products for schools, offices and niche art markets. The Companyhas two of the most recognized and endearing brands in the country – CAMEL and CAMLIN.

In 2012, Kokuyo S & T Ltd. Japan acquired majority stake in Camlin and rechristened the company as Kokuyo Camlin Limited. Kokuyo isa Japan based company with more than 100 years old history. It is a leading marketer in stationery, institutional furniture and cataloguesales and has presence in many countries in Asia.

The vast range of products manufactured and marketed by the Company include inks, colors, writing instruments, technical anddrawing instruments, office stationery, markers, fine art, notebooks and scholastic and hobby art materials.

During the latest financial year 2015 the company has reported a growth of 15.6% in its revenues at ₹5,439 million as against ₹4,704million in FY14. The growth was mainly due to increase both volume and realizations of certain products.

Its EBITDA margins improved 250 basis points to 3.1% in FY15 at ₹168 million as against 0.6% in FY14 at ₹26 million and PAT margins

improved 260 basis points to 0.9% at ₹49 million in FY15. The overall improvement in profitability of the company was due to lower

cost of materials owing to product mix, decrease in cost of operation.

In 2013, the company has embarked upon an ambitious mission to build up its capacities, capabilities and competencies and had

raised funds for construction of state of the art manufacturing plant at Patalganga Industrial Area of MIDC. The construction has

already started in January 2015 and management expects this plant to be operational by 2016.

Kokuyo (parent) is continuously streamlining its Indian operations and has implemented various systems to improve operational andmanufacturing competitiveness of the company. It is now focusing on introducing new and innovative products to the market throughits network of 1500 dealers/distributors and 300000 retailers. In past it is has introduced Kokuyo notebooks in the Indian markets withremarkable success.

We expect CAMLN to further improve its profitability in years to come and continue to grow its business through its existing productfranchise as well as launch of new innovative products from its parent company.

We initiate our coverage on Kokuyo Camlin Limited with a BUY rating and a target price of ₹135 per share.

Two of the oldest brands ‘Kokuyo’ & ‘Camlin/Camel’ with unmatched consumer connect, strong brand equity

Kokuyo Camlin Limited (CAMLN)

3 Anand Rathi Research

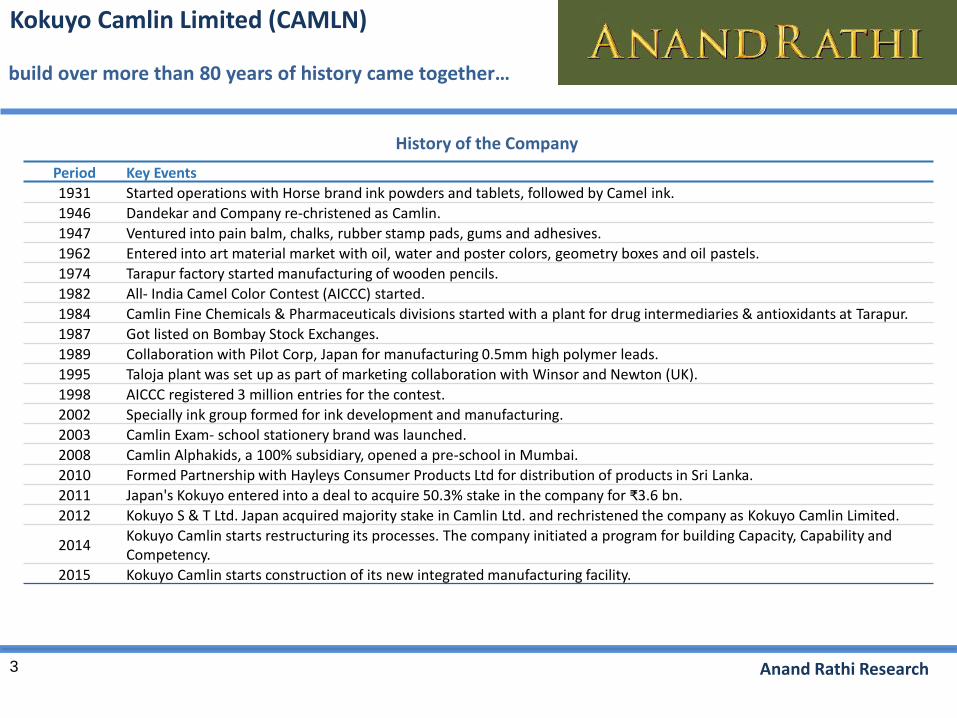

build over more than 80 years of history came together…

History of the Company

Period Key Events

1931 Started operations with Horse brand ink powders and tablets, followed by Camel ink.

1946 Dandekar and Company re-christened as Camlin.

1947 Ventured into pain balm, chalks, rubber stamp pads, gums and adhesives.

1962 Entered into art material market with oil, water and poster colors, geometry boxes and oil pastels.

1974 Tarapur factory started manufacturing of wooden pencils.

1982 All- India Camel Color Contest (AICCC) started.

1984 Camlin Fine Chemicals & Pharmaceuticals divisions started with a plant for drug intermediaries & antioxidants at Tarapur.

1987 Got listed on Bombay Stock Exchanges.

1989 Collaboration with Pilot Corp, Japan for manufacturing 0.5mm high polymer leads.

1995 Taloja plant was set up as part of marketing collaboration with Winsor and Newton (UK).

1998 AICCC registered 3 million entries for the contest.

2002 Specially ink group formed for ink development and manufacturing.

2003 Camlin Exam- school stationery brand was launched.

2008 Camlin Alphakids, a 100% subsidiary, opened a pre-school in Mumbai.

2010 Formed Partnership with Hayleys Consumer Products Ltd for distribution of products in Sri Lanka.

2011 Japan's Kokuyo entered into a deal to acquire 50.3% stake in the company for ₹3.6 bn.

2012 Kokuyo S & T Ltd. Japan acquired majority stake in Camlin Ltd. and rechristened the company as Kokuyo Camlin Limited.

2014Kokuyo Camlin starts restructuring its processes. The company initiated a program for building Capacity, Capability and Competency.

2015 Kokuyo Camlin starts construction of its new integrated manufacturing facility.

Kokuyo Camlin Limited (CAMLN)

4 Anand Rathi Research

…with extensive product portfolio of over 2500 SKUs that address the wide & varied needs of its three broad segments.

CAMLN Business Segment Products Wise

School & Education products

Fine Art & Hobby Materials Office Stationery products

Notebooks

Drawing Books

Pencils & Pens

Fountain Pen & Ink

Color Pencils

Sketch Pens

Plastic/Wax Crayons

Water Colors

Poster Colors

Oil Pastels

Geometry Box

Technical Instruments, etc

Art Materials

Art Pastels

Artists Oil Colors

Artists Acrylic Colors

Canvas & Brushes

Painting Medium

Water Color pencils

3D Glitter, Sparkle

Fabrica Coneliner

Hobby Mediums &

Brushes, Others

Gum & Paste

Markers & Marker Inks

Scissors

Staplers

Other Office Products

Accessories

Kokuyo Camlin Limited (CAMLN)

5 Anand Rathi Research

Broad segmentation of stationery industry by type and use.

Stationery Segmentation by Type Stationery Segmentation by Use

Notebook & Paper

Computer & Daily use

School Stationery Office StationeryWriting Instruments

Stationery industry includes a wide range of paper products, writing instruments, computer and daily used

stationery like staplers, erasers, binders, punch machine, children stationery and other related items.

Global market for Writing and Marking Instruments is projected to reach US$17.5 billion by 2020, driven by product

innovations, growing penchant for luxury writing instruments and increasing literacy rates in emerging countries.

Asia-Pacific represents the largest and the fastest growing market worldwide with a CAGR of 7% over the analysis

period. Growth in the region is led by increased emphasis on education, large base of students and corporates, and

growing demand for quality writing gear.

Kokuyo Camlin Limited (CAMLN)

6 Anand Rathi Research

India stationery segment market size

Segment - Products wise market

The Indian stationery industry is very heterogeneous comprising of a wide array of products ranging from pens to

printing to notepads to inks to colors and many more.

The industry is highly fragmented one, with the unorganized sector constituting almost 85%. The industry is also highly

fragmented in terms of regions, with a large number of small units scattered all over the country.

In terms of usage, the industry is broadly divided into office stationery and school stationery of which school stationery

market is estimated to be around ₹90 billion while office stationery market is estimated to be around ₹50 billion.

On product wise segmentation, Notebook & Paper products contributes around 51% while Writing Instruments and

Computer and Daily use contributes 25% and 24% respectively.

Source: Company, Anand Rathi Research

Computer & Daily use

24%

Writing Instruments

25%

Notebooks & Paper51%

Stationery Industry segment Market size (₹ Bn.)

School Stationary,

90

Office Stationary,

50

Kokuyo Camlin Limited (CAMLN)

Source: Company, Anand Rathi Research

7 Anand Rathi Research

Demographic trends supportive of stationery market in India…

Kokuyo Camlin Limited (CAMLN)

0%

25%

50%

75%

100%

2005 2025

Food, Beverages & Tobacco Apparel Housing Utilities

Household Products Personal products & Services Transportation

Communication Education & Recreation Healthcare

Necessities (47%)

Discretionary Expenses

(53%)

Necessities (30%)

Discretionary Expenses

(70%)

Demographic trends for share of

average household consumption:

Rising discretionary

expenditure.

High probability of premium

purchases.

Rise in the average household

income.

India with its rapidly burgeoning economy is underpinning growth for the office stationery market. A growing

middle-class coupled with higher government spends on education is driving growth in the school and education

segments.

Households that can afford discretionary spending is likely to go up to 94 million by 2025 from present around 10

million with its middle class growing from ~50 million to 583 million by 2025.

India is one of the fastest rising market in the world with a huge potential to tap as its current stationery market

is highly un organized and fragmented.

Source: Mckinsey, Anand Rathi Research

8 Anand Rathi Research

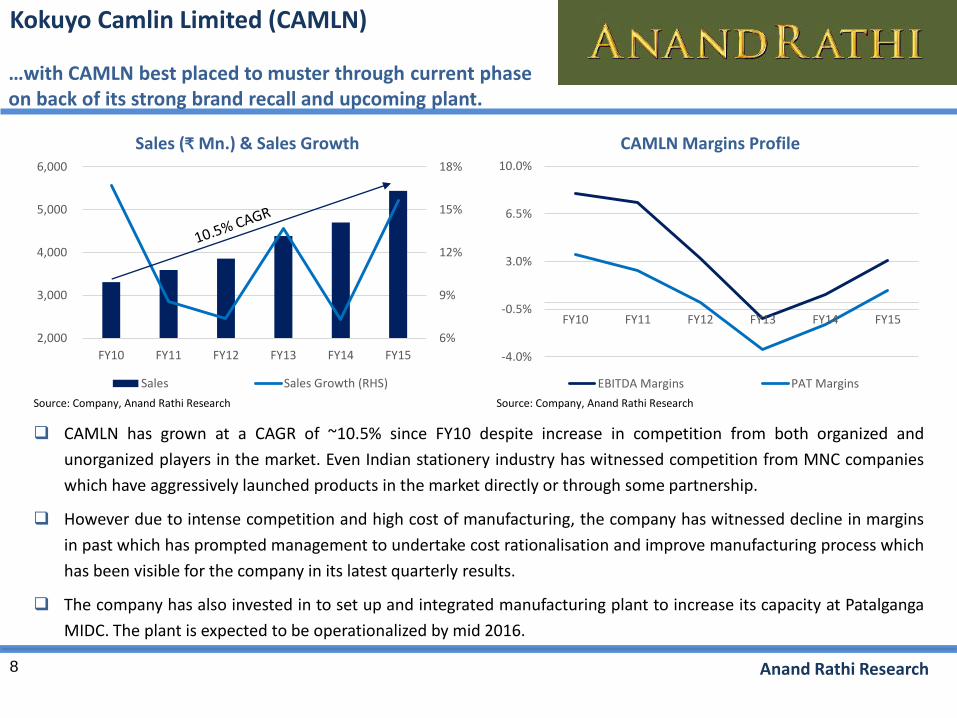

…with CAMLN best placed to muster through current phase on back of its strong brand recall and upcoming plant.

Sales (₹ Mn.) & Sales Growth

CAMLN has grown at a CAGR of ~10.5% since FY10 despite increase in competition from both organized and

unorganized players in the market. Even Indian stationery industry has witnessed competition from MNC companies

which have aggressively launched products in the market directly or through some partnership.

However due to intense competition and high cost of manufacturing, the company has witnessed decline in margins

in past which has prompted management to undertake cost rationalisation and improve manufacturing process which

has been visible for the company in its latest quarterly results.

The company has also invested in to set up and integrated manufacturing plant to increase its capacity at Patalganga

MIDC. The plant is expected to be operationalized by mid 2016.

Source: Company, Anand Rathi Research

6%

9%

12%

15%

18%

2,000

3,000

4,000

5,000

6,000

FY10 FY11 FY12 FY13 FY14 FY15

Sales Sales Growth (RHS)

CAMLN Margins Profile

-4.0%

-0.5%

3.0%

6.5%

10.0%

FY10 FY11 FY12 FY13 FY14 FY15

EBITDA Margins PAT Margins

Kokuyo Camlin Limited (CAMLN)

Source: Company, Anand Rathi Research

9 Anand Rathi Research

Which is expected to drive operating margins higher for the company

Sales (₹ Mn.) & EBITDA Margins projections

We expect CAMLN to grow its revenues at a CAGR of 18% in next few years on back of improved market

conditions for Indian stationery market which is fuelled by industrial growth and expansion in the education

sector., rising literacy rates, greater organized retailing and increasing income levels.

On profitability front, we expect company to continue to improve its profitability due to efficiency in

operations, reduction in raw materials cost in the short run while positive operating leverage due to its new

integrated manufacturing facility coming online in medium to long run.

Source: Company, Anand Rathi Research

-2.5%

0.0%

2.5%

5.0%

7.5%

2,000

3,500

5,000

6,500

8,000

FY13 FY14 FY15 FY16E FY17E

Sales (₹ Mn.) EBITDA Margin (RHS)

Kokuyo Camlin Limited (CAMLN)

10 Anand Rathi Research

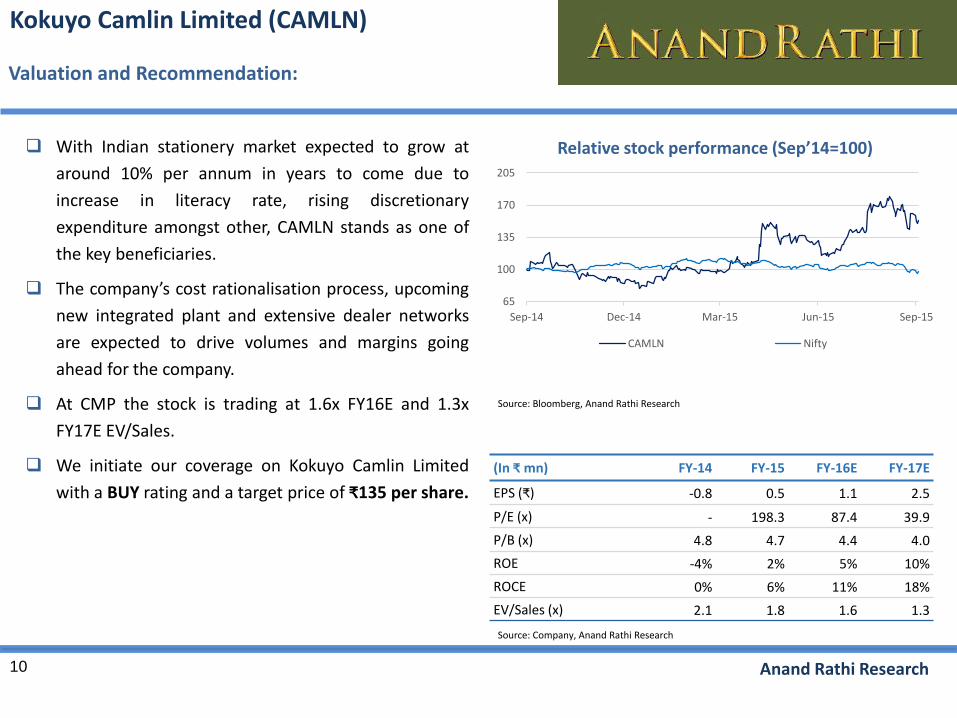

With Indian stationery market expected to grow at

around 10% per annum in years to come due to

increase in literacy rate, rising discretionary

expenditure amongst other, CAMLN stands as one of

the key beneficiaries.

The company’s cost rationalisation process, upcoming

new integrated plant and extensive dealer networks

are expected to drive volumes and margins going

ahead for the company.

At CMP the stock is trading at 1.6x FY16E and 1.3x

FY17E EV/Sales.

We initiate our coverage on Kokuyo Camlin Limited

with a BUY rating and a target price of ₹135 per share.

Relative stock performance (Sep’14=100)

Valuation and Recommendation:

Source: Bloomberg, Anand Rathi Research

Source: Company, Anand Rathi Research

(In ₹ mn) FY-14 FY-15 FY-16E FY-17E

EPS (₹) -0.8 0.5 1.1 2.5

P/E (x) - 198.3 87.4 39.9

P/B (x) 4.8 4.7 4.4 4.0

ROE -4% 2% 5% 10%

ROCE 0% 6% 11% 18%

EV/Sales (x) 2.1 1.8 1.6 1.3

65

100

135

170

205

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

CAMLN Nifty

Kokuyo Camlin Limited (CAMLN)

11 Anand Rathi Research

Margins FY-14 FY-15 FY-16E FY-17E

Sales Growth % 7.3% 15.6% 17.5% 19.2%

Operating Margin % 0.6% 3.1% 4.8% 6.5%

Net Margin % -1.7% 0.9% 1.8% 3.4%

Consolidated Financials:

Source: Company, Anand Rathi Research

(In ₹ Mn.) FY-14 FY-15 FY-16E FY-17E

Liabilities

Equity Share Capital 100 100 100 100

Reserves & Surplus 1,987 2,035 2,149 2,407

Long-Term Liabilities 131 88 88 (12)

Other Long-term Liabilities (65) (69) (69) (69)

Deferred Tax Liability 108 141 141 141

Short-term Liabilities 1,611 1,819 2,095 2,455

Total 3,872 4,114 4,504 5,023

Assets

Net Fixed Assets 852 1,084 1,028 1,112

Long-Term L&A 256 135 135 135

Other Non-Current Assets 5 6 6 6

Current Asset 2 2 2 2

Total 2,757 2,888 3,333 3,768

(In ₹ Mn.) FY-14 FY-15 FY-16E FY-17E

Net Sales 4,704 5,439 6,391 7,620

Operating Expense 4,677 5,271 6,087 7,125

EBITDA 26 168 304 495

Other Income 58 82 80 95

Depreciation 89 110 110 122

EBIT (4) 141 274 469

Interest 88 98 104 100

Misc. items - - - -

PBT (92) 43 170 368

Tax (14) (6) 56 111

PAT (78) 49 114 258

Kokuyo Camlin Limited (CAMLN)

12 Anand Rathi Research

As unorganised players account for almost 80% of the market and failure of CAMLN in executing its strategy may impact

its profitability negatively.

The company’s raw materials are crude oil derivatives and any significant volatility in crude prices may impact margins

negatively for the company.

Key Risks:

Kokuyo Camlin Limited (CAMLN)

13 Anand Rathi Research

Rating and Target Price history:

Date Rating Target Price (₹) Share Price (₹)

07-Sep-15 BUY 99 135

CAMLN rating detailsCAMLN rating history & price chart

Source: Bloomberg, Anand Rathi Research Source: Bloomberg, Anand Rathi Research

NOTE: Prices are as on 04th Sep 2015 close.

65

100

135

170

205

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

Kokuyo Camlin Limited (CAMLN)

14 Anand Rathi Research

Disclaimer:

Research Disclaimer and Disclosure inter-alia as required under Securities and Exchange Board of India (Research Analysts) Regulations, 2014

Anand Rathi Share and Stock Brokers Ltd. (hereinafter refer as ARSSBL) (Research Entity, SEBI Regn No. INH000000834, Date of Regn. 29/06/2015) is a subsidiary of the

Anand Rathi Financial Services Ltd. ARSSBL is a corporate trading and clearing member of Bombay Stock Exchange Ltd, National Stock Exchange of India Ltd. (NSEIL),

Multi Stock Exchange of India Ltd (MCX-SX), United stock exchange and also depository participant with National Securities Depository Ltd (NSDL) and Central

Depository Services Ltd. ARSSBL is engaged into the business of Stock Broking, Depository Participant, Mutual Fund distributor.

The research analysts, strategists, or research associates principally responsible for the preparation of Anand Rathi Research have received compensation based upon

various factors, including quality of research, investor client feedback, stock picking, competitive factors, firm revenues.

General Disclaimer: - This Research Report (hereinafter called “Report”) is meant solely for use by the recipient and is not for circulation. This Report does not

constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. The

recommendations, if any, made herein are expression of views and/or opinions and should not be deemed or construed to be neither advice for the purpose of

purchase or sale of any security, derivatives or any other security through ARSSBL nor any solicitation or offering of any investment /trading opportunity on behalf of

the issuer(s) of the respective security (ies) referred to herein. These information / opinions / views are not meant to serve as a professional investment guide for the

readers. No action is solicited based upon the information provided herein. Recipients of this Report should rely on information/data arising out of their own

investigations. Readers are advised to seek independent professional advice and arrive at an informed trading/investment decision before executing any trades or

making any investments. This Report has been prepared on the basis of publicly available information, internally developed data and other sources believed by ARSSBL

to be reliable. ARSSBL or its directors, employees, affiliates or representatives do not assume any responsibility for, or warrant the accuracy, completeness, adequacy

and reliability of such information / opinions / views. While due care has been taken to ensure that the disclosures and opinions given are fair and reasonable, none of

the directors, employees, affiliates or representatives of ARSSBL shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary

damages, including lost profits arising in any way whatsoever from the information / opinions / views contained in this Report. The price and value of the investments

referred to in this Report and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide

for future performance. ARSSBL does not provide tax advice to its clients, and all investors are strongly advised to consult with their tax advisers regarding taxation

aspects of any potential investment.

Continued…

Kokuyo Camlin Limited (CAMLN)

15 Anand Rathi Research

Disclaimer:

Contd…

Opinions expressed are our current opinions as of the date appearing on this Research only. We do not undertake to advise you as to any change of our views expressed in this Report. Research Report may differ between ARSSBL’s RAs and/ or ARSSBL’s associate companies on account of differences in research methodology, personal judgment and difference in time horizons for which recommendations are made. User should keep this risk in mind and not hold ARSSBL, its employees and associates responsible for any losses, damages of any type whatsoever.

ARSSBL and its associates or employees may; (a) from time to time, have long or short positions in, and buy or sell the investments in/ security of company (ies) mentioned herein or (b) be engaged in any other transaction involving such investments/ securities of company (ies) discussed herein or act as advisor or lender / borrower to such company (ies) these and other activities of ARSSBL and its associates or employees may not be construed as potential conflict of interest with respect to any recommendation and related information and opinions. Without limiting any of the foregoing, in no event shall ARSSBL and its associates or employees or any third party involved in, or related to computing or compiling the information have any liability for any damages of any kind.

Details of Associates of ARSSBL and Brief History of Disciplinary action by regulatory authorities & its associates are available on our website i. e. www.rathi.com

Disclaimers in respect of jurisdiction: This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject ARSSBL to any registration or licensing requirement within such jurisdiction(s). No action has been or will be taken by ARSSBL in any jurisdiction (other than India), where any action for such purpose(s) is required. Accordingly, this Report shall not be possessed, circulated and/or distributed in any such country or jurisdiction unless such action is in compliance with all applicable laws and regulations of such country or jurisdiction. ARSSBL requires such recipient to inform himself about and to observe any restrictions at his own expense, without any liability to ARSSBL. Any dispute arising out of this Report shall be subject to the exclusive jurisdiction of the Courts in India.

Copyright: - This report is strictly confidential and is being furnished to you solely for your information. All material presented in this report, unless specifically indicated otherwise, is under copyright to ARSSBL. None of the material, its content, or any copy of such material or content, may be altered in any way, transmitted, copied or reproduced (in whole or in part) or redistributed in any form to any other party, without the prior express written permission of ARSSBL. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of ARSSBL or its affiliates, unless specifically mentioned otherwise.

Contd…

Kokuyo Camlin Limited (CAMLN)

16 Anand Rathi Research

Disclaimer:

Contd.

Statements on ownership and material conflicts of interest, compensation - ARSSBL and Associates

Sr. No.

Statement

Answers to the Best of the knowledgeand belief of the ARSSBL/ itsAssociates/ Research Analyst who ispreparing this report

1ARSSBL/its Associates/ Research Analyst/ his Relative have any financial interest in the subject company? Nature of Interest (if applicable), is givenagainst the company’s name?. NO

2

ARSSBL/its Associates/ Research Analyst/ his Relative have actual/beneficial ownership of one per cent or more securities of the subject company, at theend of the month immediately preceding the date of publication of the research report or date of the public appearance?. NO

3ARSSBL/its Associates/ Research Analyst/ his Relative have any other material conflict of interest at the time of publication of the research report or atthe time of public appearance?. NO

4 ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation from the subject company in the past twelve months. NO

5ARSSBL/its Associates/ Research Analyst/ his Relative have managed or co-managed public offering of securities for the subject company in the pasttwelve months.

NO

6ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for investment banking or merchant banking or brokerageservices from the subject company in the past twelve months. NO

7

ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation for products or services other than investment banking ormerchant banking or brokerage services from the subject company in the past twelve months. NO

8ARSSBL/its Associates/ Research Analyst/ his Relative have received any compensation or other benefits from the subject company or third party inconnection with the research report. NO

9 ARSSBL/its Associates/ Research Analyst/ his Relative have served as an officer, director or employee of the subject company. NO

10 ARSSBL/its Associates/ Research Analyst/ his Relative has been engaged in market making activity for the subject company. NO

Kokuyo Camlin Limited (CAMLN)